Abstract

Introduction:

Few studies have examined trends in over-the-counter U.S. Food and Drug Administration–approved nicotine replacement therapy sales data and consumer preferences for nicotine replacement therapy attributes (e.g., flavor). Examination of consumer preferences may inform both public health smoking cessation programs as well as subsequent research on consumer preferences for potentially reduced-risk tobacco products U.S. Food and Drug Administration may authorize.

Methods:

NielsenIQ Retail Measurement Service data were used to examine national trends in over-the-counter nicotine replacement therapy dollar sales from 2017 to 2020 and dollar sales by retail channel and product attributes for the most recent year available at the time of analysis (2020).

Results:

Over-the-counter nicotine replacement therapy sales totaled about $1 billion annually between 2017 and 2020. Across the 4-year period, sales of gum and patches decreased, whereas lozenge sales increased (p<0.05 for all). In 2020, gum accounted for 52.7% ($511 million), lozenges accounted for 33.3% ($322 million), and patches accounted for 14.1% ($137 million) of over-the-counter nicotine replacement therapy sales. Drug stores were the retail channel accounting for the largest percentage of total over-the-counter nicotine replacement therapy sales (42.9%). Three leading brands–private label or store brands (62.8%), Nicorette (30.7%,), and NicoDerm CQ (5.7%)–accounted for 99.2% of the total over-the-counter nicotine replacement therapy market. Mint was the most common flavor, representing 41.2% of total gum and 73.6% of total lozenge sales.

Conclusions:

This analysis of over-the-counter nicotine replacement therapy sales sheds light on consumer preferences for attributes that can inform efforts to facilitate smoking cessation and research on preferences related to potentially reduced-risk tobacco products.

INTRODUCTION

Although adult cigarette smoking prevalence has declined over time, cigarette smoking remains the leading cause of preventable death in the U.S., accounting for an estimated 480,000 deaths annually.1,2 The U.S. Food and Drug Administration (FDA) has approved 7 therapeutic products that are safe and effective for smoking cessation in adults: 5 forms of nicotine replacement therapy (NRT) (nicotine patches, gum, lozenges, nasal sprays, and oral inhalers) and 2 non-nicotine medications (bupropion and varenicline).3,4 (FDA’s Center for Tobacco Products (CTP) has the authority to regulate the manufacturing, marketing, and distribution of tobacco products to protect U.S. population health. FDA’s Center for Drug Evaluation and Research regulates therapeutic tobacco cessation products, including NRT.) The nicotine patch and gum became available over the counter (OTC) in the U.S. in 1996, the nicotine lozenge was introduced as an OTC medication in 2002, and the mini-lozenge was introduced as an OTC medication in 2009.3

All 7 FDA-approved smoking cessation medications are cost-effective and increase quit rates compared with placebo among adults who smoke cigarettes, especially when used with behavioral counseling.3,4 Insurance coverage for cessation treatments that is comprehensive, barrier free, and widely promoted leads to increased use of these treatments and smoking cessation.3,4 Smoking cessation provides significant health benefits, including improving health status, enhancing quality of life, reducing the risk of premature death, and adding as much as a decade to life expectancy.3

The most effective smoking cessation treatment approach is a combination of cessation medications and behavioral counseling.3 In addition, combining short-acting forms of NRT (e.g., nicotine gum) with long-acting forms of NRT (e.g., nicotine patch) increases quit rates compared with using a single form of NRT.3,4 Learning about consumer preferences for cessation medications, such as which factors are most appealing, can help inform efforts to encourage smoking cessation. Examining trends in NRT sales can help regulators and those involved with tobacco cessation efforts understand consumer product preferences for NRT and may inform education efforts, research related to consumer preferences for potentially reduced-risk tobacco products, and public health efforts to encourage tobacco cessation and increase quit attempts. Although product sales are not proxies for individual use behaviors, sales of products can suggest consumer preferences for product attributes.5–8

Many studies of cessation medication use have used self-reported data9–13 or data on cessation medication prescriptions.14–20 Two studies examined cessation medication sales data to assess whether making NRT available OTC increased sales21,22; 2 studies examined the relationship between NRT sales, cigarette sales, and tobacco control policies23,24; 4 studies examined various aspects of demand for NRT using sales data25–28; and 1 study examined changes in NRT sales during the coronavirus disease 2019 (COVID-19) pandemic.29 In addition, the 2020 Surgeon General’s report on smoking cessation included an analysis of sales trends of OTC NRT on the basis of NielsenIQ Retail Measurement Service data from Quarter 2 of 2014 through Quarter 4 of 2018.3

The main purposes of this study are twofold: (1) to assess trends in dollar sales of OTC NRT products by product type (gum, patch, lozenge) during 2017–2020 and (2) to examine dollar sales and market shares of NRT products for the most recent year (2020) by type, retail channel, manufacturer, brand, flavor, and nicotine strength. Information currently available indicates that this is the first study to explore OTC NRT sales by product attribute.

METHODS

Study Sample

This study uses NielsenIQ Retail Measurement Service data, which are cross-sectional scanner data collected through retailers on sales of nicotine and tobacco products (also known as retail scanner data or Scantrack). NielsenIQ’s data collection methods include collection of electronic point-of-sale data from stores through product bar code checkout scanners at registers, coding of retail circulars (e.g., in-store flyers, advertisements promoting products), and in-store data collection (i.e., field auditors who capture in-store display information promoting products). NielsenIQ uses proprietary statistical methods to create estimates of U.S. dollar sales of nicotine and tobacco products by Universal Product Code. Through a contract, CTP receives licensed NielsenIQ data on nicotine and tobacco product sales in weekly increments.

Measures

U.S. national OTC NRT dollar sales were examined for a 4-year period, from Quarter 1 of 2017 through Quarter 4 of 2020 (capturing the most recent complete year of available data at the time of analysis). Quarters were assessed by calendar year, as approximately January—March (Quarter 1), April—June (Quarter 2), July—September (Quarter 3), and October—December (Quarter 4); the exact start and end dates for each quarter vary slightly by year owing to weekly incremented sales.

OTC NRT products were examined by product type; retail channel; and NielsenIQ-reported product attributes, including manufacturer, brand, flavor, and nicotine strength. All product attributes are reported on the basis of external product packaging. Licensed NielsenIQ sales data were initially screened to ensure that products were accurately classified, using variables provided in the data as well as supplementary online research when there was missing or contradictory information in the data. During the screening process, other products described as cessation aids, such as nicotine-containing discs (e.g., Verve) and non-nicotine nontobacco-containing drops (e.g., NicoBloc), were identified and removed from the analysis (these other products represented an insignificant amount of sales [0.02%] over the 4-year period). All products classified by NielsenIQ as gum, lozenges, or patches were included in the analysis.

Product type.

NRT product type was assessed using the following 3 NielsenIQ-provided categories: (1) gum, defined as an oral cessation aid that delivers nicotine to the bloodstream through buccal absorption using a chew and park method; (2) lozenges (including mini-lozenges, as identified by NielsenIQ), defined as oral cessation aids that deliver nicotine to the bloodstream through a dissolvable oral tablet; and (3) patches, defined as cessation aids that deliver nicotine to the bloodstream through a patch placed on the skin.

Retail channel.

Total U.S. national sales were assessed by combining 2 primary NielsenIQ channels: (1) convenience stores, which encompass smaller stores with a limited selection of grocery products, including chain, franchise, and independent convenience stores, and (2) Expanded All Outlets Combined (xAOC), which is a combination of food and drug stores plus select mass merchandizer (e.g., Target), club store (e.g., Sam’s Club), military commissary (e.g., Army & Air Force Exchange Service), and dollar store (e.g., dollar General) accounts. Data for xAOC are available for 4 groups: total xAOC, food stores, drug stores, and food and drug stores combined.

Results are reported from convenience stores, total xAOC, and food stores and drug stores separately to provide a more nuanced view of NRT sales within each channel. Food stores include all chain supermarkets and all independent grocery stores with an annual volume of at least $2 million and with 50% or more of sales coming from edible products. Drug stores include all chain drug stores and all independent drug stores with an annual volume of at least $1 million that sell prescription items and health and beauty products and that have prescription sales not exceeding 85% of total sales. Food and drug store totals are based on NielsenIQ projections independent of xAOC projections; it is not possible to subtract food and drug store totals from xAOC totals to assess the remainder of the xAOC channel.

Manufacturer.

Manufacturer is reported as the manufacturer listed on the product packaging or affiliated with brand ownership (e.g., GlaxoSmithKline).

Brand.

Brand is reported as the brand listed on the product packaging (e.g., Nicorette).

Flavor.

NielsenIQ-provided flavor names were recategorized into the following 4 primary categories on the basis of the flavor name found on the packaging: (1) flavored, mint; (2) flavored, nonmint, which includes fruit, clove/spice/herb, and assorted flavors; (3) undetermined, which includes nonexplicit flavor names and concept flavors (flavor descriptors not identifiable as a consumable, i.e., original flavor); and (4) missing, which includes not applicable or not stated. Because patches do not have reported flavors on the basis of external packaging, they were classified as missing flavors. No NRT product sales had a tobacco or a menthol flavor.

Nicotine strength.

Nicotine strength is reported as listed on the product packaging (2 or 4 milligrams or not stated for gum and lozenges and 7, 14, 21, or 22 milligrams or not stated for patches).

Statistical Analysis

When analyzing trends by product type, dollar sales were adjusted for inflation to 2020 dollars using the Bureau of Labor Statistics Consumer Price Index (CPI) for All Urban Consumers, not seasonally adjusted.30 Dollar sales may be driven by the prices of individual products and by units of products sold, whereas unit sales may be impacted by package sizes and by active ingredient differences. CPI-adjusted dollar sales were used for consistency across OTC NRT product types.

Dollar sales (non-CPI adjusted) and percentage of market share were calculated by retail channel, manufacturer, brand, flavor, and nicotine strength—overall and for each product type—using sales from the most recent complete year, 2020. Market share for each attribute category was calculated as the proportion of total dollar sales accounted for by the category.

Nonparametric statistical testing using quarterly data was conducted to assess trends of NRT sales by product type over the 4-year period as well as the seasonality within each year. The Friedman test was conducted to assess seasonal patterns in quarterly sales.31 If a seasonal pattern was identified, the Seasonal Kendall test was conducted to assess an overall trend across the entire period.32 If no seasonal pattern was identified, the Mann–Kendall trend test was conducted to assess trends in dollar sales.33,34 A joinpoint trend analysis using quarterly data was used to identify data points where a statistically significant change in the trend occurred (e.g., trend changes due to the onset of the COVID-19 pandemic).35 Significance was defined as a p-value<0.05. Data analyses were conducted using Tableau Desktop Professional Edition, Version 10.1, and statistical testing was conducted using R, Version 3.6.1.

RESULTS

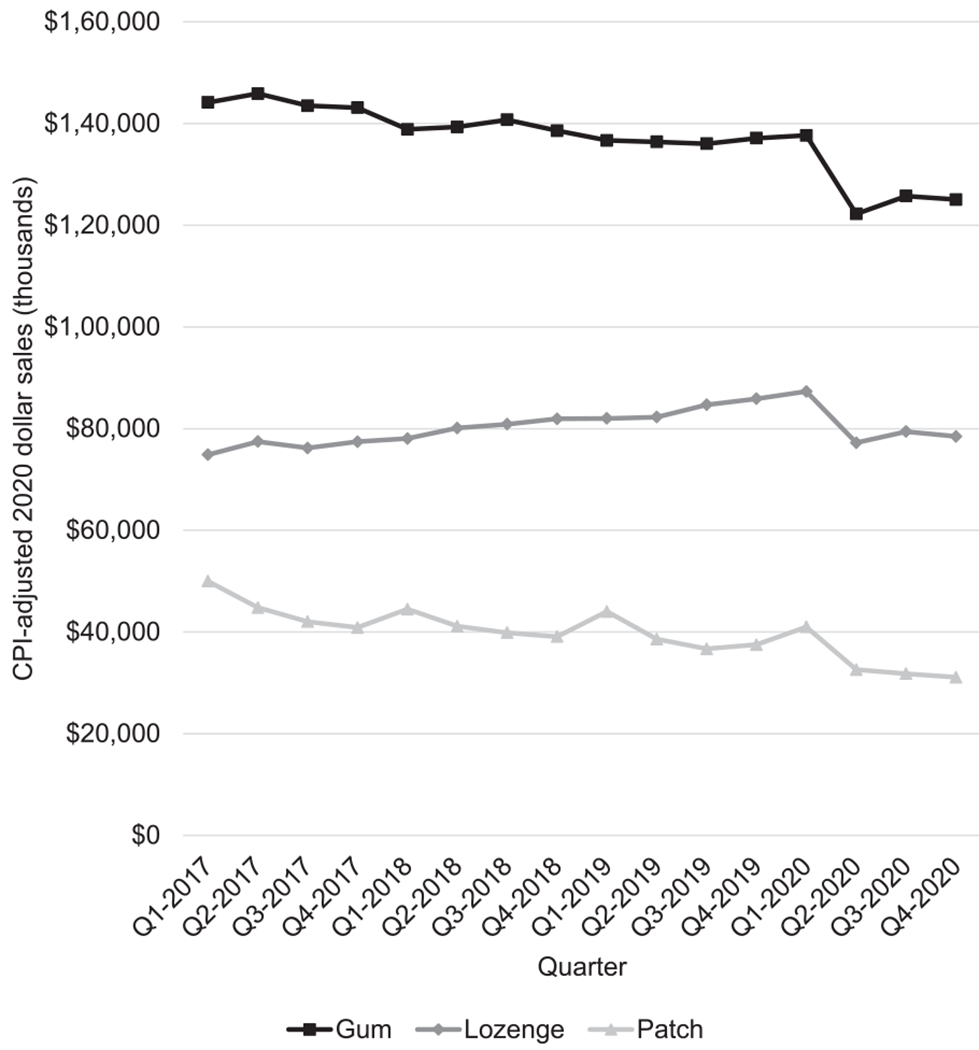

OTC NRT sales totaled about $1 billion annually between 2017 and 2020 (Table 1), with gum accounting for more than half of total dollar sales ($511 million in 2020), followed by lozenges ($322 million) and patches ($137 million). Total quarterly sales of OTC NRT significantly decreased from 2017 to 2020 (p<0.05). Across the 4-year period, dollar sales of gum and patches decreased significantly (p<0.05 for both), whereas dollar sales of lozenges increased (p<0.05) (Figure 1).

Table 1.

Annual CPI-Adjusted (BLS 2020) Dollar Sales (Thousands) of OTC NRT, by Product Type, 2017–2020

| Product type | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|

| Gum | $576,649 | $557,477 | $546,186 | $510,716 |

| Lozenge | $305,948 | $320,920 | $334,797 | $322,412 |

| Patch | $177,685 | $164,538 | $156,754 | $136,501 |

| Total | $1,060,282 | $1,042,935 | $1,037,737 | $969,628 |

BLS, Bureau of Labor Statistics; CPI, Consumer Price Index; NRT, nicotine replacement therapy; OTC, over the counter.

Figure 1.

Quarterly CPI-adjusted (BLS 2020) dollar sales (thousands) of OTC NRT products, by product type, Quarter 2017 – Quarter 4 2020.

BLS, Bureau of Labor Statistics; CPI, Consumer Price Index; NRT, nicotine replacement therapy; OTC, over the counter; Q1, Quarter 1; Q4, Quarter 4.

However, the joinpoint analysis indicates a change in the sales trend for lozenges, with a significant drop in sales starting in Quarter 1 of 2020 (p<0.05). Although visually it appears that sales of gum and patches decreased at a faster rate from Quarter 1 to Quarter 2 of 2020, this change was not significant (p=0.08 and p=0.35, respectively), possibly owing to the small number of quarterly data points after Quarter 2 of 2020. Although not significant, it appears that in Quarter 3 and Quarter 4 of 2020, sales for gum and lozenges increased but did not return to levels seen before Quarter 1 of 2020; sales of patches continued to decline during the period.

Dollar sales of patches show seasonality, with significant increases in Quarter 1 of each year compared with those of the other quarters (p<0.05). In contrast, no seasonal patterns were observed for gum and lozenges (p=0.46 for both).

Sales data for 2020 showed a pattern similar to that of OTC NRT sales by product type over 2017–2020. Gum sales accounted for just over half of the OTC NRT market ($510,716.000; 52.7%), with lozenge sales accounting for one third ($322,412.000; 33.3%) and patch sales accounting for the remainder ($136,501.000; 14.1%) (Table 2).

Table 2.

Dollar Sales (Thousands) of OTC NRT Product Types by Retail Channel and Product Attribute, 2020

| Retail channel and product attributes | Gum | Lozenge | Patch | Total |

|---|---|---|---|---|

| Overall dollar Sales (in thousands) | 510,716 (52.7) | 322,412 (33.3) | 136,501 (14.1) | 969,628 (100.0) |

| Retail channel | ||||

| Total U.S. xAOC | 506,221 (99.1) | 322,235 (99.9) | 136,500 (100.0) | 964,955 (99.5) |

| Drug storesa | 217,612 (42.6) | 138,588 (43.0) | 59,370 (43.5) | 415,570 (42.9) |

| Food storesa | 41,781 (8.2) | 24,640 (7.6) | 10,842 (7.9) | 77,263 (8.0) |

| Total U.S. convenience stores | 4,496 (0.9) | 177 (0.1) | 1 (0.0) | 4,673 (0.5) |

| Manufacturer | ||||

| Private labelb | 276,001 (54.0) | 254,364 (78.9) | 78,578 (57.6) | 608,943 (62.8) |

| GlaxoSmithKline | 230,777 (45.2) | 67,071 (20.8) | 55,060 (40.3) | 352,907 (36.4) |

| All others | 3,939 (0.8) | 976 (0.3) | 2,863 (2.1) | 7,778 (0.8) |

| Brand | ||||

| Private label | 276,001 (54.0) | 254,364 (78.9) | 78,578 (57.6) | 608,943 (62.8) |

| Nicorette | 230,777 (45.2) | 67,071 (20.8) | n/a | 297,848 (30.7) |

| NicoDerm CQ | n/a | n/a | 55,060 (40.3) | 55,060 (5.7) |

| All others | 3,939 (0.8) | 976 (0.3) | 2,863 (2.1) | 7,778 (0.8) |

| Flavor | ||||

| Flavored, mint | 210,638 (41.2) | 237,368 (73.6) | n/a | 448,006 (46.2) |

| Flavored, nonmintc | 192,934 (37.8) | 73,383 (22.8) | n/a | 266,317 (27.5) |

| Missing | 733 (0.1) | 11,661 (3.6) | 136,501 (100.0)d | 148,895 (15.4) |

| Undeterminede | 106,410 (20.8) | <1 (0.0) | n/a | 106,411 (11.0) |

| Nicotine strength | ||||

| 2 milligram | 250,838 (49.1) | 171,518 (53.2) | n/a | 422,356 (43.6) |

| 4 milligram | 259,453 (50.8) | 150,833 (46.8) | n/a | 410,286 (42.3) |

| 21 milligram | n/a | n/a | 85,899 (62.9) | 85,899 (8.9) |

| 14 milligram | n/a | n/a | 35,999 (26.4) | 35,999 (3.7) |

| 7 milligram | n/a | n/a | 14,603 (10.7) | 14,603 (1.5) |

| All others | 426 (0.1) | 60 (0.0) | <1 (0.0) | 486 (0.1) |

Note: All values are n (%). n values expressed in $. January 4, 2020–December 26, 2020. Totals may not add up to 100% owing to rounding. First rows of percentages are row percentages (dollar sales divided by total sales). All other percentages are column percentages (dollar sales divided by total sales of each product type). n/a indicates that the product type was not available in NielsenIQ RMS data. Percentages with <1.0% of the total market share of dollar sales have been combined into the all-others category, with the exception of the retail channel: convenience stores.

Drug and food store totals are based on NielsenIQ projections independent of xAOC projections. It is not possible to subtract drug and food store totals from xAOC totals.

Private label includes products that are manufactured by a company for sale under another company’s brand (typically store brands).

Flavored, nonmint includes fruit, clove/spice/herb, and assorted flavors.

Patches do not have reported flavor.

Undetermined includes nonexplicit flavor names and concept flavors (i.e., flavor descriptors not identifiable as a consumable), that is, original.

n/a, not applicable; NRT, nicotine replacement therapy; OTC, over the counter; RMS, Retail Measurement Service; xAOC, expanded All Outlets Combined.

By retail channel, most OTC NRT sales occurred in xAOCs (99.5%), with only a small portion (0.5%) occurring in convenience stores. Within xAOCs, more sales occurred at drug stores (42.9% of all OTC NRT sold) than at food stores (8.0%).

By manufacturer, nearly all OTC NRT sales were labeled as either private label (62.8%) or GlaxoSmithKline (36.4%). Private label consists of products that are manufactured by a company for sale under another company’s brand (typically store brands). GlaxoSmithKline manufactures 2 brands (NicoDerm CQ and Nicorette). Across sales of OTC NRT products, 3 leading brands—private label (62.8%), Nicorette (30.7%, gum and lozenge only), and NicoDerm CQ (5.7%, patch only)—accounted for 99.2% of the market.

Mint was the most common flavor (46.2% of sales) of OTC NRT gum and lozenges sold, followed by nonmint flavors (27.5%). Approximately 19.5% of OTC NRT gum and lozenges sold ($188,762.000) can be classified as a subcategory of fruit, 8.0% ($77,537,000) can be classified as clove/spice/herb (e.g., cinnamon), and <0.1% each can be classified as assorted flavor and chocolate/sweets. The entire undetermined category, comprising 11.0% ($106,411.000) of OTC NRT sales, was labeled with original flavor.

Nicotine strength varied by product type. For gum and lozenges, products contained 2 milligrams (49.1% and 53.2% of dollar sales, respectively) or 4 milligrams (50.8% and 46.8%, respectively) of nicotine (all other nicotine strengths for gum and lozenges were labeled as not stated). For patches, higher-dose products commanded larger shares of dollar sales, with 21-milligram, 14-milligram, and 7-milligram patches accounting for 62.9%, 26.4%, and 10.7% of dollar sales, respectively. Of note, nicotine is absorbed differently from different NRT products, and nicotine strength (or dosage) is therefore not directly comparable across different types of OTC NRT.36

DISCUSSION

Findings suggest that overall, sales of OTC NRT have decreased from 2017 to 2020. By product type, dollar sales of gum and patches have decreased, whereas dollar sales of lozenges have increased over the 4-year period. The reasons for these trends are likely complex and may involve changes in prices, marketing, tobacco policies, and consumer preferences (which may be constrained by product availability).3 For example, lozenge sales may have increased owing to sales of mini-lozenges because they increased as a share of all lozenges over the study period. This study assessed trends in dollar sales, which may be driven by the prices of individual products as well as by units of products sold.

Starting in Quarter 1 of 2020, the impacts of COVID-19 likely influenced the decrease in sales of OTC NRT across product types. In particular, sales of lozenges peaked in Quarter 1 of 2020 and then started to decline in Quarter 2 of 2020. This observation may suggest that those with quit intentions stockpiled lozenges at the beginning of the pandemic. Monthly sales data also seem to suggest that sales of all the 3 OTC NRT product types increased at the very beginning of the pandemic in the U.S. (March 2020, results not shown), indicative of the possibility of stockpiling. Temporary store closures associated with the early stages of the pandemic may have impacted decreasing sales across all OTC NRT product types starting Quarter 2 of 2020. In comparison, cigarette sales increased during 2020.37 Additional information (e.g., changes in advertising or promotions, the decline in overall tobacco product use from 2019 to 202038) should be considered to fully understand changes in sales of OTC NRT in 2020.

In examining OTC NRT manufacturers and their brands, 3 brands (GlaxoSmithKline Nicorette and NicoDerm CQ and private label) represented nearly all (99.2%) sales. Findings also show the popularity of store brands, given that private label (a category that includes products manufactured by a company for sale under another company’s brand) account for just over 60% of OTC NRT sold. Other studies examining OTC NRT purchasing behavior may provide additional context for preferences between store brands and brand names.

Nearly three quarters of lozenges sold are mint flavored, and fruit (mainly cherry) or clove/spice/herb (mainly cinnamon) flavored lozenges comprise an additional one fifth of sales. Gum shows a bit more variety in flavor preferences. Although mint flavor accounts for the largest portion of gum sales, fruit and cinnamon flavors account for the next largest share, followed by original flavor, which accounts for about one fifth of sales.

Sales of OTC NRT by nicotine strength varied by product type. Gum and lozenge sales were relatively evenly distributed between 2 milligrams and 4 milligrams of nicotine. Patch sales increased with increasing nicotine dosage, with the highest dosage (21 milligrams) accounting for the most sales, followed by the next highest dosage (14 milligrams) and then the lowest dosage (7 milligrams). For all the 3 OTC NRT product types, the FDA-approved recommended dosage typically varies by level of nicotine dependency, with the higher dosages recommended for individuals who smoke cigarettes within 30 minutes after waking or who smoke >10 cigarettes/day.39

Limitations

Product sales do not necessarily reflect the actual use of products or unique individuals purchasing OTC NRT. In addition, NielsenIQ data are in part based on projections or extrapolations, and data should be viewed as estimates and not exact counts. The NielsenIQ data licensed by CTP do not include tobacco/nicotine data from certain outlets, including but not limited to food stores with an annual volume <$2 million (e.g., bodegas), drug stores with an annual volume <$1 million, certain club stores (e.g., Costco), certain dollar stores (e. g., Dollar Tree), internet sales from point-of-sale retailers (e.g., sales from Peapod.com), and specialty tobacco stores. The attributes, including product type, used in this analysis reflect only information printed on the external product package and may not reflect the FDA classification of OTC NRT.

Although this study was unable to determine intentions of NRT use, previously published data indicate that about one third of overall NRT use by adults is for purposes other than complete cessation.40 The sales data used do not include any OTC NRT obtained through state-sponsored cessation program (e.g., quitline) or prescription, including prescriptions for OTC NRT. Individuals typically have to obtain prescriptions for OTC NRT products to have products covered or reimbursed by health insurance.41 Sales of NRT prescriptions and OTC NRT obtained by prescription may differ from OTC NRT sales reported in this study and are covered by other studies, which have shown a decrease in the uptake of prescription smoking cessation medications.17

CONCLUSIONS

This study sheds light on changes in NRT product sales over time. Examining trends in NRT sales by product type and attributes can improve the understanding of consumer purchasing and preferences and provide insight into potential ways to target public health education and efforts to increase the use of evidence-based smoking cessation therapies to encourage and support tobacco cessation. Given that the use of FDA-approved NRT cessation medications is an effective strategy for adult smoking cessation,3,4 continued surveillance of OTC NRT sales can inform public health efforts to decrease the burden of smoking-related diseases and death.

ACKNOWLEDGMENTS

The authors would like to thank Doris Gammon, Jennifer Gaber, and J. Gray Spinks from RTI International for their contributions to the data preparation and Deborah Neveleff from the U.S. Food and Drug Administration (FDA) for her review of the manuscript.

The authors’ own analyses, calculations, and conclusions were informed in part by the NielsenIQ Retail Measurement Service (RMS) data through NielsenIQ’s RMS for the Tobacco Alternatives category for the 4-year annual time periods through the week ending on December 26, 2020 for Total U.S. Expanded All Outlets Combined and convenience stores and are those of the FDA and do not reflect the views of NielsenIQ. NielsenIQ is not responsible for, had no role in, and was not involved in analyzing and preparing the results reported in this paper or in developing, reviewing, or confirming the research approaches used in connection with this report. NielsenIQ RMS data consist of weekly purchase and pricing data generated from participating retail store point-of-sale systems in all U.S. markets. See http://www.NielsenIQ.com/global/en/for more information. The findings and conclusions in this report are those of the authors and do not necessarily represent the official position of the FDA or the Centers for Disease Control and Prevention.

This work was supported by the FDA and the Centers for Disease Control and Prevention.

Footnotes

No financial disclosures were reported by the authors of this paper.

CREDIT AUTHOR STATEMENT

Sarah Trigger: Conceptualization, Methodology, Visualization, Writing – original draft, Writing – review & editing. Xin Xu: Conceptualization, Methodology, Visualization, Writing – review & editing. Ann Malarcher: Writing – review & editing. Esther Salazar: Formal analysis, Visualization, Writing – review & editing. Hyungsik Shin: Formal analysis, Visualization, Writing – review & editing. Stephen Babb: Writing – review & editing.

REFERENCES

- 1.Wang TW, Asman K, Gentzke AS, et al. Tobacco product use among adults – United States, 2017. MMWR Morb Mortal Wkly Rep. 2018;67(44):1225–1232. 10.15585/mmwr.mm6744a2. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.HHS. The health consequences of smoking—50 years of progress: a report of the Surgeon General. Atlanta, GA: HHS, Centers for Disease Control and Prevention, National Center for Chronic Disease Prevention and Health Promotion, Office on Smoking and Health; 2014. https://www.hhs.gov/sites/default/files/consequences-smoking-exec-summary.pdf. Published Accessed May 20, 2020. [Google Scholar]

- 3.HHS. Smoking cessation: a report of the Surgeon General. Atlanta, GA: HHS, Centers for Disease Control and Prevention, National Center for Chronic Disease Prevention and Health Promotion, Office on Smoking and Health; 2020. https://www.hhs.gov/sites/default/files/2020-cessation-sgr-full-report.pdf. Published Accessed May 20, 2020. [Google Scholar]

- 4.Treating tobacco use and dependence: 2008 update. Agency for Healthcare Research and Quality; 2020. https://www.ahrq.gov/prevention/guidelines/tobacco/index.html. Updated February Accessed May 20, 2020.

- 5.He J, Wang X, Vandenbosch MB, Nault BR. Revealed preference in online reviews: purchase verification in the tablet market. Decis Support Syst. 2020;132:113281. 10.1016/j.dss.2020.113281. [DOI] [Google Scholar]

- 6.Leguizamon SJ, Ross JM. Revealed preference for relative status: evidence from the housing market. J Hous Econ. 2012;21(1):55–65. 10.1016/j.jhe.2012.01.001. [DOI] [Google Scholar]

- 7.Arnot C, Boxall PC, Cash SB. Do ethical consumers care about price? A revealed preference analysis of fair trade coffee purchases. Canadian J Agric Econ. 2006;54(4):555–565. 10.1111/j.1744-7976.2006.00066.x. [DOI] [Google Scholar]

- 8.Earnhart D Combining revealed and stated data to examine housing decisions using discrete choice analysis. J Urban Econ. 2002;51 (1):143–169. 10.1006/juec.2001.2241. [DOI] [Google Scholar]

- 9.Babb S, Malarcher A, Schauer G, Asman K, Jamal A. Quitting smoking among adults — United States, 2000–2015. MMWR Morb Mortal Wkly Rep. 2017;65(52):1457–1464. 10.15585/mmwr.mm6552a1. [DOI] [PubMed] [Google Scholar]

- 10.Babb S, Malarcher A, Asman K, et al. Disparities in cessation behaviors between Hispanic and non-Hispanic white adult cigarette smokers in the United States, 2000—2015. Prev Chronic Dis. 2020;17:E10. 10.5888/pcd17.190279. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Zhang L, Babb S, Schauer G, Asman K, Xu X, Malarcher A. Cessation behaviors and treatment use among U.S. smokers by insurance status, 2000—2015. Am J Prev Med. 2019;57(4):478–486. 10.1016/j.amepre.2019.06.010. [DOI] [PubMed] [Google Scholar]

- 12.Sedjo RL, Li Y, Levinson AH. Smoking-cessation treatment: use trends among non-Hispanic white and English-speaking Hispanic/Latino smokers, Colorado 2001—2012. Am J Prev Med. 2016;51(2):232–239. 10.1016/j.amepre.2016.02.015. [DOI] [PubMed] [Google Scholar]

- 13.Kasza KA, Cummings KM, Carpenter MJ, Cornelius ME, Hyland AJ, Fong GT. Use of stop-smoking medications in the United States before and after the introduction of varenicline. Addiction. 2015;110(1):346–355. 10.1111/add.12778. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Jarlenski M, Hyon Baik S, Zhang Y. Trends in use of medications for smoking cessation in Medicare, 2007—2012. Am J Prev Med. 2016;51(3):301–308. 10.1016/j.amepre.2016.02.018. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Kahende J, Malarcher A, England L, et al. Utilization of smoking cessation medication benefits among Medicaid fee-for-service enrollees 1999—2008. PLoS One. 2017;12(2):e0170381. 10.1371/journal.pone.0170381. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Yue X, Guo JJ, Wigle PR. Trends in utilization, spending, and prices of smoking-cessation medications in Medicaid programs: 25 years empirical data analysis, 1991—2015. Am Health Drug Benefits. 2018;11(6):275–285. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6207314/. Accessed January 19, 2023. [PMC free article] [PubMed] [Google Scholar]

- 17.Tibuakuu M, Okunrintemi V, Jirru E, et al. National trends in cessation counseling, prescription medication use, and associated costs among U.S. adult cigarette smokers. JAMA Netw Open. 2019;2(5): e194585. 10.1001/jamanetworkopen.2019.4585. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 18.Ku L, Bruen BK, Steinmetz E, Bysshe T. Medicaid tobacco cessation: big gaps remain in efforts to get smokers to quit. Health Aff (Millwood). 2016;35(1):62–70. 10.1377/hlthaff.2015.0756. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Desai RJ, Good MM, San-Juan-Rodriguez A, et al. Varenicline and nicotine replacement use associated with U.S. Food and Drug Administration safety communications. JAMA Netw Open. 2019;2(9):e1910626. 10.1001/jamanetworkopen.2019.10626. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Scharf D, Fabian T, Fichter-DeSando C, Douaihy A. Nicotine replacement prescribing trends in a large psychiatric hospital, before and after implementation of a hospital-wide smoking ban. Nicotine Tob Res. 2011;13(6):466–473. 10.1093/ntr/ntr026. [DOI] [PubMed] [Google Scholar]

- 21.Burton SL, Gitchell JG, Shiffman S, Centers for Disease Control and Prevention (CDC). Use of FDA-approved pharmacologic treatments for tobacco dependence—United States, 1984—1998. MMWR Morb Mortal Wkly Rep. 2000;49(29):665–668. 10.1136/tc.2005.012989. [DOI] [PubMed] [Google Scholar]

- 22.Shiffman S, Hughes JR, Pillitteri JL, Burton SL. Persistent use of nicotine replacement therapy: an analysis of actual purchase patterns in a population based sample. Tob Control. 2003;12(3):310–316. 10.1136/tc.12.3.310. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Hu T, Sung HY, Keeler TE, Marciniak M. Cigarette consumption and sales of nicotine replacement products. Tob Control. 2000;9(suppl 2): II60–II63. 10.1136/tc.9.suppl_2.ii60. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24.Metzger KB, Mostashari F, Kerker BD. Use of pharmacy data to evaluate smoking regulations’ impact on sales of nicotine replacement therapies in New York City. Am J Public Health. 2005;95(6):1050–1055. 10.2105/AJPH.2004.048025. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25.Huang J, Wang Y, Duan Z, Kim Y, Emery SL, Chaloupka FJ. Do e-cigarette sales reduce the demand for nicotine replacement therapy (NRT) products in the U.S.? Evidence from the retail sales data. Prev Med. 2021;145:106376. 10.1016/j.ypmed.2020.106376. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26.Huang J, Gwarnicki C, Xu X, Caraballo RS, Wada R, Chaloupka FJ. A comprehensive examination of own-and cross-price elasticities of tobacco and nicotine replacement products in the U.S. Prev Med. 2018;117:107–114. 10.1016/j.ypmed.2018.04.024. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 27.Tauras JA, Chaloupka FJ, Emery S. The impact of advertising on nicotine replacement therapy demand. Soc Sci Med. 2005;60(10):2351–2358. 10.1016/j.socscimed.2004.10.007. [DOI] [PubMed] [Google Scholar]

- 28.Tauras JA, Chaloupka FJ. The demand for nicotine replacement therapies. Nicotine Tob Res. 2003;5(2):237–243. 10.1080/1462220031000073306. [DOI] [PubMed] [Google Scholar]

- 29.Bandi P, Asare S, Majmundar A, et al. Changes in smoking cessation-related behaviors among U.S. adults during the COVID-19 pandemic. JAMA Netw Open. 2022;5(8):e2225149. 10.1001/jamanetworkopen.2022.25149. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30.Consumer price index. U.S. Bureau of Labor Statistics. https://www.bls.gov/cpi/data.htm. Updated May 26, 2021. Accessed May 26, 2021.

- 31.Davey AM, Flores BE. Identification of seasonality in time series: a note. Math Comput Modell. 1993;18(6):73–81. 10.1016/0895-7177(93)90126-J. [DOI] [Google Scholar]

- 32.Hirsch RM, Slack JR. A nonparametric trend test for seasonal data with serial dependence. Water Resour Res. 1984;20(6):727–732. 10.1029/WR020i006p00727. [DOI] [Google Scholar]

- 33.Hipel KW, McLeod AI. Time Series Modelling of Water Resources and Environmental Systems. New York, NY: Elsevier Science; 1994. https://www.elsevier.com/books/time-series-modelling-of-water-resources-and-environmental-systems/hipel/978-0-444-89270-6. Accessed January 19, 2023. [Google Scholar]

- 34.Libiseller C, Grimvall A. Performance of partial Mann-Kendall tests for trend detection in the presence of covariates. Environmetrics. 2002;13(1):71–84. 10.1002/env.507. [DOI] [Google Scholar]

- 35.Kim HJ, Fay MP, Feuer EJ, Midthune DN. Permutation tests for joinpoint regression with applications to cancer rates [published correction appears in Stat Med. 200128;20(4):655]. Stat Med. 2000;19 (3):335–351. . [DOI] [PubMed] [Google Scholar]

- 36.Wadgave U, Nagesh L. Nicotine replacement therapy: an overview. Int J Health Sci (Qassim). 2016;10(3):425–435. 10.12816/0048737. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 37.Federal Trade Commission. Cigarette report for 2020. Washington, DC: Federal Trade Commission; 2021. https://www.ftc.gov/system/files/documents/reports/federal-trade-commission-cigarette-report-2020-smokeless-tobacco-report-2020/p114508fy20cigarettereport.pdf. Accessed April 18, 2021. [Google Scholar]

- 38.Cornelius ME, Loretan CG, Wang TW, Jamal A, Homa DM. Tobacco product use among adults – United States, 2020. MMWR Morb Mortal Wkly Rep. 2022;71(11):397–405. 10.15585/mmwr.mm7111a1. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 39.Centers for Disease Control and Prevention. Identifying and treating patients who use tobacco: action steps for clinicians. Atlanta, GA: Centers for Disease Control and Prevention, US Dept of Health and Human Services; 2016. https://millionhearts.hhs.gov/files/Tobacco-Cessation-Action-Guide.pdf. Accessed January 19, 2023. [Google Scholar]

- 40.Hammond D, Reid JL, Driezen P, et al. Smokers’ use of nicotine replacement therapy for reasons other than stopping smoking: findings from the ITC four country survey [published correction appears in Addiction. 2008;103(12):2075]. Addiction. 2008;103(10):1696–1703. 10.1111/j.1360-0443.2008.02320.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 41.Centers for Medicare and Medicaid Services. FAQs about Affordable Care Act implementation (part XIX). Baltimore, MD: Centers for Medicare and Medicaid Services; 2014. https://www.cms.gov/CCIIO/Resources/Fact-Sheets-and-FAQs/aca_implementation_faqs19. Published May 2 Accessed May 20, 2020. [Google Scholar]