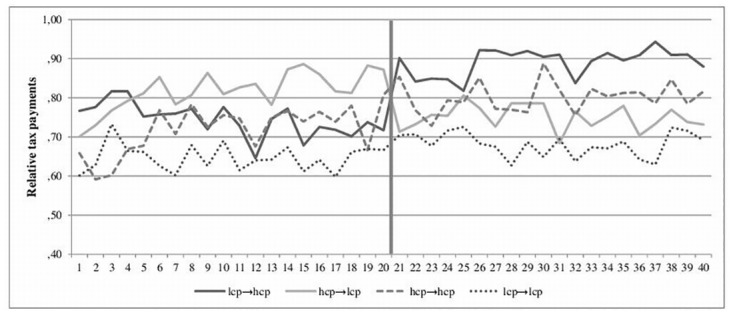

Fig 1. Experiment 2.

The impact of low and high coercive power on relative tax payments before and after the change in tax authority. Note. lcp … low coercive power, hcp … high coercive power.

Official websites use .gov

A

.gov website belongs to an official

government organization in the United States.

Secure .gov websites use HTTPS

A lock (

) or https:// means you've safely

connected to the .gov website. Share sensitive

information only on official, secure websites.

The impact of low and high coercive power on relative tax payments before and after the change in tax authority. Note. lcp … low coercive power, hcp … high coercive power.