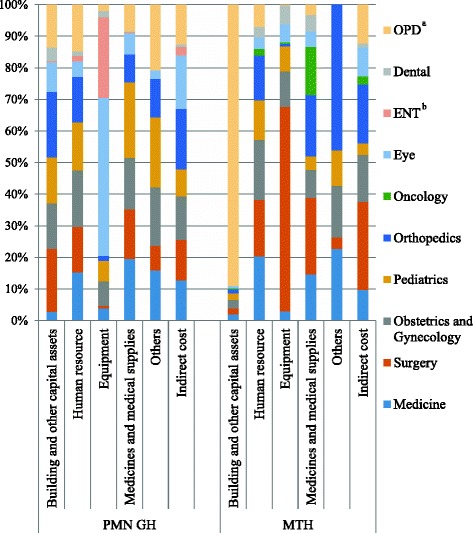

Fig. 2.

Contribution of the cost components by each cost center at Pyinmanar General Hospital (PMN GH) and Magway Teaching Hospital (MTH) in 2015–2016. The following five components constituted: 1) buildings and other capital assets, 2) human resource, 3) equipment, 4) medicines and medical supplies, and 5) others. The contributions of each cost component by the intermediate and the final cost centers were presented in this study. At PMN GH, the eye unit was the main contributor to equipment cost, while it was the surgery unit at MTH. In patient units and the operation theatre almost equally contributed to human resource. At MTH, OPD accounted for higher building cost