Abstract

We use administrative data from Wisconsin to determine the fraction of new Medicaid enrollees who have private health insurance at the time of enrollment in the program. Through the linkage of several administrative data sources not previously used for research, we are able to observe coverage status directly for a large fraction of enrollees and indirectly for the remainder. We provide strict bounds for the percentages in each status and find that the percentage of new enrollees with private insurance coverage at the time of enrollment lies between 16 percent and 29 percent, and the percentage that dropped private coverage in favor of public insurance lies between 4 percent and 18 percent. Our point estimates indicate that, among all new enrollees, 21 percent had private health insurance at the time of enrollment and that 10 percent dropped this coverage. Our results show substantially lower rates than previous studies of crowd-out following public health insurance expansions and significant rates of dual coverage, whereby new enrollees into public insurance retain their previously held private insurance coverage.

Keywords: crowd-out, Medicaid, SCHIP

Introduction

In this study, we determine the fraction of new Medicaid enrollees who have private health insurance at the time of enrollment in the program and, of those, the fraction that dropped their private coverage. This study is, to our knowledge, the first to use administrative data to estimate the movement between private and public insurance programs. Our findings also update the understanding of these movements in the context of a private insurance environment that differs substantially from that of a decade ago—in particular, one that today requires higher participant cost-sharing in the form of premiums, deductibles, and co-payments (Kaiser Family Foundation [KFF] 2011). In addition, we identify a subpopulation of new enrollees into public insurance programs that simultaneously held private coverage for at least six months following enrollment, a phenomenon that has received relatively little attention in the literature.

An understanding of the movement between private and public insurance programs is particularly important in today’s policy environment. The implementation of the Affordable Care Act (ACA), including Medicaid expansions and premium and cost-sharing subsidies for private, exchange-based health insurance, has heighted concerns about declines in employer-sponsored coverage. As of January 2013, Wisconsin was among eight states with income eligibility thresholds for parents with dependent children already in place that exceed the ACA’s 133 percent of the federal poverty level (FPL) threshold for Medicaid eligibility. An additional fifteen states had established other programs for non-disabled childless adults (KFF 2013). As a result, concern about crowd-out goes beyond the migration from employer-sponsored insurance to Medicaid, as these states must decide whether to retain expanded coverage for adults or to reduce eligibility to the 133 percent of FPL threshold, and thereby allow a greater fraction of adults to become eligible for federal subsidies of exchange-based private coverage (State Health Reform Assistance Network 2013).

Understanding the extent to which new enrollees overlap private coverage with public coverage allows for a more nuanced assessment of the prior reported crowd-out rates and may generate policy considerations about the degree to which such dual coverage is desirable.

The linking of various state administrative data sources allow us to accurately capture movements between private and public coverage for individuals who enroll in public coverage, to determine the extent the enrollees into public coverage have and maintain private coverage, and to observe job transitions that may be associated with losses of coverage, none of which have been previously possible. While our contribution is primarily empirical in nature, we also develop a simple conceptual model for understanding various approaches. This conceptual model enables us to place our estimates within the literature and allows for comparison with prior estimates of crowd-out.

The administrative data we use come from Wisconsin’s BadgerCare Plus (BC+) program, which covers children of all income levels and parent or caretaker adults up to 200 percent of FPL. The data allow us to observe the universe of enrollees in the state’s public insurance program as well as their family members. The size of our administrative data set also allows us to examine subgroups, including groups defined by income and geographic location.

Our strict upper bound for the percentage of new public insurance enrollees with private health insurance at the time of enrollment is 29 percent, with a strict lower bound of 16 percent. Not all of these enrollees dropped their private coverage. Our strict upper and lower bounds on the percentage that dropped private coverage in favor of public insurance are 18 percent and 4 percent, respectively. We also provide point estimates of these percentages, and we estimate that among all new enrollees, 21 percent had private health insurance at the time of enrollment and that 10 percent of all new enrollees dropped this coverage. While these results are for the time period after the expansion of Wisconsin’s program (April 2008–May 2009), we find similar results for the pre-expansion period (January 2006–January 2008) and for the expansion rollout (February 2008–March 2008). Higher income groups had higher rates of private insurance coverage at the time of enrollment, as did residents of urban counties.

Background

Interest in the potential displacement of private insurance coverage by public health programs increased with the expansions of state Medicaid programs in the late 1980s and early 1990s. A robust literature emerged seeking to quantify the magnitude of any such “crowd-out” effect. A comprehensive overview of the crowd-out literature lies beyond the scope of our work (for excellent reviews, see Gruber 2003; Davidson, Blewett, and Call 2004; Blewett and Call 2007; Gruber and Simon 2008); instead, we focus on situating the unique contribution of our paper within this broader literature.

The approach we take is to use high-quality administrative data to directly measure the prior and concurrent private insurance coverage of new Medicaid enrollees. As will be developed below in the conceptual model, the resulting measure is less expansive than the operationalization of crowd-out in the majority of the related literature, as it does not capture any potential effects that the availability of public coverage may have on transitions between uninsured and privately insured states. The resulting implication is that our parameter of interest should in theory be lower than the range of crowd-out rates found in the existing literature. While this range is vast and remains the subject of vigorous debate, two important benchmarks are frequently cited: (1) the (approximate) 50 percent estimate from the seminal Cutler and Gruber (1996) paper covering the Medicaid expansions of the late 1980s and early 1990s, and (2) the 25–50 percent range arrived at in an influential review of the Children’s Health Insurance Program (CHIP) era expansions by the Congressional Budget Office (CBO; 2007).

Thorpe and Florence (1999) authored the one existing study that estimates a parameter similar to ours; using children participating in the 1989–1994 rounds of the National Longitudinal Survey of Youth, they found that across the study years, between 36 and 54 percent of new Medicaid enrollees had private coverage at some point in the past year. After subtracting out children whose coverage change likely resulted from parental job loss, they estimated that approximately 16 percent of children had access to private insurance at the time of Medicaid enrollment. Our work extends this analysis in several important ways. First, we are able to include adults in our estimates of private–public insurance transitions. Moreover, as discussed above, our results are more reflective of the current employer-sponsored insurance environment, which is characterized by higher member cost-sharing relative to the study periods of Thorpe and Florence and its contemporary articles.

Finally, and arguably most importantly, we estimate concurrent private insurance coverage held by new Medicaid enrollees during their early tenure on the program. Understanding the extent to which new Medicaid enrollees “overlap” public coverage with private coverage is a key contribution to the larger crowd-out literature, as the treatment of the overlap population is an important driver of differences in estimates across previous studies. There is concern that the overlap arises from a measurement issue: either a reporting error on the part of survey recipients or an issue of timing (those who moved from one source of coverage to the other report having both). Moreover, concurrent with the implementation of eligibility expansions, Medicaid and CHIP agencies increased their use of private administrators for public-managed care programs, which likely resulted in beneficiary confusion regarding type of coverage held (see LoSasso and Buchmueller 2004 for a careful discussion of the resulting measurement error implications). Critically, it is impossible to parse true coverage overlap from measurement error in household survey data, a key limitation of the existing literature. Directly measuring coverage with administrative data greatly (if not entirely) reduces the possibility that coverage overlap reflects measurement error as opposed to a genuine phenomenon.

Policy Context: BadgerCare Plus

Wisconsin’s BC+ program was launched in February of 2008 and expanded upon Wisconsin’s existing CHIP and Medicaid program. With the expansion, BC+ covered parents and caretaker adults with family incomes up to 200 percent FPL. Adults with family incomes greater than 150 percent FPL were charged sliding-scale premiums (premiums start at $10 and are capped at 5 percent of family income).

Children of all incomes were eligible for BC+, though for both adults and children with incomes above 150 percent FPL, eligibility depended on not having access to affordable and qualified private insurance. Families of enrolled children with incomes greater than 200 percent FPL were also charged sliding-scale premiums, provided a more limited set of covered services, andcharged co-payments on non-preventive services. The families of children with incomes greater than 300 percent FPL were required to pay the full cost of coverage, which amounted to approximately $100 per month in 2008.

Under BC+, applicants with incomes over 150 percent FPL were subject to anti-crowd-out provisions. With good-cause exceptions, these individuals faced a three-month waiting period for dropped coverage and cannot have been offered employer-sponsored insurance during the previous twelve months.

Method

The methodological approach we take in this article is to use a set of high-quality linked administrative data sets with information on a large number of individuals and their families to measure the percentage of new enrollees that were previously uninsured. For a large proportion, we can measure this percentage directly; for the remainder, we can both bound and estimate it. In the following sections, we first describe these data and how they were linked in detail. We then describe the conceptual approach we use to measure crowd-out, create bounds and estimates, and compare with the literature.

Data and Sample Construction

For the analysis, we construct a longitudinal administrative data set from four administrative databases:

CARES: Wisconsin’s administra-tive enrollment and program eligibility database,

TPL: Wisconsin’s Third Party Liability database,

UI: Unemployment Insurance program quarterly wage records, and

DOL: U.S. Department of Labor (DOL) database of all self-insured firms.

Table 1 provides an overview of these data sets, including the level and frequency of observation, how they are linked, and the purpose of their usage.

Table 1.

Summary of Data Sets and Linkages.

| Data set | Level of observation | Frequency of observation | Method of linkage | Purpose of use |

|---|---|---|---|---|

| CARES (BC+ Enrollment and Eligibility) | Person | Month | SSN | Identify new Medicaid enrollees and their household members. |

| Third Party Liability | Person | Month | SSN | Observe whether enrollees have non-group coverage or if employed at fully insured firms have insurance during months enrolled. |

| Unemployment Insurance | Person-Firm | Quarter | SSN/FEIN | Observe employer of enrollees and their household members. Identify job transitions. |

| Department of Labor | Firm | Annual | FEIN | Observe whether firm has a self-insured plan. |

| Current Population Survey | Person | Annual | Regression Model | Predict probability of coverage for workers at self-insured firms. |

Note. Further details available in text. BC+ = BadgerCare Plus; SSN = Social Security Number; FEIN = Federal Employer Identification Number.

The main data source is an administrative enrollment database, CARES, from the state of Wisconsin’s Medicaid and CHIP programs, which was provided to us by agreement with the Wisconsin Department of Health Services. The unit of observation in this data set is an individual-month beginning in the first month that individual enrolled in BC+ between January 2006 and May 2009.1 For some of the analysis, we use data from other case members; a case includes all individuals associated with eligibility determination (generally, everyone in the applicant’s household). Over this time period, we have monthly enrollment data for a total of 1,392,185 enrollees in 433,525 unique cases. CARES also contains demographic and income information, including age, sex, ethnicity, citizenship, educational attainment, and sources as well as amount of household income. From the income data, we are able to observe whether the main source of income for a case is self-employment income.

The second data source is the TPL database. TPL is an individual-level database that identifies all enrollees in state health insurance programs who are covered by a private health insurance plan. This database, while an excellent resource for our study, is limited in two ways. First, the database does not contain individuals who are covered by health insurance provided by a self-funded employer (whose policies are not subject to state regulation and therefore cannot be compelled to provide information to the TPL database). Second, these data are available for each month in which an individual is enrolled in BC+ but do not contain information on the health insurance coverage of individuals in months prior to enrollment or following disenrollment. The database does identify individuals covered by fully insured employers as well as those with plans purchased in the non-group market. Those enrollees who do not have insurance according to the TPL database either do not have any source of private insurance or have health insurance through a self-funded employer. We match BC+ enrollees to the TPL database using Social Security Numbers (SSNs).

The third data source, UI, is the state’s records of employers’ quarterly wage reports, which are required by the Unemployment Insurance program. The wage reports include the employee’s SSN and quarterly wages and the employer’s Federal Employer Identification Number (FEIN) and industry classification code from 2005 to 2009. Only employers not subject to unemployment insurance laws are exempt from reporting.2 Our primary purpose in matching our enrollees to UI is to obtain the FEIN of their employers and of the employers of their family members, which we then use to identify those with self-insured employers. Because employers who are exempt from UI reporting (such as independent contractors) are unlikely to provide a self-funded health insurance plan, we are not concerned about their absence from the UI database. We match all BC+ enrollees and their case members to the UI data by SSN. Because the enrollment data are monthly, we assign a person to a firm for each month in the quarter in which we observe them in UI. Those who are observed at multiple firms are assigned the FEIN of the employer from which they had the highest earnings.

We also use the longitudinal nature of the UI data to identify cases with a worker who had a job loss around the time of enrollment, as the UI data are available for all workers in CARES both prior to and post-enrollment. We define a job loss at the time of enrollment as going from having a UI job match from any firm in the quarter of enrollment in BC+ to having no job match from any firm in the following quarter.

The final administrative data source we use is from the DOL, obtained through a Freedom of Information Act request, to determine whether a BC+ enrollee’s or case member’s employer offers a self-funded plan. The DOL data represent the universe of employers within the United States from 2003 to 2007 that self-insured for health, life, and disability and related insurance plans. These data are used to administer the Employee Retirement Income Security Act (ERISA) and are part of the reporting requirements of self-insured firms to the Internal Revenue Service. The DOL data are matched by FEIN to all enrollees that were successfully matched to UI.3

Means of enrollee characteristics are reported in Table 2. Notably, the youngest child in the family is under six for about 60 percent of our sample. The vast majority of the sample consists of cases under 150 percent FPL; this is because much of the new enrollment in this expansion occurred in populations that were income-eligible even prior to reform (Herd et al. 2013; Leininger et al. 2011). Very few households earn the majority of their income from self-employment (the definition we use for self-employed).4

Table 2.

Summary Statistics for Administrative Data.

| January 06–January 08 | February 08–March 08 | April 08–May 09 | |

|---|---|---|---|

| Male | 41.4% | 43.0% | 43.4% |

| Dane County | 5.8% | 5.1% | 5.6% |

| Milwaukee County | 29.0% | 24.4% | 26.2% |

| Youngest child <6 | 63.3% | 60.8% | 61.5% |

| Youngest child 6–12 | 23.0% | 27.7% | 24.3% |

| Youngest child 13–17 | 13.7% | 11.5% | 14.2% |

| Adult <34 | 85.6% | 80.6% | 82.5% |

| Adult 34–54 | 13.8% | 18.1% | 16.5% |

| Adult 54–64 | 0.6% | 1.2% | 1.0% |

| Less than high school | 71.2% | 66.3% | 74.1% |

| High school graduate | 23.2% | 26.8% | 20.9% |

| Some college | 5.6% | 6.9% | 5.0% |

| FPL ≤ 150% | 93.1% | 69.7% | 81.2% |

| FPL 151%–200% | 6.7% | 20.0% | 13.8% |

| FPL 201%–300% | 0.2% | 8.6% | 4.1% |

| FPL > 300% | 0.0% | 1.8% | 0.9% |

| Self-employed | 0.3% | 0.1% | 0.0% |

| Someone employed at UI firm | 72.2% | 80.7% | 72.1% |

| Of which: | |||

| Goods industry | 6.4% | 10.2% | 8.6% |

| Service industry | 93.6% | 89.8% | 91.4% |

| Non-self-insured firm | 71.4% | 68.8% | 70.8% |

| Self-insured firm | 28.6% | 31.2% | 29.2% |

| Number of observations | 472,772 | 91,975 | 326,327 |

Source. Authors’ tabulations from WI CARES System, UI System, and Department of Labor

Note. Observations consist of only new enrollees; all of the enrollees in January 2006 are left-censored, so we cannot observe the start-date of their spells. We exclude these observations from our analysis. The reference adult is the highest earner in the household, or in cases with no earnings, the oldest adult. UI = Unemployment Insurance.

We augment our administrative data with the Current Population Survey Annual Social and Economic Supplement (CPS-ASEC) when we impute employer-sponsored insurance (ESI) coverage (described below). The 2007–2009 CPS-ASEC data have 11,418 Wisconsin respondents in total. Our analytical sample consists of employed men and women who are eighteen to sixty-four years old. We further limit our sample to those living with at least one child under the age of eighteen in the family to mimic the Medicaid eligibility criteria in Wisconsin, yielding an analytical sample of 2,685 men and women.5 The health insurance question in the CPS-ASEC asks about coverage sources in the previous year. Table A1 of the appendix contains descriptive statistics of the sample population from the CPS-ASEC.

Conceptual Framework

In this article, we aim to directly measure the percentages of new public insurance enrollees that were previously uninsured and privately insured. This is a somewhat different measure of crowd-out than that in previous studies. To facilitate comparison of our method with previous studies of crowd-out and to clarify our approach, we develop a conceptual framework in the following discussion.

Crowd-out in response to an expansion in the income eligibility threshold from I0 to I1 that occurs in year t is defined as the net change in private insurance coverage between t and t + 1 as a proportion of the net change in public insurance coverage between t and t + 1 among the population with incomes between I0 and I1. Because private coverage may change for reasons unrelated to the public insurance expansion, the change in private coverage that would have occurred in the counterfactual world of no public insurance expansion (in practice operationalized as the experience of comparison populations—which, depending on the study, include across and/or within state individuals who experienced no change in public insurance eligibility) must be subtracted from this amount. Thus, the crowd-out rate resulting from an incremental expansion is given by

where T represents the actual expansion population (treatment) and C represents the counterfactual expansion population (control). By assumption, the counterfactual net change in public insurance among the expansion population is zero. If we take the additional step of decomposing the change in private insurance into the gross flows between insurance states,

then the numerator of equation (1) can be rewritten as

We can measure the first term on the right-hand side of equation (3)—the number who transition from private insurance to public insurance—directly in our administrative data.

The second term on the right-hand side of equation (3)—the difference between the number who transition from private insurance to uninsured in the expansion and counterfactual states—is of ambiguous sign. Some people who would have moved from private to uninsured will now be able to move from private to public, which would tend to make this term negative. However, the expansion may lead some employers to drop coverage for eligible employees, who then may choose not to enroll in public insurance, which would tend to make this term positive. We believe that this latter effect is likely smaller than the former effect. This term cannot be measured using administrative data on enrollment as it does not involve enrollees in public insurance programs.

The final term on the right-hand side of equation (3)—the difference between the number who transition from uninsured to private insurance in the expansion and counterfactual states—is if anything negative but probably small (Cutler and Gruber 1996; Shore-Sheppard, Buchmueller, and Jensen 2000; Marquis and Long 2003). Some employers might have added health insurance coverage (reducing the number of uninsured) but choose not to do so once public health insurance is expanded.

Thus, the direct measure of the number of people who transition from private to public insurance in response to the public insurance (which is what we measure in this article) is closely related to what would appear in the numerator of an incremental crowd-out rate. It is exactly equal to the numerator of the incremental crowd-out rate if the rates of transition between private insurance coverage and being uninsured are unaffected by the public insurance expansion.

The denominator of the crowd-out rate is the net increase in public insurance coverage. This, too, can be decomposed into flows into and out of public insurance:

We can use administrative data to measure the gross flows into public insurance coverage from being uninsured and from having private insurance coverage (the first two terms). Thus, the difference between the sum of the two quantities that we measure and the denominator of the crowd-out rate is the difference between gross enrollment and net enrollment into public insurance.

Empirical Analysis

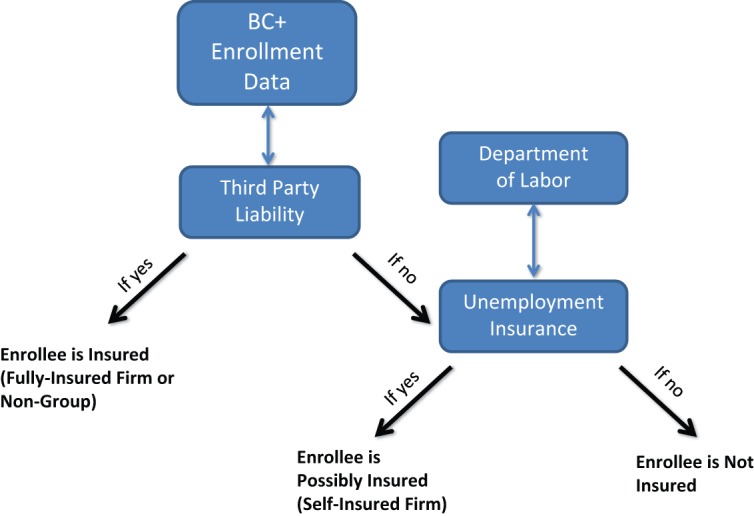

The main focus of our analysis is to find the percentage of new enrollees in public insurance that had private insurance coverage at the time of enrollment. This quantity is closely related to previously used measures of crowd-out, as discussed in the previous section. Here, we discuss our methods for obtaining strict bounds for and point estimates of this percentage. Figure 1 serves as a guide to the analysis.

Figure 1.

Process for determination of insurance status.

Note. BC+ = BadgerCare Plus.

The first step is to identify those new BC+ enrollees that had either private non-group insurance or ESI from a fully insured firm at the time of enrollment. We do this by determining whether an enrollee was covered by an insurance plan in TPL in the enrollment month. Any enrollee without a TPL match does not have non-group insurance or insurance from a fully insured firm in that month.

The second step is to identify new BC+ enrollees with ESI from a self-insured firm. We do this by, first, finding enrollees who themselves are or have a case member who is employed at a firm with a self-funded plan by using the UI-DOL match. We assume that it is not possible to have ESI from a self-insured firm without at least one family member being employed at a self-insured firm. Unlike the TPL match, however, this match on its own does not tell us whether a particular enrollee was actually covered by ESI from a self-insured firm as not all workers at a self-insured firm will be eligible for coverage. Some employees at firms that offer health insurance are themselves not eligible for health insurance either because they work part-time, are in occupations that are not covered, or have not been at the firm for a sufficient period of time. For example, Farber and Levy (2000) report that in 1997, only 91 percent of workers in firms that offered health insurance were eligible for coverage. The majority of the ineligible were part-time workers.

We use two alternative methods to address this missing information: (1) a strict bounds approach (Manski 1995) that uses only the administrative data and (2) a point estimate that imputes this information using survey data.

The strict bounds approach makes conservative assumptions on the probability of an enrollee having ESI insurance coverage conditional on a case member being employed at a self-insured firm. In it, we obtain strict upper bounds by assuming that 100 percent of enrollees who are or who have a family member employed at a self-insured firm have ESI coverage. We obtain strict lower bounds by assuming that none of these enrollees have ESI coverage. This method provides strict bounds because it encompasses the minimum and the maximum possible take-up of coverage by workers at self-insured firms.

We calculate the point estimate of the percentage of BC+ enrollees with a case member employed by a self-insured firm that were covered by that plan by first identifying those with the potential for this type of coverage using the UI-DOL data as described above. Second, we estimate the probability of their enrollment in ESI using the results of a model estimated from survey data. In particular, we estimate a probit model where the dependent variable is an indicator for ESI coverage of the highest earning worker and the independent variables are various individual and family characteristics. We are restricted in using only those variables that appear both in the survey data and in our administrative data. The means of these variables in the CPS are listed in Table A1 of the appendix. We use the 2007–2009 CPS-ASEC to estimate the probit model and calculate the predicted probabilities that the relevant case members will have ESI. We use three years of the CPS-ASEC following Census Bureau guidelines for obtaining reliable state-level estimates. We use the estimated coefficients from the probit model to predict the probability of ESI coverage for each new enrollee with a case member who is employed at a self-insured firm. We use the average predicted probability as the conditional probability for the relevant subgroup. We multiply this estimate of the conditional probability by the number of enrollees to obtain the point estimate. Further details of the model and results are reported in the appendix.

We assume any enrollee with neither a TPL match nor a case member with a DOL match is uninsured at the time of enrollment. In addition, we assume any enrollee with a job loss is uninsured at the time of enrollment regardless of TPL or DOL status.6

If all those with private health insurance at the time of enrollment in public programs dropped that coverage immediately, the analysis would end here. However, it is possible that some BC+ enrollees who have private insurance at the time of enrollment maintain their private coverage. This possibility has been underexplored in the literature to date. Therefore, the third step in our analysis is to determine the percentage of enrollees that do drop their private coverage. Individuals who do not drop their private insurance coverage in favor of public coverage have not substituted public coverage for private coverage, and thus we do not include them in our estimates of crowd-out. In such cases of dual coverage, BC+ is the secondary payer.

To determine the percentage of enrollees that had private coverage at the time of enrollment but subsequently dropped that coverage, we once again use the TPL database that identifies all BC+ enrollees with either private non-group coverage or ESI coverage from a fully insured firm. We look six months post-enrollment. We count those individuals who had coverage at the time of enrollment (month 1) but did not have it in any of the following six months (months 2–7) and were still enrolled in BC+ as having dropped their private coverage. In the case of BC+ enrollment spells shorter than 7 months, those that keep their private coverage for the entire enrollment spell are considered to not have dropped private coverage and those who drop private coverage prior to disenrollment are counted as having dropped private coverage.

We cannot directly observe the dropping of insurance coverage among those with coverage from a self-insured firm. When computing our strict lower and upper bounds, we alternatively assume that all of these enrollees or that none of these enrollees drop this coverage, as in our description of the upper and lower bounds above.

Results

This section, first, presents our estimates, based on administrative data, of the percentage of new Medicaid enrollees who have private health insurance at the time of enrollment in the program and, second, reports the fraction that dropped their private coverage. We organize results into three time periods—a period prior to the launch of BC+ (January 2006–January 2008), an initial expansion period (February and March 2008), and a post-expansion period (April 2008–November 2009). We separately consider the initial expansion period because of an auto-enrollment procedure and initial large jump in enrollment that occurred simultaneously with program launch. In addition, we report results for multiple income categories (above and below 150 percent FPL, 150–200 percent FPL, 200–300 percent FPL, and above 300 percent FPL) and residents of rural and urban counties. We do not report separate results for adults and children, as they differ little from one another.

Percentage of Enrollees with Private Coverage at Enrollment

Table 3 includes a summary of our calculations of the strict bounds for the percentage of newly enrolled individuals with private health insurance at the time they enrolled in BC+. We find a lower bound of 13.6 percent on the percentage of enrollees with private health insurance at the time of enrollment prior to the program expansion. As described above, this lower bound assumes that no enrollees who did not have non-group or ESI from a fully insured employer (based on TPL) and either themselves worked or had a family member who worked at a self-insured firm were covered by that firm’s insurance plan. The upper bound of 26.9 percent alternately assumes that 100 percent of these enrollees were enrolled in a self-insured plan.

Table 3.

What Percentage of Newly Enrolled Individuals Were Privately Insured at or Near the Time of Enrollment?

| [Lower bound, upper

bound] |

Estimate |

|||||

|---|---|---|---|---|---|---|

| January 06–January 08 | February 08–March 08 | April 08–May 09 | January 06–January 08 | February 08–March 08 | April 08–May 09 | |

| All | [13.6%, 26.9%] | [29.1%, 41.7%] | [16.0%, 28.7%] | 19.3% (.180, .201) | 34.4% (.331, .357) | 21.2% (.200, .223) |

| By poverty level | ||||||

| <150 | [13.2%, 26.3%] | [25.4%, 38.2%] | [14.3%, 26.2%] | 18.9% (.173, .203) | 30.4% (.290, .318) | 18.9% (.176, .202) |

| >150 | [18.8%, 34.3%] | [37.4%, 49.8%] | [23.6%, 39.4%] | 26.8% (.250, .287) | 43.5% (.420, .450) | 31.3% (.297, .329) |

| 150–200 | [18.3%, 33.9%] | [37.2% 50.4%] | [21.5%, 37.8%] | 23.9% (.227, .252) | 42.4% (.408, .439) | 27.6% (.261, .292) |

| 200–300 | [33.8%, 45.8%] | [37.9%, 49.1%] | [28.7%, 43.2%] | 37.8% (.370, .387) | 41.0% (.397, .423) | 32.9% (.317, .341) |

| 300+ | [29.2%, 42.3%] | [37.4%, 45.9%] | [32.5%, 45.4%] | 35.0% (.342, .357) | 39.7% (.378, .415) | 37.0% (.356, .384) |

| By county | ||||||

| Urban | [15.2%, 29.0%] | [31.1%, 43.7%] | [17.8%, 30.9%] | 19.1% (.177, .204) | 35.1% (.338, .364) | 21.7% (.206, .229) |

| Rural | [12.7%, 25.7%] | [27.9%, 40.6%] | [15.1%, 27.5%] | 16.3% (.153, .174) | 32.0% (.308, .333) | 18.8% (.178, .198) |

Source. Authors’ tabulations from WI CARES System, UI System, and Department of Labor.

Note. Tabulations include only new enrollees; all of the enrollees in January 2006 are left-censored, so we cannot observe the start-date of their spells. We exclude these censored observations from our analysis. We report in parentheses 95 percent normal bootstrap confidence intervals from at least 300 replications. All differences by column (across time periods) are significantly different from one another at the 95 percent level. UI = Unemployment Insurance.

We next consider the initial expansion period. Relative to the pre-expansion period, both upper and lower bounds are roughly 15 percentage points higher, at [29.1%, 41.7%]. This higher rate of private insurance coverage at the time of enrollment is mostly due to higher prevalence of private coverage among individuals who were auto-enrolled into BC+ in February 2008, although we also find slightly higher than average percentages with private health insurance among non-auto enrollees in February and March 2008.7

In the post-expansion period (April 2008–November 2008), our lower bound is 16.0 percent of the percentage of new enrollees with private health insurance at the time of enrollment, and our upper bound is 28.7 percent.

Again, lower and upper bounds are calculated under very conservative assumptions, given that we do not know whether a worker is eligible for ESI from their employer. However, despite making such conservative assumptions, our upper bounds are below many estimates of crowd-out in the existing literature.

Similarly, our strict lower bound is above some of the lower estimates of crowd-out in the existing literature. But, as we will show below, a significant portion of enrollees maintain their private coverage for at least six months following enrollment into BC+.

Figure 2 shows the monthly number of new enrollees, from February 2006 to June 2009. It also shows the number of new enrollees who were matched to the TPL data (and thus had private insurance from a non-group plan or from a fully insured employer-sponsored plan) but did not experience a job loss according to the UI data, and the number who were matched to either TPL or DOL (indicating the additional possibility of having coverage from a self-insured firm) and had no job loss. With the exception of February 2008, the number of enrollees in each category is fairly steady from month to month, with a slight upward trend in enrollment over the time period.

Figure 2.

Summary of administrative data matches, by month.

Note. TPL = Third Party Liability; DOL = Department of Labor.

Figure 3 illustrates the strict upper and lower bounds of the percentage of new enrollees with private insurance coverage at the time of enrollment over time. The strict upper and lower bounds on this percentage are fairly steady within time periods, are notably higher in February 2008, and are slightly higher in the post-reform period.

Figure 3.

Strict upper and lower bounds of the percent with private insurance at enrollment.

As an alternative to estimating strict bounds, we use survey data to estimate the probability of ESI coverage and apply those estimates to impute this probability among enrollees who are employed or who have a family member employed at a self-insured firm. As described above, we use the CPS to predict the probability of a worker having private health insurance conditional upon his or her employment status and demographic characteristics. The model is further described in the appendix and its estimated parameters are reported in Table A2 of the appendix. When these parameters are applied to our administrative data, we estimate that on average, 42 percent of enrollees who work for or who have a family member who works for a firm with a self-funded insurance plan are covered by ESI.

Using this method, we then estimate the percentage of new enrollees with private insurance at the time of enrollment to be 19.3 percent (95 percent CI [18.0%, 20.1%])8 during the pre-expansion period. During the initial program expansion period, we estimate this percentage to be 34.4 percent (95 percent CI [33.1%, 35.7%]). We estimate that in the post-BC+ expansion period, 21.2 percent (95 percent CI [20.0%, 22.3%]) of all enrollees had private insurance coverage at the time of enrollment. These results are summarized in Table 3.

Table 3 also presents the upper bounds, lower bounds, and point estimates stratified by income as a percentage of FPL by whether the county of residence was urban (defined as Milwaukee, Waukesha, and Dane counties) or rural (all other Wisconsin counties). Higher family income (as a percentage of FPL) was generally associated with a higher percentage of enrollees having private insurance at the time of enrollment. Enrollees living in urban as opposed to rural counties were slightly more likely to have private insurance.

Because our estimates rely on two very different sources of data—the TPL data for those with private coverage through non-group insurance or fully insured ESI and the DOL data for those potentially with coverage through self-funded plans—we separate the sources of the estimates into these two components in Table 4 to clarify these elements. For example, of the 21.2 percent of new enrollees between April 2008 and May 2009 that we estimate to have private health insurance at the time of enrollment, 16.0 percentage points represent those with coverage from a non-group plan or fully insured ESI (TPL) and 5.2 percentage points is estimated to come from coverage from a self-insured firm (DOL). Of the upper bound of 28.7 percent, 16.0 percent comes from TPL and 12.7 percent from DOL.

Table 4.

Data Sources for Estimates.

| Point

estimate |

Upper bound |

|||||

|---|---|---|---|---|---|---|

| January 06–January 08 | February 08–March 08 | April 08–May 09 | January 06–January 08 | February 08–March 08 | April 08–May 09 | |

| What percentage of newly enrolled individuals were privately insured at or near enrollment? | ||||||

| All | 19.3% | 34.4% | 21.2% | 26.9% | 41.7% | 28.7% |

| By source | ||||||

| TPL | 13.6% | 29.1% | 16.0% | 13.6% | 29.1% | 16.0% |

| DOL/CPS | 5.7% | 5.3% | 5.2% | 13.3% | 12.7% | 12.7% |

| What percentage of newly enrolled individuals dropped private insurance prior to disenrolling from BC+ (within six months of enrollment)? | ||||||

| All | 8.9% | 10.7% | 9.9% | 16.4% | 18.1% | 17.4% |

| By source | ||||||

| TPL | 3.1% | 5.5% | 4.7% | 3.1% | 5.4% | 4.7% |

| DOL/CPS | 5.8% | 5.2% | 5.2% | 13.3% | 12.7% | 12.7% |

Source. Authors’ tabulations from WI CARES System, UI System, and DOL.

Note. Table shows the portion of each estimate that comes from the two potential sources: the TPL database and the DOL data with CPS predictions. We first look for a match in TPL and then in DOL if no TPL match is found. Although reported here for the total population, relative proportions remain similar by subgroup. Left-censored observations are excluded. Rounding error may lead to imperfect addition. TPL = Third Party Liability; DOL = Department of Labor; CPS = Current Population Survey; UI = Unemployment Insurance.

We also calculated these percentages separately for children and adults, although we do not report them because they did not appreciably differ from one another. This is perhaps not surprising because the adults in this study are parents (or caretaker relatives), and children tend to have the same sources of private coverage as their parents.

Percentage of Enrollees That Dropped Private Coverage

We report our upper bound, lower bound, and point estimates of the percentage of enrollees who had private coverage at the time of enrollment and subsequently dropped that coverage in Table 5.

Table 5.

What Percentage of Newly Enrolled Individuals Dropped Private Insurance Prior to Disenrolling from BC+ (Within Six Months of Enrollment)?

| [Lower bound, upper

bound] |

Estimate |

|||||

|---|---|---|---|---|---|---|

| January 06–January 08 | February 08–March 08 | April 08–May 09 | January 06–January 08 | February 08–March 08 | April 08–May 09 | |

| All | [3.1%, 16.4%] | [5.4%, 18.1%] | [4.7%, 17.4%] | 8.9% (.076, .102) | 10.7% (.097, .118) | 9.9% (.088, .111) |

| By poverty level | ||||||

| <150 | [3.1%, 16.2%] | [4.9%, 17.7%] | [4.1%, 16.0%] | 8.7% (.073, .100) | 9.8% (.087, .110) | 8.7% (.075, .098) |

| >150 | [4.1%, 19.6%] | [6.8%, 19.2%] | [7.7%, 23.5%] | 12.2% (.104, .140) | 12.9% (.117, .140) | 15.4% (.138, .169) |

| 150–200 | [4.1%, 19.7%] | [6.0%, 19.2%] | [6.6%, 22.9%] | 9.3% (.082, .105) | 11.0% (.098, .122) | 12.5% (.110, .139) |

| 200–300 | [5.5%, 17.5%] | [7.6%, 18.7%] | [9.6%, 24.1%] | 9.5% (.089, .102) | 9.5% (.090, .100) | 12.9% (.121, .137) |

| 300+ | [5.4%, 18.5%] | [12.0%, 20.5%] | [15.8%, 28.7%] | 10.6% (.099, .112) | 13.3% (.125, .141) | 20.0% (.191, .211) |

| By county | ||||||

| Urban | [3.6%, 17.4%] | [6.5%, 19.1%] | [5.5%, 18.6%] | 7.2% (.063, .081) | 10.2% (.093, .111) | 9.2% (.082, .101) |

| Rural | [2.9%, 15.9%] | [4.9%, 17.6%] | [4.3%, 16.7%] | 6.2% (.055, .070) | 8.7% (.078, .096) | 7.9% (.070, .088) |

Source. Authors’ tabulations from WI CARES System, UI System, and Department of Labor.

Note. Tabulations include only new enrollees; all of the enrollees in January 2006 are left-censored, so we cannot observe the start-date of their spells. We exclude these censored observations from our analysis. We report in parentheses 95 percent normal bootstrap confidence intervals from at least three hundred replications. All differences by column (across time periods) are significantly different from one another at the 95 percent level with the exception of the above 150 and 200–300 income groups in the pre-reform and transitional periods. BC+ = BadgerCare Plus; UI = Unemployment Insurance.

During the pre-expansion period, 3.1 percent of new enrollees had dropped their private insurance coverage within six months after their enrollment month according to our TPL data match. This percentage is the lower bound. If, in addition, all those employed at DOL firms had private coverage and dropped that coverage, a total of 16.4 percent of new enrollees would have dropped their private insurance coverage. This percentage is the upper bound.

The upper and lower bounds for the expansion period are slightly higher. For February–March 2008, we find a lower bound of 5.4 percent and an upper bound of 18.1 percent. During the April 2008 to May 2009 post-expansion period, we find a lower bound of 4.7 percent and an upper bound of 17.4 percent.

Figure 4 illustrates the strict upper and lower bounds of the percentage of new enrollees that dropped private insurance coverage within six months of enrollment over time. The strict upper and lower bounds on this percentage are fairly steady across all time periods and are substantially lower than the bounds on the percentage with private insurance at the time of enrollment shown in Figure 3.

Figure 4.

Strict upper and lower bounds of the percent dropping private insurance within six months following enrollment.

If we predict the number of enrollees that have insurance from a self-insured firm using survey data (as described above) and assume that none of them drop this coverage, we estimate that in the pre-expansion period, 8.9 percent (95 percent CI [7.6%, 10.2%]) of enrollees dropped coverage soon after enrollment in BC+. This percentage was only slightly higher in the transitional period at 10.7 percent (95 percent CI [9.7%, 11.8%]). During the post-expansion period, we estimate that only 9.9 percent (95 percent CI [8.8%, 11.1%]) of new enrollees dropped private coverage within seven months of their enrollment date.

As with the estimates of the percentage of enrollees with private coverage at the time of enrollment, the estimates of the percentage that dropped private coverage are higher for those individuals in families with higher incomes as a percentage of FPL and are slightly higher for those enrollees who reside in urban counties.

Discussion

Wisconsin’s high-quality administrative data systems that allow linkages between databases tracking public insurance enrollment, private insurance coverage, and employment allows for precise measurement of the fraction of Medicaid enrollees that had private coverage at the time of enrollment and of the fraction that dropped this coverage. These longitudinal administrative data allow for the calculation of a measure of crowd-out that is similar to that measured in the previous literature. Our measure can help inform state and federal policymakers of the likely impacts of state-level public insurance coverage expansions on participation in private insurance markets.

Our findings suggest that recent expansions to Wisconsin’s Medicaid/CHIP program did not lead to a substantial reduction in private insurance coverage. Although a modest percentage—between 16.0 percent and 28.7 percent—of new enrollees had private coverage at the time of enrollment, only between 4.7 percent and 17.4 percent dropped this coverage with the remainder being dual covered.

Our estimates of crowd-out are relatively low compared with many estimates of crowd-out from Medicaid and CHIP expansions, which tend to be in the 25–50 percent range (CBO 2007). Moreover, they are low given that, at the time, Wisconsin policy stipulated that individuals were eligible for BC+ regardless of whether they had access to employer-sponsored insurance if either their family incomes were below 150 percent FPL or if they were required to pay more than 20 percent of an ESI premium. The large increase in public coverage in response to the BC+ expansion, therefore, substantially reduced the ranks of the uninsured or added secondary coverage to many families with private coverage.

Our estimates also indicate the existence of a relatively unexamined phenomenon—public insurance enrollees who hold both private and public coverage. A 2006 Government Accountability Office (GAO) report that uses the 2002–2004 CPS data to study this issue finds that, nationally, 13 percent of those who have Medicaid for the entire year also had private coverage at some point during that year, which is consistent with our findings (GAO 2006). We have no direct evidence on what motivates enrollees to hold private and public coverage simultaneously, although since Medicaid acts as a secondary payer in such cases, it may cover and expand scope of services, reduce out-of-pocket costs to the enrollees, or allow them to remain with a current provider.

While allowing dual coverage may seem unusual, it is not unique to Wisconsin. In 2010, we reviewed the websites for each state’s Medicaid program to determine which states allow their family and child program applicants to have dual coverage. Most states’ websites provided sufficient evidence to determine their dual coverage policy. When this was not the case, we called the state’s CHIP program office directly for further information. Nine states allowed some sort of dual coverage with their CHIP program: Alaska, Idaho, Indiana, Kansas, Maryland, Michigan, Oregon, South Dakota, and Wisconsin. These dual coverage programs range in breadth from allowing children/families with private insurance to be dually covered, with income restrictions (Alaska, Idaho, Indiana, Kansas, Maryland, South Dakota, and Wisconsin), to only allowing dual coverage in cases of underinsurance, again with income restrictions (Michigan and Oregon). We were unable to determine the policy toward dual coverage in five states (D.C., Hawaii, Maine, North Carolina, and Washington). These states’ websites were unclear on the subject of dual coverage and attempts to get more information by phone were unsuccessful. Thirty-seven states do not allow any sort of dual coverage. That is, individuals must not have private coverage under any circumstances to be eligible for these programs.

A limitation of our study, and one shared by the previous literature, is that we are unable to observe directly whether the individuals in our administrative data discontinue coverage voluntarily or whether their employers cease to offer it. In Wisconsin, there have been slight trends toward reduced employer offering and reduced employee take-up of employer-sponsored health insurance (State Health Access Data Assistance Center 2013).

We do not claim to capture all dimensions in which public coverage can substitute for private coverage. Specifically, we focus on those individuals who actually enroll in Medicaid and had private insurance at the time of enrollment. If potential enrollees are able to use Medicaid as an implicit insurance plan, available when needed but not necessary to maintain active enrollment, then we understate the degree of substitution. Most of our sample, however, would have no eligibility incentive to drop private coverage and go uninsured prior to taking up Medicaid given that BC+ premium cost-sharing does not apply to adults below 150 percent FPL and children below 200 percent FPL.

Finally, the recession that began in late 2007 and worsened throughout 2008 complicates the interpretation of the transition and post-period results. Employers could have been making changes to benefits during this time that affected the relative desirability of public and private insurance.

Despite these limitations, our study accurately captures the actual number of new Medicaid enrollees who substitute public coverage for private insurance and the number of new enrollees that were previously uninsured. Our study shows that using administrative data can yield credible estimates of the fraction of public health insurance program enrollees that have access to private health insurance. Moreover, it suggests that increases in public coverage in the post-CHIP era do not necessarily incur widespread substitution of public coverage for private coverage.

Acknowledgments

We gratefully acknowledge the financial support of Wisconsin’s Department of Health Services and the helpful comments of Robert Kaestner, Amanda Kowalski, Maximilian D. Schmeiser, Karl Scholz, and participants at the Annual Health Economics Conference, the ASSA meetings, the Population Association of America Annual Meetings, Indiana University Purdue University at Indianapolis, and the Center for Demography and Ecology seminar at the University of Wisconsin–Madison.

Appendix

We report summary statistics for our CPS sample in Table A1. We use this data to estimate a probit model of health insurance coverage. The predictors in the probit models include sex, age, geographic location, age of the youngest child in the family, educational level, self-employment status, occupational industry, firm size, earnings, and FPL. See Table A1 of the appendix for descriptive statistics on the CPS sample.

Table A1.

Descriptive Statistics from CPS Sample.

| Variable | Mean |

|---|---|

| Private insurance | 0.82 |

| Public insurance | 0.11 |

| Survey year 2008 | 0.32 |

| Survey year 2009 | 0.34 |

| Male | 0.68 |

| Dane County | 0.09 |

| Milwaukee County | 0.26 |

| Youngest child <5 | 0.4 |

| Youngest child 5–13 | 0.26 |

| Highest earner <34 | 0.26 |

| Highest earner 34–54 | 0.71 |

| Self-employed | 0.1 |

| Firm with 50 or fewer workers | 0.37 |

| FPL 151%–200% | 0.06 |

| FPL 200%–300% | 0.19 |

| FPL > 300% | 0.62 |

| High school graduate | 0.29 |

| Some college | 0.66 |

| Goods-producing industry | 0.31 |

| Highest earner <$10k | 0.02 |

| Highest earner $10k–$15k | 0.03 |

| Highest earner $15k–$20k | 0.03 |

| Highest earner $20k–$30k | 0.12 |

Note. Table shows weighted sample means for the population used in the probit model, the 2007–2010 CPS. Details of sample and variable construction are available in the text. CPS = Current Population Surveys; FPL = federal poverty level.

Except for FPL and age of the youngest child, all variables are employment or demographic characteristics of the highest earner in a family. These variables were selected and constructed to match with the available information in administrative data. The age of the highest earner is coded into 18–34, 35–54, and older than 54 years (reference group). The educational level of the highest earner is coded into less than high school (reference group), high school graduation or general education development test (GED) but no college education, and at least one year of college education. The size of the employer is coded into a dichotomous variable, with less than 100 as the reference group. The yearly earnings of the highest earner are coded into less than $10,000; $10,000–$14,999; $15,000–$19,999; $20,000–$29,999; and more than $30,000 (reference). Earnings are inflated to 2009 dollars using the Consumer Price Index for All Urban Consumers (CPI-U). FPL is divided into 150 percent and less (reference), 151–200 percent, 201–300 percent, and greater than 300 percent.

We use two indicators to identify the residential counties that are more diverse and highly urbanized: living in Dane county (mainly Madison) and living in Milwaukee or Waukesha counties. We first intended to separate urban and rural residential areas. Although CPS contains geographic information sufficient for our purpose, the administrative data only have residential county. We thus created two indicators of urban counties to match both data sets. We cannot separate Milwaukee from Waukesha in the CPS data.

We create a dichotomous indicator for the goods-producing industries, which were identified as agriculture/forestry, mining, construction, and manufacturing industries in the major industry code. Age of the youngest child is categorized into being younger than six, six to twelve (reference), and older than twelve. We also control for the survey year.

We use probit models to estimate the probability of having private insurance among workers. Table A2 of the appendix shows the marginal effects from the probit model. Because all variables are binary, the table reports the marginal effects of going from 0 to 1 for each. Our results suggest that residential area, earnings, industry, firm size, educational level, and family poverty levels predict the probability of having private insurance well. The workers from smaller firms and workers in non-goods producing industries are less likely to have health insurance. Earning and FPL are positively associated with having health insurance. The workers living in the two largest metropolitan counties in Wisconsin are more likely to have private insurance than those living in other areas. Self-employment is negatively associated with private insurance.

Table A2.

Marginal Effects from Probit Model.

| Marginal effect | |

|---|---|

| 2007 | 0.012 (0.02) |

| 2008 | −0.02 (0.046) |

| Male | −0.017 (0.02) |

| Dane County | 0.069* (0.035) |

| Milwaukee County | 0.039* (0.018) |

| Has child ≤5 | −0.018 (0.019) |

| Has child >5 and <13 | −0.023 (0.022) |

| Adult <34 | −0.059 (0.044) |

| Adult 34–54 | −0.015 (0.042) |

| Earnings <$10k | −0.306** (0.062) |

| Earnings $10k–$15k | −0.191** (0.045) |

| Earnings $15k–$20k | −0.123** (0.037) |

| Earnings $20k–$30k | −0.073** (0.024) |

| Goods industry | 0.076** (0.019) |

| Self-employed | −0.031 (0.026) |

| Small firm | −0.074** (0.017) |

| FPL 151%–200% | 0.029 (0.029) |

| FPL 201%–300% | 0.084** (0.028) |

| FPL > 300% | 0.176** (0.028) |

| High school graduate | 0.069* (0.03) |

| Some college | 0.124** (0.031) |

| Observations | 2,685 |

Note. Standard errors in parentheses. This table shows the marginal effects from the probit model used to predict the probability of private insurance over the administrative data. The model was estimated with data from the 2007–2010 CPS. Details of sample and variable construction are available in the text. FPL = federal poverty level; CPS = Current Population Surveys.

p < .05. **p < .01.

We include only new enrollees; all observations in January 2006 are left-censored, so we cannot observe the start-date of their spells. We exclude these censored observations from our analysis. We use the panel nature of the data to look six months ahead at private status, so although the data go through November 2009, the last new spells we include are those beginning in May 2009.

In general, Wisconsin employers are subject to Unemployment Insurance (UI) liability if they pay $1,500 or more in wages in any calendar quarter or have full or part-time employees working for them in twenty weeks or more during a calendar year. Special rules apply for agriculture, non-profit firms, and employers of domestic service workers.

A minor issue involves the usage of Federal Employer Identification Numbers (FEINs) to link data from different sources. FEINs are issued by the Internal Revenue Service for payroll tax reporting. Although a FEIN is unique to a firm, firms can have more than one FEIN if they have more than one location or operate under different names. For single-unit firms (which have only one establishment), there is a one-to-one relationship between the firm and the FEIN. However, multi-unit firms, such as chain stores, can have more than one FEIN, although each establishment can be associated with only one FEIN. Because the UI system sometimes cross-verifies data with the Internal Revenue Service, we are confident that FEINs used in the Department of Labor (DOL) and UI data are correctly matched. In addition, for a small sample of employers (including one retail chain, one company that owned several chains in the same industry, and one major manufacturer), we were able to directly verify that the FEINs that were submitted to UI and DOL were identical and accurately represented who owned the responsibility for the insurance offer.

Although employment information is available in CARES, Wolfe et al. (2006) found it to be of very low quality relative to UI information. Thus, we do not use employment information from CARES.

We only consider those workers who were living in a family (defined by Current Population Survey Annual Social and Economic Supplement [CPS-ASEC]) in which at least one relative child (i.e., under eighteen years old) was present. Workers who were in families without any related child or who were living alone with unrelated children were excluded from our analysis. For multiple-family households, the workers who were in unrelated subfamilies but had no related child in his or her own family would not be included in our sample.

We recognize the possibility that obtaining public coverage could induce individuals to reduce labor supply, which would result in our classifying intentional exits as job losses. Existing literature suggests that this is not a prevalent phenomenon (see, for example, Strumpf 2011). A more likely potential phenomenon is a switch to self-employment induced by receiving public coverage that results in the lack of a longitudinal match to the UI data. This phenomenon would suggest that we are misclassifying some intentional switches to self-employment as job losses. However, it is debatable whether these switches should be counted in the crowd-out figures, given that being “job locked” in a position with health insurance coverage when one prefers to be self-employed is widely considered to be welfare reducing (see, for example, Madrian 1994 and Monheit and Cooper 1994).

For a more detailed description of the auto-enrollment process that occurred in February 2008, please see DeLeire et al. (2012).

All reported confidence intervals for point estimates are 95 percent normal bootstrap confidence intervals from at least three hundred replications. Percentile and bias-corrected confidence intervals are very similar and are not reported here.

Footnotes

Authors’ Note: The views expressed in this article are those of the authors alone.

Declaration of Conflicting Interests: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding: The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by Wisconsin’s Department of Health Services.

References

- Blewett L., Call K. 2007. “Revisiting Crowd-Out.” The Synthesis Project: New Insights from Research Results, Update. Princeton, NJ: The Robert Wood Johnson Foundation. [Google Scholar]

- Congressional Budget Office. 2007. The State Children’s Health Insurance Program. Washington, DC: Congressional Budget Office. [Google Scholar]

- Cutler D. M., Gruber J. 1996. “Does Public Insurance Crowd Out Private Insurance?” Quarterly Journal of Economics 111:391–430. [Google Scholar]

- Davidson G., Blewett L., Call K. 2004. “Public Program Crowd-Out of Private Coverage: What Are the Issues?” The Synthesis Project: New Insights from Research Results, Policy Brief No. 5. Princeton, NJ: The Robert Wood Johnson Foundation. [PubMed] [Google Scholar]

- DeLeire T., Leininger L., Dague L., Mok S., Friedsam D. 2012. “Wisconsin’s Experience with Medicaid Auto-Enrollment: Lessons for Other States.” Medicare & Medicaid Research Review 2 (2): E1–20. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Farber H., Levy H. 2000. “Recent Trends in Employer-Sponsored Health Insurance: Are Bad Jobs Getting Worse?” Journal of Health Economics 19 (1): 93–119. [DOI] [PubMed] [Google Scholar]

- Government Accountability Office. 2006. “Medicaid Third Party Liability: Federal Guidance Needed to Help States Address Continuing Problems.” Publication No. GAO-06-962. http://www.gao.gov/cgi-bin/getrpt?GAO-06-862.

- Gruber J. 2003. “Medicaid.” In Means-Tested Transfer Programs in the United States, edited by Moffitt R. A. Chicago: University of Chicago Press,15-77. [Google Scholar]

- Gruber J., Simon K. 2008. “Crowd-Out 10 Years Later: Have Recent Public Insurance Expansions Crowded Out Private Health Insurance?” Journal of Health Economics 27 (2): 201–17. [DOI] [PubMed] [Google Scholar]

- Herd P., Harvey H., DeLeire T., Moynihan D. 2013. “Shifting Administrative Burden to the State: The Case Medicaid Take-Up.” Public Administration Review 73 (S1): S69–81. [Google Scholar]

- Kaiser Family Foundation. 2011. “Employer Health Benefits 2011 Annual Survey.” http://kaiserfamilyfoundation.files.wordpress.com/2013/04/8225.pdf .

- Kaiser Family Foundation. 2013. “Where Are States Today? Medicaid and CHIP Eligibility Levels for Children and Non-Disabled Adults.” http://kaiserfamilyfoundation.files.wordpress.com/2013/04/7993-03.pdf.

- Leininger L. J., Friedsam D., Mok S., Dague L., Hynes E., Bergman A., Aksamitauskas M., Oliver T., DeLeire T. 2011. “Wisconsin’s BadgerCare Plus Reform: Impact on Low-Income Families’ Enrollment and Retention in Public Coverage.” Pt. 2. Health Services Research 46 (1): 336–47. [DOI] [PMC free article] [PubMed] [Google Scholar]

- LoSasso A. T., Buchmueller T. 2004. “The Effect of the State Children’s Health Insurance Program on Health Insurance Coverage.” Journal of Health Economics 23 (5): 1059–82. [DOI] [PubMed] [Google Scholar]

- Madrian B. 1994. “Employment-Based Health Insurance and Job Mobility: Is There Evidence of Job-Lock?” Quarterly Journal of Economics 109 (1): 27–54. [Google Scholar]

- Manski C. 1995. Identification Problems in the Social Sciences. Cambridge, MA: Harvard University Press. [Google Scholar]

- Marquis M. S., Long S. H. 2003. “Public Insurance Expansions and Crowd Out of Private Coverage.” Medical Care 41 (3): 344–56. [DOI] [PubMed] [Google Scholar]

- Monheit A., Cooper P. 1994. “Health Insurance and Job Mobility: Theory and Evidence.” Industrial and Labor Relations Review 48 (1): 68–85. [Google Scholar]

- Shore-Sheppard L., Buchmueller T., Jensen G. 2000. “Medicaid and Crowding Out of Private Insurance: A Re-examination Using Firm-Level Data.” Journal of Health Economics 19 (1): 61–91. [DOI] [PubMed] [Google Scholar]

- State Health Access Data Assistance Center. 2013. “State-Level Trends in Employer-Sponsored Health Insurance.” SHADAC Report. Minneapolis: University of Minnesota. [Google Scholar]

- State Health Reform Assistance Network. 2013. “Coverage Alternatives for Low and Modest Income Consumers.” http://www.statenetwork-.org/wp-content/uploads/2013/04/State-Network-Manatt-Coverage-Alternatives-for-Low-and-Mode-st-Income-Consumers.pdf.

- Strumpf E. 2011. “Medicaid’s Effect on Single Women’s Labor Supply: Evidence from the Introduction of Medicaid.” Journal of Health Economics 30 (3): 531–48. [DOI] [PubMed] [Google Scholar]

- Thorpe K., Florence C. 1999. “Health Insurance Coverage among Children: The Role of Expanded Medicaid Coverage.” Inquiry 35 (4): 369–79. [PubMed] [Google Scholar]

- Wolfe B., Haveman R., Kaplan T., Young Cho Y. 2006. “SCHIP Expansion and Parental Coverage: An Evaluation of Wisconsin’s BadgerCare.” Journal of Health Economics 25 (6): 1170–92. [DOI] [PubMed] [Google Scholar]