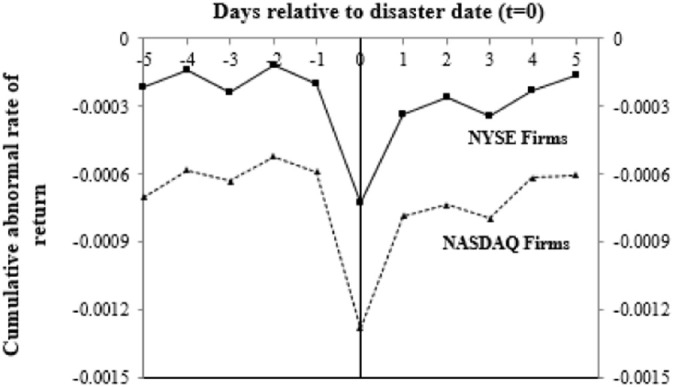

Fig. 1.

Cumulative abnormal rate of return (CAR). The figure depicts the Ebola outbreak effect surrounding the event day (t = 0) proxied by the CARs calculated using the market model for our sample of companies listed on the NYSE Composite and NASDAQ Composite. The events occurred during the 2014–2016 Ebola outbreak period (3-year period) and include a total number of 103 event days of the disease outbreak. The effect presented in the figure is based on a preliminary evaluation and it does not account for overlapping among the events' windows.