Abstract

Purpose

While the association between income and depression is well established, less explored is the relation between wealth and depression, particularly among low-income adults. We studied the relation between two types of assets—savings and home ownership—and probable depression to understand how access to different assets may shape depression among low-income US adults.

Methods

Study sample

We conducted a serial cross-sectional, observational study with 12,019 adults with low-income in the United States using National Health and Nutrition Examination Survey (NHANES) data from 2007–2016.

Measures

We measured probable major depressive disorder (MDD) with impairment using the Patient Health Questionnaire-9. Low savings was defined as having $5,000 or less in family savings.

Statistical analysis

We estimated adjusted and unadjusted prevalence, odds ratios, and predicted probability of probable MDD across asset groups.

Results

Of low-income US adults, 5.4% had probable MDD with impairment, 85.9% had low savings, and 54.9% rented their home. Persons with low savings had 2.34 (95% CI 1.44–3.79) times the odds of having probable MDD relative to those with high savings. Home owners had 2.14 (95% CI 1.20–3.86) and home renters had 3.65 (95% CI 1.45–9.20) times the odds of having probable MDD if they had low savings relative to high savings.

Conclusion

Family savings and home ownership are associated with lower burden of depression among low-income adults in the US.

Keywords: Mental health, depression, assets, housing, low-income

INTRODUCTION

Major depressive disorder (MDD) is a common mental illness in the United States. Eleven million or 4.5% of adults over 18 had at least one episode of MDD with impairment in 2017[1]. MDD affects the lives of those with mental illness and their family, social, and professional networks. It is estimated that MDD cost the US $210.5 billion in 2010, including direct medical costs, suicide-related mortality costs, and indirect workplace costs, such as presenteeism and absenteeism[2]. MDD is also associated with having more than one mental health disorder[3] and with having physical illness such as cardiovascular disease[4]. There is a robust literature on the causes of depression, which range from genetic factors to the physical and social environment[5–7].

Income is a well-established correlate of depression. Adults with lower income experience greater prevalence of MDD than persons with higher income[8]. For example, adults earning $19,999 or less in the US annually have 70% greater odds of 12-month MDD than adults earning more[9]. A meta-analysis of 56 studies on depression and socioeconomic status (SES) found that low-income adults had an average of 1.8 times the odds of being depressed relative to adults with higher SES[10]. This association is consistent globally; studies in China, Taiwan, and the Netherlands, among others, show similar associations between low income and MDD[11–13]. In the US, the relation of income to MDD is consistent across race/ethnicity, although recent studies suggest that the protective effect of income may be weaker in non-Hispanic Black persons compared to non-Hispanic white persons[14, 15].

There are several mechanisms through which income may be associated with depression. Having higher income leads to greater access of resources—including safer neighborhoods, healthier foods, and medical services—that protect against poor mental health[16]. Outside of access to material resources, higher income is also associated with social resources that protect against depression. For example, having a higher income may be associated with a higher social status in the workplace, greater control over ones’ schedule, and increased workplace autonomy; all may be associated with improved mental health[17]. Depression in and of itself also drives lower income. Depression may lead to lower income through missed work due to disability (absenteeism), underproduction (presenteeism), or unemployment[18].

Wealth is an additional asset that is independently associated with depression, over and above the role of income[19]. Wealth includes liquid assets, such as savings, and physical assets, such as homes. Among the studies on wealth and mental health, recent studies show that having savings is associated with lower risk of depression[20], and that childhood family savings is associated with reduced depression in young adults[21]. Wealth shocks in late middle-aged adults such as job loss or unexpected medical expenses are associated with increased prevalence of depressive symptoms, often a precursor of MDD[22]. There is a growing literature showing that having debt relative to available assets is also associated with depression[23]. One of the most common assets that contributes to wealth accumulation in the US is home ownership[24]. While housing instability is associated with increased depression[25], home ownership is associated with reduced depressive symptoms over time[26]. Owning a home provides stability and serves as another avenue for building wealth; in this way, it may be associated with reduced depression. Finally, neighborhood quality has been shown to be a significant factor in shaping mental health. Adults relocated to lower-poverty neighborhoods through the Moving to Opportunity (MTO) Study in New York City reported lower depressive symptoms two years after the relocation[27]. The effects of MTO appear to be mixed among adolescents, with female adolescents reporting improved mental health four to seven years after moving to lower-poverty neighborhoods with male adolescents reporting worse mental health than controls who did not move[28]. Other studies of relocation to safer neighborhoods have been met with reduced psychological distress[29], suggesting that housing and neighborhood quality shape mental health.

Having access to financial assets may in part reduce poor mental health because people can use their resources to avoid or mitigate stressors that cause poor health. Having family savings in particular may serve as a relatively flexible resource that can be used to address unexpected events[30] or even to move to neighborhoods with lower crime[27] or lower neighborhood disadvantage[31]. In this way, having family savings, particularly for low-income persons, may provide flexibility and may protect against poor mental health. Understanding how family savings and home ownership relate to depression among low-income populations can help guide interventions to prevent and treat mental illness. Addressing financial and physical assets could, for example, serve as an additional tool to prevent and mitigate poor mental health. No studies to our knowledge have looked at the connection between income, savings, and home ownership with MDD among a nationally representative group of low-income Americans.

This paper aimed to explore the relation between depression and wealth among low-income Americans. Low-income adults are at greater risk for worse health, from increased disability and higher rates of any number of chronic conditions to earlier death[32]. Thus, low-income adults may be particularly vulnerable to the effects of wealth. We studied a high-risk group—adults with low-income—to better understand how wealth relates to probable major depressive disorder, considering primarily the associations between household income, family savings, home ownership, and MDD in the US.

METHODS

Study sample

The National Health and Nutrition Examination Survey (NHANES) is an annual survey conducted by the US Government that collects health and household information about a representative sample of the US population. The present study combined data from NHANES cycles from 2007 through 2016, totaling five cycles over 10 years. 50,588 participants were interviewed from 2007–2016. For the purposes of this study we excluded persons below the age of 18 (n=19,864), persons with annual household income above 200% of the poverty level (n=16,651), and persons with missing depression data (n=2,054). The final sample contained 12,019 participants. The Brown University Human Research Protection Office determined that this study did not qualify as human subject research.

Measures

Probable major depressive disorder (MDD)

NHANES used the Patient Health Questionnaire (PHQ-9) to screen eligible participants via a computer assisted personal interview (CAPI). The PHQ-9 is a clinically validated tool for screening symptoms of depression based on the Diagnostic and Statistical Manual of Mental Disorders (DSM)-IV[33]. We created a binary response to each of the 9 symptom questions, coding them as positive if participants reported symptoms occurring more than half the time (except for suicidal ideation, which counted if participants had any presence of it). We then created a composite score for each participant. Probable major depressive disorder (MDD) with functional impairment was defined as having at least one of the two “cardinal symptoms” (1-having little interest in doing things or 2-feeling down or hopeless), having at least 4 of the other symptoms present more than half the time, and having any presence of functional impairment. This definition is consistent with others for probable MDD with functional impairment[34].

Savings

Family savings was defined as a binary variable; $5,000 or less in family savings was considered low savings and more than $5,000 was considered high savings. In years 2007–2014, participants were asked, “Do {you/NAMES OF OTHER FAMILY/you and NAMES OF FAMILY MEMBERS} have more than $5,000 in savings at this time? Please include money in your checking accounts.” Interviewers were given additional instructions that savings included cash, savings or checking accounts, stocks, bonds, mutual funds, retirement funds (such as pensions, IRAs, 401Ks) and certificates of deposit. In 2015–2016, participants were asked if they had $20,000 in family savings. If not, they were then asked their total savings or cash assets at the time. Pooling together participants who had $5,000 or less from 2015–2016 and those who had $5,000 or less in 2007–2014, we created a binary variable for low savings.

Household income

Household income was divided into four categories, roughly following the interquartile range for the categorical variables of income among study participants at or below the 200% poverty level. Annual household income levels were “$0-$14,999,” “$15,000-$24,999,” “$25,000-$44,999,” and “≥$45,000”.

Home ownership

Home ownership was defined as a binary variable. Participants were asked “Is this {mobile home/house/apartment} owned, being bought, rented, or occupied by some other arrangement by {you/you or someone else in your family}?” Home ownership was defined as “1” for participants who reported it was owned or being bought by the participant or a family member and non-home ownership was defined as “0” for renting or another arrangement.

Gender, age, race/ethnicity, education, marital status, and household size

Gender was defined as a binary variable (female or male). Age was defined as a categorical variable, grouped at 18–39, 40–59, and 60 or older, consistent with NHANES analytic guidelines. Race/ethnicity was defined as a mutually exclusive categorical variable: non-Hispanic white, non-Hispanic Black, Hispanic, and Other, which included multiracial and non-Hispanic Asian. Education was defined as a categorical variable: less than a high school degree, a high school degree or GED, having some college, and having a college degree or more. Marital status was defined as married; widowed, divorced, or separated; never married; or living with partner. Household size was defined as a continuous variable from 1 to 7.

Statistical analyses

First, we summarized unweighted frequencies of demographic characteristics across the study sample. Second, we tabulated percentages of demographic characteristics and prevalence of probable MDD in the sample weighted to the US population. Third, we estimated two-tailed weighted Pearson chi-square analysis to determine the bivariable relationship between demographics and depression, savings, and home ownership. Fourth, we estimated weighted odds ratios for the relation of savings and probable MDD. We used multiple logistic regression to calculate odds ratios and 95% confidence intervals. We present an unadjusted estimate and an adjusted estimate. The adjusted model controlled for gender, age, race/ethnicity, marital status, education, household income, home ownership, household size, family savings and NHANES cohort. Fifth, we estimated weighted odds ratio for the relation of probable MDD and savings across home owners and non-home-owners, controlling for all demographic variables and NHANES cohort waves. Sixth, we estimated the weighted predicted probabilities of probable MDD for those with and without savings among home owners and non-home-owners. We used STATA software, version 15.1, (College Station, TX: StataCorp LP) for all analyses, and incorporated the NHANES MEC survey weights for all weighted analyses.

Sensitivity analyses

First, we conducted sensitivity analysis to assess the potential bounds of associations under extreme assumptions for missing values for MDD and savings. We assessed four scenarios: in scenario 1, we assumed that all participants missing depression data had MDD and that all participants missing savings data had low savings; in scenario 2, we assumed that all participants missing depression data had MDD and that all participants missing savings data had high savings; in scenario 3, we assumed that all participants missing depression data did not have MDD and that all participants missing savings data had low savings; and in scenario 4, we assumed that all participants missing depression data did not have MDD and that all participants missing savings data had high savings. We imputed values for MDD and savings according to each scenario. With the imputed values, we measured effect estimates for each scenario to map out the extreme bounds of possible associations and to assess the range of potential true effect estimates. Second, we assessed robustness of our primary associations to various definitions of probable depression by rerunning all analyses with PHQ-9 scale score cutoffs of 5, 10, and 15.

RESULTS

Table 1 shows the frequency and percentage of demographic characteristics of the survey sample. Percentages were weighted to the US population. Of the weighted sample, 5.4% had probable MDD with functional impairment, 85.9% had less than $5,000 in family savings, and 45.1% owned their home.

Table 1.

Relation between characteristics and current probable major depressive disorder, savings, and home ownership of US adults at or below the 200% poverty level.

| Characteristic | Total | Probable major depressive disorder | Savings at or below $5,000 | Owned home | |||

|---|---|---|---|---|---|---|---|

| N (%) | N (%) | p-value | N (%) | p-value | N (%) | p-value | |

| 12,019 | 630 (5.4%) | 9,996 (85.9%) | 5,279 (45.1%) | ||||

| Gender | |||||||

| Male | 5,727 (46.1%) | 223 (4.0%) | < 0.001 | 4,722 (86.1%) | 0.615 | 2,585 (45.1%) | 0.954 |

| Female | 6,292 (53.9%) | 407 (6.6%) | 5,274 (85.8%) | 2,694 (45.0%) | |||

| Age | |||||||

| 18–39 | 4,966 (46.9%) | 203 (3.9%) | < 0.001 | 4,345 (90.0%) | < 0.001 | 1,499 (30.8%) | < 0.001 |

| 40–59 | 3,372 (29.4%) | 275 (8.6%) | 2,936 (90.9%) | 1,527 (49.7%) | |||

| 60+ | 3,681 (23.7%) | 152 (4.3%) | 2,715 (71.2%) | 2,253 (67.6%) | |||

| Race/Ethnicity | |||||||

| Non-Hispanic white | 4,429 (53.6%) | 291 (6.3%) | 0.002 | 3,378 (80.0%) | < 0.001 | 2,380 (53.0%) | < 0.001 |

| Non-Hispanic Black | 2,730 (16.0%) | 132 (5.3%) | 2,394 (93.2%) | 868 (29.1%) | |||

| Hispanic | 3,840 (23.2%) | 173 (4.0%) | 3,439 (94.8%) | 1,638 (39.4%) | |||

| Other | 1,020 (7.2%) | 34 (3.9%) | 785 (83.1%) | 393 (40.0%) | |||

| Education | |||||||

| Less than HS graduate | 4,527 (31.1%) | 246 (5.6%) | 0.069 | 3,995 (91.7%) | < 0.001 | 2,004 (45.3%) | 0.151 |

| HS graduate or GED | 3,142 (27.2%) | 171 (5.9%) | 2,607 (85.8%) | 1,407 (47.4%) | |||

| Some college | 3,276 (31.1%) | 172 (5.4%) | 2,672 (85.4%) | 1,385 (42.8%) | |||

| College graduate or more | 1,065 (10.5%) | 41 (3.4%) | 715 (69.4%) | 478 (45.3%) | |||

| Marital status | |||||||

| Married | 4,497 (38.7%) | 180 (4.0%) | < 0.001 | 3,557 (81.0%) | < 0.001 | 2,558 (58.0%) | < 0.001 |

| Widowed, divorced, or separated | 3,157 (25.7%) | 236 (8.0%) | 2,603 (85.2%) | 1,440 (48.7%) | |||

| Never married | 2,422 (24.3%) | 134 (5.4%) | 2,072 (89.5%) | 701 (29.0%) | |||

| Living with partner | 1,138 (11.4) | 61 (6.0%) | 1,040 (94.0%) | 329 (31.8%) | |||

| Household income | |||||||

| $0-$14,999 | 3,502 (26.3%) | 238 (7.0%) | < 0.001 | 3,168 (90.8%) | < 0.001 | 1,190 (34.8%) | < 0.001 |

| $15,000-$24,999 | 3,687 (30.9%) | 206 (6.1%) | 3,043 (84.3%) | 1,702 (46.7%) | |||

| $25,000-$44,999 | 3,594 (32.4%) | 149 (4.1%) | 2,888 (83.6%) | 1,808 (51.9%) | |||

| ≥$45,000 | 1,021 (10.5%) | 21 (2.5%) | 712 (83.5%) | 544 (49.7%) | |||

| Savings | |||||||

| $5,000 or less | 9,996 (85.9%) | 588 (6.1%) | < 0.001 | - | 3,921 (39.7%) | < 0.001 | |

| Over $5,000 | 1,351 (14.1%) | 29 (2.3%) | - | 975 (72.5%) | |||

| Home ownership | |||||||

| Owned home | 5,279 (45.1%) | 220 (4.7%) | 0.047 | 3,921 (76.9%) | < 0.001 | - | |

| Rented home or other arrangement | 6,734 (54.9%) | 409 (6.0%) | 6,070 (93.0%) | - | |||

| Probable major depressive disorder | |||||||

| Yes | 630 (5.4%) | - | 588 (94.2%) | < 0.001 | 220 (39.3%) | 0.037 | |

| No | 11,389 (94.6%) | - | 9,408 (85.5%) | 5,059 (45.4%) | |||

| Mean (95% CI) | Mean | Mean (95% CI) | Mean (95% CI) | ||||

| Household size | 3.3 (3.3 – 3.4) | 3.0 | 3.5 (3.4 – 3.5) | 3.3 (3.2 – 3.4) | |||

Note: Data: Adults ages 18 years or older from the 2007–2016 NHANES (n= 12,019). Frequencies (N) are unweighted. Percentages (%) and means are weighted. Percentages may not add up to 100% due to rounding. Probable major depressive disorder (MDD) with impairment measured using the Patient Health Questionnaire-9. Two-tailed chi-square analysis done for significance testing at the 95% level. Missing values excluded: education (n=9), marital status (n=805), household income (n=215), savings (n=672), and home ownership (n=6).

Table 1 also shows the bivariable relations between survey sample demographic characteristics and probable MDD, savings, and home ownership.

The following variables were associated with probable MDD (p <0.05): gender, age, race/ethnicity, marital status, household income, savings, and home ownership. More women (6.6%) than men (4.0%) had probable MDD. Prevalence of probable MDD varied by race/ethnicity: 6.3% of Non-Hispanic white persons, 5.3% of non-Hispanic Black persons, 4.0% of Hispanic persons, and 3.9% of other races had probable MDD. Participants ages 40–59 were more likely to have probable MDD (8.6%) than participants ages 18–39 (3.9%) or 60+ (4.3%). The prevalence of probable MDD was 7% for participants with an annual household income of $0-$14,999, 6.1% for $15,000-$24,999, 4.1% for $25,000-$44,999, and 2.5% for participants with a household income above $45,000. The average weighted household size for a person with depression was 3.0 and without depression was 3.5.

The following variables were associated with savings (p <0.05): age, race/ethnicity, education, marital status, household income, home ownership, and probable MDD. Participants below age 60 were more likely to have low savings than those ages 60 or older. Of non-Hispanic white participants, 80% did not have more than $5,000 in family savings; of non-Hispanic Black participants, 93.2% did not have $5,000 in family savings; of Hispanic participants, 94.8% did not have $5,000 in family savings; of other races, 83.1% did not have $5,000 in family savings. Of participants without a high school degree, 91.7% did not have family savings; of participants with a college degree or more, 69.4% did not have family savings. Of participants who owned a home, 76.9% did not have family savings; of participants who did not own a home, 93% did not have family savings. Of participants with probable MDD, 94.2% did not have family savings. Of participants without probable MDD, 85.5% did not have family savings.

The following variables were associated with home ownership (p <0.05): age, race/ethnicity, marital status, household income, savings, and probable MDD. Of participants with more than $5,000 in family savings, 72.5% owned a home; of participants without more than $5,000 in family savings, 39.7% owned a home. Of participants with probable MDD, 39.3% owned a home. Of participants without probable MDD, 45.4% owned a home.

Table 2 shows unadjusted and adjusted odds ratios of probable MDD for having less than compared to greater than $5,000 in family savings. The unadjusted odds ratio for having low savings was 2.77 (95% CI 1.67–4.61); the adjusted odds ratio controlling for all demographic characteristics was 2.34 (95% CI 1.45–3.79). Thus, the odds of having probable MDD with functional limitations was 2.34 times greater for low-income adults without $5,000 in family savings than those with $5,000 in family savings, controlling for gender, age, race/ethnicity, education, marital status, household income, home ownership, household size, and NHANES cohort wave.

Table 2.

Unadjusted and adjusted odds ratio of probable major depressive disorder by low family savings.

| Unadjusted OR (95%CI) | Fully adjusted OR (95% CI) | |

|---|---|---|

| Savings at or below $5,000 | 2.77 (1.67–4.61) | 2.34 (1.45–3.79) |

Note: Data: Adults ages 18 years or older from the 2007–2016 NHANES. Fully adjusted model controlled for age, race/ethnicity, education, marital status, household income, household size, and NHANES cohort wave. Probable major depressive disorder (MDD) with impairment measured using the Patient Health Questionnaire-9.

Table 3 shows the unadjusted and adjusted odds ratios of having probable MDD for low savings groups across home owners and non-home owners. The unadjusted odds ratio of probable MDD with functional impairment was 2.29 (95%CI 1.23 – 4.27) for participants without $5,000 in family savings who own homes. The fully adjusted odds ratio of MDD was 2.15 (95% CI 1.20–3.86) for low savings home-owners relative to high savings home-owners. The unadjusted odds ratio of MDD for low savings non-home owners was 4.06 (95% CI 1.66–9.91). The fully adjusted odds ratio of MDD for low savings non-home owners was 3.65 (95%CI 1.45–9.20), controlling for gender, age, race/ethnicity, education, marital status, household income, household size, and NHANES cohort wave.

Table 3.

Unadjusted and adjusted odds ratio of probable major depressive disorder with impairment for persons with low savings relative to high savings by home ownership status.

| Unadjusted OR (95%CI) | Fully adjusted OR (95% CI) | |

|---|---|---|

| Home owner | 2.29 (1.23–4.27) | 2.15 (1.20–3.86) |

| Non-home owner | 4.06 (1.66–9.91) | 3.65 (1.45–9.20) |

Note: Data: Adults ages 18 years or older from the 2007–2016 NHANES. Fully adjusted model controlled for age, race/ethnicity, education, marital status, household income, household size, and NHANES cohort wave. Probable major depressive disorder (MDD) with impairment measured using the Patient Health Questionnaire-9.

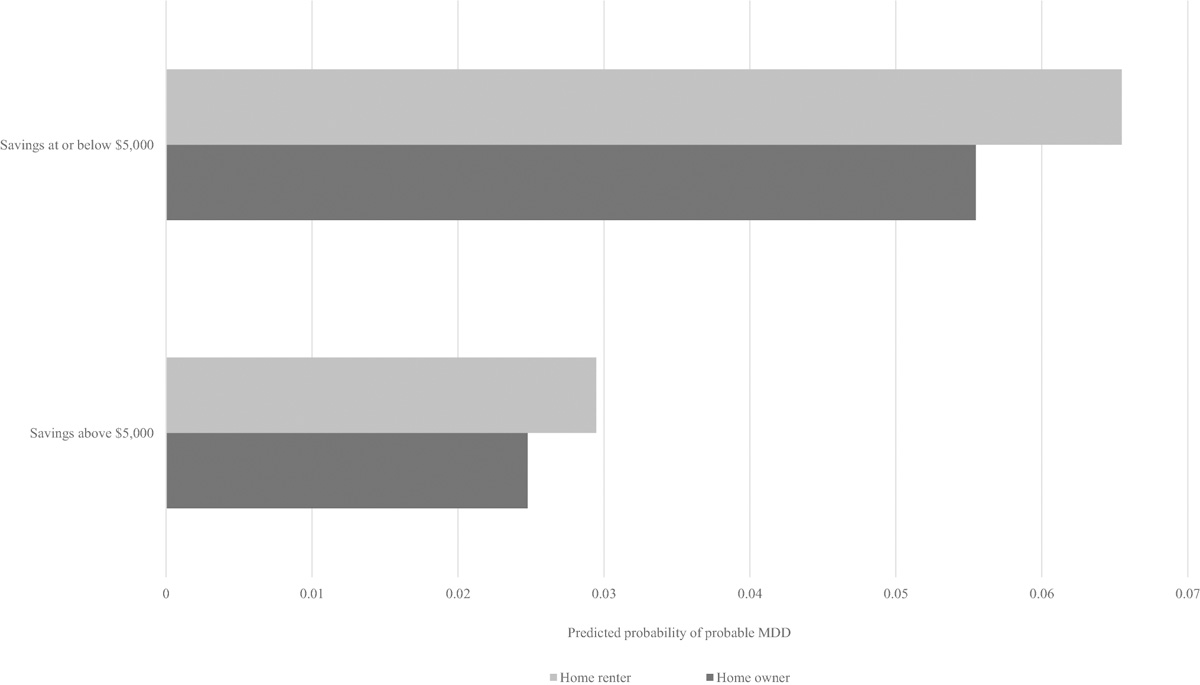

Figure 1 shows the predicted probability of depression by savings and home ownership. The predicted probability of probable MDD for a home owner with low savings was 5.55%, while that for a non-home owner with low savings was 6.55%, that for a home owner with above $5,000 in family savings was 2.48% and that for a home owner without $5,000 in family savings was 2.95%.

Figure 1.

Predicted probability of depression by savings and home ownership.

Note: Fully adjusted model controlled for age, race/ethnicity, education, marital status, household income, household size, and NHANES cohort wave.

Sensitivity analyses

Supplemental Table 1 shows adjusted and unadjusted odds ratios for savings on depression symptoms with potential extreme scenarios for missing values. All effect estimates remained positive. Supplemental Table 2 shows results of adjusted and unadjusted logistic regressions for savings on depression symptoms at continuous cutoffs of 5, 10, and 15. The positive association between low savings and depression held across all definitions of depression in all models (p-value <0.05). Predicted probabilities of depression symptoms across savings and home ownership groups (not shown) also produced similar patterns across all depression definitions.

DISCUSSION

We found that income, family savings, and home ownership were each associated with probable MDD in low-income adults in the US. The prevalence of probable MDD was higher among lower income categories. Having $5,000 or less in family savings was associated greater odds of depression compared to having more than $5,000 in family savings. The magnitude of the association of not having savings with depression was greater among non-home owners than home owners. The predicted probability of probable MDD was higher among non-home owners than home owners in both the savings and non-savings groups. These findings suggest that there is a relation between wealth and depression above and beyond the documented association between income and depression for low-income Americans.

Our findings are consistent with other studies that have found an inverse relation between wealth and poor mental health. Lê-Scherban et al. found that adolescents with higher family wealth during childhood had a lower prevalence ratio of depression than those in the bottom quartile of wealth[21]. This analysis was closest to the present study in that they looked at wealth and depression at the individual level. Scholten et al. looked to measures of objective and subjective wealth and prediction of mental health across eight countries[35]. At the individual-level, they found that increased perceived wealth was associated with reduced symptoms of depression, anxiety, and stress. Demakakos et al. analyzed subjective social status (SSS) and depression and controlled for wealth as defined by total (non-pension) assets, including houses and all forms of savings. Wealth was strongly correlated with SSS[36]. They suggested that SSS mediated some of the relation between wealth and depression. Johnson and Krueger conducted a twin study and found that perceived financial situation appeared to protect life-satisfaction more than objective wealth. They suggest that wealth protects life satisfaction against environmental disruptions and that having wealth provides individuals with more perceived control over their context[37]. Thus, wealth may affect depression through mechanisms beyond financial stability.

Our finding that depression was higher among home renters than home owners is consistent with housing and health frameworks that show that stable housing is associated with improved mental health[38]. This could be a sign that renting is on average less stable than home ownership. In a systematic review of the literature on mental health and home foreclosure, the majority of studies showed worsened mental health following foreclosure or for persons behind on their mortgage payments[39]. Low-income adults are more likely to face foreclosure, amplifying their exposure to risks that low-income individuals face for depression. In a review of the literature on housing and health, Taylor articulated four pathways through which housing relates to health broadly: stability, safety and quality, affordability, and the neighborhood pathway[40]. Our findings were consistent with the theories surrounding stability, affordability, and improved neighborhood. Owning a home may be associated not only with improved financial wellbeing (asset accumulation) but also with improved social status, increased control, and stability, all of which may be protective of mental health.

Limitations

This study has several limitations. First, this was a cross-sectional study, limiting our ability to assess temporality. Therefore, the observations noted here may equally well suggest that low savings lead to depression as that depression leads to low savings. Second, we were limited by the data. NHANES only asked participants about family savings if they were 200% at or below the poverty level from 2007 through 2014 and only starting asking all participants about savings in 2015–2016. Therefore, we are unable to document whether the association between wealth and depression differed between low- and higher-income populations. However, the most recent wave of NHANES (2015–2016) included questions about savings for all participants, allowing researchers to assess these relations across income levels. Other studies using the 2015–2016 NHANES wave to assess depressive symptoms have found that home ownership and family savings are associated with reduced depressive symptoms across all income groups[20]. Understanding these relations across income categories can better define interventions and prevention strategies. Third, the PHQ-9 used to measure of probable MDD is a screener for depressive symptoms and is not a diagnostic instrument on its own; a formal diagnosis of MDD would be made by a physician or medical professional. However, the PHQ-9 has been clinically validated with a sensitivity and specificity of 88%[33], serving as a reliable tool to measure depressive symptoms at the population-level.

Notwithstanding these limitations, this study documents the relation between wealth and depression, and that explores how multiple forms of wealth (savings and housing) relate to depression. Recognizing these associations is an important step in better understanding the relation between wealth and mental health. Resources such as savings and physical assets, including homes, may reduce financial strain and, in turn, protect against depression. Investing in social determinants, such as ownership of assets, may be a promising intervention to improve population mental health.

Supplementary Material

Acknowledgments

Funding

Catherine K. Ettman worked on this project while funded by the National Institutes of Health T32 AG 23482-15.

Footnotes

Publisher's Disclaimer: This Author Accepted Manuscript is a PDF file of an unedited peer-reviewed manuscript that has been accepted for publication but has not been copyedited or corrected. The official version of record that is published in the journal is kept up to date and so may therefore differ from this version.

Declarations

Conflicts of interest/Competing interests: Not applicable.

Code availability: STATA software, version 15.1, (College Station, TX: StataCorp LP) used.

Conflict of interest: No financial disclosures were reported by the authors of this paper.

Ethics approval

The Brown University Human Research Protection Office determined that this study did not qualify as human subject research.

Availability of data and material:

Data used are available to the public through the National Center for Health Statistics: https://www.cdc.gov/nchs/nhanes/index.htm

References

- 1.NIMH » Major Depression. https://www.nimh.nih.gov/health/statistics/major-depression.shtml. Accessed 19 Jul 2019

- 2.Greenberg PE, Fournier A-A, Sisitsky T, et al. (2015) The economic burden of adults with major depressive disorder in the United States (2005 and 2010). J Clin Psychiatry 76:155–162. 10.4088/JCP.14m09298 [DOI] [PubMed] [Google Scholar]

- 3.Kessler RC, Berglund P, Demler O, et al. (2003) The epidemiology of major depressive disorder: results from the National Comorbidity Survey Replication (NCS-R). JAMA 289:3095–3105. 10.1001/jama.289.23.3095 [DOI] [PubMed] [Google Scholar]

- 4.Goldstein BI, Carnethon MR, Matthews KA, et al. (2015) Major depressive disorder and bipolar disorder predispose youth to accelerated atherosclerosis and early cardiovascular disease: a scientific statement from the American Heart Association. Circulation 132:965–986. 10.1161/CIR.0000000000000229 [DOI] [PubMed] [Google Scholar]

- 5.Eaton WW, Shao H, Nestadt G, et al. (2008) Population-based study of first onset and chronicity in major depressive disorder. Arch Gen Psychiatry 65:513–520. 10.1001/archpsyc.65.5.513 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Kessler RC (1997) The effects of stressful life events on depression. Annu Rev Psychol 48:191–214. 10.1146/annurev.psych.48.1.191 [DOI] [PubMed] [Google Scholar]

- 7.Nedic Erjavec G, Svob Strac D, Tudor L, et al. (2019) Genetic markers in psychiatry. Adv Exp Med Biol 1192:53–93. 10.1007/978-981-32-9721-0_4 [DOI] [PubMed] [Google Scholar]

- 8.Sareen J, Afifi TO, McMillan KA, Asmundson GJG (2011) Relationship between household Income and mental disorders: findings from a population-based longitudinal study. Arch Gen Psychiatry 68:419–427. 10.1001/archgenpsychiatry.2011.15 [DOI] [PubMed] [Google Scholar]

- 9.Hasin DS, Sarvet AL, Meyers JL, et al. (2018) Epidemiology of adult DSM-5 major depressive disorder and its specifiers in the United States. JAMA Psychiatry 75:336–346. 10.1001/jamapsychiatry.2017.4602 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Lorant V, Deliège D, Eaton W, et al. (2003) Socioeconomic inequalities in depression: a meta-analysis. Am J Epidemiol 157:98–112. 10.1093/aje/kwf182 [DOI] [PubMed] [Google Scholar]

- 11.Schaakxs R, Comijs HC, van der Mast RC, et al. (2017) Risk factors for depression: differential across age? The American Journal of Geriatric Psychiatry 25:966–977. 10.1016/j.jagp.2017.04.004 [DOI] [PubMed] [Google Scholar]

- 12.Lee C-T, Chiang Y-C, Huang J-Y, et al. (2016) Incidence of major depressive disorder: variation by age and sex in low-income individuals. Medicine (Baltimore) 95:. 10.1097/MD.0000000000003110 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Liu J, Yan F, Ma X, et al. (2015) Prevalence of major depressive disorder and socio-demographic correlates: Results of a representative household epidemiological survey in Beijing, China. J Affect Disord 179:74–81. 10.1016/j.jad.2015.03.009 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Amutah-Onukagha NN, Doamekpor LA, Gardner M (2017) An examination of the sociodemographic and health determinants of major depressive disorder among black women. J Racial Ethn Health Disparities 4:1074–1082. 10.1007/s40615-016-0312-2 [DOI] [PubMed] [Google Scholar]

- 15.Assari S (2018) High income protects whites but not African Americans against risk of depression. Healthcare (Basel) 6:. 10.3390/healthcare6020037 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Richardson R, Westley T, Gariépy G, et al. (2015) Neighborhood socioeconomic conditions and depression: a systematic review and meta-analysis. Soc Psychiatry Psychiatr Epidemiol 50:1641–1656. 10.1007/s00127-015-1092-4 [DOI] [PubMed] [Google Scholar]

- 17.Russo M, Lucifora C, Pucciarelli F, Piccoli B (2019) Work hazards and workers’ mental health: an investigation based on the fifth European Working Conditions Survey. Med Lav 110:115–129. 10.23749/mdl.v110i2.7640 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 18.Kessler RC (2012) The costs of depression. Psychiatric Clinics of North America 35:1–14. 10.1016/j.psc.2011.11.005 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Dijkstra-Kersten SMA, Biesheuvel-Leliefeld KEM, van der Wouden JC, et al. (2015) Associations of financial strain and income with depressive and anxiety disorders. J Epidemiol Community Health 69:660–665. 10.1136/jech-2014-205088 [DOI] [PubMed] [Google Scholar]

- 20.Ettman C, Cohen G, Galea S (2020) Is wealth associated with depressive symptoms in the United States? Annals of Epidemiology. 43: 25–31.e1. 10.1016/j.annepidem.2020.02.001 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Lê-Scherban F, Brenner AB, Schoeni RF (2016) Childhood family wealth and mental health in a national cohort of young adults. SSM - Population Health 2:798–806. 10.1016/j.ssmph.2016.10.008 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22.Pool LR, Needham BL, Burgard SA, et al. (2017) Negative wealth shock and short-term changes in depressive symptoms and medication adherence among late middle-aged adults. J Epidemiol Community Health 71:758–763. 10.1136/jech-2016-208347 [DOI] [PubMed] [Google Scholar]

- 23.Sweet E, Nandi A, Adam E, McDade T (2013) The high price of debt: household financial debt and its impact on mental and physical health. Soc Sci Med 91:94–100. 10.1016/j.socscimed.2013.05.009 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24.Wainer A, Zabel J (2019) Homeownership and wealth accumulation for low-income households. Journal of Housing Economics 101624. 10.1016/j.jhe.2019.03.002 [DOI] [Google Scholar]

- 25.Burgard SA, Seefeldt KS, Zelner S (2012) Housing instability and health: findings from the Michigan Recession and Recovery Study. Soc Sci Med 75:2215–2224. 10.1016/j.socscimed.2012.08.020 [DOI] [PubMed] [Google Scholar]

- 26.Szabo A, Allen J, Alpass F, Stephens C (2018) Longitudinal trajectories of quality of life and depression by housing tenure status. J Gerontol B Psychol Sci Soc Sci 73:e165–e174. 10.1093/geronb/gbx028 [DOI] [PubMed] [Google Scholar]

- 27.Leventhal T, Brooks-Gunn J (2003) Moving to Opportunity: an Experimental Study of Neighborhood Effects on Mental Health. Am J Public Health 93:1576–1582 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 28.Osypuk TL, Schmidt NM, Bates LM, et al. (2012) Gender and crime victimization modify neighborhood effects on adolescent mental health. Pediatrics 130:472–481. 10.1542/peds.2011-2535 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29.Cooper C, Bebbington PE, Meltzer H, et al. (2008) Depression and common mental disorders in lone parents: results of the 2000 National Psychiatric Morbidity Survey. Psychological Medicine 38:335–342. 10.1017/S0033291707001493 [DOI] [PubMed] [Google Scholar]

- 30.Ettman CK, Abdalla SM, Cohen GH, et al. (2020) Prevalence of Depression Symptoms in US Adults Before and During the COVID-19 Pandemic. JAMA Netw Open 3:e2019686–e2019686. 10.1001/jamanetworkopen.2020.19686 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Graif C, Arcaya MC, Diez Roux AV (2016) Moving to opportunity and mental health: Exploring the spatial context of neighborhood effects. Soc Sci Med 162:50–58. 10.1016/j.socscimed.2016.05.036 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Khullar D, Chokshi D (2018) Health, income, & poverty: where we are & what could help. Health Affairs. 10.1377/hpb20180817.901935 [DOI] [Google Scholar]

- 33.Kroenke K, Spitzer RL, Williams JBW (2001) The PHQ-9: validity of a brief depression severity measure. J Gen Intern Med 16:606–613. 10.1046/j.1525-1497.2001.016009606.x [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34.Prescott MR, Tamburrino M, Calabrese JR, et al. (2014) Validation of lay-administered mental health assessments in a large Army National Guard cohort. International Journal of Methods in Psychiatric Research 23:109–119. 10.1002/mpr.1416 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35.Scholten S, Velten J, Neher T, Margraf J (2017) Wealth, justice and freedom: objective and subjective measures predicting poor mental health in a study across eight countries. SSM - Population Health 3:639–648. 10.1016/j.ssmph.2017.07.010 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 36.Demakakos P, Nazroo J, Breeze E, Marmot M (2008) Socioeconomic status and health: the role of subjective social status. Soc Sci Med 67:330–340. 10.1016/j.socscimed.2008.03.038 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 37.Johnson W, Krueger RF (2006) How money buys happiness: genetic and environmental processes linking finances and life satisfaction. Journal of Personality and Social Psychology 90:680–691. 10.1037/0022-3514.90.4.680 [DOI] [PubMed] [Google Scholar]

- 38.Singh A, Daniel L, Baker E, Bentley R (2019) Housing disadvantage and poor mental health: a systematic review. Am J Prev Med 57:262–272. 10.1016/j.amepre.2019.03.018 [DOI] [PubMed] [Google Scholar]

- 39.Tsai AC (2015) Home foreclosure, health, and mental health: a systematic review of individual, aggregate, and contextual associations. PLoS One 10:. 10.1371/journal.pone.0123182 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 40.Taylor L (2018) Housing and health: an overview of the literature. Health Affairs Health Policy Brief. 10.1377/hpb20180313.396577 [DOI] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Data Availability Statement

Data used are available to the public through the National Center for Health Statistics: https://www.cdc.gov/nchs/nhanes/index.htm