Figure 1.

Models of Liability in Artificial Intelligence and Machine Learning

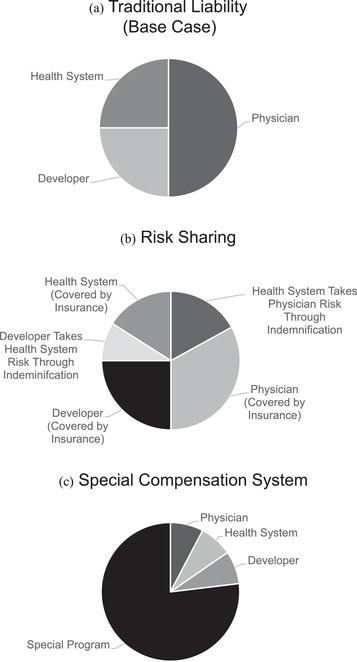

The precise division of liability in the figure models is arbitrary and not meant to reflect empirical liability, which varies by specialty, practice type, and locality, among other factors. In some cases, the precise distribution of liability is not known for a particular group due to the fragmentary nature of data in this area (e.g., settlements under individual insurance companies with nondisclosure agreements). Model A shows the division of liability under the traditional liability model. In model B, stakeholders enter into contracts to transfer and shift liability among themselves. These agreements can take the form of indemnification (one party assuming some or all of the liability of another) or insurance (spreading risk over policyholders), among others. Further, indemnification agreements can be insured (not shown). In model C, a legislature exempts AI/ML partially or completely from the traditional liability system and the government takes over all or some of the risk. Often, these systems rely on taxes or fees on relevant stakeholders. These modifications do not exist in isolation. For instance, if the legislature enacts a program to shield stakeholders from most of the liability risk (model C), stakeholders could still purchase insurance on their residual risk (model B).