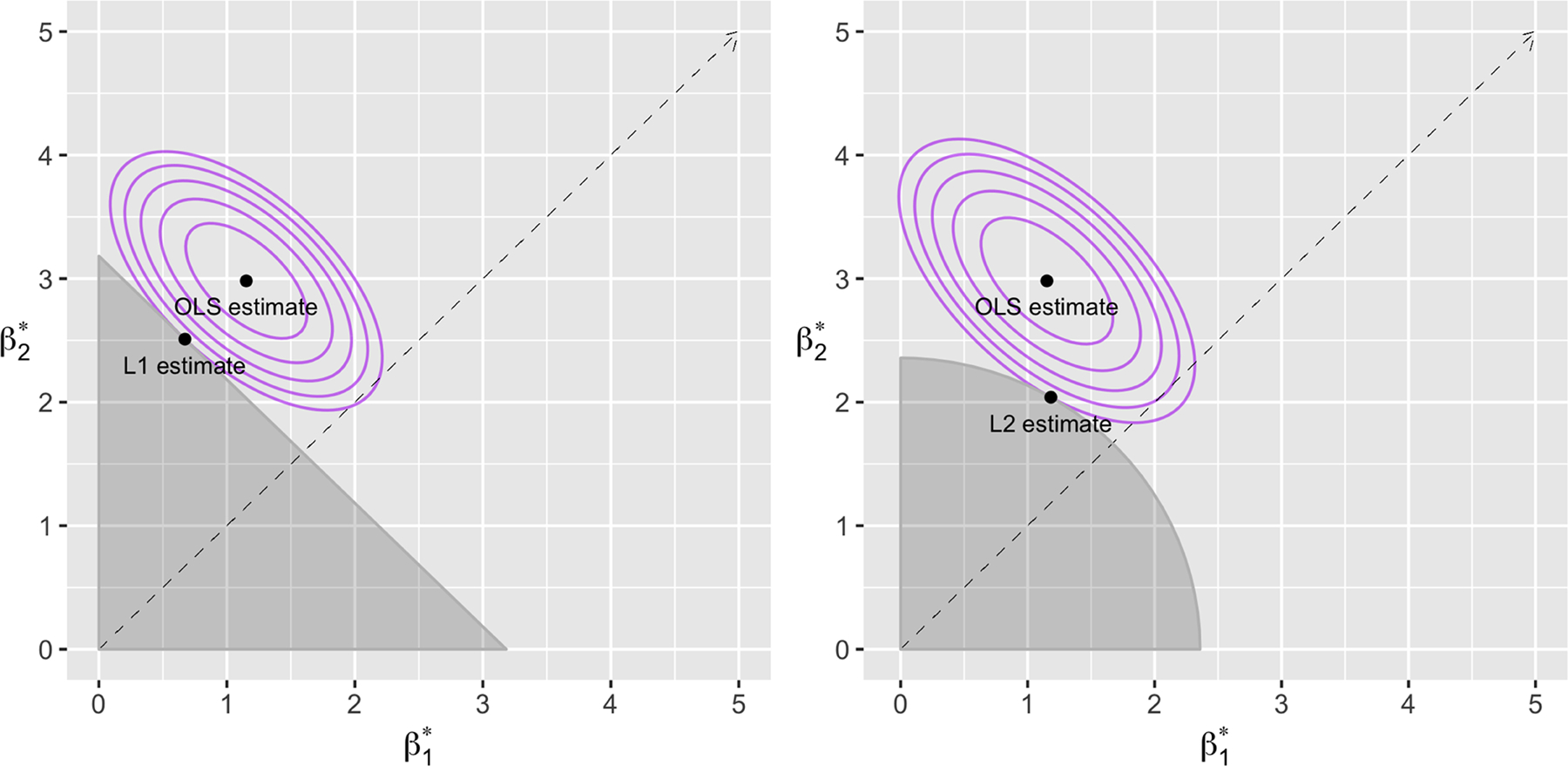

Figure 1.

Illustration of how the L2 penalty moves coefficients and therefore weights closer to equality, in a simulated setting with two positive coefficients for two positively correlated predictors. The intersection of the contours of the normal log likelihood with the shaded feasibility region for an L2-penalized regression with nonnegativity constraints (right) is closer to the dotted line of equality than the intersection with the L1 feasibility region (left). The ordinary least squares (OLS) estimator is also shown, as the minimizer of the log likelihood. Lambda was chosen by the one-standard-error rule.