Abstract

The costs required to provide acute care for patients with serious burn injuries are significant. In the United States, these costs are often shared by patients. However, the impacts of preinjury finances on health-related quality of life (HRQL) have been poorly characterized. We hypothesized that lower income and public payers would be associated with poorer HRQL. Burn survivors with complete data for preinjury personal income and payer status were extracted from the longitudinal Burn Model System National Database. HRQL outcomes were measured with VR-12 scores at 6, 12, and 24 months postinjury. VR-12 scores were evaluated using generalized linear models, adjusting for potential confounders (eg, age, sex, self-identified race, burn injury severity). About 453 participants had complete data for income and payer status. More than one third of BMS participants earned less than $25,000/year (36%), 24% earned $25,000 to 49,000/year, 23% earned $50,000 to 99,000/year, 11% earned $100,000 to 149,000/year, 3% earned $150,000 to 199,000/year, and 4% earned more than $200,000/year. VR-12 mental component summary (MCS) and physical component summary (PCS) scores were highest for those who earned $150,000 to 199,000/year (55.8 and 55.8) and lowest for those who earned less than $25,000/year (49.0 and 46.4). After adjusting for demographics, payer, and burn severity, 12-month MCS and PCS and 24-month PCS scores were negatively associated with Medicare payer (P < .05). Low income was not significantly associated with lower VR-12 scores. There was a peaking relationship between HRQL and middle-class income, but this trend was not significant after adjusting for covariates. Public payers, particularly Medicare, were independently associated with poorer HRQL. The findings might be used to identify those at risk of financial toxicity for targeting assistance during rehabilitation.

The care of severely injured burn patients is costly. Burn injuries often require intensive and prolonged critical care, which is inherently expensive due to nursing intensity, ventilatory support, and complications of critical injury. Surgical and perioperative care to facilitate wound closure is also costly. As patients heal, they require acute care for wound care and rehabilitation for weeks to months. In summary, the care of burn patients is one of the costliest of any traumatic injury.1,2

In addition to the high costs of burn care generally, healthcare costs in the United States are nearly twice that of other Organization of Economic Co-operation and Development nations.3 Healthcare financing in the United States is unique among high-income countries, whereby patients front a significant proportion of their healthcare costs.4 In disciplines such as oncology, the financial strain on patients resulting from their healthcare costs is known as financial toxicity.5 In some instances, the financial strain can be damaging to a patient’s psychological health and result in material consequences, including loss of income and personal property.6

Given the high costs of burn care and the U.S. healthcare financing model, burn survivors seemingly would suffer from financial toxicity like those suffering from other conditions.7 Financial toxicity among people living with burn injuries has not been closely examined. Furthermore, the relationship between preinjury finances and health-related quality of life (HRQL) of burn survivors has not been reported.

To address this gap in knowledge, we investigated the relationship between burn survivor finances (ie, personal income, health insurance payer) and HRQL. We hypothesized that lower income and public insurance payers would be associated with lower HRQL. The findings might be used to identify those at additional risk of unsatisfactory recovery and target multiple types of resources ranging from psychosocial support to financial assistance.

METHODS

Database and Inclusion

The Burn Model System (BMS) National Database8 is a multicenter, longitudinal database supported by the National Institute of Disability, Independent Living, and Rehabilitation Research (NIDILRR).9 Please living with burn injury are prospectively enrolled in the BMS study/database if they meet any of the following criteria:

18 to 64 years of age with a burn injury ≥20% total body surface area with surgical intervention;

≥65 years of age with a burn injury ≥10% total body surface area with surgical intervention;

≥18 years of age with a burn injury to their face/neck, hands, or feet with surgical intervention; or

≥18 years of age with a high-voltage electrical burn injury with surgical intervention.

The database follows participants longitudinally after hospital discharge and surveys participants at 6 ± 2, 12 ± 3, and 24 ± 6 months after injury from their index hospitalization.10 All adult participants (ie, aged ≥18 years) who reported data for annual income and payer were included. Annual income was added to the BMS survey in 2015. Income brackets were defined by NIDILRR at that time and continued through the study period. The exact annual income was not obtained in the study survey. Data were extracted to include a 24-month follow-up for participants enrolled from 2015 to 2018 (ie, through the end of 2020).

Variables

The primary outcome variable was Veterans RAND 12 (VR-12) score. This instrument was adopted by the BMS research consortium in 2015 given its relative ease of administration in combination with high validity and generalizability in burn survivors.9,11 The VR-12 is divided into two separate sections: physical component summary (PCS) and mental component summary (MCS) scores. The physical health component summary (PCS) score is comprised of four domains: general health, physical functioning, physical role, and bodily pain. The mental health component summary (MCS) score is comprised of the four domains: emotional role, vitality, mental health, and social functioning. For comparative purposes, the VR-12 mean for the general U.S. population is 50 with a standard deviation of 10.12 Higher scores suggest a better quality of life.

Covariables included in the multivariable model were those previously associated with HRQL,13 including demographics (eg, age, race/ethnicity, and sex) and burn severity (eg, number of operations during the index admission). The number of operations during the index hospitalization has been shown to be the more significant predictor of HRQL than traditional Baux score components (ie, burn size, inhalation injury).14,15 Payer status was determined at the time of participant discharge and included the following: commercial/private, Medicare, Medicaid, Workers’ Compensation, self-pay, and philanthropy. There was no category for “uninsured”; although, self-pay represented the cohort who did not have insurance at the time of discharge. When a participant was admitted without health insurance and subsequently obtained Medicaid coverage during hospitalization, that individual was classified as having Medicaid payer. Participant annual income was reported in six groupings: less than $25,000/year, $25,000 to 50,000/year, $51,000 to 99,000/year, $100,000 to 149,000/year, $150,000 to 199,000/year, and more than $200,000/year.

Multivariable generalized linear models were used to evaluate the association of VR-12 PCS and MCS scores with covariates at 6, 12, and 24 months postinjury.16 All covariables listed above were included a priori. For personal income, a comparison was made between the lowest income bracket and the other five brackets. For payer, commercial insurance was the reference case. For race/ethnicity, white non-Hispanic was the reference case. Gaussian distributions were used by default, while other distributions (eg, binomial, gamma) were compared for improved model fitness using an Akaike information coefficient (AIC).

Nonresponder analysis was conducted to determine whether the population of burn survivors who responded to the income survey question differed from those who did not. The response variable was whether income was reported (binary), and the explanatory variables included those listed above along with the BMS site as a cluster variable. Multilevel logistic regression was used. Statistical significance was determined at an alpha level of 0.05. All analyses were conducted with Stata/IC version 15.1 (StataCorp LLC).

RESULTS

Of 1013 potentially eligible burn survivors, 453 had complete data for income and payer (44.7%). One hundred sixty-four participants (36%) earned less than $25,000/year, 107 (24%) earned $25,000 to 49,000/year, 103 (23%) earned $50,000 to 99,000/year, 48 (11%) earned $100,000 to 149,000/year, 15 (3%) earned $150,000 to 199,000/year, and 16 (4%) earned more than $200,000/year. One hundred fifty-seven participants (35%) had commercial insurance, 80 (18%) had Medicare, 76 (17%) had Medicaid, 69 (15%) were self-pay, 60 (13%) had Workers’ Compensation, and 11 (2%) had other philanthropy.

The intersection of income and payer status demonstrated notable differences. The majority of participants who earned less than $25,000/year had either Medicare (27%) or Medicaid (30%) as payer, while only 19% of participants who earned over $200,000/year had a public payer (Table 1). The majority of participants in the top four income brackets had commercial insurance.

Table 1.

Income bracket and payer status of BMS participants 2015 to 2020

| <$25,000 (164) | $25,000–49,000 (107) | $50,000–99,000 (103) | $100,000–149,000 (48) | $150,000–199,000 (15) | <$199,000 (16) | |

|---|---|---|---|---|---|---|

| Medicare | 44 (27%) | 21 (20%) | 10 (10%) | 2 (4%) | 0 | 3 (19%) |

| Medicaid | 49 (30%) | 13 (12%) | 12 (12%) | 2 (4%) | 0 | 0 |

| Commercial | 23 (14%) | 30 (28%) | 51 (50%) | 30 (63%) | 11 (73%) | 12 (75%) |

| Workers’ Compensation | 8 (5%) | 19 (18%) | 19 (19%) | 11 (23%) | 2 (13%) | 1 (6%) |

| Self-pay | 35 (21%) | 21 (20%) | 9 (9%) | 3 (6%) | 1 (7%) | 0 |

| Philanthropy | 5 (3%) | 3 (3%) | 2 (2%) | 0 | 1 (7%) | 0 |

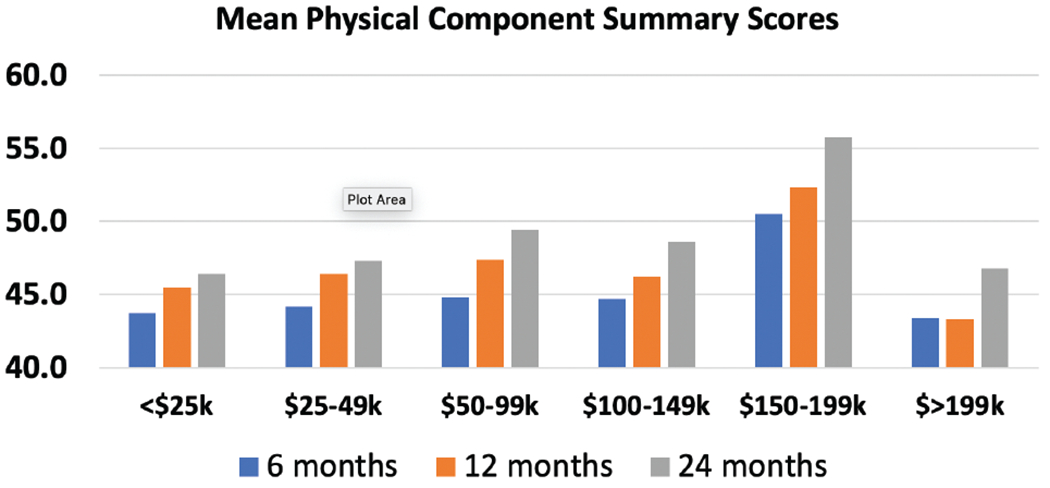

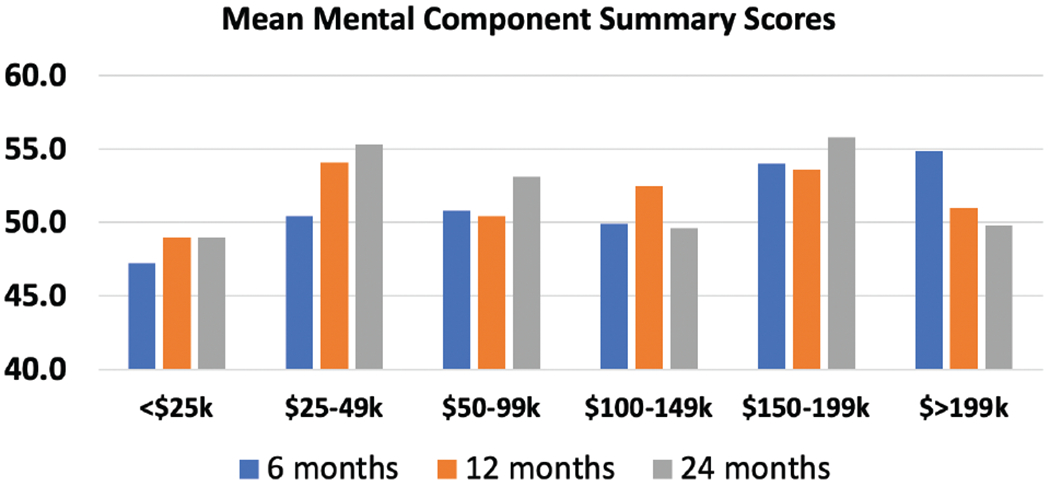

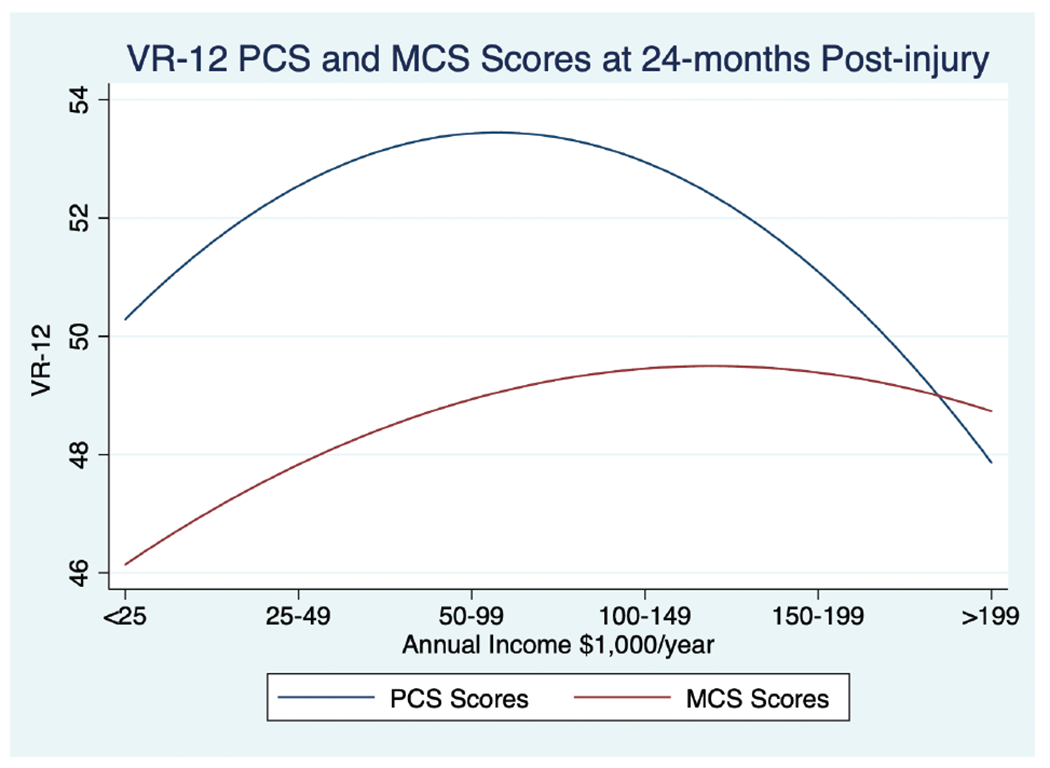

VR-12 PCS scores varied across income brackets, with a trend toward higher PCS scores at higher incomes (Figure 1). The lowest mean PCS scores at 24-month postinjury were in the group making less than $25,000/year (46.4), while the highest scores were from the group making between $150,000 and 199,000/year (55.8). A similar trend was found in mean VR-12 MCS scores, whereby the lowest mean scores at 24-month postop injury were in the group making less than $25,000/year (49.0), and the highest scores were in the group making between $150,000 and 199,000/year (55.8) (Figure 2). Applying the best fit function to VR-12 PCS and MCS scores at 24-month postinjury demonstrated a peak in PCS scores in the $50,000 to 100,000 interval, compared to a plateau in MCS scores around $100,000 to 150,000 (Figure 3).

Figure 1.

Mean VR-12 physical component summary scores stratified by income bracket. Scores were given at 6, 12, and 24 months postinjury. The population mean for PCS scores is 50.

Figure 2.

Mean VR-12 mental component summary scores stratified by income bracket. Scores were given at 6, 12, and 24 months postinjury. The population mean for MCS scores is 50.

Figure 3.

Fitted polynomial function for VR-12 PCS and MCS scores at 24-month postinjury. Trend demonstrates a peaking effect for PCS scores at $50,000 to 100,000/year, compared to a plateau effect for MCS scores starting at $100,000/year.

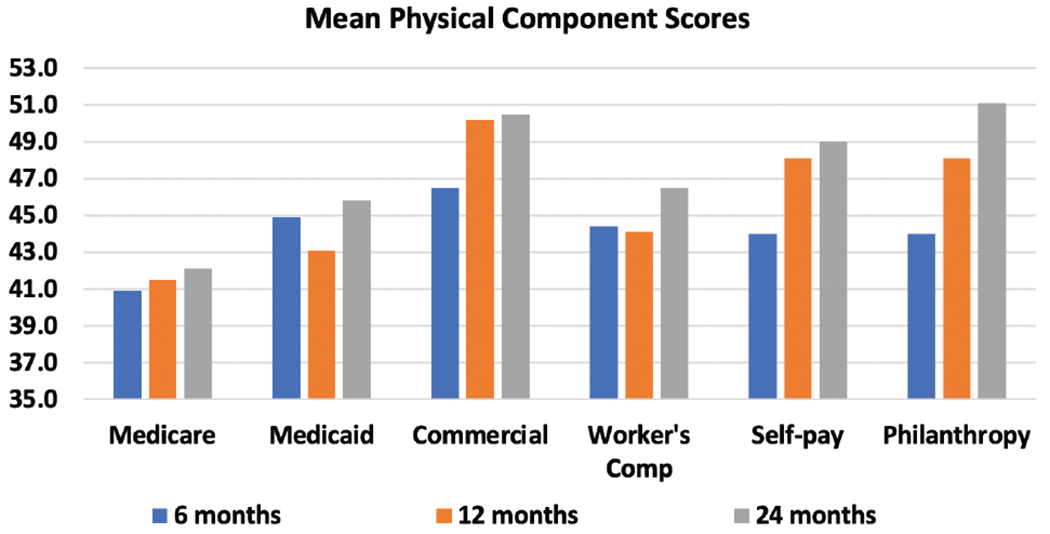

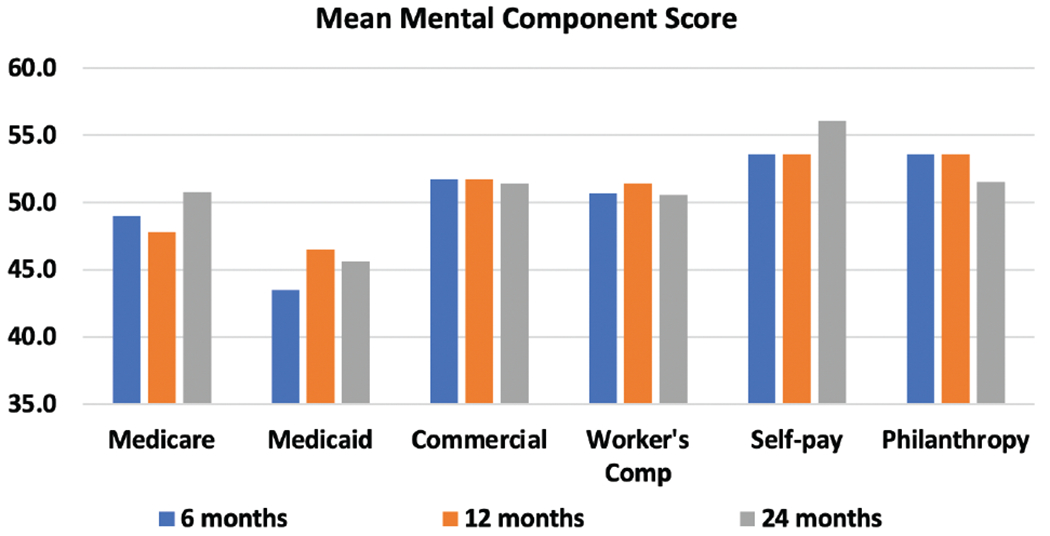

VR-12 scores also varied by payer status. Mean PCS scores were lowest for participants with Medicare payer at 6 (40.0), 12 (41.5), and 24 (42.1) months postinjury (Figure 4). Participants with commercial insurance and philanthropy had higher scores across all postinjury intervals. At 24-month postinjury, mean PCS scores were 50.5 for commercial insurance and 51.1 for philanthropy. Mean MCS scores showed a different pattern, whereby the lowest scores were found in participants with Medicaid payer across all follow-up intervals (Figure 5). The highest scores were reported from the self-pay cohort with a peak at 24-month postinjury of 56.1.

Figure 4.

Mean VR-12 physical component summary scores by the payer. Scores were given at 6, 12, and 24 months postinjury. The population mean for PCS scores is 50.

Figure 5.

Mean VR-12 mental component summary scores by the payer. Scores were given at 6, 12, and 24 months postinjury. The population mean for PCS scores is 50.

Multivariable analysis demonstrated no significant association between income and MCS scores at any follow-up interval. However, public payers were associated with lower MCS scores at 6 months (Medicaid coefficient [coef] −7.95, 95% CI −12.76 to −3.15, P < .001) and 12 months (12-month Medicare coef −5.80, 95% CI −10.69 to −0.90, P = .020) postinjury (Table 2). There was no significant association with low income and PCS scores at any follow-up interval; however, public payers were associated with lower PCS scores (Table 3). At 12-month postinjury, PCS scores were negatively associated Medicare (coef −9.87, 95% CI −14.13 to −5.60, P < .001) and Medicaid (coef −4.57, 95% CI −8.94 to −0.19, P = .041). PCS scores were also negatively associated with Medicare payer at 24-month postinjury (coef −6.42, 95% CI −11.73 to −1.11, P = .018). PCS scores were negatively associated with Workers’ Compensation at 6-month (coef −4.40, 95% CI −7.88 to −0.93, P = .013) and 12-month (coef −4.79, 95% CI −8.95 to −0.63, P = .024) postinjury. Aside from payer, notable covariables associated with lower MCS and PCS scores included black non-Hispanic race/ethnicity, older age, and higher number of operations at index admission. Hispanic ethnicity was associated with higher MCS scores at 6 and 24 months postinjury. Model sensitivity analysis was conducted using available distribution families (eg, Gaussian, inverse Gaussian, and gamma). Gaussian distributions yielded the lowest AIC.

Table 2.

Multivariable analysis evaluating VR-12 MCS scores at postinjury intervals

| Coefficient | 95% Confidence Interval | P | |

|---|---|---|---|

| MCS 6 months | |||

| Age | 0.02 | −0.09 to 0.13 | .727 |

| Male sex | 3.33 | 0.01 to 6.65 | .049 |

| Number of operations at index admission | −0.79 | −1.32 to −0.27 | .003 |

| Medicare | −4.30 | −9.41 to 0.80 | .098 |

| Medicaid | −7.95 | −12.76 to −3.15 | .001 |

| Workers’ Compensation | −0.87 | −5.28 to 3.53 | .697 |

| Self-pay | 1.63 | −2.89 to 6.16 | .479 |

| Philanthropy | 1.71 | −23.67 to 27.08 | .895 |

| Non-Hispanic black | −1.28 | −6.42 to 3.86 | .625 |

| Hispanic | 5.22 | 1.29 to 9.14 | .009 |

| Lowest income bracket | −1.75 | −5.27 to 1.77 | .330 |

| MCS 12 months | |||

| Age | 0.12 | 0.01 to 0.23 | .032 |

| Male sex | 5.76 | 2.43 to 9.08 | .001 |

| Number of operations at index admission | −0.42 | −0.90 to 0.05 | .079 |

| Medicare | −5.80 | −10.69 to −0.90 | .020 |

| Medicaid | −1.35 | −6.37 to 3.67 | .598 |

| Workers’ Compensation | −0.07 | −4.85 to 4.70 | .976 |

| Self-pay | 1.70 | −2.65 to 6.06 | .443 |

| Philanthropy | 8.96 | −14.27 to 32.19 | .450 |

| Non-Hispanic black | 5.02 | 1.19 to 8.84 | .010 |

| Hispanic | −2.56 | −6.09 to 0.97 | .155 |

| Lowest income bracket | −2.26 | −5.75 to 1.24 | .206 |

| MCS 24 months | |||

| Age | −0.04 | −0.19 to 0.11 | .630 |

| Male sex | 4.05 | −0.45 to 8.54 | .078 |

| Number of operations at index admission | −0.26 | −0.74 to 0.21 | .282 |

| Medicare | −1.09 | −7.64 to 5.47 | .745 |

| Medicaid | −6.44 | −15.67 to 2.79 | .172 |

| Workers’ Compensation | 1.85 | −4.18 to 7.89 | .547 |

| Self-pay | 4.17 | −1.56 to 9.90 | .153 |

| Philanthropy | −0.44 | −25.21 to 24.32 | .972 |

| Non-Hispanic black | 6.63 | −0.76 to 14.02 | .079 |

| Hispanic | 6.10 | 0.84 to 11.37 | .023 |

| Lowest income bracket | −3.12 | −8.18 to 1.93 | .226 |

MCS, mental component summary.

Table 3.

Multivariable analysis evaluating VR-12 PCS scores at postinjury intervals

| Coefficient | 95% Confidence Interval | P | |

|---|---|---|---|

| PCS 6 months | |||

| Age | −0.15 | −0.24 to −0.06 | .001 |

| Male sex | 0.57 | −2.05 to 3.19 | .670 |

| Number of operation index admission | −1.23 | −1.65 to −0.82 | <.001 |

| Medicare | −2.74 | −6.77 to 1.29 | .183 |

| Medicaid | −1.38 | −5.17 to 2.41 | .474 |

| Workers’ Compensation | −4.40 | −7.88 to −0.93 | .013 |

| Self-pay | −3.82 | −7.39 to −0.26 | .036 |

| Philanthropy | 2.18 | −17.85 to 22.21 | .831 |

| Black non-Hispanic | −1.47 | −5.57 to 2.63 | .482 |

| Hispanic | 1.04 | −2.09 to 4.17 | .515 |

| Lowest income bracket | −0.36 | −3.14 to 2.42 | .799 |

| PCS 12 months | |||

| Age | −0.09 | −0.19 to 0.01 | .053 |

| Male sex | −0.31 | −3.21 to 2.59 | .833 |

| Number of operation index admission | −1.33 | −1.75 to −0.92 | <.001 |

| Medicare | −9.87 | −14.13 to −5.60 | <.001 |

| Medicaid | −4.57 | −8.94 to −0.19 | .041 |

| Workers’ Compensation | −4.79 | −8.95 to −0.63 | .024 |

| Self-pay | −3.58 | −7.37 to 0.21 | .064 |

| Philanthropy | 0.96 | −19.29 to 21.21 | .926 |

| Black non-Hispanic | −3.33 | −7.93 to 1.27 | .156 |

| Hispanic | 3.25 | −0.08 to 6.58 | .056 |

| Lowest income bracket | 0.16 | −2.89 to 3.21 | .917 |

| PCS 24 months | |||

| Age | −0.12 | −0.24 to −0.99 | .046 |

| Male sex | −0.91 | −4.55 to 2.73 | .624 |

| Number of operation index admission | −0.48 | −0.86 to −0.09 | .015 |

| Medicare | −6.42 | −11.73 to −1.11 | .018 |

| Medicaid | 0.03 | −7.45 to 7.50 | .994 |

| Workers’ Compensation | −1.05 | −5.94 to −3.84 | .674 |

| Self-pay | −2.54 | −7.18 to 2.10 | .283 |

| Philanthropy | −5.39 | −25.45 to 14.66 | .598 |

| Black non-Hispanic | −8.11 | −14.08 to −2.14 | .008 |

| Hispanic | −2.53 | −6.79 to 1.73 | .244 |

| Lowest income bracket | −0.77 | −4.86 to 3.33 | .714 |

PCS, physical component summary.

Nonresponder analysis demonstrated that those who completed the survey question for income were more likely to be older with an odds ratio of 1.04 (95% CI 1.03 to 1.05, P < .001) and of Hispanic ethnicity (OR 1.78, 95% CI 1.15 to 2.75, P = .009). Those with Medicare, Medicaid, and philanthropy payers were significantly less likely to respond to the income question compared to commercially insured participants (Table 4).

Table 4.

Multivariable analysis evaluating predictors of response to income status

| Odds Ratio With 95% CI | P | |

|---|---|---|

| Age | 1.04 (1.03–1.05) | <.001 |

| Male sex | 1.13 (0.81–1.56) | .468 |

| Race/ethnicity | ||

| White non-Hispanic | Reference | |

| Black non-Hispanic | 1.04 (0.64–1.69) | .869 |

| Hispanic | 1.78 (1.15–2.75) | .009 |

| Payer | ||

| Commercial | Reference | |

| Medicare | 0.42 (0.26–0.68) | <.001 |

| Medicaid | 0.50 (0.34–0.74) | <.001 |

| Workers’ Compensation | 1.33 (0.78–2.25) | .290 |

| Self-pay | 1.37 (0.82–2.29) | .227 |

| Philanthropy | 0.01 (0.01–0.08) | <.001 |

| Number of operations at index hospitalization | 1.00 (0.99–1.01) | .794 |

DISCUSSION

This study provides the most granular data to date regarding the income background of burn survivors. The single largest cohort of burn survivors (36%) by income came from the lowest income bracket (<$25,000/year), while wealthier participants (ie, making over $99,000/year) comprised less than 20% of the total study population. According to reports by the Federal Reserve System,17 30% of Americans make under $25,000/year; therefore, the poorer burn survivor population is over-represented by 6% in the BMS database. Comparing to the higher-income brackets, 7% of Americans make over $150,000/year, which is the exact same percentage in this study. Middle-class incomes (ie, between $25,000 and 150,000) represent 63% of Americans according to the Federal Reserve System compared to 58% in this study. Thus, middle-class Americans are less commonly burned compared to the poor, whereas wealthy Americans are burned in equal proportion to the general population.

PCS scores increased in a curvilinear fashion from the lowest income bracket to the bracket making between $100,000 and 149,000/year. PCS scores were lower in the highest income bracket, such that mean scores for those participants making more than $200,000/year were similar to PCS scores for those making less than $25,000/year. Contemporary investigations into income and happiness as measured by the Gallup World Poll18 have found a similar association to what we found in this study and termed this phenomenon income satiation. Specifically, happiness peaks at an annual income of around $95,000/year (based on 2018 currencies) and declines at higher income levels. Although the VR-12 was not designed to measure happiness, it does measure quality of life, which is associated with happiness.19 Burn survivors seem to experience a similar pattern as the general population, whereby their global quality of life is, in part, reflective of personal income. Despite the trends in income and HRQL, low income as a unique covariable among other potential confounders did not demonstrate a significant relationship. This suggests that while income is an important marker of HRQL after burn injury, it should be used in conjunction with other important covariables to determine which patients are at risk for lower HRQL and in greater need of support during recovery.

Participants with Medicare as primary payer had significantly lower PCS and MCS scores at multiple postinjury intervals even when adjusted for age. As the primary payer for Americans 65 years of age and older, age could factor into why these participants reported worse HRQL. Prior investigations have demonstrated a notable relationship between advancing age and poorer physical function and vitality.20 Our analysis included age as a covariate, so the significant relationship between VR-12 scores and Medicare is more complex than simply age as a number. The effects of older age may not be adequately reflected with age as a continuous variable (eg, 50-year-old burn survivors may fair no worse than 40-year-old burn survivors), and frailty (ie, advanced age) might be a more important factor that is captured with Medicare payer status.21 In terms of risk of collinearity in analyzing age and Medicare as covariables, our analysis avoided this problem by analyzing age as a continuous variable (compared to creating age categories such as >65 years). As a continuous variable, there are sufficient differences in age and Medicare to avoid this problem. In addition, the payer listed in BMS is the primary payer. Some participants who are Medicare eligible choose to purchase a supplement or managed health plan. In instances where the health plan is managed by a commercial insurer, the participants will be listed as having commercial insurance given only the primary payer is listed in BMS.

Medicaid was also associated with lower MCS and PCS scores. Implicitly, burn survivors with commercial insurance are typically employed in higher-paying jobs or beneficiaries of someone who is employed, given that employment is the primary means of securing health insurance in the United States.22 About 40% of Medicaid recipients are unemployed.23 Employment may signal better financial health and sustainability that is otherwise not captured by income. Prior studies have in fact demonstrated that employment is an independent predictor of higher HRQL in burn survivors.24 This is particularly salient given that participants had Medicaid across the lower three income brackets and was not just seen in those making less than $25,000/year.

The self-pay cohort constituted 15% of participants, and most of these individuals were in the lowest two income brackets. The Affordable Care Act (ACA) was passed in 2010 and implemented in participating states by 201425; thus, our study occurs postimplementation. Nationally, uninsured rates have fallen to 7 to 12% since the ACA, largely due to Medicaid expansion.26 Juxtaposed to our cohort, the uninsured/self-pay rate in our study is higher. The likely explanation for this finding stems from the sites included in the study. Specifically, Texas has not expanded Medicaid to the extent of other states, and one of the main contributing facilities within BMS is in Texas. Given there may be differences between states in their payer candidacy and outcomes, we included facility as a clustering variable, and our regressions were all multilevel to take this into consideration.

Whereas payer and personal income act as proxies for a burn survivor’s financial situation and stress, neither directly reflect potential financial toxicity. A survivor of a 50% TBSA burn with Medicaid payer status and personal income of $25,000/year may accrue hospital changes well in excess of $500,000 after multiple operations and months of inpatient stay. After Medicaid payment, safety-net hospitals, many of which house burn centers, often pursue no additional patient payment. For that scenario, the patient has no financial obligation for his/her burn care despite seemingly high risk of financial toxicity. Alternatively, a burn survivor of a 3% TBSA upper extremity burn with commercial insurance and personal income of $50,000/year could have a $2000 copay and owe an additional $3000 for an episode of care which could generate significant financial toxicity despite ostensibly stable baseline finances. The current investigation could not evaluate out-of-pocket expenses for burn survivors, given that these data are not present within the BMS database. Institutional studies could assess the direct cost of care to patients, particularly looking for opportunities to bend the cost curve toward lower patient expenses without compromising care.

Drawing upon the oncology literature,6 opportunities to reduce financial toxicity include 1) acknowledging financial burden when discussing variable treatment options such as wound care (eg, if a patient has to pay out of pocket for dressings discuss differences between expensive silver dressings and cheaper generic topical ointments), 2) providing patients with financial counseling when available, 3) providing patients with best estimates of out-of-pocket expenses related to surgery, particularly if surgery can be performed outpatient, and 4) using choosing-wisely Canada and American Burn Association guidelines for testing and inpatient care.27 Recently, some28 have advocated for crowd-sourced funding as a means to supplemental medical costs.

Limitations

VR-12 was designed to measure quality of life for medical29 and surgical conditions,30 including health states in postburn survivors.13,15 VR-12 was not designed to evaluate the effects of financial toxicity. Other investigations into financial toxicity outside of burn31 have specifically employed instruments such as the Comprehensive Score for Financial Toxicity to measure financial stress. Therefore, VR-12 is likely not as sensitive in detecting adverse effects of financial toxicity, particularly if the stress does not lead to disturbances within the domains of the PCS or MCS. That said, if financial toxicity were severe enough, it would plausibly affect more generic markers of HRQL, such as those captured in the VR-12. Another limitation of our study was the inability to adjust regression coefficients for medical comorbidities. BMS does not contain complete comorbidity data, unfortunately. In a prior investigation that merged BMS outcomes data with single-institution comorbidity information,15 VR-12 scores were negatively associated with conditions such as diabetes and mental health disorders. Plausibly, there may be an association between comorbidities and income level and/or payer which would confound our results.

The BMS dataset is contextual to the burn centers it represents which may not be indicative of the experiences of burn survivors across the entire United States, although data suggest that BMS does reflect the National Burn Repository.32 This study also demonstrated response bias, such that responders to the income question were more likely to be older and of Hispanic ethnicity. In addition, responders were less likely to have a public payer. Possibly, participants of lower income were uncomfortable answering the income question; therefore, the results may not speak for all low-income burn survivors. That said, over a third of respondents had Medicaid payer, which represented the largest proportion of any group. Additionally, income brackets within the BMS dataset do not exactly correlate with federal brackets, which limits comparisons to other investigations that use federal income brackets.

CONCLUSION

HRQL was highest for burn survivors earning between $150,000 and 199,000/year. Participants who earned less than $25,000/year had the lowest VR-12 scores and particularly MCS scores. On multivariable analysis, most of the differences in HRQL associated with preinjury income were explained by differences in payer and burn severity factors. Particularly, public payers Medicare and Medicaid were independently associated with poorer VR-12 scores at multiple postinjury intervals. Providers should gain insight into their patient’s socioeconomic status, financial burdens, and their effects on HRQL as they determinate acute treatments and coordinate recovery services. Opportunities to reduce the impacts of financial toxicity include informed treatment decisions, limiting low-value care, retroactive insurance registration, financial recovery counseling, and crowdsource funding.

Funding:

The contents of this manuscript were developed under a grant from the National Institute on Disability, Independent Living, and Rehabilitation Research (90DPBU001, 90DPBU003, and 90DPBU0004). NIDILRR is a center within the Administration for Community Living (ACL), Department of Health and Human Services (HHS). The contents of this manuscript do not necessarily represent the policy of NIDILRR, ACL, HHS, and you should not assume endorsement by the Federal Government.

Footnotes

Disclosures: The authors report no conflicts of interest or financial disclosures related to this manuscript.

REFERENCES

- 1.Ahn CS, Maitz PK. The true cost of burn. Burns 2012;38:967–74. [DOI] [PubMed] [Google Scholar]

- 2.Hop MJ, Polinder S, van der Vlies CH, Middelkoop E, van Baar ME. Costs of burn care: a systematic review. Wound Repair Regen 2014;22:436–50. [DOI] [PubMed] [Google Scholar]

- 3.Papanicolas I, Woskie LR, Jha AK. Health care spending in the United States and other high-income countries. JAMA 2018;319:1024–39. [DOI] [PubMed] [Google Scholar]

- 4.Dieleman JL, Cao J, Chapin A et al. US health care spending by payer and health condition, 1996–2016. JAMA 2020;323:863–84. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Zafar SY, Abernethy AP. Financial toxicity, Part I: a new name for a growing problem. Oncology (Williston Park) 2013;27:80–1, 149. [PMC free article] [PubMed] [Google Scholar]

- 6.Lentz R, Benson AB 3rd, Kircher S. Financial toxicity in cancer care: prevalence, causes, consequences, and reduction strategies. J Surg Oncol 2019;120:85–92 [DOI] [PubMed] [Google Scholar]

- 7.Zhu Z, Xing W, Zhang X, Hu Y, So WKW. Cancer survivors’ experiences with financial toxicity: a systematic review and meta-synthesis of qualitative studies. Psychooncology 2020;29:945–59. [DOI] [PubMed] [Google Scholar]

- 8.Goverman J, Mathews K, Holavanahalli RK et al. The National Institute on Disability, Independent Living, and Rehabilitation research burn model system: twenty years of contributions to clinical service and research. J Burn Care Res 2017;38:e240–53. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9.Amtmann D, McMullen K, Bamer A et al. National Institute on disability, independent living, and rehabilitation research burn model system: review of program and database. Arch Phys Med Rehabil 2020;101:S5–15. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Burn Model Systems—guidelines for collection of follow-up data 2015; available from http://burndata.washington.edu/sites/burndata/files/files/105BMS%20-%20Guidelines%20for%20Collection%20of%20Follow-up%20Data2015-12-21.pdf; accessed 23 Apr. 2019.

- 11.Selim AJ, Rogers W, Fleishman JA et al. Updated U.S. population standard for the Veterans RAND 12-item Health Survey (VR-12). Qual Life Res 2009;18:43–52. [DOI] [PubMed] [Google Scholar]

- 12.Spiro A, Rogers WH, Qian S, Kazis LE. Imputing physical and mental summary scores (PCS and MCS) for the Veterans SF-12 Health Survey in the context of missing data. Baltimore CMS; 2004. [Google Scholar]

- 13.Sheckter CC, Carrougher GJ, McMullen K et al. Evaluation of patient-reported outcomes in burn survivors undergoing reconstructive surgery in the rehabilitative period. Plast Reconstr Surg 2020;146:171–82. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Stewart BT, Carrougher GJ, Curtis E et al. Mortality prognostication scores do not predict long-term, health-related quality of life after burn: a Burn Model System National Database study. Burns 2021;47:42–51. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Sheckter CC, Li K, Carrougher GJ, Pham TN, Gibran NS, Stewart BT. The impact of comorbid conditions on long-term patient-reported outcomes from burn survivors. J Burn Care Res 2020;41:956–62. [DOI] [PubMed] [Google Scholar]

- 16.Kaufman RL. Interaction effects in linear and generalized linear models: examples and applications using Stata. Thousand Oaks, CA: SAGE Publications; 2018. p. 609. [Google Scholar]

- 17.FRB: income and savings, report on the economic well-being of U.S. households in 2015; available from https://www.federalreserve.gov/econresdata/2016-economic-well-being-of-us-households-in-2015-Income-and-Savings.htmv; accessed 27 Feb. 2021.

- 18.Jebb AT, Tay L, Diener E, Oishi S. Happiness, income satiation and turning points around the world. Nat Hum Behav 2018;2:33–8. [DOI] [PubMed] [Google Scholar]

- 19.Medvedev ON, Landhuis CE. Exploring constructs of well-being, happiness and quality of life. PeerJ 2018;6:e4903. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Edgar DW, Homer L, Phillips M, Gurfinkel R, Rea S, Wood FM. The influence of advancing age on quality of life and rate of recovery after treatment for burn. Burns 2013;39:1067–72. [DOI] [PubMed] [Google Scholar]

- 21.Wasiak J, Lee SJ, Paul E et al. Predictors of health status and health-related quality of life 12 months after severe burn. Burns 2014;40:568–74. [DOI] [PubMed] [Google Scholar]

- 22.Enthoven AC, Fuchs VR. Employment-based health insurance: past, present, and future. Health Aff (Millwood) 2006;25:1538–47. [DOI] [PubMed] [Google Scholar]

- 23.Work among Medicaid adults: implications of economic downturn and work requirements. KFF; 2021; available from https://www.kff.org/coronavirus-covid-19/issue-brief/work-among-medicaid-adults-implications-of-economic-downturn-and-work-requirements/; accessed 27 Feb. 2021. [Google Scholar]

- 24.Mason ST, Esselman P, Fraser R, Schomer K, Truitt A, Johnson K. Return to work after burn injury: a systematic review. J Burn Care Res 2012;33:101–9. [DOI] [PubMed] [Google Scholar]

- 25.Courtemanche C, Marton J, Yelowitz A. Who gained insurance coverage in 2014, the first year of full ACA implementation? Health Econ 2016;25:778–84. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26.Garfield R, Damico A, Orgera K. The coverage gap: uninsured poor adults in states that do not expand Medicaid. Peterson KFF-Health System Tracker. Disponfvel em:. Acesso em; 2020:29. [Google Scholar]

- 27.Eleven things physicians and patients should question in burn care. Choosing Wisely Canada; available from https://choosingwiselycanada.org/burns/; accessed 27 Feb. 2021. [Google Scholar]

- 28.Zafar SY. Crowdfunded Cancer Care—a reflection on health care delivery in the US. JAMA Netw Open 2020;3:e2027191. [DOI] [PubMed] [Google Scholar]

- 29.Singh A, Gnanalingham K, Casey A, Crockard A. Quality of life assessment using the Short Form-12 (SF-12) questionnaire in patients with cervical spondylotic myelopathy: comparison with SF-36. Spine (Phila PA 1976) 2006;31:639–43. [DOI] [PubMed] [Google Scholar]

- 30.Donovan JL, Hamdy FC, Lane JA et al. ; ProtecT Study Group*. Patient-reported outcomes after monitoring, surgery, or radiotherapy for prostate cancer. N Engl J Med 2016;375:1425–37. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.de Souza JA, Yap BJ, Wroblewski K et al. Measuring financial toxicity as a clinically relevant patient-reported outcome: the validation of the COmprehensive Score for financial Toxicity (COST). Cancer 2017;123:476–84. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Lezotte DC, Hills RA, Heltshe SL et al. Assets and liabilities of the burn model system data model: a comparison with the National Burn Registry. Arch Phys Med Rehabil 2007;88:S7–17. [DOI] [PubMed] [Google Scholar]