Abstract

BACKGROUND:

In recent years, value assessment frameworks have been introduced to inform discussions about how to define and assess value in the U.S. health care system. However, there is uncertainty as to how value assessment frameworks and other approaches to achieve value such as outcomes-based contracting are perceived and used in coverage decisions.

OBJECTIVE:

To understand how U.S. payers determine value in the use of pharmaceuticals and how it differs from payers outside the United States.

METHODS:

Qualitative in-depth phone interviews with 13 executive-level public and private U.S. managed care representatives and 6 health technology assessment advisors outside the United States were conducted from September to November 2017.

RESULTS:

Despite various mechanisms used by U.S. payers to assess value, no consistent definitions of value were provided, and U.S. payers felt limited in what they can do to achieve value in pharmaceutical decision making. Value assessment frameworks are not formally considered in formulary and reimbursement decisions but are used as a reference as they become available by most or all U.S. health plans. U.S. payers expressed concerns, including limited control over pharmaceutical pricing and budget caps, and limited ability to use incremental cost per quality-adjusted life-year thresholds. Outcomes-based contracting could have some utility in specific cases where the treatment has a particularly high cost and a clear outcomes measure, but payers indicated that outcomes-based contracts can be difficult to operationalize, and determination of savings was uncertain. Payers outside the United States—who are enabled by government health care bodies, policy tools, and analytical frameworks that have no counterpart in the United States—have a wider array of instruments at their disposal. U.S. payers were largely open to learning from other health care systems outside the United States, particularly the German health care system, where patient-relevant benefit compared with a predetermined treatment comparator is the primary determinant for price negotiations.

CONCLUSIONS:

Although there is interest in including value assessment frameworks during the decision-making process in the United States, there are significant challenges to operationalizing them. The current environment in the United States restricts payers’ ability to make favorable contracts with manufacturers, and changes to the U.S. health system design are needed to facilitate this effort. Adoption of a value assessment framework in Medicare or Medicaid would accelerate adoption of these tools by private payers in the United States.

What is already known about this subject

Health care costs have been rising over recent decades and are likely to increase in the future.

Recently introduced value assessment frameworks are used to inform discussions about how to define and assess value in the U.S. health care system but have varying degrees of rigor, transparency, and perspective.

What this study adds

No consistent definitions of value were provided by U.S. payers interviewed for this study, although U.S. payers reported using value assessment frameworks as a reference as they become available.

U.S. payers felt limited in what they can do to achieve value in pharmaceutical decision making; adoption of value assessment frameworks by Medicare or Medicaid would accelerate use by private payers in the United States.

U.S. payers reported that they were largely open to learning from other health care systems outside the United States, where government-enabled health care bodies have more tools at their disposal for achieving value.

In the past decade, a rising trend has been observed in the approval of new molecular entities, including personalized medicines for both small-molecule drugs and therapeutic biologics.1,2 At the same time, health care spending has been increasing because of a variety of factors, including an aging population, higher prices for health care services, higher prices for new products, and increased volume.3 In the United States, the Centers for Medicare & Medicaid Services (CMS) projects that spending on prescription medicines will increase faster than other health care goods and services between 2017 and 2026.4 This has resulted in a debate about the value and affordability of new interventions and how to measure these 2 economic outcomes given the limited evidence available when decisions are made about the use of these interventions in the health care system.5

Value assessment frameworks inform discussions about how to define and assess value at various levels of the U.S. health care system.6 Value assessment frameworks can differ in the way in which they define components of value (e.g., efficacy, toxicity, quality of life) and may be either quantitative or qualitative in their approach to assessment.7 In recent years, several organizations have introduced value assessment frameworks to inform discussions about how to define and assess value in the U.S. health care system. These value assessment frameworks have varying degrees of rigor, transparency, and perspective. Cancer-specific frameworks are available, such as assessments from the American Society of Clinical Oncology (ASCO) and the National Comprehensive Cancer Network (NCCN), both of which take the perspective of shared decision making between the physician and patient.8,9 The Memorial Sloan Kettering Cancer Center assessment takes the perspective of the physician and policymaker.10,11 Frameworks with a broader purview, including all therapeutic areas and all types of health care interventions, are also available, such as those from the Institute for Clinical and Economic Review (ICER) and the International Society for Pharmacoeconomics and Outcomes Research (ISPOR), which consider the payer perspective.6,12-19 According to a recent report by ISPOR, the core dimensions of value assessment frameworks encompass net value and quality-adjusted life-years (QALYs) gained. Productivity and adherence-improving factors represent common dimensions that are used inconsistently across various value frameworks. Other novel dimensions for value assessment frameworks, which may be used depending on the disease type or the attributes of the intervention, include reduction in uncertainty because of a new diagnostic, fear of contagion, risk of contagion, insurance value, disease severity, value of hope, real option value, equity, and scientific spillovers.15

Several of these value frameworks include a consideration of cost-effectiveness analyses and comparative-effectiveness research for a new intervention, as these analyses are increasingly relevant to U.S. health care decision makers seeking to ensure efficient use of new treatments.13,18,20,21 Cost-effectiveness analyses are valuations of costs where the single effect of interest, common to both alternatives but achieved to different degrees, is assessed using natural units (e.g., life-years gained, disability days).22 According to Sox and Greenfield (2009), comparative-effectiveness research is defined as, “the generation and synthesis of evidence that compares the benefits and harms of alternative methods to prevent, diagnose, treat and monitor a clinical condition, or to improve the delivery of care. The purpose of [comparative-effectiveness research] is to assist consumers, clinicians, purchasers, and policy makers to make informed decisions that will improve health care at both the individual and population levels.”23

To gain a complete understanding of a product’s benefits and risks, data beyond the randomized controlled trial may be reviewed and evaluated, as stated in the WellPoint guidance on comparative effectiveness in formulary decision making.24 However, evidence of the effectiveness of these health care interventions as used in clinical practice is suboptimal, in part because efficacy determined through randomized controlled trials may differ from effectiveness in clinical populations and conditions.25,26 One approach some pharmaceutical manufacturers and payers have used to address uncertainty about the real-world outcomes of a new intervention is outcomes-based contracts, in which medicine rebates or discounts are tied to a specified outcome in the target population.27

Payers in the United States considering whether to add a new pharmaceutical product to their formulary and determining appropriate utilization management tools, such as prior authorization, copays, and coinsurance, may benefit from comparative-effectiveness evidence as well as data from clinical trials and economic analyses to help them understand the value of a new medicine in clinical practice.28 In this study, we conducted structured interviews with U.S.-based payers to understand the current landscape for assessing and achieving value in the use of pharmaceuticals. The findings were compared with those outside the United States using structured interviews with health technology assessment (HTA) advisors from Australia, Canada, France, Germany, Italy, and the United Kingdom.

Methods

Background information on value frameworks was gathered via desk research, and discussion guide materials were developed accordingly. No formal search strategy was adopted in this study; instead, several keywords (e.g., value assessment frameworks) were adopted for use in widely recognized search engines (e.g., PubMed, Google) to search for relevant studies and reviews. From these results, further sources were identified based on their list of references. Discussion guide materials consisting of a list of discussion questions and preread materials were sent to interview participants before the interviews were conducted (see www.rtihs.org/USGuide and www.rtihs.org/GlobalGuide). Structured interviews were completed with 13 senior- and executive-level public and private decision makers with pharmacy and therapeutics (P&T) committee chair responsibilities and were representative of various geographic regions in the United States (8 medical directors, 5 U.S. pharmacy directors). Medical director clinical specialties included pediatrics, internal medicine, geriatrics, obstetrics and gynecology, anesthesiology, allergy and pulmonology, and urology.

In addition to the interviews with the U.S. representatives, country-specific adaptations were made to the discussion guide, and interviews were conducted with a total of 6 HTA advisors from Australia, Canada, France, Germany, Italy, and the United Kingdom. HTA advisors were defined as a current or ex-HTA committee member or an individual with a medical or economic background who is fully aware of the HTA requirements or advises HTA bodies for the approval of new treatments. The interviews were conducted to compare research findings in the United States to those outside the United States.

Qualitative, one-on-one 1-hour teleconference interviews were conducted by study authors (Brogan and Hogue) between September and November 2017 using the discussion guide and preread materials as a basis for discussion on value frameworks and their effect on health care decision making. No statistical analysis was conducted because of the small sample size and no methodological approaches were taken to attain consensus on the findings.

Results

Defining Value and Process for Making Decisions in U.S. Health Plans

U.S. payers surveyed did not have consistent or formal definitions of value or formal assessment processes to determine value for pharmaceutical products. They were also skeptical of the prospects of achieving value within the current U.S. health care system. Value assessment is conducted in an ad hoc manner considering expected cost and clinical benefits, medical necessity, appropriate use, therapeutic alternatives, and treatment class. However, U.S. payers feel limited in what they can do to optimize value in pharmaceutical decision making.

Various mechanisms are used by U.S. payers to assess value, including not covering treatments that are not medically necessary, limiting use of higher-priced medicines by placement in a higher tier (for which the beneficiary incurs higher out-of-pocket costs), step therapy (i.e., requiring a patient to fail on 1 or more less expensive treatments before the health plan will cover a more expensive treatment), prior authorization (i.e., requiring the health plan’s approval before access is given to the treatment, which typically involves submission of additional information by the health care provider), and preferred products (i.e., competitive contracting with specific manufacturers for preferred or exclusive status within the health plan, particularly for those treatments in an existing crowded market). U.S. payers do not have systemic and effective means and feel limited in what they can do to optimize value in pharmaceutical decision making.

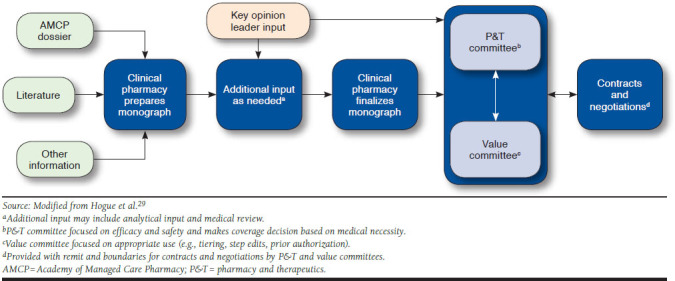

Although specific processes vary widely by payer, Figure 1 documents the representative summation of the process as indicated in interviews in which payers at U.S. health plans were presented with a map of the decision-making process for comment and critique (see the Appendix available in online article).29 In addition, the figure outlines general steps U.S. health plans often take to guide coverage decisions after a treatment is approved by the U.S. Food and Drug Administration (FDA). As an initial step, the clinical pharmacist prepares a monograph with evidence of treatment value to be reviewed by both the P&T committee and the value committee. Sources for the monograph include the Academy of Managed Care Pharmacy (AMCP) dossier provided by the manufacturer, the relevant literature, and any other information that may be available about the medicine and the disease area (e.g., competitor products, past decisions). Additional information in the monograph may also include internal analyses; medical review as determined by the plan, and if the medicine is administered by a physician and adjudicated under the medical benefit; or any potential cost offsets or medical benefit as related to treatment outcomes. After the clinical pharmacist finalizes the monograph, key opinion leaders may be brought in to provide input on the monograph or to provide expert opinion during the P&T committee and the value committee meetings.

FIGURE 1.

Process for Making Decisions in U.S. Health Plans

The P&T committee is the traditional decision-making body within a U.S. health plan; it focuses on efficacy and safety and determines whether the health plan should cover the treatment based on medical necessity and therapeutic equivalency. Value committees consider costs (e.g., budget impact and cost-effectiveness) in addition to efficacy and safety and are tasked with appropriate use of a treatment (e.g., tiering, step edits, and prior authorizations) to achieve value. The addition of value committees to the process map is the most substantial difference between the 2014 process map and the process map summarized in this study (Figure 1).29 Once the P&T committee and the value committee make their decisions, they provide guidance to the plan for negotiations and contracting with pharmaceutical manufacturers.

Value Assessment Efforts Among U.S. and Non-U.S. Payers

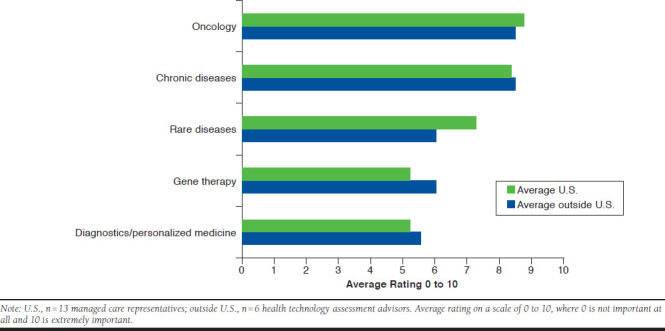

Payers were asked to rate on a scale of 0 to 10, where 0 is not important at all and 10 is extremely important, the importance of specific disease or coverage categories (e.g., chronic diseases, oncology, rare diseases, diagnostics/personalized medicine, and gene therapy) for their health plan cost-control efforts relative to value assessment. When comparing the responses from U.S. payers with those from payers outside the United States, a close alignment among the categories surveyed was identified. A notable minor difference was that U.S. payers indicated a higher importance for rare diseases when considering their cost-control efforts to better achieve value, whereas gene therapy was of higher importance to non-U.S. payers (Figure 2).

FIGURE 2.

Comparison of Specific Therapeutic Areas in Cost-Control Efforts Inside and Outside the United States

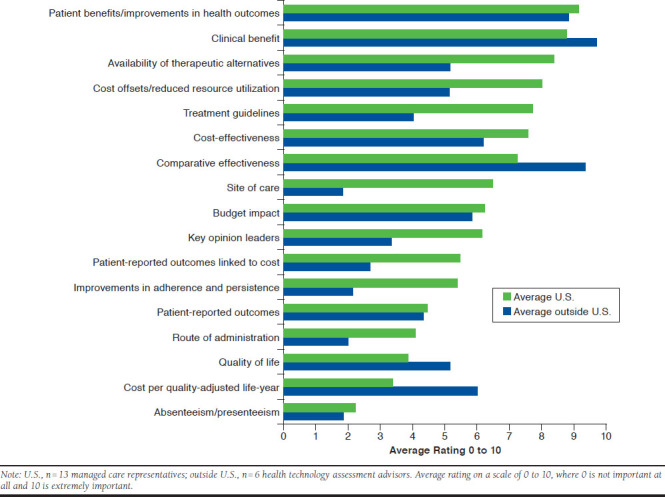

When U.S. and non-U.S. payers were asked to rate the importance of various factors for their value determinations, clinical and patient benefits or improvements in health outcomes were rated as high (a rating of 8-10) by all payers. Comparing the level of importance of various factors between U.S. and non-U.S. payers reveals some distinct differences. The availability of therapeutic alternatives, improvements in adherence and persistence, treatment guidelines, views from key opinion leaders, patient-reported outcomes linked to cost, route of administration, and site of care are all factors that are more important to U.S. payers than payers outside the United States in their value determinations. Payers outside the United States placed a higher importance than U.S. payers on cost per QALY, quality of life, and comparative effectiveness (Figure 3).

FIGURE 3.

Comparison of Specific Factors in Driving Value Assessment Efforts Inside and Outside the United States

U.S. Payer Use of Value Assessment Frameworks, Cost-Effectiveness Analysis, and Cost-Utility Analysis

U.S. payers were asked if any formal steps had been taken to make value determinations about new pharmaceuticals and if value assessment frameworks, such as those introduced by organizations including ASCO, NCCN, and ICER, are formally considered in their decision making. Two of 13 U.S. payers surveyed indicated making formal value determinations and 4 payers indicated that they formally consider value assessments, most commonly ICER and NCCN. However, all payers indicated that value assessment frameworks are considered informally as they are made available.

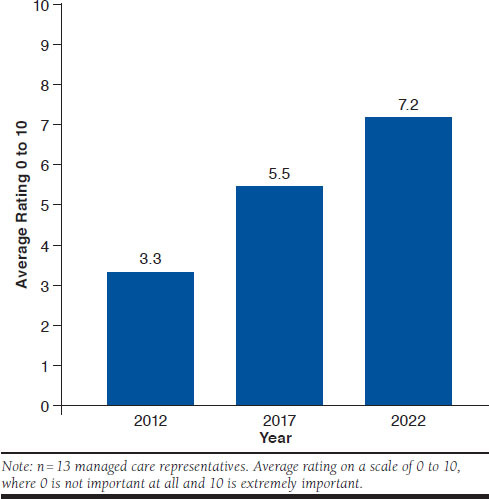

Cost-effectiveness and cost-utility analyses that are often used in countries outside the United States are part of the AMCP Format for Formulary Submissions30; however, the extent to which U.S. payers use these analyses varies. Nevertheless, when payers were probed on the importance of cost-effectiveness and cost-utility analyses to their health plans’ decision making for pharmaceuticals (using the same 0-to-10 rating scale as previously mentioned) and how this is expected to change over time, these analyses were reported to have increased in importance since 2012 and are expected to continue to increase by 2022 (Figure 4).

FIGURE 4.

Importance of Cost-Effectiveness and Cost-Utility Analyses to U.S. Payer Decision Making and Changes over Time

Limits and Challenges in Determining Value Among U.S. Payers

Payers highlighted several challenges and concerns for determining and achieving better value in the U.S. health care system. For instance, all U.S. payers interviewed indicated that they feel pressured to cover an FDA-approved treatment, regardless of cost or value, if no therapeutic alternative is available. In addition, many payers expressed concern that they have limited or no control over pharmaceutical pricing. Patient-reported outcomes and other outcomes are gaining more importance to U.S. payers as patients are bearing more cost burden associated with their health care in the United States. Payers are particularly interested in linking patient-reported outcomes to costs and outcomes (e.g., better adherence and reduced hospitalization) in order to couple the patient perspective to aspects of value. Payers also stated the need to make a coverage decision within a set time period after market entry (3 months in some cases) because of CMS requirements for Medicare Part D plans.31 Similarly, according to the Patient Protection and Affordable Care Act, CMS is legally not able to make treatment coverage decisions based on cost-per-QALY thresholds.32-35

Payers reported skepticism about the value and broad applicability of the recent proliferation of outcomes-based contracting because of the lack of demonstrated savings. In addition, payers indicated that outcomes-based contracts would result in new administrative burden to health care professionals and payers in terms of managing, tracking, and implementing the terms of the contract properly. Despite skepticism, payers reported that outcomes-based contracting could result in savings in specific cases where the treatment has a particularly high cost and there is a clear outcome that can be readily measured, as several outcomes-based contracts have been announced for high-priced treatments.36 Several U.S. payers also discussed the idea of discontinuation-based contracting as an outcomes-based contract with a simple, easily trackable outcome: in this model, when a patient discontinues a product, it serves as a proxy for treatment failure, triggering a rebate from the pharmaceutical manufacturer to the health plan.

U.S. payers surveyed were largely open to learning from the health care systems of other countries but described barriers including differences in health care system structures and U.S. law limiting CMS’s ability to use cost per QALY and the implied effect this has on private health insurance. Although cost-effectiveness analyses continue to gain traction in the United States, implementing QALY thresholds as used by the National Institute for Health and Care Excellence in the United Kingdom to compare various technologies (where treatments are less likely to be recommended for use if they surpass the QALY thresholds) was viewed as infeasible in the United States in the near term. One payer believed this was not feasible in the United States because of challenges with identifying cost-per-QALY thresholds. Another payer reported challenges with the lack of control for prices and lack of payment for indirect costs. Furthermore, the benefits of price-volume agreements such as those used in Italy and France were of limited interest to U.S. payers. These agreements require pharmaceutical manufacturers to pay back some or all of the cost of a treatment beyond its estimated budget impact. U.S. payers surveyed in this study did not consider price-volume agreements to be a viable mechanism for managing pharmaceutical costs, as the U.S. system is not set up for clawbacks and such agreements would be difficult to implement.

Several U.S. payers acknowledged the potential to achieve improved value through a German health care system approach that predicates price and coverage upon demonstration of patient benefits for a new medicine compared with an approved comparator. Several U.S. payers believed that a viable mechanism to control pharmaceutical costs and achieve more value for the U.S. health care system would be to require disease-specific outcomes measures for use in comparative-effectiveness research; 1 suggestion was that the CMS could provide guidance for collection of disease-specific outcomes for use in comparative-effectiveness research.

Discussion

Although various value frameworks exist, our study finds that they are not formally considered in formulary and reimbursement decisions but are used as a reference as they become available by most or all U.S. health plans. In part, this is because various value frameworks exist in the United States. Furthermore, U.S. payers did not have consistent definitions of value, did not have formal value assessment processes, and felt limited in what they could do to achieve value in pharmaceutical decision making. As described above, value assessments consist of various core, common, and novel dimensions.15 From an economic perspective, gross value has been described as the willingness to pay, while net value is the gross value minus the cost incurred to obtain the gross value. However, considerations should be made of the level of preference on interventions that vary by insurers and providers.6 Based on the interviews, payers were also skeptical of achieving better value in the current U.S. health care system—given the highly competitive environment among insurers—and limited national guidelines for value assessment (e.g., CMS requiring a value assessment) or price.

Outcomes-based contracting was viewed by U.S. payers as having some usefulness in select circumstances (e.g., high-priced treatment with a readily measurable outcome). However, payers did not consider outcomes-based contracting to be a broadly applicable solution, particularly because of the burden of additional data collection for payers and health care professionals, difficulties with respect to operationalization, management, and lack of demonstrated savings for implementing outcomes-based contracting. In the United Kingdom, where such agreements have been implemented, there have been challenges with the adoption of complex analytical approaches in the analysis of the data.37 Italy has implemented more than 50 national outcomes-based contracts with pharmaceutical manufacturers since 2008, but these collectively account for less than 1% of the Italian Medicines Agency’s total spending on pharmaceuticals between 2013 and 2016 and have not been a significant source of savings.38

Other developed countries have used value assessment in policies that have achieved cost savings. For instance, the United Kingdom has strict cost-effectiveness thresholds that have been used effectively to control costs by denying reimbursement of treatments that are priced too high.39 Australia, Canada, France, and Italy also consider demonstration of cost-effectiveness of new treatments to be a pivotal part of the decision-making process.40-43 Italy and France have effectively used price-volume agreements to manage pharmaceutical costs and achieve value, and the payers from France and Italy interviewed in this study both noted that price-volume agreements are the only confirmed mechanism to save money over time.40,42 These price-volume agreements are typically negotiated privately, and the details and savings for these arrangements are not transparent and publicly available. The central element for the German system is the requirement for a new treatment to show improved mortality, morbidity, quality of life, or safety compared with a previously approved medicine.44

Such assessments could be used not only by Medicare and Medicaid but also by private payers who feel limited in their current ability to assess and use value. However, changes in public policy may be necessary to explicitly provide public programs authority and resources necessary to advance value assessment. In the absence of a government entity leading this work, a private group in the United States is just beginning to systematically assess pharmaceutical agents for value, but these analyses have not been formally incorporated into coverage and reimbursement decisions by public and private payers, limiting their effect to date.12

Nevertheless, based on our structured interviews with U.S. payers, the use of value assessment frameworks, cost-effectiveness analyses, cost-utility analyses, comparative-effectiveness analyses, competitive contracting, preferred status for therapeutic equivalents, implementation of required specific outcomes measures, and more strictly defined patient-relevant benefits are expected to increase in the years ahead.

Limitations

The inherent limitations of this study should be recognized. This study was conducted qualitatively with open-ended responses and, because of the extensive time required for this approach, a small sample size of HTA advisors and payers were used. Furthermore, no statistical analysis was conducted because of the small sample size and no methodological approaches were taken to attain consensus on the findings. The U.S. payers surveyed were all executive-level, covered all regions of the United States, and collectively represented over 200 million members (not considering overlap of covered lives between the participating payers); nevertheless, because of the small sample size, the findings of this study may not be fully generalizable to all U.S. payers. Only one HTA advisor per country outside the United States was surveyed and, while the questions and input provided by these HTA advisors tended to be general in nature, some findings in this study may not be fully generalizable for a particular country. It is also worth noting that the possibility of biased responses from payers and HTA advisors could not be ruled out, but that this study did allow for respondents to provide open-ended responses. Finally, no formal definitions for price-volume agreements were provided to payers, but the concept was presumed to be defined as the “discount agreed from the manufacturer based on the manufacturer’s market share for the treatment.”

Conclusions

U.S. payers interviewed in this survey did not believe that the current environment in the United States enables them the ability to make advantageous contracts with manufacturers. Payers in other countries use such instruments more widely because they are enabled by government health care bodies, policy tools, and analytical frameworks that have no counterpart in the United States. Adoption of a value assessment framework in Medicare or Medicaid would accelerate adoption of these tools by private payers in the United States.

ACKNOWLEDGMENTS

The authors thank Josephine Mauskopf, PhD, of RTI Health Solutions, who contributed to the development of this manuscript.

APPENDIX. U.S. Payer Participants

| Geographic Coverage Area | Covered Lives | |||||

|---|---|---|---|---|---|---|

| Total, Millions | Commercial, % | Exchange, % | Medicare, % | Medicaid, % | ||

| Medical Director, P&T Chair | Regional; West | 40.0 | 77 | 4 | 4 | 15 |

| Medical Director, P&T Chair | Regional; West | 3.3 | 38 | 8 | 9 | 45 |

| C-Suite Medical Director, P&T Chair | Integrated; Northeast | 3.5 | 40 | 10 | 30 | 20 |

| C-Suite Medical Director, P&T Chair | Integrated; Mountain West | 0.82 | 68 | 15 | 5 | 12 |

| C-Suite Medical Director, P&T Chair | Regional; Northeast | 1.25 | 63 | 3 | 20 | 14 |

| Medical Director, P&T Chair | Regional; Northeast | 40.0 | 55 | < 1 | 33 | 13 |

| C-Suite Medical Director, P&T Chair | National; Midwest | 11.5a | 15 | 8 | 50 | 3 |

| Medical Director, P&T Chair | National; Midwest | 22.0 | 41 | 5 | 45 | 9 |

| C-Suite Pharmacy Director, P&T Chair | Regional; Midwest-West | 42.0 | 67 | 12 | 17 | 5 |

| C-Suite Pharmacy Director, P&T Chair | National; West | 40.0 | 70 | 3 | 15 | 12 |

| C-Suite Pharmacy Director, P&T Chair | Regional and National | 1.5 | 85 | 3 | 10 | 2 |

| Northeast | 42.0 | 95 | 0 | 5 | 2 | |

| Pharmacy Director, P&T Chair | Regional; West | 3.0 | 95 | 5 | 0 | 0 |

| C-Suite Pharmacy Director | National; Southeast | 88.0b | 70 | 8 | 9 | 8 |

a23% Tricare.

b5% Tricare.

P&T = pharmacy and therapeutics.

REFERENCES

- 1.Personalized Medicine Coalition . Personalized medicine at FDA: a progress and outlook report. 2018. Available at: http://www.personalizedmedicinecoalition.org/Userfiles/PMC-Corporate/file/PM_at_FDA_A_Progress_and_Outlook_Report.pdf. Accessed October 24, 2019.

- 2.Mullard A. 2017 FDA drug approvals. Nat Rev Drug Discov. 2018;17(2): 81-85. [DOI] [PubMed] [Google Scholar]

- 3.Papanicolas I, Woskie LR, Jha AK. Health care spending in the United States and other high-income countries. JAMA. 2018;319(10):1024-39. [DOI] [PubMed] [Google Scholar]

- 4.Cuckler GA, Sisko AM, Poisal JA, et al. National health expenditure projections, 2017-26: despite uncertainty, fundamentals primarily drive spending growth. Health Aff (Millwood). 2018;37(3):482-92. [DOI] [PubMed] [Google Scholar]

- 5.Towse A, Mauskopf JA. Affordability of new technologies: the next frontier. Value Health. 2018;21(3):249-51. [DOI] [PubMed] [Google Scholar]

- 6.Garrison LP Jr, Neumann PJ, Willke RJ, et al. A health economics approach to US value assessment frameworks-summary and recommendations of the ISPOR Special Task Force report. Value Health. 2018;21(2):161-65. [DOI] [PubMed] [Google Scholar]

- 7.Bentley TGK, Cohen JT, Elkin EB, et al. Measuring the value of new drugs: validity and reliability of 4 value assessment frameworks in the oncology setting. J Manag Care Spec Pharm. 2017;23(6-a Suppl):S34-S48. Available at: https://www.jmcp.org/doi/10.18553/jmcp.2017.23.6-a.s34. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Schnipper LE, Davidson HE, Wollins DS, et al. Updating the American Society of Clinical Oncology value framework: revisions and reflections in response to comments received. J Clin Oncol. 2016;34(24):2925-34. [DOI] [PubMed] [Google Scholar]

- 9.National Comprehensive Cancer Network . NCCN clinical practice guidelines in oncology (NCCN Guidelines) with NCCN Evidence Blocks. Available at: www.nccn.org/evidenceblocks/. Accessed October 24, 2019.

- 10.Memorial Sloan Kettering Cancer Center . Drug Abacus. Available at: https://drugpricinglab.org/tools/drug-abacus/. Accessed October 24, 2019.

- 11.Slomiany M, Madhavan P, Kuehn M, Richardson S. Value frameworks in oncology: comparative analysis and implications to the pharmaceutical industry. Am Health Drug Benefits. 2017;10(5):253-60. [PMC free article] [PubMed] [Google Scholar]

- 12.Institute for Clinical and Economic Review . Overview of the ICER value assessment framework and update for 2017-2019. March 2018. Available at: https://icer-review.org/wp-content/uploads/2018/03/ICER-value-assessment-framework-update-FINAL-062217.pdf. Accessed October 24, 2019.

- 13.Neumann PJ, Willke RJ, Garrison LP Jr. A health economics approach to US value assessment frameworks-introduction: an ISPOR Special Task Force report [1]. Value Health. 2018;21(2):119-23. [DOI] [PubMed] [Google Scholar]

- 14.Neumann PJ, Cohen JT. Measuring the value of prescription drugs. N Engl J Med. 2015;373(27):2595-97. [DOI] [PubMed] [Google Scholar]

- 15.Lakdawalla DN, Doshi JA, Garrison LP Jr, Phelps CE, Basu A, Danzon PM. Defining elements of value in health care-a health economics approach: an ISPOR Special Task Force report [3]. Value Health. 2018;21(2):131-39. [DOI] [PubMed] [Google Scholar]

- 16.Danzon PM, Drummond MF, Towse A, Pauly MV. Objectives, budgets, thresholds, and opportunity costs-a health economics approach: an ISPOR Special Task Force report [4]. Value Health. 2018;21(2):140-45. [DOI] [PubMed] [Google Scholar]

- 17.Phelps CE, Lakdawalla DN, Basu A, Drummond MF, Towse A, Danzon PM. Approaches to aggregation and decision making-a health economics approach: an ISPOR Special Task Force report [5]. Value Health. 2018;21(2):146-54. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 18.Willke RJ, Neumann PJ, Garrison LP Jr, Ramsey SD. Review of recent US value frameworks-a health economics approach: an ISPOR Special Task Force report [6]. Value Health. 2018;21(2):155-60. [DOI] [PubMed] [Google Scholar]

- 19.Garrison LP Jr, Pauly MV, Willke RJ, Neumann PJ. An overview of value, perspective, and decision context-a health economics approach: an ISPOR Special Task Force report [2]. Value Health. 2018;21(2):124-30. [DOI] [PubMed] [Google Scholar]

- 20.Murray MD. Curricular considerations for pharmaceutical comparative effectiveness research. Pharmacoepidemiol Drug Saf. 2011;20(8):797-04. [DOI] [PubMed] [Google Scholar]

- 21.Holtorf AP, Brixner D, Bellows B, Keskinaslan A, Dye J, Oderda G. Current and future use of HEOR data in healthcare decision-making in the United States and in emerging markets. Am Health Drug Benefits. 2012;5(7):428-38. [PMC free article] [PubMed] [Google Scholar]

- 22.Drummond MF, Sculpher MJ, Claxton K, Stoddart GL, Torrance GW. Methods for the Economic Evaluation of Health Care Programmes. 4th ed. Oxford: Oxford University Press; 2015:chap 1. [Google Scholar]

- 23.Sox HC, Greenfield S. Comparative effectiveness research: a report from the Institute of Medicine. Ann Intern Med. 2009;151(3):203-05. [DOI] [PubMed] [Google Scholar]

- 24.WellPoint . Use of comparative effectiveness research (CER) and observational data in formulary decision making: evaluation criteria. 2010. Available at: http://www.elsevierbi.com/~/media/Images/Publications/Archive/The%20Pink%20Sheet/72/021/00720210012/20100521_wellpoint.pdf. Accessed October 24, 2019.

- 25.Subedi P, Perfetto EM, Ali R. Something old, something new, something borrowed…comparative effectiveness research: a policy perspective. J Manag Care Pharm. 2011;17(9 suppl A):S5-9. Available at: https://www.jmcp.org/doi/abs/10.18553/jmcp.2011.17.s9-a.S05. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26.Segal JB, Kallich JD, Oppenheim ER, et al. Using certification to promote uptake of real-world evidence by payers. J Manag Care Spec Pharm. 2016;22(3):191-96. Available at: https://www.jmcp.org/doi/10.18553/jmcp.2016.22.3.191. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 27.Seeley E, Kesselheim AS. Outcomes-based pharmaceutical contracts: an answer to high U.S. drug spending? Issue Brief (Commonw Fund). 2017;2017:1-8. [PubMed] [Google Scholar]

- 28.American Academy of Actuaries . Prescription drug spending in the U.S. health care system. Issue brief. March 2018. Available at: https://www.actuary.org/content/prescription-drug-spending-us-health-care-system. Accessed October 24, 2019.

- 29.Hogue SL, Brogan AP, Earnshaw SR, Khan SB, Nelsen SH. Academy of Managed Care Pharmacy (AMCP) dossiers: use in health care decision making. Poster presented at: 19th Annual International Conference of the International Society for Pharmacoeconomics and Outcomes Research; May 31-June 4, 2014; Montreal, Canada. [Google Scholar]

- 30.Pannier A, Dunn JD.. AMCP format for formulary submissions, version 4.0. J Manag Care Spec Pharm. 2016;22(5):448. Available at: https://www.jmcp.org/doi/10.18553/jmcp.2016.16092. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Centers for Medicare & Medicaid Services . Section 30.2 provision of an adequate formulary. In: Medicare prescription drug benefit manual: chapter 6 – Part D drugs and formulary requirements. Revised January 15, 2016. Available at: https://www.cms.gov/Medicare/Prescription-Drug-Coverage/PrescriptionDrugCovContra/Downloads/Part-D-Benefits-Manual-Chapter-6.pdf. Accessed October 24, 2019.

- 32.Neumann PJ, Weinstein MC. Legislating against use of cost-effectiveness information. N Engl J Med. 2010;363(16):1495-97. [DOI] [PubMed] [Google Scholar]

- 33.Navarro RP. Changing the way we pay for health care: is value the new plastic? J Manag Care Spec Pharm. 2017;23(10):998-1002. Available at: https://www.jmcp.org/doi/10.18553/jmcp.2017.23.10.998. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34.Chambers JD, Lord J, Cohen JT, Neumann PJ, Buxton MJ. Illustrating potential efficiency gains from using cost-effectiveness evidence to reallocate Medicare expenditures. Value Health. 2013;16(4):629-38. [DOI] [PubMed] [Google Scholar]

- 35.The Patient Protection and Affordable Care Act (ACA), 42 USC §18001 (2010) . Available at: https://www.congress.gov/111/plaws/publ148/PLAW-111publ148.pdf. Accessed October 24, 2019.

- 36.Davio K. Alnylam to offer value-based contracts for $450,000 rare disease drug. 2018. AJMC. August 15, 2018. Available at: https://www.ajmc.com/focus-of-the-week/alnylam-to-offer-valuebased-contracts-for-450000-rare-disease-drug. Accessed October 24, 2019.

- 37.Palace J, Bregenzer T, Tremlett H, et al. UK multiple sclerosis risk-sharing scheme: a new natural history dataset and an improved Markov model. BMJ Open. 2014;4(1):e004073. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 38.Bisserbe N. For new Trump drug plan, a cautionary tale in Italy. Wall Street Journal. April 17, 2018. Available at: https://www.wsj.com/articles/italy-serves-cautionary-lesson-for-new-trump-drug-plan-1523959644. Accessed October 24, 2019.

- 39.National Institute for Health and Care Excellence (NICE) . Developing NICE guidelines: the manual. Process and methods guides. October 2014. Available at: https://www.nice.org.uk/media/default/about/what-we-do/our-programmes/developing-nice-guidelines-the-manual.pdf. Accessed October 24, 2019.

- 40.Agenzia Italiana del Farmaco (AIFA) . Available at: http://www.aifa.gov.it/en. Accessed October 24, 2019.

- 41.Canadian Agency for Drugs and Technologies in Health (CADTH) . Health technology assessment and optimal use: medical devices; diagnostic tests; medical, surgical, and dental procedures. November 19, 2015. Available at: https://www.cadth.ca/about-cadth/what-we-do/products-services/hta. Accessed October 24, 2019.

- 42.Haute Autorité de Santé (HAS) . Assessment of health technologies and procedures. November 27, 2015. Available at: https://www.has-sante.fr/portail/jcms/c_2035673/en/assessment-of-health-technologies-and-procedures. Accessed October 24, 2019.

- 43.Pharmaceutical Benefits Advisory Committee (PBAC) . Guidelines for preparing a submission to the Pharmaceutical Benefits Advisory Committee. Version 5.0. September 2016. Available at: https://pbac.pbs.gov.au/content/information/files/pbac-guidelines-version-5.pdf. Accessed October 24, 2019.

- 44.GKV-Spitzenverband . AMNOG–evaluation of new pharmaceutical. Available at: https://www.gkv-spitzenverband.de/english/statutory_health_insurance/amnog_evaluation_of_new_pharmaceutical/amnog_english.jsp. Accessed October 24, 2019.