Abstract

Purpose

The purpose of this exploratory sequential mixed methods study was to describe the sources of informal financial support used by adolescent and young adult (AYA) cancer survivors and how financial toxicity and demographic factors were associated with different types and magnitudes of informal financial support.

Methods

This analysis is part of a larger health insurance literacy study that included pre-trial interviews and a randomized controlled trial (RCT) for AYA cancer survivors. Eligible study participants were 18 years of age, diagnosed with cancer as an AYA (15–39 years), insured, and for the RCT sample less than 1 year from diagnosis. Interview audio was transcribed, quality checked, and thematically analyzed. RCT baseline and follow-up surveys captured informal financial support use. Chi-squared and Fisher’s exact tests were used to assess differences in informal financial support type use and frequency by financial toxicity and AYA demographics.

Results

A total of N = 24 and N = 86 AYAs participated in pre-trial interviews and the RCT respectively. Interview participants reported a variety of informal financial support sources including savings, community, family/friends, and fundraisers. However, only half of participants reported their informal financial support to be sufficient. High financial toxicity was associated with the most types of informal financial support and a higher magnitude of use. The lowest income group accessed informal financial supports less frequently than higher income groups.

Conclusion

Our study demonstrates that AYA survivors experiencing financial toxicity frequently turn to informal sources of financial support and the magnitude is associated with financial toxicity. However, low-income survivors, and other at-risk survivors, may not have access to informal sources of financial support potentially widening inequities.

Keywords: Adolescent and young adult, AYA, Cancer survivors, Financial support sources, Financial toxicity, Financial burden

Introduction

In the United States (U.S.), the economic burden of cancer-related out-of-pocket costs, or financial toxicity, is a substantial and growing problem for over 70% of cancer survivors [1]. Despite expansion of insurance coverage under the Affordable Care Act (ACA), many U.S. cancer patients remain underinsured, meaning that their health insurance coverage is insufficient to help them manage the costs of cancer care [2]. In 2019, the total patient economic burden of cancer care was estimated at $21.1 billion with $16.2 billion attributed to out-of-pocket costs and $4.9 billion in opportunity costs [3]. Financial toxicity has significant impacts on patient physical, mental, and economic health including treatment non-adherence and higher rates of anxiety and depression, as well as increased debt and bankruptcy [4–6].

Adolescent and young adult (AYA) cancer survivors, diagnosed between the ages of 15 and 39 years of age, experience disproportionately high financial toxicity when compared to cancer survivors of any other age group, which may increase their use of formal and informal financial support [7]. Being diagnosed with cancer as an AYA may be particularly challenging due to the transition to adulthood which is hallmarked by financial-related life events such as managing student loans, solidifying a career, and establishing financial independence [8, 9]. In this time of life, many AYAs do not have access to robust health insurance coverage and have limited wealth and possessions, and their cancer often interrupts employment and school trajectories [10–12]. Thus, when AYAs are unable to work due to their cancer, they may experience lost wages [13] and are often forced to access financial support to pay for their cancer care.

Formal support systems such as hospital charity care and foundation grants are typically accessed through applications and often awarded based on income requirements and perceived need [13]. In comparison, informal financial support encapsulates a variety of activities including using personal savings and seeking support from family and friends, as well as raising funds through community fundraisers and online crowdfunding [13]. Cancer survivors who experience high financial toxicity may access informal supports more frequently which may prove problematic in the context of the dynamic time of life they are diagnosed, but this has not been studied in depth.

While the financial toxicity of cancer care for AYA survivors has been well established [6, 14], the extent to which AYA survivors seek informal sources of financial support to manage their treatment costs and living expenses remains unknown. Thus, the purpose of this study was to describe the sources of informal financial support used by AYA cancer survivors to pay for their medical care and living expenses, and whether they perceive this support to be sufficient for addressing their cancer-induced financial needs. Furthermore, we aimed to explore how financial toxicity and demographic factors were associated with different types and magnitude of informal financial support. We deployed a mixed methods design utilizing and integrating qualitative and quantitative data from a larger health insurance literacy study outlined below [15].

Methods

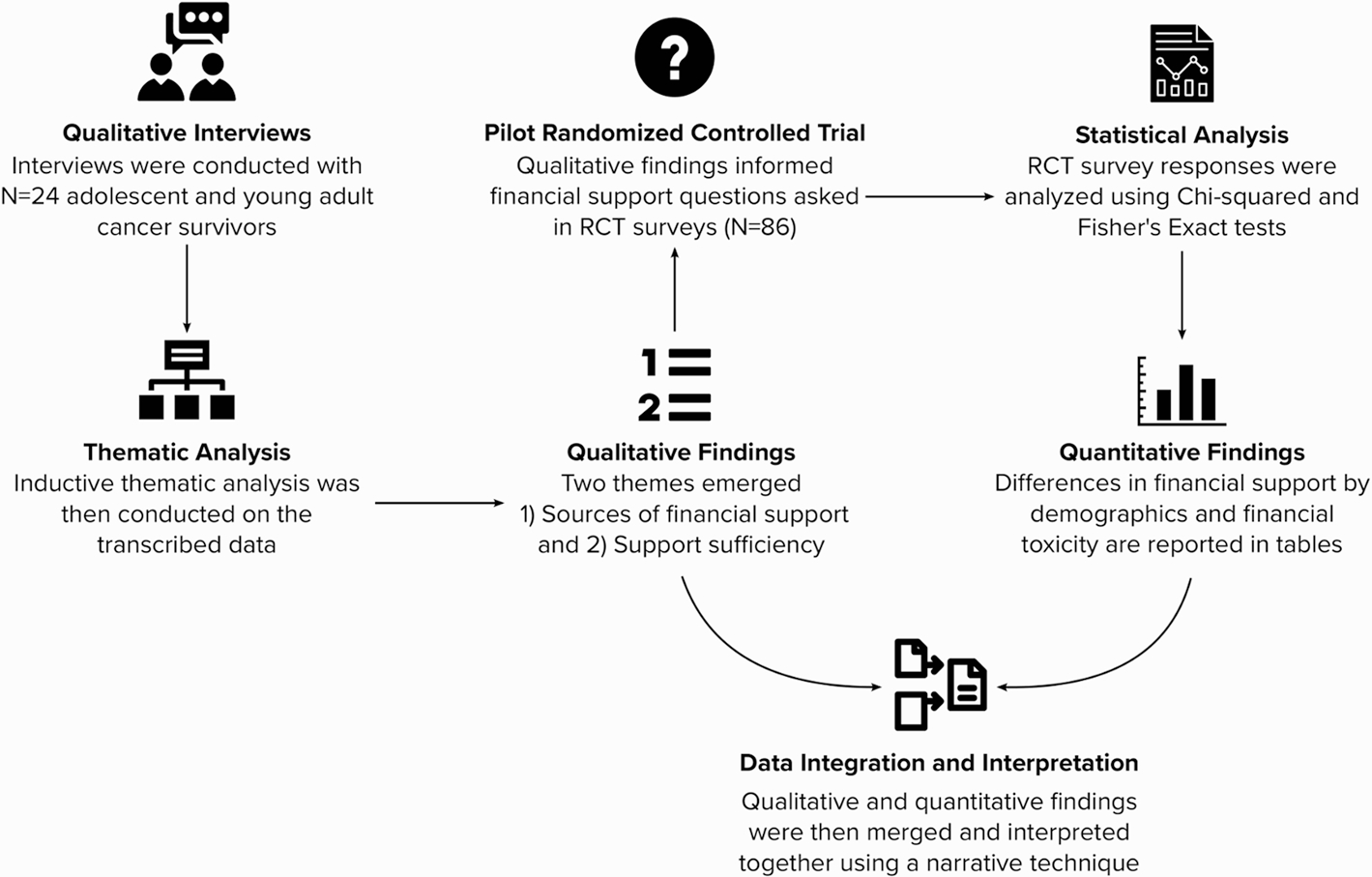

This analysis was part of the HIAYA CHAT (Huntsman Intermountain Adolescent and Young Adult Cancer Care Program “Let’s chat about health insurance”) study [15]. HIAYA CHAT is a health insurance navigation intervention for newly diagnosed AYA cancer survivors. We first conducted qualitative interviews to understand the health insurance experiences of AYA cancer survivors (both on and off treatment) and inform the development of the health insurance education intervention. Then, we conducted a pilot randomized control trial (RCT) of the intervention that enrolled participants in their first year after diagnosis. These samples were recruited sequentially and contained no overlapping participants. The current exploratory sequential mixed methods approach integrates data from two samples (qualitative interviews, n = 24; quantitative RCT surveys, n = 86) to enhance rigor and validity of the findings.

Participants, recruitment, and data collection

Eligible participants for the qualitative interviews were diagnosed with cancer as an AYA (between the ages of 15 and 39 years), were 18 years of age or older, and insured at the time of interview. RCT participants were early in their diagnosis at consent (within ~ 1 year) and received treatment at one of three hospitals in Salt Lake City, UT. Clinic schedules, provider referrals, social media posts, and an AYA navigator database were used to identify potential participants. Interview participants were sampled according to dependent insurance coverage age cut-off of 26 years, to achieve equal strata of younger (18–25 years at diagnosis) and older (26–39 years at diagnosis) participants. Interview participants were approached between October 2019 and March 2020, while RCT participants were approached between November 2020 and December 2021.

A total of 51 eligible AYAs were contacted by the study team for the qualitative interviews; 5 declined and 14 were unable to be contacted. A total of 24 AYAs were interviewed until thematic saturation occurred and the research team ended recruitment. The remaining 8 interested AYAs were invited to participate in the HIAYA CHAT RCT. The interview guide was developed by the study team to elicit AYA survivors’ experiences with their health insurance and financial toxicity including the sources of their financial support and the perceived sufficiency of the support (Supplemental File). The interviewers (ARW and KvTB) piloted the interview guide with 6 AYA survivors. Recruitment occurred concurrently with analysis to maximize reflexivity and to confirm that thematic saturation (the point at which no new themes emerged from the interviews) was achieved, decided by interviewers (ARW and KvTB) [16, 17]. AYAs who participated in the interview completed informed consent and a short survey prior to the interview. Interviews lasted 32 min on average.

A total of 186 eligible AYAs were contacted to participate in the RCT, 55 declined and 45 were unable to be contacted, 86 consented. RCT participants provided informed consent, completed a baseline survey, and were sent a follow-up survey 3 months post-intervention (5 months post baseline). The baseline survey was completed by 86 AYAs, and the follow-up survey was completed by 75 of the 86 AYAs. Attrition from the HIAYA CHAT study was not ascertained from all participants as some stopped participating in the intervention or responding to the navigator. Other participants described why they could not continue, including being too busy or needing to plan medical procedures.

Qualitative analysis

Interviews were recorded, professionally transcribed, and quality checked by the study team. An inductive thematic analysis approach was used to analyze the data [18, 19]. Two cycles of structured coding were employed in NVivo 11 [18, 19]. First cycle coding (20% of interviews) used sentence-by-sentence coding. First cycle codes were then condensed into a coding scheme [18]. An additional 20% of interviews were coded to refine the coding scheme, resulting in the finalized coding structure. Second cycle coding included testing inter-coder reliability by double-coding an additional 20% of the interviews [18]. Once discrepancies were rectified through coder consensus (ARW and KvTB), all interviews were coded into the coding structure by ARW and KvTB. The coding structure resulted in three overarching categories of feedback about health insurance literacy, cost-of-care conversations, and financial support. The analysis presented here focuses on the third category—financial support—including two themes within the category: (1) Use of and Sources of Informal Financial Support and (2) Sufficiency of Informal Financial Support.

Survey items

Survey items regarding financial support sources were added to the HIAYA CHAT intervention baseline and follow-up survey due to the priority AYA participants placed on these topics during the qualitative interviews. The question about sources of financial support was a matrix in which participants selected “yes” or “no” to each type of financial support over the past year to cover both direct medical costs and living expenses. If participants indicated that they used a crowdfunding site for financial support, they were asked to approximate how much money they (or their proxy) raised on the site.

The survey also included demographic factors such as age at diagnosis, age at participation, gender, sexual orientation, education, insurance type, and income. The COmprehensive Score for financial Toxicity (COST), a validated 11-item outcome measure asking about financial toxicity over the past 4 weeks, was also included in the baseline survey [20]. Other intervention specific measures were included in the survey but are not reported here.

Statistical analysis

Descriptive statistics were calculated for each sample (qualitative interviews, RCT surveys). Age at participation was dichotomized due to the ACA dependent coverage cut-off at age 26 (younger AYAs 18–25 vs. older AYAs 26–39). COST scores ranged from 2 to 44, which we dichotomized at 21, a common cut-off to indicate high vs. low financial toxicity [20]. Frequency of each informal financial support source was calculated from baseline and follow-up surveys (i.e., participants indicated that they used a specific financial support source at baseline or follow-up) to ensure that participants who began using informal financial sources during the study were documented. Associations of COST score and demographic factors with different types of financial support sources were calculated using chi-squared or Fisher’s exact tests. Fisher’s exact tests are recommended for estimates made on small cell sizes to reduce bias; we used for cells < 10 participants when stratified by the outcome variable [21]. Demographic factors chosen to be included in these tests included household income (those they share their finances with), age at participation, and gender, which were theoretically driven and based on known associations with financial toxicity from the current literature [22, 23].

A summary score for the total number of informal financial supports used was calculated by summing financial support sources by participant. The raw score was then grouped into three categories including using 0 sources, 1–2 sources, and 3 or more sources with a maximum of 6 sources. The categories were derived from studies of cancer-related financial toxicity [24]. A second set of bivariate analyses were conducted using this three-level variable to determine associations of COST, household income, age at participation, and gender with different number of informal financial supports used. All analyses were conducted with a pre-set significance level of α < 0.05 in STATA 14.2.

Data integration

Mixed methods data integration is a critical step for bringing together qualitative and quantitative data. Integration occurred at all stages of the analysis. First, the financial support survey questions that were included in the intervention survey were included because of qualitative findings following the approach of the exploratory sequential mixed methods design. Results were then merged using a narrative approach in which interview and survey findings are reported in the results by method then compared and contrasted [25, 26]. Step by step integration can be found in Fig. 1. All study procedures were approved by the University of Utah IRB (IRB_00091443 and IRB_00127029).

Fig. 1.

Mixed methods data integration

Footnote: RCT: Randomized controlled trial

Results

A total of N = 24 AYAs participated in individual interviews and N = 86 AYAs participated in the health insurance education RCT baseline survey. Demographic characteristics of both samples are shown in Table 1. Qualitative thematic analysis resulted in two themes regarding AYAs informal financial support: (1) Use of and Sources of Informal Financial Support and (2) Sufficiency of Informal Financial Support.

Table 1.

Demographic characteristics of adolescent and young adult cancer survivors

| Qualitative interview sample (N = 24) |

Randomized controlled trial sample (N = 86) |

|||

|---|---|---|---|---|

| N | % | N | % | |

|

| ||||

| Age at participation | ||||

| 18–25 years | 12 | 50.0 | 30 | 34.9 |

| 26–39 years | 12 | 50.0 | 56 | 65.1 |

| Gender | ||||

| Male | 10 | 41.7 | 27 | 31.4 |

| Female | 14 | 58.3 | 59 | 68.6 |

| COST score | ||||

| High financial toxicity | 13 | 54.2 | 47 | 57.3 |

| Low financial toxicity | 11 | 45.8 | 35 | 42.7 |

| Household income | ||||

| < $10,000 | - | - | 10 | 13.9 |

| $10,000-$39,000 | - | - | 15 | 20.8 |

| $40,000-$79,000 | - | - | 18 | 25.0 |

| $80,000 + | - | - | 29 | 40.3 |

| Treatment status | ||||

| On treatment | 15 | 62.5 | 60 | 69.8 |

| Off treatment | 8 | 33.3 | 26 | 30.2 |

| Education | ||||

| College graduate or higher | 8 | 33.3 | 39 | 45.4 |

| Some college | 14 | 58.3 | 27 | 31.4 |

| High school education or less | 2 | 8.3 | 20 | 23.3 |

| Race and ethnicity | ||||

| Non-Hispanic White | 19 | 79.2 | 62 | 72.9 |

| Hispanic White | 4 | 16.7 | 16 | 18.8 |

| Non-Hispanic racial minority | 1 | 4.2 | 7 | 8.2 |

| Sexual orientation | ||||

| Sexual minority | 2 | 8.3 | 7 | 8.2 |

| Heterosexual | 22 | 91.7 | 78 | 91.8 |

| Health insurance status at survey+ | ||||

| Private insurance | 21 | 87.5 | 72 | 83.7 |

| Public insurance | 5 | 20.8 | 9 | 10.5 |

| I don’t know/other | 1 | 4.2 | 5 | 5.8 |

The qualitative interview sample and RCT sample are mutually exclusive, but both were collected as part of an overall health insurance literacy study + Percentages add up to more than 100% as some participants had more than one health insurance coverage type (i.e., public and private). Income was not asked for the qualitative sample. For the qualitative interview sample, treatment status is missing N = 1. For the randomized controlled trial sample, COST score is missing N = 4 and income is missing N = 14

Use of and Sources of Informal Financial Support

Nearly all interview participants reported receiving informal financial support. When asked to elaborate on the source, participants mentioned support from community and church, extended and immediate family, and friends and coworkers.

“Just a couple friends being, like, hey, here is some money.”

“There’s probably been another like $2,000.00, if not more, that has just been donated at random by family members or family friends that have just come and given us money.”

“The church helped pay for the copay payments.”

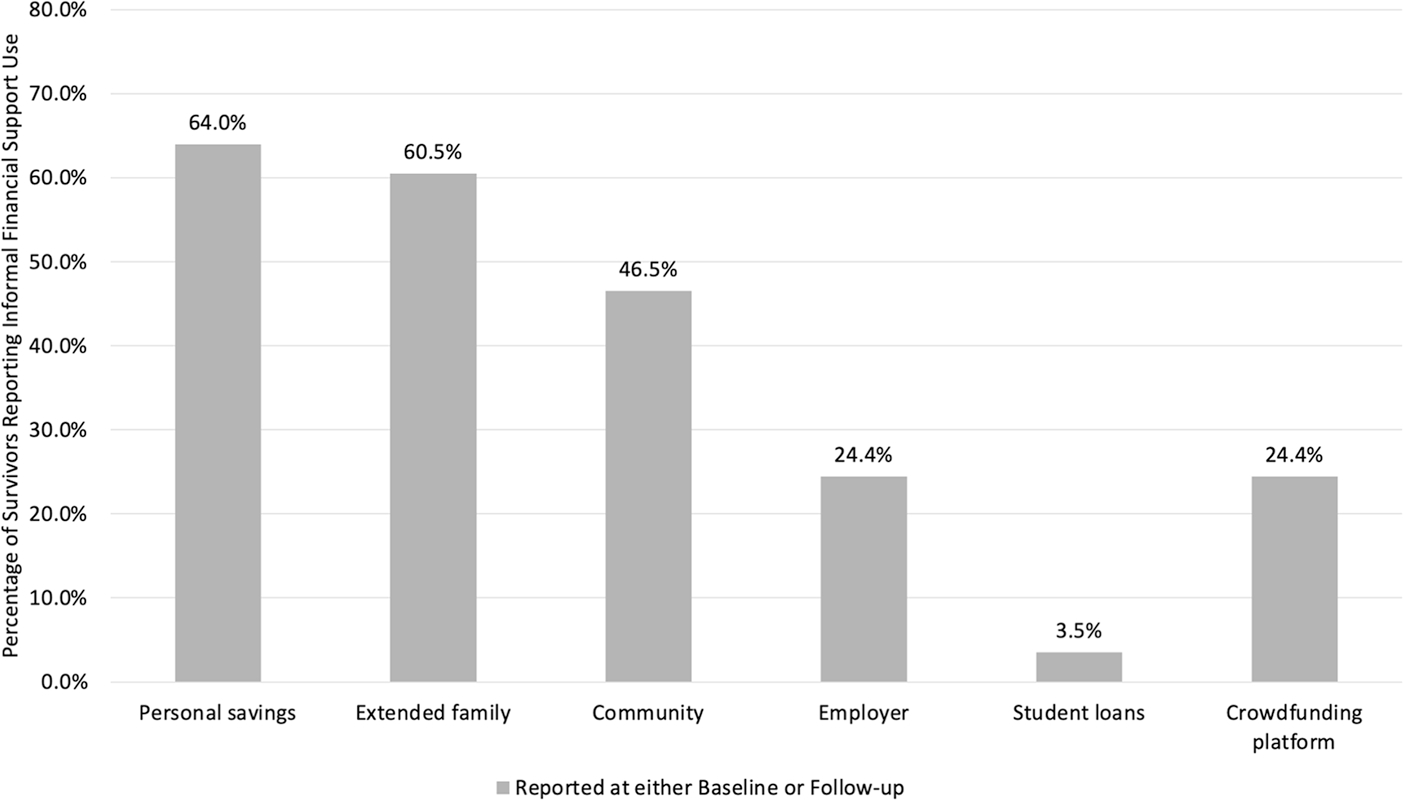

These sources were convergent with sources reported in the survey (Fig. 2), with participants reporting a high frequency of financial support from extended family (n = 52, 60.5%) and community members and organizations such as churches (n = 40, 46.5%).

Fig. 2.

Informal financial support sources among adolescent and young adult cancer survivors

Footnote: Estimates from AYA participants in a randomized controlled trial self-reporting informal financial support at either baseline or follow-up (n=86). Examples of types of informal support: Community – church, neighborhood; Employer – schedule flexibility, disability; Crowfunding platform – GoFundMe

Interview participants also reported receiving financial support directly from their employer, crowdfunding sites, and fundraisers run by family and friends. Most participants reported receiving support from multiple sources.

“I had a friend that did a really successful fundraiser through a website. I couldn’t tell you what it was, but she made t-shirts. She was able to have them design t-shirts. And so, she sold the t-shirts through their website and then the funds went to me.”

“I also got financial support from my friends and my family on GoFundMe.”

The qualitative findings were convergent with the survey findings in that support from patients’ employer and support from crowdfunding sites was reported by 21 AYAs (24.4%; Fig. 2). Fourteen of the 21 AYAs who reported receiving support from a crowdfunding site shared the dollar amount raised, which averaged $10,335 (range: $700–$30,000); not shown in tables/figures).

Sufficiency of Informal Financial Support

Sufficiency from informal financial support—that is, receiving enough financial protection—varied greatly across interview participants. Roughly half of participants perceived that their support was sufficient when combining informal sources with other existing income. A few participants, particularly ones who used crowdfunding sites, reported the support they received exceeded what they needed financially.

“Yeah. They were beyond sufficient for us.” “Up to this point, it’s covered all of it (treatment and living expenses).”

Other participants, nearly half, reported the financial support they received to be insufficient in addressing the high cost of cancer treatment. In particular, those who perceived their out-of-pocket costs to be high reported insufficiency.

“Yeah. I feel like more so, they (financial supports) helped with just living expenses, any extra things that I needed on top of what my bills were for hospital treatments.”

“So, we had a deductible, and I think the fundraising money met about half of my deductible.”

Association of financial toxicity and demographic characteristics with informal financial support

Low COST scores (indicating high financial toxicity) were associated with accessing personal savings (80.9% high toxicity vs. 45.7% low toxicity; p-value = 0.002), and receiving money from extended family (76.6% vs. 37.1%; p-value < 0.001), community (57.5% vs. 31.4%; p-value = 0.02), and/or crowdfunding (34.0% vs. 11.4%; p-value = 0.02, Table 2). Household income was associated with extended family, community, and crowdfunding financial support sources. Older age was associated with a higher proportion of participants accessing financial support through an employer (32.1% vs. 10.0%; p-value = 0.02). Gender was not associated with use of any informal financial support sources.

Table 2.

Difference in sources of informal financial support by financial toxicity, household income, age, and gender among adolescent and young adult cancer survivors

| Personal savings | Extended family | Community | Through my employer | My student loans | Crowdfunding | |

|---|---|---|---|---|---|---|

| N (%) | N (%) | N (%) | N (%) | N (%) | N (%) | |

|

| ||||||

| COST score | ||||||

| High financial toxicity | 38 (80.9)* | 36 (76.6)* | 27 (57.5)* | 11 (23.4) | 3 (6.4) | 16 (34.0)* |

| Low financial toxicity | 16 (45.7)* | 13 (37.1)* | 11 (31.4)* | 8 (22.9) | 0 (0.0) | 4 (11.4)* |

| Household income | ||||||

| < $10,000 | 5 (50.0) | 8 (80.0)* | 2 (20.0)* | 3 (30.0) | 0 (0.0) | 1 (10.0)* |

| $10,000-$39,000 | 12 (80.0) | 12 (80.0)* | 9 (60.0)* | 5 (33.3) | 1 (6.7) | 2 (13.3)* |

| $40,000-$79,000 | 14 (77.8) | 15 (83.3)* | 12 (66.7)* | 3 (16.7) | 2 (11.1) | 10 (55.6)* |

| $80,000 + | 15 (51.7) | 9 (31.0)* | 10 (34.5)* | 7 (24.1) | 0 (0.0) | 5(17.2)* |

| Age at participation | ||||||

| Younger AYA | 16 (53.3) | 21 (70.0) | 13 (43.3) | 3 (10.0)* | 1 (3.3) | 5 (16.7) |

| Older AYA | 39 (69.6) | 31 (55.4) | 27 (48.2) | 18 (32.1)* | 2 (3.6) | 16 (28.6) |

| Gender | ||||||

| Male | 16 (59.3) | 16 (59.3) | 12 (44.4) | 7 (25.9) | 1 (3.7) | 4 (14.8) |

| Female | 39 (66.1) | 36 (61.0) | 28 (47.5) | 14 (23.7) | 2 (3.4) | 17 (28.8) |

Data shown reflect the N = 86 RCT sample. Frequency of source of financial support reported with row percentages

COST score Comprehensive Score for financial Toxicity, a 11-item validated measure of cancer-related financial toxicity

Chi-squared or Fisher’s exact tests were used; astericks indicate statistical significance at p < 0.05

Frequencies for survivors who used each source of financial support are displayed and compared against those who did not (column not shown)

In Table 3, high financial toxicity was associated with use of a greater number of financial support sources (p-value < 0.001). Participants who reported accessing three or more sources of financial support were more likely to also report high financial toxicity, while those who reported no sources of informal financial support sources were more likely to report low financial toxicity. There were patterns in the number of financial support sources across income; a significantly higher proportion of participants using 3 + financial support sources were in the $40,000–$79,000 or middle-high income category (35.9%) while those in the lowest income category used 3 + financial support sources the least (15.4%). However, most survivors who used 1–2 financial support sources earned $80,000 + a year, the highest income category (p-value = 0.05).

Table 3.

Difference in the number of informal financial support sources by financial toxicity, household income, age, and gender among adolescent and young adult cancer survivors

| Number of financial support sources | ||||

|---|---|---|---|---|

|

|

|

|||

| 0 support sources | 1–2 support sources | 3 + support sources | p-value | |

|

|

||||

| N (%) | N (%) | N (%) | ||

|

| ||||

| COST score | ||||

| High financial toxicity | 2 (20.0) | 17 (47.2) | 28 (77.8) | 0.001* |

| Low financial toxicity | 8 (80.0) | 19 (52.8) | 8 (22.2) | |

| Household income | ||||

| < $10,000 | 1 (12.5) | 5 (15.6) | 4 (12.5) | 0.05 |

| $10,000-$39,000 | 0 (0.0) | 6 (18.8) | 9 (28.1) | |

| $40,000-$79,000 | 1 (12.5) | 5 (15.6) | 12 (37.5) | |

| $80,000 + | 6 (75.0) | 16 (50.0) | 7 (21.9) | |

| Age at participation | ||||

| Younger AYA | 4 (40.0) | 15 (39.5) | 11 (29.0) | 0.68 |

| Older AYA | 6 (60.0) | 23 (60.5) | 27 (71.0) | |

| Gender | ||||

| Male | 3 (30.0) | 13 (34.2) | 11 (29.0) | 0.95 |

| Female | 7 (70.0) | 25 (65.8) | 27 (71.0) | |

Data shown reflect the N = 86 RCT sample. Frequency of number of sources of financial support reported with column percentages

COST score Comprehensive Score for financial Toxicity, a 11-item validated measure of cancer-related financial toxicity

Fisher’s exact tests were used; astericks indicate statistical significance at p < 0.05

Discussion

AYA cancer survivors often face substantial and long-lasting financial repercussions due to the high cost of cancer care at a time of life when financial stability is tenuous for many [27]. While the economic consequences of cancer-related financial toxicity have been extensively studied, how AYA survivors pay for their medical care has not. Our novel findings describe the informal financial support sources that AYA survivors use to pay for their treatment costs and living expenses including taking money out of savings and receiving financial support from extended family, community, employers, and crowdfunding sites. While our results demonstrate that high financial toxicity, household income, and age at participation were associated with using sources of informal financial support, half of interview participants reported the financial support they received was insufficient to cover their costs.

Participants with a household income of $40,000–$79,000 reported the highest proportion of informal financial support use, higher even than lower income participants ($10,000–$39,000 and < $10,000). While low income is associated with financial toxicity among cancer survivors [22, 23], the lowest income participants in our sample used informal financial support less frequently. One possible explanation is that individuals in the lowest income bracket may not have access to wealth via their social networks like higher income survivors do. The literature on economic instability and social stratification suggests economic instability in times of adverse events can be overcome with household or network financial support, which is less available in lower income populations, further driving inequity [28]. Thus, this finding suggests that high out-of-pocket costs experienced by the lowest income AYA cancer survivors may be particularly devastating if they do not have the direct income to cover these costs and at the same time are not able to access informal financial support sources.

Crowdfunding is an increasingly common tool used by AYA cancer patients to meet their cancer costs and living expenses, yet the feasibility of crowdfunding as a reliable and equitable way to alleviate cancer-related financial toxicity is questionable. Our findings of crowdfunding differences by income are consistent with findings from AYA’s who describe their crowdfunding success as hinging on their social network wealth [29]. Furthermore, a recent study suggested that cancer crowdfunding success is low among cancer survivors in low-socioeconomic status areas [30]. Taken together, cancer survivors with low incomes who seek to alleviate financial toxicity through crowdfunding may not have equitable access to communities with enough disposable income to provide them with informal financial support. Expecting low-income survivors to find wealth within their impoverished social networks is unrealistic [28]. Further research is needed to fully conceptualize how survivors with limited resources access and use crowdfunding to pay for their cancer and living expenses during and after treatment.

Interventions that can increase AYA cancer survivors’ access to formal and informal financial support may help relieve cancer-related financial burden. For instance, financial navigation is a commonly recommended intervention to address financial toxicity experienced by cancer survivors. While few trials of financial navigation have been completed, preliminary findings suggest that it may increase survivors’ access to financial resources or formal financial support and may reduce financial burden [31]. However, financial navigation to date is limited to formal financial support sources, such as charity care or foundation grants [31]. The drawbacks and benefits of including informal financial supports in financial navigation are unknown but may be beneficial. For example, the integration of a crowdfunding “how to” toolkit may assist survivors from low-income or low digital literacy backgrounds in understanding how to access financial support via crowdfunding, although the merits of this approach are unstudied. Furthermore, expanding current financial aid programs within cancer centers and community organizations to include a more holistic view of survivors’ financial toxicity and available financial supports may be beneficial.

One specific instance of how to integrate informal financial supports into cancer center supportive services is social network mapping [32]. Social network mapping interventions are feasible tools for helping cancer caregivers conceptualize and activate social support resources in their social networks, and this includes instrumental support (e.g., financial support) [32]. Mapping of informal financial support sources in addition to formal financial support sources may allow young survivors and caregivers to prioritize seeking financial support through specific resource rich networks or to focus more heavily on formal sources such as foundation grants and manufacturer assistance. Furthermore, AYA organizations who often provide financial support via grants could increase the equity of their funds by using a portion of funds to support cancer crowdfunding campaigns that originate from socially vulnerable areas of the United States.

While household income and financial toxicity were associated with similar financial support sources (i.e., support from extended family, community, and crowdfunding), participants with high financial toxicity were more likely to access personal savings in addition to family, community, and crowdfunding financial support sources. This finding suggests that perceived financial toxicity should be used in conjunction with income when considering allocation of funds via formal financial support (e.g., grants). Furthermore, older AYAs were more likely to access financial support through their employer than younger AYAs. This is potentially because younger AYAs may still be finishing college and vocational training and may not yet have secured benefitted employment.

Limitations

Our study has limitations. First, all participants had health insurance, due to the eligibility criteria of the RCT, which is to educate AYAs on how to use their health insurance. However, our findings still suggest that there is substantial financial toxicity among insured AYAs. Our sample is primarily white and from the mountain west region of the United States limiting our generalizability. Next steps should compare and work to conceptualize informal financial support among other economically instable cancer survivor populations.

Conclusions

Cancer-induced financial toxicity is a well-established and studied phenomenon among AYA cancer survivors [11, 27]. However, how AYAs access informal financial support and from where is largely unstudied. AYAs reported receiving financial support from a variety of sources including personal savings, communities including churches, family (extended and immediate) and friends, employers and coworkers, and fundraisers and crowdfunding sites. However, only 50% of interview participants reported that the informal financial support they received was sufficient to meet their needs. High financial toxicity was associated with the most types of informal financial support use as well as a higher number of informal financial supports used in comparison to low financial toxicity. Income was less clearly associated with informal financial support types with the lowest income group accessing informal financial supports less frequently than higher income groups. Our study highlights that AYA survivors who experience financial toxicity often turn to informal sources of financial support to supplement paying for their living and cancer-related expenses. However, the most atrisk, low-income survivors may not have access to wealth in their social network limiting their ability to lessen their burden via informal financial support—widening inequities.

Supplementary Material

Funding

Funding for this project was awarded by the United States National Institute of Health (NIH). The grant/contract award number is R01CA242729 (PI Kirchhoff). Research reported in this publication utilized the Research Informatics Shared Resource at Huntsman Cancer Institute at the University of Utah and was supported by the National Cancer Institute of the National Institutes of Health under Award Number P30CA042014. The content is solely the responsibility of the authors and does not necessarily represent the official views of the NIH.

Footnotes

Conflict of interest The authors declare no competing interests.

Supplementary Information The online version contains supplementary material available at https://doi.org/10.1007/s00520-023-07626-5.

Ethics approval All study procedures were approved by the University of Utah IRB (IRB_00091443 and IRB_00127029).

Consent to participate Informed consent was obtained from all individual participants included in the study.

Consent for publication Not applicable. All data presented in this manuscript are de-identified.

Data Availability

The datasets generated during and/or analysed during the current study may be available from the corresponding author on reasonable request.

References

- 1.The American Cancer Society Cancer Action Network. Survivor views: cancer & medical debt. 2022. 10/03/2022]. https://www.fightcancer.org/sites/default/files/national_documents/survivor_views_cancer_debt_0.pdf.

- 2.Collins SR, Bhupal HK, Doty MM (2019) Health insurance coverage eight years after the ACA. The Commonwealth Fund, New York, NY. https://www.commonwealthfund.org/publications/issue-briefs/2019/feb/health-insurance-coverage-eight-years-after-aca. Accessed 30 Sep 2022 [Google Scholar]

- 3.Yabroff KR et al. (2021) Annual report to the nation on the status of cancer, part 2: patient economic burden associated with cancer care. JNCI J Natl Cancer Inst 113(12):1670–1682 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Fair D et al. (2021) Material, behavioral, and psychological financial hardship among survivors of childhood cancer in the Childhood Cancer Survivor Study. Cancer 127(17):3214–3222 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Zullig LL et al. (2013) Financial distress, use of cost-coping strategies, and adherence to prescription medication among patients with cancer. J Oncol Pract 9(6S):60s–63s [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Pangestu S, Rencz F (2022) Comprehensive score for financial toxicity and health-related quality of life in patients with cancer and survivors: a systematic review and meta-analysis. Value Health : J Int Soc Pharmacoeconomics Outcomes Res S1098–3015(22):02137–4 [DOI] [PubMed] [Google Scholar]

- 7.Salsman JM et al. (2019) Understanding, measuring, and addressing the financial impact of cancer on adolescents and young adults. Pediatr Blood Cancer 66(7):e27660. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Arnett JJ (2000) Emerging adulthood: a theory of development from the late teens through the twenties. Am Psychol 55(5):469. [PubMed] [Google Scholar]

- 9.Arnett JJ (2003) Conceptions of the transition to adulthood among emerging adults in American ethnic groups. New Dir Child Adolesc Dev 2003(100):63–76 [DOI] [PubMed] [Google Scholar]

- 10.Close AG et al. (2019) Adolescent and young adult oncology—past, present, and future. CA: A Cancer J Clin 69(6):485–496 [DOI] [PubMed] [Google Scholar]

- 11.Kirchhoff A, Jones S (2021) Financial toxicity in adolescent and young adult cancer survivors: proposed directions for future research. JNCI: J Natl Cancer Inst 113(8):948–950 [DOI] [PubMed] [Google Scholar]

- 12.Meernik C et al. (2021) Material and psychological financial hardship related to employment disruption among female adolescent and young adult cancer survivors. Cancer 127(1):137–148 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Zhu Z et al. (2020) Cancer survivors’ experiences with financial toxicity: a systematic review and meta-synthesis of qualitative studies. Psychooncol 29(6):945–959 [DOI] [PubMed] [Google Scholar]

- 14.Altice CK et al. (2016) Financial hardships experienced by cancer survivors: a systematic review. J Natl Cancer Ins 109(2):djw205. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15.Mann K et al. (2022) HIAYA CHAT study protocol: a randomized controlled trial of a health insurance education intervention for newly diagnosed adolescent and young adult cancer patients. Trials 23:682. 10.1186/s13063-022-06590-5 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Saunders B et al. (2018) Saturation in qualitative research: exploring its conceptualization and operationalization. Qual Quant 52(4):1893–1907 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.Guest G, Bunce A, Johnson L (2006) How many interviews are enough? An experiment with data saturation and variability. Field Methods 18(1):59–82 [Google Scholar]

- 18.Saldaña J (2021) The coding manual for qualitative researchers. Sage publications [Google Scholar]

- 19.Creswell JW, and Poth CN (2016) Qualitative inquiry and research design: choosing among five approaches. Sage publications [Google Scholar]

- 20.de Souza JA et al. (2017) Measuring financial toxicity as a clinically relevant patient-reported outcome: the validation of the COmprehensive Score for financial Toxicity (COST). Cancer 123(3):476–484 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Kim HY (2016) Statistical notes for clinical researchers: sample size calculation 2. Comparison of two independent proportions. Restor Dent Endod 41(2):154–6 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22.Yabroff KR, Bradley C, Shih Y-CT (2020) Understanding financial hardship among cancer survivors in the United States: strategies for prevention and mitigation. J Clin Oncol : Off J Am Soc Clin Oncol 38(4):292–301 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Gordon LG et al. (2017) A systematic review of financial toxicity among cancer survivors: we can’t pay the co-pay. Patient – Patient-Centered Outcomes Res 10(3):295–309 [DOI] [PubMed] [Google Scholar]

- 24.Warner EL, Millar MM, Orleans B, Edwards SL, Carter ME, Vaca Lopez PL, Sweeney C, Kirchhoff AC (2022) Cancer survivors’ financial hardship and their caregivers’ employment: results from a statewide survey. J Cancer Surviv. 10.1007/s11764-022-01203-1 [DOI] [PubMed] [Google Scholar]

- 25.Fetters MD, Curry LA, Creswell JW (2013) Achieving integration in mixed methods designs-principles and practices. Health Serv Res 48(6 Pt 2):2134–2156 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 26.Creswell JW, Clark VL (2017) Designing and conducting mixed methods research. SAGE Publications, Inc, Thousand Oaks, CA [Google Scholar]

- 27.Danhauer SC, Canzona M, Tucker-Seeley RD, Reeve BB, Nightingale CL, Howard DS, Puccinelli-Ortega N, Little-Greene D, Salsman JM (2022) Stakeholder-informed conceptual framework for financial burden among adolescents and young adults with cancer. Psychooncology 31(4):597–605. 10.1002/pon.5843 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 28.Western B et al. (2012) Economic insecurity and social stratification. Ann Rev Sociol 38(1):341–359 [Google Scholar]

- 29.Ghazal LV, Watson SE, Gentry B, Santacroce SJ (2022) “Both a life saver and totally shameful”: young adult cancer survivors’ perceptions of medical crowdfunding. J Cancer Surviv. 10.1007/s11764-022-01188-x [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30.Silver ER et al. (2020) Association of neighborhood deprivation index with success in cancer care crowdfunding. JAMA Netw Open 3(12):e2026946–e2026946 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Doherty MJ, Thom B, Gany F (2021) Evidence of the feasibility and preliminary efficacy of oncology financial navigation: a scoping review. Cancer Epidemiol Biomark Prev 30(10):1778–1784 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Reblin M, McCormick R, Mansfield KJ, Wawrzynski SE, Ketcher D, Tennant KE, Guo JW, Jones EC, Cloyes KG (2022) Feasibility, usability, and acceptability of personalized web-based assessment of social network and daily social support interactions over time. J Cancer Surviv 16(4):904–912. 10.1007/s11764-021-01083-x [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Data Availability Statement

The datasets generated during and/or analysed during the current study may be available from the corresponding author on reasonable request.