Abstract

This study includes a scoping review of prior studies investigating the effects of policy changes on child poverty rates. It further conducts an empirical analysis to estimate the relationship between child poverty rates and child maltreatment report (CMR) rates, utilizing national county-level data. The study then calculates the indirect effects of policy changes on CMR rates, mediated through child poverty rates, by integrating information from previous studies with its own empirical findings. Among the policy changes explored in prior studies, those related to a child allowance and a fully refundable Child Tax Credit demonstrate the largest indirect effects but also the highest costs. The expansion of in-kinds and near-cash benefits, such as the Supplemental Nutrition Assistance Program benefits and housing vouchers, shows moderate effects with moderate costs. Tax credits like the Earned Income Tax Credit exhibit lower effects and costs when targeted at the lowest earners, and moderate effects and costs for broader expansion. Focused tax credits, such as the Child and Dependent Care Tax Credit, had lower effects and costs, even if made fully refundable. Despite certain limitations, the study’s approach yields consistent estimates with a recent simulation study, indicating its potential validity. While some proposed policy changes may seem expensive, implementing them is anticipated to substantially reduce CMR rates, with the benefits outweighing the associated costs. Overall, the findings suggest that addressing child poverty to reduce CMRs is an attractive strategy with numerous potential benefits.

1. Introduction

Child maltreatment, such as neglect, physical abuse, sexual abuse, and emotional abuse, is a significant social problem. It is projected that over one in three U.S. children will be reported to and investigated by child protective services for child maltreatment concerns at least once during childhood (Kim et al., 2017). Research has shown that child maltreatment is associated with a wide range of negative outcomes, including health, social, behavioral, cognitive, academic, and economic problems, which persist from childhood into adulthood (World Health Organization, n.d.). Consequently, the societal burden of child maltreatment is accordingly high in the United States (Fang et al., 2012; Peterson et al., 2018). In order to contribute to the prevention of child maltreatment incidents and reports, our aim is to provide quick preliminary estimates of the indirect effects of policy changes on child maltreatment report (CMR) rates, mediating through child poverty rates.

1.1. Poverty and Child Maltreatment

Poverty has long been identified as one of the most influential risk factors for incidents and reporting of child maltreatment (Drake et al., 2022; Pelton, 2015). Children living in impoverished conditions face a significantly elevated risk of encountering incidents of child maltreatment and being reported, in comparison to those not experiencing poverty (Irwin, 2009; Sedlak et al., 2010). Moreover, communities with higher poverty rates demonstrate increased rates of child maltreatment incidents and reports across various community levels, encompassing census tracts, zip codes, and counties (Coulton et al., 2007; Kim & Drake, 2018).

Multiple theoretical foundations support the pathways from poverty to child maltreatment at the individual level. First, even though state laws and policies generally do not define the inability to provide care for a child solely due to poverty as a form of child maltreatment (Child Welfare Information Gateway, 2022), poverty can significantly limit the resources and choices available to economically disadvantaged parents, potentially increasing the likelihood of inadequate care and neglect for their children (Berger, 2004; Drake et al., 2022; Pelton, 2015). Second, in contrast to families unaffected by financial hardships, economically disadvantaged families often confront more health and safety hazards stemming from substandard housing conditions. As a result, they may need to be more vigilant in ensuring their children’s safety, which could add to the burden of supervision and consequently raise the risk of neglect (Berger, 2004; Drake et al., 2022; Pelton, 2015). Third, parents facing poverty might lean towards non-monetary approaches, like physical discipline, to manage their children’s behavior due to financial limitations (Weinberg, 2001). This inclination could potentially result in a higher propensity for physical abuse compared to parents not facing financial constraints. Fourth, as per stress theory, stress serves as an intermediary mechanism influencing both the impacts of poverty on neglect and physical abuse. Under circumstances marked by heightened stress due to financial difficulties, parents might temporarily disengage from their caregiving role due to feelings of depression (Garbarino, 1977; Pelton, 2015). Consequently, parents under such stress might be more prone to neglecting their children. Additionally, regarding physical and emotional abuse, even minor provocations from children can quickly trigger anger in financially strained parents dealing with high levels of stress (Pelton, 1978, 2015), potentially leading to abusive behaviors. Finally, in the context sexual abuse, poverty might impede the capacity of potential perpetrators to engage in socially sanctioned methods of fulfilling their sexual desires (Finkelhor, 1999). It is also plausible that poverty and single parenthood could intensify the challenge of supervising children and safeguarding them from possible perpetrators (Finkelhor, 1999). Furthermore, there is a notion that poverty could subject children to emotional strain, potentially diminishing their capability to resist potential perpetrators (Finkelhor, 1999).

There have been two distinct approaches in elucidating the impact of community conditions on child maltreatment (Coulton et al., 2007). The first approach, led by psychologists, focuses on child and family development and extends this perspective to interactions between children, families, and their surroundings (Belsky, 1980; Cicchetti & Lynch, 1993; Garbarino, 1977). From a psychological outlook, the accumulation of disadvantages, including community poverty, could augment stress on families, thereby elevating the risk of child maltreatment (Belsky, 1980; Cicchetti & Lynch, 1993; Garbarino, 1977). The second approach, led by sociologists, emphasizes sociological dynamics inherent in communities, such as social disorganization and collective efficacy (Sampson et al., 1999). According to this sociological perspective, community poverty might hinder the collaborative efforts for the well-being of community children due to the isolation of residents from essential resources, limited access to job opportunities, economic dependency, uncertainty, and fear of unfamiliar individuals (Sampson et al., 1999).

In addition to these theoretical explanations, a growing body of evidence, including some causal findings, suggests that reducing child poverty offers a viable avenue for decreasing incidents and reporting of child maltreatment (Berger et al., 2017; Cancian et al., 2013; Pac et al., 2023; Pelton, 2015).

1.2. Policies to Reduce Poverty

Almost one in six U.S. children were living in poverty in 2021 (U.S. Census Bureau, 2022). The consensus study report by the National Academies of Sciences, titled “A Roadmap to Reducing Child Poverty”, introduced policy packages aimed at halving child poverty within the next decade (National Academies of Sciences, 2019). Through policy simulations, the report identified five key policies—Earned Income Tax Credit (EITC), Child and Dependent Care Tax Credit (CDCTC), child allowance, Supplemental Nutrition Assistance Program (SNAP), and housing voucher—that, when modified (e.g., expanding benefits), could reduce child poverty by at least one percentage point. Our primary focus centers on these policies. Moreover, we underscore the Child Tax Credit (CTC), as the report proposes its substitution with a child allowance program. Furthermore, our emphasis is directed towards the impact of policy adjustments, rather than merely the existence of a policy. This approach is aimed at informing the enhancement of existing policies. To facilitate the interpretation of our findings, comprehensive descriptions of these policies are furnished in the Results section.

1.3. Current Study

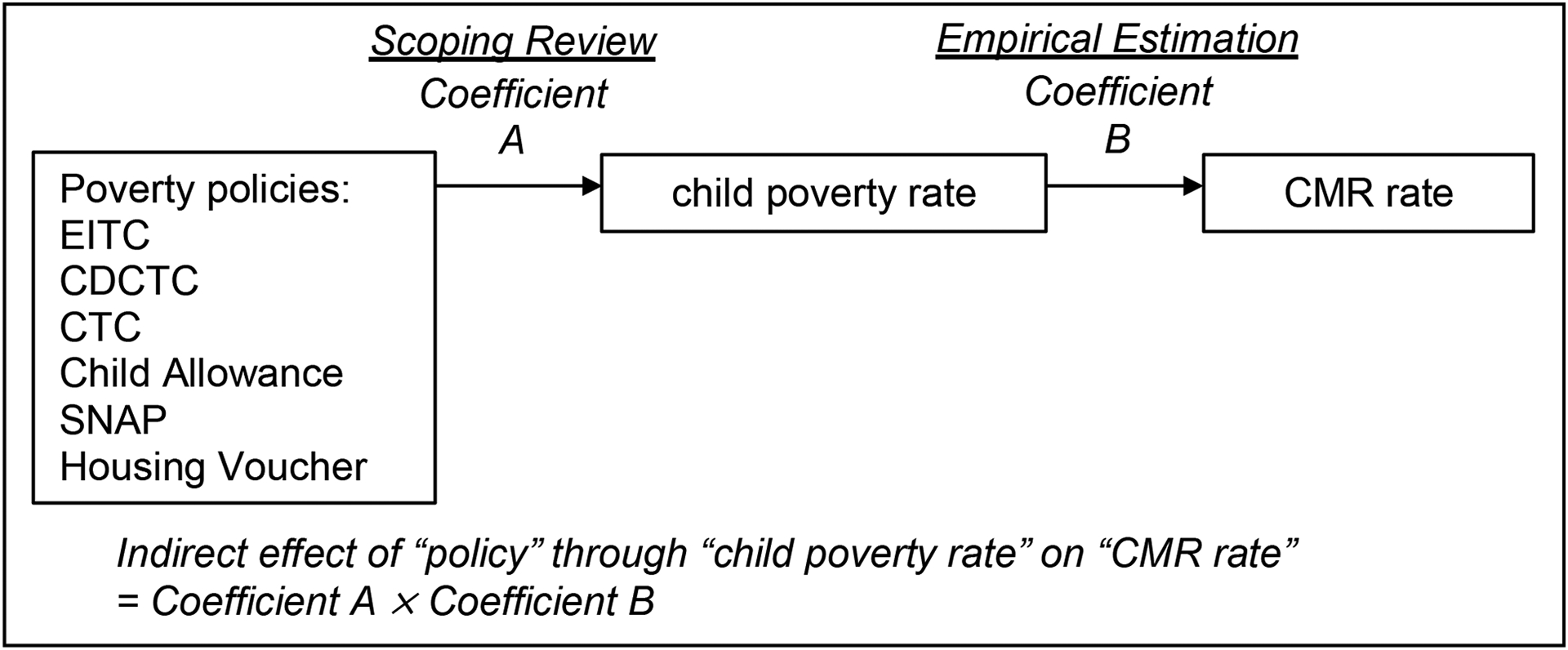

Our aim is to swiftly provide preliminary estimates for the indirect effects of policy changes through child poverty rates on CMR rates. In this study, we use the term “indirect effect” to describe and quantify the mediating effect of a policy change on the CMR rate, conveyed through the child poverty rate. In other words, when a policy change leads to a reduction in the child poverty rate, it subsequently contributes to a decrease in the CMR rate. This indirect effect can be readily calculated by multiplying the effect of a policy change on the poverty rate with the effect of the poverty rate on the CMR rate (Preacher & Selig, 2012).

To achieve our aim, we will undertake the following steps. First, we will conduct a scoping review of previous studies examining the effects of policy changes on child poverty rates. Specifically, we will review studies investigating the impacts of EITC, CDCTC, CTC, child allowance, SNAP, and housing voucher on child poverty rates. From the reviewed studies, we will extract the coefficient (Coefficient A in Figure 1) that represents the effect of a policy change (e.g., CTC expansion) on child poverty rates. Second, utilizing national data, we will empirically estimate the coefficient (Coefficient B in Figure 1) that capture the county-level relationship between child poverty rates and CMR rates. Finally, we will compute the indirect effect of a policy change (e.g., CTC expansion) on CMR rates, mediating through child poverty rates, by multiplying “Coefficient A” and “Coefficient B” (i.e., indicate effect = A × B).

Figure 1.

Conceptual model.

Note. EITC = Earned Income Tax Credit. CDCTC = Child and Dependent Care Tax Credit. CTC = Child Tax Credit. SNAP = Supplemental Nutrition Assistance Program. CMR = child maltreatment report.

It is worth noting that our approach has inherent limitations and is not sufficient for establishing causal relationships between policy changes, child poverty rates, and CMR rates. We acknowledge that we make bold assumptions regarding causality in order to provide preliminary estimates of possible indirect effects. The strength of causal evidence for the coefficients between policy changes and child poverty rates (Coefficient A) relies on the quality of prior studies included in our scoping review. While estimating the coefficients between child poverty rates and CMR rates (Coefficient B), we will take into account known risk factors such as care burden, residential instability, and demographic factors. However, it is important to recognize that this approach is correctional in nature. The estimated coefficients will not solely represent net impacts, as there may be confounding factors (e.g., substance abuse rates) that are either unavailable or unknown. We used causal terms (e.g., effect) not to claim causality, but to describe coefficients and possible effects under our bold assumptions. Despite these limitations, our estimates will be based on the best available evidence and can serve as a valuable guide for future rigorous investigations into the effects of policy changes on CMRs.

2. Methods

2.1. Effects of Policy Changes on Child Poverty (Coefficient A)

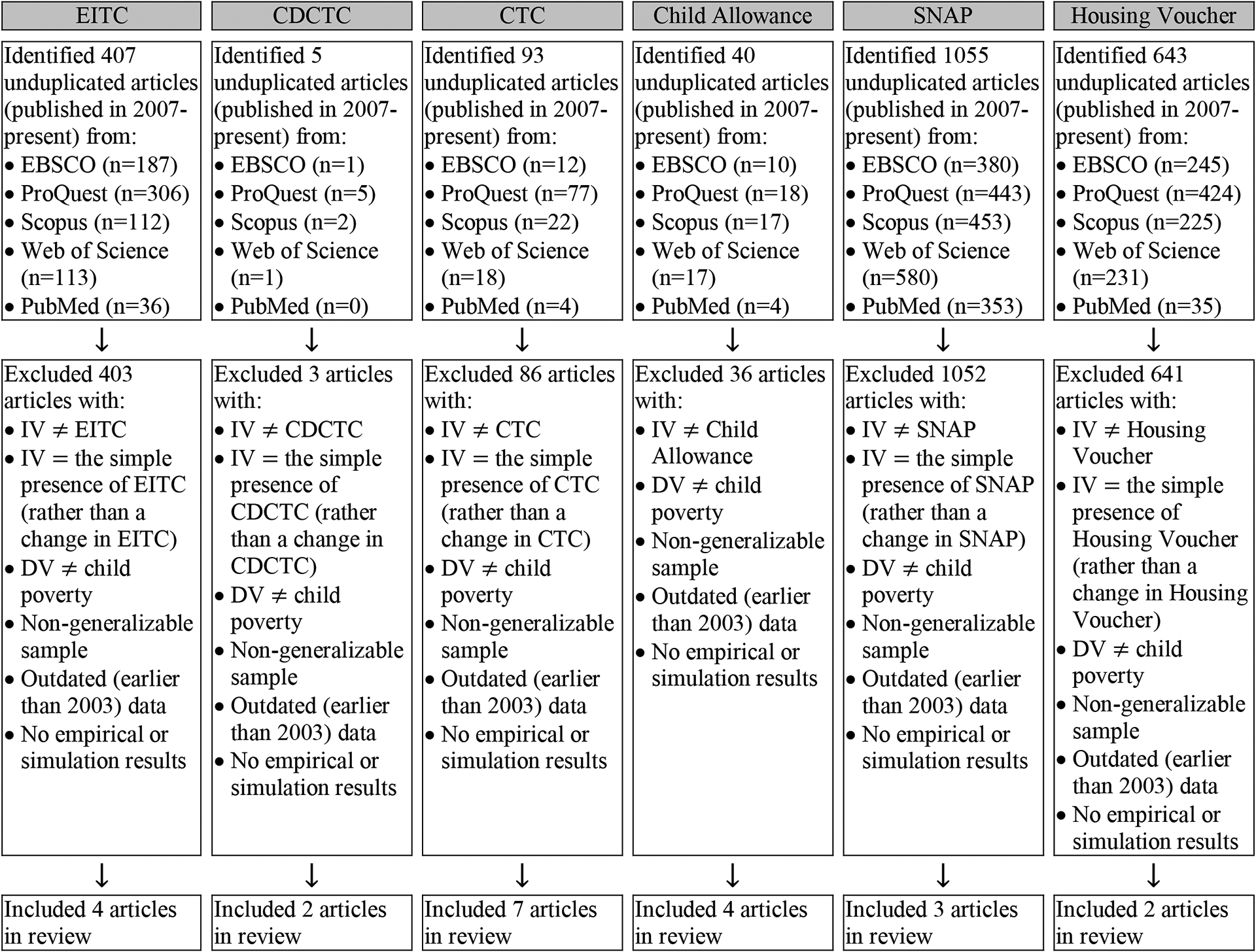

To obtain the coefficients of policy changes on child poverty rates from prior studies, we conducted a scoping review following the PRISMA 2020 guideline (Page et al., 2021). Our search approach involved using specific policy names (e.g., “child allowance”) and the keyword “poverty” in our search terms. Additionally, we incorporated search terms such as “national,” “states,” “county,” “tract,” or “community” to identify studies conducted at either national individual-level or national area-level. The complete list of search terms can be found in Supplement Table S1. To ensure comprehensive coverage, our search encompassed multiple databases and collections, including EBSCO, ProQuest, Scopus, Web of Science, and PubMed. In order to include recent findings, we limited our search to studies published from 2007 onward. The final search was conducted in June 2023.

Figure 2 presents the results of our search. From the initial search, we identified 407 articles on EITC, 5 articles on CDCTC, 93 articles on CTC, 40 articles on child allowance, 1,055 articles on SNAP, and 643 articles on housing voucher. We applied the following criteria to exclude articles: (1) the independent variable did not pertain to any of the six policies of interest; (2) the independent variable solely focused on the presence of a policy without examining changes to the policy; (3) the dependent variable did not involve child poverty; (4) the samples/estimates did not represent the entire United States; (5) the studies used outdated data earlier than 2003; or (6) the article did not present empirical or simulation results. Studies that solely examined the presence of a policy (i.e., projecting the increased level of poverty if a current policy did not exist) were excluded due to their limited implications for improving current policies. However, an exception was made for child allowance, where studies examining the presence of a child allowance program were included, considering that the United States currently does not have a child allowance program in place. Our search and review encompassed a wide range of academic sources, including academic journal articles, dissertations/theses, books, government and official publications, reports, and working papers. At least two authors participated in the screening process for the articles identified in the initial search, and the decision to include or exclude an article in our review was reached through unanimous agreement. Any disagreements were resolved through discussion. Ultimately, our review included 4 articles on EITC, 2 articles on CDCTC, 7 articles on CTC, 4 articles on child allowance, 3 articles on SNAP, and 2 articles on housing voucher (Table 1). All of these studies utilized simulations on data from the U.S. Census Current Population Survey, employing the Urban Institute’s Transfer Income Model—an extensive microsimulation model aimed as simulating key governmental programs pertaining to taxes, transfers, and healthcare that have an impact on the population of the United States (Urban Institute, n.d.).

Figure 2.

Search Process.

Note. EITC = Earned Income Tax Credit. CDCTC = Child and Dependent Care Tax Credit. CTC = Child Tax Credit. SNAP = Supplemental Nutrition Assistance Program. IV = independent variable. DV = dependent variable.

Table 1.

Studies on the Impacts of Policies on the Child Poverty Rate (CPR).

| Citation; Data; Design | Independent Variable (IV) | Dependent Variable | Results |

|---|---|---|---|

| Earned Income Tax Credit (EITC) | |||

| Giannarelli et al. (2007); 2004 CPS ASEC; Simulation | IV: expanding EITC for childless workers (increasing the credit rate from 7.65% to 20%), reducing marriage penalties (excluding 50% of a lower-earning spouse’ earnings if it would increase EITC), and increasing EITC for families with three or more children (increasing the phase-in rate from 40% to 45%) | CPR: including income, food stamps, housing subsidy, taxes, EITC, and child care expenses | IV reduced CPR from 14.4% to 13.9% (0.5 pp or 3.7% reduction); cost: $22.2B |

| Lippold (2015); 2010 CPS ASEC; Simulation | IV: expanding EITC (e.g., increasing the phase-in rate from 7.65% to 50% for married couples with no child, 34% to 70% for those with one child, 40% to 90% for those with two children, 45% to 110% for those with three children, and 45% to 130% for those with four or more children) | CPR: SPM | IV reduced CPR from 15.6% to 12.3% (3.3 pp or 22.3% reduction); cost: $182.5B |

| National Academies of Sciences (2019); 2016 CPS ASEC; Simulation | IV1: Raising EITC benefits for the lowest earners (raising benefits in the EITC phase-in and flat ranges) IV2: Raising the overall generosity of EITC benefits (raising benefits by 40% across the EITC schedule) |

CPR: SPM | IV1 reduced CPR from 13.0% to 11.8% (1.2 pp or 9.2% reduction); cost: $8.4B IV2 reduced CPR from 13.0% to 10.9% (2.1 pp or 16.2% reduction); cost: 20.2B |

| Pac et al. (2020); 2010–2012 CPS ASEC; Simulation | IV: all states provide EITC as the most generous state does (the receipt rate increased from 13% to 37% nationally; state EITC increased to 43% of the federal EITC) | CPR: SPM, including taxes, tax credits, and cash/in-kind benefits | IV reduced CPR from 14.2% to 13.0% (1.2 pp or 8.5% reduction); cost: not available |

| Child and Dependent Care Tax Credit (CDCTC) | |||

| Giannarelli et al. (2007); 2004 CPS ASEC; Simulation | IV: expanding child care subsidies (e.g., raising the income thresholds to 200% of the poverty guideline) and expanding CDCTC (e.g., raising the max credit rate to 50% while ensuring full refundability of the credit) | CPR: including income, food stamps, housing subsidy, taxes, EITC, and child care expenses | IV reduced CPR from 14.4% to 12.3% (2.1 pp or 14.6% reduction); cost: $17.1B |

| National Academies of Sciences (2019); 2016 CPS ASEC; Simulation | IV: Making the CDCTC fully refundable and focusing its benefits on families having the lowest incomes and with children below 5 years old (i.e., for families with children < age 5, the credit rate would be 100% by a $25,000 income, which declines by 10% per every $5,000 additional income and becomes zero for an income above $70,000; for families with children ages 5–12, the credit rate would be 70% by a $25,000, which declines by 7% per every $5,000 additional income) | CPR: SPM | IV reduced CPR from 13.0% to 11.8% (1.2 pp or 9.2% reduction); cost: $5.1B |

| Child Tax Credit (CTC) | |||

| Burns & Fox (2022); 2021–2022 CPS ASEC; Simulation | Baseline: the TCJA CTC (max credit = $2,000 per child for ages 0–16; phase-in rate = 15%; partially refundable) IV: expanding the CTC by the ARPA (max credit = $3,600 per child for ages 0–5 and $3,000 per child for ages 6–17, no phase-in; fully refundable) |

CPR: SPM, excluding stimulus payments | IV reduced CPR from 12.6% to 8.3% (4.3pp or 34.1% reduction); cost: not available |

| Crandall-Hollick et al. (2021); 2016–2018 CPS ASEC; Simulation | Baseline: the TCJA CTC (max credit = $2,000 per child for ages 0–16; phase-in rate = 15%; partially refundable) IV: full ARPA expansion of the CTC (max credit = $3,600 per child for ages 0–5 and $3,000 per child for ages 6–17, no phase-in; fully refundable) |

CPR: SPM | IV reduced CPR from 13.0% to 7.0% (6.0pp or 46.0% reduction); cost: $105.1B |

| Davis et al. (2019); 2016–2018 CPS ASEC; Simulation | Baseline: the TCJA CTC (max credit = $2,000 per child for ages 0–16; phase-in rate = 15%; partially refundable) IV1: increasing the state CTC to ensure the fully refundable (state + federal) credit of $2,000 per child IV2: increasing the state CTC to ensure the fully refundable (state + federal) credit of $3,600 per child for ages 0–6 and $3,000 per child for ages 7–16 |

CPR: SPM | IV1 reduced CPR from 14.8% to 11.7% (3.1pp or 20.8% reduction); cost: 30.1B IV2 reduced CPR from 14.8% to 8.4% (6.4pp or 43.3% reduction); cost: 101.8B |

| Garfinkel et al. (2016); 2014 CPS ASEC; Simulation | Baseline: the ARRA CTC (max credit = $1,000 & phase-in rate = 15%; partially refundable) IV1: max credit = $2,500 IV2: max credit = $4,000 IV3: max credit = $2,500 & phase-in rate = 37.5% IV4: max credit = $4,000 & phase-in rate = 60.0% for ages 0–5; max credit = $2,500 & phase-in rate = 37.5% for ages 6–17 IV5: max credit = $4,000 & phase-in rate = 60% |

CPR: SPM | IV1 reduced CPR from 16.5% to 15.3% (1.2pp or 7.3% reduction); cost: $59.3B IV2 reduced CPR from 16.5% to 15.1% (1.4pp or 8.5% reduction); cost: $101.0B IV3 reduced CPR from 16.5% to 13.9% (2.6pp or 15.8% reduction); cost: $75.6B IV4 reduced CPR from 16.5% to 13.1% (3.4pp or 20.6% reduction); cost: $101.6B IV5 reduced CPR from 16.5% to 12.1% (4.4pp or 26.7% reduction); cost: $150.0B |

| Giannarelli et al. (2007); 2004 CPS ASEC; Simulation | Baseline: the EGTRRA CTC (max credit: $896 in 2003; partially refundable) IV: making the CTC fully refundable |

CPR: including income, food stamps, housing subsidy, taxes, EITC, and child care expenses | IV reduced CPR from 14.4% to 11.5% (2.9 pp or 20.7% reduction); cost: $13.6B |

| Landry & Nuñez (2021); 2019 CPS ASEC; Simulation | Baseline: the TCJA CTC (max credit: $2,000 per child for ages 0–16; phase-in rate: 15%; partially refundable) IV1: full ARPA expansion of the CTC (max credit: $3,600 per child for ages 0–5 and $3,000 per child for ages 6–17; fully refundable) IV2: full refundability only (max credit: $2,000 per child for ages 0–16; fully refundable) IV3: benefit amount expansion only (max credit: $3,600 per child for ages 0–5 and $3,000 per child for ages 6–17; partially refundable) |

CPR: SPM | IV1 reduced CPR from 13.4% to 8.0% (5.4pp or 40.0% reduction); cost: $99.0B IV2 reduced CPR from 13.4% to 10.8% (2.6pp or 19.0% reduction); cost: $17.0B IV3 reduced CPR from 13.4% to 12.5% (0.9pp or 7.0% reduction); cost: $45.0B |

| Pac et al. (2020); 2010–2012 CPS ASES; Simulation | IV: All states provide CTC as the most generous state does (the receipt rate increased from 6% to 67% nationally; state CTC increased to 33% of the federal CTC) | CPR: SPM, including taxes, tax credits, and cash/in-kind benefits | IV reduced CPR from 14.2% to 13.9% (0.4 pp or 2.5% reduction); cost: not available |

| Child Allowance | |||

| Corinth et al. (2021); 2017 CPS ASEC; Simulation | Replacing the TCJA CTC (max credit: $2,000 per child; phase-in rate: 15%; partially refundable) with: IV: a child allowance of $3,600 per child for age 0–5 and $3,000 per child for age 6–17 (phasing out at higher incomes) |

CPR: SPM | IV reduced CPR from 13.7% to 10.8% (3.0pp or 21.5% reduction); cost: $101.3B |

| Garfinkel et al. (2016); 2014 CPS ASEC; Simulation | Replacing the ARRA CTC (max credit: $1,000 per child; phase-in rate: 15%; partially refundable) with: IV1: a child allowance of $2,500 per child for ages 0–5 (universal, no phase-out) and the ARRA CTC for ages 6–16 IV2: a child allowance of $4,000 per child for ages 0–5 (universal, no phase-out) and the ARRA CTC for ages 6–16 IV3: a child allowance of $2,500 per child for ages 0–17 (universal, no phase-out) IV4: a child allowance of $4,000 per child for ages 0–5 and $2,500 per child for ages 6–17 (universal, no phase-out) IV5: a child allowance of $4,000 per child for ages 0–17 (universal, no phase-out) |

CPR: SPM | IV1 reduced CPR from 16.5% to 14.5% (2.0pp or 12.1% reduction); cost: $33.7B IV2 reduced CPR from 16.5% to 13.2% (3.3pp or 20.0% reduction); cost: $63.1B IV3 reduced CPR from 16.5% to 11.4% (5.1pp or 30.9% reduction); cost: $109.3B IV4 reduced CPR from 16.5% to 10.0% (6.5pp or 39.4% reduction); cost: $138.3B IV5 reduced CPR from 16.5% to 7.8% (8.7pp or 52.7% reduction); cost: $202.9B |

| Shaefer et al. (2018); 2015 CPS ASEC; Simulation | Replacing the ARRA CTC (max credit: $1,000 per child; phase-in rate: 15%; partially refundable) and child tax exemption with: IV1: a child allowance of $3,000 per child for age 0–17 (universal, no phase-out) IV2: a child allowance of $3,600 per child for age 0–5 and $3,000 per child for age 6–17 (universal, no phase-out) IV3: a child allowance of $3,600 for the first child aged 0–5, $3,000 for the first child aged 6–17, and reduced benefits for additional children (universal, no phase-out) |

CPR: SPM | IV1 reduced CPR from 16.1% to 9.7% (6.4pp or 39.8% reduction); cost: $93.0B IV2 reduced CPR from 16.1% to 9.2% (6.9pp or 42.9% reduction); cost: $105.0B IV3 reduced CPR from 16.1% to 11.1% (5.0pp or 31.1% reduction); cost: $66.0B |

| National Academies of Sciences (2019); 2016 CPS ASEC; Simulation | Replacing the TCJA CTC and child tax exemption with: IV1: a child allowance of $2,000 per child for age 0–17 (phasing out as the TCJA CTC schedule) IV2: a child allowance of $3,000 per child for age 0–17 (phasing out between 300% and 400% of the poverty guideline) |

CPR: SPM | IV1 reduced CPR from 13.0% to 9.6% (3.4 pp or 26.2% reduction); cost: $32.9B IV1 reduced CPR from 13.0% to 7.7% (5.3 pp or 40.8% reduction); cost: $54.4B |

| Supplemental Nutrition Assistance Program (SNAP) | |||

| Giannarelli et al. (2007); 2004 CPS ASEC; Simulation | IV: Increasing the participation rate in the food stamp program from about 55% to 85% | CPR: including income, food stamps, housing subsidy, taxes, EITC, and child care expenses | IV reduced CPR from 14.4% to 13.5% (0.9 pp or 6.0% reduction); cost: $8.7B |

| National Academies of Sciences (2019); 2016 CPS ASEC; Simulation | IV1: increasing SNAP benefits by 20% for families with children, providing an additional $360 per teenager (ages 12–17) in SNAP benefits, and increasing the Summer Electronic Benefit Transfer for Children by $180 per child per summer from prekindergarten through 12th grade IV2: increasing SNAP benefits by 30% for families with children, providing an additional $360 per teenager (ages 12–17) in SNAP benefits, and increasing the Summer Electronic Benefit Transfer for Children by $180 per child per summer from prekindergarten through 12th grade |

CPR: SPM | IV1 reduced CPR from 13.0% to 11.3% (1.7 pp or 13.1% reduction); cost: $26.4B IV1 reduced CPR from 13.0% to 10.7% (2.3 pp or 17.7% reduction); cost: $37.4B |

| Pac et al. (2020); 2010–2012 CPS ASES; Simulation | IV: All states increase the SNAP enrollment rate among eligible individuals to the level of the most inclusive state (increasing the receipt rate from 81% to 93% nationally) | CPR: SPM, including taxes, tax credits, and cash/in-kind benefits | IV1 reduced CPR from 14.2% to 13.6% (0.6 pp or 4.2% reduction); cost: not available |

| Housing Voucher | |||

| Giannarelli et al. (2007); 2004 CPS ASEC; Simulation | IV: Increasing the number of available housing vouchers by 2 million (from 4.5 million to 6.5 million recipients), specifically targeting families with an income below 125% of the poverty guideline, and who have at least one elderly person, disabled person, or child | CPR: including income, food stamps, housing subsidy, taxes, EITC, and child care expenses | IV reduced CPR from 14.4% to 14.3% (0.1 pp or 0.7% reduction); cost: $9.3B |

| National Academies of Sciences (2019); 2016 CPS ASEC; Simulation | IV1: Expanding the allocation of housing vouchers to ensure a utilization rate of 50% among eligible families with children who are currently not benefiting from subsidized housing IV2: Expanding the allocation of housing vouchers to ensure a utilization rate of 70% among eligible families with children who are currently not benefiting from subsidized housing |

CPR: SPM | IV1 reduced CPR from 13.0% to 10.9% (2.1 pp or 16.2% reduction); cost: $24.1B IV1 reduced CPR from 13.0% to 10.1% (3.0 pp or 22.3% reduction); cost: $34.9B |

Note. CPS ASEC = Current Population Survey’s Annual Social and Economic Supplement. SPM = supplemental poverty measure. pp = percentage points. B = billion. TCJA = Tax Cuts and Jobs Act. ARPA = American Rescue Plan Act. ARRA = American Recovery and Reinvestment Act. EGTRRA = Economic Growth and Tax Relief Reconciliation Act.

We conducted a thorough review of the articles and extracted the following information: (1) citation, study data, and study design; (2) independent variable, which represents the proposed policy change; (3) dependent variable, which pertains to the child poverty rate and the specific measure employed to assess it; and (4) results, including the effect of a policy change on the child poverty rate, along with any associated costs. To ensure accuracy and consistency, multiple authors independently reviewed the same articles and arrived a mutual consensus regarding the extracted data.

2.2. Effects of Child Poverty Rates on CMR Rates (Coefficient B)

To obtain the coefficient of child poverty rates on CMR rates, we conducted an analysis at the county level using national data. Due to limitations in data availability, we were unable to perform individual-level or smaller area-level analyses, such as tract-level analysis. For our analysis, we utilized the National Child Abuse and Neglect Data System (NCANDS) Child Files, which provided comprehensive population-level records of all CMRs in the United States. While the Child Files provided accurate counts of children with a CMR, they did not contain valid information for poverty and control variables. Nonetheless, we were able to conduct a county-level analysis by linking the Child Files with census data and other available data at that level.

We utilized a comprehensive dataset that integrated the Child Files, census data, urbanicity data, and other county-level data for all U.S. counties spanning the years 2009 to 2018. To ensure consistency with the timeframes of prior studies selected from our scoping review for computing indirect effects (see the Results section), we specifically focused on the years 2014, 2015, 2016, and 2018. From the 2009–2019 Child Files, we extracted all CMRs with a report date falling within the years 2014, 2015, 2016, and 2018. For county-level data, including child populations, child poverty rates, and control variables, we relied on the American Community Survey 5-year estimates for the periods 2012–2016 (midyear = 2014), 2013–2017 (midyear = 2015), 2014–2018 (midyear = 2016), and 2016–2020 (midyear = 2018). The urbanicity level of counties was obtained from the 2013 U.S. Department of Agriculture Rural-Urban Continuum (RUC) Codes. Among the 3,142 U.S. counties, we excluded three Massachusetts counties and four Rhode Island counties for all years due to the absence of record submission to the NCANDS. Additionally, all 67 Pennsylvania counties were excluded from the 2014 data due to potential data entry errors concerning county identifiers. As a result, the 2014 dataset encompassed 3,068 counties, while the datasets for 2015, 2016, and 2018 included 3,135 counties.

The Child Files withheld county identifiers of counties with fewer than 1,000 reports per year to maintain confidentiality. As a result, this suppression affected many sparsely populated counties, primarily rural areas. However, the state identifiers of these suppressed counties were still available, enabling us to group them into larger pseudo county areas within each state. For our analysis, we included a total of 627 counties and pseudo counties (referred to as counties hereafter) for the year 2014, and 639 counties for the years 2015, 2016, and 2018. Moderately to highly populated rural counties were not subject to suppression, allowing us to include multiple rural counties for most states in our analysis.

The CMR rate was measured as the number of children with a CMR per 1,000 children in each county per year. The child poverty rate was measured as the percentage of children living below the federal poverty threshold in each county per year. In our analysis, we controlled for various community factors that could influence CMRs. These factors included demographic characteristics such as the percentages of Black children, Latino children, and foreign-born individuals in each county. We also considered care burden factors, including the percentages of children, elderly persons, male adults, and children with disabilities in each county. Additionally, we adjusted for residential stability by examining the percentage of people who had moved within the past year in each county. To account for urbanicity, we grouped the original nine RUC codes into three categories: large urban (RUC code 1), small urban (RUC codes 2–3), and rural (RUC codes 4–9) counties.

We employed multilevel linear models to estimate the relationship between child poverty rates and CMR rates at the county level. These models accounted for control variables and addressed the nested structure of counties within states. We estimated separate models for each year, covering the years 2014, 2015, 2016, and 2018.

2.3. Indirect Effects of Policy Changes through Child Poverty Rates on CMR Rates

The indirect effect of a policy change through child poverty rates on CMR rates is calculated by multiplying the coefficient of the policy change on child poverty rates (Coefficient A) with the coefficient of child poverty rates on CMR rates (Coefficient B). To calculate the confidence interval of an indirect effect, it is necessary to have access to the coefficients (A and B) and their standard errors (Preacher & Selig, 2012). However, none of the prior studies included in our review reported standard errors of their coefficients (i.e., Coefficient A). Therefore, we present the indirect effects without uncertainty measures around these point estimates. Nonetheless, it is expected that the standard error of Coefficient A would be small, given that previous studies conducted simulations based on a large survey dataset, specifically the Current Population Survey’s Annual Social and Economic Supplement, which encompassed over 75,000 households. We estimated the standard error of Coefficient B, and it was small, approximately one-tenth of the coefficient (as detailed in the Results section). Consequently, it is anticipated that indirect effects are statistically significant, although we are unable to provide formal significance tests.

It is important to acknowledge two limitations in our estimation of indirect effects. First, in relation to Coefficient A, all the prior studies included in our review employed a simulation design to investigate the national-level effects of policy changes on reducing child poverty. However, Coefficient B was derived from the relationship between county-level child poverty rates and county-level CMR rates. To estimate the indirect effects (A × B), we made the assumption that a reduction in national-level child poverty would result in a similar reduction in child poverty at the county level, on average. Then, we estimated the expected decrease in county-level CMR rates by considering the reduction in county-level child poverty rates. Second, with regard to Coefficient A, all the prior studies in our review measured child poverty rates using supplemental poverty measures or similar measures that accounted for both cash and noncash benefits, as well as necessary expenses. In contrast, Coefficient B was based on official poverty measures, as supplemental poverty measures were not available for estimating Coefficient B. This discrepancy has the potential to introduce biases. However, we anticipate that such biases are likely to be minimal, as there was a nearly perfect correlation between longitudinal trends of supplemental poverty measures and official poverty measures from 1998 to 2015, as reported by Shaefer and Rivera (2018).

3. Results

3.1. Effects of Policy Changes on Child Poverty Rates

This section presents the findings of the scoping review on previous studies investigating the effects of policy changes on child poverty rates, which are summarized in Table 1. Each subsection begins with a concise description of a policy to provide background information. We then provide detailed information on the policy changes proposed by previous studies and the estimated effects of these changes on child poverty rates. Finally, each subsection concludes with our selection of one or two studies per policy that will be used to calculate the indirect effects of policy changes through child poverty rates on CMR rates. All incomes, benefits, and costs are reported on an annual basis unless stated otherwise.

3.1.1. Effects of EITC Changes on Child Poverty

The EITC is a refundable federal tax credit intended to provide support to individuals with low to moderate earnings (Center on Budget and Policy Priorities, 2023b). The credit amount changes based on three income ranges: the phase-in range, the plateau range, and the phase-out range. During the phase-in range, the credit increases proportionally with each additional dollar earned. For two-parent families with two children, the credit increases by 0.40 dollar (i.e., a 40% phase-in rate) for every one dollar earned within the phase-in range of $0 to $16,510. Moving on to the plateau range, the credit remains constant at its maximum value even as a family’s income increases. Two-parent families with two children receive the maximum credit of $6,604 when their income falls within in the plateau range of $16,510 to $28,120. In the phase-out range, the credit decreases proportionally from its maximum value as each additional dollar earned. For two-parent families with two children, the credit decreases by 0.2106 dollar (i.e., a 21.06% phase-out rate) for every one dollar earned over $28,120 from the maximum value. This reduction occurs when their income falls within the phase-out range of $28,120 to $59,478. The specific amount of the EITC credit is determined by various factors, including the maximum value, the phase-in and phase-out rates, and the phase-in, plateau, and phase-out ranges, all of which vary based on marital status and the number of dependent children.

We identified four studies that examined the effects of changes to the EITC on child poverty. Giannarelli et al. (2007) proposed expanding the EITC for individuals without children by increasing their credit rate from 7.65% to 20%. They also suggested reducing marriage penalties in the ETIC by excluding 50% of a lower-earning spouse’s earnings if it would increase the EITC. Additionally, they proposed increasing the EITC credit for families with three or more children by raising the phase-in rate from 40% to 45%. Using simulations for the year 2003, the study found that these proposed changes to the EITC would reduce the child poverty rate by 0.5 percentage points or 3.7% at a national cost of $22.2 billion.

Lippold (2015) conducted simulations for the year 2010 and proposed more substantial changes to the EITC. The study suggested significant expansions of the EITC for unmarried individuals, married couples with children, and those without children. For example, the study proposed raising the phase-in rate from 7.65% to 50% for married couples without children, from 34% to 70% for those with one child, from 40% to 90% for those with two children, from 45% to 110% for those with three children, and from 45% to 130% for those with four or more children. These modifications were projected to decrease the child poverty rate by 3.3 percentage points or 22.3% at a national cost of $182.5 billion.

Pac et al. (2020) conducted simulations to estimate the potential reduction in the child poverty rate if all states provide state EITC benefits at the same level as the most generous state during the years 2010–2012. Wisconsin was identified as the most generous state, offering a 43% of the Federal EITC as state EITC benefits. The study projected that if all states were to increase their EITC benefits to the level of Wisconsin, it would result in a decrease in the child poverty rate by 1.2 percentage points or 8.5%. The study did not offer details regarding the costs linked to their suggested modifications.

Finally, the National Academies of Sciences (2019) proposed two EITC options. The first option involved increasing EITC benefits for the lowest earners by raising the credit rate within the phase-in and plateau ranges. The second option aimed to enhance the overall generosity of EITC benefits by increasing the credit amount by 40% across the entire EITC schedule. Based on simulations for the year 2015, the study found that the child poverty rate would decrease by 1.2 percentage points or 9.2% at a national cost of $8.4 billion for the first option, and by 2.1 percentage points or 16.2% at a national cost of $20.2 billion for the second option.

We selected the National Academies of Sciences (2019) as the study to calculate the indirect effects of EITC changes on CMR rates. The proposed changes in the EITC outlined in the study are expected to yield greater reductions in the child poverty rate relative to their costs compared to other proposed changes. Additionally, the study utilized more recent data compared to other studies. We did not select Giannarelli et al. (2007) and Lippold (2015) as their proposed changes were found to have high costs in relation to the expected impact on reducing child poverty, likely due to the substantial increases in EITC credits for workers without children. Furthermore, we did not select Pac et al. (2020) as they did not provide information on the associated costs of their proposed changes.

3.1.2. Effects of CDCTC Changes on Child Poverty

The CDCTC is a federal tax credit designed to provide partial reimbursement for eligible child care expenses incurred by employed parents of children under the age of 13 (National Academies of Sciences, 2019). As pointed out by Wolters et al. (2021), although the CDCTC credit rate is higher for families with lower incomes, it primarily benefits families with middle to high incomes due to three key factors. First, CDCTC credits are nonrefundable, meaning that the credit cannot exceed the amount of taxes owed by a family. The highest credit rate of 35% applies to families with an adjusted gross income (AGI) of $15,000 or less. However, families in this income range often have minimal tax liability and, therefore, can receive only a small credit. Second, higher-income families have the financial capacity to afford higher child care expenses, which makes them eligible for larger credits. The maximum eligible child care expenses are $3,000 for one child and $6,000 for two or more children. Low-income families typically spend much less than these maximum eligible expenses on child care. Lastly, the CDCTC credit does not phase out for higher incomes. The maximum credit rate of 35% applies to an AGI of $15,000 or less. The credit rate then gradually decreases to a minimum rate of 20% at an AGI of $43,000. Above $43,000, the credit rate remains constant at 20% without any further phaseout.

Two studies examined the effects of modifications to the CDCTC on child poverty. Giannarelli et al. (2007) proposed transforming CDCTC credits into a fully refundable form. They also suggested raising the maximum credit rate to 50% for families with an AGI of $30,000 or less, gradually reducing the credit rate for AGI exceeding $30,000 until it reaches a minimum rate of 20% for an AGI of $60,000 or above. In addition, they recommended expanding child care subsidies by increasing income thresholds to 200% of the poverty threshold, along with minor adjustments like work requirements and copayments. Simulations conducted for the year 2003 indicated that these proposed modifications would decrease the child poverty rate by 2.1 percentage points or 14.6% at a national cost of $17.1 billion.

Similarly, the National Academies of Sciences (2019) proposed making CDCTC credits refundable and increasing the credit rate. Specifically, the credit rate would be highest (100% for families with children under age 5 and 70% for families with children aged 5 and above) for an AGI of $25,000 or less. The credit rate would gradually decrease for AGI exceeding $25,000 and phase out completely when an AGI exceeds $70,000. The study also suggested raising the maximum eligible child care expense from $3,000 to $4,000 for one child. Using simulations for the year 2015, the study found that these proposed changes would reduce the child poverty rate by 1.2 percentage points or 9.2% at a national cost of $5.1 billion.

When comparing the proposed CDCTC changes by the National Academies of Sciences (2019) to those suggested by Giannarelli et al. (2007), the former appears to be more effective in reducing child poverty relative to its cost. Additionally, the National Academies of Sciences (2019) utilized more recent data. Therefore, we selected the National Academies of Sciences (2019) as the source for calculating the indirect effects of CDCTC changes on CMR rates.

3.1.3. Effects of CTC Changes on Child Poverty

The CTC is a federal tax credit designed to provide support to low- and moderate-income families with children. Crandall-Hollick et al. (2021) provided an overview of major legislative changes to the CTC in recent years, which we have summarized below. In 2020, the CTC was governed by the Tax Cuts and Jobs Act (TCJA), which established a maximum credit of $2,000 per child for children aged 0–16. However, the credit phased in gradually after an income threshold of $2,500, resulting in either no credit or a partial credit for many families with lower incomes. Even for families eligible for the maximum credit of $2,000, the credit was partially refundable, allowing for up to $1400 per child. The credit phased out completely for higher incomes. In 2021, the American Rescue Plan Act (ARPA) expanded the CTC. This legislation ensured that low-income families would receive the maximum credit by eliminating the phase-in stage. It also made the credit fully refundable by removing the refund cap of $1,400 per child. Additionally, the maximum credit amount was increased to $3,600 per child for children aged 0–5 and $3,000 per child for children aged 6–17. However, this expansion was temporary and only applicable to the year 2021. Starting from 2022, the CTC has reverted to the regulations set by the Tax Cuts and Jobs Act.

We identified seven studies that investigated the effects of CTC changes on child poverty. Burns and Fox (2022), Crandall-Hollick et al. (2021), and Landry and Nuñez (2021) conducted simulations to assess the effects of expanding the TCJA CTC to the ARPA CTC. They found that this expansion would result in a reduction of the child poverty rate by 4.3 percentage points or 34.1% (cost: not reported; Burns & Fox, 2022), 6.0 percentage points or 46.0% (cost: $105.1 billion; Crandall-Hollick et al., 2021), and 5.4 percentage points or 40.0% (cost: $99.0 billion; Landry & Nuñez, 2021). In their analysis, Landry and Nuñez (2021) further examined two specific aspects of the ARPA expansion: full refundability and benefit amount expansion. They discovered that full refundability would result in a greater reduction of the child poverty rate at a lower cost compared to the benefit amount expansion. Specifically, they found that full refundability would reduce the child poverty rate by 2.6 percentage points or 19.0% at a national cost of $17.0 billion, while the benefit amount expansion would reduce the child poverty rate by 0.9 percentage points or 7.0% at a national cost of $45.0 billion.

Two studies examined earlier versions of the CTC. Garfinkel et al. (2016) examined the CTC under the American Recovery and Reinvestment Act of 2009 (ARRA), which established the maximum credit of $1,000 and a phase-in rate of 15%. They conducted simulations for the year 2013, exploring various changes to the maximum credit and phase-in rate. Their least generous option (increasing the maximum credit to $2,500 while maintaining the current phase-in rate) would reduce the child poverty rate by 1.2 percentage points or 7.3% at a national cost of $59.3 billion. On the other hand, their most generous option (increasing the maximum credit to $4,000 and increasing the phase-in rate to 60%) would reduce the child poverty rate by 4.4 percentage points or 26.7% at a national cost of $150.0 billion. Giannarelli et al. (2007) examined the CTC regulated by the Economic Growth and Tax Relief Reconciliation Act of 2001. Under this version, the maximum credit was $896 in 2003, and the credit was partially refundable. Through simulations conducted for the year 2003, Giannarelli et al. (2007) analyzed the impact of making CTC credits fully refundable. They found that implementing this change would reduce the child poverty rate by 2.9 percentage points or 20.7% at a national cost of $13.6 billion.

Davis et al. (2019) and Pac et al. (2020) focused on changes of the state CTC. Davis et al. (2019) conducted simulations to explore the expansion of the state CTC in conjunction with the federal TCJA CTC for the years 2015–2017. They proposed increasing the state CTC to ensure that the combined total of state and federal credits reaches either the fully refundable amount of $2,000 per child (option A) or $3,600 per child for children aged 0–6 and $3,000 per child for children aged 7–16 (option B). Their findings indicate that option A would lead to a decrease in the child poverty rate by 3.1 percentage points or 20.8% at the national cost of $30.1 billion, while option B would result in a reduction of 6.4 percentage points or 43.3% at the national cost of $101.8 billion. In a separate study, Pac et al. (2020) conducted simulations for the years 2009–2011. They examined the scenario in which all states provide the CTC at the same level as the most generous state. Their findings demonstrate that such an arrangement would lead to a decrease in the child poverty rate by 0.4 percentage points or 2.5%. However, the cost associated with this change was not reported.

We chose Crandall-Hollick et al. (2021) and Landry and Nuñez (2021) to calculate the indirect effects of CTC changes on CMR rates because they focused on proposing changes to the federal CTC, specifically the current TCJA CTC, instead of earlier versions or the state CTC. Moreover, these studies provided information on the costs associated with their proposed changes.

3.1.4. Effects of a Child Allowance on Child Poverty

A universal child allowance refers to a monetary benefit granted to all families with children, irrespective of their income or other eligibility criteria (Garfinkel et al., 2016). Unlike most other advanced industrialized nations, the United States does not have a universal child allowance (Garfinkel et al., 2016; National Academies of Sciences, 2019). The closest comparable support in the United States is the CTC (Garfinkel et al., 2016). However, CTC benefits are exclusively provided to families who meet specific income requirements, gradually increasing as earnings rise and decreasing once earnings surpass a certain threshold (Garfinkel et al., 2016; National Academies of Sciences, 2019). A child allowance possesses distinct characteristics that differentiate it from the CTC. First, a child allowance has no phase-in stage, ensuring full benefits for all low- to moderate-income families, including those who do not earn enough to meet the eligibility criteria for the work-based CTC (Garfinkel et al., 2016; National Academies of Sciences, 2019; Shaefer et al., 2018). Therefore, child allowance benefits would enhance the economic stability of low-income families with children and promote their integration into the broader social fabric (Garfinkel et al., 2016; National Academies of Sciences, 2019; Shaefer et al., 2018). Second, a child allowance typically has no phase-out stage, providing full benefits to all families with children without reducing the benefits as incomes rise (Garfinkel et al., 2016; National Academies of Sciences, 2019; Shaefer et al., 2018). This approach avoids creating disincentives for labor participation and prevents stigmatization of low-income beneficiaries, thus avoiding stigma-induced non-participation and negative psychological effects on participants (Garfinkel et al., 2016; National Academies of Sciences, 2019; Shaefer et al., 2018). Universal benefits are likely to gain more widespread public support compared to safety net programs that exclusively target impoverished families (Shaefer et al., 2018). Child allowance benefits are typically provided on a monthly basis to enhance a family’s economic security (National Academies of Sciences, 2019; Shaefer et al., 2018). However, we present the benefits as annual amounts to maintain consistency with our presentation of other program benefits.

Four studies were identified that examined the impact of a child allowance on child poverty. Two of them conducted simulations on replacing the TCJA CTC with a child allowance (Corinth et al., 2022; National Academies of Sciences, 2019). However, their proposals include phasing out child allowance benefits at higher incomes, making them similar to the fully refundable CTC proposed in the ARPA expansion. Corinth et al. (2022) proposed replacing the TCJA CTC with a child allowance of $3,600 per child for children aged 0–5 and $3,000 per child for children aged 6–17. This replacement was found to reduce the child poverty rate by 3.0 percentage points or 21.5% at a national cost of $101.3 billion. The National Academies of Sciences (2019) conducted simulations on replacing the TCJA CTC and child tax exemption with two different options of child allowance benefits. The first option (a child allowance of $2,000 per child) was expected to reduce the child poverty rate by 3.4 percentage points or 26.2% at a national cost of $32.9 billion. The second option ($3,000 per child) was expected to reduce the child poverty rate by 5.3 percentage points or 40.8% at a national cost of $54.4 billion.

The other two studies simulated replacing the ARRA CTC with a universal child allowance without any phase-out. Garfinkel et al. (2016) proposed various options, including full replacement with a child allowance for all children or partial replacement only for younger children while maintaining the CTC for older children. Their least generous option (a child allowance of $2,500 per child for ages 0–5 and the current CTC for ages 6–16) was estimated to reduce the child poverty rate by 2.0 percentage points or 12.1% at a national cost of $33.7 billion. Their most generous option (a child allows of $4,000 per child for all ages 0–17) was estimated to reduce the child poverty rate by 8.7 percentage points or 52.7% at a national cost of $202.9 billion. Shaefer et al. (2018) proposed replacing the ARRA CTC and child tax exemption with three child allowance options. The study projected a reduction in the child poverty rate by 6.4 percentage points or 39.8% with the first option (a child allowance of $3,000 per child for ages 0–17; cost: $93.0 billion), 6.9 percentage points or 42.9% with the second option ($3,600 for ages 0–5 and $3,000 for ages 6–17; cost: $105.0 billion), and 5.0 percentage points or 31.1% with the third option ($3,600 for the first child aged 0–5, $3,000 for the first child aged 6–17, and reduced benefits for additional children; cost: $66.0 billion).

We selected two studies to calculate the indirect effects of a child allowance on CMR rates. Among studies proposing a child allowance with a phase-out, we chose Shaefer et al. (2018). Among the studies proposing a child allowance without a phase-out, we selected the National Academies of Sciences (2019). The selected studies showed slightly greater effects relative to cost compared to other studies.

3.1.5. Effects of SNAP Changes on Poverty

The SNAP is the largest non-monetary assistance program in the Unites States (National Academies of Sciences, 2019). To be eligible for SNAP, there are three federal requirements to consider. First, the gross monthly income of a household must not exceed 130% of the poverty threshold. Second, the net monthly income of a household, which consider deductions like housing and child care costs, must be equal to or below 100% of the poverty threshold. Third, the total assets of a household must be below a specific limit, which is $2,750 in 2023 (Center on Budget and Policy Priorities, 2023a). Many states have implemented more lenient restrictions on gross income and asset limits (Center on Budget and Policy Priorities, 2023a). The majority of states have set the gross income limit higher than 130% of the poverty threshold, typically around 200%, and have eliminated the asset limit altogether (SNAP Screener, 2023). However, the net income limit remains consistent at 100% across all states (SNAP Screener, 2023). SNAP benefits are designed to provide higher assistance to households with lower incomes and larger sizes. Families with zero net income are eligible to receive the maximum benefit amount, which is $740 per month for a family of three and $939 per month for a family of four in 2023 (Center on Budget and Policy Priorities, 2023a). The SNAP benefit amount is reduced by 30% of the net income (Center on Budget and Policy Priorities, 2023a). These benefits are issued monthly through an Electronic Benefit Transfer card, which functions as a debit card for making purchases (National Academies of Sciences, 2019). SNAP benefits can be used at over 254,000 retailers, allowing for the purchase of most food items (Center on Budget and Policy Priorities, 2022). However, there are exceptions where SNAP benefits cannot be utilized, such as for alcoholic beverages, cigarettes, vitamin supplements, and hot food (Center on Budget and Policy Priorities, 2022).

Three studies explored the effects of SNAP changes on child poverty. Giannarelli et al. (2007) proposed increasing the national SNAP participation rate in the food stamp program (the precursor to SNAP) from approximately 55% to 85%. Through simulations conducted for the year 2003, they found that this modification would decrease the child poverty rate by 0.9 percentage points or 6.0%, with a national cost of $8.7 billion.

While Giannarelli et al. (2007) did not specify a particular strategy for increasing participation rates, Pac et al. (2020) suggested expanding the eligibility criteria of all states to match the most inclusive state, thereby raising the SNAP enrollment rate. Their simulation based on data from 2009–2011 projected that expanding eligibility would result in a rise in the SNAP receipt rate among eligible individuals from 81% to 93%, leading to a reduction in the child poverty rate by 0.6 percentage points or 4.2%, with an unknown cost.

The National Academies of Sciences (2019) proposed two options for increasing SNAP benefits for families with children: a 20% increase (option A) or a 30% increase (option B). Additionally, they recommended providing an extra $360 per teenager (ages 12–17) in SNAP benefits and augmenting the Summer Electronic Benefit Transfer for Children by $180 per child per summer, from prekindergarten through 12th grade. Simulations conducted for the year 2015 indicated that option A would result in a reduction in the child poverty rate by 1.7 percentage points or 13.1%, at a national cost of $26.4 billion. Option B would lead to a decrease of 2.3 percentage points or 17.7% in the child poverty rate, at a national cost of $37.4 billion.

We selected the National Academies of Sciences (2019) to calculate the indirect effects of SNAP changes on CMR rates. This decision was based on several factors: the study used more recent data, focused on changes to the current SNAP program (rather than the former food stamp program), and reported the costs associated with their proposed changes.

3.1.6. Effects of Housing Voucher Changes on Poverty

The Housing Choice Voucher Program, formerly known as Section 8, serves as the primary provider of rental assistance in the United States (Center on Budget and Policy Priorities, 2021). This paragraph presents an overview of the program based on information from Center on Budget and Policy Priorities (2021). Low-income households utilize vouchers to help with their housing costs. In 2018, vouchers were utilized by over 5 million individuals from 2.3 million families with low incomes, with children comprising more than 40% of the beneficiaries. Each year, 75% of newly admitted households must have incomes classified as extremely low, meaning their incomes fall below either the poverty threshold or 30% of the local median income, depending on which amount is higher. The remaining 25% of households are eligible to have incomes up to 80% of their area’s median income. Generally, families holding vouchers are obligated to pay either 30% of their income or a minimum rent of $50 (whichever is higher) to cover their rent and utilities. The voucher subsidizes the remaining portion of these expenses. The maximum voucher amount is determined by the housing agency, considering fair market rent estimates provided by the Department of Housing and Urban Development.

The limited availability of vouchers poses the most significant challenge within the Housing Choice Voucher Program (Acosta & Gartland, 2021; National Academies of Sciences, 2019). Due to funding constraints, only 25% of eligible households receive rental assistance, resulting in extensive waiting lists for aid (Acosta & Gartland, 2021). On average, families who receive vouchers experience a wait of approximately 28 months on waitlists (Acosta & Gartland, 2021). Many eligible families are unable to join these waitlists as housing agencies have closed them due to a high influx of new applicants (Acosta & Gartland, 2021). Moreover, some families may opt not to add their names to the waitlist due to the lengthy waiting period that can span several years (Acosta & Gartland, 2021). Experts suggest that a simple expansion of housing vouchers, involving an increase in the quantity of available vouchers, could potentially alleviate poverty without the need to modify benefit levels or eligibility criteria (Acosta & Gartland, 2021; National Academies of Sciences, 2019).

We identified two studies that examined the impact of housing voucher changes on child poverty. Both studies recommended expanding the availability of vouchers. Giannarelli et al. (2007) suggested increasing the number of new vouchers by 2 million, particularly for families with incomes below 125% of the poverty threshold and with at least one elderly person, disabled person, or child. Their simulations for the year 2003 indicated that this expansion would reduce the child poverty rate by 0.1 percentage points or 0.7% at a national cost of $9.3 billion. On the other hand, the National Academies of Sciences (2019) proposed a larger expansion targeting families with children. For eligible families with children currently not benefiting from subsidized housing, the study recommended expanding the allocation of housing vouchers to achieve a utilization rate of either 50% (option A) or 70% (option B). Option A projected a reduction in the child poverty rate by 2.1 percentage points or 16.2% at a national cost of $24.1 billion, while option B projected a reduction by 3.0 percentage points or 22.3% at a national cost of 34.9 billion.

We chose the National Academies of Sciences (2019) to calculate the indirect effects of housing voucher changes on CMR rates because the study utilized more recent data and presented a more efficient and effective strategy for reducing child poverty.

3.2. Effects of Child Poverty Rates on CMR Rates

The selected studies conducted policy simulations for different years: 2014 (Shaefer et al., 2018), 2015 (National Academies of Sciences, 2019), 2015–2017 (mid-year = 2016; Crandall-Hollick et al., 2021), and 2018 (Landry & Nuñez, 2021). We estimated the relationships between county child poverty rates and county CMR rates for each of these years using national county-level data and adjusting for various control variables. The summarized results are presented in Table 2, while the full details can be found in Supplement Tables S2–S5. In all years, the adjusted coefficients of child poverty rates on CMR rates were statistically significant. The coefficient was lowest in 2015, at 1.19, indicating that for every 1 percentage point increase in the child poverty rate, the CMR rate increased by 1.19 per 1,000 children. The highest coefficient was observed in 2018, at 1.35.

Table 2.

Adjusted Coefficients of County Child Poverty (CP) Rates on Child Maltreatment Report (CMR) Rates, United States.

| Year | N | Mean CMR rate | Linear multilevel modeling results | ||

|---|---|---|---|---|---|

| Adjusted coefficients of CP rates on CMR rates | Standard error | p | |||

| 2014 | 627 | 45.35 | 1.24 | 0.11 | < .0001 |

| 2015 | 639 | 45.02 | 1.19 | 0.11 | < .0001 |

| 2016 | 639 | 46.34 | 1.22 | 0.12 | < .0001 |

| 2018 | 639 | 47.91 | 1.35 | 0.14 | < .0001 |

Note. The mean CMR rate is per 1,000 children. The mean CMR rates and the adjusted coefficients were weighted by county child populations. Each row’s coefficient was estimated by a separate linear multilevel model, using the given year’s data. All models included a state-level random intercept, the CP rate, and the control variables, including % Black children among resident children, % Latino children among resident children, % foreign-born among residents, % children among residents, % elderly persons (≥ age 65) among residents, % male among adults aged 20–64, % children with disabilities, % moved in one year, and urbanicity. Full model results are available in the Supplement.

3.3. Indirect Effects of Policy Changes through Child Poverty Rates on CMR Rates

We used the anticipated percentage point reductions in child poverty rates resulting from the chosen policy changes (as indicated in Table 1) as the values for Coefficient A in Figure 1, as they are equivalent to linear regression coefficients. The estimated coefficients of child poverty rates on CMR rates, obtained through multilevel linear modeling (as presented in Table 2), were utilized as Coefficient B in Figure 1. To calculate the indirect effects of the selected policy changes on CMR rates, mediating through child poverty rates, we multiplied Coefficient A and Coefficient B. The results are summarized in Table 3.

Table 3.

Indirect Effects of Policies through Child Poverty (CP) Rates on Child Maltreatment Report (CMR) Rates.

| Citation | Policy Change; Study Year; Cost | Coefficient A (Policy → CP) |

Coefficient B (CP → CMR) |

Indirect effect = A × B |

|---|---|---|---|---|

| Earned Income Tax Credit (EITC) | ||||

| National Academies of Sciences (2019) |

|

|

1.19 |

|

| Child and Dependent Care Tax Credit (CDCTC) | ||||

| National Academies of Sciences (2019) | Making the CDCTC fully refundable and focusing its benefits on families having the lowest incomes and with children below 5 years old; 2015; $5.1B | −1.2 | 1.19 | −1.43 |

| Child Tax Credit (CTC) | ||||

| Crandall-Hollick et al. (2021) | Full ARPA expansion of the TCJA CTC (raising max credits + full refundability); 2015–2017; $105.1B | −6.0 | 1.22 | −7.32 |

| Landry & Nuñez (2021) |

|

|

1.35 |

|

| Child Allowance | ||||

| Shaefer et al. (2018) | Replacing the ARRA CTC and child tax exemption with:

|

|

1.24 |

|

| National Academies of Sciences (2019) | Replacing the TCJA CTC and child tax exemption with:

|

|

1.19 |

|

| Supplemental Nutrition Assistance Program (SNAP) | ||||

| National Academies of Sciences (2019) |

|

|

1.19 |

|

| Housing Voucher | ||||

| National Academies of Sciences (2019) |

|

|

1.19 |

|

Note. B = billion. TCJA = Tax Cuts and Jobs Act. ARPA = American Rescue Plan Act. ARRA = American Recovery and Reinvestment Act.

The proposed change of replacing the ARPA CTC and child tax exemption with a universal child allowance (with no phase-out) of $3,600 per child for children aged 0–5 and $3,000 per child for children aged 6–17, as presented by Shaefer et al. (2018) in Table 3, was projected to have the largest anticipated indirect effect. This policy change was estimated to reduce the CMR rate by 8.56 per 1,000 children or 18.9% (from 45.35 to 36.79 per 1,000 children based on 2014 data), at a national cost of $105.0 billion. On the other hand, the most cost-effective indirect effect was expected by making the CDCTC fully refundable and targeting its benefits towards families with the lowest incomes and children under 5 years old, as proposed by the National Academies of Sciences (2019) in Table 3. This policy change was estimated to reduce the CMR rate by 1.43 per 1,000 children or 3.2% (from 45.02 to 43.59 per 1,000 children based on 2015 data), at a national cost of $5.1 billion. While the child allowance option was generous and universal, the CDCTC option was more targeted, focusing solely on refunding child care expenses and limiting the expansion to very-low-income families and younger children.

Among the selected policy changes (Table 3), the child allowance options with an allowance of $3,000 or greater tended to show large indirect effects (6.20–8.56) with high costs ($54.4B-$105.0B). The CTC changes, especially the full CTC expansion with full refundability, demonstrated large indirect effects (7.29–7.32) with high costs ($99.0B-105.1B), comparable to those of the child allowance options. The SNAP changes, the housing voucher changes, and the second proposed EITC change (i.e., raising the overall generosity of EITC benefits) showed moderate indirect effects (2.02–3.57) with moderate costs ($20.2B-$37.4B). The first proposed EITC change (i.e., raising EITC benefits for lowest earners) and the CDCTC change exhibited low indirect effects (1.43) with low costs ($5.1B-$8.4B).

4. Discussion

We initially conducted a scoping review of previous studies that examined the effects of policy changes, including alterations to EITC, CDCTC, CTC, child allowance, SNAP, and housing voucher, on child poverty rates. Subsequently, we empirically estimated the relationship between child poverty rates and CMR rates using national county-level data. Finally, we calculated the indirect effects of policy changes on CMR rates, mediating through child poverty rates, integrating information from prior studies with our own empirical findings. Among the proposed policy changes explored in prior studies, the expansion of generous cash benefits such as a child allowance and a fully refundable CTC was projected to yield the largest indirect effects with the highest associated costs. The expansion of in-kinds and near-cash benefits, such as SNAP and housing vouchers, to support the basic needs of most low-income families was expected to have moderate effects with moderate costs. Tax credits with a phase-in stage, like EITC, were anticipated to have a low effect with a low cost when targeting expansion to the lowest earners, and a moderate effect with a moderate cost for more comprehensive expansion to all eligible earners. Highly focused tax credits that solely refunded eligible child care expenses, thereby limiting benefits to a subset of low-income families, such as CDCTC, were expected to have a low effect with a low cost, even if made fully refundable.

One strength of this study is its ability to generate preliminary estimates of the indirect effects of policy changes on CMR rates through child poverty rates, leveraging existing studies and secondary/administrative data analysis. This approach facilitates the exploration of various policy options and their potential effects on CMR rates within a short timeframe and at a minimal cost. Another strength is the study’s focus on national-level effects in both the review and analysis, yielding valuable estimates at the national level that hold significant implications for federal policies.

This study has several notable limitations. First, the estimated indirect effects are based on simulations from prior studies and the current study’s observational design, rather than solid causal evidence obtained through a true experimental design. Therefore, our findings represent potential promising effects of policy changes that need to be confirmed by more rigorous future studies. Second, our estimates only pertain to the indirect effects mediated through child poverty rates. While we believe that the main pathway from policy changes to CMR rates is through child poverty, there may be other mediating factors to consider. It is possible that policies impact CMR rates through material hardships independent from poverty. However, such alternative pathways were not taken into account in our approach. Third, our estimation of indirect effects is based on the county-level relationship between child poverty rates and CMR rates. This choice was made because county was the smallest unit of analysis to estimate the relationship using national CMR data (i.e., NCANDS Child Files). As a result, our approach estimates the reduction in county CMR rates if county child poverty rates decrease to the same extent on average as the national poverty reduction caused by a policy change. More sophisticated analyses at the individual level or smaller area levels (e.g., tracts) are required to estimate CMR reductions at those levels. Fourth, there is a discrepancy in child poverty measures between Coefficients A and B. Prior studies examining effects of policy changes on child poverty rates (i.e., Coefficient A) used supplemental poverty measures or similar measures. Conversely, our estimation of the relationship between child poverty rates and CMR rates was based on official poverty measures. It is possible that a one-percentage-point decrease in a supplemental poverty measure may not exactly correspond to a one-percentage-point decrease in an official poverty measure. However, the nearly perfect association between longitudinal changes in the supplemental poverty measure and the official poverty measure over the past two decades (Shaefer & Rivera, 2018) suggests a high level of correspondence between these two measures. Finally, our estimates focused on the overall dichotomous poverty status without considering further diversity in economic conditions, such as deep poverty and near poverty. Policy options with similar effects on overall poverty may have different impacts on deep poverty and near poverty conditions. Considering these aspects is warranted in future research.

Despite these limitations, our approach yielded remarkably consistent estimates with a recent simulation study conducted by Pac et al. (2023). Pac and colleagues employed a sophisticated method, utilizing the best available causal evidence, to simulate the impact of policy-induced changes in household income on CMR rates. They examined the effects of three policy packages proposed by the National Academies of Sciences (2019) on CMR rates. In comparison to their results, our approach produced nearly identical findings, as shown in Supplement Table S6. For instance, Pac et al. (2023) anticipated that Package 4 would result in a decrease in the CMR rate of 9 per 1,000 children or 19.7%. Our approach yielded almost the same estimates, with a reduction of the CMR rate by 9 per 1,000 children or 19.6%. This high level of consistency suggests that our approach may provide estimates that closely align with valid ones.

Regarding the feasibility of implementing the proposed policy changes identified in our scoping review, some of them may be seen as costly. Specifically, the associated costs of the policy changes regarding a child allowance and the CTC often exceed $100 billion, which is comparable to the entire federal outlay for SNAP, which was $149 billion in 2022 and is projected to be $127 billion in 2023 (Congressional Budget Office, 2023). However, it is crucial to consider the economic burden of child maltreatment, as it indicates that the benefits of reducing the CMR rate would outweigh the costs of implementing policy changes. Two studies have estimated the total lifetime costs associated with all CMRs incurred annually in the United States. Fang et al. (2012) focused on tangible costs of CMRs, including health care costs, productivity losses, child welfare costs, criminal justice costs, and special education costs. They estimated the total lifetime cost to be $585 billion. On the other hand, Peterson et al. (2018) concentrated on intangible costs, such as value per statistical life and quality-adjusted life years, and projected the total lifetime cost to be $1,995 billion. Based on these estimated CMR costs, if we consider the second child allowance option proposed by Shaefer et al. (2018) in Table 3, it is expected to decrease the CMR rate by 8.56 per 1,000 children or 18.9%, with a national cost of $105.0 billion. The benefit of this CMR reduction would amount to $110.6 billion (= $585 billion × 18.9%) based on tangible costs of CMRs, and $377.1 billion (= $1,995 billion × 18.9%) based on intangible costs of CMRs. Alternatively, if we consider the second child allowance option proposed by the National Academies of Sciences (2019) in Table 3, it is expected to decrease the CMR rate by 6.31 per 1,000 children or 14.0%, at a national cost of $54.4 billion. The benefit of this CMR reduction would range from $81.9 billion to $279.3 billion. Therefore, the anticipated benefits of these policy changes outweigh their costs, even solely based on the expected reduction in CMRs. Considering that CMR reduction is just one of many benefits of reducing child poverty (National Academies of Sciences, 2019), the strategy of reducing CMRs by addressing child poverty is highly compelling.

Supplementary Material

Acknowledgements/Funding:

This work was funded by a grant from the Centers for Disease Control and Prevention (CDC), K01CE003229. The analyses presented in this publication were based on data from the National Child Abuse and Neglect Data System Child Files. These data were provided by the National Data Archive on Child Abuse and Neglect at Cornell University, and have been used with permission. The data were originally collected under the auspices of the Children’s Bureau (CB). Funding was provided by the CB. The CDC, the collector of the original data, the funder (CB), NDACAN, Cornell University, and the agents or employees of these institutions bear no responsibility for the analyses or interpretation presented here. The information and opinions expressed reflect solely the opinions of the authors.

Footnotes

Declarations of interest: none

References

- Acosta S, & Gartland E (2021). Families wait years for housing vouchers due to inadequate funding. https://www.cbpp.org/research/housing/families-wait-years-for-housing-vouchers-due-to-inadequate-funding

- Belsky J (1980). Child maltreatment: An ecological integration. American Psychologist, 35(4), 320–335. 10.1037/0003-066X.35.4.320 [DOI] [PubMed] [Google Scholar]

- Berger LM (2004). Income, family structure, and child maltreatment risk. Children and Youth Services Review, 26(8), 725–748. 10.1016/j.childyouth.2004.02.017 [DOI] [Google Scholar]