Abstract

This article proposes a performance measure to evaluate the detection performance of a control chart with a given sampling strategy for finite or small samples sequence and prove that the CUSUM control chart with dynamic non-random control limit and a given sampling strategy can be optimal under the measure. Numerical simulations and real data for an earthquake are provided to illustrate that for different sampling strategies, the CUSUM chart will have different monitoring performance in change-point detection. Among the six sampling strategies that take only a part of samples, the numerical comparing results illustrate that the uniform sampling strategy (uniformly dispersed sampling strategy) has the best monitoring effect.

Keywords: Change-point detection, optimal CUSUM chart, sampling strategy, small samples

1. Introduction

One of the basic problems of quickest change-point detection is designing an optimal control chart (or sequential test, alarm time, stopping time) to detect possible changes in the statistical behavior of a sequence of observations at some instant in time ( change point). Optimal change-point detection or an optimal control chart for change detection is usually expected to have the smallest average detection delay of all control charts subject to a constraint associated with the cost of false alarms. The need for the quickest detection of change arises in a variety of applications, including quality control [8,14], biomedical signaling and public health [3,17,19], financial markets [3], network monitoring [20], etc.

There are mainly two settings in the optimal change-point detection: one is Bayesian change-point detection in which the distribution of the change-point time is known [10,16,18], another is non-Bayesian or minimax change-point detection in which the change-point time is non-random and unknown [7,9–12]. A recent review of optimal change-point detection theory in both Bayesian and non-Bayesian settings can be found in [6].

Because of sampling constraints or to reduce the sampling cost, we have to consider how to construct an optimal control chart with the best sampling strategy for change detection, which is subject to two constraints: one is on the loss associated with false alarms, another is the cost of observations or sampling restrictions. Premkumar and Kumar [13] formulated the Bayesian change detection problem that minimizes the detection delay for sleeping/waking scheduling in a sensor network. Banerjee and Veeravalli [1,2] investigated the optimal detection problem in both Bayesian and non-Bayesian settings with a constraint on the average energy consumed by the observations. Geng et al. [4] analyzed the Bayesian change detection problem with sampling constraints. Ren et al. [15] studied the optimal detection problem in a non-Bayesian setting with communication rate constraints. All the above work is based on a common assumption that the observation sequence is infinite.

In fact, within a given limited time, people can only observe (or sample) a finite number N of samples. Sometimes we can only obtain dozens or even fewer samples. The following discussion shows that the sequential detection with finite samples can be used for people's special needs. (1) Consider a production line that produces one product per minute one day. Let the production line works 8 hours a day, then the number of sequential observations is N = 480. If someone wants to monitor the product quality of a certain day online, then the task is to design or construct an effect test for monitoring whether the 480 sequential observations ( product quality of 1 day) are abnormal in real time on line. (2) As we know, the securities market trades for 4 hours a day. If we want to monitor online the change of the trading price per minute of a stock 1 day, there are N = 240 sequential trading price data. (3) Silicosis is an occupational disease with the highest incidence rate among workers in cement production enterprises. Usually, the cement production enterprise will arrange physical examination for each employee every year to see if there is silicosis. If an employee works from the age of 20 to the age of 60, there are 40 physical examination data, that is, N = 40. (4) Diabetes is a common disease. Almost every university in Shanghai will arrange physical examinations for teachers every year, one of exam items is to check whether the blood sugar is normal. Usually, the average age of young teachers entering University is 28 and retire at the age of 60. There will be blood glucose physical examination data of 32 years for each teacher, that is, N = 32.

Due to sampling constraints or to reduce sampling costs, people can only get a part of the real samples (data). For example, if one has time only in the morning (or afternoon) to observe the changes in stock prices, he or she may correspondingly adopt the following sampling strategy: the no observed samples in the afternoon (or morning) are replaced by a given number. Therefore, we have only a real trading price data of 2 hours of morning (or afternoon), i.e. 120 real data. If every minute of data needs to pay a certain fee, to save costs and not miss too much information (data), one may take the following sampling strategy: Take a real sample every 2 minutes with replacing the samples not collected between 2 minutes with the given number. In fact, people's different needs can correspond to different sampling strategies. Hence, it is important for us to obtain the optimal control chart with the best sampling strategy in change detection for finite or small samples.

In this paper, we propose a performance measure to evaluate the detection performance of a control chart with a given sampling strategy for finite or small samples sequence and prove that the CUSUM control chart with a dynamic non-random control limit is optimal under this measure when the change point is unknown. Moreover, the numerical comparisons of six kinds of sampling strategies that take only a part of all samples are given to illustrate which sampling strategy has a faster monitoring speed.

The remainder of this paper is organized as follows. Section 2 describes a criterion for the optimal control chart with a given sampling strategy. Section 3 presents mainly the optimal CUSUM control chart. Numerical simulations and a real example for comparing several sampling strategies are given in Sections 4 and 5, respectively. Section 6 provides the conclusion and discussion. The proofs of two theorems are given in Appendix.

2. A criterion of optimal control chart with sampling strategy

Consider finite mutually independent observations, . Without loss of generality, we assume . Let τ ( ) be the unknown change point and the pre-change probability density of is before the change point and after the change point the probability density of becomes which is also known. Let and be the probability distribution and the expectation of respectively if a change occurs at the change point . When , this means that a change does not occur in the observations and therefore, the probability distribution and the expectation are denoted by and respectively for all observations .

Generally speaking, any control chart (or sequential test) for change-point detection can be modeled as a stopping time or an alarm time adapted to the filtration , where denotes the smallest σ-algebra with respect to which all of the random variables (observations) are measurable. The optimality of the stopping time usually means that the detection delay measured is in some sense the smallest of all stopping times with a probability of false alarm no greater than a preset level , or, among all stopping times with a false alarm rate no less than a given value , i.e. .

When , Moustakides [9] has proved that the following upper-sided CUSUM chart :

for c>1, is optimal under the following Lorden's measure [6]:

where , with and is the worst average delay, i.e.

However, when , an example given in [5] has shown that the following upper-sided CUSUM chart for N observations

is not optimal in the Lorden's measure , where , , for and .

Note that Lorden's measure is not easy to calculate. It is natural to ask: can we define a measure that is easy to calculate so that a modified CUSUM chart with a given sampling strategy for finite observations is still optimal under this measure?

Because of sampling constraints or to reduce the sampling cost, we need to choose an appropriate sampling strategy for change-point detection. Let denote a sampling strategy satisfying for , in which, or 0 denote that we will take a sample or not take a sample but replace with a constant at time k, respectively, that is, we have a new series of samples, for .

Remark 2.1

We know that for . Hence, when the substitute sample satisfies , it implies that the observation sequence may have a small mean shift at time k. If for , it implies that there is a possible medium or large change mean shift in the observation sequence at time k.

Next, we will present a measure with a sampling strategy to evaluate the detection performance of a control chart for an unknown change point. Let denote the set of all sampling strategies. For a given sampling strategy , let be the set of all control charts, with the sampling strategy S, which satisfy and for , where , for and , the sample space.

The upper-sided CUSUM charting statistics for a given sampling strategy S can be written as for with . As in [5], we define a measure for a given sampling strategy S to evaluate the detection performance of a control chart when detecting an upper-sided change by the following:

| (1) |

which is the average total amount of the detection delay, where and the random weight, , of the detection delay is determined by the information before the change point k since . It can be seen that the smaller , the better performs.

Remark 2.2

One reason to present the delay measure above is that the charting statistic can be considered as that there is a false medium or large change before the change point k, and can denote there being no change or a small false change before the change point k, therefore, taking the weight for the detection delay means that if the charting statistic , we do not need to consider the detection delay , if , we must consider the detection delay . Another motivation is that, by the definition of the charting statistics, with for , we see that when , that is, means that we can restart monitoring the change from time k.

Remark 2.3

To detect the lower-sided changes, for example, the mean shift from to , where , we can take the weight , where is the lower-sided CUSUM charting statistic satisfying for with . The corresponding measure, can be written as

which is the total average amount of the detection delay. In this paper, we only consider upper-sided change detection since lower-sided change detection can be dealt with by similar methods.

A criterion for an optimal control chart, with an optimal sampling strategy is defined by the following:

| (2) |

| (3) |

where the two positive constants γ and β denote the lower bound of the false alarm average time for and the upper bound of the average number of observations, respectively, which satisfy Moreover, the measure can be regarded as the generalized out-of-control average run length ( ).

3. The optimal CUSUM control chart with sampling strategy

To construct the optimal control chart, we first present a series of nonnegative CUSUM charting statistics, for a given sampling strategy in the following:

for , where and . It is clear that for .

As in [5], for a given sampling strategy S, the CUSUM control chart with a nonnegative non-random dynamic control limit, , is defined by the following:

| (4) |

where is determined by the following recursive equations:

for and c>0, is a constant which can be regarded as an adjustment coefficient for the control limits since is increasing in with and for .

The following theorem shows that the CUSUM chart with the dynamic control limit above can be optimal under the measure for any given sampling strategy .

Theorem 3.1

Let γ be a positive number satisfying . For a given , there exists a positive number such that the CUSUM chart the dynamic non-random control limit and , is optimal in the following sense:

(5)

Remark 3.1

It can be seen that Theorem 3.1. cannot give the optimal sampling strategy satisfying the constraint conditions and .

Since it is difficult to prove the optimal sampling strategy in theory, we want to find a relatively good sampling scheme by comparing two sampling strategies. To compare two sampling strategies, we present the definition of a relative increasing strategy below. A sampling strategy is called a relative increasing strategy by comparison with the sampling strategy , if and only if for all , which can be denoted as . The inequality means that strategy can extract more information (samples) than strategy S.

Theorem 3.2 shows that the more samples (information), the better the performance of the corresponding optimal CUSUM control chart.

Theorem 3.2

Let satisfy

(6) and both and be the two optimal CUSUM charts in (5) corresponding to two sampling strategies satisfying . Then

(7) for , and the optimal CUSUM chart satisfies

(8)

Let denote that we take all N samples. It is clear that any sampling strategy satisfies . Hence, we have the following corollary.

Corollary 3.3

Let the conditions in Theorem 3.2 hold. Then

(9)

It can be seen that the optimal CUSUM chart has the best detection performance of all sampling strategies and all control charts subject to a constraint on the false alarm average run length ( ).

Remark 3.2

When the condition (6) does not hold and the two sampling strategies do not meet the relative increase condition, no general theoretical results for the sampling strategies have been obtained, but we will provide numerical simulation results for these cases in the next section.

4. Numerical simulations

By numerical comparisons of the detection performance of the optimal CUSUM chart for seven kinds of sampling strategies in this section, we have two main purposes. One is to see how much the monitoring speed is different between the sampling of all samples and the sampling of missing some samples; the other is see which sampling strategy has a faster monitoring speed among six sampling strategies of missing some samples. The seven sampling strategies compared in this section are as follows, β is the number of observations,

denotes that the observation samples are taken at all times ( ) (full sampling strategy);

represents that we take the observation samples only during the first period;

represents that we take the observation samples only during the last period;

denotes that the observation samples are taken evenly and dispersedly (uniformly dispersed sampling strategy);

denotes the sampling each time with probability of ;

- represents the DE-Shiryaev sampling strategy given in [2] (e.g. take a positive constant A which can be called the warning line, it is lower than the constant control line. If the monitoring statistic is lower than the warning line, next sampling is not required but replacing by a given number. If it is higher than the warning line but lower than the control line, next sampling is required). satisfies

- denotes that if the monitoring statistic is lower than the warning line (a positive constant A), next sampling is not required but replacing by a given number, if it is higher than the warning line, next sampling is required. satisfies

Let and, after the change point , , , are mutually independent. It follows that for . We give numerical simulations to compare the detection performance of four non-random sampling strategies and three random sampling strategies for N = 60. The substitute for an observation value will be taken as 0, 0.25 and 0.5, respectively.

Consider the three cases for the number of observations . As for , if , we take observations at . If , we take observations at And if , we take observations at

Let for the CUSUM control charts with the dynamic control limit and the sampling strategy S considered here. Let the numbers of observations be , and , respectively. The simulation results of the adjustment coefficient , , the warning line A and the measure are listed in Tables 1–9 respectively for and 0.5. Note that the sampling strategy is invalid when .

Table 2.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 1.052 | 0.4619 | 0.86 | 0.862 | 0.82 | – | |

| 20.0032 | 20.0813 | 19.9731 | 20.0655 | 19.9622 | 20.1297 | – | ||

| A | – | – | – | – | – | 0.140 | – | |

| 0.4577 | 4.6915 | 3.4111 | 1.6235 | 1.9111 | 8.4980 | – | ||

| 30 | 1.73 | 1.171 | 0.4620 | 0.982 | 0.995 | 1.005 | 1.475 | |

| 29.9902 | 29.9951 | 30.0538 | 30.0158 | 30.0262 | 29.9522 | 29.9889 | ||

| A | – | – | – | – | – | 0.140 | 0.066 | |

| 0.5426 | 5.2447 | 5.4253 | 1.9208 | 2.1475 | 9.1951 | 3.7056 | ||

| 40 | 2.3 | 1.355 | 0.465 | 1.104 | 1.135 | 1.225 | 1.7 | |

| 40.1787 | 39.9391 | 40.1248 | 40.0953 | 40.1222 | 40.0960 | 40.0162 | ||

| A | – | – | – | – | – | 0.140 | 0.088 | |

| 0.6734 | 5.6734 | 7.4042 | 2.3050 | 2.4641 | 9.6218 | 5.1029 | ||

Table 3.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 1.165 | 0.4619 | 0.985 | 0.987 | 0.95 | – | |

| 20.0032 | 19.9244 | 20.0507 | 20.1278 | 20.1491 | 20.0527 | – | ||

| A | – | – | – | – | – | 0.1065 | – | |

| 0.4577 | 2.4671 | 3.4133 | 1.1217 | 1.2599 | 6.5860 | – | ||

| 30 | 1.73 | 1.34 | 0.465 | 1.12 | 1.14 | 1.155 | – | |

| 29.9902 | 30.0128 | 30.1108 | 30.0102 | 30.0168 | 30.0487 | – | ||

| A | – | – | – | – | – | 0.1065 | – | |

| 0.5426 | 2.9467 | 5.4373 | 1.2505 | 1.3937 | 7.4611 | – | ||

| 40 | 2.3 | 1.625 | 1.115 | 1.28 | 1.33 | 1.485 | 2.01 | |

| 40.1787 | 40.0563 | 40.0474 | 39.9918 | 40.0423 | 39.9682 | 39.9913 | ||

| A | – | – | – | – | – | 0.1065 | 0.062 | |

| 0.6734 | 3.3345 | 5.4259 | 1.4577 | 1.6134 | 8.2570 | 2.8311 | ||

Table 4.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 0.942 | 0.53916 | 0.74 | 0.715 | 0.66 | 1.17 | |

| 20.0032 | 20.027 | 20.0789 | 20.0286 | 19.9733 | 20.1358 | 20.0195 | ||

| A | – | – | – | – | – | 0.192 | 0.065 | |

| 0.4577 | 4.2757 | 2.2781 | 1.6848 | 1.8808 | 6.0869 | 2.2641 | ||

| 30 | 1.73 | 1.038 | 0.53918 | 0.89 | 0.88 | 0.878 | 1.24 | |

| 29.9902 | 30.0239 | 30.0195 | 29.9002 | 29.9605 | 30.0684 | 29.9109 | ||

| A | – | – | – | – | – | 0.192 | 0.093 | |

| 0.5426 | 4.6707 | 3.4101 | 1.9928 | 2.1702 | 6.3001 | 3.3299 | ||

| 40 | 2.3 | 1.16 | 0.53926 | 1.035 | 1.028 | 1.048 | 1.363 | |

| 40.1787 | 40.0412 | 40.0162 | 40.1175 | 40.1207 | 40.0229 | 40.0414 | ||

| A | – | – | – | – | – | 0.192 | 0.12 | |

| 0.6734 | 4.8850 | 4.5296 | 2.3426 | 2.4499 | 6.3192 | 4.4681 | ||

Table 5.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 1.055 | 0.53918 | 0.885 | 0.88 | 0.822 | – | |

| 20.0032 | 19.9324 | 20.1048 | 19.9853 | 20.0289 | 20.1873 | – | ||

| A | – | – | – | – | – | 0.14 | – | |

| 0.4577 | 2.9422 | 2.2650 | 1.2554 | 1.4164 | 5.1551 | – | ||

| 30 | 1.73 | 1.18 | 0.53919 | 1.045 | 1.04 | 1.006 | 1.48 | |

| 29.9902 | 30.0336 | 30.0466 | 30.1060 | 30.2288 | 29.9920 | 29.9486 | ||

| A | – | – | – | – | – | 0.14 | 0.065 | |

| 0.5426 | 3.2835 | 3.3946 | 1.4230 | 1.5462 | 5.5541 | 2.3093 | ||

| 40 | 2.3 | 1.377 | 0.545 | 1.21 | 1.215 | 1.223 | 1.69 | |

| 40.1787 | 40.0162 | 40.0079 | 40.0509 | 39.9874 | 40.0353 | 40.0655 | ||

| A | – | – | – | – | – | 0.14 | 0.089 | |

| 0.6734 | 3.5665 | 4.4235 | 1.6069 | 1.7289 | 5.7974 | 3.2478 | ||

Table 8.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 1.09 | 0.61708 | 0.995 | 0.965 | 0.825 | – | |

| 20.0032 | 20.0708 | 20.0183 | 20.0169 | 20.1259 | 20.0182 | – | ||

| A | – | – | – | – | – | 0.14 | – | |

| 0.4577 | 0.7132 | 0.8083 | 0.7746 | 0.7863 | 0.8555 | – | ||

| 30 | 1.73 | 1.28 | 0.6174 | 1.25 | 1.22 | 1.008 | 1.481 | |

| 29.9902 | 30.2001 | 30.1761 | 29.9333 | 30.1165 | 30.1203 | 29.9841 | ||

| A | – | – | – | – | – | 0.14 | 0.065 | |

| 0.5426 | 0.7857 | 0.8699 | 0.8060 | 0.8174 | 0.8736 | 0.7512 | ||

| 40 | 2.3 | 1.63 | 0.628 | 1.625 | 1.61 | 1.22 | 1.692 | |

| 40.1787 | 40.0782 | 40.0313 | 39.8233 | 40.0579 | 39.9564 | 40.092 | ||

| A | – | – | – | – | – | 0.14 | 0.089 | |

| 0.6734 | 0.8831 | 0.8919 | 0.8889 | 0.8984 | 0.8756 | 0.8599 | ||

Table 1.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 0.938 | 0.4619 | 0.735 | 0.715 | 0.65 | 1.171 | |

| 20.0032 | 19.9971 | 20.3822 | 19.9809 | 20.0154 | 20.0674 | 20.2969 | ||

| A | – | – | – | – | – | 0.192 | 0.066 | |

| 0.4577 | 6.9661 | 3.4816 | 2.3157 | 2.6917 | 10.1051 | 3.4187 | ||

| 30 | 1.73 | 1.032 | 0.4620 | 0.868 | 0.861 | 0.88 | 1.25 | |

| 29.9902 | 30.0134 | 30.1969 | 30.1281 | 30.1413 | 30.1861 | 30.2598 | ||

| A | – | – | – | – | – | 0.192 | 0.093 | |

| 0.5426 | 7.6702 | 5.4208 | 2.8846 | 3.2068 | 10.4783 | 5.3638 | ||

| 40 | 2.3 | 1.145 | 0.4621 | 0.982 | 0.985 | 1.05 | 1.365 | |

| 40.1787 | 39.9446 | 40.2532 | 40.0312 | 40.1859 | 40.1211 | 40.1091 | ||

| A | – | – | – | – | – | 0.192 | 0.12 | |

| 0.6734 | 7.9904 | 7.3986 | 3.4693 | 3.7255 | 10.7379 | 7.375 | ||

Table 9.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 1.205 | 0.6174 | 1.14 | 1.11 | 0.955 | – | |

| 20.0032 | 20.06 | 29.1920 | 19.9856 | 20.0145 | 20.0150 | – | ||

| A | – | – | – | – | – | 0.1065 | – | |

| 0.4577 | 0.5859 | 0.8052 | 0.6780 | 0.6937 | 0.7948 | – | ||

| 30 | 1.73 | 1.44 | 0.628 | 1.425 | 1.39 | 1.155 | – | |

| 29.9902 | 30.1226 | 30.0324 | 30.0104 | 29.9585 | 30.0487 | – | ||

| A | – | – | – | – | – | 0.1065 | – | |

| 0.5426 | 0.6768 | 0.8562 | 0.7345 | 0.7379 | 0.8096 | – | ||

| 40 | 2.3 | 1.85 | 1.115 | 1.852 | 1.85 | 1.49 | 2.008 | |

| 40.1787 | 40.0221 | 40.0474 | 40.0151 | 40.1107 | 40.0735 | 40.0913 | ||

| A | – | – | – | – | – | 0.1065 | 0.0618 | |

| 0.6734 | 0.7949 | 0.8599 | 0.8288 | 0.8485 | 0.8322 | 0.8014 | ||

By comparing the measure of the CUSUM charts with the dynamic control limit for seven sampling strategies , , , , , and in Tables 1–9, we can make the following five conclusions:

For all cases, the full sampling strategy is optimal amongst all seven sampling strategies since its corresponding measure is the least among all measures for the seven sampling strategies.

Excepting the case in Tables 7–9 and the case in Table 6 for , the detection performance of the uniformly dispersed sampling strategy is better than the sampling strategy , the sampling strategy is better than the sampling strategy , the sampling strategy is better than and , and are better than . and , since the measure of is smallest. Meanwhile, the detection performance of and is better than that of and .

For the case in Tables 7–9, the detection performance of the six sampling strategies , , , , and is not too different.

The adjustment coefficient of the dynamic control limit for the sampling strategy is greatest of all adjustment coefficients for the six sampling strategies , , , , and in all cases.

As a whole, among the six sampling strategies that take only a part of samples, the numerical comparing results illustrate that the uniform sampling strategy has the best monitoring effect.

Table 7.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 0.97 | 0.61707 | 0.815 | 0.76 | 0.675 | 1.172 | |

| 20.0032 | 19.9630 | 19.9372 | 20.1206 | 19.9615 | 20.1102 | 20.0484 | ||

| A | – | – | – | – | – | 0.192 | 0.0648 | |

| 0.4577 | 0.8079 | 0.8169 | 0.8617 | 0.8239 | 0.9049 | 0.8033 | ||

| 30 | 1.73 | 1.105 | 0.61709 | 1.075 | 1.01 | 0.885 | 1.245 | |

| 29.9902 | 30.1056 | 30.1513 | 30.0324 | 30.1414 | 30.0291 | 30.0813 | ||

| A | – | – | – | – | – | 0.192 | 0.093 | |

| 0.5426 | 0.8612 | 0.8837 | 0.8906 | 0.8656 | 0.9221 | 0.8632 | ||

| 40 | 2.3 | 1.375 | 0.61780 | 1.425 | 1.325 | 1.051 | 1.36 | |

| 40.1787 | 40.0447 | 40.1382 | 40.2172 | 39.8161 | 40.1768 | 39.9597 | ||

| A | – | – | – | – | – | 0.192 | 0.12 | |

| 0.6734 | 0.9303 | 0.9328 | 0.9501 | 0.9259 | 0.9260 | 0.9269 | ||

Table 6.

Comparison of for with .

| Sampling strategies | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 1.375 | 1.17 | 0.53919 | 1.035 | 1.02 | 0.952 | – | |

| 20.0032 | 19.9407 | 20.0439 | 20.0977 | 20.1199 | 20.1410 | – | ||

| A | – | – | – | – | – | 0.1065 | – | |

| 0.4577 | 1.6404 | 2.2613 | 0.9064 | 1.0074 | 4.0474 | – | ||

| 30 | 1.73 | 1.35 | 0.545 | 1.212 | 1.205 | 1.156 | – | |

| 29.9902 | 30.0331 | 30.0019 | 29.9861 | 30.0344 | 30.1053 | – | ||

| A | – | – | – | – | – | 0.1065 | – | |

| 0.5426 | 1.9422 | 3.3056 | 0.9929 | 1.0905 | 4.5446 | – | ||

| 40 | 2.3 | 1.65 | 1.115 | 1.445 | 1.45 | 1.488 | 2.01 | |

| 40.1787 | 40.1433 | 40.0474 | 40.0477 | 39.9851 | 40.0353 | 40.1093 | ||

| A | – | – | – | – | – | 0.1065 | 0.0618 | |

| 0.6734 | 2.2098 | 3.4268 | 1.1389 | 1.2404 | 5.0067 | 1.8873 | ||

Figure 1 is a diagram of the control limits of four sampling strategies , , and for and . It can be seen that the four dynamic control limits all decrease monotonically.

Figure 1.

A diagram of the control limits of different sampling methods.

5. Real data

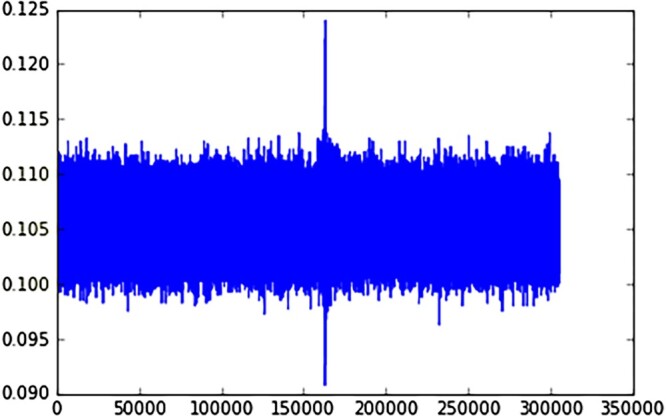

According to the Chinese earthquake network, on 7 January 2015, in Yilan County, an earthquake measuring 5.2 Richter scale occurred. The data measurements (acceleration in a specific direction) from a sensor are recorded from 12:43:32 to 12:53:32 before and after an earthquake. Since the data are at a relatively high frequency (about 500 Hz), we collect data every 2 microseconds. A simple plot of the measurements against time is shown as follows. There is a significant signal in the middle of Figure 2, which should correspond to the earthquake at 12:48:32. In fact, there is a delay of approximately 0.8 seconds in this data.

Figure 2.

The value of accelerations collected by the sensor in the earthquake.

We know that every seismic sensor has a battery inside. Assuming that the sensor collects one sample every microseconds, the service life of the battery is 1 year. To extend the service life of the battery, at the same time, do not lose too much information (data), we can adjust the sensor so that it collects a sample (data) every 2 microseconds. Based on this consideration, we compare the detection performance of the six sampling strategies , and for N = 60 (60 observations) of seismic sensors to see how much the monitoring speed is different between the sampling of all samples and the sampling of missing some samples. Here, means that we take observations in both the first and last periods. That is, we take observations at .

We first normalize the data by the pre-change mean and variance. Then the pre-change distribution can be approximated as and the post-change distribution as . Accordingly, the likelihood ratio is approximated. The substitute for observation value is . Consider the three cases with numbers of observations and 30. For , we take observations at , and , respectively for and 12.

Let for the CUSUM control chart with the dynamic control limit and the sampling strategy S considered here. The simulation results are listed in Tables 10–12 for , and , respectively.

Table 11.

Comparisons of for with .

| Sampling strategies | |||||||

|---|---|---|---|---|---|---|---|

| 20 | 0.492 | 0.436 | 0.3937 | 0.385 | 0.38 | 0.409 | |

| 20.1 | 19.9847 | 20.0314 | 20.0119 | 20.0978 | 19.9267 | ||

| A | – | – | – | – | – | 0.9662 | |

| 0.2131 | 7.3484 | 8.8998 | 1.4004 | 2.0166 | 13.7606 | ||

| 30 | 0.57 | 0.486 | 0.4358 | 0.4357 | 0.4356 | 0.44 | |

| 29.9636 | 29.9018 | 30.2007 | 30.1277 | 30.1620 | 29.9118 | ||

| A | – | – | – | – | – | 0.9662 | |

| 0.2452 | 8.7327 | 9.5817 | 1.5448 | 2.1545 | 14.2786 | ||

| 40 | 0.705 | 0.535 | 0.489 | 0.49 | 0.491 | 0.505 | |

| 40.2044 | 40.2213 | 39.7759 | 39.9962 | 40.1309 | 40.0014 | ||

| A | – | – | – | – | – | 0.9662 | |

| 0.2666 | 9.4934 | 10.3945 | 1.5842 | 2.1596 | 14.4995 | ||

Table 10.

Comparisons of for with .

| Sampling strategies | |||||||

|---|---|---|---|---|---|---|---|

| 20 | 0.492 | 0.4 | 0.358 | 0.35 | 0.341 | 0.3575 | |

| 20.1 | 19.9667 | 20.3461 | 19.9128 | 20.1344 | 20.9090 | ||

| A | – | – | – | – | – | 0.975 | |

| 0.2131 | 12.0601 | 14.0645 | 2.5005 | 3.4470 | 17.7804 | ||

| 30 | 0.57 | 0.436 | 0.3937 | 0.3933 | 0.39299 | 0.3936 | |

| 29.9636 | 30.0716 | 30.1626 | 30.0058 | 29.6563 | 29.9852 | ||

| A | – | – | – | – | – | 0.975 | |

| 0.2452 | 13.3404 | 14.2171 | 2.6707 | 3.8024 | 18.0551 | ||

| 40 | 0.705 | 0.4892 | 0.4358 | 0.436 | 0.4363 | 0.45 | |

| 40.2044 | 40.0470 | 39.9516 | 40.0173 | 40.0552 | 40.057 | ||

| A | – | – | – | – | – | 0.975 | |

| 0.2666 | 13.9110 | 14.7122 | 2.9020 | 3.8802 | 18.2491 | ||

Table 12.

Comparisons of for with .

| Sampling strategies | |||||||

|---|---|---|---|---|---|---|---|

| 20 | 0.492 | 0.4633 | 0.4353 | 0.414 | 0.4135 | 0.4354 | |

| 20.1 | 19.9520 | 20.1454 | 20.0048 | 20.1483 | 19.9642 | ||

| A | – | – | – | – | – | 0.959 | |

| 0.2131 | 3.4562 | 5.3101 | 0.7657 | 1.1008 | 9.7635 | ||

| 30 | 0.57 | 0.515 | 0.468 | 0.468 | 0.467 | 0.487 | |

| 29.9636 | 30.0518 | 30.0045 | 29.8777 | 29.9630 | 30.0837 | ||

| A | – | – | – | – | – | 0.959 | |

| 0.2452 | 4.54054 | 5.7852 | 0.8118 | 1.1475 | 10.3039 | ||

| 40 | 0.705 | 0.6 | 0.535 | 0.537 | 0.54 | 0.555 | |

| 40.2044 | 40.1145 | 40.1159 | 39.9882 | 39.9543 | 40.062 | ||

| A | – | – | – | – | – | 0.959 | |

| 0.2666 | 5.2234 | 5.9845 | 0.8637 | 1.1861 | 10.8010 | ||

It can be seen from Tables 10–12 that the full sampling strategy, , is best, and the uniformly dispersed sampling strategy, , is also good, being better than the sampling strategies , , and .

6. Conclusion and discussion

In this paper, for finite or small samples we obtain two theoretical results: one is that for a given sampling strategy S, the CUSUM chart with the dynamic non-random control limit is optimal under the measure , and the other is that if and condition (10) holds, the optimal CUSUM chart is better than the optimal CUSUM chart , therefore, the optimal CUSUM chart has the best detection performance of all sampling strategies and all control charts subject to a constraint on the false alarm average run length ( ).

The numerical simulations in Tables 1–9 illustrate that when substitutes for the observation value, which does not satisfy condition (10), the optimal CUSUM chart still has the best detection performance for the number of observations , and . This leads to the following problem: can the result of Theorem 3.2 still hold for ? Here, but the condition (10) implies that . In other words, the condition is more general than (10).

When the number of samples is restricted, or the number of samples is limited to reduce the cost of sampling, we see from Tables 1–12 that the uniformly dispersed sampling strategy is better than the sampling strategies , , , , and except in the case where . Therefore, we prefer to recommend the use of a uniformly dispersed sampling strategy when the number of samples is less than the total number of samples. Further, this leads to another problem: is the uniformly dispersed sampling strategy best among all sampling strategies with the same number of samples when ?

The above two problems are worthy of further study.

Acknowledgments

The authors would like to thank two referees and one associate editor for their many valuable comments that have improved and perfected our article.

Appendix: Proofs of Theorems.

Proof Proof of Theorem 3.1 —

Let and . We first prove the following equality:

(A1) where is the indicator function. Since

and , it follows that

Thus

since and . Note that for , we further have

This is (A1). Let

(A2) for , be a series of random variables, where a>0 is a constant. It follows from (A1) and (A2) that

(A3) Let . By a similar method of proof to Theorems 1 and 3 in [5] we can prove that

(A4) for every , and that there is a positive constant and a dynamic non-random control limit such that .

Note that . By (A3) and (A4) we have for as long as , which means (5). This completes the proof.

Proof Proof of Theorem 3.2 —

It follows from Theorem 3.1 that

(A5) for . Hence, to prove (7), it is only necessary to show

(A6) Note that , , , , , and . It follows that

and furthermore

By using and mathematical induction, we find that

for , and therefore, (A6) holds. Thus (7) follows from (A5) and (A6), and (7) implies (8). This completes the proof.

Funding Statement

This work was supported by the National Natural Science Foundation of China (11531001) and RGC Competitive Earmarked Research Grants.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- 1.Banerjee T. and Veeravalli V.V, (2011). Bayesian quickest change detection under energy constraints, in Information Theory and Applications. Workshop, IEEE, 1–10

- 2.Banerjee T. and Veeravalli V.V., Data-efficient quickest change detection in minimax settings, IEEE. Trans. Inf. Theory. 59 (2013), pp. 6917–6931. [Google Scholar]

- 3.Frisén M, Optimal sequential surveillance for finance, public health, and other areas (with discussion), Seq. Anal. 28 (2009), pp. 310–337. [Google Scholar]

- 4.Geng J., Bayraktar E., and Lai L.F., Bayesian quickest change-point detection with sampling constraints, IEEE Trans. Inf. Theory. 60 (2014), pp. 6474–6490. [Google Scholar]

- 5.Han D., Tsung F.G., Xian J.G., and Yu M.M, Optimal sequential tests for monitoring changes in the distribution of finite observation sequences, Stat. Sin. 32 (2022), pp. 1317–1342. [Google Scholar]

- 6.Johnson P., Moriarty J., and Peskir G, Detecting changes in real-time data: a user's guide to optimal detection, Phil. Trans. R. Soc. A. 375 (2021), pp. 20160298. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Lorden G, Procedures for reacting to a change in distribution, Ann. Math. Stat. 42 (1971), pp. 1897–1908. [Google Scholar]

- 8.Montgomery D.C, Introduction to Statistical Quality Control, 6th ed, John Wiley & Sons, New York, 2009. [Google Scholar]

- 9.Moustakides G.V, Optimal stopping times for detecting changes in distribution, Ann. Stat. 14 (1986), pp. 1379–1387. [Google Scholar]

- 10.Nath S. and Wu J.X, Quickest change point detection with multiple postchange models, Seq. Anal. 39 (2020), pp. 543–562. [Google Scholar]

- 11.Pollak M, Optimal detection of a change in distribution, Ann. Stat. 13 (1985), pp. 206–227. [Google Scholar]

- 12.Polunchenko A.S. and Tartakovsky A.G, On optimality of the Shiryaev–Roberts procedure for detecting a change in distribution, Ann. Stat. 38 (2010), pp. 3445–3457. [Google Scholar]

- 13.Premkumar V.K. and Kumar A, (2008). Optimal sleep-wake scheduling for quickest intrusion detection using wireless sensor networks, INFOCOM. The 27th Conference on Computer Communications, 1400–1408

- 14.Qiu P., Introduction to Statistical Process Control, Boca Raton, FL, Chapman and Hall/CRC, 2014. [Google Scholar]

- 15.Ren X.Q., Johansson K.H., Shi D.W., and Shi L., Quickest change detection in adaptive censoring sensor network, IEEE Trans. Control. Netw. Syst. 5 (2018), pp. 239–250. [Google Scholar]

- 16.Shiryaev A.N., Optimal Stopping Rules, Springer-Verlag, New York, 1978. [Google Scholar]

- 17.Siegmund D, Change-points: from sequential detection to biology and back, Seq. Anal. 32 (2013), pp. 2–14. [Google Scholar]

- 18.Tartakovsky A.G, Asymptotic optimality in Bayesian change-point detection problems under global false alarm probability constraint, Theory Probab. Appl. 53 (2009), pp. 443–466. [Google Scholar]

- 19.Woodall W.H. and Montgomery D.C, Some current directions in the theory and application of statistical process monitoring, J. Qual. Technol. 46 (2014), pp. 78–94. [Google Scholar]

- 20.Woodall W.H., Zhao M.J., Paynabar K., Sparks R., and Wilson J.D, An overview and perspective on social network monitoring, IIE Trans. 49 (2017), pp. 354–365. [Google Scholar]