Abstract

Objective:

To examine the prevalence of lack of health insurance and its changes over time among adult residents (aged 18–64 years) in 50 states and the District of Columbia (DC).

Study design:

Cross-sectional surveys.

Methods:

We aggregated annual state-based Behavioral Risk Factor Surveillance System (BRFSS) data from 1993 through 2014 to provide nationwide and state-based prevalence estimates for lack of insurance among adults aged 18–64 years. The adjusted prevalence was estimated using log-linear regression analyses with a robust variance estimator after controlling for demographic variables. The trend was assessed separately for the periods 1993–2010 and 2011–2014 due to methodologic changes in the BRFSS.

Results:

From 1993 through 2010, the adjusted prevalence of lack of health insurance increased by 0.54% (P < 0.0001) annually (range: 16.3% in 1995 to 19.1% in 2005); this prevalence decreased significantly in 2014 (15.1%). In 2014, Georgia, Mississippi, and Texas had the highest adjusted prevalences (range: 23.0–24.6%) of lack of health insurance, and DC, Massachusetts, and Rhode Island had the lowest (range: 6.2–10.1%). The changes in the prevalence of lack of insurance over time varied significantly by state.

Conclusions:

The nationwide prevalence of lack of health insurance decreased significantly in the past few years, especially in 2014 when about one-seventh of Americans aged 18–64 years reported lack of health insurance coverage. The huge variations in the prevalence of lack of health insurance and its changes over time among states suggest continuing efforts to ensure healthcare access for all Americans are needed to improve the overall health of the population.

Keywords: Health insurance, Healthcare access, Behavioral Risk Factor Surveillance, System (BRFSS)

Introduction

Access to health care is an important measure in public health programs and may contribute to the prevention and management of diseases and improvement of overall well-being of the population. In the United States, health insurance coverage has historically improved access to health care,1–4 and thus has been used as a proxy for access to health care, although issues related to quality of care, timeliness of services, availability of services, deductibles, and other out-of-pocket expenses still exist among people with healthcare coverage. On the other hand, lacking health insurance has been associated with delayed diagnosis and treatment of medical conditions, poorer health outcomes, and worse health-related quality of life.5–7 Passage of the 2010 Affordable Care Act (ACA; PL 111–148; PL 111–152) helped more US residents gain health insurance coverage,8,9 effectively providing better access to health services (e.g., clinical preventive services and treatment) that may improve the overall health of Americans.10,11 Current Congressional Budget Office estimates indicate that by 2018, 24 million more working-aged Americans will have obtained private insurance through new health insurance exchanges and 12 million Americans will have gained coverage under Medicaid.12 These healthcare reforms were not only associated with improved access to care, but also associated with reduced mortality and improved self-rated health.13,14

Surveillance data from the National Health Interview Survey (NHIS) have shown a generally increasing trend in the prevalence of lack of insurance among US adults aged 18–64 years between 1997 and 2010 and then a decreasing trend between 2010 and the first nine months of 2014.15 These findings are similar to those from the US Census.16 However, prevalence estimates for lack of health insurance over time in individual states are largely unknown. The Behavioral Risk Factor Surveillance System (BRFSS), a state-based survey, provides data on health conditions, health behaviors, and healthcare access and utilization for all states, the District of Columbia (DC), and other participating US territories. Therefore, in this study, we aggregated annual state-based BRFSS data from 1993 through 2014 to provide nationwide and state-based prevalence estimates for lack of health insurance and to examine how the prevalence of lack of health insurance changed over two time periods (i.e., 1993 through 2010 and 2011 through 2014) by sociodemographic characteristics (age, gender, race/ethnicity, education, marital status, and employment status) and by state.

Methods

Data for this study came from the BRFSS, a population-based telephone survey conducted annually in all 50 states, DC, and selected US territories. The purpose of the BRFSS is to collect health information including health-related behavioral risk factors, preventive health practices, healthcare access, and chronic conditions among non-institutionalized US adults aged 18 years or older. The BRFSS survey design, sampling methods, data collection, and weights have been described elsewhere.17–19 The BRFSS has been reviewed by the Human Research Protection Office at the Centers for Disease Control and Prevention and determined to be exempt research.

Since 1993, data on healthcare access were collected from almost all 50 states and DC (with the exceptions that some states did not participate in BRFSS in some years [i.e., Wyoming in 1993, Rhode Island in 1994, DC in 1995, and Hawaii in 2004]). From 1993 through 2010, states conducted the BRFSS surveys on landline telephones only. In 2011, BRFSS survey methodology changed in two ways: 1) it uses a dual-frame (i.e., landline and cellular phone) sampling design; and 2) it uses a new weighting methodology—iterative proportional fitting (or raking) to replace the poststratification weighting method used previously.20 The median survey response rate ranged from 71.4% for the 1993 BRFSS to 46.4% for the 2013 BRFSS.21 The sample size ranged from 102,263 in 1993 to 506,467 in 2011.

Health insurance coverage, the main outcome variable for this study, was assessed by asking the participants ‘Do you have any kind of health care coverage, including health insurance, prepaid plans such as health maintenance organizations (HMOs), or government plans such as Medicare?’ In the 2011–2014 BRFSS, the Indian Health Service was also included as a form of healthcare coverage. We limited our analysis to adults aged 18–64 years because those aged 65 years or older are generally covered by Medicare. The responses to the question were dichotomized as yes (for having any health insurance coverage) = 0/no (lack of insurance) = 1.

The covariates for this study included respondents’ age (categorized as 18–24, 25–44, 45–64 years), sex, race/ethnicity (non-Hispanic white, non-Hispanic black, Hispanic, or others—including Asian, American Indian or Alaska Native, Native Hawaiian or Other Pacific Islander, and any other races), education (<high school, high school graduate/GED, some college, or ≥college), marital status (married, previously married—i.e., divorced/widowed/separated, never married/member of an unmarried couple), and employment status (employed for wages, self-employed, unemployed, or others—including homemaker, student, retired, and unable to work).

Statistical analysis

We first excluded adults aged 65 years and older who participated in the surveys during the study period 1993 to 2014. We further excluded those adults aged 18–64 years who responded ‘don’t know/not sure,’ refused to answer, or had missing responses to any of the study variables from the study. We estimated the weighted prevalence of lack of insurance by demographic characteristics and by survey year and age-standardized to the 2000 projected US population. For each survey year, the adjusted prevalence estimates were computed by conducting log-linear regression analyses with a robust variance estimator using lack of insurance as the outcome after adjustment for the demographic covariates described previously. Due to the changes in BRFSS sampling frame and weighting methodology implemented since 2011, we tested the changes over time in lack of insurance separately for the periods 1993–2010 and 2011–2014. From 1993 through 2010, the regression coefficients (β) of the survey year (we used β*100 to obtain an absolute change per year) were used to assess the changes over time in the prevalence of lack of insurance after controlling for demographic characteristics. From 2011 through 2014, linear and quadratic trends were tested by applying orthogonal polynomial contrast coefficients to the regression models. The prevalence estimates of lack of insurance by state were reported for selected years (1995, 2000, 2005, 2010, and 2011–2014). We used SAS (version 9.3, SAS Institute Co, Cary, NC) and SUDAAN software (release 9.0; Research Triangle Institute, Research Triangle Park, NC) to account for the multistage, disproportionate stratified sampling design. A P-value of <0.05 denotes a statistical significance.

Results

Of all survey participants aged 18 years or older who resided in the 50 states and DC, adults aged 65 years or older accounted for 19.0% in 2000 to 35.6% in 2014 and were excluded from the study. After further excluding adults aged 18–64 years who responded ‘don’t know/not sure,’ refused to answer, or had missing responses to any of the study variables (ranging from 0.6% in 1993 to 3.3% in 2014), eligible sample sizes ranged from 81,488 in 1993 to 328,059 in 2011 for our analysis.

Demographic characteristics

From 1993 through 2010, the proportions of young adults (aged 18–24 years), non-Hispanic whites, adults employed for wages, and adults with lower educational attainment (<high school graduate) decreased gradually (data not shown). During 2011–2014, the proportion of young adults rebounded to the levels as shown in the 1990s. The proportions of non-Hispanic whites and of adults employed for wages also decreased from 2011 to 2014, but the proportions of non-Hispanic blacks, Hispanics, adults of other racial groups, and unemployed adults increased from 2003 to 2010 and also increased from 2011 to 2014.

Age-standardized prevalence of lack of insurance

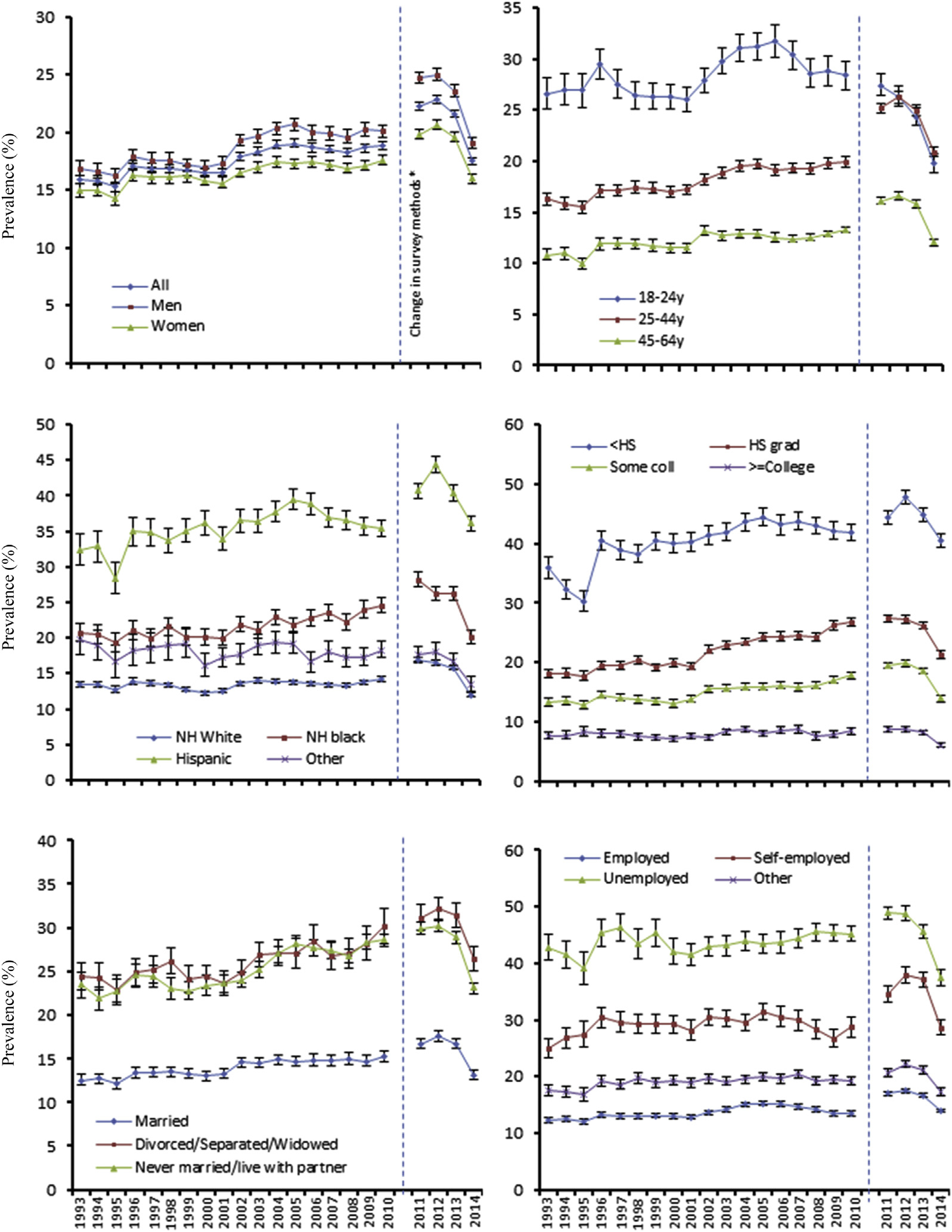

Overall, the age-standardized prevalence of lack of insurance ranged from 15.3% in 1995 to 19.0% in 2005 before 2011, and from 22.8% in 2012 to 17.5% in 2014 afterward. Within each year, the prevalence of lack of insurance varied by demographic characteristics (Fig. 1). Specifically, the prevalence of lack of insurance was higher among younger adults (aged 18–24 years during the period 1993–2010 or aged 18–44 years during the period 2011–2014) than among older adults (aged 45–64 years); higher among men than women; highest among Hispanics and lowest among non-Hispanic whites; highest among adults with less than a high school education and lowest among adults with a college education or more; higher among previously married or unmarried adults than married adults; and highest among unemployed adults and lowest among adults employed for wages for both time periods(Fig.1).

Fig. 1 –

Age-standardized prevalence (with 95% CI) of lack of health insurance among US adults aged 18–64 years by demographic characteristics and by survey year, BRFSS 1993 through 2014. Since the BRFSS survey methodology changed in 2011, results from 1993 through 2010 should not be compared with those from 2011 through 2014. Coll = college; grad = graduate; HS = high school; NH = non-Hispanic.

Adjusted prevalence of lack of insurance

Within each year, the multivariable-adjusted prevalence estimates for lack of insurance presented similar patterns to the age-standardized prevalence estimates in individual demographic groups (Table 1, for estimates for individual years, please see Appendix Table 1).

Table 1 –

Adjusteda prevalence (with standard error) of lack of health insurance among adults aged 18–64 years, by demographic characteristics and by survey year, BRFSS, 1993 through 2010.b

| Demographic characteristic | 1995 | 2000 | 2005 | 2010 | β | P-value |

|---|---|---|---|---|---|---|

|

| ||||||

| n | 89,765 | 144,176 | 257,231 | 284,702 | ||

| All | 16.3 (0.3) | 17.3 (0.2) | 19.1 (0.2) | 18.8 (0.2) | 0.0054 | <0.0001 |

| Age (years) | ||||||

| 18–24 | 19.6 (0.8) | 19.2 (0.5) | 20.8 (0.5) | 18.2 (0.5) | 0.0013 | 0.2677 |

| 25–44 | 16.6 (0.3) | 17.9 (0.3) | 20.6 (0.3) | 20.7 (0.2) | 0.0062 | <0.0001 |

| 45–64 | 10.7 (0.3) | 12.6 (0.3) | 15.1 (0.2) | 15.1 (0.2) | 0.0094 | <0.0001 |

| Sex | ||||||

| Men | 16.3 (0.4) | 16.9 (0.3) | 19.9 (0.3) | 18.6 (0.2) | 0.0043 | <0.0001 |

| Women | 14.6 (0.3) | 15.9 (0.2) | 17.7 (0.2) | 17.6 (0.2) | 0.0069 | <0.0001 |

| Race/ethnicity | ||||||

| Non-Hispanic white | 13.7 (0.2) | 13.2 (0.2) | 15.0 (0.2) | 14.9 (0.2) | 0.0042 | <0.0001 |

| Non-Hispanic black | 15.7 (0.5) | 16.8 (0.5) | 18.0 (0.4) | 19.0 (0.4) | 0.0092 | <0.0001 |

| Hispanic | 23.0 (1.0) | 27.2 (0.6) | 29.6 (0.6) | 27.1 (0.5) | 0.0067 | <0.0001 |

| Other | 18.2 (1.3) | 17.8 (0.9) | 20.5 (0.7) | 19.2 (0.6) | −0.0058 | 0.0067 |

| Education | ||||||

| <High school | 25.6 (0.8) | 29.7 (0.6) | 32.1 (0.6) | 30.1 (0.6) | 0.0049 | <0.0001 |

| High school graduate | 17.9 (0.4) | 19.9 (0.3) | 23.3 (0.3) | 23.6 (0.3) | 0.0114 | <0.0001 |

| Some college | 13.3 (0.4) | 13.4 (0.3) | 16.5 (0.3) | 17.6 (0.3) | 0.0069 | <0.0001 |

| ≥College | 8.7 (0.4) | 7.6 (0.2) | 8.6 (0.2) | 8.6 (0.2) | −0.0053 | 0.0001 |

| Marital status | ||||||

| Married | 11.4 (0.3) | 12.4 (0.2) | 14.4 (0.2) | 14.0 (0.2) | 0.0094 | <0.0001 |

| Divorced/separated/widowed | 21.1 (0.8) | 21.3 (0.5) | 23.5 (0.5) | 23.6 (0.4) | 0.0064 | <0.0001 |

| Other | 20.5 (0.6) | 21.1 (0.4) | 24.2 (0.4) | 23.2 (0.3) | 0.0037 | <0.0001 |

| Employment | ||||||

| Employed for wages | 12.4 (0.3) | 13.3 (0.2) | 15.7 (0.2) | 13.5 (0.2) | 0.0088 | <0.0001 |

| Self-employed | 29.5 (1.0) | 32.2 (0.8) | 32.0 (0.7) | 29.2 (0.6) | 0.0019 | 0.1077 |

| Unemployed | 27.5 (1.4) | 29.1 (0.9) | 32.6 (0.8) | 33.8 (0.5) | 0.0023 | 0.0293 |

| Other | 15.2 (0.5) | 16.7 (0.4) | 17.4 (0.3) | 16.0 (0.3) | 0.0022 | 0.0303 |

Adjusted for all other demographic variables listed. β: regression coefficient for survey year (continuous).

Although all years of data were included in the trend analyses, data are depicted only for selected years (1995, 2000, 2005, 2010) to reduce the size of the table. For all years (1993 through 2010), please see Appendix Table 1.

Trends in the adjusted prevalence of lack of insurance by demographic characteristics

From 1993 through 2010, the prevalence of lack of insurance generally increased by 0.54% per year (P < 0.0001, Table 1). Within levels of demographic characteristics, significantly increasing trends were observed among both men and women; adults aged 25 years or older; non-Hispanic whites, non-Hispanic blacks, and Hispanics; adults with less than a college education; all marital groups; and adults employed for wages, unemployed, and other employment group. Significantly decreasing trends were observed among adults in other racial groups and among adults with a college education or more.

From 2011 through 2014, the prevalence of lack of insurance peakedin2012, and then decreased significantly (showing both significant linear and quadratic trends, P < 0.0001, Table 2). Compared with 2011 and 2012, the prevalence of lack of insurance decreased by 4.4% in 2013 and by 22.6% in 2014. The 2012 peak and subsequent decrease in the prevalence of lack of insurance occurred in all demographic subgroups except that non-Hispanic whites and blacks and unemployed adults showed no peak but only a decreasing trend (Table 2).

Table 2 –

Adjusteda prevalence (with standard error) of lack of health insurance among adults aged 18–64 years, by demographic characteristics and by survey year, BRFSS, 2011 through 2014.b

| Demographic characteristic | 2011 | 2012 | 2013 | 2014 | P for linear | P for quadratic |

|---|---|---|---|---|---|---|

|

| ||||||

| n | 328,059 | 305,494 | 311,101 | 284,144 | ||

| All | 18.9 (0.1) | 19.2 (0.1) | 18.4 (0.1) | 15.1 (0.1) | <0.0001 | <0.0001 |

| Age (years) | ||||||

| 18–24 | 20.6 (0.4) | 20.9 (0.4) | 19.4 (0.4) | 16.2 (0.4) | <0.0001 | <0.0001 |

| 25–44 | 25.1 (0.2) | 25.7 (0.3) | 24.9 (0.3) | 20.4 (0.2) | <0.0001 | <0.0001 |

| 45–64 | 18.4 (0.2) | 18.9 (0.2) | 17.6 (0.2) | 13.5 (0.2) | <0.0001 | <0.0001 |

| Sex | ||||||

| Men | 23.0 (0.2) | 23.2 (0.2) | 21.9 (0.2) | 17.7 (0.2) | <0.0001 | <0.0001 |

| Women | 20.4 (0.2) | 21.2 (0.2) | 19.9 (0.2) | 16.2 (0.2) | <0.0001 | <0.0001 |

| Race/ethnicity | ||||||

| Non-Hispanic white | 18.2 (0.2) | 17.8 (0.2) | 16.9 (0.2) | 13.0 (0.2) | <0.0001 | n.s. |

| Non-Hispanic black | 23.0 (0.4) | 21.9 (0.4) | 21.8 (0.4) | 17.0 (0.4) | <0.0001 | n.s. |

| Hispanic | 31.4 (0.4) | 34.0 (0.5) | 31.0 (0.4) | 26.4 (0.4) | <0.0001 | <0.0001 |

| Other | 19.8 (0.6) | 20.4 (0.6) | 18.9 (0.6) | 15.6 (0.6) | <0.0001 | <0.0001 |

| Education | ||||||

| <High school | 34.1 (0.5) | 35.1 (0.5) | 33.9 (0.5) | 30.2 (0.5) | <0.0001 | <0.0001 |

| High school graduate | 25.3 (0.3) | 25.4 (0.3) | 24.3 (0.3) | 19.7 (0.3) | <0.0001 | <0.0001 |

| Some college | 19.8 (0.3) | 20.2 (0.3) | 18.8 (0.3) | 14.0 (0.2) | <0.0001 | <0.0001 |

| ≥College | 9.6 (0.2) | 9.8 (0.2) | 8.9 (0.2) | 6.8 (0.2) | <0.0001 | <0.0001 |

| Marital status | ||||||

| Married | 16.2 (0.2) | 16.5 (0.2) | 15.7 (0.2) | 12.8 (0.2) | <0.0001 | <0.0001 |

| Divorced/separated/widowed | 26.3 (0.4) | 27.5 (0.4) | 26.5 (0.4) | 21.3 (0.4) | <0.0001 | <0.0001 |

| Other | 26.1 (0.3) | 26.2 (0.3) | 24.9 (0.3) | 20.0 (0.3) | <0.0001 | <0.0001 |

| Employment | ||||||

| Employed for wages | 17.6 (0.2) | 18.2 (0.2) | 17.3 (0.2) | 14.6 (0.2) | <0.0001 | <0.0001 |

| Self-employed | 34.3 (0.6) | 36.2 (0.6) | 35.5 (0.6) | 28.1 (0.6) | <0.0001 | <0.0001 |

| Unemployed | 37.5 (0.5) | 37.5 (0.5) | 35.7 (0.5) | 28.6 (0.6) | <0.0001 | <0.0001 |

| Other | 17.9 (0.3) | 18.7 (0.3) | 17.4 (0.3) | 14.0 (0.3) | <0.0001 | <0.0001 |

Adjusted for all other demographic variables listed. n.s.: not significant.

Since the BRFSS survey methodology changed in 2011, results from 1993 through 2010 should not be compared with results from 2011 through 2014.

Adjusted prevalence of lack of insurance and the trends over time by state

From 1995 through 2010, the prevalence of lack of insurance varied significantly across the states (Table 3). Overall, Arkansas, Louisiana, and Montana had the highest prevalences of lack of insurance (ranging from 24.6% to 26.3% in 2010), and Massachusetts, Hawaii, and DC had the lowest (ranging from 6.3% to 8.9% in 2010). From 1995 through 2010, the adjusted prevalence of lack of insurance significantly increased in 25 states, especially in Georgia, Michigan, Nebraska, South Carolina, Tennessee, and Wisconsin. The adjusted prevalence of lack of insurance significantly decreased in three states (California, Maine, and Massachusetts) and DC (Table 3).

Table 3 –

Adjusteda prevalence (with standard error) of lack of health insurance among adults aged 18–64 years, by state (including DC) and by survey year, BRFSS, 1995 through 2010.

| State | 1995 | 2000 | 2005 | 2010 | β | P-value |

|---|---|---|---|---|---|---|

|

| ||||||

| Alabama | 16.9 (1.1) | 20.7 (1.2) | 21.9 (1.2) | 21.1 (0.9) | 0.0406 | 0.0937 |

| Alaska | 16.3 (1.4) | 20.7 (1.5) | 19.1 (1.3) | 22.5 (2.0) | 0.0678 | 0.0727 |

| Arizona | 16.7 (1.2) | 18.6 (1.5) | 21.4 (1.4) | 16.6 (1.1) | 0.0196 | 0.5008 |

| Arkansas | 19.4 (1.2) | 23.5 (1.1) | 25.3 (0.9) | 26.3 (1.5) | 0.0864 | 0.0006 |

| California | 17.6 (1.0) | 15.8 (0.6) | 14.6 (0.6) | 14.6 (0.4) | −0.0692 | 0.0009 |

| Colorado | 16.8 (1.1) | 17.0 (1.1) | 19.1 (0.7) | 18.5 (0.7) | 0.0286 | 0.2057 |

| Connecticut | 12.0 (1.0) | 11.6 (0.7) | 13.0 (0.8) | 14.1 (1.0) | 0.0242 | 0.4961 |

| Delaware | 14.7 (1.0) | 11.4 (1.0) | 11.8 (0.9) | 14.2 (1.2) | −0.0431 | 0.2747 |

| District of Columbia | – | 11.9 (0.9) | 12.1 (1.0) | 8.9 (0.9) | −0.1723 | 0.0057 |

| Florida | 19.4 (0.9) | 20.0 (0.7) | 23.7 (0.8) | 21.5 (0.7) | 0.0445 | 0.0076 |

| Georgia | 11.6 (0.9) | 17.4 (0.8) | 20.3 (0.9) | 22.5 (1.0) | 0.1896 | <0.0001 |

| Hawaii | 6.5 (0.7) | 7.6 (0.5) | 9.6 (0.6) | 7.5 (0.7) | 0.0225 | 0.5420 |

| Idaho | 18.7 (0.9) | 23.7 (0.8) | 24.0 (0.9) | 24.9 (1.0) | 0.0652 | 0.0004 |

| Illinois | 14.3 (0.9) | 14.1 (0.8) | 17.7 (0.9) | 16.1 (1.0) | 0.0358 | 0.1744 |

| Indiana | 13.5 (0.9) | 14.3 (0.9) | 20.5 (0.8) | 19.8 (0.8) | 0.1202 | <0.0001 |

| Iowa | 13.7 (0.8) | 13.5 (0.9) | 16.3 (0.9) | 15.9 (1.0) | 0.0263 | 0.3488 |

| Kansas | 16.2 (1.2) | 15.8 (0.8) | 18.8 (0.7) | 18.9 (0.8) | 0.0307 | 0.2530 |

| Kentucky | 18.1 (1.0) | 19.1 (0.8) | 23.8 (1.0) | 23.6 (1.1) | 0.0803 | 0.0003 |

| Louisiana | 22.7 (1.2) | 24.2 (0.8) | 26.3 (1.2) | 24.6 (0.9) | 0.0131 | 0.4993 |

| Maine | 21.0 (1.4) | 19.1 (1.3) | 18.1 (1.0) | 17.7 (0.9) | −0.0935 | 0.0007 |

| Maryland | 11.8 (0.6) | 13.0 (0.8) | 15.9 (0.7) | 14.4 (0.8) | 0.0504 | 0.0301 |

| Massachusetts | 13.6 (1.1) | 11.0 (0.5) | 13.3 (0.7) | 6.3 (0.4) | −0.2118 | <0.0001 |

| Michigan | 11.3 (0.8) | 11.7 (0.9) | 17.1 (0.6) | 18.3 (0.8) | 0.1642 | <0.0001 |

| Minnesota | 11.0 (0.6) | 11.5 (0.9) | 10.8 (1.1) | 13.8 (1.1) | 0.0280 | 0.4346 |

| Mississippi | 16.1 (1.2) | 23.1 (1.2) | 22.0 (1.0) | 24.1 (0.9) | 0.0941 | 0.0001 |

| Missouri | 21.1 (1.5) | 16.3 (0.9) | 18.2 (1.2) | 20.3 (1.2) | −0.0209 | 0.5217 |

| Montana | 22.2 (1.6) | 22.4 (1.3) | 29.6 (1.3) | 25.2 (1.3) | 0.0606 | 0.0218 |

| Nebraska | 11.3 (1.0) | 13.4 (0.8) | 20.0 (0.9) | 19.6 (1.0) | 0.1643 | <0.0001 |

| Nevada | 16.0 (1.1) | 16.3 (1.1) | 21.5 (1.1) | 21.1 (1.4) | 0.1004 | 0.0010 |

| New Hampshire | 16.2 (1.3) | 12.9 (1.2) | 17.1 (0.8) | 18.8 (1.0) | 0.0536 | 0.1249 |

| New Jersey | 9.4 (1.1) | 14.8 (0.7) | 17.2 (0.5) | 14.7 (0.6) | 0.1122 | 0.0003 |

| New Mexico | 18.9 (1.3) | 20.5 (0.8) | 20.4 (0.7) | 16.7 (0.8) | −0.0182 | 0.4045 |

| New York | 12.9 (0.8) | 14.5 (0.8) | 14.8 (0.7) | 13.7 (0.6) | −0.0184 | 0.4550 |

| North Carolina | 15.6 (0.9) | 16.9 (1.0) | 22.4 (0.5) | 22.1 (0.7) | 0.0992 | <0.0001 |

| North Dakota | 13.9 (1.1) | 18.2 (1.3) | 17.8 (1.0) | 16.8 (1.3) | 0.0153 | 0.6330 |

| Ohio | 13.9 (1.3) | 14.7 (1.1) | 18.4 (1.1) | 18.2 (0.8) | 0.0926 | 0.0054 |

| Oklahoma | 20.1 (1.4) | 22.0 (1.0) | 25.3 (0.8) | 23.1 (0.8) | 0.0550 | 0.0153 |

| Oregon | 16.5 (0.8) | 17.5 (0.7) | 21.6 (0.6) | 21.1 (1.2) | 0.0699 | 0.0034 |

| Pennsylvania | 12.4 (0.8) | 12.6 (0.8) | 14.9 (0.7) | 16.0 (0.7) | 0.0747 | 0.0023 |

| Rhode Island | 13.0 (1.0) | 13.1 (0.8) | 13.7 (0.9) | 16.1 (0.9) | 0.0103 | 0.7362 |

| South Carolina | 14.6 (1.0) | 18.2 (0.9) | 24.5 (0.8) | 22.5 (1.1) | 0.1316 | <0.0001 |

| South Dakota | 11.6 (1.0) | 15.7 (0.8) | 17.3 (0.9) | 15.8 (1.0) | 0.0593 | 0.0469 |

| Tennessee | 13.4 (1.0) | 14.3 (0.9) | 18.8 (1.2) | 21.7 (1.1) | 0.1557 | <0.0001 |

| Texas | 19.9 (1.3) | 21.2 (0.6) | 26.0 (0.7) | 23.3 (0.6) | 0.0525 | 0.0025 |

| Utah | 14.7 (1.0) | 15.4 (1.0) | 20.6 (0.9) | 20.3 (0.8) | 0.0970 | <0.0001 |

| Vermont | 14.9 (1.0) | 14.8 (0.9) | 17.8 (0.8) | 12.8 (0.9) | −0.0470 | 0.0896 |

| Virginia | 14.4 (1.1) | 15.8 (1.2) | 16.8 (1.1) | 17.0 (1.4) | 0.0372 | 0.2731 |

| Washington | 14.4 (0.8) | 13.7 (0.8) | 19.0 (0.4) | 19.1 (0.6) | 0.1016 | <0.0001 |

| West Virginia | 21.4 (1.1) | 26.4 (1.3) | 25.2 (1.1) | 24.4 (1.2) | 0.0151 | 0.4757 |

| Wisconsin | 9.9 (1.0) | 10.6 (0.8) | 15.3 (1.0) | 15.8 (1.1) | 0.1276 | 0.0004 |

| Wyoming | 21.0 (1.1) | 24.6 (1.3) | 25.6 (1.0) | 22.7 (1.1) | 0.0082 | 0.6901 |

Adjusted for all demographic variables listed in Table 1. β: regression coefficient for survey year (continuous).

From 2011 through 2014, the adjusted prevalence of lack of insurance significantly and linearly decreased in 15 states—Alaska, Connecticut, Georgia, Idaho, Indiana, Louisiana, Massachusetts, Mississippi, Missouri, Nebraska, Nevada, North Dakota, Oklahoma, South Dakota, and Utah (Table 4). Three states—Hawaii, Maine, New Hampshire, and DC—showed no significant change. The remaining states showed significant quadratic trends with or without accompanying linear trends; the overall decreasing trends in the lack of insurance in these states resulted mostly from a significant decrease in 2014 (Table 4). In 2014, Georgia, Mississippi, and Texas had the highest adjusted prevalences of lack of insurance (ranging from 23.0% to24.6%); Massachusetts, DC, and Rhode Island had the lowest (ranging from 6.2% to 10.1%) (Table 4).

Table 4 –

Adjusteda prevalence (with standard error) of lack of health insurance among adults aged 18–64 years, by state (including DC) and by survey year, BRFSS, 2011 through 2014.b

| State | 2011 | 2012 | 2013 | 2014 | P for linear | P for quadratic |

|---|---|---|---|---|---|---|

|

| ||||||

| Alabama | 23.7 (0.9) | 25.2 (0.9) | 22.0 (1.0) | 19.3 (0.8) | <0.0001 | 0.0279 |

| Alaska | 24.6 (1.3) | 22.3 (1.0) | 21.9 (1.1) | 19.6 (1.1) | 0.0036 | n.s. |

| Arizona | 19.4 (1.2) | 21.2 (0.9) | 22.6 (1.3) | 15.6 (0.6) | n.s. | <0.0001 |

| Arkansas | 30.5 (1.4) | 32.8 (1.1) | 29.7 (1.2) | 21.1 (1.2) | <0.0001 | <0.0001 |

| California | 17.5 (0.4) | 19.8 (0.5) | 16.3 (0.5) | 13.7 (0.5) | <0.0001 | <0.0001 |

| Colorado | 22.3 (0.7) | 22.3 (0.6) | 21.2 (0.6) | 15.7 (0.5) | <0.0001 | <0.0001 |

| Connecticut | 15.9 (0.8) | 13.6 (0.6) | 12.9 (0.7) | 10.8 (0.6) | <0.0001 | n.s. |

| Delaware | 13.7 (0.9) | 15.2 (1.0) | 15.3 (0.8) | 11.7 (0.9) | n.s. | 0.0076 |

| District of Columbia | 8.3 (0.9) | 9.6 (1.0) | 10.1 (0.9) | 10.1 (1.2) | n.s. | n.s. |

| Florida | 27.5 (0.7) | 25.3 (1.0) | 25.9 (0.6) | 20.0 (0.7) | <0.0001 | 0.0149 |

| Georgia | 28.2 (0.8) | 26.9 (0.9) | 26.5 (0.8) | 24.6 (0.9) | 0.0051 | n.s. |

| Hawaii | 11.4 (0.7) | 13.2 (0.8) | 10.3 (0.6) | 10.3 (0.7) | n.s. | n.s. |

| Idaho | 29.4 (1.2) | 26.4 (1.2) | 26.8 (1.1) | 22.8 (1.1) | 0.0002 | n.s. |

| Illinois | 20.6 (1.0) | 20.5 (1.0) | 19.7 (0.9) | 14.7 (0.8) | <0.0001 | 0.0146 |

| Indiana | 25.2 (0.8) | 24.9 (0.8) | 23.2 (0.7) | 20.5 (0.7) | <0.0001 | n.s. |

| Iowa | 17.8 (0.8) | 16.9 (0.8) | 16.0 (0.8) | 12.2 (0.7) | <0.0001 | 0.0420 |

| Kansas | 23.4 (0.5) | 24.1 (0.7) | 24.1 (0.5) | 20.6 (0.6) | 0.0034 | 0.0005 |

| Kentucky | 24.6 (0.8) | 24.3 (0.8) | 24.9 (0.8) | 14.3 (0.8) | <0.0001 | <0.0001 |

| Louisiana | 26.3 (0.8) | 27.2 (1.0) | 25.0 (1.3) | 22.5 (0.8) | 0.0002 | n.s. |

| Maine | 18.6 (0.7) | 20.1 (0.7) | 19.1 (0.8) | 17.8 (0.9) | n.s. | n.s. |

| Maryland | 16.5 (0.8) | 17.4 (0.8) | 16.7 (0.7) | 11.8 (0.8) | <0.0001 | 0.0007 |

| Massachusetts | 9.1 (0.4) | 8.0 (0.4) | 8.3 (0.5) | 6.2 (0.5) | 0.0002 | n.s. |

| Michigan | 20.1 (0.7) | 19.1 (0.7) | 20.0 (0.7) | 14.9 (0.7) | <0.0001 | 0.0028 |

| Minnesota | 16.9 (0.6) | 16.8 (0.6) | 16.4 (0.8) | 11.2 (0.5) | <0.0001 | 0.0001 |

| Mississippi | 29.6 (0.8) | 27.9 (0.9) | 28.4 (1.0) | 23.0 (1.1) | <0.0001 | n.s. |

| Missouri | 23.8 (1.0) | 24.6 (1.0) | 21.3 (1.0) | 19.7 (1.0) | 0.0004 | n.s. |

| Montana | 29.0 (1.0) | 29.3 (0.9) | 27.0 (0.9) | 20.4 (1.0) | <0.0001 | 0.0003 |

| Nebraska | 22.9 (0.5) | 21.3 (0.6) | 20.9 (0.7) | 18.0 (0.6) | <0.0001 | n.s. |

| Nevada | 28.1 (1.1) | 26.0 (1.0) | 22.6 (1.0) | 16.8 (1.1) | <0.0001 | n.s. |

| New Hampshire | 20.6 (1.0) | 21.3 (1.1) | 21.2 (1.0) | 19.1 (1.1) | n.s. | n.s. |

| New Jersey | 18.2 (0.5) | 18.9 (0.5) | 19.4 (0.6) | 14.9 (0.5) | 0.0010 | <0.0001 |

| New Mexico | 20.9 (0.6) | 20.5 (0.6) | 20.7 (0.7) | 14.1 (0.6) | <0.0001 | <0.0001 |

| New York | 16.6 (0.7) | 17.6 (0.8) | 15.8 (0.6) | 13.4 (0.6) | 0.0007 | 0.0207 |

| North Carolina | 25.5 (0.8) | 26.5 (0.6) | 25.4 (0.7) | 21.7 (0.7) | 0.0004 | 0.0020 |

| North Dakota | 21.1 (1.1) | 21.6 (1.2) | 16.7 (0.9) | 14.0 (1.0) | <0.0001 | n.s. |

| Ohio | 19.5 (0.8) | 21.1 (0.7) | 19.5 (0.7) | 15.5 (0.8) | <0.0001 | 0.0002 |

| Oklahoma | 28.4 (0.9) | 23.9 (0.8) | 23.7 (0.8) | 18.6 (0.7) | <0.0001 | n.s. |

| Oregon | 24.8 (1.0) | 24.8 (1.0) | 27.6 (1.0) | 15.5 (0.9) | <0.0001 | <0.0001 |

| Pennsylvania | 17.8 (0.7) | 18.6 (0.6) | 17.3 (0.6) | 15.2 (0.7) | 0.0030 | 0.0502 |

| Rhode Island | 16.8 (0.8) | 18.7 (0.9) | 19.5 (0.8) | 10.1 (0.8) | <0.0001 | <0.0001 |

| South Carolina | 25.6 (0.7) | 27.5 (0.7) | 25.2 (0.7) | 22.7 (0.7) | 0.0004 | 0.0057 |

| South Dakota | 18.6 (1.1) | 17.7 (0.9) | 18.1 (1.2) | 14.9 (1.1) | 0.0323 | n.s. |

| Tennessee | 24.0 (1.4) | 25.5 (1.0) | 24.4 (1.0) | 20.2 (1.1) | 0.0178 | 0.0072 |

| Texas | 28.2 (0.7) | 29.0 (0.7) | 27.3 (0.6) | 23.4 (0.6) | <0.0001 | 0.0008 |

| Utah | 24.8 (0.6) | 23.5 (0.7) | 21.7 (0.6) | 18.8 (0.5) | <0.0001 | n.s. |

| Vermont | 14.3 (0.8) | 15.8 (0.9) | 15.2 (0.9) | 11.7 (0.7) | 0.0055 | 0.0016 |

| Virginia | 20.5 (1.0) | 21.4 (0.8) | 21.5 (0.8) | 18.1 (0.7) | n.s. | 0.0114 |

| Washington | 23.4 (0.7) | 23.3 (0.6) | 23.5 (0.7) | 14.6 (0.7) | <0.0001 | <0.0001 |

| West Virginia | 29.9 (1.1) | 29.0 (1.0) | 28.1 (0.9) | 16.0 (0.9) | <0.0001 | <0.0001 |

| Wisconsin | 17.5 (1.0) | 17.3 (1.0) | 17.2 (1.0) | 12.7 (0.8) | 0.0009 | 0.0315 |

Adjusted for all demographic variables listed in Table 1. n.s.: not significant.

Since the BRFSS survey methodology changed in 2011, results from 1993 through 2010 should not be compared with results from 2011 through 2014.

Discussion

By using large, state-based population surveillance data from BRFSS, we were able to examine the changes in the prevalence of lack of health insurance among adult state residents over more than 20 years. Most importantly, we were able to provide a state-focused perspective on changes in this prevalence. Our results demonstrated that the adjusted prevalence of lack of insurance overall increased from 1993 through 2010, but decreased nonlinearly afterward. This prevalence and its changes over time varied significantly by state (including DC).

To the best of our knowledge, this study is the first to present state-specific trends in the prevalence of lack of insurance for the periods 1993 through 2010 and 2011 through 2014. These prevalence estimates and a generally increasing trend in lack of insurance during 1993–2010 resembled those reported by the NHIS and the US Census.15,16,22 From 1993 through 2010, the BRFSS used a landline sampling frame. As the proportion of adults using only cellular telephones continue to increase,23 the ability to reach potential survey participants solely through landline telephones became more difficult. As a result, the representativeness of the sample may have become compromised, particularly among population groups that only use cellular telephones. Cellular telephone–only users are more likely to be younger, to be a member of a minority group, and to have a lower income than those using only landline telephones.23 The decreasing trend in the proportion of young adults (aged 18–24 years) from 1993 through 2010 observed in the present study may partially reflect the loss of these young adults from the BRFSS sampling frame. In 2011, the BRFSS included cellphone-only users in its sampling frame and improved its weighting methodology. This is likely to improve BRFSS coverage among young adults and members of minority groups. These changes have improved the nationwide estimate of the prevalence of lack of insurance comparable with other surveys.20

The ACA included mandatory funding for prevention and wellness programs and activities to improve both access to affordable, quality, and accountable health care and the overall quality of the nation’s healthcare system.8,9 In September 2010, a provision of the ACA extended private health insurance coverage to young adults aged 19–25 years through their parents’ health insurance plan.24 The ACA enactment may have partially contributed to the significant, decreasing trend in the prevalence of lack of insurance in 2013 and 2014. In 2014, the ACA extended health insurance coverage to low-income Americans through expansion of Medicaid eligibility in states that choose to participate.8,9,12,25,26 The health insurance coverage gains realized through Medicaid expansion, the Health Insurance Marketplace, and the individual market coverage may have helped reduce the percentage of uninsured working-aged adults.27 In a recent analysis, researchers estimated that the ACA increased the number of insured working-aged adults by an estimated 16.9 million compared with the number who would have been insured had the law not been enacted.28 In addition, inclusion of the number of young adults aged 19–25 years who gained insurance coverage as a result of the earlier coverage expansion to young adults increases this estimate by an additional 1.2 million to 18.1 million working-aged adults who would otherwise be uninsured in absence of the ACA.28 While many of the long-term health outcomes associated with increased access to health insurance are not yet known, early evidence indicates substantial improvements in post-ACA trends in access to medical care (e.g., increases in the proportion of adults who have a usual healthcare provider and those with easy access to medications), financial security (e.g., increases in the ability to afford needed medical care),and health (e.g., decreases in the proportion of adults reporting fair or poor health and those reporting activity limitations related to poor health) compared with pre-ACA trends.29,30 Clearly, state-level data from the continuing BRFSS and other nationally representative population-based surveys can help assess the impact of the ACA on healthcare access and utilization in the US.

Notably, we found the prevalence of lack of insurance varied greatly by state, ranging from 6.2% in Massachusetts to 24.6% in Georgia in 2014. Although, we adjusted for population demographic characteristics, contextual differences such as social, cultural, and political norms related to healthcare access and individual and community financial resources may also have contributed to the observed variation by state. For example, the sweeping health reform initiative in Massachusetts in 2006, an act providing access to affordable, quality, and accountable health care, has been credited for having reduced the prevalence of lack of insurance in Massachusetts.31–33 In 2014, the prevalence of lack of insurance was low nationwide and the health insurance coverage gains have been especially strong in the states with Medicaid expansion.27 During this time period, substantial reductions in the prevalence of lack of insurance occurred in both Medicaid expansion states and non-expansion states, with states who expanded Medicaid having the largest reductions.34 Moreover, recent evidence suggests that coverage gains have been achieved without negative effects on employment in expansion states.30,35,36 Contributing factors that may either promote or temper state-level health insurance coverage gains include increased awareness of and eligibility for Medicaid, implementation of the Health Insurance Marketplaces (e.g., state based; federally funded; state-partnership; and federally facilitated), the prevalence of employer-based coverage, and the size of immigrant populations.

The main strengths of this study are the BRFSS’ ability to produce state-level estimates each year for more than 20 years, its large sample sizes, and its generally consistent questions on health insurance coverage—that allowed us to assess trends in nationwide and state prevalences of lack of insurance over time. Limitations do exist, however. First, all responses including health insurance coverage were self-reported and subject to recall bias. Second, because response rates and sampling frame coverage in BRFSS states varied substantially, particularly during the rapid increase in cellular telephone-only households (i.e., from 2005 to 2010), the BRFSS may have underestimated the prevalence of lack of insurance when compared with other national surveys.37 Third, although including cellular telephone usage in the sampling frame and implementing raking to estimate sampling weights improved coverage, undercoverage in the sampling frame remains a challenge. Based on NHIS data, the estimated prevalence of cellular telephone–only adults in the US was 38%,38 ranging from 19.4% in New Jersey to 52.3% in Idaho,39 and the cellular telephone–only households continue to rise in the US. On the other hand, the uninsured rate was significantly higher among adults under age 65 years with cellular phone only than among adults under 65 years living with landline households at the time of interview.40,41 In BRFSS, cellular telephone samples account for only ~20% of completed interviews,42 which may result in undercoverage bias, and the uninsured rates could have been underestimated. Furthermore, the change in survey methodology implemented in 2011 resulted in a break in trend analysis. Having just four years of BRFSS data after survey methodology change is a major constraint in assessing trends; therefore, continuation of state BRFSS surveys in coming years is imperative for providing a confirmatory trend analysis post-2010.

In summary, our results demonstrated a generally increasing trend in the prevalence of lack of health insurance from 1993 through 2010, and a nonlinearly decreasing trend from 2011 through 2014 among US adults aged 18–64 years. In 2014, approximately one-seventh of Americans aged 18–64 years reported lack of health insurance. The prevalence of lack of insurance varied greatly by state ranging from 6.2% in Massachusetts to 24.6% in Georgia in 2014. Continuing efforts are needed to help more Americans secure healthcare coverage that allows them to optimally access quality care and achieve optimal health.

Supplementary Material

Acknowledgements

The authors would like to thank the state BRFSS coordinators for their assistance in data collection. All authors contributed substantially to the study concept and design, data analysis and interpretation, and writing, review, and critical revision of the manuscript.

Footnotes

Competing interests

The findings and conclusions in this report are those of the authors and do not necessarily represent the official position of the Centers for Disease Control and Prevention.

Ethical approval

BRFSS procedures were reviewed by the Human Research Protection Office of the Centers for Disease Control and Prevention and determined to be exempt research.

Appendix A. Supplementary data

Supplementary data related to this article can be found at doi: 10.1016/j.puhe.2017.01.005.

REFERENCES

- 1.Ahluwalia IB, Bolen J, Garvin B. Health insurance coverage and use of selected preventive services by working-age women, BRFSS. J Womens Health (Larchmt) 2006;2007(16):935–40. [DOI] [PubMed] [Google Scholar]

- 2.Faulkner LA, Schauffler HH. The effect of health insurance coverage on the appropriate use of recommended clinical preventive services. Am J Prev Med 1997;13:453–8. [PubMed] [Google Scholar]

- 3.Powell-Griner E, Bolen J, Bland S. Health care coverage and use of preventive services among the near elderly in the United States. Am J Public Health 1999;89:882–6. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Cokkinides V, Bandi P, Shah M, Virgo K, Ward E. The association between state mandates of colorectal cancer screening coverage and colorectal cancer screening utilization among US adults aged 50 to 64 years with health insurance. BMC Health Serv Res 2011;11:19–25. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Institute of Medicine. Coverage matters: insurance and health care. Washington (DC): National Academies Press; 2001. [PubMed] [Google Scholar]

- 6.Institute of Medicine. Care without coverage: too little, too late. Washington (DC): National Academies Press; 2002. [Google Scholar]

- 7.Institute of Medicine. America’s uninsured crisis: consequences for health and health care. Washington, DC: The National Academies Press; 2009. [PubMed] [Google Scholar]

- 8.Patient Protection and Affordability Act. Pub L No. 111–148 (March 23, 2010), 124 Stat. 119. Available at http://www.gpo.gov/fdsys/pkg/PLAW-111publ148/pdf/PLAW-111publ148.pdf.

- 9.Health Care and Education Reconciliation Act. Pub L No. 111–152 (March 30, 2010), 124 Stat. 1029. Available at http://www.gpo.gov/fdsys/pkg/PLAW-111publ152/pdf/PLAW-111publ152.pdf.

- 10.Institute of Medicine. The future of public health. Washington (DC): National Academy Press; 1988. Available at, http://www.nap.edu/openbook.php?isbn=0309038308. [Google Scholar]

- 11.Coates RJ, Ogden L, Monroe JA, Buehler J, Yoon PW, Collins JL. Conclusions and future directions for periodic reporting on the use of adult clinical preventive services of public health priority–United States. MMWR 2012;61(Suppl):73–8. [PubMed] [Google Scholar]

- 12.Insurance Coverage Provisions of the Affordable Care Act–CBO’s March 2015 Baseline. Available at https://www.cbo.gov/sites/default/files/cbofiles/attachments/43900-2015-03-ACAtables.pdf.

- 13.Sommers BD, Long SK, Baicker K. Changes in mortality after Massachusetts health care reform: a quasi-experimental study. Ann Intern Med 2014;160:585–93. [DOI] [PubMed] [Google Scholar]

- 14.Sommers BD, Baicker K, Epstein AM. Mortality and access to care among adults after state Medicaid expansions. N Engl J Med 2012;367:102–34. [DOI] [PubMed] [Google Scholar]

- 15.Martinez ME, Cohen RA. Health insurance coverage: early release of estimates from the national health interview survey. January–September 2014. [Google Scholar]

- 16.DeNavas-Walt C, Proctor BD, Smith JC. Income, poverty, and health insurance coverage in the United States. U.S: Department of Commerce, U.S. Census Bureau; 2012. [Google Scholar]

- 17.Mokdad AH, Stroup DF, Giles WH. Public health surveillance for behavioral risk factors in a changing environment. Recommendations from the Behavioral Risk Factor Surveillance Team. MMWR Recomm Rep 2003;52:1–12. [PubMed] [Google Scholar]

- 18.Nelson DE, Holtzman D, Bolen J, Stanwyck CA, Mack KA. Reliability and validity of measures from the Behavioral Risk Factor Surveillance System (BRFSS). Soc Prev Med 2001;46 (Suppl 1):S3–42. [PubMed] [Google Scholar]

- 19.Nelson DE, Powell-Griner E, Town M, Kovar MG. A comparison of national estimates from the national health interview survey and the behavioral risk factor surveillance system. Am J Public Health 2003;93:1335–41. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Centers for Disease Control and Prevention. Methodologic changes in the behavioral risk factor surveillance system in 2011 and potential effects on prevalence estimates. MMWR 2012;61:410–3. [PubMed] [Google Scholar]

- 21.Centers for Disease Control and Prevention. Behavioral Risk Factor Surveillance System (BRFSS). Available at http://www.cdc.gov/brfss/.

- 22.SHADAC (State Health Access Data Assistance Center). Comparing federal government surveys that count the uninsured. Robert Wood Johnson Foundation; 2013. [Google Scholar]

- 23.Blumberg SJ, Luke JV, Ganesh N, Davern ME, Boudreaux MH, Soderberg K. Wireless substitution: state-level estimates from the National Health Interview Survey, January 2007–June 2010. Natl Health Stat Rep 2011;28:1–26. [PubMed] [Google Scholar]

- 24.Sommers BD, Kronick R. The Affordable Care Act and insurance coverage for young adults. JAMA 2012;307:913–4. [DOI] [PubMed] [Google Scholar]

- 25.Collins SR, Rasmussen PW, Doty MM. Gaining ground: Americans’ health insurance coverage and access to care after the Affordable Care Act’s first open enrollment period. Issue Brief (Commonw Fund) 2014;16:1–23. [PubMed] [Google Scholar]

- 26.Shaw FE, Asomugha CN, Conway PH, Rein AS. The Patient Protection and Affordable Care Act: opportunities for prevention and public health. Lancet 2014;384:75–82. [DOI] [PubMed] [Google Scholar]

- 27.ASPE Data Point. Health Insurance Coverage and The Affordable Care Act. 2015. Available at http://aspe.hhs.gov/sites/default/files/pdf/111826/ACA%20health%20insurance%20coverage%20brief%2009212015.pdf.

- 28.Blumberg LJ, Garrett B, Holahan J. Estimating the counterfactual: how many uninsured adults would there be today without the ACA? Inquiry 2016;53:1–13. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29.Sommers BD, Gunja MZ, Finegold K, Musco T. Changes in self-reported insurance coverage, access to care, and health under the affordable care act. JAMA 2015;314:366–74. [DOI] [PubMed] [Google Scholar]

- 30.Obama B United States health care reform: progress to date and next steps. JAMA 2016;316:525–32. 10.1001/jama.2016.9797. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Chapter 58: An Act Providing Access to Affordable, Quality, Accountable Health Care. The 186th General Court of the Commonwealth of Massachusetts. Available at http://www.malegislature.gov/Laws/SessionLaws/Acts/2006/Chapter58.

- 32.Dhingra SS, Zack MM, Strine TW, Druss BG, Simoes E. Change in health insurance coverage in Massachusetts and other New England States by perceived health status: potential impact of health reform. Am J Public Health 2013;103:e107–14. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 33.Okoro CA, Dhingra SS, Coates RJ, Zack M, Simoes EJ. Effects of Massachusetts health reform on the use of clinical preventive services. J Gen Intern Med 2014;29:1287–95. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34.Arkansas Witters D Kentucky set pace in reducing uninsured rate. Gallup; 2016. Available at, http://www.gallup.com/poll/189023/arkansas-kentucky-set-pace-reducing-uninsured-rate.aspx. [Google Scholar]

- 35.Kaestner R, Garrett B, Gangopadhyay A, Fleming C. Effects of the ACA Medicaid expansions on health insurance coverage and labor supply. National Bureau of Economic Research; 2015. [NBER working paper No. 21836]. [DOI] [PubMed] [Google Scholar]

- 36.Gooptu A, Moriya AS, Simon KI, Sommers BD. Medicaid expansion did not result in significant employment changes or Job reductions in 2014. Health Aff (Millwood) 2016;35:111–8. [DOI] [PubMed] [Google Scholar]

- 37.Li C, Balluz LS, Ford ES, Okoro CA, Zhao G, Pierannunzi C. A comparison of prevalence estimates for selected health indicators and chronic diseases or conditions from the behavioral risk factor surveillance system, the National Health Interview Survey, and the National Health and Nutrition Examination Survey, 2007–2008. Prev Med 2012;54:381–7. [DOI] [PubMed] [Google Scholar]

- 38.Blumberg SJ, Luke JV. Wireless substitution: early release of estimates from the National Health Interview Survey, January–June 2013. Natl Cent Health Statistics; December 2013:1–19. Available at, http://www.cdc.gov/nchs/nhis.htm. [Google Scholar]

- 39.Blumberg SJ, Ganesh N, Luke JV, Gonzales G. Wireless substitution: state-level estimates from the National Health Interview Survey. Natl Health Stat Rep 2012;2013(70):1–16. [PubMed] [Google Scholar]

- 40.Blumberg SJ, Luke JV. Wireless substitution: early release of estimates from the National Health Interview Survey, July–December 2015. Natl Cent Health Statistics; 2015:1–13. Available at, http://www.cdc.gov/nchs/data/nhis/earlyrelease/wireless201605.pdf. [Google Scholar]

- 41.Cantor JC, Brownlee S, Zukin C, Boyle JM. Implications of the growing use of wireless telephones for health care opinion polls. Health Serv Res 2009;44:1762–72. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 42.Centers for Disease Control and Prevention. The BRFSS Data User Guide. The Cellular Telephone Sample. Available at http://www.cdc.gov/brfss/data_documentation/PDF/UserguideJune2013.pdf. [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.