Abstract

Making evidence-based policy decisions is challenging when there is a lack of information, especially when deciding provider payment rates for publicly funded health insurance plans. Therefore, the goal of this study was to estimate the cost of a cochlear implant operation in a tertiary care setting in India. We also looked at the patients’ out-of-pocket (OOP) expenses for the cochlear implant surgery. From the perspectives of the patients and the healthcare systems, we assessed the financial costs of the cochlear implantation procedure. A bottom-up pricing model was used to assess the cost that the healthcare system would bear for a cochlear implant procedure. Information on all the resources (both capital and ongoing) required to offer cochlear implantation services for hearing loss was gathered over the course of a year. 120 individuals with hearing loss who had cochlear implantation surgery disclosed their out-of-pocket (OOP) costs, which included both direct medical and non-medical expenses. All costs for the budgetary year 2018–2019 were anticipated. The unit health system spent ₹ 151($2), ₹ 578($7.34) and ₹ 37,449($478) on ear exams, audiological evaluations, and cochlear implant surgeries, respectively. Per bed-day in the otolaryngology ward, hospitalization cost ₹ 202($2.6), or ₹ 1211($15.5). The estimated average out-of-pocket cost for a cochlear implant operation was ₹ 682,230($8710). Our research can be used to establish package rates for publicly funded insurance plans in India, plan the growth of public sector hearing care services, and do cost-effectiveness assessments on various hearing care models.

Supplementary Information

The online version contains supplementary material available at 10.1007/s12070-023-04389-7.

Keywords: Tinnitus, Cognition, Verbal memory, Working memory, Auditory attention

Introduction

Cochlear implantation (CI) is the only treatment option that is widely accepted for people with severe to profound hearing loss when a high-tech digital hearing aid fails to offer them meaningful clinical and physical benefits [1]. More than 13% of all expenditures in India go toward treating young children with hearing impairment [2]. Numerous cost-utility assessments of CI conducted across various nations and patient populations reveal that, despite the increasing overall cost of the CI process, unilateral CI is seen as a more cost-effective treatment option than traditional hearing aids [3–6].

Treatments like cochlear implants have both direct costs that the patient is responsible for covering out-of-pocket (OOP) and indirect costs that the healthcare system is responsible for covering. Out-of-pocket (OOP) costs account for 68 to 70% of all healthcares spending in India [7]. In India, the majority of the time, the cost of the cochlear implant treatment is covered by the patients and their families. This significantly strains the family’s finances and, in some cases, leads to treatment dropout.

Unilateral cochlear implantation is available in India through a variety of national initiatives, including the Ministry of Social Welfare’s Assistance to Disabled Person Scheme, state health insurance programs (Chief Ministers Comprehensive Health Insurance Schemes), national programs, and armed forces medical care. These plans, however, fall short of what the population now requires. One of the challenges to program expansion and the development of effective plans is the absence of easily accessible information on the costs related to cochlear implantation. Because of this, the reimbursement costs for the majority of health benefits packages (HBPs) under publicly financed health insurance schemes (PFHIs) are established by expert consultation rather than utilizing scientifically obtained cost data.

The cost-effectiveness of cochlear implantation in India has only been examined in one study. According to the study, unilateral cochlear implantation is an economical treatment option because the procedure and the cochlear implant device are projected to cost ₹445,00 and ₹36,500, respectively [8].

It is crucial to calculate the cost of healthcare and OOP for the cochlear implantation operation. In light of this, the current study was conducted to determine the patient’s out-of-pocket (OOP) and healthcare costs associated with the cochlear implantation process.

Materials and Methods

Study Setting

The current study was carried out in the Speech and Hearing Unit of a tertiary care public sector hospital in North India’s Otolaryngology Department. The five to six states in the country’s northwest that frequently refer patients to our multispecialty hospital’s otolaryngology department which offers cutting-edge comprehensive care to persons who are deaf. The hospital has resources to provide surgical, speech, and audiological therapy treatment options for persons with hearing loss.

Inclusion Criteria

A total of 120 children who underwent cochlear implantation and attended the speech and hearing unit of the otolaryngology department in the tertiary healthcare Center were included in the study in order to gather data on OOP expenditure. (1) Inclusion is limited to those with bilateral severe to profound hearing loss. (2) Individuals with just one Cochlear Implant.

Data Collection

Healthcare System Cost

The cost of the healthcare system, or the cost paid by the hospital, was determined using the economic costing approach and the combined (top-down and bottom-up) micro costing technique [9–12]. It includes determining and evaluating numerous resources that are employed to provide healthcare services associated with the CI procedure. The various cost centers at each level included personnel, area/space occupied, furniture, consumables, equipment, overheads, and utilities (Table 1).

Table 1.

Sources and characteristics of data collected in ENT department

| Data center | Data Collection Source | Concerned Department | Parameter |

|---|---|---|---|

| Space/Area | Facility maps | Engineering | Area in square feet |

| Human Resource | Accounts Details | Accounts department | Annual Salary in Indian rupees |

| Overheads | Quarterly Bills | Water & Electricity Department | Annual Charges in Indian rupees |

| Furniture | Procurement register | Store & ENT department | Cost in Indian Rupees |

| Consumables | Stock registers | Hospital Store | Annual Expenditure on Consumables in Indian rupees |

| Equipment’s/Tools | Indent Register | Store & ENT department | Cost in Indian Rupees |

|

Annual Patient’s Data |

Annual Report, outpatient register & impatient register | Medical record Department | Total no. of patient treated/consulted yearly |

| Utility | Utility register | Laundry & otolaryngology department | Annual expenditure in Indian rupees |

The expenses of overhead, infrastructure, equipment, and human resources were assessed using the top-down method. The price of prescription drugs, consumables, and diagnostics was calculated using a bottom-up methodology. All hearing screening and assessment specialists’ pay stubs were used to compile data on human resource costs, which the institution’s accounts department later verified. Facility maps made by the hospital engineering planning division were looked at in order to estimate the total floor area of authorized space used to provide various services for patients with cochlear implants [13]. The sizes of each room in the building are precisely described on these maps. The size of typical locations used for services offered to people with cochlear implants and other medical difficulties, such as waiting rooms, could also be inferred from the maps. To calculate the economic value of the space used for treatment, the floor area utilized under that service center and the market rental rates for comparable space were multiplied. The Central Store and Otolaryngology Department’s spending and procurement registers were reviewed to ascertain the price of furnishings and equipment for the provision of care.

The cost of the consumables used in CI was also calculated using the stock and indent records. Market pricing was applied in cases when procurement prices were not available. Based on the yearly expenses for each department, overhead costs were determined, including those for biological waste, power, water, telephone, diet, and internet. Additionally, the proper departments were billed for the cost of the utilities used, including sanitation and washing. Using data from the annual report and departmental statistics, estimates of the output produced by the Otolaryngology department were created (number of outpatient consultations, inpatient admissions, and operations). The admission records were used to calculate the number of diagnostic procedures that were recommended for the Individuals.

Time Allocation and Expert Opinion

Following the compilation of preliminary data, experts involved in providing rehabilitation services, including both medical and technical staff members, were questioned using pretested questionnaires from previous Indian studies about the amount of time provided for their regular and fixed activities [14–16]. The amount of time spent on routine jobs (such as research, operating rooms, outpatient and inpatient departments, etc.) was inquired of the medical staff (meetings, teaching, etc.). Similar to this, technical staff members were questioned regarding the department’s numerous fixed and ongoing activities. Regarding the durability of the tools, supplies, furniture, medications, and their use in the OPD, OT, and in-patient departments’ varied procedures, experts were questioned (IPD).

Out- of Pocket Expenditure

Data regarding out-of-pocket expenditure which includes both direct medical and non-medical costs borne by the Individuals’ families was collected using a pretested structured Performa [17]. OP expenditure was collected at the three stages: pre-operative phase, operative and postoperative phase. In our healthcare setup, hearing assessment and auditory verbal therapy/auditory training services are provided in the OPD, while surgical and ward stay services in IPD. For both the OPD and IPD visits, information regarding the expenses on travelling, diagnostic and laboratory tests, drugs, accommodation, food and hospital charges was collected. Up until the child was discharged following the cochlear implant surgery, information on OOP costs for IPD individuals was gathered.

The primary categories into which the preoperative phase was divided were the cost of the hearing assessment (speech and audiology tests), the number of visits, and the number of tests carried out prior to the surgery. OOP data was gathered from the time of surgery till the day of discharge. Expenses for the bed charges, medicine, drugs, testing fee, meals, transportation and cochlear implant device and other costs are all included. Similar data were obtained from individuals receiving auditory word therapy in the OPD setting about post-operative OOP.

Additionally, we gathered information on the socioeconomic and demographic characteristics of the patients and their families, such as their age, gender, place of residence, income, monthly consumption costs, level of education, and professional status.

Data Analysis

Healthcare Costing

Unit cost of cochlear implantation procedures’ were determined. The cost of each OPD visit, audiological tests, cochlear implant surgery cost, and hospital/ward expenses for those with cochlear implants were all covered. Capital expenditures were annualized and discounted at a rate of 3% during the equipment’s lifespan in order to produce a comparable yearly cost (while taking inflation and time preference for money into consideration) [18, 19]. To calculate the economic value of the space used for treatment, the floor area beneath the service center that is being used and the market rental rates for spaces of a similar size were multiplied. Based on the time allocation interviews and expert analysis, the appropriate apportioning data were used to estimate the apportioning factor for allocation of shared spending for joint or shared activity. Time allocation interviews revealed that the majority of the shared cost of human resources was accounted for by administrative, teaching, research, and outpatient care responsibilities. Similar to this, the expert’s judgment was utilized to decide how much should be shared across various evaluation, surgical, and ward procedures in terms of equipment, consumables, overhead, medications, space, and utilities.

Out-of-Pocket Expenditure

The mean OOP expenditure (95% Confidence Intervals) on OPD visits, hospital stays, and the cost of follow-up (speech therapy) was calculated using SPSS version 26.0.

All costs were calculated in Indian rupees (₹), and the 1$ = ₹78.3275 in 2021–2022 exchange rate was used to convert them to US dollars.

Results

Profile of Study Hospital

In total, 67,293 persons were registered with the ENT department. The ENT examination and Audiology and Speech departments had 32,413 and 29,789 outpatient visits in 2018–2019, respectively. The 3,939 surgeries performed in the ENT operating room included 48 CI surgeries. The annual number of audiological procedures needed for cochlear implantation, including pure tone audiometry, speech audiometry, immittance audiometry, otoacoustic emissions, and auditory brainstem responses, is shown in Table 2.

Table 2.

Annual number of audiological procedures conducted in the ENT department

| Sr. No. | Audiological Assessment Procedure | Annual Number of procedures |

|---|---|---|

| 1. | Pure tone audiometry | 8210 |

| 2. | Speech Audiometry | 2098 |

| 3. | Impedance audiometry | 4605 |

| 4. | Auditory brainstem response | 1110 |

| 5. | Oto-acoustic emissions | 3028 |

Pure tone audiometry− PTA, Speech audiometry−SA, Impedance audiometry− IA, Auditory brainstem response− ABR, Oto−acoustic emissions−OAE

Sample Characteristics

To learn out more about their out-of-pocket costs, we interviewed with the parents of 120 children who were using unilateral cochlear implants. Of the 120 individuals, 48.5% were men and 51.5% were women. 30% of the respondents were from rural areas, whereas 70% of the respondents were from urban areas.

Health System Costs

Unit Health System Costs

In the unit health system, the registration costs for the ENT exam and audiological evaluation were ₹13 ($0.17) and ₹21 ($0.27), respectively. A visit to the OPD for an ear examination cost the hospital ₹151 ($2). The audiological evaluation cost was ₹578, or $7.34. The surgery for a cochlear implant cost ₹37,449, or $478 per unit. In the Otolaryngology ward, a hospital bed cost ₹202 ($2.6) per bed-day. When considering the average six-day stay in the ENT ward after cochlear implant surgery, the cost of the hospital stay per unit was ₹1211 (about $15.5) (supplementary Table 1).

Input-wise Distribution of Health System cost

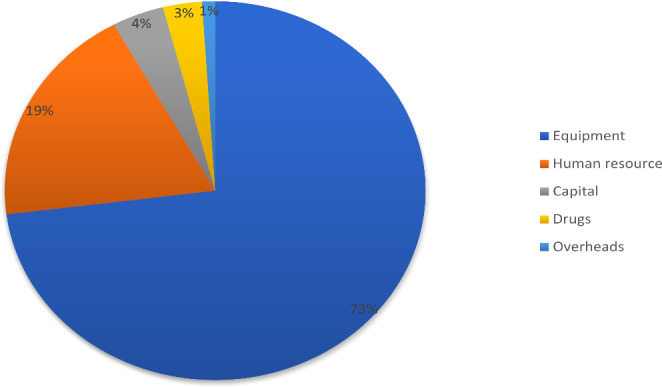

The cost of cochlear implantation was mainly comprised of equipment, as shown in Fig. 1, followed by human resources (19%), capital (4%), pharmaceuticals (3%), overheads (1%), consumables (1%), and utilities (1%).

Fig. 1.

Input wise distribution of health system costs for cochlear implant surgery in a tertiary care hospital of India

Input-wise Distribution of Cost of Audiological Assessment and Auditory Verbal Therapy/Auditory Training

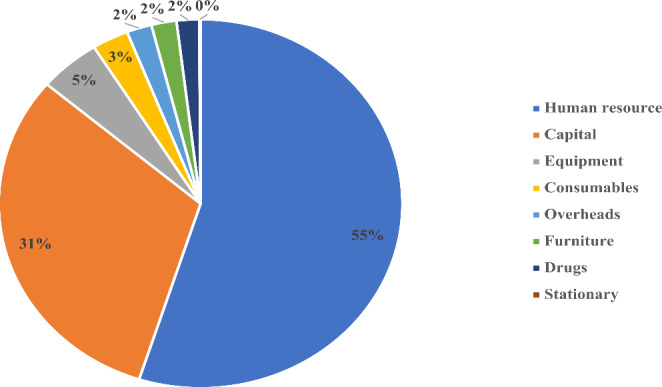

Of the overall cost on audiological assessment and auditory verbal therapy, salaries constituted the major component (54.6%), followed by capital (31.1%), equipment (4.9%), consumables (2.9%), overheads (2.5%), furniture (2%), drugs (1.8%) and stationary (0.1%) [Fig. 2].

Fig. 2.

Input-wise distribution of health system costs for Audiological assessment and auditory verbal therapy/ auditory therapy in a tertiary care hospital of India

Annual Health System cost of Cochlear Implant Surgery

The average annual cost of doing cochlear implant surgery was ₹1,797,527 ($22,948) to the healthcare system. Table 3 displays the annual mean costs of various cochlear implant surgical components at tertiary medical centers.

Table 3.

Annual costs of delivering cochlear implantation services at Tertiary Health centers in north India

| Sr. No. | Cost Centre | Cost in INR(₹) | Cost in dollars ($) |

|---|---|---|---|

| 1 | Human resource | 349,568 | 4463.32 |

| 2 | Building/Infrastructure | 64,893 | 828.56 |

| 3 | Furniture | 1078 | 13.76 |

| 4 | Equipment | 1,320,453 | 16859.71 |

| 5 | Drugs | 52,687 | 672.71 |

| 6 | Consumables | 115 | 1.46 |

| 7 | Utility | 1850 | 23.62 |

| 8 | Overheads | 6883 | 87.90 |

| Total | 1,797,527 | 22,951 |

Unit cost of Cochlear Implant Surgery

Table 4 shows the unit cost in dollars and rupees for various components of cochlear implant surgery.

Table 4.

Unit cost of various components of Cochlear implant surgery in tertiary health care centre

| Sr. No. | Cost centre | Cost in INR | Cost in dollars |

|---|---|---|---|

| 1 | Human resource | 7282 | 93 |

| 2 | Building/Infrastructure | 1352 | 17.27 |

| 3 | Furniture | 22 | 0.28 |

| 4 | Equipment | 27509 | 351 |

| 5 | Drugs | 1097 | 14 |

| 6 | Consumables | 2 | 0.025 |

| 7 | Utility | 38 | 0.49 |

| 8 | Overheads | 143 | 1.82 |

| Total cost | 37446 | 478 |

Out- of -Pocket Expenditure

The average pre-operative out-of-pocket expenditure in the OPD was determined to be ₹53,383 ($682). The estimated average out-of-pocket cost for hospitalization and cochlear implant surgery was ₹682,230 ($8710) [Table 5]. The estimated average monthly out-of-pocket cost for speech and verbal therapy is ₹4,453 ($57) per month. The findings show that travel, food, and hearing aids accounted for the majority of preoperative evaluation out-of-pocket costs. The OOP was greatly enhanced by the price of the medications and supplies required during the procedure and hospital stay. Bed fees and drug costs made up the majority of post-surgery hospitalization OOP. OOP for auditory verbal therapy is primarily made up of travel costs and the price of speech therapy equipment.

Table 5.

Average out of pocket expenditure for Hospitalization and cochlear implant surgery

| Sr. No. | Cost Centre | Cost in INR | Cost in dollars |

|---|---|---|---|

| 1 | Implant | 646066.7 | 8248.3 |

| 2 | Radiological | 3725 | 41.8 |

| 3 | Blood test | 800 | 10.21 |

| 4 | Consumables | 14820 | 189.2 |

| 5 | Travelling cost | 2172 | 27.72 |

| 6 | IPD stay | 14667 | 187.25 |

| Total cost | 682230 | 8710 |

Table 5 displays the average out of pocket expenditure for hospitalization and cochlear implant surgery. The overall Pre-, Peri, and Postoperative out-of-pocket expenditure for cochlear implantees are shown in Table 6.

Table 6.

Overall table of OOP

| Stages | Mean OOP | Major contribution |

|---|---|---|

|

Pre-operative OOP (Audiological assessment + Hearing aid fitting) |

53383.33 |

Travelling charges, food charges, audiology test Hearing aid cost, travelling charges |

|

Peri-opeartive OOP (Surgery + Ward stay) |

682230.33 | Implant cost, Consumables cost, Bed charges and medicine/Drug cost |

| Post-operative OOP | 4453.33 | Speech therapy material and travelling charges |

Input Wise Distribution of OOP Expenditure

CI Procedure

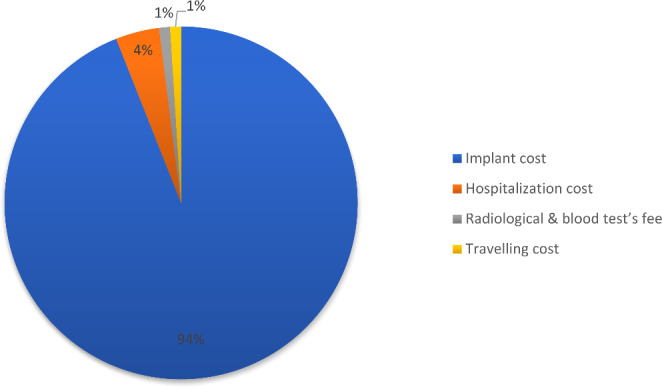

Cost of the Implant was the major component (94.69%) in OOP expenditure, followed by hospitalization cost (4.31%), radiological & blood test’s fee (0.66%) and travelling cost (0.31%).[Figure 3].

Fig. 3.

Input-wise distribution of OOP for cochlear implant surgery in a tertiary care hospital of India

Pre-operative OOP while Availing Audiological Services

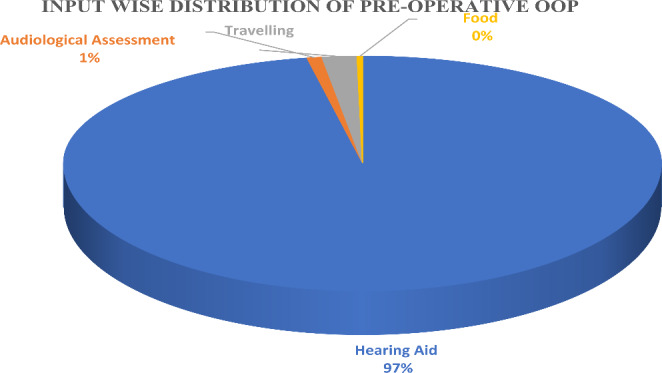

Of all the pre-operative OOP, hearing aid cost constituted the major portion (95.90%), followed by travelling cost (2.23%), fee of audiological assessment tests (0.95%), accommodation cost (0.46%) and food (0.34%). (Fig. 4)

Fig. 4.

Pre -op Out of pocket expenditure for Audiological services

Post-operative OOP

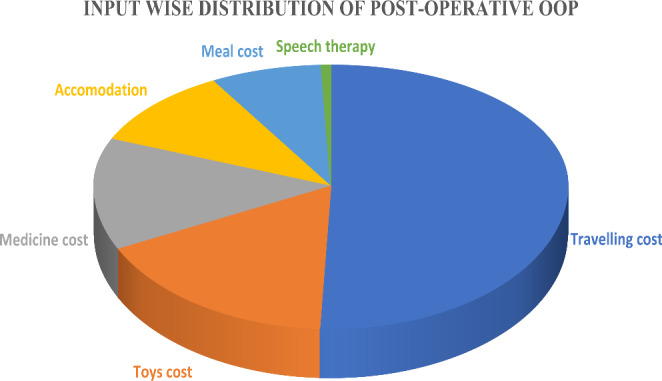

Of all post-operative OOP costs, travel expenses accounted for the majority (50.71%); toys (16.99%), drugs (12.65%), housing (10.10%), meals (8.68%), and speech therapy (0.78%) were the next most significant post-operative OOP expenses (Fig. 5).

Fig. 5.

Post Operative out of pocket expenditure for rehabilitative services

Discussion

Overview of Present Study Findings

The goal of the current study was to determine the cost of the Indian healthcare system and OOP charges related to CI surgery. While the total cost to the health system for the CI surgery was anticipated to be ₹38,659 (or $493.55), the average out-of-pocket expenditure, including the IPD stay, was ₹682,230 (or $8720). The cost of the implant used in the treatment accounted for the majority of the Individuals’ OOP costs. People and their families appear to be experiencing severe financial difficulties as a result of the high cost of the Cochlear implant.

Comparison of the Findings

Health System Costing

Comparing our findings with those of renowned Indian studies on the economic analysis of cochlear implantation is essential. The medical system spent ₹37,449 ($478) on the cochlear implant surgery. In a previous study, the cost of cochlear implant surgery was estimated to be $36,500 ($466), which is consistent with the findings of the current study [8]. However, the previous study omitted a significant amount of information. In order to take into account every potential variable, the present research has been carried out far more extensively.

The costs of auditory verbal therapy, auditory training, and audiological examination were determined to be most significant when it came to human resources. This is in line with the findings of the workgroup on tertiary medical institutes in India, which revealed that in the majority of states, salaries and wages might make up to 70% of the entire budgetary allocation [7, 20].

Our study’s findings are consistent with a number of other national and international research on hospital costs that found that a hospital’s overall operating costs are primarily attributable to its human resources [16, 17, 21]. However, for CI, the cost of the hospital is mainly made up of the cost of the surgical materials, followed by the price of the salary of the staff. This is because cochlear implantation requires sophisticated surgical techniques and specialized tools and equipment.

The current study is the most extensive economic analysis of the price of cochlear implantation in India to date because unit prices for each procedure and utilization of each input are analyzed separately. The unit cost for an ENT examination at the outpatient department is estimated in our study to be ₹151 ($1.9), which is consistent with the results of earlier costing studies conducted in tertiary healthcare facilities. According to our analysis, the unit costs for cochlear implant surgery and the price per bed-day for hospitalization in the otolaryngology ward were ₹37,449 ($478) and ₹1211 ($15.5), respectively. The results of this study are consistent with several other costing studies that represent inpatient expenditures per bed-day and for surgery [10, 15, 16].

Out of Pocket Expenditure

The results of the OOP expenditures analysis show that the largest contributors to OOP during OPD visits are transportation and eating expenses. This might be because just a few facilities in Himachal Pradesh, Punjab, Haryana, Jammu & Kashmir, and Uttarakhand are equipped to handle complex otolaryngology procedures like cochlear implantation. At the time of surgery, medication and supplies make up the majority of OOP costs. Generally speaking, the Indian government offers a range of services and resources, such as employee wages, capital infrastructure (buildings and equipment), and essential medical supplies. The majority of the time, however, the supply of medications and consumables does not fulfill all of the requirements for treatment.

Only about half of the necessary pharmaceuticals are readily available in North Indian states’ medical facilities, according to an assessment of those facilities [22]. The most recent National Sample Survey 71st Round Report revealed similar findings revealing a lack of availability of all necessary medications in public facilities [23]. These reasons may provide light on why OOP costs at the time of operation were dominated by prescription drugs and consumables. Similar to this, bed expenses and medication costs account for the majority of OOP costs during an Otolaryngology ward stay.

The results of our study, which were based primarily on data from a single public tertiary care hospital, have limited universal applicability due to changes in research settings, resource consumption, hospital efficiency, and other factors. Second, we failed to account for indirect expenses like productivity loss. Thirdly, apportioning variables required to be employed to calculate the cost at each cost centre since the whole pooled data for the supply and services at a tertiary care hospital was available. The breakdown of the overall expenses may need to be corrected as a result. Fourth, given the absence of purchase price information for specific equipment, we utilized market pricing to indicate the projected cost under specific conditions.

This is of the first studies to thoroughly evaluate the financial cost of CI in India. The theoretical foundations and presumptions that were investigated and published in the Indian setting are crucial for figuring out OOP spending and health system costs.

Conclusion

The study findings can be used to guide policy decisions, such as determining or changing cochlear implantation reimbursement rates and payment rates for a variety of publicly financed insurance plans in India. Our study’s estimation of the cost of cochlear implantation can be used to assess the cost-effectiveness of various hearing loss treatment options.

Electronic Supplementary Material

Below is the link to the electronic supplementary material.

Acknowledgements

The work stated here is research work done under funded project of Department of health and research and the principal investigator was Dr Anuradha. Further, we would like to thank all the subjects who participated in the present research work.

Author Contributions

Conceptualization: AS and SP; Data curation: AS; Formal analysis: SS and DG; Funding Acquisition: AS; Investigation: RT and RK; Methodology: AS and NP; Project Administration: AS, RT and RK; Resources: AS, RT, RK, SS and DG; Software: None; Supervision: AS and SP; Validation: None; Visualization: AS and SP; Writing original draft: AS, RT, RK and DG; Writing review and editing: AS, SP, SM and NP.

Funding

This Project received specific grants from Department of health and research, Indian council of medical research, New Delhi, India.

Data Availability

Data supporting the results will be available upon request from the corresponding author. The data is not accessible to the public because of confidentiality and ethical restrictions.

Ethics Approval

The Institute ethics committee granted the ethical approval (based on Helsinki Declarartion of 1975, as revised in 2008) and assigned it a reference number XXXXXXXX. Before information about OOP was obtained, the parents gave their Informed consent and approval. The participants were made aware that discontinuing the study at any stage would not have any adverse effects on their medical care.

Conflict of interest

There is no conflict of interest. I had full access to all of the data in this study and I take complete responsibility for the integrity of the data and the accuracy of the data analysis.

Disclosure

The Authors hereby certify that the work shown here is genuine, original and not submitted anywhere, either in part or full. All the necessary permissions from the patient, hospital and institution has been taken for submitting to neurology India”.

Blinded for review

The study and the data have been blinded for unbiased comments from reviewers.

Footnotes

This work published has been a part of Department of health and research funded study. All the authors mentioned have been either principal investigator, co- Principal investigators, junior research fellow and senior research fellow in the study. They have all contributed immensely toward the completion of the study.

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

References

- 1.Wilson BS, Dorman MF. Cochlear implants: a remarkable past and a brilliant future. Hear Res. 2008;242(1–2):3–21. doi: 10.1016/j.heares.2008.06.005. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.Drennan WR, Banerjee S, Garrison L. Estimating cost-effective device prices for Pediatric Cochlear implantation in India. Value in Health. 2015;18(3):A183. doi: 10.1016/j.jval.2015.03.1058. [DOI] [Google Scholar]

- 3.Bond M, Mealing S, Anderson R et al (2009) The effectiveness and cost-effectiveness of cochlear implants for severe to profound deafness in children and adults: a systematic review and economic model. [DOI] [PubMed]

- 4.Lee H-Y, Park E-C, Joong Kim H, Choi J-Y, Kim H-N. Cost-utility analysis of cochlear implants in Korea using different measures of utility. Acta Otolaryngol. 2006;126(8):817–823. doi: 10.1080/00016480500525213. [DOI] [PubMed] [Google Scholar]

- 5.Schulze-Gattermann H, Illg A, Schoenermark M, Lenarz T, Lesinski-Schiedat A. Cost-benefit analysis of pediatric cochlear implantation: German experience. Otology & Neurotology. 2002;23(5):674–681. doi: 10.1097/00129492-200209000-00013. [DOI] [PubMed] [Google Scholar]

- 6.Sarant J, Harris D, Bennet L, Bant S. Bilateral versus unilateral cochlear implants in children: a study of spoken language outcomes. Ear Hear Jul-Aug. 2014;35(4):396–409. doi: 10.1097/aud.0000000000000022. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Goyanka R, Garg CC (2023) Out-of-pocket expenditure on Medicines and Financial Risk Protection in India: is the sustainable development goal in Sight? Indian J Hum Dev.:09737030231169340

- 8.Swami H, Arjun A, Shivanand S. Cost-effectiveness of pediatric unilateral/bilateral cochlear implant in a developing country. Otology & Neurotology. 2021;42(1):e33–e39. doi: 10.1097/MAO.0000000000002862. [DOI] [PubMed] [Google Scholar]

- 9.Chapko MK, Liu CF, Perkins M, Li YF, Fortney JC, Maciejewski ML. Equivalence of two healthcare costing methods: bottom-up and top‐down. Health Econ. 2009;18(10):1188–1201. doi: 10.1002/hec.1422. [DOI] [PubMed] [Google Scholar]

- 10.Chauhan AS, Prinja S, Ghoshal S, Verma R, Oinam AS. Cost of treatment for Head and Neck cancer in India. PLoS ONE. 2018;13(1):e0191132. doi: 10.1371/journal.pone.0191132. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.DeCormier Plosky W, Bollinger LA, Alexander L, et al. Developing the Global Health Cost Consortium unit cost study repository for HIV and TB: methodology and lessons learned. Afr J AIDS Res. 2019;18(4):263–276. doi: 10.2989/16085906.2019.1680398. [DOI] [PubMed] [Google Scholar]

- 12.Jana A, Basu R. Examining the changing health care seeking behavior in the era of health sector reforms in India: evidences from the national sample surveys 2004 & 2014. Global Health Research and Policy. 2017;2:6–6. doi: 10.1186/s41256-017-0026-y. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Prinja S, Singh MP, Guinness L, Rajsekar K, Bhargava B. Establishing reference costs for the health benefit packages under universal health coverage in India: cost of health services in India (CHSI) protocol. BMJ open. 2020;10(7):e035170. doi: 10.1136/bmjopen-2019-035170. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Prinja S, Manchanda N, Mohan P, et al. Cost of neonatal intensive care delivered through district level public hospitals in India. Indian Pediatr. 2013;50:839–846. doi: 10.1007/s13312-013-0234-6. [DOI] [PubMed] [Google Scholar]

- 15.Prinja S, Gupta A, Verma R, et al. Cost of delivering health care services in public sector primary and community health centres in North India. PLoS ONE. 2016;11(8):e0160986. doi: 10.1371/journal.pone.0160986. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Sangwan A, Prinja S, Aggarwal S, Jagnoor J, Bahuguna P, Ivers R. Cost of trauma care in secondary-and tertiary-care public sector hospitals in North India. Appl Health Econ Health Policy. 2017;15:681–692. doi: 10.1007/s40258-017-0329-7. [DOI] [PubMed] [Google Scholar]

- 17.Kaur G, Prinja S, Ramachandran R, Malhotra P, Gupta KL, Jha V. Cost of hemodialysis in a public sector tertiary hospital of India. Clin Kidney J. 2018;11(5):726–733. doi: 10.1093/ckj/sfx152. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 18.Drummond M, Sculpher M (2005) Common methodological flaws in economic evaluations. Medical care.:II5-II14 [DOI] [PubMed]

- 19.Prinja S, Chauhan AS, Angell B, Gupta I, Jan S. A systematic review of the state of economic evaluation for health care in India. Appl Health Econ Health Policy. 2015;13:595–613. doi: 10.1007/s40258-015-0201-6. [DOI] [PubMed] [Google Scholar]

- 20.Thakur J. Key recommendations of high-level expert group report on universal health coverage for India. Indian J Community Med Dec. 2011;36(Suppl 1):S84–S85. doi: 10.4103/0970-0218.94716. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Prinja S, Sharma Y, Dixit J, Thingnam SKS, Kumar R. Cost of treatment of valvular Heart Disease at a tertiary hospital in North India: policy implications. PharmacoEconomics-Open. 2019;3:391–402. doi: 10.1007/s41669-019-0123-6. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22.Prinja S, Bahuguna P, Tripathy JP, Kumar R. Availability of medicines in public sector health facilities of two north Indian States. BMC Pharmacol Toxicol. 2015;16:1–11. doi: 10.1186/s40360-015-0043-8. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Prinja S, Aggarwal AK, Kumar R, Kanavos P. User charges in health care: evidence of effect on service utilization & equity from north India. Indian J Med Res. 2012;136(5):868. [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Data Availability Statement

Data supporting the results will be available upon request from the corresponding author. The data is not accessible to the public because of confidentiality and ethical restrictions.