Abstract

The proliferation of Distributed Energy Resources (DERs) is paving the way for new energy-efficient services that aim to make end-users more active. According to the literature, these services will be managed by a central figure, aggregators. This paper proposes several business models to accommodate them in the electric power industry. Several potential alternatives are identified from the study of different design elements, such as the control strategy, architecture, and signals that need to be exchanged. These alternatives are then tested by analyzing pairwise relationships between all the actors involved (Aggregator-Prosumers, Aggregator-DSO, and Aggregator-TSO). Every business model is first explained individually, including how contracts would operate, in order to determine their advantages and drawbacks. Finally, a comparison of all the alternatives is put forward together with an overview of the main initiatives that have already been implemented.

Keywords: Aggregator, Business model, Design elements, Flexibility

Acronyms

AGC Automatic Gain Control

AMI Automated Metering Infrastructure

AMS Aggregator Management System

ASM Ancillary Service Market

CCP Customer Connection Point

DERs Distributed Energy Resources

DESs Distributed Energy Systems

DG Distributed Generation

DMS Distribution Management System

DSO Distribution System Operator

EB Energy Box

EMO Energy Market Operator

EMS Energy Management System

ES Energy Storage

EV Electric Vehicle

ICT Information and Communication Technologies

RES Renewable Energy Sources

SM Smart Meter

SME Small and Medium Enterprises

TMS Transmission Management System

TSO Transmission System Operator

VG Variable Generation

1. Introduction

The improvement of Distributed Generation (DG) technologies is already creating new alternatives for on-site power generation, driving increasing adoption, and impacting distribution system operations. Even more, some emerging distributed generation options are fueled by natural gas and take advantage of the synergies among air conditioning, gas, and electricity.

Distributed Energy Storage (ES) technologies are being improved daily, and may enable a massive adoption and new capabilities that could alter how electric power systems operate. Moreover, with the introduction of the Electric Vehicle (EV), additional storage capability and new ancillary services to the electricity system may be provided [1], [2].

These new DERs, which are altering demands on the electric power system, connected with the fast development and introduction of Information and Communication Technologies (ICT) into the electric system, are prompting innovative business models and enabling the proliferation of new Distributed Energy Systems (DESs), from microgrids and virtual power plants to the remote aggregation of controllable loads and smart charging systems for EV fleets. These are some of the opportunities for creating new energy efficient services for consumers that will provide value to end energy users and upstream electricity market actors. Fig. 1 illustrates this framework, whose main actors and enabling technologies are the following:

-

•

Prosumers correspond to those end-users who can modify their consumption due to an external signal or produce their own energy through DERs. This can be done thanks to the integration of multiple energy resources (including gas), smart devices, and the different final uses of energy in a building: electricity, heating, cooling, and transportation (electric vehicles).

-

•

Integration and innovative use of ICT for smart home and building energy services. Interface points with the electricity and gas grids will be equipped with smart meters that will allow real-time pricing and time discrimination for network tariffs. The energy box will be the intelligent system that will ensure an optimal use of energy resources, while fulfilling the comfort levels requested by the prosumer.

-

•

(Prosumer) aggregators[3], [4], [5] which, under sustainable business models, collect the information from the different prosumers and provide energy prices and services in direct connection with them, using advanced models to operate in the wholesale energy market and in the ancillary services market.

Figure 1.

Conceptual framework and design of prosumers' aggregation business models.

These trends have been accelerated and shaped by public policy. Many countries are making efforts to prevent further climate change, which requires significant modifications in the electric power sector during the next few decades, prompting demand for low-carbon innovation and greater system efficiency. Due to the price reduction in distributed generation [6], synergies among electricity, gas, air conditioning, and poly-generation, and together with the intelligent aggregation of these distributed resources to trade energy and services in the markets, the energy business in developed countries is bound to undergo a paradigm shift. In fact, the technical capabilities of flexible loads to provide ancillary services have already been studied in terms of their suitability [7], their potential [8], and the scope of measurement and control [9].

The flexibility of prosumers has also been modeled in the literature. Refer to [10] for a review in which flexibility services are classified based on the target type of grid (i.e., distribution or transmission). Some interesting examples are [11], where a deterministic MIP optimization model is applied to a load aggregator participating simultaneously in the Nordic wholesale and tertiary regulation capacity power markets, and [12], where 20 residential houses reschedule their home appliances to fulfill flexibility requests using metaheuristics.

Implementation models that focus on the regulation for the aggregator and their relationship with balancing service providers and balancing responsible parties have been analyzed in [13]. However, the design of business models for the increasingly popular concept of aggregation of prosumers by integrating retail markets, distributed renewable energy, demand response, and advanced ICT is not considered.

Aggregator models within the energy sector have attracted attention in the literature, with several studies addressing diverse aspects of their operational frameworks, regulatory environments, and technical implementations.

Regarding relationships between agents, [14] offers a theoretical examination of the symbiotic relationship between aggregators and Distribution System Operators (DSOs), defining five distinct business models within the Norwegian context. However, their analysis is lacks of a holistic consideration of the technical and economic dynamics at play. Similarly, [15] and [16] explain the primary attributes of prosumer-oriented business models, scrutinizing prevailing regulatory paradigms and identifying barriers and facilitators. In particular, these studies superficially acknowledge that aggregation is a fundamental business model, without going deeper into its operational details. Additionally, research by [17] highlights the significance of digital alignment, comprising strategic decision support and operational support, in fostering business model efficiency, underscoring the relevance of technological integration in contemporary business processes of SMEs.

Business model canvas framework was applied in [18] to analyze aggregator-centric business models, defining the consumer-aggregator-electricity markets nexus from a strategic business point of view. However, their discourse overlooks technical fundamentals, concentrating instead on specific market domains such as day-ahead trading and reserve allocation. Introducing an innovative perspective, [19] advocates for an energy-as-a-service business paradigm tailored to aggregators of prosumers, thereby augmenting the discussion of conceptual frameworks about aggregation. Industrial reports, such as the one from [20], define business models and regulatory and economic relationships, leaving the technical part missing. Notable contributions by [21] delve into prosumer engagement within aggregation paradigms, leveraging reinforcement learning techniques to optimize portfolio management for helping distribution grid resilience.

In the regulatory domain, the status quo and challenges about aggregation have been extensively explored across various references [22], [23], [24], [25], with similar conclusions regarding persisting impediments despite the efforts made by policymakers.

Economic ramifications of aggregator interventions are investigated by [26], who estimate the revenue potential for prosumers engaged in explicit demand response, albeit with a brief assessment of the underlying business models. Moreover, several studies as [27], [28], [29], [30] expound upon remuneration mechanisms within aggregator frameworks, encompassing diverse modalities such as aggregated electric vehicles and blockchain-driven tariff regimes.

Bidding strategies constitute another focal point within the aggregator literature, with [31] proposing a comparative analysis of bidding strategies concerning distributed energy resource orchestration. Additionally, [32] and [33] proffer optimal bidding strategies tailored to aggregator interventions across diverse energy and reserve markets.

Notwithstanding these advancements, contractual dynamics among stakeholders remain relatively underexplored, albeit gaining traction within academic discourse. Noteworthy contributions by [34] and [35] advocate for decentralized contract designs tailored to demand response initiatives and reserve trading paradigms, respectively.

The proliferation of DERs is heralding a new era of energy efficiency services to empower end-users to become more actively engaged in the energy landscape. However, while existing literature has extensively explored various aspects of aggregator business models and their interactions within the electricity market, there remains a notable gap in the discourse. Specifically, the design of business models accommodating the aggregation of prosumers, encompassing retail markets, distributed renewable energy, demand response, and advanced ICT integration, has not received adequate attention.

The studies presented in the literature review have primarily focused on regulatory [22], [23], [24], [25] and economic [14], [15], [16], [18], [19], [20], [21], [34], [35] frameworks analyses, overlooking the technical-economic difficulties of operationalizing aggregator-centric business models. Furthermore, while some investigations touch upon the financial impacts and bidding strategies [31], [32], [33] associated with aggregator participation, a comprehensive understanding of the holistic landscape remains unavailable.

Thus, the motivation behind this paper is to address these gaps in the literature by proposing and analyzing several innovative business models tailored to accommodate the aggregation of prosumers, with a particular focus on technical relations within the aggregator and other agents and considering the regulation. By delving into the design elements, control strategies, architectural considerations, and signal exchanges inherent in these models, we aim to provide valuable insights into their operational viability and comparative advantages.

This paper delves into the realm of aggregation, focusing on effective asset management by aggregators and the development of innovative business models. The study begins with exploring aggregation models across different layers, emphasizing the business and management dimensions. In the business layer, this study provides an in-depth description of the relationships between aggregators and key stakeholders, including prosumers, DSOs, and ancillary services markets. The paper also scrutinizes the flow of information among these agents within the management layers. To facilitate a holistic understanding of the evolving landscape, the research proposes diverse business models tailored for both DG and aggregation. Rather than presenting comprehensive business models that simultaneously analyze interactions among all stakeholders, this paper offers multiple alternatives for pairwise relationships. It concludes with a comparative analysis of these models, accounting for the prevailing regulatory landscape. This comprehensive study provides valuable insights to aggregators, policymakers, and industry stakeholders navigating the dynamic energy sector.

It should be noted that the scope of this study is confined to the European context; consequently, the findings and discussions presented herein should be interpreted considering this geographical limitation. However, it is conceivable that several of the recommendations proposed could be adapted and applied to contexts beyond Europe, albeit with careful consideration of regional specificities. It is important to note that this study proposes a theoretical framework for applying business models. However, a quantitative analysis of these models will be conducted in future research.

The contributions made by this paper are outlined as follows:

-

•

The paper proposes and evaluates a suite of novel business models from a technological point of view designed to facilitate the integration of prosumers within the electric power sector. Existing research focus on the relation with other actors and economic fluxes among them.

-

•

It delves into the exploration of design principles, control mechanisms, architectural frameworks, and the dynamics of signal transactions intrinsic to these models. This examination aims to show their operational feasibility and delineate their comparative merits.

-

•

The paper conducts a investigation into the pairwise interactions among pivotal stakeholders (Aggregator-Prosumers, Aggregator-Distribution System Operators (DSO), and Aggregator-Transmission System Operators (TSO)). This analysis is intended to unravel the complexities inherent in each proposed business model and to articulate their potential ramifications.

-

•

A comparative scrutiny of the proposed models against existing initiatives is carried out to understand the aggregator's inner business models. This comparative discourse aspires to enrich the academic dialog and offer empirical insights that could guide policymakers, industry practitioners, and academic inquiries.

Section 2 briefly introduces the concept of flexibility, its importance, and its current state. Section 3, identify the design elements for business models that can be created around flexibility services. In Section 4, several business models built from the combination of the abovementioned elements are analyzed. Finally, in Section 5, the fitting of existing companies in the considered business models is discussed.

2. Flexibility and aggregation of DERs

The objective of electricity systems is to ensure reliable delivery of electricity at an affordable cost to consumers. Flexibility can be defined as the ability of a system to respond to variability and uncertainty of demand and supply. Loads change, sometimes in unpredictable ways (e.g., due to a soccer match), and conventional generators (i.e., OCGT, CCGT, pumped hydro, coal...) usually adapt the production to the demand through market mechanisms (offering balancing services in ancillary service markets). Unfortunately, these generators may sometimes be unavailable due to unexpected events such as natural disasters or mechanical failures. In future decarbonized energy systems, the number of generators that provide this flexibility (generation flexibility) is reduced since Renewable Energy Sources (RES) are considered Variable Generation (VG). RES provide power that changes over time based on weather conditions and sun paths. This may introduce faster changes in aggregate supply than in systems without VG. As a result, VG increases the response requirements. In addition, the energy sector will see a significant demand for systems that manage all the distributed energy resources DERs in the following years to comply with the European directives that require 70% renewable production by 2030. Therefore, demand flexibility becomes essential for balancing electricity systems with high renewable shares.

DG, ES, demand response, and the introduction of ICT into distribution electricity networks make up the so called DERs that will provide this flexibility. Their small capacity allows them to supply services in a local manner that traditional centralized generation cannot. For instance, some network investments could be postponed [36], [37] since DERs increase the usage of distribution networks. Moreover, DERs reduce network losses since the distance between generation and consumption is shortened [37] and help solve local contingencies [38], [39], [40].

In most cases, DER technologies imply some sort of aggregation to offer services to the grid, making small groups of commercial, industrial, or residential customers. Aggregation of resources presents advantages over individual DERs operation. These advantages, described in [41], are: a reduction of the risk of failing to fulfill market commitments, guarantee the possibility of entering markets, decrease the costs derived from not meeting market commitments, and exploit arbitrage potentials when network charges deal preferably with large loads (the aggregation of smaller devices allows offering a service several times with different loads instead of always using the same large load). Aggregation of resources can be carried out in different ways, such as microgrids (MG), virtual power plants (VPP), or EV fleets as seen in Table 1 [42].

Table 1.

Aggregation overview. Adapted from [42].

| Aggregation | What |

EV |

DG |

ES |

Loads (Residential, Commercial, Industrial) |

| Ways |

EV Fleets |

VPP |

– |

||

| Microgrids | |||||

| Aggregation of dispersed loads | |||||

| Types of services |

Buy/Sell Energy |

||||

| Buy/Sell Ancillary Energy Services | |||||

| How | Charging Strategies | Operation Management | Demand Response / Demand Shifting | ||

Nowadays, only a few countries allow the participation of demand in the Ancillary Service Market (ASM). The EU has recently noticed this fact and has published regulations to enforce the admission of demand in these markets with a view to obtaining a renewable system by 2030 (Fig. 2). This has paved the way for the update of the regulation in some EU countries. The agent dealing with demand in the ASM is known as aggregator. Currently, aggregators concentrate on industrial and large businesses where achieving the required volume and increasing or decreasing demand is more accessible. However, they are only helpful when big demand changes are necessary, since you typically have to turn on or off entire processes. Furthermore, depending on their nature, these processes can take some time to start and stop. Aggregators also work with big batteries, although this has a negative effect on the environment if its whole life-cycle is considered. Nevertheless, they are ignoring about 40% of the total consumption, Small and Medium Enterprises (SME) and residential buildings where manageable loads such as heating and domestic hot water account for 79% of the consumption [43].

Figure 2.

New relationships between agents.

Conventional generation plants and renewable generation participate in day-ahead markets with the demand aggregated by retailers to obtain the final unit commitment for the following day. Mismatches are corrected in intraday markets. In both cases, the Transmission System Operator (TSO) will review and correct the economic dispatch to obtain a correct system operation. The TSO also establishes the need for frequency restoration in each period to solve the real-time frequency deviations, at time scales ranging from seconds to tens of minutes. Until now, these services have been provided by hydro, CCGT, or OCGT groups that can react to these changes. However, new mechanisms need to be developed to accommodate renewable generators in large shares since their production depends on the weather.

Until recently, consumers did not have self-generation or automatic load-shifting systems, and thus were “forced” to accept energy prices set by third parties. Each day, more and more end-users are installing PV panels, ES, or smart-thermostats that enable them to react to prices and become prosumers. In this operating framework, prosumers are exposed to variable energy or grid tariffs. The only way to take advantage of their flexibility is by shifting their loads to periods with low energy or grid prices or periods when their own generation cost is lower than the purchasing price. This is known as implicit flexibility. It should be noted that large consumers can participate through the interruptibility service, but this is the last resource for the TSO to maintain balance [44].

A system with a high renewable generation share should seek for alternatives to balance frequency deviations produced by mismatches between production and consumption. Demand emerges as the natural solution. In order to reach the energy volume of conventional power plants, end-users' demand and storage are accumulated by their aggregator, who will determine how to better buy energy for their clients from the wholesale markets as well as how to offer their services to the TSO and DSOs through ASMs in order to obtain extra profit (explicit flexibility) [44], [45].

In a report from Pöyry and the Imperial College [45], some additional potential cost-savings are presented. They compare a system that continues to rely on conventional generation with one that has flexibility through aggregation. The benefits are the avoidance of energy curtailment from low-carbon generation sources, efficient provision of operating reserve and response facilities, potential savings in generation capacity due to the reduced need for low-carbon capacity in the system, the peak reduction, and the reduced need for backup capacity.

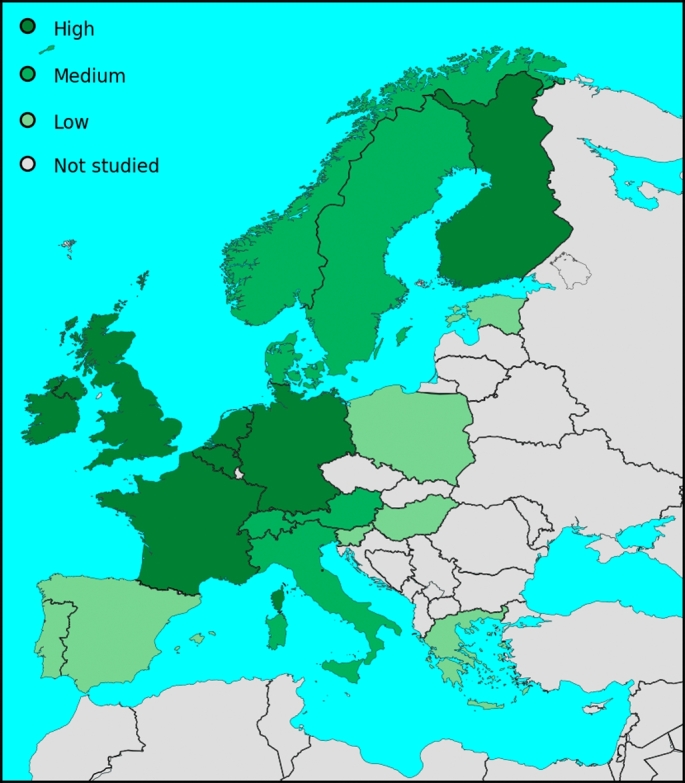

Some European markets have been reviewed in [46] in search of demand participation. A visual summary is presented in Fig. 3.

Figure 3.

Situation of demand participation in Europe.

-

•

The Mediterranean region (Spain, Portugal, and Italy) can be studied using Spain as reference. Aggregation participation in ASM is currently under adaptation by the TSO [47] and the Regulator [48]. This has been done following the European electricity balancing guideline [49] and the Clean Energy Package, which provide new rights to consumers. In addition, local congestions are also being studied in the IREMEL project [40]. A new service for large consumers, called Servicio de Respuesta Activa de la Demanda (Active Demand Response Service in English), has recently been implemented in Spain for consumers who have at least 1 MW of electricity in their power supply [50].

-

•

The Nordic countries welcome the aggregation of demand resources, with Finland being the most open. The Nordic TSOs have harmonized terms for the participation of aggregated resources. Balancing real-time data is readily available, most importantly the balancing price, and more of the balancing process is automated.

-

•

In the United Kingdom, markets are open to demand participation (mainly industrial and commercial) and several initiatives and projects (TRANSITION, FUSION, MADE, Intraflex, Future Flex) which investigate the rules and the roles of different demands in demand response programs or markets exist [51], [52]. In 2022, the National Grid Energy System Operator launched the “Demand Flexibility Service” for small consumers. It allowed consumers to reduce their electricity usage in response to signals from their retailers, earning them £3 per kWh saved [53].

-

•

Central Europe (Germany, Austria, and the Netherlands) are partially open to aggregation of demand-side resources with high interconnectivity, providing access to cross-border power exchanges. Flexibility in central Europe strives to a) support the increasing presence of renewable electricity, mainly coming from offshore wind parks and distributed wind and solar generation; b) overcome the limitations of grid construction (Germany); c) achieve sector coupling; d) implement the Clean Energy Package; and e) encourage growth of EVs.

In the realm of regulations, one of the primary obstacles to advancing aggregation business models is the state of regulatory frameworks, as noted by [54]. Studies have explored business models for mobility services, as exemplified by [55]. References [56], [25] have contributed to defining aggregator business models, with a particular focus on the utilization of tariffs for market participation. In a novel approach, [19] introduced a distinctive method for business model participation; however, their work primarily concentrates on a singular business model.

These previous investigations have predominantly concentrated on delineating business models for indirect market participation or introducing innovative tariff concepts (e.g., “energy-as-a-service”) yet they have not provided a comprehensive exploration of direct market engagement. The explicit definition of each design element within these business models, encompassing control types, hardware architectures, signal types, and the intricate interrelationships among various agents and their respective significance, remains somewhat elusive. To address this discernible gap, this study endeavors to rectify the situation by delivering a comprehensive definition of business models. Moreover, it delves into the intricate layers that constitute these models, encompassing both the management and business layers, thereby offering a more holistic perspective on aggregator business models.

The methodology employed in this study comprises two distinct phases aimed at analyzing aggregator business models.

In the initial phase, it is undertaked the delineation of various design elements inherent to aggregators, which are essential for their effective functioning within the energy landscape. Through the review of existing literature, it is defined these design elements to form the foundational basis of our analysis.

Subsequently, after defining these design elements, it is proposed specific configurations tailored to each business model and agent within the aggregator ecosystem. Then, it is delineated the operational characteristics and strategic imperatives associated with each proposed configuration. This phase serves to clarify the details of the aggregators' business models, providing a roadmap for their implementation and deployment within the electricity market.

In the final phase of our methodology, it is presented and compared the identified business models, evaluating their respective strengths and weaknesses. Through a systematic comparative analysis, it is discerned the distinctive attributes and performance metrics of each model, shedding light on their operational viability and potential implications for stakeholders.

3. Design elements for business models

The business models proposed later in this paper (Section 4) have been conceived considering a specific regulatory context, which is the most common in European countries. Models have been decomposed into two different layers (business and management) for enhanced understandability (Fig. 4). This theoretical framework for the analysis changes from the typical one used by the rest of authors, as it is based on the analysis by differentiating between the different layers of the aggregation, this idea was proposed by [57]. While the agents and their commercial relations are described in the business layer, the management layer includes the necessary information flow between agents.

Figure 4.

Regulatory context: the electricity business.

Regarding the business layer, the TSO is the agent that owns and operates the transmission grid. The two main activities of the generators are selling energy through the energy market operated by the Energy Market Operator (EMO) and providing ancillary services to the TSO. DSOs own and operate the distribution grid. The retailer is the agent in charge of selling electricity to final customers. These final customers pay the retailer for the service while the retailer procures the energy and pays regulated tariffs to DSOs for grid services and other system-regulated costs. A key aspect of this regulatory context is that the distribution activity is unbundled from supply; therefore, retailers trade energy while distributors provide network services. To conclude, the final customer is the agent who requires electricity and signs a contract with a retailer to acquire it.

The information flow between markets and management systems is represented in the management layer. In this regulatory context, two different types of markets are considered: the energy market and the ASM (A/S Market in the figure). In the energy market, retailers typically buy energy and generators sell energy. The energy price and energy exchanges are cleared in the energy market. The ancillary services market is the market through which generators sell ancillary services to the TSO to ensure system security.

Currently, agents have implemented different management systems to aid in the decision-making process. DSOs have a Distribution Management System (DMS) which controls the distribution grid operation and the Automated Metering Infrastructure (AMI) which collects the metering information that comes from the customers. This AMI has a line of communication with future Smart Meter (SM) owned by DSOs, which sense hourly energy consumption and peak consumption. They include bidirectional communications to send periodical measurements as well as receive power commands in real time. In a smart grid context, each Customer Connection Point (CCP) will be presumably equipped with a SM, so individual customer information would be at DSOs' disposal. Just like DSOs have a DMS for decision-making, retailers have an Energy Management System (EMS) to assist decision-makers in trading energy in the market, and the TSO has a Transmission Management System (TMS) to manage the transmission power network. Finally, generators have the Automatic Gain Control (AGC), which tries to stabilize the power grid.

Before trying to come up with business models that could integrate the figure of an aggregator, the different design elements that need to be considered when conceptualizing the business models have been identified. These elements allow to determine at a glance how the various alternatives compare and ensure that nothing essential is left out.

3.1. Definition

-

•

Control type: It can be either centralized or decentralized depending on whether the ultimate control commands (e.g., those that affect individual devices) are issued by the aggregator or decided by the local intelligence that manages the prosumers' devices.

-

•

Architecture: From a hardware point of view, it is non-hierarchical if every single measurement or command goes from one end to the other of the communication line. Conversely, if intermediate devices aggregate the information to reduce the bandwidth required, it would be hierarchical.

-

•Types of signals: Includes all the signal categories that can be issued to communicate the Aggregator Management System (AMS) and the Energy Box (EB).

-

–References: Inputs to closed-loop control systems that would try to follow them as closely as possible (e.g., reference for the air-conditioning system, the room's temperature should be as close as possible to 21 °C). The result cannot be immediately observed because the control takes time to reach the steady state.

-

–Commands: Control orders issued to individual devices (e.g., turn off the air conditioning). They can be immediately applied.

-

–Temporal parameters: Input data required by the optimization models that vary with time (e.g., price or consumption curves).

-

–Soft constraints: Restrictions that should ideally be met but that can be relaxed exceptionally (e.g., the prosumer would like the garden lights turned on from 6 to 8 p.m., but would not mind too much if they are lit up with a thirty-minute delay).

-

–Hard constraints: Restrictions cannot be violated under any circumstance (e.g., the refrigerator can never be turned off).

-

–

-

•

Communication between agents: It refers to the direction of the information flow: none (no information is shared), unidirectional (either only upstream or only downstream), bidirectional, bidirectional and iterative (both agents iteratively share information until they come to terms), and finally, market-based if all agents reach an agreement through a market mechanism.

-

•

Manageability: It refers to the degree of control over the prosumers' devices. It can be either direct, which means that the aggregator has control over individual loads and generators, or indirect, in which the ultimate decision is in the prosumers' hands. Both of them can also be full or partial. The former means that there is no limit on the type of loads that can be managed, the time frame in which they can be controlled, or the number of times the reference can be changed, among others. A partial scheme would impose one or several constraints (e.g., the air-conditioning system can only be managed between 5 and 8 p.m. and the prosumer only permits the aggregator to turn it off once in that period).

-

•

Risk allocation: This design element indicates how risk is handled. It can be shared or assumed entirely by one of the parties involved.

3.2. Comparison of the alternatives within each design element

Table 2 shows a qualitative comparison of the categories defined inside each design element. As can be observed, centralized control is bound to provide more profits than decentralized because everything could be individually taken into account in the optimization model —if the computers running it are powerful enough, which might not be valid if the number of devices is too large—, at the expense of a more complex ICT infrastructure that would take several years to deploy.

Table 2.

Comparison of the identified design elements. N/A means not applicable.

| Limited # of prosumers | Economically efficient | ICT infrastructure | Time to implantation | |

|---|---|---|---|---|

| Control type | ||||

| Centralized | Upper bound | +++ | +++ | Long term |

| Decentralized | No | ++ | ++ | Short term |

| Architecture (Hardware) | ||||

| Hierarchical | No | N/A | ++ | Medium term |

| Non-hierarchical | Upper bound | N/A | +++ | Long term |

| Types of signals | ||||

| References | No | N/A | N/A | Short term |

| Commands | No | N/A | N/A | Medium term |

| Temporal parameters | No | N/A | N/A | Medium term |

| Soft constraints | No | N/A | N/A | Short term |

| Hard constraints | No | N/A | N/A | Medium term |

| Communication between agents | ||||

| Market | Lower bound | N/A | +++ | Long term |

| Iterative bidirectional | No | N/A | ++ | Long term |

| Bidirectional | No | N/A | + | Medium term |

| Unidirectional | No | N/A | + | Short term |

| None | No | N/A | - | Short term |

| Manageability | ||||

| Full & Direct | No | +++ | +++ | Long term |

| Restricted & Direct | No | ++ | ++ | Medium term |

| Full & Indirect | Lower bound | ++ | + | Short term |

| Restricted & Indirect | Lower bound | + | + | Short term |

| None | No | - | - | Short term |

| Risk allocation | ||||

| Unilateral | N/A | N/A | N/A | N/A |

| Shared | N/A | N/A | N/A | N/A |

| None | N/A | N/A | N/A | N/A |

Centralized control will almost always go together with a non-hierarchical hardware architecture to allow the central intelligence to operate on a device basis. However, the huge information flow cannot surpass the bandwidth. This is currently a technical limitation that would have to be addressed. Still, this approach will continue to have an upper bound on the number of prosumers in the foreseeable future. Therefore, a hierarchical approach would allow overcoming this problem by aggregating data at different levels. The trade-off would be that device-specific data will no longer be available upstream.

Concerning the type of signals shared by the agents, they are neither good nor bad by themselves. It depends only on how they are managed. Implantation time has been estimated to depend on whether devices will be able to understand these signals in the near future or if it will take longer.

In the case of communication mechanisms, as they get more complex, they require more ICT infrastructure and, thus, more time before they can be put into practice. In addition, for a market to make sense, a minimum number of prosumers should participate.

Regarding manageability, better profits should be obtained as the system gains more control over the devices. Once again, more control translates into deploying more ICT infrastructure. Finally, which risk allocation scheme is better depends entirely on the point of view.

4. New business models

This section proposes several possible business models that could be implemented in an electric system where distributed generation and the figure of an aggregator play a key role. These models draw on the concepts that have been established and in prior research conducted by one of the authors of this paper, as outlined in [57].

The reasons behind aggregation have already been outlined in previous sections. The intention is not to advocate a certain model but to state objective facts associated with each possible model. For this reason, instead of presenting full business models in which the relationships between all the actors involved are analyzed simultaneously, multiple alternatives for pairwise relationships are put forward. The advantage of this approach is that, except for some constraints, a custom business model can be configured for each specific case using any of these pairwise relationships as building blocks. Succinctly, the interaction between all the actors, both at the business and management layers, is summarized in Fig. 5.

Figure 5.

Fundamental relationships between the actors of the electric system (top) and the information flow required for its management (bottom). Modification of structure proposed in [57].

From a business perspective, prosumers sign a contract with an aggregator that is, in some manner, the central actor, because it is also connected to the rest of the parties directly involved. Aggregators interact with the EMO to buy energy to satisfy customers' demand and sell any excess energy produced. They also check the feasibility of their planning stage with the Distribution System Operator (DSO), assist them in real-time congestion solving, and provide ancillary services to the TSO. DSOs can also limit individual prosumers' maximum power to solve congestions. To do so, they receive information from the smart meters through the AMI. Power limiting commands have to be forwarded and understood by EBs, which should manage their loads to satisfy the constraint and avoid a blackout. Finally, traditional centralized generators sell energy in the electricity market and ancillary services to the TSO.

Subsequently, different possibilities of interaction between aggregators and the rest of the actors (i.e., prosumers, DSO, and TSO through the ancillary services market) in the management layer are explained.

4.1. Relationship with prosumers

As shown in Fig. 6, four alternatives are considered both in the planning and operation phases for the relationship between aggregators and prosumers. Although DSOs are not depicted in Fig. 6, they are also affected by the actions of the aggregators because, as AMS attempt to smartly shape the energy profile of its prosumers throughout the day, the efficiency of the distribution grid is enhanced. DSOs should compensate the aggregator for this benefit in some manner. This topic will be treated in Section 4.2. Therefore, access tariffs are not considered in the following models because they are a consequence of the interaction between aggregators and the DSO.

Figure 6.

Proposed planning and operation business models for aggregators and prosumers.

The business models introduced in Fig. 6 have been obtained by combining the design elements defined in Section 3 as shown in Table 3. The following subsections delve into each of the models by explaining the general management mechanism and explicitly proposing possible contract configurations. The advantages and inconveniences of each approach are also put forward.

Table 3.

Breakdown of the proposed aggregator-prosumer relationships in their design elements. A and P stand for aggregator and prosumer, respectively. Arrows indicate information flow directions and ‘cons.’ means consumption.

| AGGREGATOR-PROSUMER |

||||

|---|---|---|---|---|

| Gateway | Max. power | Price-driven | Iterative | |

| Control type | ||||

| Centralized | x | |||

| Decentralized | x | x | x | |

| Architecture (Hardware) | ||||

| Hierarchical | x | x | x | |

| Non hierarchical | x | x | x | x |

| Types of signals | ||||

| References | A → P | P → A | ||

| Commands | A → P | |||

| Temporal parameters | A → P (price) | A → P (price) P → A (cons.) | ||

| Soft constraints | P → A | |||

| Hard constraints | P → A | A → P | ||

| Communication between agents | ||||

| Market | ||||

| Iterative bidirectional | x | |||

| Bidirectional | x | |||

| Unidirectional | x | x | ||

| None | ||||

| Manageability | ||||

| Full & Direct | x | |||

| Restricted & Direct | x | |||

| Full & Indirect | x | x | x | |

| Restricted & Indirect | x | x | x | |

| None | ||||

| Risk allocation | ||||

| Unilateral | x | A | P | |

| Shared | x | x | ||

| None | ||||

Regarding contracts, aggregators are assumed to own and install EBs to prosumers. To make it easier for prosumers to switch aggregators anytime, the following payment procedure is proposed. The prosumer pays for the installation costs plus monthly installments until the equipment is amortized because aggregators' business is not selling hardware but load management.

Hardware could be either proprietary or standard. In the former case, the equipment will always belong to the aggregator. If a prosumer decides to change the aggregator, the old equipment would be replaced by that of the new aggregator, and the prosumer would have to pay the installation fee again. In case the devices are not amortized yet, there would be no penalty because the leaving aggregator could install them again elsewhere. Should the equipment be standard, it could also be owned by the prosumer. The advantages and disadvantages of both approaches are the following:

Standard hardware The cost of the technology would be lower because it would easily benefit from economies of scale and if it belonged to the prosumer, it would be easier to change the aggregation service provider because they would only need to change their software. Nevertheless, it will take time until a standard is established, which would delay the implantation of aggregation technologies. Hence, this would be a medium to long-term alternative. Moreover, if it is owned by the prosumer, the initial investment would be higher. In addition, hardware renewal would be slower because it would be each prosumers responsibility. Aggregators would have to deal in the long run with equipment with different capabilities.

Proprietary hardware The initial investment is lower with respect to prosumer-owned hardware, and the integration of software and hardware would possibly allow the development of better control algorithms. Unfortunately, the fact that a new installation is required every time the prosumer wants to sign a contract with a different aggregator might discourage change.

4.1.1. Energy box as a gateway

The gateway model grants the AMS access to all or some electrically powered devices (full or restricted management). EBs are simply pass-through systems to enable prosumers' preferences (soft and hard constraints) reach the AMS along with the device measurements. With this information, the AMS would act as a central intelligence, optimizing all its prosumers and issuing commands to control every single device in real time. Regarding billing, two possibilities exist depending on how risk management is carried out:

-

•

Prosumers and aggregators agree upon an hourly price curve that will be valid throughout the duration of the contract. Optionally, a fixed management fee could also be included. The aggregator would also earn money by wisely bidding in the energy market. In this case, risk is assumed by the aggregator because its profit depends almost entirely on how well it gets along in the market.

-

•

Prosumers pay/receive the market price for the energy consumed/generated, and in addition, they are charged a fixed management fee that depends on their manageable power (i.e., generators and loads that can be controlled by the aggregator through the energy box). The income of the aggregator would be precisely this additional quantity, which is related to the manageable power because it has the potential for savings. The more manageable loads and generators available, the more profits the prosumer can obtain. In this occasion, market risk is split between both parties. The risk derived from the uncertainty of energy prices is assumed by the prosumer, whereas the responsibility for possible penalties due to deviations from the commitments made in the market would fall on the aggregator.

In addition, in case any hard constraint imposed by the prosumer is violated during operation, the aggregator would have to pay a fee determined upon signature.

As a consequence of being centralized and highly manageable, this solution would allow for maximizing the profits of aggregators and prosumers as every single device could be individually controlled and, therefore, included in their optimization model. Unfortunately, the ICT infrastructure to handle the huge amount of devices that need to be controlled and optimized does not scale well with the number of customers, because immense amounts of data would have to be transmitted to the AMS to enable centralized control and manage every device individually. Therefore, there is currently an upper bound on the number of prosumers that cannot be technically surpassed. Implementing a hierarchical management structure to overcome this limit is not a viable option because, in that case, individual devices would no longer be included in the global optimization.

Moreover, lending control over all the devices to an aggregator might not be acceptable for all types of customers. For instance, residential customers would probably be against an aggregator controlling their appliances. Conversely, this scheme could be interesting in generation (e.g., the aggregator would manage every windmill in a wind farm separately).

4.1.2. Limit the maximum power

Another possibility is that the AMS imposes an upper bound (hard constraint) on the power that may be consumed and generated by each prosumer at every time slot based on historical data. With this information, each energy box would locally determine how to allocate loads and how to manage its renewable energy sources and storage systems. This could be a short-term transition model between the current scheme and the model proposed in the following section.

Hourly energy prices would be established during the negotiation of the contract. The other solution proposed in the previous model is not possible in this case because, as optimizations are performed locally and the only information shared by the aggregators are maximum power restrictions, prosumers' energy boxes do not have information about market prices they can use to smartly schedule their energy consumption and generation. Risk is assumed entirely by the aggregator. This seems the only sensible option because prosumers have no knowledge about how the market or the system are behaving. If, during operation, there is a deviation between the maximum power and that finally provided plus a margin agreed upon signature, the aggregator would have to pay a fee as occurred in the previous model. This would be generally due to a real-time modification decided between the aggregator and the DSO. Hence, in reality, the penalty is being paid by the DSO, and the aggregator is simply an intermediary.

As a consequence of being decentralized, not very manageable, and having a unidirectional information flow, it requires very little ICT infrastructure because optimization is carried out by each prosumer locally. In addition, this approach scales well with the number of customers and would allow hierarchical control (if necessary) as big aggregators could manage smaller ones by issuing maximum power commands.

This solution is not optimal from the point of view of profits neither for the aggregator nor for prosumers because the system is decentralized and, more importantly, because prices are fixed in advance and do not take part directly in the planning or operation stages. In other words, the control signals issued by the aggregator allow almost no management of prosumers' devices.

4.1.3. Price-driven approach

In this model, data flow goes only in one direction. Based on historical data, each AMS provides electricity power-price curves (temporal parameters for EB optimization models) for each time t to its prosumers' EB in advance, in the hope that they use this information to rationally schedule their energy production and demand over the following hours. Therefore, planning depends mainly on how well-estimated price curves are. It is important to note that prosumers will only behave as expected with this model if a relatively large number is managed by the same aggregator because they would compensate for each other's randomness.

Likewise, in the second contract proposed in the gateway model, prosumers are charged/paid the market price for the energy consumed/produced plus a quantity proportional to their manageable power in the concept of management fee. Therefore, risk is shared because prosumers have to cope with market price volatility and aggregators with possible unfulfilled commitments. During operation, distributed generation and demand can be fine-tuned by modifying instantaneous price curves to correct deviations. The cost of any error in the curves delivered in the planning stage outside some predefined margins should be assumed by the aggregator. Therefore, in order to give prosumers an incentive to change their schedule, price curves should be modified either by increasing the prices at which generated energy is purchased or by reducing the expense of sold energy at non-problematic hours.

Individual prosumers' profit and degree of freedom would be higher because they would be able to allocate their resources according to the price curve as desired. Moreover, hierarchical control is also possible in this approach. Unfortunately, as a consequence of every prosumer optimizing locally, the profit aggregators and prosumers would not be optimal. However, as market prices are known by the local optimizers, it should be better than in the maximum power model because, with more information, they should improve how they manage their DERs (i.e., DERs are more manageable).

4.1.4. Iterative approach

Finally, the price-driven approach can be enhanced if an iterative communication mechanism between the aggregator's and prosumers' management systems is established. In this model, the aggregator submits the price curves to the prosumers, who optimize their local devices and answer with their schedule (planned consumption). If the aggregator is not completely satisfied with the planning result, it can modify the curves and send a new proposal to the customers. This process can be repeated as many times as necessary.

The contract would be almost exactly the same as in the previous model except for a difference in how risk is split. Possible penalties for not fulfilling market commitments would be charged to prosumers (for not sticking to their schedule). However, prosumers can compensate for each other's deviations, and they would only have to pay in case the aggregated deviation of all the prosumers managed by the aggregator is outside the admissible range. Consequently, the risk is lowered thanks to aggregation.

In addition to the advantages of the price-driven approach, aggregators' profit is likely to increase with respect to the previous model because they would be able to refine their price curves, and consequently modify the demand, thanks to the feedback received from the prosumers. Nevertheless, this approach requires a slightly more sophisticated ICT infrastructure than the price-driven alternative to enable bidirectional communication and implement the iterative process.

4.1.5. Comparison

Table 4 presents an overview and comparative analysis of the four distinct models proposed in the preceding subsections. The table summarizes the key conclusions derived from the analysis of each model and presents them in a concise yet informative manner. As can be observed, models 2 to 4 could be progressively implemented over the following years. Once the ICT infrastructure required to issue maximum power commands to prosumers is installed, it would be easy to send prices too. Finally, the bidirectional communication mechanism that would allow prosumers to agree their schedule with the aggregator based on energy prices would be implemented. By contrast, the complexity of the infrastructure required for the first model, and the more than probable reluctance of some types of customers, would restrain its implementation in the short and medium terms.

Table 4.

Comparison of the business models proposed for the aggregator-prosumer relationship.

| AGGREGATOR-PROSUMER RELATIONSHIP |

||||

|---|---|---|---|---|

| 1. Gateway | 2. Max. power | 3. Price-driven | 4. Iterative | |

| Prosumers' profit | +++ | + | ++ | ++ |

| Aggregators' profit | +++ | ++ | ++ | +++ |

| Limited # of prosumers | Upper bound | No | Lower bound | Lower bound |

| ICT infrastructure | Complex | Simple | Simple | Average |

| Hierarchical control | ✕ | (✓) | ✓ | ✓ |

| Implantation time | Long term | Short term | Medium term | Long term |

| Penalizations | Fee | Fee | Price | Price deviations |

| Typical customers | Generators | Households, industrial, and tertiary | Households, industrial, and tertiary | Industrial, tertiary, smart homes, smart buildings, smart districts, and microgrids |

4.2. Interaction with DSOs

The following agents aggregators have to deal with are DSOs because in order to manage their prosumers' energy, they need to make use of the distribution grid. This section outlines five ways in which this relationship could be established (Fig. 7). While reading through this section, it should be borne in mind that all unexpected contingencies are solved in real-time by the DSO by limiting prosumers' maximum power via their SMs. DSOs will be held liable for the incurred expenses according to the quality criteria established in national regulations. Consequently, this section deals only with congestions that can be prevented thanks to the interaction between aggregators and DSOs. Following the same procedure used in the previous section, Table 5 shows which design elements are used to build each of the proposed models.

Figure 7.

Proposed interaction models between aggregators and DSOs.

Table 5.

Breakdown of the proposed aggregator-DSO relationships in their design elements. A and D stand for aggregator and DSO, respectively. Arrows indicate information flow directions and ‘cons.’ means consumption.

| AGGREGATOR-DSO |

||||

|---|---|---|---|---|

| Isolated | Tariff-based | Iterative | Market | |

| Control type | ||||

| Centralized | ||||

| Decentralized | x | x | x | x |

| Architecture (Hardware) | ||||

| Hierarchical | ||||

| Non hierarchical | x | x | x | x |

| Types of signals | ||||

| References | ||||

| Commands | ||||

| Temporal parameters | D → A (price) | A → D (cons.) D → A (price) | A → D (cons.) A → D (price) | |

| Soft constraints | ||||

| Hard constraints | ||||

| Communication between agents | ||||

| Market | x | |||

| Iterative bidirectional | x | |||

| Bidirectional | ||||

| Unidirectional | x | |||

| None | x | |||

| Manageability | ||||

| Full & Direct | ||||

| Restricted & Direct | ||||

| Full & Indirect | x | x | x | |

| Restricted & Indirect | ||||

| None | x | |||

| Risk allocation | ||||

| Unilateral | A | A | ||

| Shared | x | |||

| None | x | |||

4.2.1. AMS as gateway

An alternative could be that the DSO issued commands through the AMS to control how prosumers operate and guarantee the system stability and the quality of supply. This solution is not valid in a system where distribution is unbundled from supply because the DSO and the aggregator would be virtually the same agent. The aggregator would work only as a pass-through. It is presented here as a reference but will not be further analyzed.

4.2.2. Isolated

This is the current model, in which there exists no communication or any type of relationship between aggregators and DSOs. If the distribution network cannot cope with the grid usage of the aggregators, a contingency occurs. This model is used as a baseline for the rest of the proposed solutions.

4.2.3. Tariff-based approach

It is the equivalent of the price-driven approach in the relationship between aggregators and prosumers. DSOs would issue access tariffs for every node. The aggregators would then optimize their prosumers with one of the business models proposed in Section 4.1. During operation, the DSO would be able to modify access tariffs in order to prevent, or at least mitigate, the effect of expected contingencies.

The contract would clearly state that the aggregator would pay the DSO by means of the access tariff, which would include a fixed and a variable term. The regulator would be responsible for establishing the formula that has to be used to compute the real-time tariffs in every node depending on energy losses and the quality of service. This variable component would be employed for distribution network expansion. The mechanism to divide the money should be determined, bearing in mind that those areas that require new lines more urgently should receive a higher share.

The fact that DSOs costs are taken into account by the aggregator increases the expected profits with respect to the isolated model. Furthermore, there would be fewer contingencies that result in a blackout than with the current scheme. However, communication is not bidirectional.

4.2.4. Iterative

Every aggregator submits its expected energy profile for the next few hours, and with all of their information, the DMS answers with a set of access tariffs. With this new information, aggregators would recompute their schedule and submit it again. This process is iteratively repeated until the DSO and the aggregators come to terms. With this mechanism, the DSO makes sure that the planned network usage is feasible.

Likewise, in the tariff-based approach, access tariffs would have a fixed and a variable component and would be calculated using an algorithm defined by the regulator according to quality and loss reduction criteria. The variable term would be used to expand the distribution grid in those areas in which more money was raised, which should be those in which additional lines are more necessary. If, during operation, an aggregator does not fulfill its schedule and, as a consequence, congestion occurs, it will be penalized. Therefore, risk is being assumed by the aggregator.

As a consequence of the iterative process, contingencies would drastically diminish, whereas its ICT infrastructure is more complex because it needs to provide bidirectional communication between DSOs and aggregators.

4.2.5. Market-based

During the planning stage, all aggregators go to a market in which they bid for the power they can drain from each node managed by the DSO. The market would be cleared in the following manner. The DSO would classify the bids for each node in descending order, and power would be assigned to each aggregator until the node's power limit is reached. All power would be paid at the clearing price.

Access tariffs would also have fixed and variable terms. The fixed term would be determined by the regulator, whereas the variable would be the result of market clearing. As in the previous two models, the variable term would be used for line expansion. In addition, to discourage aggregators from abusive bidding (i.e., buying all the capacity to stop other aggregators from fulfilling their commitments), underuse of the purchased capacity during operation outside a predefined margin would be penalized. The penalization scheme for contingencies would be the same as in the previous model. Risk is allocated to the aggregator.

Apart from the fact that all contingencies that can be detected in advance would be avoided, aggregators would have the possibility of altering nodal prices as opposed to the tariff-based approach in which they are imposed by the regulator. As a result, lower access tariffs should be theoretically achieved. Nonetheless, the ICT infrastructure is quite sophisticated because, in addition to bidirectional communication, a market needs to be set up.

4.2.6. Comparison

In the preceding subsections, a number of potential models were discussed with regard to their feasibility within a liberalized system. The most pertinent information and conclusions regarding these models have been collated in Table 6.

Table 6.

Summary of the viable relationships between aggregators and DSOs.

| AGGREGATOR-DSO RELATIONSHIP |

||||

|---|---|---|---|---|

| 2. Isolated | 3. Tariff-based | 4. Iterative | 5. Market-based | |

| Aggregators' profit | ++ | ++ | + | +++ |

| Quality of service | + | ++ | +++ | +++ |

| ICT infrastructure | None | Average | Complex | Complex |

| Implantation time | Current model | Medium term | Medium-long term | Long term |

The proposed tariff-based and iterative models are considered previous stages to a final market-based system. They are solutions suitable for specific contexts like natural monopolies or developing systems, but several deficiencies start to arise when factors such as competency and high performance are introduced.

A tariff-based model would serve as a good transition model to a market-based interaction. Compared to an isolated system, it helps avoid contingencies in the network and takes into account information from the DSO. However, as communication only flows in one direction, coordination would still be low, making it difficult or even impossible to solve certain contingencies. This would be a good solution for a system which does not have a developed market platform.

An iterative interaction model would make sense in a context where there is a monopoly of an aggregator in a constraint management zone. The moment there are more of them, the risk of not reaching an agreement between parties, or arriving at a non-optimal result for all of them, becomes real. This could lead to a situation that could compromise service and that would not guarantee a level playing field for aggregators.

The interaction of aggregators with the DSO is a matter that is deeply dependent on the regulation of each market. As aforementioned, according to European regulation [49], during the next few years, electric markets should start allowing the participation of demand through aggregators. This change is already bringing changes into how DSOs manage their contingencies, including flexibility as a key tool. As a result, a homogenization in the developed electrical markets can be observed, at the transmission level and also at the distribution level, since market-based mechanisms are the best way to ensure transparency and to achieve better network management with a reduced cost.

4.3. Ancillary services market

Finally, the aggregator has at its disposal many distributed generators and storage systems that could be used to provide ancillary services to the TSO through the A/S market. On this occasion, only two alternatives have been considered (Fig. 8), one of which has been ruled out for the reasons explained below.

Figure 8.

Possibilities of interaction between aggregators and the TSO.

4.3.1. Direct communication

In this scheme, the AMS sends bids to the A/S market and receives a commitment that needs to be forwarded to the DMS to determine its feasibility. If it is feasible, it is submitted to the prosumers' energy boxes. Otherwise, the market would have to modify the commitment. During contingencies, the process is analogous with the difference that the AMS sends measurements to the TSO and receives commands in response.

4.3.2. Communication through the DSO

The other alternative is that aggregators delegate the responsibility of interacting with the ancillary services market to the DSO. The advantage is that there is no need to check if the commitment is technically feasible because the DMS already knows. However, this option has been discarded because it does not make much sense that the DSO, which has no interest in maximizing prosumers' profits, goes to the market and makes bids on their behalf.

5. Aggregation business models in existing energy companies

An analysis of the main European markets and over 80 companies has been carried out in order to have an insight into how the industry is implementing the proposed business models, their rationale, and the implications of these decisions. The relationship between aggregators and prosumers has a very clear tendency towards a specific model: energy box as a gateway, while the interaction with DSOs is through a market-based mechanism. This last fact comes as no surprise since it is the approach used across most of the European electric systems (e.g., IREMEL [40], TRANSITION [51], PICLO-FLEX [58]). Finally, as concluded before, aggregators and TSOs interact directly using ancillary services markets.

The reason for the prevalence of the energy box as a gateway is that this model allows for a global optimization while each prosumer's preferences can be taken into account. Besides, it is highly flexible while profits are maximized and risk is minimized through aggregation. Scalability is a challenge, but ICT infrastructure has improved to a level where the data flow is manageable for even a large number of prosumers. Notwithstanding, most of the analyzed companies are oriented towards industrial clients, which eliminates this issue as they manage a low number of clients with big assets. In this case, the operation of assets is easier, as industrial environments usually have already developed centralized control systems. Furthermore, even those companies which are oriented to residential clients usually aim to manage specific type of assets such as batteries, PV panels, EV charging posts, or heat pumps which are considered to be the low-hanging fruit.

The industrial sector does not have a representative business model as each case is different and requires a unique solution (e.g., [59], [60], [61], [62], [63], [64], [65], [66]). Some can benefit from installing PV or wind to support their operation and sell the surplus to the grid. Others can manage their loads, which are very intensive in energy, such as in the metallurgic industry or factories with high use of pumping. An additional model is the use of backup batteries for critical systems to provide flexibility while always maintaining a security charge.

By contrast, both in the residential and commercial sectors a rising business model (e.g. [67], [68], [69], [70], [71], [72], [73]) is the aggregation of large volumes of batteries combined with PV panels. Batteries have the advantage of being able to provide very fast response times, which makes them ideal for participating in both fast markets and local flexibility markets. Then, by just measuring the total demand of the installation, and together with the embedded metering of the batteries and solar generation, one can predict and optimize the operation of the battery to carry out peak-shaving, take advantage of time-of-use tariffs, and provide highly profitable flexibility services to the grid in multiple markets. This business model is even attracting battery manufacturers, since through an easy technology integration and their capacity to recycle some of their assets they can offer more competitive prices. The downside is the high investment needed for the batteries and PV systems, which have long return times. Additionally, batteries need to be replaced after a number of charging cycles, which on a big scale can pose an environmental problem.

Another common model is the management of heating and cooling through the control of heat pumps or centralized heating [74], [75], [76]. This technology usually only allows to participate in slower markets and it is mainly offered in local flexibility markets. It has the disadvantage that controlling thermal elements requires thermal modeling of the installation, which requires data on the behavior of the building. Additionally, it requires knowledge of the user preferences and habits. However, the investment needed is very moderate compared to the previous case. This model has bigger computational needs as you have to control more data and consider more variables.

A less frequent business model is that in which the aggregator reaches many different types of assets [77], [78], [66]. This is caused by the fact that each asset needs a different modeling, and making them compatible increases complexity exponentially in terms of computing, data structure, and monitoring. In return, it benefits from the advantages of each asset type and from the synergies between them while offering a vertical service to the customer.

What all the previous models have in common is the fact that optimization is centralized due to the fact that in order to aggregate assets and operate them jointly, all of the latest information is needed. Decisions are made by the platform intelligence and then distributed among all assets. Usually, there is a second layer of intelligence that makes small adjustments in real-time to ensure deviations in customers' behaviors cancel each other out thanks to the large scale. Regarding the reluctancy of certain users to lend control of their appliances, it can be mitigated by allowing them to closely monitor the status of their devices and even override the commands issued by the aggregator sometimes. Besides, the fact that users can then centralize the control of their assets can be seen as an additional drive for the clients.

The other two considered models, limiting the max power and the price-driven approach, appear not to not be attractive to the market so far due to the fact that they would not be competitive enough compared to the energy box as a gateway. Decentralized models do not offer an optimal operation of the assets, and a unidirectional communication flow is not flexible enough to respond to changes in markets effectively.

6. Conclusion

This study provides several valuable insights into the world of aggregator business models and their role in the evolving energy landscape.

First and foremost, it offers a comprehensive exploration of how are the different options for aggregators regarding the use of the design elements and outlines the key considerations essential for developing innovative business models for aggregators. It highlights the significance of aggregation models across both the business and management layers, shedding light on the complex interrelations between aggregators and various stakeholders. These stakeholders include prosumers, DSOs, and ancillary service markets, with a particular focus on their commercial interactions within the business layer. Moreover, it delves into the intricate information flows between these agents, especially in the management layers.

Furthermore, this paper introduces a range of business models catering to both DG and aggregation. Rather than presenting exhaustive, all-encompassing models that simultaneously analyze relationships among all involved actors, the paper offers multiple alternatives for pairwise relationships. This approach enhances flexibility and adaptability to different contexts and regulatory settings, offering practical insights into the varying design elements that can be employed in specific scenarios. The qualitative comparison of these alternative business models, considering factors such as the number of prosumers involved, economic efficiency, required ICT infrastructure, and the time to implementation, provides valuable guidance for stakeholders and policymakers alike.

In addition to these contributions, the paper conducts a review of European regulations to define the regulatory framework. It elucidates the current interactions between different agents and proposes an interaction framework for aggregators, covering both management and business layers. This analysis enables the identification and definition of the design elements essential for conceptualizing the various business models explored in this paper.

One of the critical outcomes of this study is the proposal of alternative business models that can be implemented under different regulatory contexts, enabling a more nuanced and flexible approach for aggregators in various markets. Additionally, the comparison of these models highlights the importance of considering specific design elements and their impact on the feasibility and success of aggregator business models. These insights provide a valuable framework for stakeholders and policymakers to navigate the rapidly changing energy landscape.

It must be emphasized that the insights derived from this research are confined to the European context, given that it formed the cornerstone of this analysis. However, it should be recognized that with appropriate adjustments to the variables involved, the approach and findings of this study possess the potential for applicability in other regional contexts.

This paper contributes to the existing literature on traditional business model analysis by introducing a novel perspective that focuses on the technical aspects of business model aggregation. It delineates the essential elements required for facilitating communication between agents and examines the implications of these technical factors on business models. By integrating both technical and economic flows within the analysis, this work paves the way for the derivation of innovative business models. This approach enriches the academic discourse on business model analysis, in addition it also offers practical insights for the development of more cohesive and efficient business strategies.

As a path for future work, it would be beneficial to investigate the willingness of consumers to engage in each type of relationship, the extent of control they desire over their equipment, and the preferred rate structures. This could provide further insights into the acceptance and viability of various business models. Additionally, assessing the impact of these business models on consumer savings and the overall profitability of aggregator business models would be a valuable avenue for future research.

Collectively, the findings of this paper advance our understanding of aggregator business models and offer a practical framework for their implementation in real-world scenarios. The potential avenues for future work mentioned will help expand our knowledge and refine the practical application of these models in the evolving energy sector.

Data availability statement

No data was used for the research described in the article.

CRediT authorship contribution statement

Francisco Martín-Martínez: Writing – original draft, Investigation, Formal analysis, Conceptualization. Jaime Boal: Writing – original draft. Álvaro Sánchez-Miralles: Supervision, Project administration, Methodology, Funding acquisition. Carlos Becker Robles: Writing – review & editing, Investigation, Formal analysis, Conceptualization. Rubén Rodríguez-Vilches: Writing – review & editing, Investigation, Formal analysis, Conceptualization.

Declaration of Competing Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Acknowledgements

This paper has been prepared in the framework of the ReDREAM project, funded by the European Union's Horizon 2020 research and innovation program (Horizon2020 Framework Programme) under grant agreement number 957837.

Contributor Information

Francisco Martín-Martínez, Email: fmartin@comillas.edu.

Jaime Boal, Email: jaime.boal@iit.comillas.edu.

Álvaro Sánchez-Miralles, Email: alvaro@comillas.edu.

Carlos Becker Robles, Email: becker@stemyenergy.com.

Rubén Rodríguez-Vilches, Email: rrodriguezv@comillas.edu.

References

- 1.EDSO; May 2014. Flexibility: the role of DSOs in tomorrow's electricity market. Tech. rep. [Google Scholar]

- 2.BDEW, German Association of Energy and Water Industries; Mar. 2015. Smart grid traffic light concept. Design of the amber phase.https://www.bdew.de/media/documents/Stn_20150310_Smart-Grids-Traffic-Light-Concept_english.pdf Tech. rep. [Google Scholar]

- 3.Eid C., Codani P., Chen Y., Pérez Y., Hakvoort R. Aggregation of demand side flexibility in a smart grid: a review for European market design. 12th International Conference on the European Energy Market (EEM); Lisbon, Portugal; 2015. pp. 1–5. [DOI] [Google Scholar]