Abstract

How renters respond to economic hardship, and how landlords respond when tenants fail to make rent, are understudied questions, owing largely to limited data. We use experiences from the COVID-19 pandemic to begin answering these questions. Drawing on both new census data and two original surveys of renters in Los Angeles County, we test nine hypotheses about the sources of renter distress and landlord reactions to it. We find that lost work and lost income are the primary drivers of missed or late payments. Most tenants who fell behind entered into repayment plans with their landlords. Eviction threats were uncommon but increased as the pandemic persisted. Landlords were more likely to threaten eviction as tenants fell further behind, and smaller landlords were more likely than larger ones to cut tenant services and threaten or initiate evictions. Our evidence suggests that government income support helped tenants pay rent and thus helped stave off eviction threats. We also find that tenants took on other forms of debt, such as credit cards, loans from family, etc., to make rent. These debt burdens generally will not be relieved by housing assistance, and so require other policy responses.

Keywords: Renters, eviction, COVID-19, income

Little academic research examines tenants’ decisions to pay or withhold rent. A sizable literature investigates when and why homeowners pay their mortgages, and the consequences when they do not, but equivalent studies for renters are largely absent. This omission is notable, because renters are, along almost every dimension, more vulnerable than homeowners. About 25% of homeowners own their housing free and clear, meaning they do not have a mortgage payment. Many of those with payments, moreover, have fixed-rate mortgages, and thus face decreasing real costs over time, even in cities where real rents are rising.

Homeowners, compared to renters, also have a higher ability to pay. The median household income for homeowners is almost double that of renters ($78,000 to $40,000; U.S. Census Bureau, 2018b), and where median liquid savings among homeowners is $3,700, among renters it is zero.1 Homeowners also have illiquid savings: they reside in a safety net that is the housing unit itself. If necessary, owners can rent out some rooms for extra money, or sell the home and use the proceeds to move. Renters have fewer such options. Finally, in many places, renters have fewer legal protections against removal. It is often easier for a landlord to evict a tenant than for a lender to foreclose on a homeowner.

A fast-growing body of research does study eviction, which is one outcome (and often the most severe outcome) of rent nonpayment. But not all eviction results from nonpayment, and the questions of when nonpayment leads to eviction, and what leads to nonpayment itself, have gone largely unstudied.2 So too has the question of how tenants balance a choice between two bad outcomes: incurring rental debt, or paying rent by incurring other forms of debt, such as putting rent on credit cards.

This article addresses these heretofore underexamined questions, using data from the COVID-19 emergency in Los Angeles, California. The COVID pandemic gives housing researchers both the means and the opportunity to learn more about nonpayment. The massive economic contraction that accompanied the public health response to COVID threw many tenants into economic distress, making it difficult for them to pay rent. The pandemic also generated a new data set—the U.S. Census Pulse Survey—that tracked rent payment and renter well-being in a way no prior data set had. The Pulse thus offers an unprecedented window into renter behavior, and we draw on it in this research.

The Pulse also, however, left some important questions unasked: about the size of the tenant’s debt, as well as the characteristics of landlords, and how landlords react to nonpayment. To complement the Pulse, in this article we also draw on two waves of an original survey of tenants in Los Angeles County, which cover these topics in more depth.

As we will discuss, neither the Pulse nor our survey is perfect, so we are cautious about making inferences. As we will also discuss, the COVID-19 pandemic was unique in two nontrivial ways, and readers should interpret our results with those circumstances in mind. First, during COVID-19 a large number of tenants suddenly had trouble paying. If the broader prevalence of nonpayment affects decisions made by both tenants and landlords, then results from the pandemic may not automatically generalize to instances when tenants’ inability to pay is less common. Second, during COVID-19 eviction was not an option for many landlords, including landlords in Los Angeles. Landlords could start an eviction process but could not legally remove tenants. These circumstances were unique.

A third limitation is that we only study Los Angeles. We do so for a reason: examining one area minimizes confounds that could arise from interregional variance in economic conditions, stay-at-home orders, and government assistance. But it also limits generalizability. We will show, however, that trends in renter distress in LA did not depart dramatically from those elsewhere.

These caveats aside, our results suggest the following: during COVID renters were, all else equal, more likely than owners to miss housing payments. They also missed rent at a rate substantially higher than the pre-COVID baseline. Lost work and lost income were the overwhelming drivers of these missed payments, and government programs that restored income (such as stimulus checks and unemployment insurance (UI)) appear to have had a protective effect. Although eviction threats were rare, reports of them increased as the pandemic went on, and landlords were more likely to threaten eviction as tenants fell further behind. Smaller landlords were more likely to threaten eviction than larger ones, even controlling for the fact that tenants in smaller units were more likely to miss a payment. Finally, many tenants, both those behind on rent and those who stayed current, took on other forms of debt to make rent, relying on credit cards, emergency loans, savings accounts, and friends and family.

Our article contributes, most obviously, to the growing body of work about the economic fall-out of, and policy response to, the COVID-19 pandemic. More broadly, our findings add some nuance and detail to conventional analyses of tenant troubles. We offer some of the literature’s first detailed analyses of nonpayment and its consequences. In particular, we provide some empirical estimates of how tenants may take on debt to stay current with their landlords. This debt is a worthy topic for future research. Concerns about housing precarity are often, and understandably, focused on eviction. But eviction is only the most acute and visible consequence of renter distress. Many renters in our sample stayed current on rent but borrowed to do so. Given their low incomes, escaping the debt that resulted may take many years.

Background: To Pay or Not to Pay

Most of the literature examining missed housing payments investigates mortgage delinquency and default—homeowners who encounter financial difficulty and elect to not pay (Buschbom et al., 2018; Corbae & Quintin, 2015; Mayer et al., 2014). This research emphasizes both the selective and the game-theoretic nature of nonpayment: selective because not all homeowners find themselves in situations where payment is difficult, and game-theoretic because when that situation arises, the mortgage payment becomes less a mutually beneficial exchange between borrower and lender, and more a strategic interaction. The borrower weighs nonpayment against its likely consequences, and banks in turn weigh the costs and benefits of their own actions in the event the borrower does not pay.3

Mortgages differ substantially from rental contracts, but a similar calculus could surround renters and landlords. Tenants unable to pay a coming month’s rent can react in several ways. They might seek help from friends or family members, put some or all of their rent on a credit card, or seek payday or emergency loans. They might pay rent late, and/or pay only a portion of their rent. In the extreme, they may choose to not pay rent at all or to move. The ultimate decision will depend on their ability to pay (the cash they have or can get), other expenses they face (food, medicine, and so on), their expectations of assistance (from the government, nonprofits, or family and friends), and, not least, the perceived consequences of not paying. Tenants who see their landlord as forgiving may be more likely to withhold payment, and spend their limited money instead on other priorities. Tenants who anticipate a harsh reaction from their landlords, in contrast, might devote at least some resources to rent, and do so by taking on other forms of debt or forgoing other expenses. Note that in this latter case, the tenant makes rent but does not escape financial distress; the distress manifests not in unpaid rent but in decreased spending elsewhere, or in higher debt levels from credit cards or other loans.

If tenant perceptions matter, then errors in those perceptions could be consequential. They may also be common. Tenants who rent from family or friends, or from small landlords with whom they regularly interact, might be more likely to withhold payment, believing their personal relationships will insulate them from reprisal or repercussion. But landlords must react when tenants miss a payment, and many of the factors they consider when deciding their reaction will be invisible to the tenant (just as many factors precipitating tenant nonpayment may be invisible to the landlord).

When tenants miss a payment, landlords need to consider their own expenses and reserves, along with the costs and benefits of trying to remove the tenants who haven’t paid. How building owners weigh these different factors will vary across landlords, and likely vary across types of landlord (e.g., corporate vs. mom-and-pop), but how they will vary is not obvious to the tenant and indeed not even obvious, a priori, to researchers. For example: are small landlords more likely to own their property free and clear, and thus (perhaps combined with personal knowledge of their tenants) less likely to evict when rent goes unpaid? Or are corporate landlords, because they have larger cash reserves that let them absorb losses (or more knowledge of and access to assistance programs), the ones who will show more forbearance? Little existing evidence can be brought to bear on these questions. The U.S. Census Bureau conducts a Rental Housing Finance Survey, but data on debt-to-equity ratios are missing for about 60% of its sample, making it hard to say that one class of landlord or another is better equipped to absorb unpaid rent.4 Unpaid rent, furthermore, is only one type of expense: landlords must also contend with property taxes, utilities, and maintenance, much of which lies outside the easy observation of tenants deciding whether to pay or researchers who study payment.

This opacity could create a mismatch between how tenants anticipate landlords will react and how landlords actually react. If tenants believe smaller landlords will be more forgiving, but smaller landlords are in fact more concerned about missed payments (because each rent payment represents a larger share of their income) then tenants may miss some rent and expose themselves to harassment or removal. Decker (2021), in a nationwide survey of small (one to four units) rental property owners, finds that although these owners are generally more affluent than average, many have precarious financial circumstances and their buildings are not particularly profitable. Precarity increased, moreover, with the onset of COVID-19.

Landlords with nonpaying tenants might threaten those tenants with eviction, but the threat might be designed more to make the tenant pay than to make the tenant leave. Garboden and Rosen (2019) show that eviction threats are much more common than actual evictions, and use interviews with landlords in three markets to help explain why. Threatening eviction is a fast and low-cost way to make tenants prioritize their rent bills over other spending priorities. Eviction itself, in contrast, is often viewed by landlords as a costly and (in some markets) time-consuming process that does not guarantee any back rent and does guarantee the need to find a new tenant. For this reason, eviction is often a last resort, used only when other attempts to obtain back rent have been exhausted. Smaller landlords reported using a more ad hoc approach to decisions about threatening, filing, or executing an eviction, whereas larger landlords often had a more structured process. All landlords, however, wanted to minimize the frequency of eviction proceedings and maximize rent payment (Garboden & Rosen, 2019).

When landlords do consider removing tenants—as opposed to just threatening them with removal—they need to weigh the likelihood of quickly filling the vacated unit. Here the broader context of nonpayment, real or perceived, matters. A situation where almost every tenant pays but a few do not differs from one where many tenants across a region fall behind. This does not mean that evictions will be more common when the economy is strong—to the contrary, evictions generally rise during downturns (Desmond & Gershenson, 2017; Lens et al., 2020)—but it does suggest that if a recession is deep enough to make rents soften and vacancy rise, landlords might judge it better to wait for late payment, or negotiate a repayment plan, than to evict a current tenant and risk not finding a new one. The landlord’s judgment here will depend in part on his or her perception of how many other landlords have tenants who are not paying, and of what those landlords will do.5 But it may also depend on circumstances specific to the building: if a nonpaying tenant occupies a rent-stabilized unit whose current price is well below market rate, the returns to eviction (through vacancy decontrol) may be high even if the eviction results in months of vacancy.

Finally, racial animus or stereotype could influence decisions to evict. If landlords dislike or distrust racial minorities, or assume that other potential tenants (or landlords) do, they may react differentially to nonpayment, and be more likely to remove racial minorities who fall behind.6

If a downturn is broad enough, as it was during the COVID-19 emergency, governments might try to influence this decision process, both by expanding assistance to economically distressed people (and thus helping them make rent) and by affirmatively constraining landlords’ ability to evict. Governments did both during COVID-19. The federal Coronavirus Aid, Relief, and Economic Security (CARES) Act, passed in April 2020, delivered assistance checks to over 170 million U.S. households, and also expanded UI. Multiple levels of government, through courts, agencies, and legislatures, also enacted rules to slow or stop evictions (Duong, 2020; Hutson, 2020).

None of these eviction moratoria canceled or forgave rent, and none, to our knowledge, stopped landlords from initiating evictions (e.g., notifying tenants and filing paperwork with a court). Most did, however, delay the date when those evictions could be heard and acted upon.7 Landlords governed by these moratoria who wish to lawfully evict tenants must file an eviction and wait, during which time they collect no rent and risk having the tenant damage the unit. These landlords might be better served working out repayment plans (or, as discussed above, by threatening tenants with eviction but not actually initiating it). Some may decide, however, to unlawfully evict tenants. They could threaten eviction or serve tenants with papers and hope the tenants are unaware of moratoria and move out, or turn off utilities or otherwise harass occupants. Some journalistic evidence suggests that harassment rose markedly when COVID stay-at-home orders began (e.g., Dillon, 2020), and Reina et al. (2021), in a survey of tenants who applied for rental assistance in LA City and County, found that 15% reported being harassed by their landlords.

An additional point is that the efficacy of both eviction moratoria and renter assistance hinge on awareness of them, and this awareness may vary by landlord type. If larger, corporate landlords are more aware of both moratoria and assistance programs (because they are well resourced and have personnel who track legal and legislative action), and more sensitive to scrutiny of their actions, they may be less likely to threaten or initiate eviction and more likely to direct tenants to help. Smaller landlords, in contrast, might be more likely to threaten or initiate eviction in part because they are unaware of regulations prohibiting it and unaware of programs offering an alternative path to being paid.

In total, this reasoning suggests that not all tenants will be equally likely to miss payment. It further suggests that if tenants who do miss payment are not randomly distributed across buildings—and probably they are not, because tenants with higher and more stable incomes may be in newer or more expensive buildings—then not all landlords will be equally likely to have tenants in arrears. Tenants who do experience economic shocks can take some combination of the following options: pay late, less, or not at all; borrow money from others or their future selves (their savings); negotiate with their landlords, or move—presumably to someplace where rent will be lower.

Based on these options and the discussions above, we construct nine hypotheses:

Renters, all else being equal, will be more likely than owners to struggle with housing payments.

The primary factor in renters’ difficulty to pay will be lost income through losses in employment or hours.

Even controlling for lost work and earnings, nonwhite renters and lower income renters are more likely to report being unable to pay, probably owing to unobserved wealth constraints, less affluent social networks, and racial discrimination in access to credit.

Government income support will be associated with less nonpayment.

Even controlling for income and job loss, renters will be more likely to be late or miss payment if their landlord is a friend or family member, or a “mom-and-pop” landlord, owing to the higher likelihood of personal relationships.

Renters who lose work or income will take on other forms of debt to help pay the rent: they will deplete their savings, put rent on credit cards, or borrow from lenders or friends and family.

Controlling for nonpayment, smaller landlords will be more likely to threaten or initiate eviction, owing to greater reliance on any single tenant’s rent payments and/or their lower level of awareness about moratoria.

Controlling for nonpayment, landlords will be more likely to threaten nonwhite renters with eviction.

Landlords will be more likely to threaten or initiate eviction as renters fall further behind (with threats being more common than actual initiation).

Data and Methods

Some of the hypotheses above are straightforward (e.g., lost income predicts nonpayment) and some more ambiguous (e.g., small landlords will be more likely to evict). To date, however, few have been testable, because the data to test them have been lacking. Although the Home Mortgage Disclosure Act (HMDA) mandates careful collection of lending terms, mortgage payment, delinquency, and foreclosure for owner-occupied dwellings (e.g., Loya, 2022), no comparable data exist to measure payment and nonpayment of rent, or the relationship between nonpayment and eviction. Specifically, no data source regularly and comprehensively tracks American rental payment. The National Multifamily Housing Council (NMHC) collects data that are regular (monthly), but not comprehensive—the council’s survey concentrates on higher-end and professionally managed properties. Nationwide, only about 13% of rental properties are professionally managed (U.S. Census Bureau, 2018a),8 and higher-end and professionally managed buildings probably differ systematically from the rest of the stock.

Those caveats aside, the NMHC suggests that rental nonpayment pre-COVID was rare—by the end of a typical month in 2019, for example, 96–97% of tenants had paid—and that during the first year of COVID (2020) these figures fell by about a percentage point, whereas in the second year they fell an additional percentage point (NMHC Tracker, 2022).

The U.S. Census Bureau’s American Housing Survey (AHS) is more comprehensive than the NMHC (using a representative sample of U.S. housing units) but less regular (administered only every two years). Since 2013, the AHS has asked tenants about rent payment and delinquency in the previous three months. Like the NMHC, the AHS suggests that before COVID, rental nonpayment was rare. Nationwide in both 2013 and 2017, just over 93% of tenants paying cash rent reported paying in full in the previous three months. Between 3% and 4% reported missing or only partially paying rent in one of those months, whereas 1.5% reported missing or partially paying rent in two or more months. The AHS also asks about eviction, but unfortunately does not, in its public use file, link responses to that question to responses about rent delinquency. As such, we cannot know if an eviction threat was made to a delinquent tenant, or—if it was—if delinquency was the only or primary reason for the eviction. Nevertheless, in 2017 about 2% of all tenants reported receiving an eviction threat, and 20% of those threatened (0.4% of all tenant households) reported receiving a court-ordered eviction notice (U.S. Census Bureau, 2014, 2018b).

Our focus in this article is on Los Angeles, and the AHS does include a representative sample of tenants in the Los Angeles–Long Beach–Anaheim Metropolitan Statistical Area (MSA)—this geography is essentially Los Angeles and Orange Counties. The 2017 AHS suggests that pre-COVID, rental delinquency in the Los Angeles MSA was even less common than it was nationwide. Nearly 97% of LA tenants paying cash rent reported paying their rent in full in the past three months, with 2.4% reporting one month of missed or partial rent payment, and less than 1% of tenants being behind by two months. Almost no LA tenants reported being behind on three months of rent (U.S. Census Bureau, 2018b).9 Similar to the national data, 2% of all MSA tenants reported being threatened with eviction. We can treat these figures as baseline (pre-COVID) levels of nonpayment and (with some reservations) of eviction threats. We now turn to the COVID-era data sources that let us carry out our tests.

The Census Pulse Survey

In late April 2020, the U.S. Census Bureau began administering its Household Pulse Survey (HPS, or Pulse). In its first wave (12 weeks) the census administered the Pulse weekly, and subsequently made it biweekly and revised some of its questions, as we describe below.10 Unlike other census products, the Pulse was created and deployed rapidly, fielded frequently, had small sample sizes and did not achieve the high response rates common to Census surveys. For all these reasons the Census Bureau considers the Pulse experimental.11 The survey was designed and weighted to provide representative information at the person level for the United States overall, for each state, and for the nation’s 15 largest MSAs. The latter fact allows us to examine trends in the Los Angeles MSA (again, covering Los Angeles and Orange Counties). We use data from the first two waves. In Wave 1 of the Pulse, we focus on the following housing question:

Did you pay your last month’s rent or mortgage on time? Select only one answer.

[Yes/No/Payment was deferred]

We combine responses to this question with questions about lost work (“In the last seven days, did you do any work for pay or profit?”), lost income (“Have you, or has anyone in your household, experienced a loss of employment income since March 13, 2020?”), and questions asking about UI receipt, CARES stimulus payments, and whether the household had relied in the past seven days on unconventional forms of spending to meet its usual needs (e.g., relying more on credit cards, loans, or savings, or borrowing from family members).

In combination, these questions let us test three of our hypotheses: that renters will have more trouble paying than owners, that lost work and income will be the major drivers of renters’ inability to pay, and that UI or other government assistance can help alleviate that difficulty.12

The Wave 1 Pulse has some limitations. The largest, for our purposes, is that the rental question only asks if payment is late. Because rent can be paid late but nevertheless paid in part or full, responses to this question do not automatically indicate whether a household is in arrears.13

The survey thus provides evidence of difficulty paying, but does not tell us whether at month’s end the rent was paid in full, in part, or not at all.14 The survey also offers no information on the consequences of nonpayment or the renter’s larger housing context (e.g., what sort of unit the tenant lives in, the level of rent, or who the tenant rents from). It does not indicate if tenants are behind on multiple months of rent, because it has no cumulative nonpayment question similar to that in the AHS survey (e.g., “Were you late this month and the month before?”).15 A further issue is that the employment question only reveals whether a respondent was unemployed during the week of the survey, and does not reveal how long the unemployment spell has been. The income question, similarly, tells us whether a household lost income after March 13, 2020, but not how much income, or over what length of time. As such, the lost income question is likely to become less salient over time; during the Pulse’s first wave, an affirmative response would indicate recent income loss. By the second wave, an affirmative response might refer to income that was lost months before.

Subsequent waves of the Pulse addressed some of these limitations. Beginning with Wave 2, the Pulse did not ask if the current month’s rent was late, but instead asked: “Is this household currently caught up on rent [mortgage] payments?” Thus, the nature of the trouble paying changes (from being late in the current month to being behind overall). The latter Pulse waves also asked what type of unit the tenant lives in.16

The Los Angeles County Renter Survey

We complement the Pulse with our second data source: an original survey of Los Angeles County renter households that we designed, and that a survey firm (LRW Research) administered twice, first in July 2020 and second in March 2021. Each wave had about 45 questions, and each received 1,000 responses. Wave 1 was completed 79% online and 21% by telephone (both land-line and cellular). Wave 2 was 73% online and 27% by telephone. We built the survey quotas to demographically and economically match 2019 census ACS data (one-year estimates) for LA County renter households, along dimensions of race, age, gender, and income. Unlike the Pulse and AHS, we do not include Orange County, but this geographic difference is not as large as it may seem. LA County holds over 80% of the MSA’s renters, and almost 88% of its tenants whose household incomes are below $25,000 per year (U.S. Census ACS, 2019).

Geographically, we sought to have 40% of our respondents in the City of Los Angeles and 60% in the remainder of the county, omitting zip codes that were predominantly large group quarters, such as the premises of colleges, universities, and military bases. The Wave 1 survey was available in English, Spanish, and Mandarin, and Wave 2 in English and Spanish (because no Wave 1 respondents used the Mandarin option). We fielded each wave on the 6th of the month, one day after rent is typically due. We sought to close each wave by month’s end. We were able to do so with Wave 2, but in Wave 1 reaching the target sample of 1,000 respondents necessitated holding the survey open for three days in August (40 respondents completed the survey in those three days).17

Both survey waves asked about the prior three months of rent payment. Wave 1, for instance, asked if respondents paid rent in full, in part, and (if payment was made) on time in May, June, and July 2020. Wave 2 asked about January, February, and March 2021.18 To avoid any confusion, we named the relevant month when asking each question. The May question, for example, asks:

In talking to people about the current situation, we are finding that many people are having trouble paying rent this month. What about you? In May, has your household (a) Paid rent in full (b) Paid part of the rent, (c) Not paid rent at all?

Both survey waves asked how respondents usually paid rent before COVID-19, and if during the pandemic they were relying on different and unconventional payment sources (e.g., credit cards, savings, friends or family). For renters who paid partly or not at all in a given month, we ask if landlords have negotiated with them, threatened an eviction, or begun an eviction. (During the time period of our surveys, Los Angeles was covered by an eviction moratorium. Respondents reporting evictions may thus be reporting that papers were filed in court, to be acted on when the moratorium expired, or that landlords had said an eviction was filed, whether it was or not.) We also ask if landlords have responded to nonpayment by turning off utilities or refusing to perform needed maintenance.

In Wave 2, but not Wave 1, we additionally ask if tenants have missed any payments since the pandemic began in March 2020, and ask tenants to estimate the total amount of money they owe. Because of this change, in Wave 2 we also ask all tenants, and not just those who report being behind in the three months we focus on, if their landlords have threatened or started an eviction. We round both surveys out with a series of questions about demographics, lost employment and earnings, and characteristics of rental buildings, such as building size, rent, and management structure (e.g., corporations or individuals).19

Appendix Tables A1 and A2 examine the representativeness of our samples by comparing our completed surveys with our target quotas and other Census proportions. Briefly, in Wave 1 we undersampled male renters—particularly older, more affluent males—and Asian households. We met our Wave 1 quota of lower-income households, but we note that 50 respondents (5%) did not answer our income question. If nonresponse to income questions increases as income falls (and these 50 respondents did report lower than average rents and education levels, and were more likely to be Hispanic), then our Wave 1 sample might be moderately biased toward households of lower socioeconomic status.20 In Wave 2 we missed our low-income quota, but 22 respondents did not report their income, and these respondents likewise reported lower levels of education and rent, and were less likely to be White.

Compared to census ACS data, our samples overrepresent renters in single-family homes. About 28% of respondents in both samples report being in single-family homes; the 2019 ACS places the same figure for Los Angeles County closer to 21%. The Pulse, notably, also oversamples these renters: 31% of Pulse Wave 2 renters in the Los Angeles MSA are in single-family homes, whereas the ACS reports the figure as 21% (the same as the county). This overrepresentation of single-family homes might explain why rents in our survey are slightly higher than those in the county. The median asking rent was $1,417 in our Wave 1 sample and $1,600 in Wave 2. In the 2019 ACS it was $1,176 (in 2020 dollars).

We can also compare our responses about paying late to the Pulse. In our Wave 1 sample, the share of renters who paid late in any given month is about 16%, and in Wave 2 it was 17%. In Wave 1 of the Pulse, the share of renters late on the current month’s rent averages 15% across 12 weeks. In Wave 2 (where the question was slightly different) it averaged about 13%. Again, the geographies here differ, because the Pulse also includes Orange County whereas our survey does not, but (again) most of the MSA’s renters are in Los Angeles County.

Overall, our samples appear to be reasonably representative of county renters, with some discrepancies suggesting a bias toward lower-income households, and some (such as the prevalence of single-family homes) suggesting the opposite. A final potential bias involves differential response: struggling households may be less likely to agree to participate in surveys.

Policy Context

The different waves of the surveys we examine were fielded at different times during the pandemic, and as mentioned above, the amount of protection and assistance available to renters varied across these times. For the entirety of the period we study, tenants could not be legally evicted from their units due to nonpayment: they were protected by overlapping moratoria from local, state and national agencies. In the early months of the pandemic, which are covered by the first waves of both the Pulse and the LA County Renter Survey, the federal government offered direct assistance in two primary ways: cash stimulus payments through the CARES Act, and enhanced UI. The first CARES checks were deposited in bank accounts in mid-April, and the Pulse began asking about stimulus receipt after that time—meaning that the first few weeks of the Pulse contained no question about stimulus receipt. Enhanced unemployment, similarly, began flowing the week of April 10 (Luhby, 2020), although the rollout was slow, particularly in California where an overwhelmed state system was snarled by delays (Wire & McGreevy, 2021; also, UI was not available to undocumented workers). Thus, UI receipt, like the stimulus, is largely absent from the first weeks of the Wave 1 Pulse but present in subsequent weeks.

Crucially, the first wave of federal UI enhancements ended on August 1, and a second, less-generous round of UI enhancement ($300 rather than $600) did not begin until the early months of 2021 (Laponsie, 2020; Pinho, 2020). The second wave of the Pulse, then, occurred while UI was not boosted. The second wave of the LA County Renter Survey captured the second wave of enhanced UI, but the enhancement was smaller and some workers had by that point begun to exhaust benefits (Bell et al., 2021). We thus expect the impact of UI to be strongest earlier in the pandemic, and weakest midway through our study period, when the program was least generous.21

A final policy note is that considerable uncertainty hung over the entire study period. It was often unclear—to both tenants and landlords—how long the eviction moratoria would last, and how rental debt would ultimately be disposed of. Advocates on different sides of these discussions called for moratoria to end sooner or be made permanent, for rental debt (or rent) to be canceled entirely, and for different forms and magnitudes of direct rental assistance (e.g., Martinez, 2020; Weill-Greenberg, 2020). Many tenants may not have been aware of the moratoria: in the Wave 2 Pulse, for example, LA tenants who owed rent were asked if they feared eviction in the next two weeks, and over 40% said yes. Some of these tenants may have feared illegal eviction, or just feared an eviction threat, but the high proportion also suggests that many renters may have been unaware of the protections available. Appendix Figure A1 displays the overlapping timelines of our surveys, the Pulse survey, various eviction moratoria, and state and federal income supports.

Empirical Approach

Our surveys allow us, first, to descriptively estimate the prevalence of nonpayment at different points in the COVID-19 pandemic. From there we estimate a series of regressions. The dependent and independent variables differ based on the survey employed and the question addressed, but the basic model takes the following form:

where the dependent variable, Renter Distress, is a binary indicator of some form of housing trouble (we use “distress” as a broad term that can variously indicate being late on rent, behind on rent, drawing on savings or going into debt to pay rent, etc). The independent variables of interest are—again with differing emphasis depending on the model—whether the respondent lost income or lost work, the type of landlord, and whether the respondent received UI (or enhanced UI, if applicable). γt is a vector of respondent characteristics, including income, education, race and ethnicity, age, household size, and whether they reported contracting COVID-19. For Wave 1 of the Pulse, we estimate random effects panel logits, to account for the survey being a weakly balanced panel. The census administered the survey every week, usually asking different people the same questions each time, but sometimes (in about one third of cases) returning to previous respondents and surveying them again. We control for the week administered, as well as the influence of repeat respondents, by treating each respondent as a random effect, but attaching a fixed effect to each week. Subsequent Pulse waves were not panels. We present all output as odds ratios.

Results

In what follows we first present descriptive statistics from both the Pulse and the LA County Renter Survey. We then present regression results from the Pulse, which test our first four hypotheses, followed by regression results from the LA County Renter Survey, which let us test all nine of our hypotheses.

Descriptive Statistics

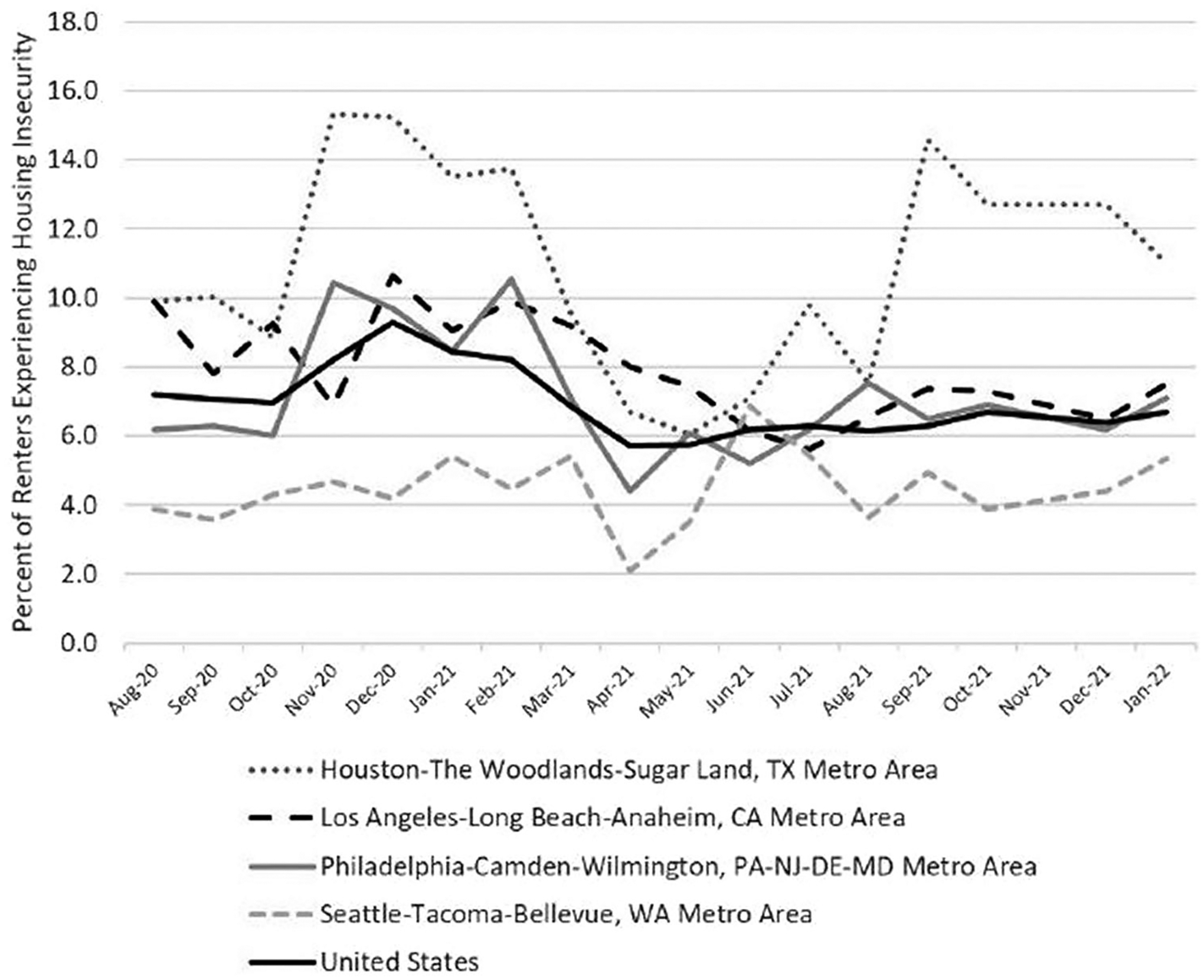

Our descriptive analysis begins by situating Los Angeles in the broader context of housing insecurity during the COVID-19 pandemic. Figure 1 uses Pulse data from August 2020 to January 2022 (weeks 13–42 of the survey) and compares housing insecurity trends in Los Angeles to trends in three other large MSAs (those with the highest, lowest, and median levels of distress) and the nation as a whole. In the figure, housing insecurity is defined as the share of households that are behind on rent or mortgage payments and have low confidence in their ability to make the next month’s payment.22 Although Los Angeles exhibited higher-than-average levels of such insecurity, it was not the MSA with the highest levels—Houston, Miami, New York, and Atlanta all exceeded it—and LA was not much higher than the overall U.S. average.

Figure 1.

Housing insecurity across metropolitan areas, August 2020–January 2022.

Source: U.S. Census Household Pulse Survey.

We now turn to lost work or income, and the nonpayment of rent. Table 1 shows, using data from our four surveys (Pulse Waves 1 and 2, and County Renter Survey Waves 1 and 2) that all these phenomena became more prevalent during the COVID-19 pandemic. Both waves of the Pulse show almost 40% of renter households reporting being involuntarily unemployed during the survey week. Reports of having lost income or work sometime during COVID are even more prevalent, at over 50% of all four samples. These results suggest large increases in unemployment: by way of comparison, the 2019 ACS showed an overall unemployment rate in Los Angeles MSA of about 3%.

Table 1.

Descriptive statistics on renter distress by data source.

| Variable | Pulse Wave 1 | Pulse Wave 2 | LA County Wave 1 | LA County Wave 2 |

|---|---|---|---|---|

| Unemployed | 40 | 38 | N/A | N/A |

| Lost job or income | 68 | 59 | 62 | 53 |

| Had COVID | a | 13 | 11 | 27 |

| Late on rent | 10 | 13 | 22 | 29 |

Note. Values in columns are percentages.

There was a low prevalence of COVID-19 in Pulse Wave 1, largely due to lack of testing. “Unemployed” in Pulse refers to being involuntarily unemployed during the week of the survey. “Lost job or income” means the household lost work or hours at some point during the pandemic. “Late on rent” in Pulse Wave 1 means the current month’s rent is late. In Pulse Wave 2 it refers to being behind on rent generally. In Waves 1 and 2 of the LA County Renter Survey it means respondents paid late at least once in the three previous months.

All four surveys also suggest that rent nonpayment rose dramatically during COVID-19. Recall that our baseline estimates of nonpayment in Los Angeles, from the 2017 AHS, suggested that only 3% of LA MSA tenants were not fully current on the previous three months of rent. Table 2 shows that across Wave 1 of the Pulse, the average share late on the current month’s rent was 10%, whereas in Wave 2 the share behind on rent was 13%.

Table 2.

Descriptive statistics on rent payment, borrowing, and landlord–tenant interactions. LA County Renter Survey.

| Variable | Survey Wave 1 (2020) | Survey Wave 2 (2021) |

|---|---|---|

| Did not pay rent at all in one of the three past months | 7 | 7 |

| Paid partial rent in one of the three past months | 16 | 31 |

| Paid rent late in one of the three past months | 21 | 29 |

| To pay rent, did the household use: | ||

| Credit card? | 12 | 26 |

| Pre-COVID baseline | 3 | 6 |

| Emergency or payday loan? | 13 | 21 |

| Savings? | 30 | 39 |

| Money borrowed from friends and family? | 21 | 29 |

| Did the households unable to pay rent on time or in full: | ||

| Discuss a repayment plan?a | 68 | 70 |

| Enter into a repayment plan?b | 75 | 79 |

| Experience reduction in services?a | 20 | 28 |

| Experience an eviction threat?a | 16 | 25 |

| Have an eviction initiated?a | 6 | 19 |

Note. “Reduction in services” means the landlord did not perform needed maintenance and/or shut off utilities.

Only asked of renters who paid late, partially or not at all in the previous three months.

Only asked of renters who had discussed a repayment plan.

The LA County Renter Survey tells a similar story. That survey asked more specific questions about when and whether households were able to pay rent, and did so in a manner more directly comparable to the prepandemic questions in the AHS. In Wave 1 of the County Renter Survey, 22% of households were unable to pay on time in one of the previous three months. In Wave 2 this figure was 29%.23

Table 2 breaks some of these numbers down further. The AHS showed that in 2017 only 1% of tenants in the LA MSA were two full months behind on rent, and that well under 1% were three months behind. Both waves of the LA County Renter survey suggest that during the pandemic these proportions spiked. Of the 22% of renters unable to pay on time in at least one month in Wave 1, about a quarter were able to pay in full by that month’s end, meaning about 17% of renters were unable to fully pay rent in at least one month. About 7% of renters were unable to pay at all in at least one month (although not shown in the table, 2% of renters had not paid any rent in any of the three months). In January, February, and March 2021, the share of tenants missing an entire month’s payment was still at 7%, but levels of partial and late payment had jumped to 31% and 29% of tenant households. By any measure we have compiled, then, nonpayment surged well above its prepandemic trend, and appeared to worsen as the pandemic went on.

Failure to pay rent on time and in full is the most direct indicator of renter distress. Table 2 also highlights a second indicator, however, which is tenants paying rent with funds other than earned income, by dipping into savings or borrowing.24 Both waves of the LA County Renter survey asked households how they paid their rent, both before and during COVID. In both waves of the survey, few tenants reported using a credit card prior to the shelter-in-place orders (3% in Wave 1, 6% in Wave 2). As COVID progressed, these proportions jumped. Overall, 12% of tenants in Wave 1 reported putting at least some rent on a credit card during the three months we asked about; in Wave 2 this figure was 26%. These figures suggest at least a fourfold increase in the use of credit cards to pay rent.25

Although not shown in the table, the use of credit cards was 3 times higher among tenants who reported paying late or not paying in full, and grew most rapidly among lower-income tenants. In Wave 1, for example, only 1.5% of the lowest income renters reported pre-COVID credit card payments, but by May of 2020 this proportion had more than quadrupled, to almost 7%.

Credit cards were the only form of borrowing for which we established a pre-COVID baseline, but not the only form of borrowing tenants resorted to during the pandemic. Table 2 also shows that tenant households turned to friends and family, dipped into their savings, and took out payday or emergency loans. Although again not shown in the table, the use of all these methods was more common amongst households late or behind in at least one month.26

At the same time, however, households current on rent were not immune to relying on unconventional sources of funds for rent. Over 10% of households current on rent reported needing help from friends or family in at least one month, and over 20% used their savings to pay. Smaller but still notable proportions relied on credit cards and emergency loans.

The final rows of Table 2 examine landlord responses to late or missed payments. Most tenants unable to pay rent, in part or in full, discuss or enter into repayment plans with their landlords. In Wave 1, about half of households who missed at least one full month of rent report discussing a repayment plan with their landlord, and about two thirds of households that discuss a plan enter into one. Repayment plans became only slightly more common in Wave 2.

Much smaller shares of tenants who had trouble paying report conflict with their landlords, but conflicts became more common in the survey’s second wave. In Wave 1, about 20% of tenants who had difficulty paying reported their landlord had ceased repairs or turned off utilities, and nearly 30% reported this in the second wave. Similarly, in Wave 1, 15% of tenants behind on rent reported being threatened with eviction, and about 6% reported an eviction being initiated against them. These numbers jumped to 25% and 19%, respectively, less than a year later.

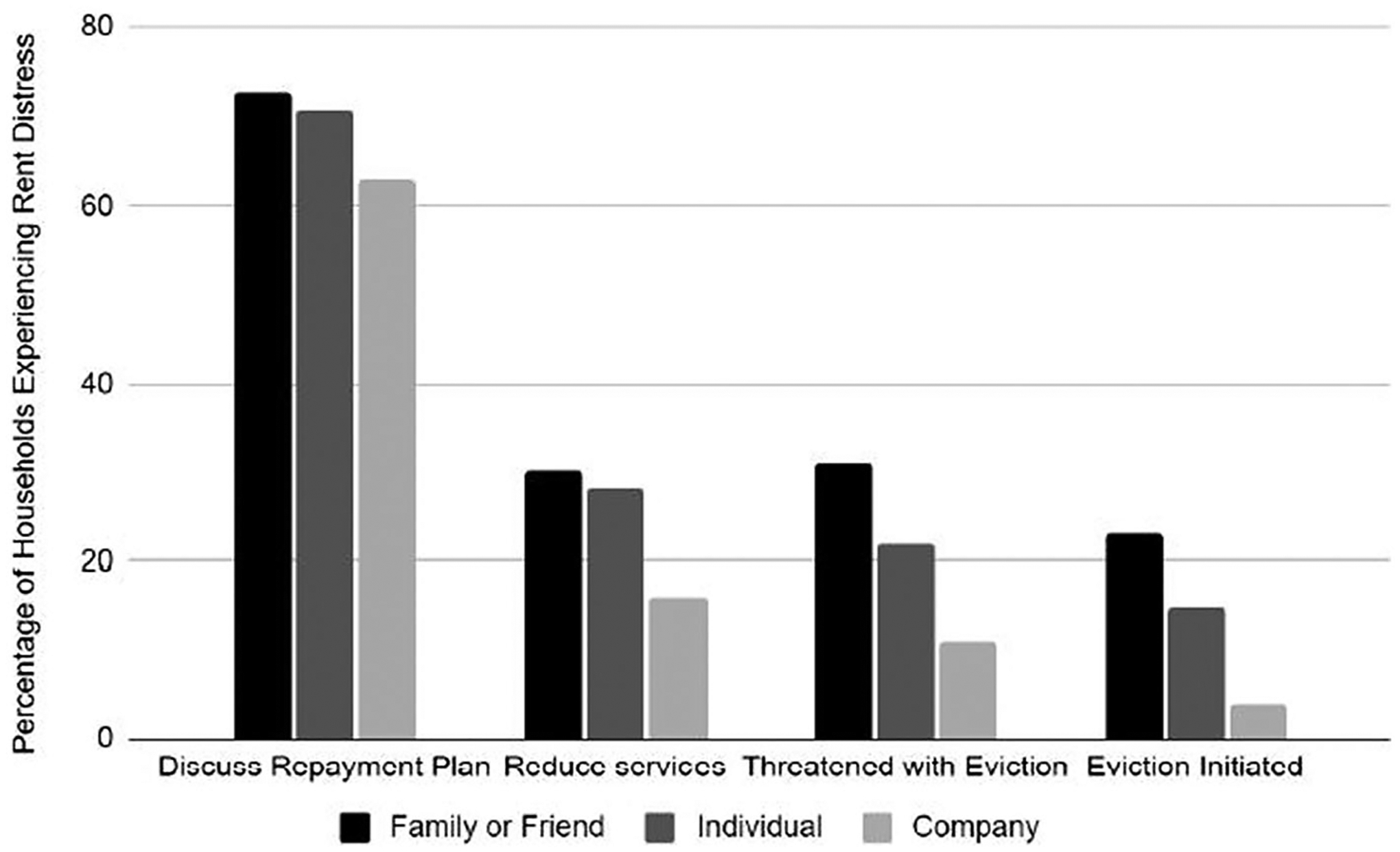

Figure 2 breaks down these landlord reactions by landlord type, and shows what appear to be significant differences. In short, almost all landlord reactions to late payment or nonpayment are more common among smaller landlords. Perhaps unsurprisingly, repayment plans are more common when the landlord is a family member or friend of the tenant (77%) than when the landlord is an individual or “mom-and-pop” landlord (68%) or a rental/management company landlord (68%). Controlling for nonpayment, plans are discussed more often with Black (76%) or Hispanic (75%) tenants than for White (64%) or Asian (43%) tenants (these proportions are not shown in the figure).

Figure 2.

Landlord actions by type of landlord.

Note. “Rent Distress”: Late payment, partial payment, or entirely missed one rent payment in the previous three months. “Reduce services”: Landlord did not make needed repairs, or turned off utilities. Source. Waves 1 and 2 (combined) of LA County Renter Survey.

Figure 2 also shows that nonpayment is most strongly associated with threatened or actually initiated evictions if the tenant rents from family members or friends, or from individual landlords. Between 22% and 31% of nonpaying tenants in these landlord arrangements report being threatened with eviction, compared to only 11% of nonpaying tenants who rent from rental or management companies. Similarly, rates of reported evictions being initiated are between 15% and 20% for smaller landlords, and 4% for larger rental firms.

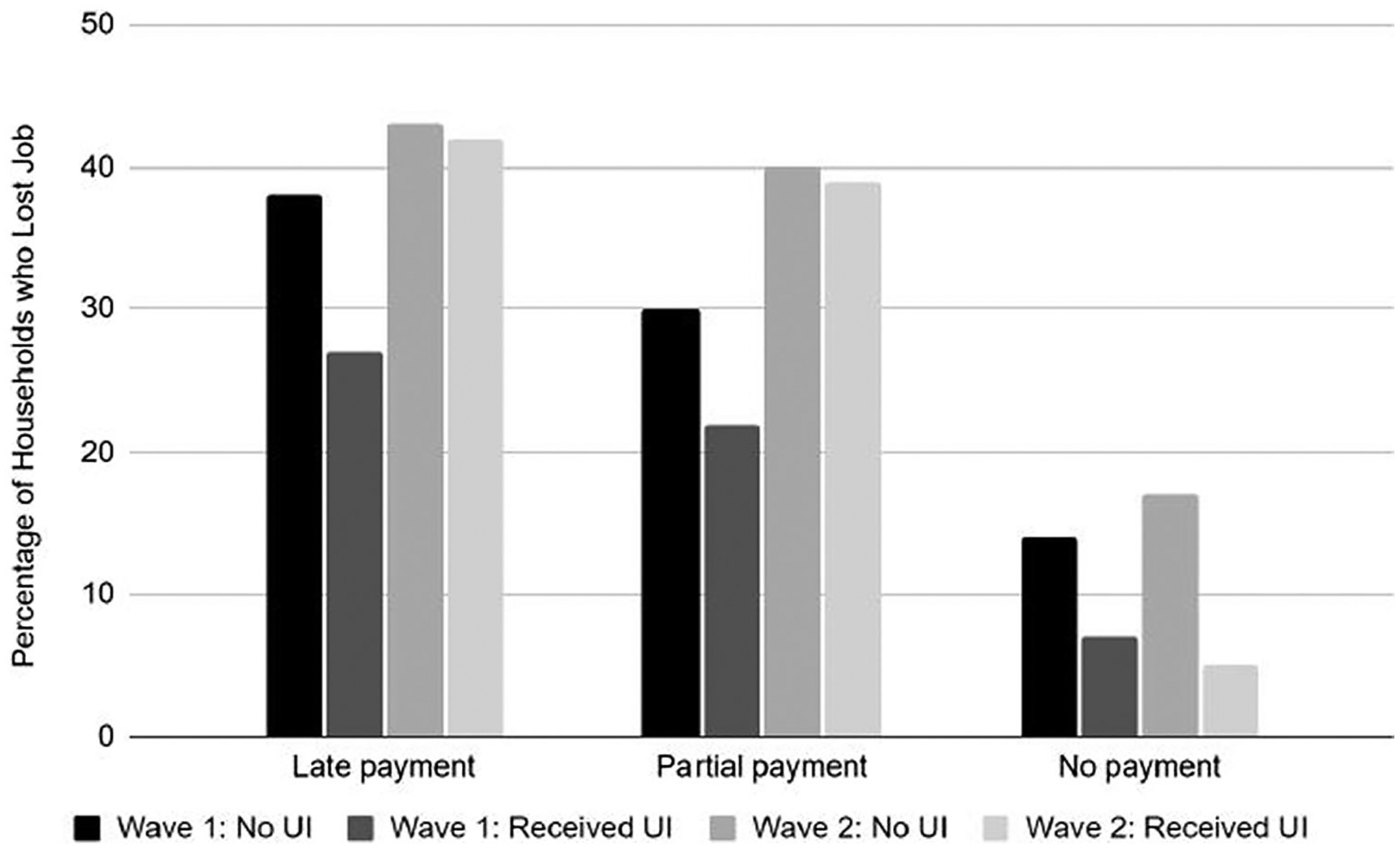

In Wave 1 of the LA County Renter Survey, 61% of households that lost work reported receiving unemployment benefits; the proportion in Wave 2 was 64% (Figure 3). In the first wave, households receiving benefits were more likely to pay rent in full and on time. Only 27% of households that lost work but received assistance paid late, compared to 38% who lost work but didn’t receive assistance. Similarly, 22% of households that lost work but received assistance paid partial rent, and 7% didn’t pay at all. In contrast, 30% of households that lost work but did not receive assistance paid partial rent, and 14%—double the share of households drawing benefits—didn’t pay at all.

Figure 3.

Renter distress and unemployment insurance (UI).

Source. Waves 1 and 2 of the LA County Renter Survey.

Figure 3 also shows, however, that the relationship between unemployment and renter distress changed notably between survey waves. In Wave 2, those who received UI had an almost identical rate of late or partial payment of rent compared to those who did not. However, they continued to default completely on rent at a much lower rate. In fact, in the second wave of the survey those who did not receive UI were more than 3 times as likely to not pay rent at all.

Finally, we might expect that nonpayment would be more common when tenants have closer personal relationships to their landlords. Our data bear this expectation out. Late payment and nonpayment are both more common among tenants who rent from friends and family. Such tenants comprised about 12% of our sample, but 25% of renters who missed at least part of their rent in one month. Conversely, tenants renting from management companies accounted for over 40% of our sample but less than 35% of households with late or missed payments. Tenants who rent from friends and family are, we should note, also lower-income than other tenants: almost 60% have household incomes below $50,000; for other tenants this figure is just under 50%.

Regression Results: Pulse Data

Tables 3 and 4 report regression results from the first two waves of the Pulse. The regressions are logits, with the results reported as odds ratios. Each table’s first model shows that renters, even controlling for lost income and a wide array of other factors, are more likely than owners to be delinquent on their housing payment (supporting our first hypothesis). Table 3 shows renters are 40% more likely than owners to be late on the current month’s housing payment, and Table 4 shows that they are 19% more likely to be so. Note that these figures likely underestimate the true gap between owners and renters, because both models omit the roughly 30% of homeowners who own their homes free and clear.

Table 3.

Associations with late housing payments, U.S. Census Pulse Wave 1.

| 1 | 2 | 3 | 4 | |

|---|---|---|---|---|

| Variables | Late payment (all HHs) | Late rent (renter HHs) | Late rent (lost work/income) | Late rent (lost work/income) |

| Renter | 1.406*** (0.001) |

|||

| Lost employment income | 3.508*** (0.004) |

4.154*** (0.006) |

||

| Currently unemployed | 1.346*** (0.001) |

1.486*** (0.001) |

||

| Unconventional spending | 3.666*** (0.008) |

3.682*** (0.008) |

||

| UI income | 0.255*** (0.000) |

0.268*** (0.001) |

||

| Stimulus aid | 0.810*** (0.001) |

|||

| Second income quartile | 1.170*** (0.001) |

1.097*** (0.001) |

1.106*** (0.001) |

1.202*** (0.002) |

| Third income quartile | 0.644*** (0.001) |

0.676*** (0.001) |

0.707*** (0.001) |

0.850*** (0.002) |

| Top income quartile | 0.285*** (0.000) |

0.266*** (0.001) |

0.252*** (0.001) |

0.115*** (0.001) |

| Female | 0.984*** (0.001) |

0.969*** (0.001) |

0.974*** (0.001) |

1.624*** (0.002) |

| Age 18–30 | 1.038*** (0.001) |

1.220*** (0.001) |

1.316*** (0.001) |

0.854*** (0.001) |

| Age 65 or older | 0.378*** (0.001) |

0.282*** (0.001) |

0.305*** (0.001) |

0.164*** (0.001) |

| Persons in household | 1.020*** (0.000) |

1.022*** (0.000) |

1.031*** (0.000) |

1.047*** (0.000) |

| Children in household | 1.056*** (0.000) |

1.071*** (0.000) |

1.052*** (0.001) |

1.012*** (0.001) |

| Black | 2.193*** (0.003) |

2.633*** (0.004) |

2.398*** (0.004) |

1.457*** (0.004) |

| Asian | 0.758*** (0.001) |

0.733*** (0.001) |

0.538*** (0.001) |

0.916*** (0.003) |

| Hispanic | 1.165*** (0.001) |

1.457*** (0.002) |

1.248*** (0.002) |

1.328*** (0.003) |

| No HS diploma | 1.007*** (0.001) |

1.049*** (0.001) |

0.968*** (0.001) |

0.859*** (0.001) |

| BA or higher | 0.499*** (0.001) |

0.432*** (0.001) |

0.394*** (0.001) |

0.543*** (0.001) |

| N | 17,197 | 8,994 | 5,717 | 3,092 |

| F | −2.89E + 07 | −1.96E + 07 | −1.73E + 07 | −8.03E + 06 |

Note. Data are from U.S. Census Pulse weeks 1–12 (models 1–2) and 8–12 (3–5). Coefficients are odds ratios. Regressions are random-effects logit models, with week fixed effects. Person-weighted. Rerunning regressions with replicate weights does not change the results. Model 1 includes all HHs except owners who have no mortgage. Model 2 includes all renter HHs; Models 3 and 4 include renter HHs who have lost work or income. “Unconventional Spending” means the respondent is relying on credit cards, loans, family, or savings to cover normal expenses. Standard errors in parentheses.

p < .05.

p < .01.

p < .001.

Table 4.

Associations with late housing payments, U.S. Census Pulse Wave 2.

| 1 | 2 | 3 | 4 | |

|---|---|---|---|---|

| Variables | In arrears (all HHs) | Owe rent (renter HHs) | Owe rent (renter HHs) | Owe rent (lost work/income) |

| Renter | 1.185*** (0.068) |

|||

| Lost employment income | 2.924*** (0.185) |

2.869*** (0.256) |

2.449*** (0.245) |

|

| Currently unemployed | 1.660*** (0.093) |

1.755*** (0.130) |

1.660*** (0.128) |

|

| Unconventional spending | 1 525*** (0.124) |

1.800*** (0.174) |

||

| Received UI | 0.826 (0.120) |

0.840 (0.124) |

||

| Applied for UI | 1.321* (0.193) |

1.479*** (0.221) |

||

| Second income quartile | 1.315*** (0.099) |

1.024 (0.093) |

1.005 (0.093) |

1.020 (0.105) |

| Third income quartile | 1.080 (0.076) |

0.778*** (0.073) |

0.768*** (0.073) |

0.739*** (0.079) |

| Fourth income quartile | 0.671*** (0.053) |

0.464*** (0.058) |

0.477*** (0.060) |

0.395*** (0.059) |

| Female | 0.902* (0.049) |

0.798*** (0.057) |

0.792*** (0.058) |

0.808*** (0.066) |

| Age 18–30 | 0.724*** (0.064) |

0.584*** (0.064) |

0.574*** (0.063) |

0.562*** (0.067) |

| Age 65+ | 0.793*** (0.069) |

0.872 (0.111) |

0.916 (0.119) |

0.775 (0.130) |

| Black | 1.818*** (0.199) |

1.726*** (0.237) |

1.803*** (0.250) |

1.680*** (0.263) |

| Asian | 2.465*** (0.182) |

2.166*** (0.231) |

2.153*** (0.233) |

1.417*** (0.185) |

| Latino | 1.596*** (0.108) |

1.611*** (0.144) |

1.647*** (0.149) |

1.404*** (0.141) |

| Persons in HH | 1.046** (0.022) |

1.058** (0.029) |

1.061** (0.030) |

1.060* (0.032) |

| Number of children in HH | 1.184** (0.081) |

1.244** (0.118) |

1.257** (0.120) |

1.228* (0.130) |

| BA or higher | 0.756*** (0.045) |

0.748*** (0.059) |

0.756*** (0.060) |

0.665*** (0.059) |

| No HS diploma | 1.389*** (0.175) |

1.168 (0.173) |

1.177 (0.178) |

1.294 (0.212) |

| Constant | 0.036*** (0.004) |

0.056*** (0.008) |

0.045*** (0.007) |

0.146*** (0.025) |

| No. of observations | 15,918 | 7,897 | 7,758 | 4,575 |

| No. of weeks | 13 | 13 | 13 | 13 |

Note. Data from U.S. Census Pulse weeks 13–26. Coefficients are odds ratios. Regressions are random-effects logit models, with week fixed effects. Weighted by person Model 1 includes all HHs except owners who have no mortgage. Models 2 and 3 include all renter HHs; Model 4 includes renter HHs who have lost work or income. “Unconventional Spending” means the respondent is relying on credit cards, loans, family, or savings to cover normal expenses. Standard errors in parentheses.

p < .05.

p < .01.

p < .001.

Because we have controlled for income, adverse economic shocks, and most demographics, these owner–renter differences likely reflect attributes of renters we cannot directly observe, such as lower levels of savings and less affluent friend-and-family networks. This finding reinforces the assertion we made in the article’s introduction: the literature’s relative lack of attention to rental nonpayment is incongruent with the relative vulnerability renters face.

The remaining columns in both tables examine renters alone. The dependent variable in these models is either late rent payment in the current month (Wave 1 of the Pulse) or being behind on rent generally (Wave 2).27 Some of these models examine all renters, while in others the sample is restricted to tenants who have lost work or income. This restriction shrinks the sample size substantially, but allows us to better isolate the associations between nonpayment and various forms of assistance that tenants might receive.

Examining all renters (Model 2 in the tables) suggests that lost employment income is by far the strongest predictor of delinquent rent payment (consistent with our second hypothesis). The odds of a tenant household with lost employment income being late on the current month’s rent are over 4 times the odds for a similar household that did not lose income (in Wave 1). Similarly, in Wave 2, tenant households that lost income have odds of being behind on rent almost 3 times as large as those of households that did not lose income (2.5 times once we control for unconventional spending and UI application and receipt). Being currently unemployed also strongly predicts delinquency, with the odds of being late on the current month’s rent being 49% higher (Wave 1) and behind on rent 75% higher (Wave 2).

Socioeconomic characteristics predict delinquency in smaller but mostly expected ways. Of note, lower income and educational attainment strongly predict delinquency, and Blacks and Latinos, even controlling for income, were more likely to report being late than Whites (lending support to our third hypothesis).28

In our regressions that restrict the sample to households that lost work or income (Models 3 and 4 in Table 3, and Model 4 in Table 4), our interest is primarily focused on three potential ways to compensate for that lost income. The first is unconventional spending, meaning the household reports relying more on credit cards, loans, savings, or borrowing from family and friends to cover their normal expenses (these may include rent, but are not restricted to rent). The second, which is only meaningful in Wave 1, is a stimulus payment from the federal CARES Act. The third is UI, which, as we have noted, was boosted substantially during Wave 1 of the Pulse but had fallen sharply when Wave 2 was administered.

In both Pulse waves, unconventional spending is strongly associated with rent delinquency. We do not consider this result causal. It is more likely that both borrowing and delinquency spring from the same underlying economic distress, and that this shared positive correlation outweighs any negative interaction between the two (e.g., people being able to put some of their rent on a credit card to stay current).

Direct assistance from the government, in contrast—in the form of stimulus and UI—in Wave 1 does appear to be protective.29 Table 3 suggests that among renters who lost work or income, receipt of a CARES stimulus check was associated with a 20% reduction in the odds of being late on the current month’s rent. The coefficients associated with UI receipt are stronger, and suggest a 75% reduction in the odds of paying rent late in the current month.

In Wave 2, the association between UI and rent payment all but vanishes.30 The sign remains negative, but the coefficients shrink and UI receipt is only statistically significant at the 10% level in one of three models. The Pulse thus lends only mixed support for our fourth hypothesis—that government support will be associated with reduced nonpayment. One potential explanation for this mixed result, again, is the much-diminished size of UI during Wave 2. A second potential explanation is that the Pulse captures the duration of neither pandemic-related unemployment nor pandemic-related UI. In Wave 1, the short duration of the pandemic to that point meant these were intrinsically correlated. By Wave 2, however, they may have diverged, and some respondents may have had (for example) 10 weeks of unemployment but only two weeks of UI.

Regression Results: Our Los Angeles Renter Survey

Turning now to the LA County Renter Survey, Table 5 reports results from five regressions that examine various forms of nonpayment. Recall that in both waves of this survey we asked about three forms of difficulty paying rent: paying late, paying in part, or not paying at all. These questions, compared to the Pulse, allow us to examine nonpayment in more detail, but the surveys also have smaller sample sizes than the Pulse, which will likely affect significance tests.

Table 5.

Associations with rent delinquency (odds ratios)—LA County Renter Survey.

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| Variables | Any distress (Wave 1) | Any distress (Wave 2) | Late payment | Partial payment | Nonpayment |

| Lost job | 4.233*** (0.908) |

2.272*** (0.500) |

2.097*** (0.461) |

1.699*** (0.293) |

2.927*** (0.712) |

| Lost work hours or income | 1.926*** (0.451) |

1.634** (0.354) |

2.030*** (0.465) |

1.089 (0.204) |

1.654* (0.466) |

| Has had COVID-19 | 1.748** (0.417) |

1.419** (0.250) |

1.089 (0.217) |

1.305* (0.196) |

1.315 (0.298) |

| Receives unemployment insurance | 0.683* (0.134) |

0.928 (0.193) |

0.891 (0.171) |

1.139 (0.179) |

0.495*** (0.114) |

| Landlord type: Individual | 0.999 (0.177) |

1.387* (0.245) |

1.275 (0.232) |

1.271 (0.188) |

0.949 (0.203) |

| Landlord type: Family or friend | 2.642*** (0.675) |

1.905*** (0.443) |

1.255 (0.313) |

2.282*** (0.427) |

1.162 (0.327) |

| Rent (thousands of US$) | 1.031 (0.117) |

1.078 (0.108) |

0.983 (0.110) |

1.077 (0.0841) |

1.017 (0.130) |

| Moved in last year | 0.983 (0.157) |

2.015*** (0.315) |

0.669** (0.109) |

1.951*** (0.247) |

1.239 (0.236) |

| Single-family home | 1.140 (0.222) |

0.536*** (0.094) |

0.902 (0.176) |

0.710** (0.101) |

1.139 (0.246) |

| Multifamily home (10+ units) | 0.999 (0.192) |

0.307*** (0.063) |

1.146 (0.225) |

0.410*** (0.071) |

0.699 (0.172) |

| Black | 1.847** (0.465) |

1.545* (0.398) |

1.545* (0.380) |

1.400 (0.288) |

1.287 (0.378) |

| Asian | 0.575* (0.172) |

0.968 (0.246) |

0.509** (0.171) |

1.320 (0.273) |

0.298** (0.145) |

| Hispanic | 1.071 (0.211) |

0.810 (0.160) |

1.025 (0.209) |

1.005 (0.164) |

0.875 (0.204) |

| Over 65 years old | 0.776 (0.200) |

0.539** (0.139) |

0.782 (0.204) |

0.714 (0.163) |

0.810 (0.248) |

| Household size | 1.100 (0.069) |

1.283*** (0.087) |

1.071 (0.069) |

1.212*** (0.059) |

1.020 (0.078) |

| Any children in household | 1.499** (0.303) |

0.748 (0.139) |

1.127 (0.221) |

1.071 (0.158) |

0.912 (0.214) |

| Female | 1.252 (0.193) |

1.012 (0.152) |

1.167 (0.180) |

0.929 (0.114) |

1.418* (0.263) |

| No high school diploma | 0.644* (0.167) |

1.212 (0.291) |

0.847 (0.211) |

0.920 (0.188) |

1.146 (0.314) |

| BA or more education | 0.787 (0.141) |

0.781 (0.133) |

0.840 (0.155) |

0.773* (0.108) |

0.966 (0.213) |

| Married | 0.857 (0.142) |

0.558*** (0.094) |

1.070 (0.194) |

0.744* (0.115) |

1.032 (0.222) |

| Income < $25,000 | 1.332 (0.254) |

1.385* (0.271) |

1.007 (0.186) |

1.081 (0.171) |

1.493* (0.313) |

| Household income > $100,000 | 0.546** (0.138) |

1.297 (0.261) |

0.454*** (0.122) |

1.661*** (0.264) |

0.494** (0.159) |

| Received CARES stimulus check | 0.716* (0.123) |

||||

| Lives outside City of Los Angeles | 0.942 (0.154) |

0.861 (0.131) |

1.130 (0.181) |

0.702*** (0.087) |

1.229 (0.235) |

| Wave 2 of survey | 0.968 (0.162) |

1.845*** (0.250) |

1.069 (0.211) |

||

| Constant | 0.170*** (0.065) |

0.288*** (0.109) |

0.0603*** (0.023) |

0.0627*** (0.019) |

0.0341*** (0.015) |

| Pseudo R2 | 0.15 | 0.18 | 0.05 | 0.16 | 0.06 |

| No. observations | 1,000 | 1,000 | 2,000 | 2,000 | 2,000 |

Note. Standard errors in parentheses, “Any distress” includes households that have paid late, partially, or not at all. Models 3–5 combine both waves of the survey.

p < .1.

p < .05.

p < .01.

Our regression approach is as follows: The first two columns of Table 5 examine each wave, and analyze a dependent variable coded 1 if a respondent reported any form of renter distress (late, partial, or entirely missed payment) in any of the three months and 0 otherwise. The next three columns combine the two surveys (and add a survey-specific fixed effect) and examine the different forms of distress separately.

Our results are largely consistent with those from the Pulse. Losing work or income powerfully predicts renter distress (supporting hypothesis 2).31 The odds of renter distress for a household that lost work are from roughly 2 to over 4 times as high as the odds for tenant households that did not lose work, depending on the form of renter distress. The odds for tenant households that lost work or income, similarly, are between 1.5 and two times as high. Households with someone who contracted COVID-19 were substantially more likely to report renter distress in both waves of our survey.

One unexpected finding involves income. In general, lower-income households are at high risk for nonpayment. In our Wave 2 survey, however, high-income households are significantly more likely to pay only partial rent, although they are less likely to pay late or not at all. This finding might be noise, but it may also reflect some moral hazard generated by state renter assistance programs. Knowing that the state government was debating ways to pay renter debt to landlords, households confident in their ability to pay, or to find new housing if necessary, may have strategically deferred some payment.

Similar to the Pulse, the LA County regressions show Black tenants to be at greater risk for nonpayment, but unlike the Pulse the results for Hispanic tenants are noisy and nonsignificant. This result may owe to a smaller sample size, or to the LA County Renter Survey having more detailed controls than the Pulse. Whatever the reason, the LA County Renter Survey thus provides only mixed support for hypothesis 3.

The regressions also show that as hypothesized (hypothesis 5), nonpayment is more common among tenants who rent from family and friends.32 The coefficient associated with this landlord type is always positive and is statistically significant in three of the five models, suggesting that the odds of tenants with these landlords reporting some form of nonpayment are 1.8 to 2.5 times as high as those of tenants who report renting from a corporate landlord. Variables measuring the size of the rental building, as opposed to its management structure, do not yield consistent results.

Finally, these models do suggest that UI helped. In Wave 1 (when, again, UI was most generous) tenants who received it had odds of renter distress that were 31% lower than those of tenants who did not. UI was not significant in three other models, including the model for Wave 2 (when it was less generous) and in combined-wave models that examine late or partial payment. In the combined model that examines missing rent completely, however, UI is strongly negative. This model suggests that the odds of missing an entire month’s payment were 50% lower for households receiving UI. A majority of households (70%) reported receiving stimulus checks through the federal CARES act, and these households were 30% less likely to experience problems making rent. Thus, the LA County Renter Survey, like the Pulse, offers strong but not entirely consistent support for hypothesis 4.

Table 6 examines renter responses from another angle: the associations with tenant borrowing and the amount of accrued rent debt. We estimate three regressions: a logit regression where the dependent variable is coded 1 if the respondent resorted to any form of borrowing (including dipping into savings) to cover rent, and 0 otherwise, and two Ordinary Least Squares (OLS) regressions that estimate how much back rent a tenant owes—one measured in months and the other in dollars (these latter regressions use only Wave 2 of the survey). In short, lost work and hours strongly predict borrowing, and also predict owing more back rent, albeit with slightly less consistency. Higher rents, larger households, and renting from a family member or friend also predict tenant debt. These results are largely consistent with our hypothesis 6. The latter two regressions in Table 6, which examine rental arrears, reinforce our findings above: lost work and lost income predict more trouble paying. We consider this additional support for our hypothesis 2.

Table 6.

Associations with paying rent borrowed money and with lost work—LA County Renters Survey.

| 1 | 2 | 3 | |

|---|---|---|---|

| Variables | Any borrowing (odds ratios) | Back rent owed (months) (OLS coefficients) | Back rent owed (US$) (OLS coefficients) |

| Lost job | 2.612*** (0.371) |

0.556** (0.279) |

393 (477) |

| Lost work hours or income | 1.590*** (0.225) |

0.160 (0.300) |

−511 (513) |

| Has had COVID-19 | 1.731*** (0.238) |

0.390* (0.217) |

−742** (371) |

| Receives UI | 0.990 (0.138) |

−0.132 (0.250) |

−160 (427) |

| Landlord type: Individual | 0.954 (0.109) |

−0.0673 (0.249) |

−615 (426) |

| Landlord type: Family or friend | 1.823*** (0.309) |

0.886*** (0.298) |

−649 (510) |

| Rent (thousands of US$) | 1.236*** (0.087) |

0.377*** (0.127) |

878*** (218) |

| Moved in last year | 1.545*** (0.160) |

0.478** (0.204) |

−363 (349) |

| Single-family home | 0.642*** (0.080) |

−0.690*** (0.230) |

−785** (393) |

| Multifamily home 10+ units | 0.642*** (0.081) |

−0.800*** (0.293) |

−291 (502) |

| Black | 0.828 (0.140) |

−0.060 (0.323) |

−251 (552) |

| Asian | 0.935 (0.156) |

−0.818** (0.333) |

−776 (570) |

| Hispanic | 0.823 (0.106) |

−1.566*** (0.266) |

−1,972*** (456) |

| Over 65 years old | 0.525*** (0.085) |

0.358 (0.374) |

363 (641) |

| Household size | 1.152*** (0.051) |

0.162* (0.086) |

273* (148) |

| Any children in household | 1.065 (0.139) |

−0.065 (0.234) |

−202 (399) |

| Female | 0.899 (0.089) |

−0.340* (0.199) |

−133 (341) |

| No high school diploma | 0.700** (0.118) |

0.339 (0.323) |

1,285** (552) |

| BA or more education | 0.811* (0.093) |

−0.385* (0.228) |

−279 (390) |

| Married | 0.594*** (0.068) |

−0.0476 (0.237) |

−931** (405) |

| Low income | 1.094 (0.141) |

−0.249 (0.265) |

−1,301*** (454) |

| High income | 0.775* (0.109) |

0.392 (0.255) |

−30 (437) |

| Lives outside City of Los Angeles | 0.690*** (0.071) |

−0.582*** (0.196) |

957*** (335) |

| Constant | 0.620** (0.142) |

3.411*** (0.536) |

3,028*** (917) |

| Pseudo R2 | 0.12 | 0.31 | 0.19 |

| No. observations | 2,000 | 489 | 489 |

Note. Standard errors in parentheses. “Any borrowing” means the respondent used a credit card, payday loan, savings, or loan from family or friend to pay rent. Model 1 sample is both survey waves; Models 2 and 3 are restricted to Wave 2 respondents owing back rent. “Low income” refers to household annual income of less than $25,000. “High income” refers to household annual income of more than $100,000.

p < .1.

p < .05.

p < .01.

Tables 7 and 8 present regressions that analyze landlord response, allowing us to test hypotheses 7–9. We use two sets of regressions because, as discussed above, our survey asks about eviction in two different ways. In Wave 1, when the county was still in the early stages of the pandemic, questions about landlord reactions were only asked of people who reported being behind in one of the previous three months. When we fielded Wave 2, however, in addition to asking about the previous three months we asked respondents if they had fallen behind at all, and as such also asked all respondents—not just those delinquent in the previous three months—if their landlords had threatened or initiated an eviction, or denied repairs or turned off utilities.

Table 7.

Landlord response to distress (odds ratios)—LA County Renter Survey.

| 1 | 2 | 3 | 4 | |

|---|---|---|---|---|

| Repayment plan | Reduced services | Threatened to evict | Initiated eviction | |

| Entered into repayment plan | 2.102** (0.682) |

1.271 (0.394) |

1.316 (0.493) |

|

| Months of late payment | 1.069 (0.326) |

0.555** (0.156) |

1.192 (0.342) |

0.775 (0.248) |

| Months of partial payment | 2.163 (1.335) |

4.351** (2.569) |

1.559 (0.984) |

5.304* (5.309) |

| Months of nonpayment | 1.743 (0.997) |

1.483 (0.716) |

0.887 (0.489) |

0.571 (0.397) |

| Lost job | 1.420 (0.550) |

2.242** (0.841) |

1.676 (0.630) |

1.934 (0.856) |

| Lost work hours or income | 0.560 (0.223) |

1.214 (0.504) |

0.703 (0.295) |

0.700 (0.359) |

| Received unemployment insurance | 1.274 (0.405) |

1.197 (0.362) |

1.387 (0.428) |

1.503 (0.543) |

| Landlord type: Individual | 0.866 (0.307) |

1.698 (0.580) |

1.855* (0.667) |

2.383* (1.081) |

| Landlord type: Family or friend | 0.797 (0.319) |

2.341** (0.896) |

3.456*** (1.386) |

3.932*** (1.963) |

| Rent (thousands of US$) | 1.062 (0.168) |

1.165 (0.167) |

1.113 (0.158) |

1.256 (0.199) |

| Moved in last year | 0.990 (0.276) |

1.133 (0.295) |

1.177 (0.313) |

1.187 (0.365) |

| Single-family home | 1.112 (0.343) |

0.826 (0.236) |

0.908 (0.264) |

0.997 (0.332) |

| Multifamily home with 10+ units | 0.772 (0.307) |

0.910 (0.372) |

1.503 (0.632) |

1.072 (0.559) |

| Black | 1.504 (0.609) |

0.669 (0.256) |

0.666 (0.251) |

0.570 (0.254) |

| Asian | 1.843 (0.928) |

1.184 (0.489) |

0.779 (0.321) |

1.068 (0.480) |

| Hispanic | 1.327 (0.451) |

0.754 (0.248) |

0.353*** (0.118) |

0.418** (0.166) |

| Over 65 years old | 6.117** (4.964) |

0.856 (0.485) |

0.501 (0.303) |

0.226* (0.195) |

| Household size | 0.927 (0.098) |

0.874 (0.091) |

1.155 (0.119) |

1.227* (0.148) |

| Children in household | 1.303 (0.419) |

1.365 (0.413) |

0.572* (0.174) |

0.689 (0.240) |

| Female | 1.564 (0.426) |

0.964 (0.252) |

0.649 (0.173) |

0.847 (0.267) |

| Education: No high school | 1.208 (0.550) |

0.449 (0.231) |

1.119 (0.524) |

1.665 (0.907) |

| Education: BA or more | 1.115 (0.338) |

1.086 (0.290) |

1.153 (0.316) |

1.473 (0.464) |

| Married | 0.673 (0.221) |

0.782 (0.255) |

1.557 (0.506) |

0.897 (0.361) |

| Income < $25,000 | 0.494** (0.159) |

2.258** (0.757) |

0.899 (0.314) |

1.053 (0.455) |

| Household income > $100,000 | 1.686 (0.655) |

1.618 (0.524) |

1.032 (0.337) |

1.009 (0.369) |

| Lives outside City of Los Angeles | 1.544 (0.409) |

0.850 (0.213) |

0.548** (0.140) |

0.606* (0.180) |

| Wave 2 of survey | 1.008 (0.312) |

1.620 (0.486) |

2.320*** (0.724) |

2.751*** (1.079) |

| Constant | 0.765 (0.719) |

0.021*** (0.021) |

0.075*** (0.074) |

0.004*** (0.006) |

| Pseudo R2 | 0.09 | 0.13 | 0.17 | 0.23 |

| No. observations | 394 | 394 | 394 | 394 |

Note. Standard errors in parentheses. The sample is restricted to households that reported distress (i.e., late payment, partial payment or nonpayment). “Reduced Services” means the landlord reduced maintenance or cut off utilities.

p < .1.

p < .05.

p < .01.

Table 8.

Associations with eviction threats (odds ratios)—LA County Renter Survey.

| Threat of eviction | Eviction initiated | Reduced services | ||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | |

| Months behind in rent | 1.408*** (0.0908) |

1.400*** (0.0961) |

1.148** (0.0747) |

|||

| Back rent (log of US$) | 1.610*** (0.227) |

1.683*** (0.282) |

1.539** (0.265) |

|||

| Landlord: Family or friend | 1.957 (0.829) |

2.586** (1.055) |

2.460* (1.215) |

3.148** (1.503) |

0.681 (0.304) |

0.802 (0.361) |

| Small landlord | 1.301 (0.494) |

1.357 (0.500) |

1.642 (0.756) |

1.673 (0.746) |

0.741 (0.281) |

0.751 (0.285) |

| Speaks English poorly | 0.756 (0.433) |

0.545 (0.313) |

0.911 (0.598) |

0.638 (0.421) |

0.153** (0.127) |

0.125** (0.106) |

| Sick with COVID | 3.338*** (0.916) |

4.103*** (1.104) |

2.715*** (0.800) |

3.501*** (1.014) |

2.881*** (0.837) |

3.361 *** (0.998) |

| Black | 0.611 (0.256) |

0.710 (0.283) |

0.397** (0.179) |

0.490* (0.211) |

0.612 (0.267) |

0.626 (0.274) |

| Hispanic | 0.456** (0.169) |

0.406** (0.147) |

0.383** (0.157) |

0.367** (0.147) |

0.800 (0.311) |

0.900 (0.358) |

| Asian | 0.642 (0.270) |