Abstract

This cross-sectional study examines trends in US prescription fills for semaglutide products by payment method between January 2021 and December 2023.

Introduction

Semaglutide was first approved under the brand name Ozempic (Novo Nordisk) as a weekly injection by the US Food and Drug Administration (FDA) in 2017 and is a first-line treatment for patients with type 2 diabetes at high cardiovascular risk.1 Alongside evidence of semaglutide’s cardiovascular and weight loss benefits,2 the FDA approved Rybelsus (Novo Nordisk), an oral formulation for the treatment of type 2 diabetes, in 2019, and Wegovy (Novo Nordisk), another injectable formulation for obesity, in June 2021.1 Increased awareness of semaglutide’s weight loss benefits has fueled demand, including for off-label use, contributing to shortages for Ozempic and Wegovy since March 2022.3 Semaglutide’s limited supply and insurance coverage, including coverage prohibitions for weight loss drugs in Medicare Part D and coverage restrictions (prior authorization, nonpreferred status, or step therapy) in many state Medicaid plans,4,5 may contribute to barriers and disparities in accessing semaglutide due to its high out-of-pocket costs.6 In this cross-sectional study, we analyze trends in prescriptions dispensed at retail pharmacies for semaglutide between January 2021 and December 2023.

Methods

We used data from IQVIA’s National Prescription Audit PayerTrak, which captures 92% of prescriptions filled and dispensed to individuals at retail pharmacies in the US. We calculated monthly fills for semaglutide by drug brand (Ozempic, Wegovy, and Rybelsus) and payment method (commercial insurance, Medicaid, Medicare Part D, and cash) between January 2021 and December 2023. This study was exempted and informed consent was waived because it is not considered human participants research by the University of Southern California institutional review board. The study followed the STROBE reporting guideline.

Analyses were conducted using Stata, version 17.0 (StataCorp, LLC). A 2-sided P < .05 was considered significant.

Results

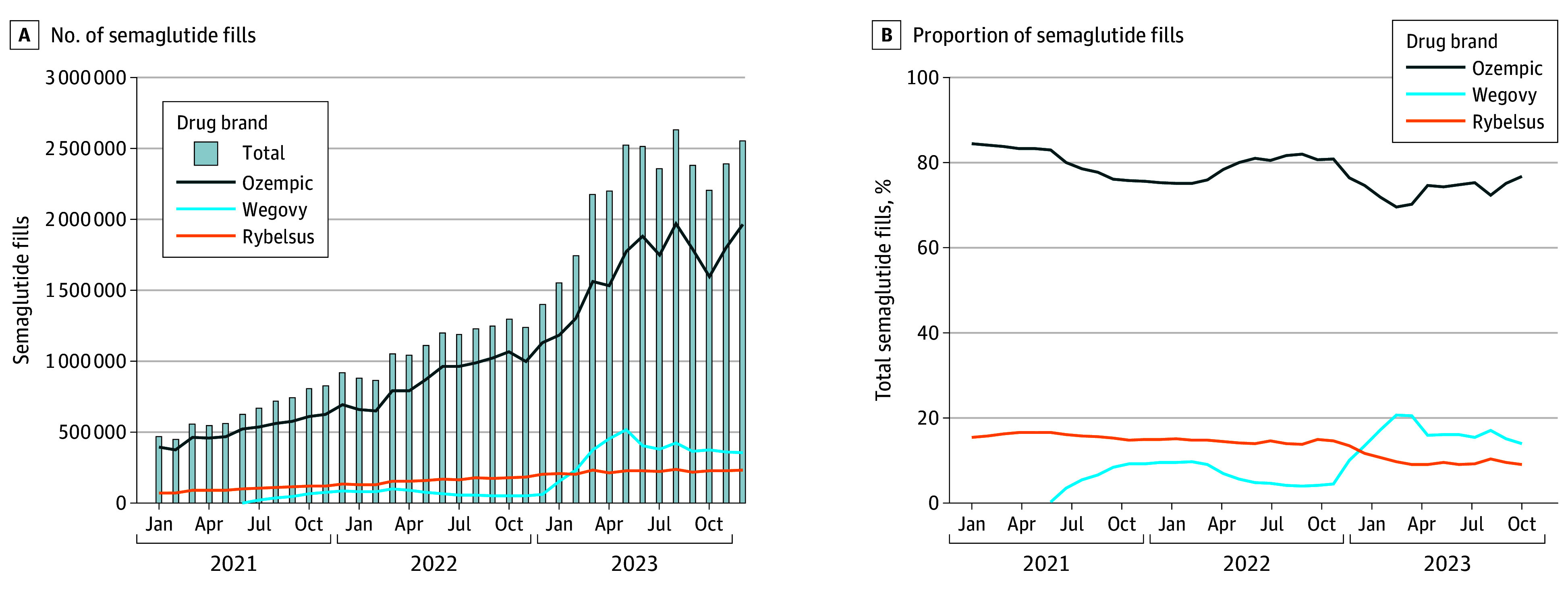

The number of semaglutide fills increased by 442% between January 2021 and December 2023 (from 471 876 to 2 555 308), with Ozempic accounting for over 70% or more of semaglutide fills during this period (Figure). Although increases were observed for all 3 drug brands, the extent and timing of these increases varied. For example, Ozempic peaked in August 2023 (1 968 892 fills) before reaching a plateau, increasing by 392% between January 2021 and December 2023. Notable increases in Wegovy fills started in January 2023 (157 554 fills), peaked in May 2023 (519 510 fills), and subsequently plateaued, increasing by more than 1361% between July 2021 and December 2023.

Figure. Trends in Semaglutide Prescription Fills by Drug Brand Between January 2021 and December 2023.

These data are from IQVIA’s National Prescription Audit PayerTrak on monthly prescription fills dispensed at retail pharmacies in the US.

Increases in monthly semaglutide fills were observed across all payment methods for all 3 drug brands between 2021 and 2023 (Table). However, semaglutide prescriptions paid through commercial insurance persistently accounted for most fills for all 3 drug brands, particularly for Wegovy.

Table. Changes in Semaglutide Prescriptions Filled by Drug Brand and Method of Payment Between January 2021 and December 2023a.

| Characteristic | Fills by method of payment | |||||||

|---|---|---|---|---|---|---|---|---|

| No. of monthly fills, mean (SD) | Proportion of monthly fills, mean (IQR) | |||||||

| 2021 | 2022 | 2023 | P valueb | 2021 | 2022 | 2023 | P valueb | |

| All semaglutide fills | 659 492 (147 800) | 1 148 123 (161 532) | 2 270 564 (326 866) | <.001 | NA | NA | NA | NA |

| Ozempic | ||||||||

| Total | 526 289 (95 463) | 909 927 (154 356) | 1 676 258 (246 594) | <.001 | NA | NA | NA | NA |

| Commercial | 346 850 (66 124) | 598 503 (104 237) | 1 027 892 (143 899) | <.001 | 65.8 (65.2-66.3) | 65.7 (65.2-66.2) | 61.4 (60.7-62.2) | <.001 |

| Medicaid | 40 096 (6371) | 75 385 (15 834) | 163 142 (26 309) | <.001 | 7.6 (7.5-7.9) | 8.2 (7.9-8.6) | 9.7 (9.5-10.0) | <.001 |

| Medicare Part D | 138 327 (22 854) | 233 028 (33 529) | 478 492 (78 055) | <.001 | 26.4 (26.0-26.7) | 25.7 (25.2-26.4) | 28.5 (27.8-29.3) | <.001 |

| Cash | 1017 (195) | 3011 (1255) | 6732 (292) | <.001 | 0.2 (0.2-0.2) | 0.3 (0.2-0.4) | 0.4 (0.4-0.4) | <.001 |

| Wegovy | ||||||||

| Total | 49 599 (30 209) | 70 958 (17 777) | 368 686 (94 174) | <.001 | NA | NA | NA | NA |

| Commercial | 43 501 (27 411) | 65 761 (16 149) | 329 340 (82 461) | <.001 | 86.0 (83.8-89.4) | 92.8 (92.4-93.4) | 89.5 (89.1-89.7) | .03 |

| Medicaid | 363 (351) | 2483 (649) | 30 797 (9721) | <.001 | 0.6 (0.3-0.9) | 3.6 (3.4-4.2) | 8.2 (8.2-8.5) | <.001 |

| Medicare Part D | 324 (187) | 700 (151) | 4438 (1785) | <.001 | 0.8 (0.6-0.7) | 1.0 (0.9-1.1) | 1.2 (0.9-1.5) | .02 |

| Cash | 5410 (2583) | 2014 (1593) | 4112 (689) | .24 | 12.7 (9.0-15.2) | 2.6 (1.6-3.1) | 1.2 (1.0-1.2) | <.001 |

| Rybelsus | ||||||||

| Total | 104 270 (20 656) | 167 238 (21 206) | 225 620 (10 501) | <.001 | NA | NA | NA | NA |

| Commercial | 73 242 (12 415) | 106 716 (12 283) | 130 991 (5390) | <.001 | 70.7 (68.7-72.2) | 63.9 (63.1-64.5) | 58.1 (57.6-58.4) | <.001 |

| Medicaid | 4696 (1557) | 12 544 (2856) | 19 687 (835) | <.001 | 4.4 (3.9-5.0) | 7.4 (6.9-8.1) | 8.7 (8.6-9.0) | <.001 |

| Medicare Part D | 25 952 (6926) | 47 715 (6103) | 74 311 (4683) | <.001 | 24.5 (23.4-26.2) | 28.5 (28.3-28.7) | 32.9 (32.4-33.6) | <.001 |

| Cash | 380 (226) | 263 (42) | 631 (220) | .01 | 0.4 (0.2-0.6) | 0.2 (0.1-0.2) | 0.3 (0.2-0.3) | .20 |

Abbreviation: NA, not applicable.

These data are from IQVIA’s National Prescription Audit PayerTrak on monthly prescription fills dispensed at retail pharmacies in the US.

P values represent the level of significance using a t test for the difference between 2023 and 2021.

In 2023, commercial insurance accounted for 61.4% (IQR, 60.7%-62.2%) of Ozempic, 89.5% (IQR, 89.1%-89.7%) of Wegovy, and 58.1% (IQR, 57.6%-58.4%) of Rybelsus fills. While Medicare Part D accounted for 28.5% (IQR, 27.8%-29.3%) and 32.9% (IQR, 32.4%-33.6%) of Ozempic and Rybelsus fills, respectively, in 2023, it only accounted for 1.2% (IQR, 0.9%-1.5%) of Wegovy fills. In contrast, Medicaid accounted for less than 10% of semaglutide fills for all 3 drug brands in 2023.

Discussion

The number of prescriptions filled for semaglutide has increased substantially, reaching 2.6 million prescriptions filled at retail pharmacies by December 2023. While Ozempic persistently accounted for most semaglutide fills, increases were considerably greater for Wegovy since its approval for weight loss in June 2021. These increases, which primarily occurred following increased awareness of weight-loss benefits in late 2022,3 are likely contributing to the FDA-reported shortage of Ozempic and Wegovy first issued in March 2022. Despite the disproportionate burden of obesity in Medicaid and Medicare Part D populations4,5 and recent increases in public spending on weight-loss medications,4,5,6 most Wegovy fills were for the commercially insured. Limitations of this study include a lack of data on individual-level variables (age, race, and ethnicity) and indications for use (diabetes or obesity). Future research should examine how changes in Medicare Part D and Medicaid coverage restrictions influence disparities in access to these essential medications.

Data Sharing Statement

References

- 1.Medications containing semaglutide marketed for type 2 diabetes or weight loss. US Food and Drug Administration. 2024. Accessed February 10, 2024. https://www.fda.gov/drugs/postmarket-drug-safety-information-patients-and-providers/medications-containing-semaglutide-marketed-type-2-diabetes-or-weight-loss

- 2.Sattar N, Lee MMY, Kristensen SL, et al. Cardiovascular, mortality, and kidney outcomes with GLP-1 receptor agonists in patients with type 2 diabetes: a systematic review and meta-analysis of randomised trials. Lancet Diabetes Endocrinol. 2021;9(10):653-662. doi: 10.1016/S2213-8587(21)00203-5 [DOI] [PubMed] [Google Scholar]

- 3.Blum D. The Wegovy shortage continues, leaving patients on the weight loss drug in limbo. New York Times. October 5, 2023. Accessed February 10, 2024. https://www.nytimes.com/2023/10/05/well/live/wegovy-shortage-ozempic-fda.html

- 4.Baig K, Dusetzina SB, Kim DD, Leech AA. Medicare Part D coverage of antiobesity medications—challenges and uncertainty ahead. N Engl J Med. 2023;388(11):961-963. doi: 10.1056/NEJMp2300516 [DOI] [PubMed] [Google Scholar]

- 5.Liu BY, Rome BN. State coverage and reimbursement of antiobesity medications in Medicaid. JAMA. 2024;331(14):1230-1232. doi: 10.1001/jama.2024.3073 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Eberly LA, Yang L, Essien UR, et al. Racial, ethnic, and socioeconomic inequities in glucagon-like peptide-1 receptor agonist use among patients with diabetes in the US. JAMA Health Forum. 2021;2(12):e214182. doi: 10.1001/jamahealthforum.2021.4182 [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Data Sharing Statement