Abstract

Most companies include carbon offsets in their net-zero strategy. However, many offset projects are poor quality and fail to reduce emissions as claimed. Here we focus on the twenty companies retiring the most offsets from the voluntary carbon market over 2020–2023. We examine if their offsets could be considered high quality and likely to benefit the climate. We curate an original company-level dataset to examine quality and climate benefits across four dimensions: (1) use of offsets from low/high-risk project types; (2) age of projects and credits; (3) price of credits; and (4) country of implementation. We find that companies have predominantly sourced low-quality, cheap offsets: 87% carry a high risk of not providing real and additional emissions reductions, with most offsets originating from forest conservation and renewable energy projects. Further, most offsets do not meet industry standards regarding age and country of implementation. These findings provide further evidence that the voluntary carbon market is not supporting effective climate mitigation. Particularly, we show that its persisting quality issues are exacerbated by the demand for low-quality offsets by individual companies.

Subject terms: Climate-change mitigation, Business

Trencher and colleagues investigate the twenty companies making the largest purchases of offsets from the voluntary carbon market from 2020 to 2023. They find that 87% of the purchased offsets carry a high risk of not providing real and additional emissions reductions. Further, most offsets do not meet industry standards regarding age and country of implementation. The findings reinforce concerns that the voluntary carbon market is failing to support effective climate mitigation.

Introduction

Increasing numbers of companies have pledged to reach net zero by 20501 to support climate mitigation efforts under the Paris Agreement2. To reach this goal with minimal changes to the underlying business, many companies are using or plan to use carbon offsets (also known as carbon credits)3. Offsets can be procured at low cost and are abundant on the voluntary carbon market (VCM). The appeal of offsets lies in their ability to allow companies to outsource decarbonisation efforts to external initiatives, thus avoiding the more difficult task of transforming their own operations and supply chains and phasing out fossil fuels4,5. The VCM has consequently grown rapidly. Valued at approximately US $2 billion in 2022, it is forecast to expand further in value and scale as companies increasingly seek to offset their emissions6.

However, claims by companies that offsets provide a reliable tonne-for-tonne means to neutralise their greenhouse gas (GHG) emissions have lost credibility due to increasing evidence that many offset projects are of low quality and fail to deliver the emissions reductions they promise7. Criticism has particularly concerned offsets from REDD+ (forest conservation)8–11 and renewable energy projects12–14. Such projects issue credits based on the claim to have avoided GHG emissions, but they are prone to over-crediting and exaggerating their ‘additionality’ (i.e. when a project would not be implemented without the revenue generated by selling offsets)15. The larger concern is that if offsets do not represent real GHG reductions, global emissions will increase if companies use them to counterbalance their carbon-emitting activities16. Recognising this, the science-based targets initiative, seeking to align corporate decarbonisation strategies with pathways to keep global warming below 1.5 °C, requires that companies pursue net-zero targets by reducing emissions within their value chain without using offsets17. As terms like ‘junk’18, ‘worthless’19 and ‘carbon con’20 are increasingly associated with offsets, companies relying on offsetting to accelerate decarbonisation also risk accusations of greenwashing21–23.

Suppliers and buyers of offsets have attempted to circumvent such concerns by claiming to use ‘quality’ offsets21,24. Guidance about offset quality has also emerged from VCM governance frameworks and from best-practice principles proposed by various stakeholders25–28. Despite considerable heterogeneity across different conceptions of quality29, most stress the need to ensure additionality and permanence, avoiding over-crediting and double-counting, and protecting against negative effects on society and the natural environment7,15,26,28,30.

Such quality principles, however, do not guarantee genuine climate benefits. Consider the case of an offset from a wind farm or forest conservation project that started 15 years ago. The climate impact of claiming such an offset today may be compromised in four ways. First, renewable energy projects carry a high risk of overestimating emissions reductions and lacking additionality12,13,15. Second, using historical mitigation activities to offset emissions today fails to promote new decarbonisation activities beyond those already scheduled to occur31. Indicators of quality should therefore consider the age of offset projects and credits32,33. Third, quality indicators should also address price. Cheap offsets typically originate from over-credited projects with low additionality15, diverting funds from projects with higher quality control measures that cost more11. Fourth, in countries where renewable energy has diffused widely and become standard practice, there is a weak argument for additionality. Thus, projects like renewable energy should be implemented in countries where such technologies have not yet mainstreamed due to technological, financial or policy hurdles12,13. Meanwhile, to draw down and permanently sequester historical emissions in pursuit of net-zero emissions, VCM best-practice principles34,35 and researchers36–38 have emphasised the importance of upscaling investments in carbon removal.

Since offset quality is strongly influenced by characteristics at the individual project level, the extant literature has focused on GHG accounting methodologies and assessing project-level climate benefits8,11–13,30,39. Yet there remains a need for a framework and indicators that can be applied with readily available market-level data to determine if the offsets retired by large corporate buyers correspond with key metrics of high quality and high climate benefits. However, firm-level analyses5,40–42 are few, despite many companies depending heavily on offsets to pursue decarbonisation goals. Further, scholars have yet to exhaustively study the publicly available data on registries to examine the behaviour of large-scale corporate offset buyers.

Accordingly, we examine the characteristics and quality of the offsets used by the twenty companies responsible for retiring the largest volumes on the VCM between January 2020 and December 2023. We build an original dataset that compiles each company’s offset procurements from the VCM’s three largest registries: Verra’s Verified Carbon Standard (VCS), the United Nation’s Clean Development Mechanism (CDM) and Gold Standard (GS). After clarifying the extent to which offset retirements support emissions avoidance or removal, we set out to answer: ‘To what extent could the offsets retired by these companies be considered high quality and likely to benefit the climate?’. We investigate retirement behaviour across four dimensions (Table 1): (1) use of offsets from low/high-risk project types; (2) age of projects and credits; (3) cost of credits and (4) country of implementation (applied only to renewable energy projects).

Table 1.

Framework for assessing offset quality and climate benefits

| Dimension | Indicator | Rule or standard illustratively used, coding framework and data source | Scientific basis in literature |

|---|---|---|---|

| 1. Relative quality risks | Do credits come from offset project types with a lower likelihood of overstating their emissions reduction or additionality? | Categorisations of offset project types with a lower, medium and higher risk using the relative quality risks framework in the Quality Offsets Guide by the Stockholm Environmental Institute and GHG Management Institute15. | 8,10,12,13,15,16 |

| 2. Age | Is the window between the offsetting activity and the time of retirement in line with industry standards? | Rule by Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) that excludes credits with a vintage year and project start year earlier than 2016. | 15,21,32,75 |

| 3. Price | Does the credit come from offset project types that typically sell for above-average prices? | Estimates of the average price paid for offsets by project category from Ecosystem Marketplace76. | 11,15,21 |

| 4. Country of implementation (applied to renewable energy projects) | Do credits derive from projects implemented in low-income countries where the diffusion of renewable energy is low and hampered by market or policy conditions? | (1) Rule by GS and VCS that limits eligible renewable energy projects to those located in a least developed country (LDC), and (2) Rule by GS that limits eligible renewable energy projects to those located in a low-income country or lower-middle income country where the penetration rate of the proposed energy technology is below 5%. Country classifications and data from World Bank79 and IRENA57. | 12,13,58 |

The analysis reveals that these twenty companies predominantly sourced their offsets from low-quality avoidance activities. Most offsets carry a high risk of overestimating emissions reductions and fail to meet industry standards regarding age and country of implementation. We also find that companies have actively targeted cheap credits. Our results provide further evidence that predominant practices on the VCM are not supporting effective climate mitigation. Our contribution is to demonstrate that individual companies are a major cause of persisting quality issues due to their demand for problematic and cheap offset types known to overstate emission reductions. We also provide the first publicly available dataset compiling the attributes of offsets used by the largest corporate buyers on the VCM. This complements the extant literature’s focus on supply-side issues such as project characteristics and registry methodologies.

Results

Scale and context of offsetting activity

Collectively, the twenty companies examined retired 134 MtCO2e over 2020–2023 (Fig. 1a). This volume is considerable, representing just over one-fifth of all global retirements made on the three registries (VCS, CDM and GS) during the same period (Table S1).

Fig. 1. Volume of offset retirements and proportion of emissions avoidance and emissions removal.

a Absolute volumes of all offsets retired by each company over 2020–2023. b Relative shares of avoidance or removal offsets retired over 2020–2023. Both panels show aggregated yearly results for each company that appear in Table S3a, b. c Absolute volume of avoidance and removal offsets for all companies by year. d Relative share of avoidance and removal offsets for all companies by year. Classification into avoidance, removal and mixed follows the University of California Berkeley’s Voluntary Registry Offsets Database64.

All companies but one in our sample have used offsets to claim carbon neutrality or pursue decarbonisation targets (Table S2). Domains of offset use extend from operational emissions (e.g. Boeing, Telstra and Norwegian CL) to various claims of ‘carbon-neutral’ products, such as offset-bundled LNG tankers (Shell and Chevron), parcel delivery (DPD and Yamato) and flights (Delta Airlines and easyJet).

The two largest offset buyers are Shell and Delta Airlines, each retiring around 23.5 MtCO2e over 2020–2023 (Fig. 1a and Table S3a, b). Retirements by these two companies alone make up roughly 35% of all offsets in the data set. Most companies retired far less than this: mean and median retirement volumes in the dataset are 6.71 MtCO2e and 3.84 MtCO2e, respectively, over 2020–2023.

When procuring offsets, the companies have predominantly targeted VCS (Table S4), which makes up 102 MtCO2e or 76% of all offsets retired by the twenty companies. This volume represents one quarter (24%) of all retirements made on VCS globally over 2020–2023 (Table S1). CDM is the next most targeted registry, accounting for 26.4 MtCO2e or 20% of all retirements. This volume represents 22% of all worldwide retirements conducted through CDM during the four-year period. The third registry, GS, is the least used, making up only 5.16 MtCO2e or 4% of all global retirement made on this registry. In sum, our results show that the twenty companies examined are among the largest buyers on VCS and CDM, the two largest registries globally in terms of credit issuances21.

Mitigation approach: retirements focus on emissions avoidance

Offset projects fall into two broad categories: (1) avoidance, where mitigation activities like renewable energy or improved forest protection generate credits based on the claim that GHG emissions were avoided compared to a counterfactual scenario where the activity was not implemented; and (2) removals, where nature-based or engineering-based initiatives directly capture and sequester atmospheric CO2. Stakeholders28,35, industry guidelines27,43, researchers36–38,44 and the IPCC45 underscore the importance of removals for achieving net zero, minimising emissions overshoot, and drawing down historical emissions, which could help reverse temperature rise once net zero is reached. The authoritative Oxford Principles even declare that organisations must ‘shift toward carbon removals’ away from avoidance34. Pro-removal discourse often emphasises engineering-based removal with permanent geological storage. However, such technologies are immature, in short supply, and were unavailable on the registries studied during 2020–2023. Accordingly, we consider here each company’s share of offsets from nature-based removal activities (e.g. afforestation, soil enhancement).

Results show that almost all offsets retired by the twenty companies are from avoidance projects (Fig. 1b, d). Avoidance offsets account for over 97% (131 MtCO2e) of all retirements in the dataset. Similarly, eighteen companies sourced 90% or more of their offsets from avoidance activities. In contrast, offsets from removal projects account for merely 2.3% of all retirements across the companies. Only three (PetroChina, easyJet and Audi) demonstrate meaningful engagement with carbon removal, each obtaining 5% or more of their offsets from removal projects.

We also do not find any evidence of a shift towards carbon removals (Fig. 1c, d and Table S3b). Indeed, the annual share of pure removal offsets rose substantially in only one year; reaching 1.1% in 2021 compared to 0.3% in 2020. This share remained stagnant in 2021, then contracted to 0.6% in 2023. Furthermore, only two companies (Audi and Takeda) visibly increased their share of removal credits over the four years. Most evident is Audi, increasing its removals share from none in 2020–2021 to 10% over 2022–2023. However, many companies decreased their share of removal credits over the same period: Shell, Volkswagen, Boeing, PetroChina and EY each reduced their removal share in 2022–2023 to below half of 2020–2021 levels. Thus, we find that demand for avoidance credits is substantial, persistent over time, and unaffected by VCM discourse around the need to reduce reliance on avoidance and shift towards carbon removal.

It should be emphasised that carbon removal projects are not immune to the quality issues affecting avoidance projects46. For instance, afforestation and soil enhancement projects have been found to overestimate carbon stockage16 and lack additionally47,48. Furthermore, nature-based solutions are unable to store carbon permanently for the millennial timescales required for effective climate mitigation44,49. These issues motivate us to separate the above analysis of mitigation strategy from the following evaluation of offset quality.

Relative quality risks: retirements dominated by high-risk offsets

The offset projects used by the companies are shown in Fig. 2a, d. In the first dimension of our quality assessment, we adopt a framework of relative quality risks published by the Stockholm Environmental Institute and the GHG Management Institute15. Although the framework does not assess quality based on individual project characteristics, it operationalises the view that some project types are, ceteris paribus, more likely to lack additionality, overestimate emissions reductions, or encounter leakage.

Fig. 2. Types of offset projects and quality risks for offsets retired in 2020–2023.

a Relative share of offset credits organized into differing relative risk profiles defined by the Stockholm Environmental Institute and GHG Management Institute15. b Relative share of retired offset credits organised into project categories defined by the University of California Berkeley’s Voluntary Registry Offsets Database64. c Breakdown of offset volumes sourced from forestry and land use projects. d Breakdown of offset volumes sourced from renewable energy projects. ‘Solar’ shows merged results for centralised and distributed solar. ‘Other’ shows merged results for geothermal and bundled.

We find that companies have overwhelmingly sourced high-risk offsets (Fig. 2a). 87% of credits fall into this high-risk category, whereas those credits with a low-risk profile make up only 6.0% of all retirements.

Most high-risk offsets stem from forestry and land use projects (mainly REDD+ initiatives, which conserve tropical forests and prevent deforestation) and large-scale renewable energy projects sized > 15 MWe. Medium-risk projects (e.g. household and community biodigesters, cookstoves, small-scale renewable energy projects sized ≥ 15 MWe) make up only 6.7% of purchased credits (Fig. 2b).

REDD+, classified as high-risk, is the most frequently used offset type by far (Fig. 2c). Comprising 58.2 MtCO2e (43%) of all credits retired, REDD+ projects feature in the retirement portfolios of sixteen companies. Notably, Gucci obtained 100% of its offsets from REDD+ projects. The strong preference for offsetting emissions via REDD+ projects should cause significant doubt regarding firms’ net-zero claims because most projects investigated in prior research have not achieved their stated climate benefits and over-issued credits. These investigations showed tendencies to exaggerate historical deforestation trends or regional baselines8,9,11,48, failures to reduce deforestation to levels claimed by developers8,10, and emissions leakage, where deforestation shifts to another area11.

Renewable energy projects are the next most sourced offset type, comprising 36%. Wind projects are the most voluminous (40%) in this category, followed by solar (33%) and hydropower (16%). Most of these renewable installations are large-scale, classified by the aforementioned framework15 as higher risk. This is due to the strong likelihood of miscalculating emissions avoided through fossil-power displacement or their weak additionality, since revenue from renewable electricity rather than offset sales is usually the decisive factor for investments. Numerous studies confirm the high likelihood of such problems ocurring12,13,50,51. Furthermore, renewable electricity has become competitive relative to fossil fuels around the world due to declining costs and supportive government policies52. As such, installing renewable energy has become standard practice rather than additional.

In our sample, twelve companies have offset their emissions with hydropower. Norwegian CL, a global cruise operator, sourced more than half its offsets from hydropower while Banco BV and Chevron each retired 2.99 MtCO2e and 1.38 MtCO2e. However, hydropower projects are highly unlikely to be additional, since most receive government support as infrastructure projects and are built regardless of the opportunity to capture extra revenue through offset sales50. As a result, hydropower projects are no longer allowed to register on VCS and are prohibited under a number of emissions trading schemes53 and best-practice VCM frameworks54.

Age: heavy reliance on historical actions not meeting industry standards

The second dimension of our quality assessment addresses the age of offsets, considering both vintage years and project start years. Results indicate that companies have sourced most of their offsets from aged projects, too old to meet even lenient quality standards in the VCM.

Figure 3 indicates that three-quarters (75%) of offsets retired would fail to meet eligibility rules for the carbon offsetting and reduction scheme for international aviation (CORSIA), managed by the United Nation’s International Civil Aviation Organization. To qualify in CORSIA, offset credits must derive from projects that started issuing credits in 2016 or later. Likewise, a project’s vintage year, or the year a particular mitigation action occurred, must also be 2016 or later.

Fig. 3. Share of offset credits retired by project start year and vintage year.

The relative share (%) of offset credits retired by all twenty companies in 2020–2023, organised into project start years and vintage years. Darker shades indicate a higher relative share. Project start years reflect the first year that an offset project began issuing credits. Vintage years capture the year in which a specific climate action occurred (e.g. a wind turbine generated electricity). Credits sourced from CDM are not shown as this registry does not disclose vintage years. Years after 2016, marked in blue, are illustratively used as a lenient indicator to designate a maximum age limit for project start years and vintage years set by the CORSIA, a governance mechanism for international airlines. This maximum age limit has also been adopted by other credit trading platforms.

In applying the 2016 cut-off year to our analysis, we acknowledge that CORSIA targets airlines, sets only a soft standard31,55, and that meeting the cut-off year does not inherently guarantee key quality attributes such as additionality. Nonetheless, the 2016 cut-off year aligns with what many industry stakeholders and offset trading platforms (e.g. CBL and ACX) have considered an acceptable age limit for offsets32 (see “Methods”). Moreover, setting a limit on the maximum vintage and project start year addresses quality concerns in at least two ways. First, it assures that offset projects adopt newer procedures when calculating emissions avoidance or removal, as methodologies are continuously updated to correct historical faults32. Second, it prevents the use of older credits, where the additionality is doubtful if a project continues to operate despite not having sold all its credits15,33.

Examining only vintages years shows that many companies have predominantly selected post-2016 credits, thereby meeting one part of the CORSIA rule. This is notably the case for Takeda, whose credits are all from 2016 or later, and for six other companies (Volkswagen, Eni, Telstra, Audi, Yamato and Skoda) sourcing 80% or more of their credits from post-2016 vintages (Fig. S1). Conversely, seven companies (Shell, Delta, Sasol, DPD, Gucci, PetroChina and Norwegian CL) have obtained the majority of their credits from pre-2016 vintages, presumably because older credits typically trade for lower prices21. For these seven companies, the tendency to source older vintages remains visible even when accounting for the age of the vintage year at the time of retirement (Fig. S2).

However, when considering project start years, we find that most of the offsets sourced by the twenty companies derive from old projects that began issuing credits a decade or more ago (start year ≤ 2013), (Fig. S3). This tendency is particularly pronounced for eight companies (Shell, Delta, Takeda, Sasol, DPD, Chevron, Norwegian CL and Hu-Chems), which each obtained three-quarters or more of their credits from projects started in 2013 or earlier. Overall, for all twenty companies combined, two-thirds (65%) of retired credits come from projects aged a decade or more. Our findings thus indicate that the majority of offsetting expenditures by the twenty companies have not supported the formation of new climate initiatives.

It is important to note that the Paris Agreement has established stricter rules than CORSIA for crediting periods. Specifically, offsets traded under its Article 6.4 mechanism (designed to replace the CDM) must come from mitigation activities that started in 2021 or later, a standard also advocated by the Science Based Targets initiative33. Although we do not expect the twenty companies in our dataset to have adhered to this rule during the period of analysis (2020–2023), it is notable that a mere 0.4% of their offsets came from projects with post-2021 start years (Fig. 3). This further illustrates how the offsets purchased by the twenty companies fall considerably short of contemporary quality standards.

Price: preference for low-quality offsets driven by low cost

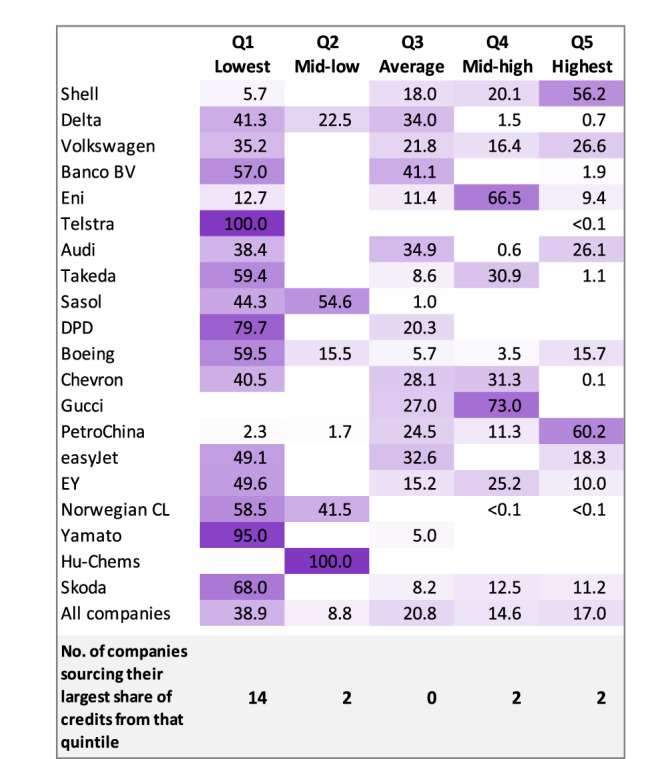

Because low-quality offsets tend to trade cheaper than higher-quality ones11,15,21, the third dimension of our assessment investigates buying preferences for cheaper credits. The results (Fig. 4) reveal a distinct preference for purchasing cheaper credits for most companies.

Fig. 4. Share of offset credits retired by price category.

The relative share (%) of credits retired by each company in 2020–2023, is organised into five quintiles. Each reflects the average estimated price of eight types of offset projects contained in our database relative to the price of other offset types (see Table S5). The bottom row shows the number of companies for whom a plurality of offsets (i.e. largest share) falls into that quintile. Pricing estimates for each project type are sourced from Ecosystem Marketplace76. To capture price fluctuations, we coded price categories each year. The table shows aggregated results for yearly trends, compiled in Fig. S4.

Sixteen companies have sourced a plurality of their credits from offset projects whose average estimated price falls into the two lowest price quintiles. For eleven companies in this group, low-price credits constitute the majority of offsets retired. Projects in the two lower price quintiles consist of RE, industrial/commercial and chemical processes, from which credits sold on average between $0.98 tCO2e and $5.39 tCO2e during 2020–2023 (Table S5). Moreover, our data show that the preference for cheaper credits is persistent for many companies (Fig. S4). Conversely, only four companies purchased the plurality of their offsets from the two higher price quintiles. Two companies featured in this group are Shell and PetroChina, each sourcing 80% and 98% of their offsets from the two upper quintiles. This result especially reflects their preference for REDD+ and afforestation offsets, which sold higher than other project types during 2020–2023, namely between $5.15 and $15.60 (Table S5).

These results correlate with earlier findings regarding the large share of offsets purchased from renewable energy projects (Fig. 2), indicating that the popularity of renewable offsets appears to reflect their consistently lower cost relative to other categories. Conversely, the companies choosing forestry and land-use offsets (mostly from REDD+ projects) have seemingly tolerated their price premium relative to other offset project types.

This interpretation, however, requires caution, since two trends suggest that companies have sourced forestry and land-use offsets in a way that would reduce their price premium relative to cheaper project types. First, our analysis of vintage years (Fig. S5) shows that companies choosing nature-based projects tend to choose older credits, especially compared to renewable energy projects. Second, our analysis of retirement volumes (Table S6) shows a strong tendency to purchase forestry and land-use offsets in large quantities (defined as >82.6 ktCO2e, the fifth quintile). Because selecting older vintages and purchasing in bulk are two strategies known to lower per-tonne offset costs21,56, both trends suggest that many companies have actively sought to reduce the price premium incurred when procuring forestry and land-use credits.

Country of implementation for renewable energy projects: few meet additionality rules

Eighteen companies have sourced 48.4 MtCO2e of credits (36% of all retirements) from renewable energy projects (Fig. 2b, d). Two registries, GS and VCS, have set explicit rules regarding the minimum conditions for renewable energy projects seeking registration to demonstrate additionality. Since similarly explicit guidance is lacking for other project types, including forestry and land use, industrial and commercial, we limit the fourth dimension of our quality assessment to renewable energy projects. We apply two tests to determine a minimum degree of additionality, with passing either test being sufficient. The first test, based on criteria set by GS and VCS, requires that renewable electricity projects be implemented in a least developed country (LDC). The second test, based on criteria set by GS, requires that projects target a low-income country (LIC) or lower-middle-income country (LMIC) where the penetration of the proposed technology is below 5% of all grid-connected generation capacity. Both rules ensure that projects are implemented in developing countries where renewable energy is not yet mainstream, and where technological, market and policy barriers hinder its diffusion. Although these rules apply only to cases of new project registration, both provide a meaningful test of additionality from the perspective of contemporary quality standards.

Few of the renewable energy offsets sourced by the companies satisfy either test (Fig. 5 and Fig. S7). The tightening of additionality standards by GS and VCS has not observably diverted offset demand away from low-quality renewable energy projects. For the first test, only 106 ktCO2e (0.2% of total retirements) come from projects implemented in an LDC, with only offsets from Mauritania and Uganda satisfying this condition. For the second test, over one-third (38%) of offsets come from projects that started issuing credits in a year when that country simultaneously met the low-income thresholds and had penetration rates for the deployed renewable energy technologies below 5%. Furthermore, although not required by GS or VCS, no offsets satisfy both tests.

Fig. 5. Registry additionality criteria for renewable energy projects.

The share of renewable energy (RE) offset credits retired by all twenty companies in 2020–2023 by country of origin and the share that meets additionality criteria set by registries. Test 1 (based on rules from GS and VCS) checks if a renewable energy project is located in a LDC. Test 2 (based on rules by GS) checks if the project is located in a LIC or LMIC where the penetration level of the proposed energy technology is below 5% of all grid-installed electricity capacity. The share of renewable energy offsets passing either additionality test is marked in blue. An offset credit only needs to pass one of the two tests to demonstrate a minimum degree of additionality. The period 2005–2021 for LIC/LMIC classifications covers all project start years in the dataset. Data for country classifications and renewables shares are sourced from the United Nations80, World Bank79 and IRENA57. For test 2, full results by country and renewable energy technology appear in Fig. S7. Bundled energy offsets (limited to 213,465 tCO2e from India) are excluded when conducting test 2 since these projects mix renewables technologies.

The renewable energy offsets used by the surveyed companies originate from projects implemented in 26 countries (Table S7). Most offsets, however, originate from just three countries—Brazil, China and India—that collectively supplied 84% of all renewables credits (Fig. S8). According to the second additionality test, offsets from Brazil and China especially have questionable additionality, because projects in these two countries started after Brazil and China had reached upper-middle income status and when penetration rates for the respective renewable energy technologies had exceeded 5% (Fig. S7). Moreover, Brazil and China collectively provided 4.47 MtCO2e of hydropower offsets to the companies. However, the additionality of these projects could be challenged because hydropower has long been a mainstream technology, and therefore common practice, in each country. Indeed, during 2005–2021 (the period covering all project start years in our dataset), hydropower’s share of electricity generation lay between 57–77% in Brazil and around 15–22% in China57. Conversely, around half (58%) of the renewables offsets from India (an LMIC) exhibit a stronger case for additionality, mainly because solar electricity did not exceed the 5% threshold until 2017.

In a complementary analysis, we examine the attractiveness of Brazil’s, China’s and India’s policy environment for renewable energy diffusion, since research and registry principles consider a weak policy environment a critical indicator of a project’s additionality58,50. Specifically, we compare each country’s annual score from the World Bank’s regulatory indicators for sustainable energy (RISE) project59, which evaluates the effectiveness of renewable energy policies, to the average score of OECD nations. Results show that renewable energy projects implemented in Brazil, China and India have emerged in a period of high governmental support (Fig. S9). Since 2010, RISE scores for India and Brazil have remained within the range of OECD nations, which received the highest scores globally for policies supporting renewables diffusion. India’s RISE score has even caught up to and closely aligned with Denmark’s and Germany’s since 2017, the two countries consistently attracting the highest scores globally. By demonstrating the attractive policy conditions enjoyed by renewable energy projects in Brazil, China and India, this supplementary analysis provides further grounds to doubt the additionality of offsets sourced from these three countries over the past decade.

In sum, our analyses provide multiple reasons to suspect that many renewable energy projects in Brazil, China and India lack additionality, and therefore, a genuine climate impact.

Summary of offset quality: most credits fail to meet multiple indicators

As a final and integrated analysis, we examine the quality and likely climate benefits of the offsets retired by each company across all four dimensions discussed in the previous sections (see “Methods”, Table 1), because an offset can simultaneously meet or fail multiple indicators. For non-renewable energy offsets, we assigned a score of ‘1’ for each of the following indicators met: (1) the project or credit does not fall into a high-risk category; (2) it meets CORSIA requirements for vintage and start year (i.e. 2016 or later) and (3) it has an estimated price higher than the average of other offset types. For renewable energy offsets, we add a fourth indicator, verifying if an offset originated from a LDC or from a LIC/LMIC with a low-penetration rate (<5%) for that energy technology. If all indicators are met, a non-renewable energy credit receives the highest score of ‘3’ while a renewable energy credit obtains ‘4’. Results (Fig. 6a, c) show that scores for most companies are concentrated between 0 and 2, meaning that most offsets purchased in 2020–2023 meet only half or fewer of the quality and climate benefit indicators applied here.

Fig. 6. Simultaneous application of all quality indicators to offsets retired.

a Average scores by company for all non-renewable energy credits (tested with three indicators) and renewable energy credits (tested with four indicators) retired over 2020–2023 using indicators of quality and climate benefits explained in Table 1 and Methods. Average scores were computed by weighting the relative share of credits from each company that received a particular score, shown in bottom two panels. For example, Delta Airline’s score for non-renewable credits, was calculated as 36.66 × 0 + 62.66 × 1 + 0.70 × 2 then divided by 100 to arrive at 0.64 against a maximum possible score of 3. Two companies (Gucci and Hu-Chems) marked with asterisks (*) did not retire any offsets from renewable energy projects. b Relative share of scores by company for all non-renewable energy credits (left) and renewable energy credits (right). For example, a share of 20% in the score category 1 indicates that 20% of the offsets retired by that company met only one criterion.

For non-renewable energy offsets, the average weighted score is 1.03 for all companies combined. Just under one-tenth (9.0%) of these offsets meet none of the three indicators, while 79% meet only one (Fig. 6b). This result especially reflects the tendency to source offsets from old projects started before 2016 in categories that typically sell at below average prices (Table S5). The tendency to procure low-scoring, low-quality credits is particularly pronounced for Norwegian CL and Telstra, for whom more than 99% of all non-renewable energy offsets scored ‘0’. Yamato stands out as the only company to meet all three criteria for all its renewables offsets. These offsets, however, represent only 5.0% (124 ktCO2e) of Yamato’s total retirements.

For renewable energy offsets, the average score for all companies is 0.81. This indicates even lower quality than the non-renewable energy offsets. Around half (48%) of the renewables credits fail to meet any of the four indicators, while roughly one quarter (24%) meet only one (Fig. 6c). In addition to the fact that renewables offsets typically trade for lower-than-average prices (Table S5), this outcome reveals a strong tendency to source credits from old projects located in countries not meeting contemporary additionality standards with respect to national income and renewable energy penetration rates. Further, most renewable energy projects are large-scale (>15 MWe). Such projects are deemed to carry a higher quality risk15, since profitability from selling electricity rather than offset credits is more likely the decisive factor for investment decisions.

Discussion

This study focused on the twenty largest buyers of carbon offsets over 2020–2023 in the VCM’s three major registries. Amid mounting concerns that many offsets are poor quality and fail to deliver genuine and additional emission reductions, we investigated the extent to which the offsets used by the twenty companies align with four dimensions of quality and high climate benefits.

The analysis reveals prolific retirements of low-quality and cheap offsets. In fact, none of the twenty companies could claim that a substantial portion of their retired offsets adhered to VCM quality standards and indicators of high climate benefits. Specifically, we find that 87% of offsets originate from high-risk project types such as REDD+ and large-scale RE, which are prone to overstating emissions reductions and over-issuing credits. Our analysis of buying behaviour suggests that many companies have continuously sourced these low-quality offsets because of their low cost. Furthermore, we find that most offsets derive from aged projects, indicating that the bulk of company spending on offsetting has not supported new investments in climate mitigation.

Particularly, the analysis on renewable energy credits, making up 36% of all retirements, reveals practices that deviate considerably from quality standards on the VCM. Around half (48%) of the renewables credits fail to meet any of the four indicators in our framework, while roughly one quarter (24%) meet only one (Fig. 6c). Most notably, only 106 ktCO2e (0.2%) of these credits come from renewables projects implemented in least-developed countries, where a strong case could be made for additionality—a condition now required by two registries, GS and VCS. Meanwhile, only 38% of renewables credits meet less stringent rules set by GS regarding country income and technology penetration levels. With 84% of renewables credits issued from projects implemented in Brazil, China and India, our analysis on the attractiveness of each country’s policy environment casts further doubts on the additionality of projects in these countries. This is because weak government policy—a cornerstone argument for additionality—does not apply to these countries.

Faced with mounting pressures to ‘clean up’ the market, there has been no shortage of guidance in the form of principles, recommendations, rule changes and commitments on the VCM to combat its chronic quality issues and bad behaviour27,34,54,60. However, our results reveal a persisting problem in the adoption of this guidance. The largest corporate buyers of offsets, who collectively account for over 20% of retirements on the VCM’s three largest registries, continue to source low-quality, cheap credits with minimal climate benefits. These findings support the growing body of evidence that the VCM—designed as a voluntary industry-led market operating free from government oversight and regulation—is plagued by fundamental quality issues that undermine its effectiveness in reducing global emissions11,13,37,58. While prior research has focused on offset projects7,9,16, registries58 and methodologies61, our results underscore the significant role of purchasing decisions by individual companies in perpetuating these quality issues. They reveal that companies in our sample have actively targeted—and therefore increased demand for—cheap offsets and project types with questionable climate benefits. Our study thus shows that the VCM’s unresolved quality issues arise not only from the supply side24, but also from demand for low-quality offsets.

All companies except one in our study have pledged net-zero targets or claim to provide carbon-neutral services (Table S2). These companies operate in diverse sectors like energy (Shell, Chevron, Eni and Sasol), aviation (Delta, easyJet and Boeing), car manufacturing (Audi, Volkswagen and Skoda), telecommunications (Telstra) and fashion (Gucci). Our results show that the offsets supporting these claims neither meet indicators of quality nor provide high climate benefits. The neutralisation effect of the investigated companies’ offsetting strategies is therefore highly likely to be overstated. Overstating environmental performance is an important indicator of greenwashing62. Our findings thus suggest that any decarbonisation claims connected to the use of these offsets lack integrity and amount to greenwashing.

Also pertinent to global efforts to reach net-zero emissions46, we find that carbon removal makes up only 2.5% of all offsets retired by the twenty companies in 2020–2023. This amount is lower than the average share of removals for all non-CDM retirements made globally, which is 4.1% in the same period63. As confirmed by our analysis and prior studies11,21, the preference for avoidance offsets can be largely explained by their low cost. Cheap offsets derive especially from RE, chemical processes, and industrial projects, which have traded between $1–5 per tCO2e since 2020 (Table S6). Conversely, costlier removal credits like afforestation have hovered in the range of $8–16 per tCO2e, considerably impeding their uptake21. Additionally, there is a severely limited supply of nature-based removal offsets compared to avoidance offsets on the VCM, with removals making up only around 5% of credits issued over 2020–202364. Our findings thus highlight a pressing need for much larger investments in carbon removal33. As underscored by the IPCC65, physically drawing down historical carbon emissions from the atmosphere may prove critical for addressing emissions overshoot and sustaining negative emissions after net zero is reached.

Our evaluation of offset quality (Table 1), however, does not link offset quality to a company’s mitigation approach, specifically the choice of avoidance vs removal offsets. This methodological decision reflects three considerations. First, the registries examined in this study do not yet offer technology-based carbon removals with permanent storage, which some stakeholders34,36,38 promote as a long-term goal for quality enhancement. Second, some VCM stakeholders and researchers worry that prioritising removals may distract from the urgent need to reduce emissions at the source. To use the ‘rapidly filling bathtub’ metaphor suggested by Ellis and colleagues66, assuming that avoidance and removal offsets equally satisfy quality criteria, atmospheric emissions overflow can be stopped by both ‘reducing the tap’s flow and pulling the plug out’. Third, upscaling nature-based removals is unlikely in itself to solve many of the VCM’s inherent quality problems37,46. Research shows that many afforestation and soil-sequestration projects do not capture carbon as claimed16 or would have proceeded without the extra revenue from offset sales16,48. Furthermore, nature-based removals are unable to store carbon on millennial time-scales49, and stockage can easily be reversed if perturbed by wildfires, drought, disease or changed land-management practices15,67. These unresolved quality risks for carbon removal projects call the utility of offsets as a decarbonisation strategy into deeper question. At the same time, these risks reinforce the urgency of pursuing emissions reductions and carbon neutrality by directly phasing out fossil fuels across society.

Our findings point to a need for corrective actions to address the ongoing quality issues in the VCM. We foresee two plausible options. In the first option, governments would intervene to regulate the VCM, restricting the use of offsets solely to those sourced from government-approved schemes that adhere to stringent quality control measures. But this would be unlikely to overcome all quality issues, since even forestry-based removal projects in government-regulated regimes fail to provide genuine, additional and permanent carbon sequestration, including in California68,69 and Australia16. Furthermore, renewable energy offsets generated through CDM, overseen by the United Nations, also suffer from low quality and low additionality13. With such abundant evidence that carbon offsets do not provide a reliable means of neutralising emissions, more fundamental change is required. In the second option, therefore, until verifiable and permanent removals become widely available, the VCM would be strictly limited to ‘contribution’ and no longer used for offsetting emissions11,27,28. In this way, companies would still support climate mitigation and co-benefits for sustainable development by buying offsets from outside their value chain, but refrain from claiming to have neutralised their emissions33. The shift from compensation to contribution would generate a need for companies to redirect their investments towards reducing in-house emissions and implementing transformative changes in technologies and business practices. Such a decarbonisation approach would incur higher costs than offsetting. Yet various modelling pathways, including those from the International Energy Agency70, underscore that transitioning away from fossil fuels is the surest and quickest pathway to net zero and meeting Paris Agreement targets71.

By revealing a demand for low-quality and cheap offsets, our analysis demonstrates that the self-regulating VCM lacks the ability to push its largest buyers towards offsets that meet even modest indicators of quality and climate benefits. Consequently, prevailing offsetting practices on the VCM cannot be seen as an effective substitute for regulatory policies that force physical changes in the energy technologies, supply chains and business models of large emitters. This view extends beyond regional or national markets to encompass international climate governance. Consider for instance Article 6 of the Paris Agreement, which allows countries to use carbon credits for domestic emission reductions, including offsets sourced from the VCM. As our study suggests, without fundamental market-level changes and greater adherence to quality principles, efforts to grow the VCM through integration with the Paris Agreement risk amplifying demand for low-quality offsets with limited or no climate benefits.

Methods

Our study followed a design shown in Fig. 7 and outlined below.

Fig. 7.

Research design of study.

Sample construction

Our analysis covers the world’s three largest carbon offset registries: Verra’s VCS the United Nation’s CDM and GS. In 2022, projects listed on these three registries accounted for 85% of all voluntary carbon offsets issued globally21.

We selected twenty companies for analysis, recognising that a small number of companies have retired a disproportionally large volume of credits from the above registries14. This strategy helped confine our analysis to a manageable sample size but still cover a significant portion of retirement activity across the three registries. This was achieved since the twenty companies examined are responsible for 21% of all credits retired worldwide on VCS, CDM and GS over 2020–2023 (Table S1).

To identify the twenty largest buyers over 2020–2023 on the three registries, we obtained a proprietary list from Allied Offsets (a data-analysis firm). When building our sample of companies, we excluded Toucan (a US-based blockchain start-up) due to its unique mission of purchasing and retiring low-quality offsets, thereby preventing heavy emitters from using them for emissions compensation.

Data collection

Data collection occurred from October 2022 to February 2024. The principal data for analysis was sourced from the publicly available information on the online databases of the three offset registries VCS, CDM and GS. We identified the retirements belonging to each of the twenty companies in our sample by manually searching for their names in fields for retirement beneficiaries or reasons. We also used variations or codes for company names, since Delta Airlines, for example, frequently records its name as ‘DL’. Our analysis is limited to identifiable retirements and does not consider instances where a company retired credits but did not disclose its name on that registry.

Our analysis covers retirement activity from January 1, 2020, to December 31, 2023. Two reasons underpin our selection of this period. First, the chosen registries underwent a rapid growth of credit issuances during this period21. Second, the four years since the start of 2020 have seen a rapid increase in the adoption of net-zero targets by companies and the use of offsets for decarbonising operations, supply chains and various products and services1.

We collated the data from each registry into a single database (Supplementary Data 1). This was organised by company, and offset project and then all cases of retirement transactions were identified on each registry. To verify the accuracy and replicability of our calculation of each company’s retirement volumes, we purchased proprietary data from a firm (Allied Offsets) and cross-checked their results with ours. This triangulation process increases the accuracy of our dataset in two ways. First, it helped us overcome situations where a particular company discloses its name in registry records using a code name known only to those working inside the VCM (this was the case for Sasol). Second, it helped us verify the replicability of our manual procedure for searching the three registries for each company’s retirements.

Mitigation approach

To examine the focus of mitigation activities supported by offset procurements, we coded projects as removal, avoidance or mixed following categories suggested by the University of California Berkeley’s Voluntary Registry Offsets Database64. As a small difference, we use the term ‘avoidance’ in our study to denote what the Berkeley database terms ‘reduction’. This reflects our view that avoidance better captures the speculative nature of offsetting projects that issue credits based on counterfactual claims to have avoided GHG emissions. It should also be noted that both the Berkeley database and ours consider REDD+ projects as avoidance/reduction, even though some protected forest sinks also remove atmospheric carbon. This categorisation is supported by literature72, which demonstrates that in terms of surface area and tonnes of carbon avoided or removed, the primary function of REDD+ projects is avoidance, through preventing deforestation.

Framework for assessing offset quality and climate benefits: construction and application

Our analysis of each company’s offsetting behaviour was guided by the question: ‘To what extent could the offsets retired by these companies be considered high quality and likely to benefit the climate?’ To objectively assess the quality and likely climate benefits of offsets retired by each company, we adopted various indicators, standards and principles that are used on the VCM, advocated by its various stakeholder bodies, or discussed in the peer-reviewed literature. These were identified through a targeted review of the relevant grey and academic literature. This strategy avoids the integration of subjective value-based judgements in the analysis. The resulting framework consists of four dimensions and indicators (Table 1) that evaluate the quality and likely climate benefits of offsets from four key perspectives emphasised in the VCM and peer-reviewed literature: (1) use of offsets from low/high-risk project types; (2) age of projects and credits; (3) price of credits and (4) country of implementation. The main features and rationale of this framework, as well as any analytical decisions and additional data sources, are summarised below.

It is important to note that we do not include the mitigation approach (i.e. avoidance or removal) as an indicator of offset quality. Some industry frameworks like the Science Based Targets initiative and the International Standards Organization have stipulated that companies should exclusively use removals when using offsets to reach net-zero targets25,43,73. However, as already explained, our methodological decision reflects evidence that non-durable removal techniques like afforestation and soil enhancement also suffer from quality issues, especially with regard to carbon stockage estimation15,16 and additionality47,48. Furthermore, due to technological immaturity, offsets from engineering-based removals with durable storage—promoted by some stakeholders as critical for quality enhancement34,36,44—were not traded on the studied registries.

Relative quality risks

We first coded project types in accordance with categories used by the University of California Berkeley’s Voluntary Registry Offsets Database64. This classifies an offset project into a specific sector (e.g. industrial and commercial) and type (e.g. energy efficiency, waste gas recovery). Next, we evaluated the quality risks of each project type with a framework developed by the Stockholm Environmental Institute and GHG Management Institute15, which defines three relative risk levels: lower risk, medium risk, and higher risk. Based on interviews with experts, the framework operationalises the view that some types of offset projects, all else being equal, involve a higher relative risk of failing basic quality criteria (additionality, accurate emissions accounting, etc.) than other types of projects. Projects falling into the higher risk category include forestry and land use (encompassing both avoidances [e.g. REDD+] and afforestation), large-scale renewables (>15 MW), and agriculture. Examples of projects in the medium risk category are small-scale renewables (≤15 MW), energy efficiency (demand-side) and household/community projects like improved cookstoves. Projects considered to involve a lower relative quality risk are fewer, key examples being methane destruction (without utilisation) and N2O gas destruction. It should be noted that the framework is not intended to provide an exhaustive evaluation of project-level quality attributes, which can vary strongly from project to project. However, many of the framework’s evaluations are supported by ample literature. For instance, numerous studies show that REDD+9,11, afforestation16,48, renewables12,13, agriculture47 and cooking stove39 projects tend to suffer from low additionality and over-crediting. Conversely, project types such as N2O gas destruction may be more likely to be additional58,74, since their investment is typically not justifiable in the absence of revenue from carbon credits, and newer methodologies address historical problems such as perverse incentives to increase N2O production before issuing credits.

When placing offset projects into quality risk categories, we checked project documentation on registries to decide key factors such as capacity size for renewables installations, utilisation of methane gas (for grid-connected power) for landfill methane projects, etc. In a few cases where we were unsure about what risk categories to assign offset projects too, we contacted the authors15 for guidance.

Age

Our analysis of age encompasses two perspectives. The first, project start year, measures the start of the first credit issuance period. This captures the year when an offset project started its emissions avoidance/removal activities (e.g. the year when a wind farm connected to the grid). The second, vintage, measures the year when a climate action associated with an offset credit was conducted (e.g. a particular year during which deforestation activities were prevented).

Debates continue about what should be considered a suitable maximum for offset vintages or project start years31,32,34. Thus, there is no definitive age limit that would guarantee quality. Recognising this, we adopt as an illustrative indicator a rule from CORSIA, which governs offsetting in the global aviation industry, and prohibits the use of offset credits with a vintage year or project start year before 2016. Although this lenient cut-off year by no means constitutes a rigorous standard, it has been adopted as a defacto yardstick by some commodity trading platforms that screen for quality (e.g. ACX’s sustainable development goals tonne or global nature tonne+ and CBL’s Global Emissions Offset).

There are several reasons why younger offsets may offer higher climate benefits than older ones. First, newer offset projects ensure that investments are directed towards contemporary rather than historical climate actions. This is essential for supporting the formation of new or recent climate mitigation initiatives and for minimising the use of offset credits from historical projects that cannot deliver further emissions reductions beyond what they are already scheduled to do31,33. Second, old projects that still issue credits for past actions (i.e. back issuing) or that have large volumes of unsold vintages are unlikely to be additional. Because such a project has continued to operate despite not having sold all of its credits, there is a strong argument to suspect that the initiative did not need revenue from offset sales to attain bankability, and therefore is not additional32. Third, older projects are likely to use older methodologies, which in many cases have been discredited and updated due to problems. Older projects are therefore more prone to overestimating emissions reductions and over-issuing credits32,75. Credit prices on the VCM reflect preferences for newer vintages, which generally fetch higher premiums from buyers21.

Price

Another important indicator of credit quality is the price since cheaply priced credits are widely assumed to reflect the low quality and low additionality15,21. Our attention to this indicator also recognises that when companies consistently choose cheap credits, project implementers lose the incentive to supply high-quality credits, which in most cases require higher prices. Preferences for cheap credits can thus drive a race to the bottom by incentivising low-cost projects with weak measures to ensure climate integrity11.

Because the VCM experiences sharp fluctuations in credit prices, we focused our analysis on the relative prices of different offset types—i.e. the cost of one type of offset, such as RE, compared to another type, such as chemical processes. Estimates of average annual prices were obtained from Ecosystem Marketplace, which publishes estimates based on a yearly survey distributed to its member organisations, which use offsets76. We then arranged these average price estimates into quintiles (Table S3), calculating for the twenty companies in our sample the volume of credits that fell into each price range each year (Fig. S4).

Country of implementation (applied to renewable energy projects)

The country of implementation is a critical determinant of a project’s additionality, reflecting whether a project would have been financially feasible and therefore implemented without the opportunity to generate extra revenue by selling carbon credits. To ensure additionality, it is crucial that offsetting projects are implemented in countries where significant barriers (technological, financial, regulatory etc.) for that particular technology exist12. Conversely, if a mitigation technology or activity is standard practice in a country, it should not be considered additional21. Although such considerations are relevant to all kinds of offsetting projects, we limited our analysis to renewable energy projects. This is because the VCM has established explicit criteria regarding the countries where the implementation of renewable energy activities could be considered additional. Our analysis consists of two tests that apply criteria introduced by VCS and GS between 2019 and 2020.

Using a criterion from GS and VCS, the first test determines if the renewable energy project is implemented in a LDC77,78. The second test, using criteria from GS, checks if the project is located in a low-income or LMIC where the share of the proposed renewable electricity technology is below 5% of all installed electricity capacity77. To sufficiently demonstrate a minimum level of additionality, an offset project need only satisfy one test. Although these tests would only take effect in the case where a new offset project sought admission to either registry, both tests nonetheless provide an objective means to assess an offset’s potential additionality (and therefore quality and climate benefit) with contemporary industry standards. Notably, both the adopted criteria emerged in response to the realisation that many early renewable energy projects issuing offset credits on the major registries were implemented in countries where attractive market, policy and technology conditions had lowered the barriers to upscaling, thereby reducing the likelihood that these projects were additional52.

Analysis: verification with experts

To check the soundness of our methods, results and interpretations, we conducted six interviews during October 2022 and October 2023, presenting our evolving methodology to experts working in the VCM. All experts possess several years of experience in their current roles. We used their advice to improve our methodology and interpretations of results. The interviewed experts were composed of one researcher at a Europe-based think tank (Carbon Market Watch) and four analysts working at data firms in Europe and North America (Trove Research, Carbon Direct and Allied Offsets). This composition of experts allowed us to obtain diverse feedback on our study that reflected critical, neutral and supportive positions regarding the climate integrity of the VCM.

Limitations

Our study has several limitations. First, our analysis is confined to the retirements that we could identify on the three registries and does not consider instances where a company has retired offsets but has not disclosed its name in the relevant fields on the registry. Thus, the scale of actual retirements may be larger than that captured by our analysis, particularly because many companies will conceal offset retirements to escape public scrutiny or purchase offsets through intermediaries or internal means. This limitation could be overcome by using other sources of offset retirement disclosure, such as annual surveys submitted to CDP (Climate Disclosure Project). We did not use this data as not all companies in the sample report to CDP. Besides, CPD data also lacks vintage years. Second, we did not analyse the various policies within companies that might dictate their offsetting behaviour and how they use offset credits for decarbonisation and pursuing net-zero targets. Analysing these factors, including interviews with company representatives, would deepen understanding of the many determinants of corporate offsetting behaviour. Third, our analysis of offset quality does not account for the varying conditions of individual projects, which are a key determinant of quality. Scholars have used various methods to appraise individual project quality, such as Internal Rate of Return12,50, baseline settings and methodologies11 and effectiveness at actually reducing emissions8,9,58. With around 500 projects used by the twenty companies, we consider a project-by-project quality analysis beyond the scope of this research. Although we could have used project quality ratings by private firms in the VCM (e.g. BeZero and Calyx), ratings are not available for around three-quarters of the projects in our database. This reduces their utility for our analysis. Fourth, we did not have access to actual transaction prices paid by companies, since such data is not publicly available.

Supplementary information

Description of Additional Supplementary Files

Acknowledgements

We express thanks to the experts who shared their insights and helped us to improve our methodology, analysis and interpretations.

Author contributions

G.T. conceived the study, collected data and performed the analysis with contributions from S.N. and J.C. G.T. wrote the manuscript and drew all figures. S.N., J.C. and M.J. all contributed to drafting the manuscript and improving the analysis.

Peer review

Peer review information

Nature Communications thanks Derik Broekhoff and the other, anonymous, reviewer(s) for their contribution to the peer review of this work. A peer review file is available.

Data availability

The main dataset used for analysis, compiling the volume and characteristics of the offsets retired by each company, has been made available in Supplementary Data 1 as an electronic spreadsheet.

Competing interests

The authors have no competing interests to declare.

Footnotes

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

The online version contains supplementary material available at 10.1038/s41467-024-51151-w.

References

- 1.Hale, T. et al. Assessing the rapidly-emerging landscape of net zero targets. Clim. Policy22, 18–29 (2022). 10.1080/14693062.2021.2013155 [DOI] [Google Scholar]

- 2.Rekker, S., Ives, M. C., Wade, B., Webb, L. & Greig, C. Measuring corporate Paris compliance using a strict science-based approach. Nat. Commun.13, 4441 (2022). 10.1038/s41467-022-31143-4 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.Fankhauser, S. What next on net zero? One Earth4, 1520–1522 (2021). 10.1016/j.oneear.2021.10.017 [DOI] [Google Scholar]

- 4.Trencher, G., Blondeel, M. & Asuka, J. Do all roads lead to Paris? Comparing pathways to net-zero by BP, Shell, Chevron and ExxonMobil. Climatic Change176, 83 (2023). 10.1007/s10584-023-03564-7 [DOI] [Google Scholar]

- 5.Christiansen, K. L. et al. Our burgers eat carbon”: investigating the discourses of corporate net-zero commitments. Environ. Sci. Policy142, 79–88 (2023). 10.1016/j.envsci.2023.01.015 [DOI] [Google Scholar]

- 6.BloombergNEF. Long-term carbon offsets outlook 2023 (cited 30 July 2023); https://www.bloomberg.com/professional/insights/commodities/long-term-carbon-offsets-outlook-2023/.

- 7.Probst, B., Toetzke, M., Anadón, L. D., Kontelon, A. & Hoffman, V. Systematic review of the actual emissions reductions of carbon offset projects across all major sectors (Research Square, 2023). 10.21203/rs.3.rs-3149652/v1.

- 8.West, T. A. P. et al. Action needed to make carbon offsets from forest conservation work for climate change mitigation. Science381, 873–877 (2023). 10.1126/science.ade3535 [DOI] [PubMed] [Google Scholar]

- 9.West, T. A. P., Börner, J., Sills, E. O. & Kontoleon, A. Overstated carbon emission reductions from voluntary REDD+ projects in the Brazilian Amazon. Proc. Natl. Acad. Sci.117, 24188–24194 (2020). 10.1073/pnas.2004334117 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Guizar-Coutiño, A., Jones, J. P. G., Balmford, A., Carmenta, R. & Coomes, D. A. A global evaluation of the effectiveness of voluntary REDD+ projects at reducing deforestation and degradation in the moist tropics. Conserv. Biol.36, e13970 (2022). 10.1111/cobi.13970 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Haya, B. K. et al. Quality assessment of REDD+ carbon credit projects. Berkeley Carbon Trading Project2023 (cited 20 September 2023); https://gspp.berkeley.edu/research-and-impact/centers/cepp/projects/berkeley-carbon-trading-project/REDD+.

- 12.Lo, A. Y. Carbon offsetting and renewable energy development. Geographical Res.61, 158–163 (2023). 10.1111/1745-5871.12600 [DOI] [Google Scholar]

- 13.Calel, R., Colmer, J., Dechezleprêtre, A. & Glachant, M. Do carbon offsets offset carbon? 2021 (cited 4 July 2023); https://www.lse.ac.uk/granthaminstitute/publication/do-carbon-offsets-offset-carbon/.

- 14.Rathi, A., White, N. & Pogkas, P. Junk Carbon Offsets Are What Make These Big Companies ‘Carbon Neutral’2022 (cited 2 December 2022); https://www.bloomberg.com/graphics/2022-carbon-offsets-renewable-energy/.

- 15.Broekhoff, D., Gillenwater, M., Colbert-Sangree, T. & Cage, P. Securing Climate Benefit: A Guide to Using Carbon Offsets2019 (cited 20 June 2023); https://www.offsetguide.org/wp-content/uploads/2020/03/Carbon-Offset-Guide_3122020.pdf.

- 16.Macintosh, A. et al. Australian human-induced native forest regeneration carbon offset projects have limited impact on changes in woody vegetation cover and carbon removals. Commun. Earth Environ.5, 149 (2024). 10.1038/s43247-024-01313-x [DOI] [Google Scholar]

- 17.Science Based Targets. SBTI Corporate Manual Version 2.12023 (cited 10 October 2023); https://sciencebasedtargets.org/resources/files/SBTi-Corporate-Manual.pdf.

- 18.White, N. Carbon Offset Gatekeepers Are Failing to Stop Junk Credits 2023 (cited 20 August 2023); https://www.bloomberg.com/news/articles/2023-03-21/top-carbon-offset-registries-are-failing-to-stop-junk-credits

- 19.Greenfield, P. Carbon credit speculators could lose billions as offsets deemed ‘worthless’2023 (cited 25 August 2023); https://www.theguardian.com/environment/2023/aug/24/carbon-credit-speculators-could-lose-billions-as-offsets-deemed-worthless-aoe.

- 20.Source Material. The Carbon Con 2023 (cited 25 August 2023); https://www.source-material.org/vercompanies-carbon-offsetting-claims-inflated-methodologies-flawed/.

- 21.World Bank. State and Trends of Carbon Pricing 2023 (cited 15 August 2023); https://openknowledge.worldbank.org/items/58f2a409-9bb7-4ee6-899d-be47835c838f.

- 22.Trouwloon, D., Streck, C., Chagas, T. & Martinus, G. Understanding the use of carbon credits by companies: a review of the defining elements of corporate climate claims. Glob. Chall.7, 2200158 (2023). 10.1002/gch2.202200158 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.UN. Integrity Matters: Net-Zero Commitments by Businesses, Financial Institutions, Cities and Regions2023 (cited 15 August 2023); https://www.un.org/sites/un2.un.org/files/high-level_expert_group_n7b.pdf.

- 24.Valiergue, A. & Ehrenstein, V. Quality offsets? A commentary on the voluntary carbon markets. Consum. Mark. Cult.26, 1–13 (2022).

- 25.Allen, M. et al. The Oxford Principles for Net Zero Aligned Carbon Offsetting2021 (cited 30 March 2021); https://www.smithschool.ox.ac.uk/publications/reports/Oxford-Offsetting-Principles-2020.pdf.

- 26.Integrity Council for the Voluntary Carbon Market. Core Carbon Principles and Assessment Framework2023 (cited 10 March 2024); https://icvcm.org/the-core-carbon-principles/.

- 27.VCMI. Claims Code of Practice: Building integrity in voluntary carbon markets2023 (cited 1 October 2023); https://vcmintegrity.org/vcmi-claims-code-of-practice/.

- 28.Day, T. et al. Corporate Climate Responsibility Monitor 2023 (cited 10 February 2023); https://carbonmarketwatch.org/publications/corporate-climate-responsibility-monitor-2023/.

- 29.Huber, E., Bach, V. & Finkbeiner, M. A qualitative meta-analysis of carbon offset quality criteria. J. Environ. Manag.352, 119983 (2024). 10.1016/j.jenvman.2023.119983 [DOI] [PubMed] [Google Scholar]

- 30.Broekhoff, D. & Spalding-Fecher, R. Assessing crediting scheme standards and practices for ensuring unit quality under the Paris agreement. Carbon Manag.12, 635–648 (2021). 10.1080/17583004.2021.1994016 [DOI] [Google Scholar]

- 31.Warnecke, C., Schneider, L., Day, T., La Hoz Theuer, S. & Fearnehough, H. Robust eligibility criteria essential for new global scheme to offset aviation emissions. Nat. Clim. Change9, 218–221 (2019). 10.1038/s41558-019-0415-y [DOI] [Google Scholar]

- 32.Turner, G. & Grocott, H. The Global Voluntary Carbon Market: Dealing With the Problem of Historic Credits2021 (cited 15 August 2022); https://trove-research.com/wp-content/uploads/2021/01/Global-Carbon-Offset-Supply_11-Jan-1.pdf.

- 33.Science Based Targets. Above and Beyond: An SBTi Report on the Design and Implementation of Beyond Value Chain Mitigation (BVCM)2024 (cited 1 May 2024); https://sciencebasedtargets.org/resources/files/Above-and-Beyond-Report-on-BVCM.pdf.

- 34.Axelsson, K. et al. Oxford Principles for Net Zero Aligned Carbon Offsetting (revised 2024)2024 (cited 14 March 2024); https://www.smithschool.ox.ac.uk/sites/default/files/2024-02/Oxford-Principles-for-Net-Zero-Aligned-Carbon-Offsetting-revised-2024.pdf.

- 35.World Economic Forum. The Voluntary Carbon Market: Climate Finance at an Inflection Point2023 (cited 25 August 2024); https://www3.weforum.org/docs/WEF_The_Voluntary_Carbon_Market_2023.pdf.

- 36.Boyd, P. W., Bach, L., Holden, R. & Turney, C. Carbon offsets aren’t helping the planet—four ways to fix them. Nature620, 947–949 (2023). 10.1038/d41586-023-02649-8 [DOI] [PubMed] [Google Scholar]

- 37.Cullenward, D., Badgley, G. & Chay, F. Carbon offsets are incompatible with the Paris Agreement. One Earth6, 1085–1088 (2023). 10.1016/j.oneear.2023.08.014 [DOI] [Google Scholar]

- 38.Carton, W. et al. Net Zero, Carbon Removal and the Limitations of Carbon Offsetting (CSSN Position Paper 2022:1) (cited 20 July 2022); https://www.cssn.org/wp-content/uploads/2022/06/Net-Zero-and-Carbon-Offsetting-Position-Paper.pdf.

- 39.Gill-Wiehl, A., Kammen, D. M. & Haya, B. K. Pervasive over-crediting from cookstove offset methodologies. Nat. Sustain.7, 191–202 (2024). 10.1038/s41893-023-01259-6 [DOI] [Google Scholar]

- 40.Engler, D., Gutsche, G., Simixhiu, A. & Ziegler, A. On the relationship between corporate CO2 offsetting and pro-environmental activities in small- and medium-sized firms in Germany. Energy Econ.118, 106487 (2023). 10.1016/j.eneco.2022.106487 [DOI] [Google Scholar]

- 41.Jaraitė, J., Kurtyka, O. & Ollivier, H. Take a ride on the (not so) green side: How do CDM projects affect Indian manufacturing firms’ environmental performance? J. Environ. Econ. Manag.114, 102684 (2022). 10.1016/j.jeem.2022.102684 [DOI] [Google Scholar]

- 42.Guix, M., Ollé, C. & Font, X. Trustworthy or misleading communication of voluntary carbon offsets in the aviation industry. Tour. Manag.88, 104430 (2022). 10.1016/j.tourman.2021.104430 [DOI] [Google Scholar]

- 43.ISO. International Organization for Standardization2023 (cited August 2023); https://www.iso.org/netzero.

- 44.Schenuit, F. et al. Secure robust carbon dioxide removal policy through credible certification. Commun. Earth Environ.4, 349 (2023). 10.1038/s43247-023-01014-x [DOI] [Google Scholar]

- 45.IPCC. AR6 Climate Change 2022: Mitigation of Climate Change, the Working Group III contribution 2022 (cited 25 May 2023); www.ipcc.ch/report/sixth-assessment-report-working-group-3/.

- 46.Fankhauser, S. et al. The meaning of net zero and how to get it right. Nat. Clim. Change12, 15–21 (2022). 10.1038/s41558-021-01245-w [DOI] [Google Scholar]

- 47.Barbato, C. T. & Strong, A. L. Farmer perspectives on carbon markets incentivizing agricultural soil carbon sequestration. npj Clim. Action2, 26 (2023). 10.1038/s44168-023-00055-4 [DOI] [Google Scholar]

- 48.Salo, E., Rinne, J. & Kaskeala, N. From Crisis to Confidence: Rethinking Integrity in the Voluntary Carbon Market2023 (cited 10 September 2023); https://www.compensate.com/articles/from-crisis-to-confidence-rethinking-integrity-in-the-voluntary-carbon.

- 49.UNEP. Emissions Gap Report 2023: Broken Record 2023 (cited 10 May 2024); https://www.unep.org/resources/emissions-gap-report-2023.

- 50.Cames, M. et al. How additional is the Clean Development Mechanism? Analysis of the application of current tools and proposed alternatives2016 (cited 1 December 2022); https://climate.ec.europa.eu/system/files/2017-04/clean_dev_mechanism_en.pdf.

- 51.Trove Research. The Role of “Reduction” and “Removal” Projects in the Voluntary Carbon Market (cited 23 July 2023); https://trove-research.com/reports-and-commentary/.

- 52.BloombergNEF. Global Carbon Market Outlook 2022 (cited 15 August 2023); https://www.bloomberg.com/professional/blog/global-carbon-market-outlook-2022-bulls-trump-bears/.

- 53.La Hoz Theuer, S. et al. Offset Use Across Emissions Trading Systems (ICAP, 2023).

- 54.Climate Impact Partners. The Carbon Neutral Protocol 2023: The global standard for carbon neutral programmes (cited 10 October 2023); https://www.carbonneutral.com/the-carbonneutral-protocol/technical-specifications-and-guidance/step-4-reduce-1/4-7-excluded-emission-reduction-project-types.

- 55.Nick, S. & Thalmann, P. Towards true climate neutrality for global aviation: a negative emissions fund for airlines. J. Risk Financ. Manag.15, 505 (2022) 10.3390/jrfm15110505 [DOI] [Google Scholar]

- 56.Favasuli, S. & Sebastian, V. Voluntary carbon markets: how they work, how they’re priced and who’s involved. in Insight. 40–47 (S&P Global Platts, 2021).