Abstract

Background

The long-term financial impact of cancer care has not been adequately addressed in young adults. As part of a remote intervention study, we describe medical financial distress and hardship among young adult survivors of blood cancer at study entry.

Methods

Young adults were recruited from 6 US hospitals. Using a Research Electronic Data Capture link, young adults confirmed their eligibility—namely, currently 18 to 39 years of age, blood cancer diagnosis 3 or more years ago, off active treatment, and not on parent’s insurance. Following consent, the baseline assessment was sent. The primary outcome measure, the Personal Financial Wellness Scale, measured financial distress (scored as severe, 1-2; high, 3-4; average, 5-6; and low to no, 7-10). Medical financial hardship encompassed material hardship, psychological impact, and coping behaviors. Descriptive summary statistics and linear regression were used.

Results

Among the 126 participants, 54.5% came from minority racial or ethnic groups. Median time since diagnosis was 10 years (interquartile range = 6-16 years), with 56% having received a diagnosis when they were between 18 and 39 years of age. The overall mean (standard deviation) Personal Financial Wellness Scale score was 5.1 (2.4), but 49% reported severe or high distress. In multivariable analysis, female sex, Hispanic ethnicity, and lower income were strongly associated with worse Personal Financial Wellness Scale scores. Among participants with severe financial distress (n = 26), 72% reported 2 or more household material hardships, had worse scores across all psychological domains, and altered survivorship care because of cost (68%).

Conclusions

Nearly half of long-term young adult cancer survivors reported severe or high levels of financial distress. Individuals with severe or high distress also reported more medical financial hardship than other participants. This finding highlights the need for ongoing financial intervention in this vulnerable population.

ClinicalTrials.gov

There is increasing recognition that many patients with cancer experience deleterious financial effects, including substantial out-of-pocket expenses; loss or alteration of employment; and, in extreme cases, loss of savings and property. The term financial toxicity was coined to describe these impacts (1-4), likened to an acute toxicity of treatment. This conceptualization of medical cost consequences has been critically needed, but the long-term cost consequences survivors continue to face years after the completion of cancer treatment has been underappreciated and understudied. Financial distress and medical financial hardship, described to encompass material burden, psychological impact, and behavioral consequences (5-7), can be long lasting. Similar to other late effects of cancer treatment (8,9), the potential for long-term financial distress and hardship requires ongoing surveillance, monitoring, and intervention.

Young adult (ie, aged 18-39 years) cancer survivors are especially vulnerable to the long-term financial distress and hardship of cancer and its treatment compared with older adults. First and foremost, survival for the majority of young adults is measured in decades. Second, for survivors of childhood and adolescent cancer aging into the young adult age group or individuals with onset of cancer during young adulthood, the cancer experience collides with key developmental milestones, including educational and vocational attainment, social and financial independence, and gradual acquisition and stabilization of finances. Kayser et al. (10) highlighted that young adults are less financially stable than older adults, with financial stressors such as student loan debt, bad credit, and costs associated with starting or raising a family. In contrast to older adults, who are at risk for bankruptcy or consumption of assets, young adults often lack the opportunity to have acquired such assets (11,12) and have historically faced health insurance uncertainty (13).

To explore and alleviate current financial distress and hardship among young adult cancer survivors, we developed a multisite, 6-month, fully remote, hybrid effectiveness-implementation study (14). Linendoll et al. (14) previously described the study’s design, including the United States (US) Health Insurance Portability and Accountability Act–compliant Research Electronic Data Capture (REDCap) (15,16) web-based study database; aims; assessment schedule; and the 3-arm randomized financial navigation intervention. The study’s primary outcome measure, the Personal Financial Wellness Scale (17), was used to measure financial distress. The Personal Financial Wellness Scale has demonstrated an association of higher financial distress among younger aged cancer survivors (18-20). This report highlights the financial late effects of the assembled young adult survivors of blood cancer cohort at study entry, describing factors associated with financial distress. We hypothesized that vulnerable participants (eg, traditionally underrepresented racial and ethnic groups) would report greater financial distress. We also present medical financial hardship domains by categorical financial distress level to identify areas of particular concern.

Methods

Assembling the cohort

Enrollment spanned from February 2022 through April 2023, with recruitment staggered across 6 US hospitals. Tufts Medical Center (Tufts Institutional Review Board [IRB] No. 00001828; ClinicalTrials.gov identifier NCT05620979) served as the central site, managing the study database and performing all enrollment, assessment, and intervention procedures (14). Each recruitment site had dedicated young adult champions and served diverse and often underrepresented populations, defined by race, ethnicity, socioeconomic demographics, or geography.

Sites screened their clinic database or the electronic health record for off-treatment young adult patients who had been diagnosed with a blood cancer. Sites then shared IRB-approved information about the study that contained a survey link to the eligibility checklist embedded in the study database. Interested young adults had to confirm that they were 18 to 39 years of age and had been diagnosed with blood cancer more than 3 years previously. They had to identify site of care and whether they had been diagnosed when they were younger or older than 18 years of age as well as confirm that they had completed treatment or were on a long-term oral medication. If the young adult checked that they had been diagnosed with another cancer, they were eligible to participate if treatment for the second cancer had been completed or they were taking an oral anticancer medication. The ability to read and understand English and having a primary residence in the US were also required. Young adults were not eligible if they were on their parent’s medical insurance. This exclusion criterion was based on concerns that the participant would be less knowledgeable and more financially protected with regard to insurance coverage and its costs (14). If all eligibility criteria were met, the central study team shared the informed consent form electronically. If the form was not signed after 2 prompts, the contact information was deleted.

Measure dissemination and variables

After provision of consent, an email or text message with a unique survey link to the baseline measures was sent from the study database. Questions were programmed to be optional, enabling participants to skip questions or stop at any time. Participants were sent a $25 electronic gift card as remuneration upon completion of the primary outcome measure. Up to 2 automated reminders were sent if the assessment was not completed. A final attempt to capture the Personal Financial Wellness Scale was made by phone. If this attempt was unsuccessful, the participant was withdrawn.

Established scoring algorithms were used for validated measures, including instructions about the handling of missing data. Analyses of the 8-item Personal Financial Wellness Scale were categorized based on previous reports (17,20), as follows: severe (ie, overwhelming to extremely high financial distress), 1 to 2; high (ie, very high to high financial distress), 3 to 4; average (ie, average to moderate financial distress), 5 to 6; and low to no financial distress, 7 to 10.

Self-reports of medical interventions beyond frontline therapy and associated with higher costs were combined to create an indicator for adverse clinical features. These features included a history of relapse or salvage therapy, receipt of hematopoietic stem cell transplant, receipt of cellular therapy (ie, chimeric antigen receptor T-cell therapy), or currently taking an oral anticancer medication. Similarly, engagement with mental health care was identified by affirmative responses to seeing or seeking a mental health professional or taking a medication for anxiety or depression.

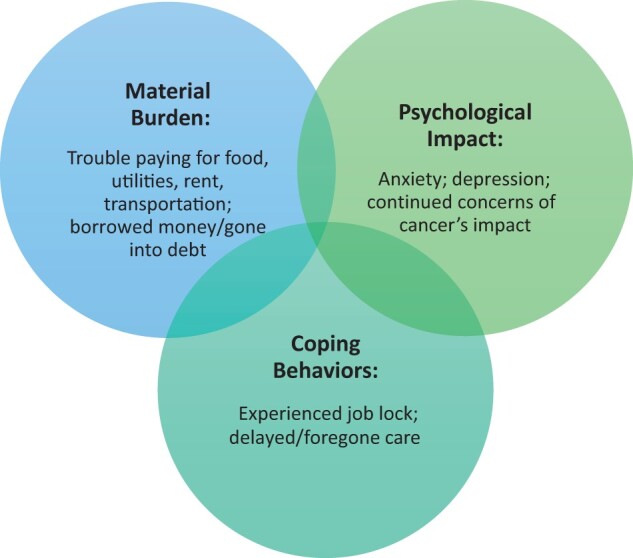

The variables used to describe the 3 domains of medical financial hardship are illustrated in Figure 1. The first domain, material hardship, was defined according to 4 household material challenges—food, utility, rent or mortgage, and transportation (21,22)—experienced over the prior 12 months. Food insecurity was defined as food not lasting often or sometimes. Financial assistance, such as a history of borrowing money or going into debt (23) or receiving financial support within the prior year was also captured. The second domain, psychological impact, was described by scores obtained from 6 Patient-Reported Outcomes Measurement Information System (PROMIS) validated short forms: 1) physical function, 2) fatigue, 3) anxiety, 4) depression, 5) emotional support, and 6) general efficacy, plus the Quality of Life in Neurological Disorders (Neuro-QoL) applied cognition instrument (14,24). Additional items regarding the perceived impact of cancer on education or employment and concern that cancer would limit earnings (23) were also included within this domain. The third domain, coping behaviors, was examined by the participants’ decision to stay at their job to keep insurance (23) or modified (ie, delayed, forewent, or changed) survivorship care utilization because of cost (23). Coping behavior items regarding care utilization from the 2017 Medical Expenditure Panel Survey (23) were adapted to focus on current survivorship experiences.

Figure 1.

Domains of medical financial hardship exploreda. aDiagram Inspiration from (5).

Statistical analysis

Analyses were restricted to participants who completed the Personal Financial Wellness Scale and demographic measures. Summary statistics (eg, means [standard deviation, SDs], frequencies [percentiles]) were used to describe demographic characteristics and medical history for the entire sample. To identify differences in distress, these variables were then summarized by categorical Personal Financial Wellness Scale score. Because there has been limited use of the Personal Financial Wellness Scale in young adult cancer populations (19), we calculated Cronbach ɑlpha as a measure of internal consistency reliability (>.8 is acceptable for established scales) (25,26). We hypothesized that younger age, female sex, non-White race or Hispanic ethnicity, lower education, lower household income, having public insurance, and adverse clinical features would be associated with greater distress on the Personal Financial Wellness Scale scores. To test these relationships, we fit univariable linear regression models and a multivariable linear regression model that included all these variables. Models were restricted to participants with complete data; model assumptions, including linearity, were assessed. Finally, we used summary statistics to describe the 3 domains of medical financial hardship by categorical Personal Financial Wellness Scale score. To understand differences in psychological impact reported on PROMIS or Neuro-QoL scales by Personal Financial Wellness Scale category, we relied on the measures’ previously established minimal important difference (ie, 1/3-1/2 the SD of 10 or 3-5 units), depending on the particular scale and methods used to estimate it (27-30). A 2-sided ɑlpha of .05 was used, and analyses were performed in SAS Enterprise Guide, version 8.1, software (SAS Institute Inc, Cary, NC).

Results

Assembling the cohort

Of the 363 eligibility checklists submitted (Figure 2), 59% were eligible to participate. The remaining submitters were not eligible (30%), provided duplicate submissions (4%), or did not provide contact information (7%). The most common ineligible responses, not mutually exclusive, were coverage through a parent’s or guardian’s insurance (45%), being in active treatment (21%), and within 3 years of initial diagnosis (13%). The informed consent form was signed by 71% of eligible young adults, of whom 83% completed baseline measures. The analytic cohort consisted of 126 participants.

Figure 2.

Study analytic cohort CONSORT diagram.

Study sample

The mean (SD) age of the cohort was 30.4 (5.2) years, 60.8% of the cohort were female, and 55.5% were either Hispanic (32.5%) or non-Hispanic non-White (22.0%) (Table 1). Fifty-six percent of the sample had been diagnosed between the ages of 18 and 39 years; the remainder were diagnosed at younger than 18 years of age. The median time since diagnosis was 10 years (interquartile range [IQR] = 6-16 years). Lymphoma (Hodgkin or non-Hodgkin) was the most common diagnosis (54.0%), followed by leukemia (46.0%, acute or chronic); 37.3% of participants were characterized as having adverse clinical features; and 54.4% reported engagement with mental health care. Although most participants (79%) resided in the same state as their site of care (ie, California, Texas, South Carolina, Massachusetts), the overall cohort was drawn from 18 states.

Table 1.

Baseline demographic characteristics and medical history, by categorical Personal Financial Wellness Scale scorea

| Characteristic | All participants | Severe distress (score 1-2) | High distress (score 3-4) | Average distress (score 5-6) | Low to no distress (score 7-10) |

|---|---|---|---|---|---|

| Total, No. (%) | 126 (100) | 26 (20.6) | 36 (28.6) | 33 (26.2) | 31 (24.6) |

| Demographic characteristics | |||||

| Current age, mean y, (SD) | 30.4 (5.2) | 30.0 (5.5) | 30.3 (5.1) | 29.6 (4.8) | 31.8 (5.3) |

| Female sex, No. (%) | 76 (60.3) | 19 (73.1) | 26 (74.3) | 16 (48.5) | 15 (48.4) |

| Race or ethnicity, No. (%) | |||||

| Hispanic | 40 (32.5) | 12 (48.0) | 15 (44.1) | 8 (24.2) | 5 (16.1) |

| Non-Hispanic non-White | 27 (22.0) | 6 (24.0) | 8 (23.5) | 6 (18.2) | 7 (22.6) |

| Non-Hispanic White | 56 (45.5) | 7 (28.0) | 11 (32.4) | 19 (57.6) | 19 (61.3) |

| Currently partnered, No. (%) | 81 (65.3) | 12 (48.0) | 21 (60.0) | 27 (81.8) | 21 (67.7) |

| Dependent children, No. (%) | 46 (36.8) | 8 (30.8) | 14 (40.0) | 14 (42.4) | 10 (32.3) |

| Highest level of education, No. (%) | |||||

| <4-y college degree | 45 (36.3) | 14 (56.0) | 17 (48.6) | 9 (27.3) | 5 (16.1) |

| 4-y college degree or more | 79 (63.7) | 11 (44.0) | 18 (51.4) | 24 (72.7) | 26 (83.9) |

| Currently a student, No. (%) | 26 (21.3) | 8 (32.0) | 10 (28.6) | 2 (6.3) | 6 (20.0) |

| Currently employed, No. (%) | 103 (82.4) | 18 (69.2) | 26 (74.3) | 30 (90.9) | 29 (93.6) |

| Total income, No. (%) | |||||

| <$20 000 | 34 (28.8) | 10 (41.7) | 14 (41.2) | 4 (13.8) | 6 (19.4) |

| $20 000-$39 999 | 22 (18.6) | 7 (29.2) | 5 (14.7) | 8 (27.6) | 2 (6.5) |

| $40 000-$79 999 | 26 (22.0) | 6 (25.0) | 10 (29.4) | 9 (31.0) | 1 (3.2) |

| ≥$80 000 | 36 (30.5) | 1 (4.2) | 5 (14.7) | 8 (27.6) | 22 (71.0) |

| Type of insurance, No. (%) | |||||

| Private | 81 (64.8) | 14 (53.9) | 16 (45.7) | 25 (75.8) | 26 (83.9) |

| Any public | 40 (32.0) | 12 (46.2) | 16 (45.7) | 7 (21.2) | 5 (16.1) |

| Other/uninsured | 4 (3.2) | 0 (0.0) | 3 (8.6) | 1 (3.0) | 0 (0.0) |

| Medical history | |||||

| Age at diagnosis, No. (%) | |||||

| ≤17 y | 56 (44.4) | 11 (42.3) | 16 (44.4) | 18 (54.6) | 11 (35.5) |

| 18-39 y | 70 (55.6) | 15 (57.7) | 20 (55.6) | 15 (45.5) | 20 (64.5) |

| Time since diagnosis, median y, (Interquartile range) | 10 (6-16) | 10 (6-13) | 9 (5-14) | 11 (8-15) | 10 (5-18) |

| Diagnosis,b No. (%) | |||||

| Leukemia (including acute and chronic) | 57 (46.0) | 14 (53.9) | 18 (50.0) | 17 (51.5) | 8 (27.6) |

| Lymphoma (including Hodgkin and non-Hodgkin) | 67 (54.0) | 12 (46.2) | 18 (50.0) | 16 (48.5) | 21 (72.4) |

| Adverse clinical features,c No. (%) | 47 (37.3) | 12 (46.2) | 12 (33.3) | 14 (42.4) | 9 (29.0) |

| Relapse/treatment failure | 26 (20.8) | 9 (34.6) | 3 (8.6) | 8 (24.2) | 6 (19.4) |

| Hematopoietic stem cell transplant | 35 (28.0) | 11 (42.3) | 8 (22.9) | 10 (30.3) | 6 (19.4) |

| Treated with cellular therapy | 14 (11.2) | 1 (3.9) | 4 (11.4) | 5 (15.2) | 4 (12.9) |

| Currently taking oral anticancer medication | 4 (3.2) | 0 (0.0) | 1 (2.9) | 2 (6.1) | 1 (3.2) |

| Mental health care,d No. (%) | 68 (54.4) | 22 (88.0) | 17 (47.2) | 15 (45.5) | 14 (45.2) |

Item-level missingness may result in fewer responses than the column number indicates.

Two participants with other blood cancer diagnoses are not listed here, given cell size suppression.

Adverse clinical features includes relapse or treatment failure, hematopoietic stem cell transplant, treatment with cellular therapy (ie, chimeric antigen receptor T-cell therapy), or currently taking oral anticancer medication.

Responded yes to at least 1 of the following: seeing mental health professional, looking for mental health professional, or taking medication for anxiety or depression.

Financial distress

The overall mean (SD) summary score of the Personal Financial Wellness Scale was 5.1 (2.4). The Cronbach ɑlpha for the total scale was .94, demonstrating excellent internal consistency. When categorizing Personal Financial Wellness Scale results, 20.6% of participants were severely distressed (scores 1-2), 28.6% were highly distressed (scores 3-4), 26.2% were average (scores 5-6), and 24.6% reported low to no financial distress (scores 7-10).

Factors associated with financial distress

As hypothesized, female sex and Hispanic ethnicity were associated in univariable analysis with lower Personal Financial Wellness Scale scores (ie, worse distress), whereas higher education, being employed, higher income, and private insurance were associated with better Personal Financial Wellness Scale scores (ie, less distress) (Table 2). In multivariable analysis, adjusting for other factors, female sex, Hispanic ethnicity, and higher income remained strongly associated with Personal Financial Wellness Scale scores. Specifically, female participants had worse financial distress than male participants (β = ‒0.9, Standard Error [SE] = 0.4, P = .04), Hispanic participants had worse financial distress than non-Hispanic White participants (β = ‒1.1, SE = 0.5, P = .03), and participants with higher incomes had less financial distress than participants with incomes below $20 000 per year (β = 2.6, SE = 0.7, P < .01).

Table 2.

Univariable and multivariable linear regression model for factors associated with financial distress, by Personal Financial Wellness Scale score, n = 115a

| Univariable model |

Multivariable model |

|||

|---|---|---|---|---|

| β (SE) | P b | β (SE) | P c | |

| Current age, y | 0.1 (0.1) | .25 | ‒0.1 (0.1) | .33 |

| Female sex | ‒1.3 (0.5) | .01 | ‒0.9 (0.4) | .04 |

| Race or ethnicity | ||||

| Hispanic | ‒2.0 (0.5) | <.01 | ‒1.1 (0.5) | .03 |

| Non-Hispanic non-White | ‒0.7 (0.6) | .20 | ‒0.7 (0.5) | .18 |

| Non-Hispanic White | (Referent) | — | — | — |

| Highest level of education | ||||

| <4-y of college | (Referent) | — | — | — |

| ≥4-y college degree | 1.8 (0.5) | <.01 | 0.8 (0.4) | .07 |

| Currently employed | 2.0 (0.6) | <.01 | 0.9 (0.6) | .11 |

| Total income | ||||

| <$20 000 | (Referent) | — | — | — |

| $20 000-$39 999 | 0.2 (0.6) | .77 | 0.3 (0.6) | .67 |

| $40 000-$79 999 | 0.2 (0.5) | .76 | 0.2 (0.6) | .71 |

| ≥$80 000 | 3.2 (0.5) | <.01 | 2.6 (0.7) | <.01 |

| Type of insurance | ||||

| Private | 1.5 (0.5) | <.01 | ‒0.4 (0.5) | .41 |

| Any public/other/uninsured | (Referent) | — | — | — |

| Years since diagnosis | ||||

| <10 | (Referent) | — | — | — |

| ≥10 | 0.3 (0.5) | .53 | ‒0.2 (0.4) | .68 |

| Adverse clinical features | ||||

| Absent | (Referent) | — | — | — |

| Present | ‒0.7 (0.5) | .14 | ‒0.7 (0.4) | .11 |

Restricted to participants with complete data on all these variables.

Global P values for categorical variables in univariable analysis: race or ethnicity <.01, total income <.01.

Global P values for categorical variables in multivariable analysis: race or ethnicity = .18, total income <.01.

Medical financial hardship: material burden

Household material hardship over the prior 12 months was endorsed by 43.6% of the sample (21.0% with 1 insecurity; 22.6% with ≥2 insecurities) (Table 3). The most often endorsed type of household material hardship was food insecurity (33.9%). Among participants who reported severe financial distress, 72.0% had 2 or more household material hardships (compared with 0.0% in the low to no financial distress group). Of the entire sample, more than one-third (36.6%) had borrowed money or gone into debt at some point or had received financial support (39.2%) within the previous year. In addition, 64.0% of participants who reported severe financial distress had borrowed money or gone into debt (compared with 16.1% in the low to no distress group).

Table 3.

Material hardship, by categorical Personal Financial Wellness Scale scorea

| All participants, No. (%) | Severe distress (score 1-2), No. (%) | High distress (score 3-4), No. (%) | Average distress (score 5-6), No. (%) | Low to no distress (score 7-10), No. (%) | |

|---|---|---|---|---|---|

| Total | 126 (100) | 26 (20.6) | 36 (28.6) | 33 (26.2) | 31 (24.6) |

| Household material hardship | |||||

| No. of household material hardships in past 12 mo | |||||

| None | 70 (56.5) | 1 (4.0) | 16 (45.7) | 23 (69.7) | 30 (96.8) |

| 1 | 26 (21.0) | 6 (24.0) | 10 (28.6) | 9 (27.3) | 1 (3.2) |

| ≥2 | 28 (22.6) | 18 (72.0) | 9 (25.7) | 1 (3.0) | 0 (0.0) |

| Food insecurityb | 42 (33.9) | 21 (84.0) | 13 (37.1) | 8 (24.2) | 0 (0.0) |

| Utility insecurity | 12 (9.8) | 8 (32.0) | 3 (8.8) | 0 (0.0) | 1 (3.2) |

| Rent/mortgage insecurity | 24 (19.5) | 15 (60.0) | 9 (25.7) | 0 (0.0) | 0 (0.0) |

| Lack of reliable transportation | 15 (12.1) | 8 (32.0) | 4 (11.4) | 3 (9.1) | 0 (0.0) |

| Financial assistance | |||||

| Ever borrowed money or gone into debt | 45 (36.6) | 16 (64.0) | 14 (41.2) | 10 (30.3) | 5 (16.1) |

| Family ever borrowed money or gone into debt | 34 (27.4) | 10 (40.0) | 15 (42.9) | 7 (21.2) | 2 (6.5) |

| Received any financial support to help pay for cancer survivorship care or living expenses in the past 12 mo | 49 (39.2) | 14 (53.9) | 14 (40.0) | 12 (36.4) | 9 (29.0) |

Item-level missingness may result in fewer responses than the column number indicates.

Food not lasting “often true” or “sometimes true” collapsed as insecurity.

Medical financial hardship: psychological impact

Although most of the overall sample’s mean PROMIS and Neuro-QoL scores were similar to the US general population average (SD) score of 50 (10), the mean [SD] anxiety domain score (55.2 [10.3]) (Table 4) was half an SD higher (ie, worse anxiety), equal to the minimal important difference. Participants with higher levels of financial distress reported worse scores across all domains. Comparing the severe financial distress group with the low to no distress group on negatively worded domains, mean (SD) scores for fatigue were 58.2 (9.5) vs 44.7 (7.9); for anxiety, they were 64.6 (9.5) vs 48.1 (7.9); and for depression, they were 59.0 (10.7) vs 45.7 (6.0). For each of these comparisons, the magnitude of difference between PROMIS scores was greater than a full SD difference. The same pattern was seen in the positively worded domains, with comparable magnitudes of difference between the severe and low to no financial distress groups. Specifically, participants with severe financial distress reported lower mean [SD] levels of physical function (46.5 [6.2]) vs 56.1 [2.9]), less emotional support (50.5 [9.0] vs 57.7 [6.0]), lower general self-efficacy (46.1 [10.0] vs 56.0 [8.3]), and worse cognitive function (47.4 [8.9] vs 54.5 [7.6]) compared with the low to no distress group.

Table 4.

Psychological impact, by categorical Personal Financial Wellness Scale scorea

| Characteristic | All participants | Severe distress (score 1-2) | High distress (score 3-4) | Average distress (score 5-6) | Low to no distress (score 7-10) |

|---|---|---|---|---|---|

| Total, No. (%) | 126 (100) | 26 (20.6) | 36 (28.6) | 33 (26.2) | 31 (24.6) |

| PROMIS/Neuro-QoL domain, mean (SD) b | |||||

| Physical function | 51.3 (6.7) | 46.5 (6.2) | 50.0 (6.7) | 52.0 (6.7) | 56.1 (2.9) |

| Fatiguec | 50.7 (9.9) | 58.2 (9.5) | 52.0 (9.3) | 49.2 (8.8) | 44.7 (7.9) |

| Anxietyc | 55.2 (10.3) | 64.6 (9.5) | 56.3 (9.4) | 53.5 (8.0) | 48.1 (7.9) |

| Depressionc | 50.6 (10.0) | 59.0 (10.7) | 51.7 (10.2) | 47.8 (8.3) | 45.7 (6.0) |

| Emotional support | 53.9 (8.2) | 50.5 (9.0) | 52.2 (7.9) | 54.9 (8.4) | 57.7 (6.0) |

| General self-efficacy | 51.1 (9.7) | 46.1 (10.0) | 50.1 (9.9) | 51.6 (8.4) | 56.0 (8.3) |

| Cognition function | 51.6 (8.2) | 47.4 (8.9) | 51.5 (7.8) | 52.3 (7.5) | 54.5 (7.6) |

| Ongoing perception of cancer’s impact, No. (%) | |||||

| Cancer impacts on education/employment | |||||

| No impact | 66 (53.6) | 4 (16.0) | 18 (51.4) | 23 (71.9) | 21 (67.7) |

| Impact on education only | 11 (8.9) | 6 (24.0) | 1 (2.9) | 2 (6.3) | 2 (6.5) |

| Impact on employment only | 27 (22.0) | 8 (32.0) | 8 (22.9) | 4 (12.5) | 7 (22.6) |

| Impact on education and employment | 19 (15.5) | 7 (28.0) | 8 (22.9) | 3 (9.4) | 1 (3.2) |

| Concerned that cancer would limit earnings | 57 (46.0) | 14 (56.0) | 23 (65.7) | 13 (39.4) | 7 (22.6) |

Item-level missingness may result in fewer responses than the column number indicates. PROMIS = Patient-Reported Outcomes Measurement Information System; Neuro-QoL = Quality of Life in Neurological Disorders.

PROMIS and Neuro-QoL scores are standardized to have mean (SD) of 50 (10).

Higher scores indicate worse-than-average responses for negatively worded concepts (ie, greater fatigue, greater anxiety, greater depression).

Nearly half the participants (46.4%) endorsed that cancer continued to affect their education or employment. The perceived impact was greater among individuals in the severe distress group than individuals in the low to no distress group (84.0% vs 32.3%). Similarly, 46.0% of the sample were concerned that cancer would limit their earnings, with higher levels of concern in the severe (56.0%) and high (65.7%) distress groups than in the low to no distress (22.6%) group.

Medical financial hardship: coping behaviors

Many (29.6%) participants endorsed staying at their job to keep insurance (Table 5). Nearly half the sample (44.8%) reported making a decision (eg, delay) within the previous year that affected their survivorship care because of cost, with specialist care being the most commonly affected (32.0%). Making this decision because of the cost of care was more commonly reported by the severe (68.0%) and high (63.9%) distress groups than the low to no (16.1%) distress group. Individuals in the severe distress category (60.0%) were more likely to have delayed or forgone mental health-care services than any other type of care.

Table 5.

Coping behaviors, by categorical Personal Financial Wellness Scale scorea

| Characteristic | All participants, No. (%) | Severe distress (score 1-2), No. (%) | High distress (score 3-4), No. (%) | Average distress (score 5-6), No. (%) | Low to no distress (score 7-10), No. (%) |

|---|---|---|---|---|---|

| Total | 126 (100) | 26 (20.6) | 36 (28.6) | 33 (26.2) | 31 (24.6) |

| Stayed at job to keep insurance | 37 (29.6) | 8 (30.8) | 10 (28.6) | 11 (33.3) | 8 (25.8) |

| Changed cancer survivorship care because of cost in the past 12 mo | |||||

| Any survivorship careb | 56 (44.8) | 17 (68.0) | 23 (63.9) | 11 (33.3) | 5 (16.1) |

| Tests | 26 (20.8) | 6 (24.0) | 12 (33.3) | 6 (18.2) | 2 (6.5) |

| Specialist visits | 40 (32.0) | 10 (40.0) | 19 (52.8) | 8 (24.2) | 3 (9.7) |

| Prescription medication | 15 (12.0) | 4 (16.0) | 7 (19.4) | 4 (12.1) | 0 (0.0) |

| Other (nonprescription) treatment | 19 (15.3) | 8 (32.0) | 8 (22.9) | 3 (9.1) | 0 (0.0) |

| Mental health care | 28 (22.4) | 15 (60.0) | 8 (22.2) | 3 (9.1) | 2 (6.5) |

| Other changes | 7 (5.8) | 1 (4.2) | 3 (8.3) | 3 (9.4) | 0 (0.0) |

Item-level missingness may result in fewer responses than the column number indicates.

Any survivorship care: Responded yes to at least 1 of the following: tests, specialist visits, prescription medication, other (nonprescription) treatment, mental health care, or other.

Discussion

We sought to characterize financial distress and medical financial hardship among a broadly assembled young adult blood cancer survivor cohort. Recruitment at the 6 diverse young adult clinical programs successfully resulted in a cohort of 54.5% individuals from minority racial or ethnic groups, who were a median of 10 years from initial diagnosis. Financial distress, as self-reported on the Personal Financial Wellness Scale, was broadly distributed across the full range of the measure’s scale, from severe to no distress. In particular, 49% of our young adult participants reported severe or high financial distress vs the previously reported 30% of the general noncancer adult population (17). In multivariable linear regression analysis, female sex and Hispanic ethnicity were associated, as hypothesized, with more financial distress, as was lower income. Participants who reported severe or high financial distress reported experiencing higher levels of medical financial hardship, defined by greater material hardship and psychological impact, and demonstrated concerning coping behaviors compared with young adults who had less financial distress.

More than one-third (33.9%) of the overall sample reported food insecurity. Individuals with severe or high levels of financial distress reported substantial material hardship. Over the prior year, 84.0% of severely financially distressed participants reported food insecurity, and 60.0% reported rent or mortgage insecurity. A substantial proportion of participants who reported severe distress had directly borrowed some amount of money (64.0%) or reported that their family had borrowed money or gone into debt (40.0%). Ketterl et al. (31) found that 14.4% of young adults or their families had borrowed $10 000 or more in their study. An impact on finances within the previous year was felt by 53.9% of severely distressed, 40.0% of high distressed, and 36.4% of average distressed participants who needed financial support to help pay for survivorship care or living expenses.

Greater rates of fatigue, anxiety, and depression were reported by young adults in the severe and high financial distress groups compared with their counterparts with less financial distress. They also reported worse physical function, emotional support, general self-efficacy, and cognitive function than participants with average and low to no financial distress, based on minimal important difference estimates for between-group differences. Of further concern, despite the median decade that had passed since diagnosis, cancer continued to have a perceived negative impact on work and/or school for nearly half the cohort (46.4%).

A similar proportion of participants in all distress groups (severe, 30.8%; high, 28.6%; average, 33.3%; low to no, 25.8%) reported job lock, defined as remaining in an employment position to retain insurance benefits. This phenomenon has previously been described in cancer survivor cohorts (32-34). The significant proportion (>60%) of young adults with severe or high levels of financial distress who reported an impact on their cancer survivorship care because of cost within the previous year is worrisome. Survivors should be educated about potential treatment late effects and be engaged in long-term care per oncologic guidelines—of particular importance for the participants with adverse clinical features (37.3%) because their treatment indicates greater need for ongoing care, but this care may then put them at increased risk for additional medical debt. Participants with severe financial distress were more likely to report engagement with mental health care (88.0%) but strikingly were also more likely to have delayed or foregone that care (60.0%). Mental health concerns have been well documented in young adult cancer survivors (35-37). For young adults who have a mental health-care professional or are taking medication but cannot sustain these costs, this translates to inadequate mental health care. Interestingly, participants who reported high financial distress reported greater impact on their survivorship care in the areas of testing, specialist visits, and prescription medication than any other distress group. Participants in low to no financial distress were much less likely to report an impact on care utilization.

We acknowledge lessons learned in our recruitment process and limitations in this study. Local recruitment site IRBs had divergent determination about their role in this centrally managed, fully remote study, ranging from the request for full review to decline of review (as not human subject research), which affected the rollout of the study. Importantly, the study was developed and implemented during the COVID-19 pandemic, which potentially had both positive (eg, familiarity with tele-connection) and negative impacts (eg, additional stressors, such as furloughed study staff, more limited access to care for participants).

Given our aim to explore and alleviate financial distress through a financial navigation intervention in a young adult survivor cohort, eligibility criteria were mainly confined to treatment history and independent insurance coverage. Even when casting this wide net, close to half of young adults reported severe or high financial distress. Participants who reported severe or high financial distress also described more medical financial hardship than their less distressed counterparts.

Results of our 6-month intervention will be shared because it is imperative to understand the range of financial issues that survivors are dealing with and what steps, if any, they have taken to mitigate the impact. The status of participants at study entry provides a sobering snapshot of financial distress among young adult survivors. These findings highlight the ongoing need to investigate and address the financial late effects of cancer to optimize the outcomes for this vulnerable population.

Acknowledgements

No funding sources participated in the collection, analysis, interpretation of data, or the writing of the manuscript. The content is solely the responsibility of the authors and does not necessarily represent the official views of any funding source.

Ethics approval statement: Approval was granted by the Tufts Health Sciences IRB in the fall of 2021 (STUDY 00001828). The protocol was reviewed by all participating recruitment sites, with reliance agreements executed as applicable by local IRB determination.

Patient consent statement: Informed consent was obtained from all participants included in the study.

Contributor Information

Susan K Parsons, Division of Hematology and Oncology and Institute for Clinical Research and Health Policy Studies, Tufts Medical Center, Boston, MA, USA.

Rachel Murphy-Banks, Division of Hematology and Oncology and Institute for Clinical Research and Health Policy Studies, Tufts Medical Center, Boston, MA, USA.

Angie Mae Rodday, Institute for Clinical Research and Health Policy Studies, Tufts Medical Center, Boston, MA, USA.

Michael E Roth, Department of Pediatrics Patient Care, Division of Pediatrics, The University of Texas MD Anderson Cancer Center, Houston, TX, USA.

Kimberly Miller, Department of Population and Public Health Sciences, Keck School of Medicine of the University of Southern California, Los Angeles, CA, USA.

Nadine Linendoll, Division of Hematology and Oncology and Institute for Clinical Research and Health Policy Studies, Tufts Medical Center, Boston, MA, USA.

Randall Chan, Department of Pediatrics, Los Angeles General Medical Center, Los Angeles, CA, USA.

Howland E Crosswell, AYA Cancer Care Program, Bon Secours Mercy, St Francis Cancer Center, Greenville, SC, USA.

Qingyan Xiang, Institute for Clinical Research and Health Policy Studies, Tufts Medical Center, Boston, MA, USA.

David R Freyer, Departments of Pediatrics, Medicine, and Population and Public Health Sciences, Cancer and Blood Disease Institute, Children’s Hospital Los Angeles & University of Southern California Norris Comprehensive Cancer Center, Los Angeles, CA, USA.

Data availability

The data underlying this article are available in the article.

Author contributions

Susan K. Parsons, MD, MRP (Conceptualization; Formal analysis; Funding acquisition; Investigation; Methodology; Project administration; Resources; Supervision; Validation; Visualization; Writing—original draft; Writing—review & editing); Rachel Murphy-Banks, MA (Conceptualization; Investigation; Methodology; Project administration; Resources; Supervision; Validation; Visualization; Writing—original draft; Writing—review & editing); Angie Mae Rodday, PhD, MS (Conceptualization; Data curation; Formal analysis; Investigation; Methodology; Visualization; Writing—review & editing); Michael E. Roth, MD (Resources; Writing—review & editing); Kimberly Miller, PhD, MPH (Resources; Writing—review & editing); Nadine Linendoll, PhD, MDiv, GNP (Writing—review & editing); Randall Chan, MD (Resources; Writing—review & editing); Howland E. Crosswell, MD (Resources; Writing—review & editing); Qingyan Xiang, PhD (Data curation; Writing—review & editing); David R. Freyer, DO, MS (Resources; Writing—review & editing).

Funding

This work was supported by the Leukemia & Lymphoma Society (award No. PHS9005-21). The project used Research Electronic Data Capture (REDCap) for data management (National Center for Advancing Translational Sciences, National Institutes of Health, grant No. UL1TR002544). Dr Freyer was supported in part by the National Cancer Institute (grant No. P30CA014089).

Conflicts of interest

The authors have no conflicts of interest.

References

- 1. Zafar SY, Peppercorn JM, Schrag D, et al. The financial toxicity of cancer treatment: a pilot study assessing out-of-pocket expenses and the insured cancer patient's experience. Oncologist. 2013;18(4):381-390. doi: 10.1634/theoncologist.2012-0279 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2. Lentz R, Benson AB 3rd, Kircher S.. Financial toxicity in cancer care: prevalence, causes, consequences, and reduction strategies. J Surg Oncol. 2019;120(1):85-92. doi: 10.1002/jso.25374 [DOI] [PubMed] [Google Scholar]

- 3. O'Connor JM, Kircher SM, de Souza JA.. Financial toxicity in cancer care. J Community Support Oncol. 2016;14(3):101-106. doi: 10.12788/jcso.0239 [DOI] [PubMed] [Google Scholar]

- 4. Zafar SY, Abernethy AP.. Financial toxicity, Part I: a new name for a growing problem. Oncology (Williston Park). 2013;27(2):80-149. [PMC free article] [PubMed] [Google Scholar]

- 5. Altice CK, Banegas MP, Tucker-Seeley RD, Yabroff KR.. Financial hardships experienced by cancer survivors: a systematic review. J Natl Cancer Inst. 2017;109(2):djw205. doi: 10.1093/jnci/djw205 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6. Pisu M, Martin MY.. Financial toxicity: a common problem affecting patient care and health. Nat Rev Dis Primers. 2022;8(1):7. doi: 10.1038/s41572-022-00341-1 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7. Nathan PC, Huang IC, Chen Y, et al. Financial hardship in adult survivors of childhood cancer in the era after implementation of the Affordable Care Act: a report from the Childhood Cancer Survivor Study. J Clin Oncol. 2022;41(5):1000-1010. doi: 10.1200/JClinOncol.22.00572 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8. Chao C, Bhatia S, Xu L, et al. Chronic comorbidities among survivors of adolescent and young adult cancer. J Clin Oncol. 2020;38(27):3161-3174. doi: 10.1200/JClinOncol.20.00722 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 9. Gegechkori N, Haines L, Lin JJ.. Long-term and latent side effects of specific cancer types. Med Clin North Am. 2017;101(6):1053-1073. doi: 10.1016/j.mcna.2017.06.003 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10. Kayser K, Smith L, Washington A, Harris LM, Head B.. Living with the financial consequences of cancer: a life course perspective. J Psychosoc Oncol. 2021;39(1):17-34. doi: 10.1080/07347332.2020.1814933 [DOI] [PubMed] [Google Scholar]

- 11. Zheng Z, Jemal A, Han X, et al. Medical financial hardship among cancer survivors in the United States. Cancer. 2019;125(10):1737-1747. doi: 10.1002/cncr.31913 [DOI] [PubMed] [Google Scholar]

- 12. Lu AD, Zheng Z, Han X, et al. Medical financial hardship in survivors of adolescent and young adult cancer in the United States. J Natl Cancer Inst. 2021;113(8):997-1004. doi: 10.1093/jnci/djab013 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13. Parsons SK, Kumar AJ.. Adolescent and young adult cancer care: financial hardship and continued uncertainty. Pediatr Blood Cancer. 2019;66(4):e27587. doi: 10.1002/pbc.27587 [DOI] [PubMed] [Google Scholar]

- 14. Linendoll N, Murphy-Banks R, Sae-Hau M, et al. Evaluating the role of financial navigation in alleviating financial distress among young adults with a history of blood cancer: a hybrid type 2 randomized effectiveness-implementation design. Contemp Clin Trials. 2023;124:107019. doi: 10.1016/j.cct.2022.107019 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 15. Harris PA, Taylor R, Thielke R, Payne J, Gonzalez N, Conde JG.. Research electronic data capture (REDCap)—a metadata-driven methodology and workflow process for providing translational research informatics support. J Biomed Inform. 2009;42(2):377-381. doi: 10.1016/j.jbi.2008.08.010 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16. Harris PA, Taylor R, Minor BL, et al. REDCap Consortium. The REDCap consortium: Building an international community of software platform partners. J Biomed Inform. 2019;95:103208. doi: 10.1016/j.jbi.2019.103208 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17. Prawitz AD, Garman ET, Sorhaindo B, O'Neill B, Kim J, Drentea P.. Incharge financial distress/financial well-being scale: development, administration, and score interpretation. Financ Counsel Plan. 2006;17(1):34-50. doi: 10.1037/t60365-000 [DOI] [Google Scholar]

- 18. Meeker CR, Wong YN, Egleston BL, et al. Distress and financial distress in adults with cancer: an age-based analysis. J Natl Compr Canc Netw. 2017;15(10):1224-1233. doi: 10.6004/jnccn.2017.0161 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19. D’Rummo KA, Nganga D, Chollet-Hinton L, Shen X.. Comparison of two validated instruments to measure financial hardship in cancer survivors: comprehensive score for financial toxicity (COST) versus personal financial wellness (PFW) scale. Support Care Cancer. 2022;31(1):12. doi: 10.1007/s00520-022-07455-y [DOI] [PubMed] [Google Scholar]

- 20. Thom B, Friedman DN, Aviki EM, et al. The long-term financial experiences of adolescent and young adult cancer survivors. J Cancer Surviv. 2023;17(6):1813-1823. doi: 10.1007/s11764-022-01280-2 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21. Zheng DJ, Shyr D, Ma C, Muriel AC, Wolfe J, Bona K.. Feasibility of systematic poverty screening in a pediatric oncology referral center. Pediatr Blood Cancer. 2018;65(12):e27380. doi: 10.1002/pbc.27380 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22. Bona K, London WB, Guo D, Frank DA, Wolfe J.. Trajectory of material hardship and income poverty in families of children undergoing chemotherapy: a prospective cohort study. Pediatr Blood Cancer. 2016;63(1):105-111. doi: 10.1002/pbc.25762 [DOI] [PubMed] [Google Scholar]

- 23. Agency for Healthcare Research and Quality. Medical Expenditure Panel Survey (MEPS). Cancer Experiences Questionnaire; 2017. https://meps.ahrq.gov/mepsweb/survey_comp/survey_results_saq_ques.jsp?SAQ=Cancer+Experiences+Questionnaire+-+English&Year3=AllYear&Submit2=Search. Accessed April 29, 2024.

- 24. Northwestern University. Health Measures. PROMIS® Patient-Reported Outcomes Measurement System and Neuro-QoL. http://healthmeasures.net. Accessed April 29, 2024

- 25. Cronbach LJ. Coefficient alpha and the internal structure of tests. Psychometrika. 1951;16(3):297-334. [Google Scholar]

- 26. Nunnally J, Bernstein I.. Psychometric Theory. 3rd ed. New York, NY: McGraw-Hill, Inc.; 1994. [Google Scholar]

- 27. Terwee CB, Peipert JD, Chapman R, et al. Minimal important change (MIC): A conceptual clarification and systematic review of MIC estimates of PROMIS measures. Qual Life Res. 2021;30(10):2729-2754. doi: 10.1007/s11136-021-02925-y [DOI] [PMC free article] [PubMed] [Google Scholar]

- 28. Kroenke K, Stump TE, Chen CX, et al. Minimally important differences and severity thresholds are estimated for the PROMIS depression scales from three randomized clinical trials. J Affect Disord. 2020;266:100-108. doi: 10.1016/j.jad.2020.01.101 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29. Amtmann D, Kim J, Chung H, Askew RL, Park R, Cook KF.. Minimally important differences for Patient Reported Outcomes Measurement Information System pain interference for individuals with back pain. J Pain Res. 2016;9:251-255. doi: 10.2147/JPR.S93391 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 30. Bartlett SJ, Gutierrez AK, Andersen KM, et al. Identifying minimal and meaningful change in a Patient-Reported Outcomes Measurement Information System for rheumatoid arthritis: use of multiple methods and perspectives. Arthritis Care Res (Hoboken). 2022;74(4):588-597. doi: 10.1002/acr.24501 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31. Ketterl TG, Syrjala KL, Casillas J, et al. Lasting effects of cancer and its treatment on employment and finances in adolescent and young adult cancer survivors. Cancer. 2019;125(11):1908-1917. doi: 10.1002/cncr.31985 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32. Kirchhoff AC, Nipp R, Warner EL, et al. "Job lock" among long-term survivors of childhood cancer: a report from the Childhood Cancer Survivor Study. JAMA Oncol. 2018;4(5):707-711. doi: 10.1001/jamaoncol.2017.3372 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 33. Kent EE, de Moor JS, Zhao J, Ekwueme DU, Han X, Yabroff KR.. Staying at one's job to maintain employer-based health insurance among cancer survivors and their spouses/partners. JAMA Oncol. 2020;6(6):929-932. doi: 10.1001/jamaoncol.2020.0742 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34. Ghazal LV, Merriman J, Santacroce SJ, Dickson VV.. Survivors' dilemma: young adult cancer survivors' perspectives of work-related goals. Workplace Health Saf. 2021;69(11):506-516. doi: 10.1177/21650799211012675 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35. Salsman JM, Garcia SF, Yanez B, Sanford SD, Snyder MA, Victorson D.. Physical, emotional, and social health differences between posttreatment young adults with cancer and matched healthy controls. Cancer. 2014;120(15):2247-2254. doi: 10.1002/cncr.28739 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 36. De R, Sutradhar R, Kurdyak P, et al. Incidence and predictors of mental health outcomes among survivors of adolescent and young adult cancer: a population-based study using the IMPACT cohort. J Clin Oncol. 2021;39(9):1010-1019. doi: 10.1200/JClinOncol.20.02019 [DOI] [PubMed] [Google Scholar]

- 37. Husson O, Prins JB, Kaal SE, et al. Adolescent and young adult (AYA) lymphoma survivors report lower health-related quality of life compared to a normative population: results from the PROFILES registry. Acta Oncol. 2017;56(2):288-294. doi: 10.1080/0284186X.2016.1267404 [DOI] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Data Availability Statement

The data underlying this article are available in the article.