Abstract

Background

Advanced therapy medicinal products (ATMPs) are an innovative output of biomedical research, characterized by a high level of uncertainty on long-term efficacy and safety, elevated price tags and often complex administration. All these elements compounded make their European authorization, national price negotiation for reimbursement and subsequent dispensation and administration to the patient less straightforward and often less successful than for less innovative drugs. To assess if these hurdles have affected patient access and how are ATMPs used in Italy, we have analysed availability, access and expenditure of ATMPs in the period spanning from 2016 to 2023.

Methods

We have analysed real world data on the duration of ATMP regulatory evaluations for authorisation and reimbursement, time to first patient access and expenditure for ATMPs through the Italian National Health System (INHS) expenditure data flow, as well as information on patient mobility and availability of health facilities specialized in administering ATMPs.

Findings

Of the 18 ATMPs currently authorized in Europe, 9 are reimbursed by the INHS, but only 6 were actually used, generating a cumulative expenditure of roughly 300 Mln€ from 2016 to 2023, largely owing to CAR-T therapies. Time to patient access reaches an average of 340.6 days from the day publication in the official Gazette of the reimbursement decision to first patient treatment in one of the 107 health facilities authorized for ATMP administration, after an even longer evaluation time by regulatory agencies.

Conclusion

Since the first reimbursement decision for an ATMP in Italy, back in 2016, these innovative drugs became progressively more and more available, both in terms of numbers and in terms of coverage across the country. Almost all Italian regions have at least one centre for ATMP administration and has performed a treatment in 2023. Notwithstanding their high per-treatment prices, ATMPs currently have a rather contained expenditure, however it is bound to keep growing in the next few years.

Supplementary Information

The online version contains supplementary material available at 10.1007/s40259-024-00683-0.

Key Points

| The data currently available on ATMP coverage in Europe is mostly describing which products are available in the member states, and what hurdles their characteristics represent for HTA assessment. | |

| This analysis shows how advanced therapies have been used over the years in Italy, detailing the expenditure generated and the number of treated patients in the different regions of this country, highlighting national and regional differences. | |

| Notwithstanding a very high per-treatment price, as of now these drugs are generating a relatively contained albeit rapidly increasing expenditure. |

Introduction

Since their first approval [1], ATMPs have been characterized by the promise of transformative and long-term benefits to patients with high unmet medical needs. However, the rarity of the conditions for which ATMPs were developed is also the reason behind the suboptimal design of pivotal trials that are often single-arm with low numbers of enrolled subjects and follow-up times that do not deliver long-term data on safety and efficacy [2, 3], also making their approval rate lower than for other drugs [4]. Additionally, ATMP administration requires highly qualified and experienced professionals able to safely administer the drug, manage the underlying disease of the patients as well as the consequences of the treatment and their side effects, a complex scenario, especially in the case of autologous ex-vivo gene therapies [5, 6].

These peculiarities paired with skyrocketing prices hardly justifiable from a manufacturing and ethical point of view [7], configures a challenge for HTA agencies world wide [8–12] and are likely to tether the accessibility of ATMPs to patients. Within the European Union, Italy is one of the countries with the highest number of reimbursed ATMPs, as well as one of the first countries to implement outcome-based payment mechanisms developed in an effort to curb the chronological misalignment between costs and benefits characterizing these drugs [13–15].

In spite of the efforts put in by stakeholders to allow safe and fast patient access, difficulties in negotiating a reimbursement price have already resulted in drug withdrawals. Indeed, the first ATMP to be ever authorized, Glybera (alipogene tiparvovec, UniQure), was discontinued for commercial reasons [16], Strimvelis changed three different marketing authorization holders (MAHs) in an attempt to keep the drug on the market [17], and Bluebird Bio decided to withdraw two ATMPs from the European market, one of which had already reached an advanced negotiation stage with the Italian Medicines Agency prior to European withdrawal [18].

To understand how ATMPs are used in Italy, and if the abovementioned hurdles have affected access to treatment, we conducted a study on the availability of these products to patients across the country, how they have penetrated the Italian market and what expenditure they have generated over the years.

Methods

This is a descriptive study conducted on all ATMPs authorized by the European Commission and evaluated or under evaluation for reimbursability by the Italian Medicines Agency in the period from January 2016 to December 2023. Analyses were conducted on regulatory and reimbursement status, expenditure, consumption and timelines from clinical development to the first acquisition of ATMP by the INHS to provide an overview of the current state of ATMP access in Italy.

The following aspects were analysed:

Availability of ATMPs

Access to treatment

Expenditure

Patient mobility.

Availability and Use of ATMPs

Information on authorized and reimbursed ATMPs in Italy was gathered from the Official Gazette of the Italian Republic (OG) [19], scientific literature, European Public Assessment Reports (EPARs), www.clinicaltrials.gov, the ‘Pricing and Reimbursement Negotiation’ (NPR) System, the Union Register of Medicinal Products [20] and the GALLERY© database with a data cut-off set at the 31 December 2023.

Six indicators were developed to describe the time elapsed for key milestones for each ATMP authorized at EMA level (Fig. S1), all the times were expressed in days.

-

(i)

Clinical development time: time from the first date of the clinical study (considered as the beginning of the first phase I or II study using a specific ATMP in any indication) to the first EMA evaluation date.

-

(ii)

EMA assessment time: time from the EMA procedure start date to the EC decision.

-

(iii)

Lag time between European Commission (EC) decision and Pricing and Reimbursement dossier (P&RD) submission: from the EC decision to the submission of the P&RD to AIFA. This is the only indicator that can have negative values, as the submission date of the dossier to AIFA may precede the decision date of the European Commission. Descriptive statistics are calculated on 17 ATMPs.

-

(iv)

AIFA assessment time: time from the submission of the P&RD to AIFA to the date of publication of the AIFA decision on reimbursability in the OG. Descriptive statistics are calculated on 12 ATMPs. There are less ATMPs considered in this indicator, compared with the indicator on ‘lag time between EC decision and P&RD’ as the former only refers to the evaluations that have a final reimbursement decision, and the latter also includes submitted dossiers currently under evaluation.

-

(v)

The first purchase of an ATMP by a public health care facility was considered as an index (proxy) for drug administration to the patient and, therefore, indicative of access to treatment. The first purchase date of an ATMP in each region was selected for ‘year’ and ‘month’, the 15th day of the month was chosen for equal distribution. Descriptive statistics were calculated on all first regional access times, for all ATMPs. For this indicator only the data cut-off is 31 December 2023.

-

(vi)

Overall regulatory time: sum of (ii) to (iv).

Access to Treatment

We analysed the distribution of centres qualified to administer ATMPs with information retrieved from the AIFA registries, tools introduced by the Italian Medicines Agency with the aim of verifying the prescriptive appropriateness, after the reimbursement decision of a drug for a specific therapeutic indication [21]. Centres qualified to administer more than one ATMP were counted only once. The centres considered active are those that performed at least one treatment since their authorization. Inactive centres were estimated by subtracting active centres from the total.

The data on single treatments in 2023 was used to calculate the number of treatments performed in each region, thus, estimating the average number of treatments per active facility. The number of active facilities and treatments per million inhabitants (pmp) were calculated as ratio of the resident population in 2023 in each region, geographical area, or the whole country.

Expenditure

For the evaluation of ATMP expenditure over time, we used the ‘drug traceability’ flow. Data on expenditure for ATMPs purchased by public facilities of the INHS (known as the direct procurement channel) were analysed between 1 January 2016 and 31 December 2023. This dataset does not take in account the effect of managed entry agreements (MEAs [22]) where applicable, and represents the actual expenditure for each year plus value added tax (VAT). To evaluate the annual growth rate of spending on ATMP drugs, the compound annual growth rate (CAGR %) was calculated (using the following formula:

where ‘final value’ means the value of expenditure incurred by the INHS in the last year of the interval considered (2023), ‘initial value’ means the value of the first year in which a more substantial expenditure was observed (2019), the number of years is the period expressed in years from 2019 to 2023 and all expressed in percentage.

Expenditure was estimated as national, regional or divided by geographical area and the percentage difference of expenditure between 2022 and 2023, was calculated to measure the increase in spending in 2023. To contextualize the spending for ATMPs, we also evaluated it as a percentage of both the total INHS expenditure and the total expenditure by public health facilities (direct procurement channel). The period 2016–2023 was also stratified by type of ATMP, by region, or geographical area.

Patient Mobility

The data on single treatments with ATMPS was also used to measure patient mobility across Italian regions. In particular, to measure the extent of patient inter-regional mobility, we calculated, for each region, the percentage of treatments performed on patients that were resident in another Italian region in 2023.

Results

ATMPs Availability in Italy

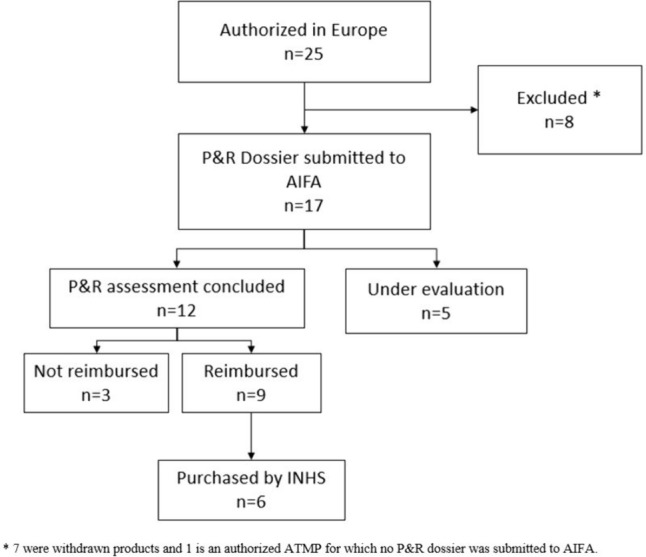

Since the coming into force of the Regulation 2007/1394 (i.e. ATMP Regulation) until the data cut off of on 31 December 2023, the EC has granted marketing authorizations for 25 ATMPs (Fig. 1); roughly one third (7 out of 25) was subsequently withdrawn from the European market following the decision of the MAHs owing to various causes [23]. In particular, only Zalmoxis [24] was withdrawn because of the failure of a post-authorization phase 3 study to meet its primary endpoint, while the other six withdrawals were owing to commercial reasons [2], after the drugs were on the market for an average time of 3.5 years [25–29]. Withdrawn products were excluded from the analysis as well as one ATMP for which no dossier for pricing and reimbursement (P&R) has been submitted up to the data cut-off date. Hence, we included in our analysis 17 authorized ATMPs in Italy with a reimbursement decision or with an ongoing P&R evaluation whose characteristics are summarized in Table 1. On the basis of the definitions set out in the Regulation [30], the majority are gene therapies (13 out of 17; 75.5%), while 2 are tissue therapies and 2 are somatic cell therapies. Gene therapies can be further divided into ex-vivo gene therapies (8/13; 61.5%), such as CAR-T therapies, and in-vivo gene therapies (5/13; 38.5%). In terms of therapeutic area, 58.8% (10/17) are intended to treat non-oncologic conditions while 41.2% (7/17) have onco-haematologic indications. The vast majority of these ATMPs (15 out of 17; 88.2%) were granted an orphan designation, pursuant regulation 141/2000 on orphan medicines [31], thus accessing fast-track authorisation procedures, such as the conditional marketing authorization (CMA) or the authorisation under exceptional circumstances (UEC). Indeed, in our dataset, the majority of medicines were approved via special procedures, i.e. 41.2% (n = 7) received a CMA and 11.8% (n = 2) received an authorisation UEC, while 8 (47.0%) received a full approval (Table 1).

Fig. 1.

Flow chart of the ATMPs authorized by the European Commission included in the analysis up to 31 December 2023. AIFA Italian Medicines Agency; ATMPs advanced therapy medicinal products; INHS Italian National Health System; P&R pricing and reimbursement

Table 1.

EU-authorized ATMPs with a P&R dossier submitted to AIFA (n = 17), up to 31 December 2023

| N | Brand name | Active substance | ATMP | CAR-T | Clinical condition | Oncologic condition | Orphan drug | EC authorization | Ex-factory price | Publication of the reimbursement resolution in the OG | AIFA decision | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Holoclar | Ex vivo expanded autologous human corneal epithelial cells containing stem cells | Tissue engineered | No | Moderate to severe limbal stem cell deficiency | No | Yes | CMA | 17/02/2015 | € 95,000 | 24/02/2017 | Reimbursed |

| 2 | Strimvelis | An autologous CD34+ enriched cell fraction that contains CD34+ cells transduced with retroviral vector that encodes for the human adenosine | Ex vivo gene therapy | No | Severe combined immunodeficiency due to ADA deficiency (ADA- SCID) | No | Yes | Standard | 26/05/2016 | € 594,000 | 01/08/2016 | Reimbursed |

| 3 | Spherox | Spheroids of human autologous matrix-associated | Tissue engineered | No | Symptomatic articular cartilage defects of the knee | No | No | Standard | 10/07/2017 | n.a. | 26/11/2021 | Not reimbursed |

| 4 | Kymriah | Tisagenlecleucel | Ex vivo gene therapy | Yes |

Relapsed or refractory B-ALL Relapsed or refractory DLBCL |

Yes | Yes | Standard | 23/08/2018 | € 320,000 | 12/08/2019 | Reimbursed |

| 5 | Yescarta | Axicabtagene ciloleucel | Ex vivo gene therapy | Yes | Relapsed or refractory DLBCL and PMBCL | Yes | Yes | Standard | 23/08/2018 | € 320,000 | 11/11/2019 | Reimbursed |

| 6 | Luxturna | Voretigene neparvovec | In vivo gene therapy | No | Inherited retinal dystrophy caused by confirmed biallelic RPE65 mutations | No | Yes | Standard | 22/11/2018 | € 360,000 | 09/01/2021 | Reimbursed |

| 7 | Alofisel | Darvadstrocel | Somatic cell therapy | No | Complex perianal fistulas in Crohn disease | No | Yes | Standard | 23/03/2018 | n.a. | 08/10/2018 | Not reimbursed |

| 8 | Zolgensma | Onasemnogene abeparvovec | In vivo gene therapy | No | 5q spinal muscular atrophy (SMA) with up to three copies of the SMN2 gene | No | Yes | CMA | 18/05/2020 | € 2,155,124.65 | 13/03/2021 | Reimbursed |

| 9 | Tecartus | Brexucabtagene autoleucel | Ex vivo gene therapy | Yes | Relapsed or refractory mantle cell lymphoma (MCL) | Yes | Yes | CMA | 14/12/2020 | € 360,000 | 11/03/2022 | Reimbursed |

| 10 | Libmeldy | Atidarsagene autotemcel | Ex vivo gene therapy | No | Metachromatic leukodystrophy (MLD) | No | Yes | Standard | 17/12/2020 | € 2,875,000.00 | 07/04/2022 | Reimbursed |

| 11 | Abecma | Idecabtagene vicleucel | Ex vivo gene therapy | Yes | Relapsed and refractory multiple myeloma | Yes | Yes | CMA | 18/08/2021 | n.a. | 19/08/2023 | Not reimbursed |

| 12 | Upstaza | Eladocagene exuparvovec | In vivo gene therapy | No | Severe aromatic L-amino acid decarboxylase deficiency | No | Yes | UEC | 18/07/2022 | € 3,500,000 | 04/12/2023 | Reimbursed |

| 13 | Carvykti | Ciltacabtagene autoleucel | Ex vivo gene therapy | Yes | Relapsed and refractory multiple myeloma | Yes | Yes | CMA | 25/05/2022 | n.a. | n.a. | Under assessment |

| 14 | Breyanzi | Lisocabtagene maraleucel | Ex vivo gene therapy | Yes | Relapsed or refractory DLBCL, HGBCL, PMBCL and FL3B | Yes | No | Standard | 04/04/2022 | n.a. | n.a. | Under assessment |

| 15 | Roctavian | Valoctocogene roxaparvovec | In vivo gene therapy | No | Severe haemophilia A | No | Yes | CMA | 24/08/2022 | n.a. | n.a. | Under assessment |

| 16 | Ebvallo | Tabelecleucel | Somatic stem cell therapy | No | Relapsed or refractory EBV positive post-transplant lymphoproliferative disease (EBV+ PTLD) who have received at least one prior therapy | Yes | Yes | UEC | 16/12/2022 | n.a. | n.a. | Under assessment |

| 17 | Hemgenix | Etranacogene dezaparvovec | In vivo gene therapy | No | Severe and moderately severe Haemophilia B | No | Yes | CMA | 20/02/2023 | n.a. | n.a. | Under assessment |

AIFA, Italian Medicines Agency; ATMPs, advanced therapy medicinal products; P&R, pricing and reimbursement; CMA, conditional marketing authorization; UEC, under exceptional circumstances; DLBCL, diffuse large B cell lymphoma; PMBCL, primary mediastinal B cell lymphoma; HGBL, high grade lymphoma; ALL, acute lymphoblastic leukaemia; FL3b, follicular lymphoma type 3b; EBV, Epstein–Barr virus; n.a., not available

As of 31 December 2023, 12 authorized ATMPs concluded the evaluation of the P&R dossier with a final decision published in the Italian OG, with a positive decision in the majority of cases: 9 out of 12 (75.0%) are reimbursed and 3 (25.0%) are not, while 5 are currently under evaluation (Table 1). The average ex-factory price of the nine reimbursed ATMPs is €1,175,458.9€, with price tags ranging from 95,000€ to 3,500,000€.

Between the publication of the reimbursement decision for the first ATMP and the expenditure data cut off of 31 December 2023, 6 of the 9 reimbursed ATMPs were directly purchased at least once by INHS facilities (Fig. 1). Two ATMPs (Strimvelis and Limbmeldy) indicated for ultra-rare diseases with an expected incidence in Italy of no more than two patients per year each were never directly purchased through the INHS.

Patient Access Timelines

To evaluate the time needed for an ATMP to reach the bed of a patient in Italy, we analysed the duration of the different phases of their life cycle. For all 17 ATMPs authorized by the EMA we measured the time from the first clinical trial to the publication of the EC decision (Fig. S1). For 12 ATMPS with a final decision in the Italian OG we extended the analysis to the end of the evaluation by regulatory agencies. Finally, for six ATMPs we could also calculate the time to first patient access, considered as the first purchase of the drug by an Italian health facility (Fig.S1).

As shown in Table 2 and Fig. S2, clinical development had an average duration of 9.8 years (3588 days) while the average duration of the European assessment was 1.5 years (547 days). In Italy, the average time for the P&R assessment for ATMPs was 1.2 years (446 days, n = 12 ATMPs), which is in line with the time necessary to appraise new orphan drugs (484 days in average) [32]. From the beginning of the EMA evaluation to the publication of the reimbursement decision in the Italian OG, the total regulatory time was 3.2 years.

Table 2.

Time of clinical development, regulatory assessment and patient access for ATMPs in Italy (data shown in days)

| N | Brand name | AIFA decision | Clinical development timea | EMA assessment timea | Lag time between EC and AIFAa.d | AIFA assessment timeb | Regulatory timeb | Average time to first patient accessc |

|---|---|---|---|---|---|---|---|---|

| 1 | Holoclar | Reimbursed | 6474 | 692 | 367 | 361 | 1430 | 430 |

| 2 | Strimvelis | Reimbursed | 8447 | 364 | −51 | 116 | 431 | – |

| 3 | Spherox | Not reimbursed | 5650 | 1656 | 886 | 682 | 3256 | – |

| 4 | Kymriah | Reimbursed | 2787 | 273 | −51 | 397 | 627 | 387 |

| 5 | Yescarta | Reimbursed | 3084 | 371 | −48 | 481 | 816 | 611 |

| 6 | Luxturna | Reimbursed | 3605 | 462 | 31 | 709 | 1241 | 305 |

| 7 | Alofisel | Not reimbursed | 2452 | 729 | −93 | 271 | 928 | – |

| 8 | Zolgensma | Reimbursed | 1608 | 564 | 8 | 283 | 863 | 148 |

| 9 | Tecartus | Reimbursed | 1522 | 321 | −45 | 483 | 773 | 155 |

| 10 | Libmeldy | Reimbursed | 3500 | 385 | −13 | 450 | 861 | – |

| 11 | Abecma | Not reimbursed | 1591 | 454 | −41 | 768 | 1185 | – |

| 12 | Upstaza | Reimbursed | 1908 | 902 | 122 | 348 | 1406 | – |

| 13 | Carvykti | Under ev. | 2036 | 370 | 33 | – | – | – |

| 14 | Breyanzi | Under ev. | 1636 | 627 | 58 | – | – | – |

| 15 | Roctavian | Under ev. | 2141 | 405 | 83 | – | – | – |

| 16 | Hemgenix | Under ev. | 2827 | 333 | −10 | – | – | – |

| 17 | Ebvallo | Under ev. | 9732 | 386 | 109 | – | – | – |

| Mean | 3588 | 547 | 79 | 446 | 1151 | 340.6 | ||

| Median | 2787 | 405 | 8 | 424 | 896 | 216.0 | ||

| Std. Dev. | 2500 | 333 | 234 | 195 | 729 | 328.5 | ||

| IQR | 1697 | 257 | 128 | 201 | 477 | 425.0 |

AIFA, Italian Medicines Agency; ATMPs, advanced therapy medicinal products; EC, European Commission; under ev, under evaluation; Std. Dev., standard deviation; IQR, inter-quartile range

aStatistics calculated on n = 17 ATMPs

bStatistics calculated on n = 12 ATMPs

cStatistics calculated on n = 6 ATMPs

dFor eight ATMPs the dossier was submitted to AIFA before the EC decision.

We have subsequently analysed the time to first patient access, data was available for 6/12 ATMPs showing high variability, with a national average time ranging from 148 to 611 days after the OG publication (Table 2).

By disaggregating the access time data and focusing at the regional level we can observe that regions, such as Molise, Sardegna, Marche, Friuli Venezia Giulia and Abruzzo, have a longer average patient access time (450–1313 days on average); the shortest access times were registered in Lombardia, Emilia Romagna and Toscana (116–131 days on average). The highest variability was observed in Friuli Venezia Giulia (northern Italy) and Sardegna (southern Italy; Fig. 2). The longest times were relative to the first treatments with Yescarta and Kymriah (1342 and 1283 days both in Molise, respectively), the shortest (4 and 33 days in Umbria and Puglia, respectively) were registered for the first treatments with Tecartus and Zolgensma, respectively. When looking at access times by geographical areas (Table 3) we can see that, nationally, time to patient access averages at 340.6 days (median time 216.0 days). Northern and central Italy average at 281.5 and 290.9 days respectively, while southern Italy averages at 436.8 days.

Fig. 2.

Days to patient access for each region. Data are shown in days as mean (lozenge) and median (middle bar), boxes range from first to third quartile and whiskers span from minum to maximum. The number above each box represents the number of ATMPs acquired by the INHS. ATMPs advanced therapy medicinal products; INHS Italian National Health System

Table 3.

Patient access time at regional and national level

| Area | No. of ATMPs | Mean | Min | P25 | Median | P75 | Max | Std |

|---|---|---|---|---|---|---|---|---|

| Italy | 6 | 340.6 | 4.0 | 96.0 | 216.0 | 521.0 | 1342.0 | 328.5 |

| Northern Italy | 6 | 281.5 | 33.0 | 96.0 | 140.5 | 429.0 | 1039.0 | 274.9 |

| Central Italy | 6 | 290.9 | 4.0 | 126.0 | 186.0 | 428.0 | 780.0 | 252.3 |

| Southern Italy | 5 | 436.8 | 33.0 | 95.0 | 264.0 | 612.0 | 1342.0 | 405.6 |

min, minimum; P25, 25th percentile; P75, 75th percentile; max, maximum; std, standard deviation

To measure the level of preparedness for ATMP administration in all Italian regions we have analysed the number of health facilities authorized to administer ATMPs, and those that have performed at least one treatment (Table 4). The distribution remains rather heterogeneous, and very strikingly, while the facilities authorized to ATMP administration cover all Italian regions, on average 56% of them are actually active. 107 health facilities are authorized for ATMP administration in Italy (without distinction on the type of ATMP), which corresponds to 1.8 facilities for one million inhabitants (pmp). This ratio differs slightly when zooming into the different geographical areas where northern Italy has 1.7 facilities pmp (46 authorized), central Italy has 1.4 facilities pmp (16 authorized) and southern Italy has 2.3 facilities pmp (45 authorized facilities). However, when looking at the active facilities, the national average drops to one facility pmp with the lowest ratio in Southern Italy (0.8 facilities), followed by Central Italy (0.9 facilities pmp) and Northern Italy (1.2 facilities pmp). Therefore, while 74% and 69% of authorized facilities in Central and Northern Italy are active, only 33% of all authorized facilities are active in Southern Italy, leaving regions, such as Molise, Basilicata and Sardegna with no coverage. This also entails that some regions, such as Marche, have two centres pmp, while others have four times less or none at all. Similarly, only 3.8 treatments pmp were administered in Southern Italy in 2023, compared with 8.1 treatments pmp in Northern Italy and 5.4 in Central Italy. However, when calculating the number of treatments performed per centre in each region or geographical area, the national average of six treatments per centre is rather close to the Northern, Central and Southern Italy averages, ranging from 5.1 to 6.5. Although a greater variability is uncovered at the regional level, where in regions, such as Emilia Romagna, 19,5 treatments per facility were performed in 2023, while in Marche 1 treatment per facility was performed (Table 4).

Table 4.

Distribution of authorized and active facilities in relationship with regional population and number of ATMP treatments in 2023 (n = 6 ATMPs)

| Region | Authorized facilities | N of authorized facilities per Mln inhabitants | Active facilities | Inactive facilities | N of active facilities per Mln inhabitants | N of treatments in 2023 | N of treatments per active facility | N of treatments per Mln inhabitants |

|---|---|---|---|---|---|---|---|---|

| Italy | 107 | 1.8 | 60 | 47 | 1.0 | 360 | 6.0 | 6.1 |

| Northern Italy | 46 | 1.7 | 34 | 12 | 1.2 | 221 | 6.5 | 8.1 |

| Piemonte | 4 | 0.9 | 4 | 0 | 0.9 | 27 | 6.8 | 6.4 |

| Valle D’Aosta | 1 | 8.1 | 0 | 1 | – | 0 | – | – |

| Lombardia | 24 | 2.4 | 18 | 6 | 1.8 | 102 | 5.7 | 10.2 |

| Trentino Alto Adige | 3 | 2.8 | 1 | 2 | 0.9 | 0 | 0.0 | – |

| Veneto | 6 | 1.2 | 5 | 1 | 1.0 | 33 | 6.6 | 6.8 |

| Friuli Venezia Giulia | 2 | 1.7 | 2 | 0 | 1.7 | 5 | 2.5 | 4.2 |

| Liguria | 2 | 1.3 | 2 | 0 | 1.3 | 15 | 7.5 | 9.9 |

| Emilia Romagna | 4 | 0.9 | 2 | 2 | 0.5 | 39 | 19.5 | 8.8 |

| Central Italy | 16 | 1.4 | 11 | 5 | 0.9 | 63 | 5.7 | 5.4 |

| Toscana | 3 | 0.8 | 3 | 0 | 0.8 | 30 | 10.0 | 8.2 |

| Umbria | 1 | 1.2 | 1 | 0 | 1.2 | 7 | 7.0 | 8.2 |

| Marche | 4 | 2.7 | 3 | 1 | 2.0 | 3 | 1.0 | 2.0 |

| Lazio | 8 | 1.4 | 4 | 4 | 0.7 | 23 | 5.8 | 4.0 |

| Southern Italy | 45 | 2.3 | 15 | 30 | 0.8 | 76 | 5.1 | 3.8 |

| Abruzzo | 4 | 3.1 | 1 | 3 | 0.8 | 9 | 9.0 | 7.1 |

| Molise | 3 | 10.3 | 0 | 3 | – | 2 | – | 6.9 |

| Campania | 8 | 1.4 | 4 | 4 | 0.7 | 20 | 5.0 | 3.6 |

| Puglia | 9 | 2.3 | 5 | 4 | 1.3 | 15 | 3.0 | 3.8 |

| Basilicata | 3 | 5.6 | 0 | 3 | – | 0 | – | – |

| Calabria | 2 | 1.1 | 2 | 0 | 1.1 | 11 | 5.5 | 6.0 |

| Sicilia | 5 | 1.0 | 3 | 2 | 0.6 | 18 | 6.0 | 3.7 |

| Sardegna | 11 | 7.0 | 0 | 11 | – | 1 | – | 0.6 |

mln, million

Expenditure

The expenditure data analysis was conducted on six ATMPs directly purchased by the INHS in the period from August 2016 to December 2023 (Table 1). The expenditure trend reflects the progressive market entry of new ATMPs starting in May 2017. From 2016 to 2018 no or negligible expenditure data were retrieved. After 2019, the expenditure trends increased with a CAGR of 205% from 2019 to 2023 (Table 5). Overall, despite the high costs per treatment of these medicines (Table 1), their impact on the total INHS expenditure in 2023 (26.3 Bln €) is 4.6‰ and accounts for 7.4‰ when compared with the expenditure for medications directly purchased by health facilities (16.4 Bln€, Table 5).

Table 5.

Annual expenditure from 2016 to 2023 stratified by ATMP category (n = 6 ATMPs)

| Year | ATMP expenditure in million € | Incidence on total SSN expenditure (‰) | CAR-T | Non-CAR-T | ||

|---|---|---|---|---|---|---|

| Ex vivo gene therapy (mln €) | Tissue-engineered therapy (mln €) | In vivo gene therapy (mln €) | Ex vivo gene therapy (mln €) | |||

| 2016 | 0 | 0 | 0 | 0 | 0 | 0 |

| 2017 | 0.09 | 0 | 0 | 0.1 | 0 | 0 |

| 2018 | 0 | 0 | 0 | 0 | 0 | 0 |

| 2019 | 1.4 | 0.1 | 1.2 | 0.2 | 0 | 0 |

| 2020 | 16.7 | 0.7 | 16.7 | 0 | 0 | 0 |

| 2021 | 73.5 | 3.1 | 48.4 | 0.2 | 25 | 0 |

| 2022 | 86 | 3.4 | 70.6 | 0.2 | 15.3 | 0 |

| 2023 | 121.4 | 4.6 | 106.7 | 0.1 | 14.6 | 0 |

mln, million

The expenditure for ATMPs is driven by CAR-T ex-vivo gene therapies (106.7 Mln € in 2023) with an increasing trend, while all other AMTPs generated a lower expenditure (14.7 Mln€ in 2023), in decline compared with 2021 and 2022 (Tab.5).

The regional expenditure trend from 2016 to 2023 confirms the progressive spread of ATMPs over time and across territories, starting with very few regions in 2017 and 2019 to 86% coverage of the national territory in 2023, with a particular surge registered from 2020 onwards (Table 6). In 2023, the highest expenditure share was observed in the Northern regions (57.7% of the national ATMP expenditure), with Lombardia (26.6Mln €) leading the list. However, regions from other areas of Italy were also very active, for instance, comparing data from 2022 and 2023, expenditure increased the most in Abruzzo (+ 181.4%), Piemonte (+ 117.9%) and Veneto (+ 106.8%).

Table 6:

Regional and national expenditure in the period from 2016 to 2023, and treatments performed in 2023 (n = 6 ATMPs).

| Regions | Expenditure in mln € | % of the 2023 national ATMP expenditure | ∆ % 2023–2022 | 2023 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | Treatments | % of non-resident treated patients | |||

| Italy | – | 0.1 | – | 1.4 | 16.7 | 73.5 | 86.0 | 121.4 | 100.0% | 41.1% | 360 | 18.3% |

| Northern Italy | – | 0.1 | – | 0.8 | 11.7 | 40.0 | 48.5 | 70.0 | 57.7% | 44.3% | 221 | 21.7% |

| Piemonte | – | – | – | – | 0.6 | 1.7 | 5.1 | 11.2 | 9.2% | 117.9% | 27 | 3.7% |

| Valle D’Aosta | – | – | – | – | – | – | – | – | 0.0% | – | 0 | 0.0% |

| Lombardia | – | – | – | 0.8 | 9.4 | 24.7 | 23.0 | 26.6 | 21.9% | 15.4% | 102 | 26.5% |

| Pa Bolzano | – | – | – | – | – | – | – | – | 0.0% | – | 0 | 0.0% |

| Pa Trento | – | – | – | – | – | – | 0.3 | – | 0.0% | −100.0% | 0 | 0.0% |

| Veneto | – | – | – | – | 0.5 | 2.7 | 5.7 | 11.8 | 9.7% | 106.8% | 33 | 12.1% |

| Friuli Venezia Giulia | – | – | – | – | – | 0.3 | 1.9 | 3.2 | 2.6% | 66.0% | 5 | 40.0% |

| Liguria | – | – | – | – | 0.3 | 3.0 | 4.1 | 6.0 | 5.0% | 47.9% | 15 | 13.3% |

| Emilia Romagna | – | 0.1 | – | – | 0.9 | 7.7 | 8.4 | 11.2 | 9.2% | 34.0% | 39 | 30.8% |

| Central Italy | – | – | – | 0.3 | 2.7 | 13.2 | 19.3 | 27.9 | 23.0% | 45.1% | 63 | 4.8% |

| Toscana | – | – | – | – | 1.0 | 5.3 | 6.8 | 10.3 | 8.5% | 51.6% | 30 | 0.0% |

| Umbria | – | – | – | – | 0.8 | 2.5 | 2.1 | 4.1 | 3.4% | 89.7% | 7 | 0.0% |

| Marche | – | – | – | – | – | 0.2 | 1.6 | 1.9 | 1.6% | 21.4% | 3 | 0.0% |

| Lazio | – | – | – | 0.3 | 0.9 | 5.3 | 8.7 | 11.6 | 9.6% | 33.3% | 23 | 13.0% |

| Southern Italy | – | – | – | 0.3 | 2.3 | 20.3 | 18.3 | 23.4 | 19.3% | 28.3% | 76 | 19.7% |

| Abruzzo | – | – | – | – | – | 0.8 | 1.0 | 2.9 | 2.4% | 181.4% | 9 | 22.2% |

| Molise | – | – | – | – | – | – | – | 0.4 | 0.3% | – | 2 | 0.0% |

| Campania | – | – | – | – | 0.7 | 11.9 | 6.2 | 7.5 | 6.2% | 20.4% | 20 | 55.0% |

| Puglia | – | – | – | 0.2 | 0.7 | 0.8 | 2.0 | 3.7 | 3.0% | 84.4% | 15 | 6.7% |

| Basilicata | – | – | – | – | – | – | – | – | 0.0% | – | 0 | 0.0% |

| Calabria | – | – | – | 0.2 | 0.7 | 2.1 | 2.3 | 3.6 | 3.0% | 56.6% | 11 | 9.1% |

| Sicilia | – | – | – | – | 0.2 | 3.4 | 6.6 | 5.2 | 4.3% | −21.1% | 18 | 0.0% |

| Sardegna | – | – | – | – | – | 1.3 | 0.2 | 0.2 | 0.2% | 39.2% | 1 | 0.0% |

mln, million; Δ, difference

When looking at the 360 ATMP treatments administered in 2023 we can observe that 18.3% of these were for Italian patients who were not resident in the region of treatment. This phenomenon, know as inter-regional mobility is owing to the fact that, in Italy, patients are free to chose any accredited health facility in the country for the treatment they need [33]. Some regions are more active than others in treating non-resident patients, in particular 55% and 30.8% of all treatments performed in Campania and Emilia Romagna in 2023, respectively, were for patients coming from other Italian regions (Table 6). The majority of inter-regional movements in 2023 were aimed at receiving CAR-T treatments; however, in the case of Campania, patients came from all over Italy to be treated with Luxturna.

Discussion

The data gathered in this study on the availability and use of ATMPs in Italy from their introduction, shows their increasing diffusion from 2016 onwards, with details at the regional level on expenditure and patient mobility. The vast majority of ATMPs for which a P&R dossier was submitted were granted reimbursability, generating an expenditure mainly owing to the appearance of CAR-T therapies. With the recent and impending approval of new gene therapies for haemophilia, new CAR-Ts for multiple myeloma and new indications for CAR-Ts already available in Italy, onco-hematologic ATMPs are expected to remain the ones with the highest economic impact on the Italian NHS.

Overall, notwithstanding their very high per-treatment price and CAGR, ATMPs currently represent 4.6‰ of the national pharmaceutical expenditure. However, as ATMP expenditure increases, the matter of sustainability, one of the major hurdles for ATMP diffusion, is becoming more and more crucial. In fact, while the INHS already covers exceedingly high life-long costs for chronic treatments (haemophilia treatment is a fitting example), these are therapies known to be effective, and treatment failure can be met with treatment interruption, thus eliminating the risk of paying for ineffective or harmful treatment. On the other hand, no data is currently available to corroborate the predictions of pharmaceutical companies that successful treatment with ATMPs will represent future savings by averting chronic treatments costs, increasing quality of life, activity and productivity of patients and caregivers, in spite of a high one-off price. In addition to the lack of evidence of long term curative potential, as opposed to a palliative care potential, recent reports on secondary malignancies detected in patients treated with commercial CAR-T therapies are raising questions on their safety [34, 35]. Furthermore, CAR-T therapies share with other ex-vivo gene therapies hurdles inherent to their autologous nature, exposing them to manufacturing failure, release of out-of-specification batches [36] in addition to manufacturing and transportation bottlenecks [37–39] reducing patient access, or even leading to withdrawal from the market, as is the case for Carvykti [40].

We also analysed ATMP availability in Italy in terms of time needed to for the first patient treatment. Across geographical areas, data on ATMP access time and number of performed treatments seems rather homogenous, however, the regional level shows a higher level of variability, most likely resulting from several intertwining factors, such as the plurality of Italian pharmaceutical policy-making centres. In fact, Italian regions have different strategies to allow drug dispensation following the publication of the reimbursement resolution in the Italian OG, which translates into an interregional variability in the choice of drugs that hospitals can prescribe, and in the timing necessary to make new drugs available for dispensation.

In the case of ATMPs, regional policy differences are exacerbated by the complexity of the administration itself, often requiring specialized structures and highly experienced teams that need training and qualification. For autologous ex-vivo gene therapies, for instance, the process of apheresis, cell modification and subsequent re-infusion in the patient has led the AIFA Technical Scientific Committee (CTS) to require that hospitals administering, such drugs have a JACIE accreditation for allogeneic transplant, in addition to the EMA mandated qualification process for which the MAH is responsible [41, 42]. We have also estimated that roughly 45% of health facilities authorized for ATMP administration remained inactive, showing that several regions had planned on a much higher activity than what was actually delivered, with a consequent imbalance in the number of active centres available per million of inhabitants between different regions. The main reason of the inactivity of such a large proportion of authorized facilities could be a lack of demand. In fact, in the smallest regions, which are also the ones with the fewer active centres, this is likely owing to the epidemiology of the rare diseases for which ATMPs are indicated. Inter-regional mobility, where patients travel to more active and renowned centres, instead of relying on accredited centres in their region of residence, could also be a reasonable explanation for this scenario. Indeed, more than one quarter of all ATMP treatments were performed in regions where patients were non-resident, with an extreme example in the case of Luxturna for which almost 40% of the treatments were performed in Campania, for patients coming from all over Italy, even from regions that have active facilities for the administration of this same drug. This phenomenon is bound to create a snowball effect in which more active and renowned centres become more and more attractive, while smaller centres, albeit with the required accreditations, fail to treat patients because of a lack of demand. Excellence centres are national reference points with large catchment areas going well beyond regional borders, especially in the case of rare and ultra-rare diseases, leaving regions with fewer inhabitants less likely to have facilities with the required expertise in treating patients with rare or ultra-rare diseases.

Unfortunately, while patient mobility allows to choose the most experienced facilities, it also raises a concern for timeliness of treatment and treatment equality, as the time and financial burden required to receive care in locations that are distant from home might not be equally sustainable for all patients.

Limitations

Limitations of this study are owing to the small numbers of ATMPs used for treating Italian patients so far, as well as the relatively short time of observation. Also, the effect of outcome-based managed entry agreements (MEAs) on the expenditure for ATMPs could not be calculated, which could represent an underestimation of the current ATMP expenditure. Another limitation of our work lies in the estimation of the assessment time required by regulatory agencies. In fact, our dataset also encompasses clock-stops, which is the working time required by the pharmaceutical companies to supply documentary integration, as well as an average waiting time of 70 days between the EC decision and submission of the P&R dossier to AIFA. Negative times in the latter category are owing to the possibility given to MAH of orphan drugs, hospital medicines and medicines having exceptional therapeutic relevance to submit the P&R dossier to AIFA after the CHMP positive opinion, before the EC issues its decision, pursuant Law 189/2012, a case that occurred for 9/17 ATMPs. Additionally, time of purchase of an ATMP by a public health care facility is an approximation of the actual time of treatment of a patient.

Conclusions

Our study, which is the first of its kind with this level of detail for a single European country, shows a rapidly evolving picture with all Italian regions adapting to a new category of pharmaceuticals, albeit at different paces. Currently, the small numbers of ATMPs used and the short time they have been available on the market hamper further conclusions; however, as the range of available therapies increases, subsequent studies will allow the identification of new patterns of consumption and expenditure and evaluate the appropriateness of actions taken by health and regulatory authorities to facilitate the access to these treatments. Nonetheless, it is necessary to keep in mind that the possible approval and reimbursement of new upcoming ATMPs, some of which have broader populations of eligible patients, might require new paradigms to maintain an economic and organizational sustainability, and that, increasing the ATMP budget cannot be the only way forward. Therefore, as new AMTPs arrive on the market, a substantial effort is still required from pharmaceutical companies, regulatory agencies, health facilities and regions to enable a faster and more uniform access throughout the national territory, as well as to guarantee the sustainability of these therapies for the INHS.

Supplementary Information

Below is the link to the electronic supplementary material.

Acknowledgements

We thank the Monitoring Registers Office of the Italian Medicines Agency for sharing the data on health facilities authorized for ATMP administration. A preliminary version of this analysis was published on the Sixth Report (Chapter 4) of the Italian ATMP Forum [43].

Ethics Declarations

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Conflict of Interest

None declared.

Ethics Approval

Not applicable.

Consent to Participate

Not applicable.

Consent for Publication

Not applicable.

Availability of Data and Material

Not applicable.

Code Availability

Not applicable.

Author Contribution

F.T. and P.R.d.V.C.: study design, data interpretation, writing; P.R.d.V.C., A.E., M.L. and A.L.G. data collection, analysis and interpretation; P.R.d.V.C., M.L. and A.E.: manuscript drafting; F.T.: team supervision and manuscript editing. All authors read and approved the final manuscript and declare no conflicts of interest. The views expressed in this article are the personal views of the authors and may not be understood or quoted as being made on behalf of or reflecting the position of their institutional affiliation.

References

- 1.Ylä-Herttuala S. Endgame: glybera finally recommended for approval as the first gene therapy drug in the European Union. Mol Ther. 2012;20(10):1831. 10.1038/MT.2012.194. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.Elsallab M, Bravery CA, Kurtz A, Abou-El-Enein M. Mitigating deficiencies in evidence during regulatory assessments of advanced therapies: a comparative study with other biologicals. Mol Ther Methods Clin Dev. 2020;18(September):269–79. 10.1016/j.omtm.2020.05.035. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.Barkholt L, Voltz-Girolt C, Raine J, Salmonson T, Schüssler-Lenz M. European regulatory experience with advanced therapy medicinal products. Nat Rev Drug Discov. 2018;18(1):8–9. 10.1038/nrd.2018.200. [DOI] [PubMed] [Google Scholar]

- 4.Bravery CA, Ball O, Robinson S. EU market authorisation strategy: lessons from the first 22 ATMP submitted to the EMA. Cell Gene Ther Insights. 2019;5(6):759–91. 10.18609/cgti.2019.088. [Google Scholar]

- 5.Gribben J, Chabannon C, Yakoub-agha I, Einsele H. The EBMT/EHA CAR-T Cell Handbook. 2022. 10.1007/978-3-030-94353-0. [PubMed]

- 6.Foglia E, et al. Multidimensional Results and Reflections on CAR-T: The Italian Evidence. Int J Environ Res Public Health. 2023. 10.3390/IJERPH20053830. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Flotte TR. Ethical implications of the cost of molecularly targeted therapies. Hum Gene Ther. 2015;26(9):573–4. 10.1089/hum.2015.29010.trf. [DOI] [PubMed] [Google Scholar]

- 8.Olry de Labry-Lima A, Ponce-Polo A, García-Mochón L, Ortega-Ortega M, Pérez-Troncoso D, Epstein D. Challenges for economic evaluations of advanced therapy medicinal products: a systematic review. Value Heal. 2023;26(1):138–50. 10.1016/j.jval.2022.07.004. [DOI] [PubMed] [Google Scholar]

- 9.ten Ham RMT, et al. Key considerations in the health technology assessment of advanced therapy medicinal products in Scotland, The Netherlands, and England. Value Heal. 2022;25(3):390–9. 10.1016/j.jval.2021.09.012. [DOI] [PubMed] [Google Scholar]

- 10.Gozzo L, et al. Health technology assessment of advanced therapy medicinal products: comparison among 3 European countries. Front Pharmacol. 2021;12(October):1–9. 10.3389/fphar.2021.755052. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Drummond M, et al. How are health technology assessment bodies responding to the assessment challenges posed by cell and gene therapy? BMC Health Serv Res. 2023. 10.1186/s12913-023-09494-5. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 12.Ronco V, Dilecce M, Lanati E, Canonico PL, Jommi C. Price and reimbursement of advanced therapeutic medicinal products in Europe: are assessment and appraisal diverging from expert recommendations? J Pharm Policy Pract. 2021;14(1):1–11. 10.1186/s40545-021-00311-0. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Rejon-Parrilla JC, Espin J, Garner S, Kniazkov S, Epstein D. Pricing and reimbursement mechanisms for advanced therapy medicinal products in 20 countries. Front Pharmacol. 2023. 10.3389/fphar.2023.1199500. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 14.Iglesias-López C, Agustí A, Vallano A, Obach M. Financing and reimbursement of approved advanced therapies in several European countries. Value Heal. 2023;26(6):841–53. 10.1016/j.jval.2022.12.014. [DOI] [PubMed] [Google Scholar]

- 15.Dabbous M, Chachoua L, Caban A, Toumi M. Managed entry agreements: policy analysis from the European perspective. Value Heal. 2020;23(4):425–33. 10.1016/j.jval.2019.12.008. [DOI] [PubMed] [Google Scholar]

- 16.Senior M. After Glybera’s withdrawal, what’s next for gene therapy? Nat Biotechnol. 2017;35(6):491–2. 10.1038/nbt0617-491. [DOI] [PubMed] [Google Scholar]

- 17.Valsecchi MC. Rescue of an orphan drug points to a new model for therapies for rare diseases. Nat Italy. 2023. 10.1038/D43978-023-00145-1. [Google Scholar]

- 18.Izeta A, Cuende N. Regulation of advanced therapies in Europe: are we on the right track? Cell Stem Cell. 2023;30(8):1013–6. 10.1016/j.stem.2023.07.004. [DOI] [PubMed] [Google Scholar]

- 19.Gazzetta Ufficiale della Repubblica italiana. https://www.gazzettaufficiale.it/ricerca/atto/serie_generale/originario?reset=true&normativi=false

- 20.Union Register of Medicinal Products. https://ec.europa.eu/health/documents/community-register/html/reg_hum_atc.htm

- 21.AIFA. https://www.aifa.gov.it/en/registri-farmaci-sottoposti-a-monitoraggio. Registries. https://www.aifa.gov.it/en/registri-farmaci-sottoposti-a-monitoraggio

- 22.Xoxi E, Facey KM, Cicchetti A. The evolution of AIFA registries to support managed entry agreements for orphan medicinal products in Italy. Front Pharmacol. 2021. 10.3389/fphar.2021.699466. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Wilkins GC, Lanyi K, Inskip A, Ogunbayo OJ, Brhlikova P, Craig D. A pipeline analysis of advanced therapy medicinal products. Drug Discov Today. 2023;28(5): 103549. 10.1016/j.drudis.2023.103549. [DOI] [PubMed] [Google Scholar]

- 24.European Medicines Agency EMA. Zalmoxis Withdrawal MA. 2014;44(September): 587151. [Online]. Available: https://www.ema.europa.eu/en/medicines/human/EPAR/zalmoxis.

- 25.European Medicines Agency EMA. Glybera expiry of the marketing authorisation in the European Union. Eur Med Agency. 2017;44(October):713863. [Online]. Available: https://www.ema.europa.eu/en/medicines/human/EPAR/glybera.

- 26.European Medicines Agency EMA. Provenge Withdrawal MA. 2015;44(May):303072. https://www.ema.europa.eu/en/medicines/human/EPAR/provenge.

- 27.European Medicines Agency EMA. Zynteglo Withdrawal MA. 2014;44(September): 192892. [Online]. Available: https://www.ema.europa.eu/en/medicines/human/EPAR/zynteglo.

- 28.European Medicines Agency EMA. MACI Expiry of the marketing authorisation in the European Union. 2018;44(July):457300. [Online]. Available: https://www.ema.europa.eu/en/medicines/human/EPAR/maci.

- 29.European Medicines Agency EMA. ChondroCelect Withdrawal MA. 2016;44(July): 6000. https://www.ema.europa.eu/en/medicines/human/EPAR/chondrocelect

- 30.Detela G, Lodge A. EU regulatory pathways for ATMPs: standard, accelerated and adaptive pathways to marketing authorisation. Mol Ther Methods Clin Dev. 2019;13(June):205–32. 10.1016/j.omtm.2019.01.010. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 31.Hofer MP, et al. Marketing authorisation of orphan medicines in Europe from 2000 to 2013. Drug Discov Today. 2018;23(2):424–33. 10.1016/j.drudis.2017.10.012. [DOI] [PubMed] [Google Scholar]

- 32.A Marcellusi, PLC Paola Raimondo, C Galeone. Time to market access in Italia: durata del processo di P&R per i farmaci per le malattie rare. Glob. 2023;10: 79–88. 10.33393/grhta.2023.2610. [DOI] [PMC free article] [PubMed]

- 33.Fattore G, Petrarca G, Torbica A. Traveling for care: inter-regional mobility for aortic valve substitution in Italy. Health Policy (New York). 2014;117(1):90–7. 10.1016/j.healthpol.2014.03.002. [DOI] [PubMed] [Google Scholar]

- 34.Levine BL, et al. Unanswered questions following reports of secondary malignancies after CAR-T cell therapy. Nat Med. 2024. 10.1038/s41591-023-02767-w. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35.Ghilardi G, et al. T-cell lymphoma and secondary primary malignancy risk after commercial CAR T-cell therapy. Nat Med. 2024. [DOI] [PubMed]

- 36.Bersenev A, Kili S. Management of ‘out of specification’ commercial autologous CAR-T cell products. Cell Gene Ther Insights. 2018;4(11):1051–8. 10.18609/cgti.2018.105. [Google Scholar]

- 37.Shah M, Krull A, Odonnell L, de Lima MJ, Bezerra E. Promises and challenges of a decentralized CAR T-cell manufacturing model. Front Transplant. 2023;2(September):1–9. 10.3389/frtra.2023.1238535. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 38.Bristol Myers hits CAR-T manufacturing bottleneck as Abecma demand outstrips supply | Fierce Pharma. https://www.fiercepharma.com/manufacturing/bristol-myers-hits-car-t-manufacturing-bottleneck-as-abecma-demand-outstrips-supply (Accessed Feb. 09, 2024).

- 39.Cancer center leaders lay bare CAR-T makers’ struggles. https://www.fiercepharma.com/pharma/johnson-johnson-bristol-myers-kite-pharma-car-t-cell-therapy-struggle-sloan-kettering (Accessed Feb. 09, 2024).

- 40.J&J shelves Carvykti’s UK launch amid manufacturing shortfalls. https://www.fiercepharma.com/pharma/johnson-johnson-scraps-carvykti-launch-plan-uk-car-t-manufacturing-remains-lacking (Accessed Feb. 09, 2024).

- 41.Yakoub-Agha I, et al. Management of adults and children undergoing chimeric antigen receptor T-cell therapy: best practice recommendations of the European Society for Blood and Marrow Transplantation (EBMT) and the Joint Accreditation Committee of ISCT and EBMT (JACIE). Haematologica. 2020;105(2):297–316. 10.3324/haematol.2019.229781. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 42.Jommi C, Bramanti S, Pani M, Ghirardini A, Santoro A. CAR T-cell therapies in italy: patient access barriers and recommendations for health system solutions. Front Pharmacol. 2022;13(June):1–11. 10.3389/fphar.2022.915342. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 43.Sesto Report Italiano sulle Advanced Therapy Medicinal Products. 2023. https://www.atmpforum.com/report/.

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.