Abstract

BACKGROUND:

Per capita spending on drugs in the United States is double that of Canada. One commonly debated point when comparing the 2 countries is whether this additional spending allows residents of the United States access to valuable therapies not available in Canada.

OBJECTIVE:

To characterize the therapeutic value of prescription drugs used in the United States that are not marketed in Canada.

METHODS:

This cross-sectional study used IQVIA Multinational Integrated Data Analysis System data to identify drugs purchased in the United States but not in Canada from 2017 to 2021. Drug listing and regulatory review statuses were obtained. We categorized the drugs into 8 mutually exclusive groups: listing status in Canada (“cancelled post-market” or “dormant; approved but not marketed; cancelled pre-market”), other alternatives available (“formulation unavailable,” “existing drug class,” or “therapeutically similar”), “pre-approval,” “atypical access available,” or “unavailable without alternatives marketed” in Canada. Therapeutic value assessments of drugs in the last category were obtained from 3 international organizations.

RESULTS:

2,084 products were purchased in the United States but not in Canada from 2017 to 2021; 1,685 were excluded because they were not prescription drugs, were combinations in which each active pharmaceutical ingredient was already available in the United States as a separate drug, had been discontinued in the United States by August 30, 2023, or were marketed in Canada by August 30, 2023. After exclusions, there were 399 drugs; 120 (30%) were “cancelled post-market,” 38 (10%) were “dormant; approved but not marketed; cancelled pre-market,” 49 (12%) were “formulation unavailable,” 130 (33%) were “existing drug class,” 35 (9%) were “therapeutically similar,” 3 (1%) were “preapproval,” 15 (4%) were “atypical access available,” and 9 (2%) were “unavailable” in Canada. 6 of the 9 drugs had been evaluated by 1 or more independent organizations, and all 6 were rated as offering minor to no additional therapeutic value compared with existing drugs.

CONCLUSIONS:

There was similar access to important prescription drug therapies in the United States and Canada. Overall, the additional spending in the United States may not have necessarily translated into access to important therapeutic innovations.

The United States spends the most per capita in the world on prescription drugs. In 2021, the annual per capita spending in the United States was US $1,432 vs US $814 in Canada, and the Organisation for Economic Co-operation and Development average of US $614.1 It is commonplace in current political discourse to compare the United States with Canada when discussing drug costs. Prescription drug coverage in Canada is similar to that in the United States with a mix of both public and private coverage. However, Canada spends nearly half per capita.1-3

One commonly debated point when comparing the 2 countries is whether the increased per capita spending in the United States allows access to therapeutically valuable and innovative therapies unavailable in other countries.2 The United States accesses new drugs sooner, given manufacturers’ prioritization of regulatory applications in that country because of the revenue generated from sales there.4 In addition, the United States approves more new drugs than any other jurisdiction.5 However, not all new drugs are important therapeutic innovations, defined as “the extent to which [they improve] net health outcomes related to that need.”6

Only a third of new drugs entering the US market with either an accelerated approval or conditional authorization are of moderate or greater therapeutic value compared with existing medications.7 We set out to identify the prescription drugs available in the United States that are not marketed in Canada and describe their therapeutic value.

Methods

We conducted a cross-sectional study of prescription drugs that were purchased in the United States but not in Canada from 2017 to 2021. A drug (including vaccine) was defined as a unique combination of the following 2 factors: active pharmaceutical ingredient(s) (API) and formulation.

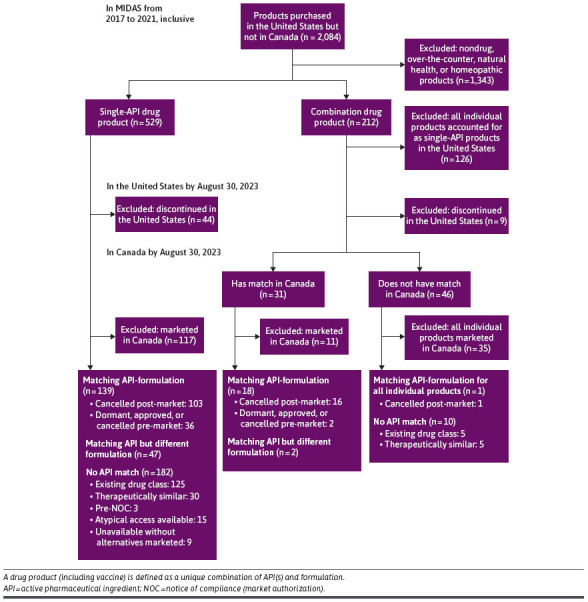

Screening took place across 3 steps. In the first step, using IQVIA’s Multinational Integrated Data Analysis System (MIDAS) database, we excluded nondrugs, over-the-counter products, natural health products, and homeopathic products purchased in the United States but not in Canada to identify all prescription drugs purchased in the former but not in the latter from 2017 to the end of 2021. We then excluded combination products in which each API was already available in the United States as a separate product. In the second step, we used the US Food and Drug Administration (FDA) drug search function to exclude drugs discontinued in the United States as of August 30, 2023. In the third step, we used Health Canada’s Drug Product Database (DPD) to exclude drugs marketed in Canada from January 1, 2022, to August 30, 2023; for combination products marketed in the United States but not in Canada, we excluded those in which each API was marketed in Canada as a separate product. The DPD lists all drugs authorized for sale by Health Canada regardless of whether they are currently being sold.

The remaining prescription drugs, available only in the United States, were then categorized into 3 groups based on a combination of their APIs and formulation (Table 1). These groups were then subcategorized to explain in greater detail why Canada lacked or had limited access to the drug, or why Canada may have had alternatives despite unavailability of the specific US-only drug.

TABLE 1.

Categories of Prescription Drugs Available in the United States but Not in Canada

| Outcome of search on Health Canada’s Drug Product Database | Status in Canada | Number of drugs (%) |

|---|---|---|

| Match across API and formulation but not marketed | Cancelled post-market | 120 (30) |

| Dormant; approved but not marketed; cancelled pre-market | 38 (10) | |

| Match across API but not formulation | Same API but different formulation | 49 (12) |

| No match across API | Existing drug class (drug with the same mechanism of action marketed in Canada) | 130 (33) |

| Therapeutically similar (drug with similar effectiveness and safety marketed in Canada) | 35 (9) | |

| Pre-notice of compliance (submission being considered by Health Canada) | 3 (1) | |

| Atypical access available (available through special access programs) | 15 (4) | |

| Not available drug without alternatives marketed | 9 (2) |

API = active pharmaceutical ingredient.

First, we considered drugs available in the United States (or individual APIs, for combination products without matches in the DPD) that were listed in the DPD but not marketed. Among those drugs, we identified products listed as “cancelled post-market” or as “dormant; approved but not marketed; cancelled pre-market” (ie, drugs that were previously marketed in Canada but have not had any recorded sales for at least 12 consecutive months, drugs that were approved but have never been marketed and drugs that were approved but then had their registration cancelled before they were marketed). Second, we considered drugs with alternative formulations of the US API that were marketed in Canada. We categorized these as “same API but different formulation.” Third, we considered drugs with APIs not listed in the DPD and categorized them into the following 5 classes: (1) “existing drug class,” if there was at least 1 drug with the same mechanism of action marketed in Canada; (2) “therapeutically similar,” if there was a drug in another class with similar effectiveness and safety marketed in Canada; (3) “pre-notice of compliance,” if there was a submission for the drug pending regulatory review, as listed on Health Canada’s Drug and Health Product Submissions Under Review database; (4) “atypical access available,” if available through special access programs from manufacturers or government agencies; and (5) “unavailable without alternatives marketed.”8 The availability of drugs with comparable effectiveness and safety was determined through a search of available literature and product labeling. Similar effectiveness and safety in humans according to the literature was reviewed by 2 authors (CC and MH), with disagreements reconciled by a third author (MT).

The therapeutic value of drugs in the “unavailable without alternatives marketed” category was determined by searching the databases of 3 organizations that evaluate the efficacy and safety of new drugs: Prescrire International, an independent French bulletin; the Haute Autorité de Santé, the French body that assesses the efficacy and safety of drugs; and the Institute for Quality and Efficiency in Health Care, the German health technology assessment organization.9-11 We selected these 3 organizations because they report in English and use ordinal ratings that allow discrete categorizations of the additional therapeutic value of medicines. Their assessments are rigorous and systematic, and their ratings have been used by other researchers.12 If more than 1 organization assessed a drug, the highest rating was used.

Data analysis was descriptive and completed using R 4.3.1 and Microsoft Excel. With the exception of MIDAS, all data were publicly available, and the University of Pittsburgh Institutional Review Board approved our study (#21060160). Results are reported according to the STROBE Reporting Guidelines.13

Results

There were 2,084 drugs (defined at the unique API[s] and formulation level) purchased in the United States but not in Canada. After applying exclusions, our final analysis included 399 drugs (Figure 1). Among drugs in the United States that had matching APIs and formulation in Canada, 120 (30%) were “cancelled post-market” and 38 (10%) were in one of the following subcategories: “dormant; approved but not marketed; cancelled pre-market.” There were 49 (12%) drugs that had “matching API but different formulation” in Canada. Among drugs in the United States that did not have matching APIs in Canada, 130 (33%) were part of an “existing drug class,” 35 (9%) had “therapeutically similar” alternatives, 3 (1%) were at the “pre-notice of compliance” stage of drug approval, and 15 (4%) had “atypical access available.”

FIGURE 1.

Flow Diagram for Classifying Products Purchased in the United States From 2017 to 2021, Compared With Canada

Only 9 (2%) drugs were unique to the United States without therapeutic equivalents in Canada. Six of the 9 drugs had been evaluated by 1 or more organizations and all 6 were rated as offering minor to no therapeutic value (Supplementary Table 1 (199KB, pdf) , available in online article). The therapeutic value of the remaining 3 has yet to be given an ordinal therapeutic rating by the 3 organizations that we consulted.

Discussion

Among 399 drugs available in the United States that are not on the Canadian market, only 9 are unavailable as an API in Canada and 6 of these only offer little to no therapeutic value compared with available therapies. Our research found that many of the drugs not available in Canada have therapeutic and chemically similar alternatives in Canada, suggesting that few of the drugs unavailable in Canada would be likely to have important health impacts on a population level.

This study builds on previous research that has looked at drugs that are approved in the United States and have not been submitted to Health Canada for approval.14,15 Lexchin found that of the 364 new drugs approved by the FDA between 2014 and 2021, 116 (31.9%) were not submitted to Health Canada. Although there was no relative change in the introduction of therapeutically important new medicines compared with all medicines not marketed in Canada, the absolute number decreased.14 Gaudette et al concluded that most of the new active substances approved by either the FDA or the European Medicines Agency and not submitted for Health Canada review would reach few Canadians and would have a limited health impact.15 None of the 3 drugs without therapeutic ratings that were only available in the United States appear to have significant therapeutic value. One drug (fenoldopam), once used for treating hypertensive emergencies, has been discontinued in both its brand name and generic forms in the United States, indicating its limited value, whereas another (omacetaxine mepesuccinate), a second-line treatment for chronic myeloid leukemia in patients unresponsive to tyrosine kinase inhibitors, is not listed by the National Cancer Institute as a treatment option.16 A third drug (pramlintide), used for insulin-dependent diabetes (types 1 and 2), shows potential benefits in glycemic control and weight reduction, but its low-quality evidence and associated risks such as diabetic ketoacidosis and gastrointestinal issues highlight the need for further long-term studies to assess its clinical value.17

The majority of new drugs introduced into high-income countries lack significant new therapeutic benefits compared with existing products. Out of 267 new drugs approved by either the FDA or the European Medicines Agency in the decade 2007-2017 that had their therapeutic value evaluated by at least 1 of 5 independent organizations, only 31% had a high therapeutic value.7 In this analysis, ratings of “moderate” or better qualified as “high.”7 In Canada, only 52 (15.1) new drugs out of 345 approved between 1997-2012 were rated as innovative.18 New drugs launched in the United Kingdom over roughly the same time period were rated as highly, moderately, and slightly innovative based on criteria that incorporated clinical usefulness (offering a therapeutic advantage) and the process through which innovation arises (ie, through a revolutionary or disruptive transformation and incorporating an assessment of pharmaceutical novelty). Out of 290 drugs, 26%, 18%, and 56% were rated highly, moderately, and slightly innovative, respectively.19 After investigating the added therapeutic benefit of 216 new drugs and new indications for existing drugs introduced into the German market between 2011 and 2017, the German health technology assessment agency Institute for Quality and Efficiency in Health Care (IQWiG) concluded that only 54 (25%) had a considerable or major added benefit.20

One of the most frequent defenses in favor of drugs that do not offer a significant therapeutic gain is that the presence of these drugs increases patient choice. In theory, this argument is true, but the reality is that clinical trials do not test new drugs on patients who have either not responded to existing therapies or who have discontinued their treatments because of side effects. The result is that when these new “me-too” drugs appear on the market, their place in the therapeutic armamentarium is largely unknown. Furthermore, very few premarket clinical trials are superiority ones; in a Canadian study looking at drugs approved between 2012 and 2021, the figure was less than 2% of 664 trials.21

Finally, companies claim that the revenue from the drugs that lack major therapeutic innovation is important in generating the capital needed for research and development into new drugs. However, over the decade 2012-2021, 14 leading pharmaceutical companies distributed $747 billion to shareholders in the form of dividends and share buybacks compared with spending $660 billion on research and development (R&D).22 This disparity indicates that although companies emphasize the importance of these revenues for R&D, a notable portion of profits is also directed toward enhancing shareholder value, which raises questions about the balance between reinvestment in research and rewarding investors. Furthermore, the precise allocation of funds between R&D and shareholder returns is often opaque, making it challenging to assess the true impact of these investments on innovation. It is also important to consider that companies face significant uncertainty regarding the outcomes of their R&D efforts, which can influence how they allocate their profits and develop their business strategies.

LIMITATIONS

Our results are not without limitations. First, we had available drug purchasing data from 2017 to 2021 and the results may have slightly changed in the last 2 years. The length of our study window allowed us to potentially capture drugs despite temporary disruptions in drug utilization; however, drug listing status may have changed during or after this period. We accounted for drug status changes by checking the listing status of these drugs by the FDA and Health Canada in 2023. Second, there is some added value in having differing formulations and combination drugs for patients. However, these products likely do not warrant being considered breakthroughs; their absence does not limit patient outcomes to a large degree, and they can be more expensive. Third, we attempted to capture alternative routes of access in Canada for drugs not sold there. Importantly, many of these drugs may be accessible through drug access programs, such as compassionate use or special access programs, with response times from Health Canada typically within 1 day and approval rates of more than 90%, and thus they may still be available to Canadians. Some access programs may have been missed or have more informal routes that we are unable to capture. We did not consider informal access as being true access. Lastly, we did not conduct a true assessment of value but rather leveraged external assessment of clinical value, which was not available for all drugs. Future work should further explore the added true value gained from drugs unique to the United States in a more systematic manner.

Conclusions

This study highlights that many drugs available in the United States but not in Canada already have existing therapeutically and chemically similar alternatives in Canada and that only a small number of drugs are unique to the United States despite its higher drug spending per capita. Further research is needed to develop a more nuanced assessment of the added value of combination therapies and different formulations at an individual level to assess whether the extra spending per capita is providing US residents with access to true therapeutic innovation.

Funding Statement

This project was funded through a grant from AHRQ (R01-HS-027985) “Clinical implications of drug shortages during COVID-19 in the United States and Canada” to Dr Suda. The funder/sponsor did not participate in the work.

REFERENCES

- 1.OECD. Health at a Glance 2023: OECD Indicators. OECD Publishing; 2023. [Google Scholar]

- 2.Shajarizadeh A, Hollis A. Delays in the submission of new drugs in Canada. CMAJ. 2015;187(1):E47-51. doi:10.1503/cmaj.130814 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.Cicchiello A, Gustaffson L. Brand-name drug prices: The key driver of high pharmaceutical spending in the US. Commonwealth Fund. 2021;(November):17. [Google Scholar]

- 4.Statistica. Prescription drugs – worldwide. 2024. Accessed August 26, 2024. https://www.statista.com/outlook/hmo/pharmacies/prescription-drugs/worldwide

- 5.Centre for Innovation in Regulatory Science. R&D Briefing 77: New drug approvals in six major authorities 2010–2019: Focus on Facilitated Regulatory Pathways and Internationalisation. Centre for Innovation in Regulatory Science. CIRS; 2020. [Google Scholar]

- 6.Morgan S, Lopert R, Greyson D. Toward a definition of pharmaceutical innovation. Open Med. 2008;2(1):e4-7. [PMC free article] [PubMed] [Google Scholar]

- 7.Vokinger KN, Kesselheim AS, Glaus CE, Hwang TJ. Therapeutic value of drugs granted accelerated approval or conditional marketing authorization in the US and Europe from 2007 to 2021. JAMA Health Forum. 2022;3(8):e222685. doi:10.1001/jamahealthforum.2022.2685 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Valiquet D. The Patented Medicines (Notice of Compliance) Regulations. Parliamentary Information and Research Service; 2006. https://publications.gc.ca/collections/Collection-R/LoPBdP/PRB-e/PRB0614-e.pdf [Google Scholar]

- 9.Institut für Qualität und Wirtschaftlichkeit im Gesundheitswesen. Accessed August 26, 2024. https://www.iqwig.de/en/

- 10.Haute Autorité de Santé. Accessed August 26, 2024. https://www.has-sante.fr

- 11.Prescribe International. Prescribe international publications, 2023. Accessed August 26, 2024. https://english.prescrire.org/en/Summary.aspx [Google Scholar]

- 12.Hwang TJ, Ross JS, Vokinger KN, Kesselheim AS. Association between FDA and EMA expedited approval programs and therapeutic value of new medicines: Retrospective cohort study. BMJ. 2020;371:m3434. doi:10.1136/bmj.m3434 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 13.Von Elm E, Altman DG, Egger M, Pocock SJ, Gøtzsche PC, Vandenbroucke JP; STROBE Initiative. The Strengthening the Reporting of Observational Studies in Epidemiology (STROBE) statement: Guidelines for reporting observational studies. J Clin Epidemiol. 2008;61(4):344-9. doi:10.1016/j.jclinepi.2007.11.008 [DOI] [PubMed] [Google Scholar]

- 14.Lexchin J. Therapeutic value of new medicines not submitted to Health Canada 2014-2021: Cross-sectional study. Health Policy. 2023;136:104901. doi:10.1016/j.healthpol.2023.104901 [DOI] [PubMed] [Google Scholar]

- 15.Gaudette É, Rizzardo S, Wladyka SB, Rahman T, Pothier KR. Is Canada missing out? An assessment of drugs approved internationally between 2016 and 2020 and not submitted for Health Canada review. CMAJ. 2023;195(23):E815-20. doi:10.1503/cmaj.230339 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 16.Rosshandler Y, Shen AQ, Cortes J, Khoury HJ. Omacetaxine mepesuccinate for chronic myeloid leukemia. Expert Rev Hematol. 2016;9(5):419-24. doi:10.1586/17474086.2016.1151351 [DOI] [PubMed] [Google Scholar]

- 17.Avgerinos I, Manolopoulos A, Michailidis T, et al. Comparative efficacy and safety of glucose-lowering drugs as adjunctive therapy for adults with type 1 diabetes: A systematic review and network meta-analysis. Diabetes Obes Metab. 2021;23(3):822-31. doi:10.1111/dom.14291 [DOI] [PubMed] [Google Scholar]

- 18.Lexchin J. Health Canada’s use of its priority review process for new drugs: A cohort study. BMJ Open. 2015;5(5):e006816. doi:10.1136/bmjopen-2014-006816 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Ward DJ, Slade A, Genus T, Martino OI, Stevens AJ. How innovative are new drugs launched in the UK? A retrospective study of new drugs listed in the British National Formulary (BNF) 2001-2012. BMJ Open. 2014;4(10):e006235. doi:10.1136/bmjopen-2014-006235 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Wieseler B, McGauran N, Kaiser T. New drugs: Where did we go wrong and what can we do better? BMJ. 2019;366:l4340. doi:10.1136/bmj.l4340 [DOI] [PubMed] [Google Scholar]

- 21.Lexchin J. Quality and quantity of data used by Health Canada in approving new drugs. Original Research. Front Med (Lausanne). 2023;10:1299239. doi:10.3389/fmed.2023.1299239 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 22.Lazonick W, Tulum Ö. Sick with “shareholder value”: US pharma’s financialized business model during the pandemic. Compet Change 2023;28(2):251-73. doi:10.1177/10245294231210975 [Google Scholar]