Abstract

Objectives

To develop a framework of factors to characterize health plans, to identify how plan characteristics were measured in a national survey, and to apply our findings to an analysis of the predictors of screening mammography.

Data Source

The primary data were from the 1996 Medical Expenditure Panel Survey.

Study Design

Women ages 40+, with private insurance, and no history of breast cancer were included in the study (N=2,909). We used multivariate logistic regression to estimate mammography utilization in the past two years relative to health plan and demographic factors. Health plan measures included whether there is a defined provider network, whether coverage is restricted to a network, use of gatekeepers, level of cost containment, copayment and deductible amounts, coinsurance rate, and breadth of benefit coverage.

Principal Findings

We found no significant difference in reported mammography utilization using a dichotomous comparison of individuals enrolled in managed care versus indemnity plans. However, women in health plans with a defined provider network were more likely to report having received a mammogram in the past two years than those without networks (adjusted OR=1.21, 95 percent CI=1.07–1.36), and women in gatekeeper plans were more likely to report receiving mammography than those without gatekeepers (adjusted OR=1.18, 95 percent CI=1.03–1.36). Restricted out-of-network coverage, use of cost containment, enrollee cost sharing, and breadth of benefit coverage did not appear to affect mammography use.

Conclusions

It is important to examine the effect of individual health plan components on the utilization of health care, rather than use the traditional broader categorizations of managed versus nonmanaged care or simple health plan typologies.

Keywords: Health plans, mammography screening, managed care, utilization

Understanding the influence of managed care on the utilization of preventive health services has been problematic, partly because well-developed measures of health plans are not readily available. Previous studies typically used dichotomous comparisons such as “managed care” versus fee-for-service, or health maintenance organization (HMO) versus non-HMO (e.g., Haas et al. 2002; Tu, Kemper, and Wong 1999). Phillips et al. (2000) reviewed all relevant studies published between 1990 and 1998 (18 studies) to examine whether enrollees in managed care plans receive more preventive services than those enrolled in fee-for-service plans. They found that the majority of studies relied upon poorly defined categories of health plans based only on patient-level measures of insurance and that the overall evidence on the impact of managed care on utilization was uncertain. Among the studies reviewed, 37 percent indicated that managed care enrollees were significantly more likely to receive preventive care; 3 percent indicated that they were significantly less likely to do so; and 60 percent found no difference in utilization.

Other studies have examined differences in utilization using existing plan typologies, for example comparing HMOs, preferred provider organizations (PPOs), independent practice associations (IPAs), and so on (e.g., Gordon, Rundall, and Parker 1998). However, such plan categorizations may no longer be as useful because the characteristics that constitute different insurance products may now vary or be as similar within a particular type as between types (McGlynn 1998). Even traditional fee-for-service plans have embraced some aspects of managed care, further blurring the distinction between managed and “nonmanaged” care.

There have also been efforts to replace older managed care typologies with more sophisticated frameworks (e.g., Brach et al. 2000; Weiner and de Lissovoy 1993). Applying these more complex and comprehensive typologies, however, may pose a significant challenge to researchers seeking explicit and concise measures to use in empirical analyses. What appears lacking in the literature is a framework that is “user-friendly” and that looks beyond the traditional insurance labels to the specific features of health plans that may affect the utilization of health services.

The objectives of this study were to:

1. Develop a framework of factors and measures to explicitly characterize health plans;

2. Identify health plan measures available in the 1996 Medical Expenditure Panel Survey (MEPS); and

3. Apply our findings to an empirical analysis of the predictors of women's use of screening mammography.

Screening mammography was chosen as the outcome variable of interest in order to put a framework of health plan characteristics “to the test” in understanding the use of one preventive health service. Several policy organizations have endorsed periodic mammography, but differ on the recommended interval and age to begin screening (American Cancer Society 1997; American College of Obstetricians and Gynecologists 2000; American Medical Association 1999; Feig et al. 1998). In February 2002, the U.S. Preventive Services Task Force (USPSTF) updated its previous guidelines to advise screening mammography every one to two years for women ages 40 and older (U.S. Preventive Services Task Force 2003).

Although general consensus has been reached on the value of preventive screening, at least for some age groups, many women do not receive mammograms as frequently as recommended. A study based on the National Health Interview Survey (NHIS) found that only about one quarter (27 percent) of women ages 50 to 74 had the appropriate number of lifetime mammography exams recommended in national guidelines (Phillips, Kerlikowske et al. 1998). Estimates vary widely, but a steadily upward trend of mammography utilization in the past decade has been noted. Between 1990 and 2000, the percent of women 40 years of age and older who reported a screening mammogram within the past two years increased from 52 to 70 percent (National Center for Health Statistics 2002). Factors consistently associated with higher rates of screening mammography include younger age, higher education, higher income, urban residence, having a usual source of health care, physician recommendation, and reported breast problems (Hsia et al. 2000; Phillips, Kerlikowske et al. 1998; Zapka et al. 1991).

The present study extends the scope of earlier research on mammography by examining the relationship between specific health plan characteristics and women's likelihood of being screened. Our aim was to first create a framework of factors for characterizing health plans that may be useful to researchers studying the effects of managed care and to then identify plan measures available in one national survey. Moving beyond simple, dichotomous comparisons and older typologies of managed care, we then estimate the influence of several organizational and financial characteristics of health plans on women's completion of screening mammography.

Theoretical Framework

Conceptual Model

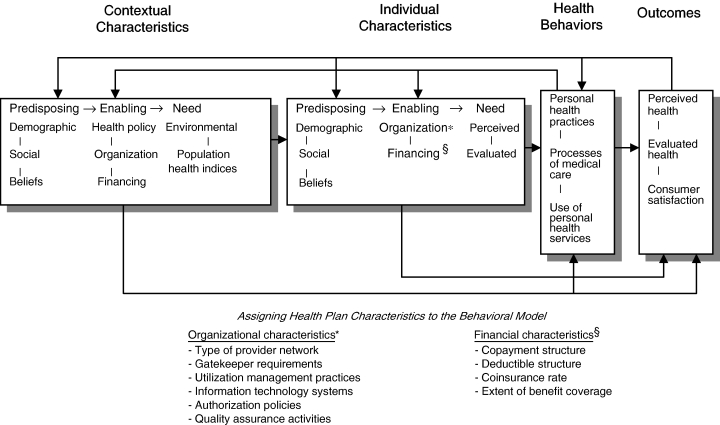

The conceptual model for this study (Figure 1) derives from the behavioral model of health care utilization, a widely used framework developed by Andersen, Aday, and others (Aday, Andersen, and Fleming 1980; Andersen 1968; Andersen 1995; Phillips, Morrison et al. 1998). This model integrates a broad range of individual and contextual factors found to be associated with health services use and has been well described elsewhere (e.g., Andersen and Davidson 2001).

Figure 1.

The Behavioral Model of Health Services Utilization

Source:Andersen and Davidson (2001)

The behavioral model serves as the underlying model for our analyses, however, we refined this framework with additional measures of the health care delivery system that we have not seen described previously in relation to the model. Specifically, we assigned several health plan characteristics as individual, enabling characteristics.1 Type of provider network, gatekeeper requirements, utilization management practices (e.g, disease management, clinical guidelines, cost containment, and so on), information technology systems (e.g., reminders for patients' ongoing care needs, provider education, and so on), authorization policies (e.g., prior authorization for specialist care or hospitalization, and so on), and quality assurance activities (e.g., provider profiling and credentialing, grievance and appeals process, and so on) are listed as organizational characteristics of the health plan that are expected to influence health services use. Copayment structure, deductible structure, coinsurance rate, and the extent of benefit coverage are included as financial plan characteristics seen as likely to impact utilization behavior.

Health plans may be in a unique position to influence the use of screening mammography because of their organizational and financial links to both providers and patients. Plans typically use a variety of information-sharing mechanisms to promote mammography screening (e.g., disseminating screening guidelines via websites, newsletters, and provider manuals, sponsoring phone and postcard reminder systems, and so on). As a HEDIS (Health Plan Employer Data and Information Set) measure of performance, health plans may also track mammography rates and then use such quality benchmarks to motivate networked physicians to encourage screening among their patients.

Such information-sharing strategies may be particularly effective when coupled with a more centralized health plan structure that limits enrollees' choice of providers. Organizational characteristics such as having a defined provider network, restricted out-of-network coverage, use of gatekeepers, and the use of cost containment measures (e.g., penalty for second surgical opinion or for emergency room use out of network) may contribute to a more formalized plan structure with established communication channels. These plan features may increase the capacity of the plan to manage information flows from administrators, to providers and to patients related to the appropriate use of screening mammography. Primary care gatekeepers also serve as an important conduit of information to patients about the need for preventive care. The use of gatekeepers may improve the ability of health plans to convey information to their enrollees regarding the importance of adhering to screening guidelines. Restricting patients' choice of providers through defined network arrangements, cost containment, and reduced out-of-network coverage may also help facilitate mammography utilization. With a more limited pool of providers to target, the health plan may be better able to share information related to mammography screening protocols and guidelines, and thereby increase utilization.

With regard to financial features of the health plan, both economic theory and empirical evidence suggest that deductibles, coinsurance, copayments, and other forms of patient cost sharing may curb the utilization of health services (Broyles and Rosko 1988; Solanki and Schauffler 1999). Similarly, restricting the provision of benefits for a group of health services may decrease use within that category of service. Lower patient cost sharing and more extensive plan benefit packages are expected to result in a lower effective “price” to the enrollee for screening mammography services. Although they are indirect measures of the cost of obtaining a mammogram, these financial characteristics may increase the demand for screening mammography, and thereby increase utilization.

Study Hypotheses

By deconstructing health insurance into its individual plan characteristics, we adopt a “components approach” to predict how specific features of the health plan influence women's use of screening mammography. Below, we present hypotheses based on health plan information available for the study.

Organizational Characteristics of the Health Plan:

H1: Individuals in plans with a defined provider network will have higher screening utilization than individuals without a defined network.

H2: Individuals in plans that restrict coverage for care to a network will have higher screening utilization than individuals in plans that do not restrict coverage to a network.

H3: Individuals in plans with gatekeepers will have higher screening utilization than individuals in plans without gatekeepers.

H4: Individuals in plans that use cost-containment strategies will have higher screening utilization than individuals in plans that do not use cost containment.

Financial Characteristics of the Health Plan:

H5: Individuals in plans with lower patient cost sharing will have higher screening utilization than individuals in plans with higher cost sharing.

H6: Individuals in plans with greater benefit coverage will have higher screening utilization than individuals in plans with less benefit coverage.

Methods

Data Sources

The principal data were obtained from the 1996 MEPS. The MEPS is a nationally representative survey sponsored by the Agency for Healthcare Research and Quality (AHRQ) and the National Center for Health Statistics. This survey was chosen because it is widely used to examine the association of health insurance with outcomes at the patient level, and it includes detailed measures of insurance coverage and health plan characteristics. The MEPS Household Component (HC) is the core survey with a 1996 response rate of 78 percent and a sample size of 22,601 (Agency for Healthcare Research and Quality 2000). The MEPS HC uses an overlapping panel design in which data are collected through a series of five rounds of interviews over a two-and-a-half-year period. Using computer-assisted personal interviewing (CAPI) technology, data for two calendar years were collected from each household.

We also included data from the MEPS Health Insurance Plan Abstraction (HIPA) file (Agency for Healthcare Research and Quality 2001). The HIPA obtains data on private insurance plans held by MEPS household respondents by coding data from health plan booklets mailed in by respondents. Thus, the MEPS contains data not only from individual consumers but their health plan booklets, which expands and validates individual reports of coverage. The 1996 linked MEPS HC-HIPA files contained information for 54 percent of the potential population. Finally, we used a limited amount of data from the 1995 National Health Interview Survey (NHIS) to examine health insurance coverage for the year before data obtained from the MEPS. The sampling frame for the 1996 MEPS is drawn from the 1995 NHIS, and therefore the NHIS provides lagged and validation data for these respondents that would otherwise be unavailable.

Sample Selection

The study sample included women ages 40 and older with private health insurance (N =2,909). Analyses excluded publicly insured respondents2 because limited data were obtained on these individuals' insurance characteristics in MEPS and in order to have a more homogeneous study population. Respondents with multiple plans were coded based on the characteristics of any of their health plans since their primary plan was not identified.

Measures

We developed a core list of factors for characterizing health plans and then mapped available MEPS measures onto this framework (Table 1). In our table, we distinguish four primary perspectives: enrollee, medical group, provider, and plan. Although the perspectives overlap to some degree, the categorization provides a useful organizing framework for characterizing health plans.

Table 1.

A Framework of Health Plan Factors and Available MEPS Measures

| Perspective | General Factors | MEPS Measures |

|---|---|---|

| Enrollee | Choice of providers/Existence of network | • Whether a defined network of providers |

| Out-of-network coverage | • Whether coverage for care is restricted to a network | |

| Use of gatekeepers | • Whether plan requires enrollee to sign up with a primary care gatekeeper | |

| Cost-sharing | • Copayment amount | |

| • Deductible amount | ||

| • Coinsurance rate | ||

| Benefit coverage | • Breadth of plan's benefit coverage (coverage of medical, dental, vision, and prescription drug services) | |

| Provider | Basic compensation arrangement to provider | § |

| Nature of risk or rewards to providers | § | |

| Contractual exclusivity | § | |

| Medical Group | Basic compensation to medical group | § |

| Nature of risk or rewards to medical group | § | |

| Practice arrangements | § | |

| Plan | Administrative and management strategies (“utilization management”) | • Level of cost containment used by plan (use of utilization review, preadmission certification, etc.) |

| Provider networks | § | |

| Ownership/Governance | § |

Data not available in the1996 MEPS HC or MEPS HIPA data files.

Our framework of health plan factors was informed by a literature review and synthesis of articles published between 1990 and 2000 that contained conceptualizations, measures, and typologies of managed care and health plans. We included articles in our review if they:

Described a framework or typology of managed care or health insurance; or

Defined specific characteristics or measures for categorizing health plans; and

Were published between January 1990 and December 2000 (last search conducted May 2001).

We identified a total of 10 articles that met our search criteria (Brach et al. 2000; Conrad et al. 1998; Docteur, Colby, and Gold 1996; Gold and Hurley 1997; Grembowski 1998; Grembowski et al. 2000; Landon, Wilson, and Cleary 1998; Tu, Kemper, and Wong 1999; Weiner and de Lissovoy 1993; Welch, Hillman, and Pauly 1990). These articles included both solely conceptual typologies (n =6) and empirical studies that developed health plan measures (n =4).

Based on the articles, we identified 14 general factors and multiple specific measures for characterizing health plans (see Appendix for complete framework). For example, under the enrollee perspective, we identified cost sharing as a general factor and copayment, deductible, and coinsurance rate as specific measures for this concept. Since our aim was to synthesize the existing recent literature, only health plan factors evident in the reviewed articles were included in our final table. However, we do note additional relevant factors that have become more important in recent years, such as the type of specialists that can be seen without referral and variations in compensation arrangements for providers.

Dependent Variable

The completion of a mammogram within the past two years was the outcome variable of interest. Biennial rather than annual screening was chosen for the outcome measure because of variation in guidelines issued by organizations and to provide a conservative estimate of adherence to recommendations.

Control Variables

Demographic data included age, race/ethnicity, education level, marital status, and residence (MSA versus non-MSA). Frequency of dental check-up in the past year included the categories: never, less than once a year, once a year, twice a year or more. This variable was included as a measure of the individual's “preventive orientation,” or propensity toward obtaining preventive health care. The number of office-based doctor visits in the past year was included as a measure of individuals' interaction with and overall exposure to the health care system. These control variables were all derived from individual self-report3 in the MEPS survey. In addition, an insurance coverage variable combined data from the MEPS and NHIS to indicate the number of months the respondent had coverage over the past two years.

Health Plan Variables

Health plan variables were selected based on the conceptual model and a mapping of available MEPS data onto our framework of plan factors. Plan measures were derived from self-report, information obtained from the health plan booklets mailed in by MEPS survey respondents, or a combination of these data sources (described below).

Managed care versus indemnity plan

We categorized respondents as being in a managed care or indemnity plan based on the plan type recorded in the plan booklet (HIPA data file). This variable was used for the dichotomous comparison of managed care versus indemnity.

Whether a defined provider network

Respondents were designated as having a plan with a defined network of providers if any of the following were true: (1) the respondent self-reported being in an HMO or having a book or list of doctors associated with their health plan; or (2) the plan booklet indicated the plan was a PPO, exclusive provider organization (EPO), HMO, or an HMO with a point of service (POS) option.

Whether coverage for care is restricted to a network

Respondents were defined as being in a plan that restricts coverage for care to a network if any of the following were true: (1) the respondent self-reported being in a plan that does not pay for visits to a doctor outside the plan without a referral; or (2) the plan booklet indicated the plan was a closed HMO or EPO.

Use of gatekeepers

Respondents were considered as being in a gatekeeper plan if any of the following were true: (1) the respondent self-reported being in an HMO4 or being in a plan that required them to sign up with a gatekeeper; or (2) the plan booklet indicated that a primary care doctor referral is required in order to see a specialist.

Use of cost-containment measures

Based on plan booklet data, a dichotomous measure of cost containment was created by combining eight different HIPA variables indicating the health plan's use of cost containment strategies.5

Copayment amount

Copayment amount was obtained from the copayment for an office-based physician visit reported in the health plan booklet. If respondents reported having more than one health plan, the minimum copayment amount was used for the measure. Copayment categories of none, $1–5, $6–10, and $11+ were used for the descriptive analyses, while a continuous variable was used in regression analyses.

Deductible amount

This measure was derived from the individual deductible amount for a doctor visit reported in the plan booklets. For respondents with multiple health plans, the minimum deductible amount across all plans was used. Deductible categories of none, $1–100, $101–250, and $251+ were used in the descriptive analyses, while a continuous variable was used in regression.

Coinsurance rate

Coinsurance rate was determined using a MEPS plan booklet variable that provided “the percent of total costs for a doctor visit that are covered by the insurance plan after any deductibles have been met and before maximums take effect” (Agency for Healthcare Research and Quality 2001).6 The coinsurance rate variable was categorized as none, 1–19 percent, and 20 percent or more for the descriptive analyses, while a continuous variable was used in the regression models.

Breadth of plan's benefit coverage

The health plan's breadth of benefit coverage was measured using several plan booklet measures. An index was created using four HIPA variables indicating the plan's coverage of medical services (i.e., hospital room and board, office visits, surgery), dental services, vision, and prescription drugs. This variable was coded as 1 if the plan covered medical services only, 2 if the plan covered medical services and one or two additional services, and 3 if the plan covered all four types of services.

Statistical Analyses

We examined bivariate relationships between reported mammography use and categorical versions of the predictor variables using chi-square tests. All analyses were performed using sampling weights to reflect the U.S. civilian, noninstitutionalized population and standard error adjustment to account for the complex survey design (Stata 7.0). We used multivariate logistic regression to estimate the likelihood of being screened by mammography in the past two years. Variables for regression were retained based on theory, a priori study hypotheses, statistical significance, and parsimony. Hosmer-Lemeshow goodness-of-fit tests (Hosmer and Lemeshow 2000) were performed to assess how adequately the models described the outcome measure. We calculated the predicted probabilities of screening mammography (for women in and not in plans with specific features) by adjusting for all covariates based on the characteristics of a “typical” respondent.7 We used instrumental variable estimation and other sensitivity analyses to address the potential for selection bias (see Results; details available on request).

Repeated Regressions Approach

We adopted a repeated regressions approach in order to deconstruct the type of health plan into its constituent components and to test each health plan variable individually. In our first model, we included demographic control variables alone; subsequent models included these same control variables in addition to each health plan variable added one at a time.

Before selecting this analytical strategy, we devoted considerable effort testing “fuller” regression models (i.e., models that entered all health plan variables simultaneously). However, high correlations between many of the health plan variables made it conceptually illogical and statistically difficult to include all of the variables in a model as if they were mutually exclusive. Due to the skip patterns of the MEPS survey, as well as the nature of health plan features, many of our plan measures were strongly associated (e.g., the pairwise correlation between the use of gatekeepers and whether a defined network was 0.7). In addition, when multiple plan variables were entered into regression simultaneously, the model's N was severely reduced (e.g., n =505 versus N =2,909 overall). Although MEPS is one of the few surveys to collect plan booklet data, there is also an inherent limitation in what plan booklets report, resulting in missing or inconsistent data for many of the plan characteristics. Thus, due to multicollinearity concerns and a markedly reduced sample size, we felt it was statistically infeasible to rely on results from the regression models that entered all of the health plan variables at once.

We also considered it essential to test various composite measures that combined multiple plan characteristics into a single index. We carefully reviewed the work of Grembowski et al. (2000) in which the authors develop indexes measuring the degree of “managedness” and covered benefits of health insurance plans. Using our more limited MEPS data, we tested several indexes. For example, an index of “enrollee economic burden,” including information on copayment amount, deductible amount, and coinsurance rate, was created as a measure of the patient's overall financial burden. A separate index for the degree of overall “managedness” of the health plan combined four organizational health plan variables: whether there is a defined network of providers, whether coverage for care is restricted to a network, the use of gatekeepers, and the use of cost-containment strategies. Despite extensive testing of these and similar indexes (e.g., indexes that combined different plan variables, that were assigned different weights, that used additive versus multiplicative values, and so on), bivariate and regression analyses yielded no linear trends and no significant findings.

Results

Overall, 74 percent of the study sample reported having received screening mammography in the past two years.

Bivariate Results

We assessed the bivariate associations between mammography completion and a series of demographic and health plan characteristics (Table 2). First, we found no significant differences in mammography utilization using a traditional and less precise comparison of individuals enrolled in managed care versus indemnity plans (p =.63). However, in analyses focused on specific plan features, women in health plans with a defined provider network were more likely to report having received a mammogram in the past two years than women in plans without networks (77 percent versus 69 percent, p <.001). Similarly, women in gatekeeper plans were more likely to report receiving mammography than women in plans without gatekeepers (77 percent versus 72 percent, p <.001). We found no significant patterns in mammography completion by whether coverage for care is restricted to a network, use of cost containment, copayment and deductible amount for a doctor visit, coinsurance rate, and extent of the plan's benefit package.

Table 2.

Bivariate Relationships between Demographic and Health Plan Variables and Having Had Mammography in Past Two Years

| Variable | N | Percent had mammography in past two years |

|---|---|---|

| Total | 2,807 | 74% |

| CONTROL VARIABLES | ||

| Age | ||

| 40–49 | 1,097 | 71%*** |

| 50–69 | 1,236 | 82% |

| 70+ | 474 | 60% |

| Race/ethnicity | ||

| White | 2,186 | 74% |

| Hispanic | 258 | 72% |

| African American | 275 | 74% |

| Other | 88 | 73% |

| Education | ||

| < High school | 464 | 61%*** |

| High school graduate | 1,072 | 75% |

| College graduate | 968 | 75% |

| > College | 300 | 84% |

| Marital status | ||

| Married | 1,871 | 76%*** |

| Widowed | 409 | 61% |

| Divorced/Separated | 392 | 75% |

| Never married | 135 | 71% |

| Residence | ||

| Non-MSA | 612 | 67%*** |

| MSA | 2,195 | 75% |

| Dental check-up frequency | ||

| Never | 318 | 54%*** |

| Less than once a year | 567 | 63% |

| Once a year | 636 | 75% |

| Twice a year or more | 1,285 | 83% |

| Insurance coverage in past two years | ||

| 0–11 months | 38 | 55%** |

| 12–23 months | 164 | 67% |

| Continuous coverage | 2,605 | 74% |

| Number of doctor visits in past year | ||

| None | 367 | 59%*** |

| 1–2 visits | 762 | 71% |

| 3–4 visits | 533 | 76% |

| 5+ visits | 1,145 | 80% |

| HEALTH PLAN VARIABLES | ||

| Type of health plan | ||

| Managed care | 660 | 76% |

| Indemnity | 117 | 78% |

| Whether defined network of providers | ||

| No | 1,049 | 69%*** |

| Yes | 1,647 | 77% |

| Whether coverage for care is restricted to a network | ||

| No | 672 | 76% |

| Yes | 413 | 78% |

| Use of gatekeepers | ||

| No | 1,290 | 72%*** |

| Yes | 1,327 | 77% |

| Use of cost containment measures | ||

| No | 333 | 79% |

| Yes | 689 | 75% |

| Copayment amount for doctor visit | ||

| None | 651 | 75% |

| $1–5 | 142 | 78% |

| $6–10 | 334 | 78% |

| $11+ | 92 | 74% |

| Deductible amount for doctor visit | ||

| $0 | 877 | 77% |

| $1–100 | 114 | 76% |

| $101–250 | 240 | 73% |

| $251+ | 138 | 79% |

| Coinsurance rate | ||

| 0% | 900 | 76% |

| 1–19% | 109 | 77% |

| 20%+ | 375 | 77% |

| Generosity of plan's benefit package (medical, prescription drugs, dental, vision) | ||

| Medical only | 174 | 72% |

| Medical + 1 or 2 services | 949 | 77% |

| All four services covered | 242 | 79% |

Chi-square test across categories:

p <.001,

p <.01,

p <.05. Higher household income and better health status were also statistically significant predictors of mammography use in the bivariate analyses.

Individual and demographic predictors of mammography completion were as expected based on previous studies. Higher education, married status, more frequent dental check-ups, MSA residence, and a greater number of physician visits in the past year were all strongly and positively associated with mammography completion (p <.001). Women ages 50–69 were also more likely to report mammography use than women ages 40–49 or 70 and older (p <.001). We found no significant difference in screening rates by race overall, while not surprisingly, women reporting continuous insurance coverage over the past two years were more likely report mammography use than women with a lapse in health insurance (p <.01).

Logistic Regression Results

To determine the relative importance of the individual and health plan variables in terms of their predictive value for the completion of mammography, we constructed several logistic regression models with mammography completion in the past two years as the outcome variable (Table 3). In the initial model (Model 1) we included demographic control variables alone. Models 2–9 included these same control variables in addition to each health plan variable added one at a time.

Table 3.

Logistic Regression Results: How Specific Health Plan Characteristics Are Associated with Mammography Utilization

| Model | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | 1* | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| Having a defined provider network | — | 1.21§ | — | — | — | — | — | — | — |

| [1.07–1.36] | |||||||||

| P=.002 | |||||||||

| Coverage for care restricted to a network | — | — | 1.18 | — | — | — | — | — | — |

| [0.83–1.70] | |||||||||

| P=.331 | |||||||||

| Use of gatekeepers | — | — | — | 1.18 | — | — | — | — | — |

| [1.03–1.36] | |||||||||

| P=.021 | |||||||||

| Use of cost-containment measures | — | — | — | — | 0.78 | — | — | — | — |

| [0.56–1.10] | |||||||||

| P=.149 | |||||||||

| Copayment amount | — | — | — | — | — | 1.01 | — | — | — |

| [1.00–1.03] | |||||||||

| P=.104 | |||||||||

| Deductible amount | — | — | — | — | — | — | 1.00 | — | — |

| [1.00–1.00] | |||||||||

| P=.783 | |||||||||

| Coinsurance rate | — | — | — | — | — | — | — | 1.01 | — |

| [1.00–1.02] | |||||||||

| P=.130 | |||||||||

| Breadth of benefit coverage# | — | — | — | — | — | — | — | — | 1.13 |

| [0.92–1.39] | |||||||||

| P=.231 | |||||||||

| Model N | 2,803 | 2,692 | 1,085 | 2,613 | 1,021 | 1,218 | 1,368 | 1,383 | 1,364 |

Model 1 included control variables only.

Regression results reported include Odds Ratio, 95% Confidence Interval, and P-value.

Plan's coverage of medical, dental, vision, and prescriptive drugs services, categorized as 1=medical only, 2=medical + 1 or 2 services, 3=all 4 services covered.

Control variables specified across all models included age (1=50–69, 0=other), race/ethnicity (1=nonwhite, 0=white), education (years), marital status (1=married, 0=other), residence (1=MSA, 0=non-MSA), dental check-up frequency (1=never, 2=< once a year, 3=once a year, 4=twice a year or more), insurance coverage in past two years (1=continuous coverage, 0=not continuous), number of doctor visits in past year, and whether self-report survey response in MEPS.

As in the bivariate analyses, women in plans with a defined network of providers were more likely to be screened than women in plans that did not have a defined network (adjusted OR=1.21, 95 percent CI=1.07–1.36). Similarly, women in gatekeeper plans were more likely to be screened than women in plans that did not require a gatekeeper (adjusted OR=1.18, 95 percent CI=1.03–1.36). The predicted probabilities of screening for a “typical” respondent (adjusted for all covariates) demonstrated only a modest association between these plan features and mammography use. The screening rate for women in defined network plans was calculated as 78 percent versus 75 percent for women in plans without a defined network; likewise, the screening rate for women in gatekeeper plans was 78 percent versus 75 percent for women in plans without gatekeepers. Other health plan covariates tested were not significantly associated with mammography completion.

Finally, we specified a logistic model using an ordinal variable that combined the network and gatekeeper variables, where 0=neither, 1=gatekeeper OR network, 2=gatekeeper and network. This variable was significant and positively associated with screening (adjusted OR=1.10, 95 percent CI=1.03–1.19), suggesting a combined and positive influence on mammography use when both plan features are present.

Selection Bias

An important concern for this study was selection bias, that is, whether certain types of patients choose health plans with certain features, thereby potentially biasing observed findings based on plan characteristics. Many studies have examined whether healthier people enroll in managed care or HMO plans (Hellinger 1995; Hellinger and Wong 2000). However, evidence of selection bias in these studies has been mixed, and we found no research relevant to selection into plans with specific features, such as having a defined provider network or gatekeepers. It is also meaningful to note that approximately half of our sample did not have a choice in plans, and we hypothesized that the potential for selection bias would be much lower among these individuals. Nonetheless, we used several empirical strategies to evaluate whether our results were biased by choice of plans. (See Appendix for specific methods and results).

First, we tested for selection bias using instrumental variable (IV) estimation. The focus of our analyses was on the defined network and gatekeeper variables, since we found these characteristics to be positively associated with mammography screening. We identified two instruments, occupational establishment size and insurance premium in 1995, which were expected to be related to women's choice of plans, but not associated with mammography utilization. Validity of the IVs was assessed by checking for their explanatory power for the defined network and gatekeeper variables and their noncorrelation with mammography use. These instruments performed well in the first stage regressions (p <.01, t-tests). We then conducted the test of endogeneity (i.e., the Davidson and Mackinnon test) and found that we cannot reject the null hypothesis that the defined provider network and gatekeeper variables are exogenous factors. Thus, test results are consistent with the view that estimates from the regular regression models are not subject to selection bias. Applying the instruments in two-stage estimation yielded results that were generally consistent with the results reported above although the odds ratios are increased in magnitude in the instrumented models, suggesting that the uninstrumented models may actually underestimate the true effect. However, confidence intervals for the IV estimates were very large, suggesting that these models were more unstable than the uninstrumented regression models. We therefore present results based on the regular logistic regression models rather than the IV estimates.

We also compared results for women that did and did not have a choice in plans as a way to further assess the selection issue. Logistic results for these two samples were very similar, consistent with the view that selection bias is not a significant factor. Finally, we hypothesized that key dimensions of selection bias are health status and “preventive orientation” (as measured by frequency of dental checkup), and we added these factors as control variables to our models. The fact that results remained robust after controlling for these observable aspects of selection increases our confidence that other unobserved aspects of it are not having a strong influence on our results. Based on these analyses, we conclude that the potential for selection bias is minimal, and if it does exist, it does not appear to affect our key findings.

Discussion

We found that women in health plans that have a defined network of providers or gatekeeper requirements are more likely to report having received screening mammography in the past two years than women in plans without these characteristics. In contrast, restricting out-of-network coverage, use of cost containment, cost sharing, and breadth of benefit coverage did not appear to affect mammography use. Moreover, we found no significant difference in screening mammography using a more traditional comparison of respondents enrolled in managed care versus indemnity plans. These findings indicate the importance of moving beyond simple, dichotomous categorizations and older typologies of managed care, to examine the effect of individual health plan characteristics on the utilization of health services.

Our findings suggest that health plans with defined provider networks or gatekeeper requirements may help facilitate the appropriate use of highly recommended preventive services, such as screening mammography. Limiting the pool of providers may increase the ability of the plan's administrators to convey information to providers, including the importance of promoting mammography among patients. For example, many plans disseminate information on preventive care through provider newsletters, meetings, websites, or e-mail reminders. Such strategies may be even more effective when combined with a defined provider network arrangement. Gatekeepers also serve as important messengers to patients regarding preventive screening and the appropriate adherence to mammography guidelines. As a care coordinator for their patients, gatekeepers may contribute to improved access to care, continuity of care, or the ability to effectively encourage the use of preventive services. Gatekeeper requirements may also increase the likelihood of having a usual source of care, which in previous studies has been shown to increase the use of screening mammography (Gordon, Rundall, and Parker 1998).

Most researchers would agree that studies of health services use should look beyond the broad categorizations of managed care, and the differences in mammography rates among women in plans with different plan components observed in this study supports this view. However, it is important to note that our analyses address only one type of health service, a preventive service that is widely available and strongly promoted among women of certain age groups. The relationship between individual plan characteristics and other types of health services, particularly ones that are less uniformly recommended, could be quite different. For example, a recent study of prostate cancer screening, a more controversial screening procedure, found that having a defined provider network and gatekeeper requirements were associated with lower rates of utilization, while enrollees facing less financial burden (i.e., lower copayments, deductibles, and coinsurance) were more likely to be screened (Liang et al. 2004). Thus, plan characteristics may have a very different impact on utilization, depending on the type of health service being considered, how universally it is recommended, and even patient gender. These relationships should be explored more fully in future studies.

Our analyses were subject to several limitations. First, the MEPS does not provide information on every plan characteristic that may affect utilization in a complex health care environment. Our mapping of MEPS onto a framework of health plan factors indicates that while the survey includes a wide range of plan variables, large gaps remain. As in most population-based health surveys, factors at the enrollee level were the most likely to be included, while little information is measured at the provider, plan, and particularly, medical group level (e.g., provider compensation and contractual arrangements). No one survey can measure all elements related to health insurance, nor should it. However, the use of followback surveys—whether based on plan booklet abstraction or surveys of employers and other insurance providers—can expand the measurement of plan factors and add validity to household data.

Moreover, although study analyses did not demonstrate a significant association between mammography use and several of the health plan variables that we tested (i.e., restricted out-of-network coverage, cost containment, cost sharing, benefit coverage), this may be due to insufficient sample size and power or the fact that many of the plan measures were not directly relevant to mammography screening. For example, our cost-sharing variables were based on out-of-pocket costs for a general office-based doctor visit, rather than being specific to a mammography appointment. The lack of significant associations for some plan characteristics could also reflect the broad diffusion of mammography as a preventive service. Screening mammography is a mandated benefit in most states, receives high public attention, and is tracked within plans as a HEDIS measure. Another screening service with less consumer awareness and a lower diffusion state of its technology (e.g., colorectal screening) could potentially be related to some of these “non-significant” factors.

A further limitation is that our study variables were based primarily on self-report, and may be subject to misclassification error. Although self-reported measures can be inaccurate, our key variables appear reasonably accurate for this study (e.g., 85 percent of gatekeeper plans based on plan booklet data were also classified as gatekeeper plans per self-report). Previous studies also found that respondents are able to recall accurately whether they had a mammogram in a one- to two-year timeframe (Barratt et al. 2000), which was the focus of our analyses.

Another potential problem is the temporal ordering of the dependent and independent variables, an issue typically ignored in prior studies (Phillips, Morrison et al. 1998). While our key plan characteristics were recorded at the time of the MEPS survey, utilization of mammography screening occurs at a point in time earlier. We found similar results in sensitivity analyses restricting our sample to individuals who had continuous insurance coverage in the past two years, using an outcome variable closer to the utilization timeframe (screening within the past year), and using MEPS event level data (i.e., data obtained at the time of a specific visit) that reported both mammography screening use and insurance information simultaneously. However, we could not completely control for possible temporal bias.

Finally, our findings should not be interpreted as demonstrating a direct causal relationship between individual plan characteristics and reported mammography use. The correlation among some of the health plan characteristics was quite high, making it difficult to attribute differences in utilization to one particular plan feature. Due to multicollinearity concerns and model instability, it was not workable to specify all of the health plan variables in the same regression model. We must be careful to conclude that being in a plan with either a defined provider network or a gatekeeper was associated with higher mammography use in this study. Future work is needed to fully ascertain the independent effects of these plan features and to test composite measures of health plan characteristics using comprehensive data sources. While it is important to be cautious about attributing an effect to a specific feature, given the scarcity of research in this area, our findings using a repeated regressions approach warrant further attention.

The health plan components model adopted for these analyses is an important first step in understanding how the different organizational and financial levers in the current health care environment affect individuals' use of health services. We developed an updated framework of health plan measures that is intended to be useful to researchers working with MEPS and similar surveys. Moreover, this study is one of few studies to use recent, nationally representative data to examine the impact of individual plan features on mammography completion. Consumers and policymakers should recognize that individual characteristics of the plan—not just whether or not it is managed care—may affect utilization and outcomes. Although it may be convenient to rely on the broader categorizations in designing policy, it is essential to look past the traditional labels to the specific health plan features that are the foundation of policy concern.

Acknowledgments

We are grateful for contributions from Thomas G. Rundall and Stephen M. Shortell, University of California at Berkeley; Harold S. Luft, Karla Kerlikowske, and Julie Sakowski, University of California at San Francisco; and Laurence C. Baker, Stanford University.

Appendix Complete Framework of Health Plan Factors

| Perspective | General Factors | Specific Factors |

|---|---|---|

| Enrollee | Choice of providers/Existence of network | • No network defined; all providers are accessible |

| • Open network (network exists but enrollees may choose out-of-network providers with coverage, usually at a higher cost) | ||

| • Closed network (network exists and enrollees must stay inside network for care with coverage)* | ||

| Out-of-network coverage | • Whether coverage for care is restricted to a network | |

| Use of gatekeepers | • Whether enrollee must see primary care physician before seeing specialist§ | |

| Cost-sharing | • Copayment amount/coinsurance rate | |

| • Deductible amount | ||

| Benefit coverage | • What services are covered (e.g., drugs, vision) | |

| Provider | Basic compensation arrangement to provider¶ | • Salary |

| • Fee-for-service (discounted, undiscounted) | ||

| • Capitation (full, partial) | ||

| Nature of risk or rewards to providers | • Use of bonuses | |

| • Use of withholds | ||

| • Services that are included in compensation calculations | ||

| • Insurance risk (how risk is shared among different players, including limits put on the risk assumed) | ||

| Contractual exclusivity | • Exclusive | |

| • Providers are members of multiple networks | ||

| Medical Group | Basic compensation to medical group | • NA (no group) |

| • Fee-for-service (discounted, undiscounted) | ||

| • Capitation (full, partial) | ||

| Nature of risk or rewards to medical group | • Use of bonuses, withholds | |

| • Services that are included in compensation calculations | ||

| • Insurance risk (how risk is shared among different players, including limits put on the risk assumed) | ||

| Practice arrangements | • Type of network practice arrangement (e.g., ownership or contract-based integration) | |

| Plan | Administrative and management strategies (“utilization management”) | • NA |

| • Administration (e.g., information system technology, claims processing, and so on) | ||

| • Preauthorization rules (e.g., referral preauthorization for specialist visits) | ||

| • Use of carve-outs | ||

| • Utilization management (e.g., critical pathways, disease management tools, clinical guidelines, information sharing, use of health risk assessments to manage care, drug formularies, prevention-oriented policies, and so on) | ||

| • Quality/consumer satisfaction (e.g., provider profiling and credentialing, grievance and appeals process, quality assurance activities, training or education programs, reporting requirements of the organization, and so on) | ||

| Provider networks | • NA | |

| • Closed network | ||

| • Open network | ||

| Ownership/Governance# | • For-profit/not-for-profit, self-insured | |

| • Participation of providers in medical policy development |

A closed network may be either a fixed roster of providers (with exclusive contracts) or a network of “any willing providers.” However, this distinction was not made explicitly in the key articles reviewed from the enrollee perspective (note that this factor was in the key articles from the provider perspective, i.e., whether the provider has an exclusive contract or sees patients from different plans).

Health plans may also differ in the range of specialists who can be seen without a referral (e.g., ob-gynecologists, dermatologists, cardiologists that may be seen without referral from a primary care physician). Health plans may also differ in whether the rules for self-referral are different for within-network vs. out-of-network referrals and the breadth of coverage for self-referral. These characteristics were not specifically discussed in the key articles reviewed.

Compensation arrangements may also vary by provider within a system and by type of service for an individual provider. Again, this distinction was not noted in the key articles reviewed.

Governance mechanisms may also vary by plan, IPA, or medical group, although this was not explicitly noted in the key articles reviewed.

Notes

It is important to note that health plan characteristics are potentially measured at the group or individual level and could therefore be viewed as appropriate to the contextual characteristics, as well as to the individual characteristics component of the behavioral model. We considered the health plan variables used in this study to be individual characteristics since health plan information was linked in MEPS to individual patients or individual plan enrollees.

Publicly insured respondents included respondents classified in MEPS as having “Medicaid only” or “Medicaid or other public assistance.”

In the study sample, 75 percent of respondents self-reported to the MEPS, while 25 percent of the surveys were completed by someone else in the household other than the woman being screened.

The skip pattern of the MEPS household survey is such that respondents who report being in a closed HMO are not asked regarding gatekeeper requirements, since these HMO enrollees are assumed to be in a gatekeeper plan (Agency for Healthcare Research and Quality 2000). Thus, in creating the gatekeeper variable, respondents that reported being in a closed HMO are assumed to be in a gatekeeper plan.

Strategies included in the cost-containment measure were whether preadmission certification, preadmission testing, utilization/concurrent review, nonemergency weekend admission, penalty for emergency room use out of network, penalty for second surgical opinion, outpatient surgery incentive, and other type of cost containment.

This original MEPS variable incorporated information on both copayments and coinsurance. Thus, the plan's actual coinsurance rate was calculated by combining it with (i.e., subtracting out) the reported copayment amount for a doctor visit.

The probability of mammography screening was calculated for a woman, aged 50–69, white, 12 years of education, married, MSA resident, dental check-up once a year, continuous insurance coverage in past two years, five doctor visits in past year, and self-report survey response.

This work was supported by funding from the National Cancer Institute (R01 CA81130). Partial support was also provided by the Agency for Healthcare Research and Quality (PO1 HS10771 and PO1 HS10856) and the Russell M. Grossman Endowment.

References

- Aday LA, Andersen R, Voorhis Fleming G. Health Care in the U.S.: Equitable for Whom? Beverly Hills, CA: Sage; 1980. [Google Scholar]

- Agency for Healthcare Research and Quality . MEPS HC-012 1996 Full Year Consolidated Data File. Rockville, MD: Agency for Healthcare Research and Quality; 2000. p. C35. [Google Scholar]

- Agency for Healthcare Research and Quality . MEPS HC-017: Household Component—Health Insurance Plan Abstraction Linked Data, 1996. Rockville, MD: Agency for Healthcare Research and Quality; 2001. pp. C9–11. [Google Scholar]

- American Cancer Society ACS Guidelines for the Early Detection of Breast Cancer: Update 1997. CA: A Cancer Journal for Clinicians. 47(3):150–3. doi: 10.3322/canjclin.47.3.150. [DOI] [PubMed] [Google Scholar]

- American College of Obstetricians and Gynecologists . Primary and Preventive Care; Periodic Assessments. Washington, DC: American College of Obstetricians and Gynecologists; 2000. [Google Scholar]

- American Medical Association 1999. Report 16 of the Council on Scientific Affairs(A-99).Mammographic Screening for AsymptomaticWomen. Available at http://www.ama-assn.org/ama/pub/article/2036-2346.html [accessed November 2003].

- Andersen R. A Behavioral Model of Families Use of Health Services. Chicago: Center for Health Administration Studies, University of Chicago; 1968. [Google Scholar]

- Andersen RM. Revisiting the Behavioral Model and Access to Medical Care: Does It Matter? Journal of Health and Social Behavior. 1995;36(1:):1–10. [PubMed] [Google Scholar]

- Andersen RM, Davidson PL. Improving Access to Care in America. In: Andersen RM, Rice TH, Kominski GF, editors. Changing the U.S. Health Care System. San Francisco: Jossey-Bass; 2001. pp. 3–30. [Google Scholar]

- Barratt A, Cockburn J, Smith D, Redman S. Reliability and Validity of Women's Recall of Mammographic Screening. Australian and New Zealand Journal of Public Health. 2000;24(1):79–81. doi: 10.1111/j.1467-842x.2000.tb00728.x. [DOI] [PubMed] [Google Scholar]

- Brach C, Sanchez L, Young D, Rodgers J, Harvey H, McLemore T, Fraser I. Wrestling with Typology; Penetrating The ‘Black Box’ of Managed Care by Focusing on Health Care System Characteristics. Medical Care Research and Review. 2000;57(2, supplement):93–115. doi: 10.1177/1077558700057002S06. [DOI] [PubMed] [Google Scholar]

- Broyles RW, Rosko MD. The Demand for Health Insurance and Health Care; A Review of the Empirical Literature. Medical Care Review. 1988;45(2):291–338. doi: 10.1177/107755878804500205. [DOI] [PubMed] [Google Scholar]

- Conrad DA, Maynard C, Cheadle A, Ramsey S, Marchus-Smith M, Kirz H, Madden CA, Martin D, Perrin EB, Wickizer T, Zierler B, Ross A, Noren J, Liang S. Primary Care Physician Compensation Method in Medical Groups. Journal of the American Medical Association. 1998;279(11):853–8. doi: 10.1001/jama.279.11.853. [DOI] [PubMed] [Google Scholar]

- Docteur ER, Colby DC, Gold M. Shifting the Paradigm; Monitoring Access in Medicare Managed Care. Health Care Financing Review. 1996;17(4):5–21. [PMC free article] [PubMed] [Google Scholar]

- Feig SA, D'Orsi CJ, Hendrick RE, Feig SA, D'Orsi CJ, Hendrick RE, Jackson VP, Kopans DB, Monsees B, Sickles EA, Stelling CB, Zinninger M, Wilcox-Buchalla P. American College of Radiology Guidelines for Breast Cancer Screening. American Journal of Roentgenology. 1998;171(1):29–33. doi: 10.2214/ajr.171.1.9648758. [DOI] [PubMed] [Google Scholar]

- Gold M, Hurley R. The Role of Managed Care ‘Products’ in Managed Care ‘Plans’. Inquiry. 1997;34(1):29–37. [PubMed] [Google Scholar]

- Gordon NP, Rundall TG, Parker L. Type of Health Care Coverage and the Likelihood of Being Screened for Cancer. Medical Care. 1998;36(5):636–45. doi: 10.1097/00005650-199805000-00004. [DOI] [PubMed] [Google Scholar]

- Grembowski DE. Managed Care and Physician Referral. Medical Care Research and Review. 1998;55(1):3–31. doi: 10.1177/107755879805500101. [DOI] [PubMed] [Google Scholar]

- Grembowski DE, Diehr P, Novak LC, Roussel AE, Martin DP, Patrick DL, Williams B, Ulrich CM. Measuring the ‘Managedness’ and Covered Benefits of Health Plans. Health Services Research. 2000;35(3):707–34. [PMC free article] [PubMed] [Google Scholar]

- Haas JS, Phillips KA, Sonneborn D, McCulloch CE, Liang SY. The Effect of Managed Care Insurance on the Use of Preventative Care for Specific Ethnic Groups in the United States. 2002;40(9):743–51. doi: 10.1097/00005650-200209000-00004. [DOI] [PubMed] [Google Scholar]

- Hellinger F. Selection Bias into HMOs and PPOs; A Review of the Evidence. Inquiry. 1995;32(2):135–42. [PubMed] [Google Scholar]

- Hellinger F, Wong H. Selection Bias into HMOs; A Review of the Evidence. Medical Care Research and Review. 2000;57(4):405–39. doi: 10.1177/107755870005700402. [DOI] [PubMed] [Google Scholar]

- Hosmer DW, Lemeshow S. Applied Logistic Regression. New York: Wiley; 2000. [Google Scholar]

- Hsia J, Kemper E, Kiefe C, Zapka J, Sofaer S, Pettinger M, Bowen D, Limacher M, Lillington L, Mason E. The Importance of Health Insurance as a Determinant of Cancer Screening; Evidence from the Women's Health Initiative. Preventive Medicine. 2000;31(3):261–70. doi: 10.1006/pmed.2000.0697. [DOI] [PubMed] [Google Scholar]

- Landon B, Wilson IB, Cleary PD. A Conceptual Model of the Effects of Health Care Organizations on the Quality of Medical Care. Journal of the American Medical Association. 1998;279(17):1377–82. doi: 10.1001/jama.279.17.1377. [DOI] [PubMed] [Google Scholar]

- Liang SY, Phillips KA, Tye S, Haas JS, Sakowski J. Does Patient Cost Sharing Matter? Its Impact on Recommended versus Controversial Cancer Screening Services. American Journal of Managed Care in press. 2004 [PubMed] [Google Scholar]

- McGlynn EA. The Effect of Managed Care on Primary Care Services for Women. Women's Health Issues. 1998;8(1):1–14. doi: 10.1016/s1049-3867(97)00095-9. [DOI] [PubMed] [Google Scholar]

- National Center for Health Statistics . Health, United States, 2002 with Chartbook on Trends in the Health of Americans. Hyattsville, MD: National Center for Health Statistics; 2002. [Google Scholar]

- Phillips KA, Fernyak S, Potosky AL, Halpin Schauffler H, Egorin M. Use of Preventive Services by Managed Care Enrollees; An Updated Perspective. Health Affairs. 2000;19(1):102–16. doi: 10.1377/hlthaff.19.1.102. [DOI] [PubMed] [Google Scholar]

- Phillips KA, Kerlikowske K, Baker LC, Chang SW, Brown ML. Factors Associated with Women's Adherence to Mammography Screening Guidelines. Health Services Research. 1998;33(1):29–53. [PMC free article] [PubMed] [Google Scholar]

- Phillips KA, Morrison KR, Andersen R, Aday LA. Understanding the Context of Health Care Utilization; Assessing Environmental and Provider-Related Variables in the Behavioral Model of Utilization. Health Services Research. 1998b;33(3):571–96. [PMC free article] [PubMed] [Google Scholar]

- Solanki G, Halpin Schauffler H. Cost-Sharing and the Utilization of Clinical Preventive Services. American Journal of Preventive Medicine. 1999;17(2):127–33. doi: 10.1016/s0749-3797(99)00057-4. [DOI] [PubMed] [Google Scholar]

- Stata Corp . Stata Statistical Software: Release 7.0. College Station: Stata Corporation; 2001. [Google Scholar]

- Tu HT, Kemper P, Wong HJ. Do HMOs Make a Difference? Use of Health Services. Inquiry. 1999;36(4):400–10. [PubMed] [Google Scholar]

- U.S. Preventive Services Task Force . Guide to Clinical Preventive Services, Periodic Updates. Rockville, MD: Agency for Healthcare Research and Quality; 2003. [Google Scholar]

- Weiner JP, de Lissovoy G. Razing a Tower of Babel; A Taxonomy for Managed Care and Health Insurance Plans. Journal of Health Politics, Policy and Law. 1993;18(1):75–103. doi: 10.1215/03616878-18-1-75. [DOI] [PubMed] [Google Scholar]

- Welch WP, Hillman AL, Pauly MV. Towards New Typologies for HMOs. Milbank Quarterly. 1990;68(2):221–43. [PubMed] [Google Scholar]

- Zapka J, Stoddard A, Maul L, Costanza M. Interval Adherence to Mammography Screening Guidelines. Medical Care. 1991;29(8):697–707. doi: 10.1097/00005650-199108000-00003. [DOI] [PubMed] [Google Scholar]