Abstract

Objective

To determine who chooses a Consumer-Driven Health Plan (CDHP) in a multiplan, multiproduct setting, and, specifically, whether the CDHP attracts the sicker employees in a company's risk pool.

Study Design

We estimated a health plan choice equation for employees of the University of Minnesota, who had a choice in 2002 of a CDHP and three other health plans—a traditional health maintenance organization (HMO), a preferred provider organization (PPO), and a tiered network product based on care systems. Data from an employee survey were matched to information from the university's payroll system.

Principal Findings

Chronic illness of the employee or family members had no effect on choice of the CDHP, but such employees tended to choose the PPO. The employee's age was not related to CDHP choice. Higher-income employees chose the CDHP, as well as those who preferred health plans with a national provider panel that includes their physician in the panel. Employees tended to choose plans with lower out-of-pocket premiums, and surprisingly, employees with a chronic health condition themselves or in their family were more price-sensitive.

Conclusions

This study provides the first evidence on who chooses a CDHP in a multiplan, multiproduct setting. The CDHP was not chosen disproportionately by the young and healthy, but it did attract the wealthy and those who found the availability of providers more appealing. Low out-of-pocket premiums are important features of health plans and in this setting, low premiums appeal to those who are less healthy.

Keywords: Health insurance, consumer-driven health plans, health plan choice, adverse selection

“Consumer-driven” health plans (CDHPs) have moved beyond the concept stage and are now available to employees of many large companies. Established insurers, such as Aetna, Humana, Cigna, UnitedHealth Group, and WellPoint are introducing their own CDHPs to compete with products offered by start-up companies such as Definity Health, Luminos, MyHealthBank, and others (Freudenheim 2001). It appears that these products appeal to employers in a period when health insurance premiums are rising at double-digit rates (BNA 2001; Gabel, et al. 2001) and a return to more restrictive forms of managed care seems unpalatable to employees (Galvin and Milstein 2002; Iglehart 2002).

A database now exists for assessing the early experience of employers and employees with these plans. Using data from a survey of employees at the University of Minnesota, matched to information from the university's payroll system, we address the question: Who chooses to join a CDHP and, specifically, does this plan attract the healthier employees in a company's risk pool? The research provides important, early information on the impact of CDHPs and the research and policy issues that are likely to arise if they become more commonly available as a health benefit option.

Significance

Consumer-driven health plans differ from traditional insurance and managed care products in design and philosophy (Christianson, Parente, and Taylor 2002; Gabel, Lo Sasso, and Rice 2002; Robinson 2002). In the design of a CDHP plan, a portion of the employer's tax-deductible contribution to health benefits typically is put into a “health spending account” from which the employee purchases services. Major medical insurance or some form of “wrap-around” coverage is also a key part of the benefit design with first-dollar coverage for preventive care often included. If an employee spends all of the dollars in her spending account in a given year, she then spends her own money until the deductible requirement in the major medical coverage is met. Expenditures in excess of the deductible are covered by the major medical plan with an out-of-pocket maximum included in the plan design. The benefit design can be tailored to cover all or a part of these “excess” expenditures.

The use of information technology to create “informed consumers” is a distinguishing CDHP feature (Lutz and Henkind 2000; Wiggins and Emery 2001). To facilitate informed decision making, the employee is provided with information about health care providers, including physician education and experience, prices, and quality ratings. Usually, this information is available on the Internet to ensure easy access and to promote its use (Christianson, Parente, and Taylor 2002). Many CDHPs have interactive customer support systems that allow subscribers to track medical expenditures deducted from their accounts on the Internet. Consumer-directed health plans offer online linkages to prescription drug benefit programs as well as online benefit eligibility information to ensure prompt payment to medical providers.

Interviews with employees and CDHP managers suggest that larger employers find CDHPs attractive for several reasons (Christianson, Parente, and Taylor 2002). Philosophically, these employers want informed employee decisions to “drive the market.” Under the CDHP spending account approach, employers believe their employees have an incentive to seek price information on providers and to carefully consider their need for services, because any unexpended funds “roll over” into next year's account balance (Parrish 2001). This reduces the annual gap between the spending account contribution and the deductible faced by the employee in subsequent years. Also, employers see CDHPs as potentially reducing their administrative expenses. If the CDHP is popular with employees, it may mean that other health plans can be dropped. Finally, some employers may see the CDHP approach as a way to divorce the amount their contribution increases each year from trends in premiums, linking it instead to overall employee compensation increases. In this respect, CDHPs function as “transition vehicles” that could be used to redefine the role of employers as health insurance purchasers, much as defined contribution retirement accounts did with respect to retirement benefits (Trude and Ginsburg 2000).

Health policy analysts and others have expressed concerns about how CDHPs could affect the private health insurance market. As noted in a New York Times article, “some health benefits experts…warn that they [CDHPs] could be more unfair than current plans to people who are sick and that they could discourage people who need care from getting it” (Freudenheim 2001). The issue of “selection” when defined contribution plans are offered alongside more traditional plans has also been raised. This is not a new issue; when HMOs were introduced, it was thought that they might attract a healthier mix of enrollees, leaving sicker employees in conventional plans and driving up premiums in these plans until the plans became unaffordable. Now, it is argued that CDHPs could have a similar effect on HMOs and other health plans. If CDHPs attract healthy employees, premiums in competing plans might increase faster than otherwise would be the case. Depending on pricing strategies and whether or not the employer is self-insured, this could increase total health benefit costs to employers and employees.

Study Setting

This research draws on the early experience of the University of Minnesota, which adopted a CDHP in 2002. The University of Minnesota (UM) is a land-grant university whose main campus is located in the Twin Cities of Minneapolis and St. Paul, with smaller campuses in several other locations throughout Minnesota. The UM has 17,500 employees and annual expenditures of $1.8 billion. Prior to 2002, the UM was part of the State Employees Group Insurance Plan (SEGIP), which covers Minnesota state government employees and their dependents. The SEGIP is the largest employment-based health benefit program in Minnesota, with more than 150,000 covered lives. The SEGIP program offered a variety of health plans—including an HMO and several preferred provider organizations, but it had experienced a period of instability and rising premiums (Sutton, Feldman, and Dowd 2004).

Seeking increased flexibility and a set of stable options, the university decided to withdraw from SEGIP in January 2002. Responding to the needs of a diverse workforce that included clerical, administrative, and professional employees, the university selected an unusually wide set of options: a CDHP, a traditional health maintenance organization (HMO), a preferred provider organization (PPO), and a set of tiered “care systems” that contracted directly with health care providers. The traditional HMO was “HealthPartners Classic,” which had been a popular plan among university employees in the SEGIP program. HealthPartners Classic featured generous coverage for network physicians and hospitals, but it did not cover out-of-network care. It was also the “low-cost” plan for the UM employees in the Twin Cities in 2002, with the UM paying the full cost of employee-only coverage for this option and 90 percent of the difference in premiums between family and employee-only coverage.

The PPO was PreferredOne, with nominal copayments for in-network hospital and health care services and 70 percent coverage for eligible out-of-network expenses after the enrollee paid a deductible. Compared with the low-cost HMO, the PPO was significantly more expensive for employees and dependents.

Under the Choice Plus “care system” product offered by Patient Choice Healthcare, consumers can choose among integrated teams of medical care providers of various structures (basically primary-care-centered health systems with affiliated specialists, hospitals, and allied professionals). Care systems are grouped into three cost tiers with standardized benefits but with different premiums depending on the bids submitted by the care systems in each tier (Christianson et al. 1999; Christianson and Feldman 2002; Schultz 2001).

Finally, the university offered two CDHP products sponsored by Definity Health. Option 1 had deductibles of $1,250 per person and $2,500 per family; Option 2 had deductibles of $2,000 and $4,000. The university allocated $500 for an employee or $1,000 for a family into a personal care account for Option 1; Option 2 had university contributions of $1,000 and $2,000 to the personal care account. Both options featured 100 percent coverage of in-network hospital and health care services once the deductible was met, but Option 2 had 20 percent coinsurance for eligible out-of-network expenses versus 30 percent in Option 1. Both options were available throughout the state, and the total premiums and employee out-of-pocket premiums were priced within a few cents of one another. Table 1 presents 2002 enrollment and premium data for the UM health plans.

Table 1.

2002 Premium Contributions per Biweekly Pay Period and Enrollment

| Employee-Only Coverage | Family Coverage | |||||||

|---|---|---|---|---|---|---|---|---|

| Total Cost | Less UM Contribution | Employee Contribution | Enrollment | Total Cost | Less UM Contribution | Employee Contribution | Enrollment | |

| HealthPartners Classic | $137.84 | $137.84 | $0.00 | 5,027 | $344.59 | $323.92 | $20.67 | 3,967 |

| Patient Choice Cost Group I | $137.84 | $137.84 | $0.00 | $344.59 | $323.92 | $20.67 | ||

| Patient Choice Cost Group II | $147.15 | $137.84 | $9.31 | 2,091 | $363.15 | $323.92 | $39.23 | 2,808 |

| Patient Choice Cost Group III | $157.90 | $137.84 | $20.06 | $389.65 | $323.92 | $65.73 | ||

| PreferredOne National | $189.61 | $137.84 | $51.77 | 731 | $467.83 | $323.92 | $143.91 | 997 |

| Definity Health Option 1 | $150.52 | $137.84 | $12.68 | 349 | $375.55 | $323.92 | $51.63 | 346 |

| Definity Health Option 2 | $150.48 | $137.84 | $12.64 | $375.47 | $323.92 | $51.55 | ||

| Total Single and Family | 8,198 | 8,118 | ||||||

| Total Enrollment | 16,316 | |||||||

UM=University of Minnesota

Data and Methods

To provide empirical evidence on who chooses a CDHP, we conducted an analysis of health plan choice in the first year that Definity Health was introduced into the health benefit offerings at the University of Minnesota. Data for our analysis were taken from two sources: a survey of UM employees, and information from the university's payroll system. We surveyed all UM enrollees in Definity Health during spring 2003 to obtain information on the employee's entire 2002 calendar year experience with his or her health plan. A random sample of non-Definity Health members also was surveyed. Trained employees of the university's human resources department conducted the interviews by phone, which took approximately 10 minutes for non-CDHP enrollees and 15–20 minutes for CDHP enrollees, who responded to a longer set of questions. There were 430 completed interviews from Definity Health enrollees (63 percent response rate) and 501 from enrollees in other health plans (73 percent response rate). The Definity Health response rate was lower because the interviews were conducted during work hours and proportionately more Definity Health members were administrators or medical care providers with administrative staff managing their communications.

Specific questions on the survey drew on our past and ongoing research relating to the Buyers Health Care Action Group (Feldman, Christianson, and Schultz 2000; Schultz et al. 2001) and on other research studies (Schlesinger, Druss, and Thomas 1999; CAHPS™ 1998). We relied on the survey to determine whether the employee or any dependent had a chronic illness. (“Do you or a dependent have a chronic condition such as asthma, hypertension [high blood pressure], diabetes, or arthritis?”) We discuss the validity of this measure of health status in more detail in the concluding section.

We also asked employees to rate the importance of several health plan features, including:

The health plan has a national network of providers and hospitals;

The health plan's network includes my doctors;

The health plan covers preventive care services, such as physical exams;

The health plan does not require referrals or preauthorizations;

The amount of potential out-of-pocket expense (costs in addition to my paycheck contributions) is small, or the health plan has no copayments;

The balance in a personal care account or medical savings account rolls over to the next benefit year to pay for out-of-pocket medical expenses;

The plan has online tools and resources (such as provider lists or prescription drug prices) that I need to manage my health care.

After rating each feature, the employee selected three that were most important. Previous research (Harris, Schultz, and Feldman 2002; Harris and Keane 1999) has shown that these preference ratings can be interacted with choice-specific indicator variables and included in health plan choice models. The coefficients of such variables represent the average amount of each characteristic embodied in each choice, as perceived by the employees who make the choice. For example, employees with a strong preference for “no preauthorizations” should be more likely to choose plans that offer this feature. A positive plan-specific coefficient in the choice model for this preference variable would indicate that the plan in question is perceived as not requiring preauthorizations.

The second data source for our study was information from the university's payroll system. This indicated which plan the employee chose and whether she had single or family coverage, her 2002 federal taxable wages from the university, and certain demographic information such as age, sex, and zip code of residence.

The analysis uses methods that the investigators have applied extensively in prior research (Feldman et al. 1989; Dowd and Feldman 1994/1995; Harris, Schultz, and Feldman 2002). The model's specification is as follows. Let S=(Z1,…,ZJ) be a mutually exclusive and exhaustive choice set of J alternatives, where each alternative j is characterized by a vector of m value-relevant attributes, namely, Zj=(zj1,…,zjm). Let Yi=(yi1,…,yin) be a vector of n attributes characterizing the ith decision maker (either an individual or family) choosing from choice set S. For any such choice set S, and for any decision maker described by the set of attributes Yi, choice models generate a vector of probabilities (Pi1,…,PiJ), where Pij is the probability that the decision maker will choose alternative j from choice set S. The probabilities must sum to one.

Our choice model is based on the theory of utility maximization. We assume that the ith decision maker derives “utility” or satisfaction from alternative j, based on a function of its attributes, Zj, personal attributes, Yi, and interactions between alternative-specific and personal attributes, Xij. Thus, the utility function is Uij=f(Zj,Yi,Xij). For example, utility is considered to be a function of personal attributes such as health status, health plan attributes such as price, and the interaction of price and health status.

We use conditional logit techniques to estimate the utility function, based on the observed health plan choices. This method is motivated by a random utility function because there are errors in maximization due to imperfect perception and optimization, as well as errors due to unobserved relevant variables. Conditional logit estimates the effects of choice and decision-maker characteristics on choice probabilities for all decision-making units, h=1,…,N, as:

where Uhj=αj+β′Zj+γj′Yh+θ′Xhj+ehj for the k=1,…J alternatives in the choice set, αj is an alternative-specific constant with αJ=0, γj is a vector of alternative-specific coefficients with γJ=0, and β and θ are vectors of coefficients that are invariant across alternatives). The random term, ehj, represents unobserved, decision-maker specific aspects of utility from alternative j, which are assumed to be independently and identically distributed with an extreme value distribution.

The price of each health plan (one of the Zj variables in the model) was measured by its “tax-adjusted” out-of-pocket premium, because the UM lets employees pay their out-of-pocket premiums with tax-free dollars (Dowd et al. 2001). Employee health status (a Yh variable) was measured by the response to the survey question on chronic illness. Health status was interacted with plan-specific dummy variables, allowing us to estimate the effect of health status on the probability of joining each plan. Favorable selection into the CDHP plan would be indicated by a negative coefficient on the interaction of “chronic illness × CDHP.”

We multiplied health status times the out-of-pocket premium for each plan to create a new Xij variable in the choice model. The coefficient of this new variable indicates whether employees with chronic illnesses are less sensitive than are “healthy” employees to price differences among health plans. This finding, if observed, would imply that changes in relative prices lead to changes in plans' costs arising from changes in the distribution of risks (Strombom, Buchmueller, and Feldstein 2002).

Following prior research (Schultz 2001), the choice equation includes a number of other Yh variables, such as the employee's gender and her age, each interacted with plan-specific dummy variables. The coefficients of these variables stand for unmeasured characteristics of the choices that provide differential utility to men and women, or older versus younger workers.

How to group the employees for analysis of health plan choice is an important issue. Our previous research suggests that employees should be combined with those who face similar choices, and separate choice models should be estimated for each group (Feldman et al. 1989). In particular, separate choice models should be estimated for (1) single employees with no dependents, (2) families who have no other sources of health insurance, and (3) families who have multiple sources of health insurance (because both spouses or both partners work for companies that offer health insurance). However, in this analysis we could not determine whether employees with single coverage were “true” singles (i.e., single employees with no dependents). Similarly, we did not have access to the other choices faced by employees with family coverage. Therefore, we combined employees with single and family coverage, as has been done by some prior research (Short and Taylor 1989).

Another important estimation issue is whether the alternatives in the choice set are really independent. An alternative assumption is that some choices are closer substitutes than others. The most likely close substitutes would be Definity Health Options 1 and 2. The three cost tiers offered by Choice Plus also represent a plausible set of close substitutes. We considered using the nested logit or multinomial probit models, which impose less-restrictive assumptions about health plan substitution than conditional logit. However, because a low proportion of UM employees chose Definity Health, the sample sizes for Options 1 and 2 were not large enough to estimate the alternative models. Given that nested logit/multinomial probit was not feasible, we also combined the Choice Plus options and assigned the middle-tier premium to this composite product.

The final methodological issue concerns our sampling procedure, which oversampled Definity Health enrollees and undersampled those from other health plans. To correct for this “choice-based” sampling design, we weighted the survey responses by the inverse of the population proportion in each plan. The Manski-Lerman (1977) correction was used at convergence to obtain appropriate standard errors.

Results

In this section we present descriptive statistics, and we discuss the coefficients and marginal effects from the conditional logit model of health plan choice. The descriptive statistics for the data used in the analysis are presented in Table 2. The actual sample means and standard deviations for data on employee plan choice, medical premiums, demographic characteristics, and health plan feature preferences are contrasted to data weighted to approximate the entire employee population's distribution of health plan choices. The average age of the respondents is 46 years, about 44 percent of them are women, and the average employee salary net of taxes in 2002 was $31,702. Thirty-six percent of the respondents or their families have a chronic health condition.

Table 2.

Variable Names and Descriptive Statistics

| Total (N = 915) | |||||

|---|---|---|---|---|---|

| Variable | Description | Sample Mean | Standard Deviation | Weighted Mean | Weighted Standard Deviation |

| Plan Choices of Employees | |||||

| HMO | In HealthPartners HMO=1, else=0 | 0.314 | 0.464 | 0.551 | 2.101 |

| CDHP | In Definity (consumer-driven plan)=1, else=0 | 0.457 | 0.498 | 0.043 | 0.853 |

| PTC | In Choice Plus=1, else=0 | 0.177 | 0.382 | 0.300 | 1.937 |

| PPO | In PreferredOne PPO=1, else=0 | 0.052 | 0.223 | 0.106 | 1.300 |

| Employee Chararacteristics | |||||

| Employee's tax-adjusted medical insurance annual premium | $ 1,522.77 | 823.427 | $ 1,556.85 | 3,636.050 | |

| Employee or immediate family member has chronic condition = 1, else = 0 | 0.360 | 0.480 | 0.370 | 2.040 | |

| Employee elected a family contract = 1, single contract = 0 | 0.485 | 0.500 | 0.514 | 2.112 | |

| Employee's salary minus tax liabilities | $ 31,702.54 | 19,642.040 | $ 27,250.66 | 62,359.420 | |

| Employee is female=1, male=0 | 0.447 | 0.497 | 0.434 | 2.094 | |

| Employee age in 2002 | 45.86 | 11.712 | 44.043 | 50.605 | |

| Employee answered flexible spending account quiz question = 1, else = 0 | 0.71 | 0.454 | 0.725 | 1.887 | |

| Employee Preferences for Health Plan Features: 1=important feature, 0=else | |||||

| Health plan has a national network of providers and hospitals. | 0.271 | 0.445 | 0.210 | 1.721 | |

| Health plan covers preventive services, such as physical exams. | 0.493 | 0.500 | 0.515 | 2.112 | |

| The health plan's network includes my doctors. | 0.701 | 0.458 | 0.650 | 2.015 | |

| The health plan does not require referrals or preauthorizations. | 0.412 | 0.492 | 0.339 | 2.000 | |

| The health plan has no copayments. | 0.420 | 0.494 | 0.535 | 2.107 | |

| The balance in a personal care account or medical savings account rolls over to the next benefit year to pay for medical expenses. | 0.242 | 0.428 | 0.197 | 1.679 | |

| The plan has online tools and resources that I need to manage my care. | 0.070 | 0.255 | 0.070 | 1.077 | |

Note: Health plan population weights are used in the logit choice model.

Two specifications of the conditional logit choice model are presented in Table 3. In both specifications, the reference health plan for comparison is HealthPartners, the traditional HMO. The model in the first four columns of Table 3 includes plan choice intercepts but not premiums. The rationale for using plan choice intercepts as a proxy for premiums is explained by the prices associated with the plan choices. Specifically, HealthPartners had a no-cost employee contribution for single contracts and a very small employee contribution for family contracts, making it a popular plan. This means that any plan intercept really serves as a premium variable as well. As proxies for premiums, the plan intercepts perform well with each associated with a statistically significant coefficient (in bold).

Table 3.

Health Plan Choice Model Estimates

| Using Plan Intercepts as Proxy for Premium | Using Plan Intercepts and Premium | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | Description | Coefficient | Standard Deviation | T-Statistic | Marginal Effect | Coefficient | Standard Deviation | T-Statistic | Marginal Effect |

| Health Plan Intercepts (Health Partners is the reference category) | |||||||||

| CDP—Definity Intercept | −3.707 | 1.046 | −3.545 | −44.354 | −2.572 | 0.887 | −2.899 | −37.191 | |

| PTC—Patient Choice Intercept | −4.152 | 0.341 | −12.187 | −69.730 | −4.061 | 0.348 | −11.668 | −67.566 | |

| PPO—PreferredOne Intercept | −8.282 | 0.506 | −16.375 | −58.012 | −7.003 | 0.859 | −8.151 | −45.43 | |

| Medical Insurance Tax-Adjusted Premium | |||||||||

| Employee Medical Insurance Premium-Adjusted | −0.002 | 0.0007 | −2.265 | ||||||

| Premium and Chronic Interaction | −0.001 | 0.0001 | −7.878 | ||||||

| Premium and Family Contract Interaction | 0.001 | 0.0007 | 1.749 | ||||||

| Employee Chararacteristics Interacted with Health Plan Intercepts | |||||||||

| CDP Chronic Patient or Family Member | −0.142 | 0.314 | −0.453 | −1.7 | 0.409 | 0.271 | 1.507 | 5.911 | |

| PTC | −0.106 | 0.110 | −0.958 | −1.774 | −0.109 | 0.117 | −0.936 | −1.819 | |

| PPO | 0.456 | 0.108 | 4.222 | 3.191 | 1.818 | 0.219 | 8.301 | 11.792 | |

| CDP Family Contract = 1, Single = 0 | −0.296 | 0.295 | −1.003 | −3.542 | −0.418 | 0.319 | −1.31 | −6.038 | |

| PTC | 0.380 | 0.108 | 3.524 | 6.381 | 0.368 | 0.114 | 3.233 | 6.126 | |

| PPO | 0.038 | 0.110 | 0.349 | 0.269 | 0.083 | 0.649 | 0.129 | 0.541 | |

| CDP After-Tax Income (in thousands) | 0.019 | 0.006 | 3.269 | 0.225 | 0.013 | 0.005 | 2.404 | 0.187 | |

| PTC | 0.007 | 0.003 | 2.741 | 0.121 | 0.007 | 0.003 | 2.524 | 0.109 | |

| PPO | 0.006 | 0.002 | 2.355 | 0.04 | −0.004 | 0.003 | −1.664 | −0.029 | |

| CDP Gender, Female=1, Male=0 | −0.012 | 0.298 | −0.04 | −0.143 | −0.013 | 0.251 | −0.05 | −0.181 | |

| PTC | −0.340 | 0.109 | −3.128 | −5.711 | −0.324 | 0.114 | −2.856 | −5.396 | |

| PPO | −0.375 | 0.113 | −3.32 | −2.625 | −0.203 | 0.119 | −1.7 | −0.608 | |

| CDP Employee Age | 0.021 | 0.015 | 1.384 | 0.247 | 0.008 | 0.012 | 0.621 | 0.111 | |

| PTC | 0.031 | 0.006 | 5.648 | 0.522 | 0.030 | 0.006 | 5.279 | 0.503 | |

| PPO | 0.038 | 0.005 | 7.431 | 0.269 | 0.036 | 0.006 | 6.574 | 0.235 | |

| CDP Employee Benefit Knowledge | −0.330 | 0.281 | −1.175 | −3.946 | −0.132 | 0.248 | −0.534 | −1.912 | |

| PTC | 0.287 | 0.115 | 2.493 | 4.815 | 0.282 | 0.119 | 2.374 | 4.689 | |

| PPO | −0.567 | 0.109 | −5.197 | −3.97 | −0.636 | 0.116 | −5.48 | −4.123 | |

| Employee Preferences for Health Plan Features Interacted with Health Plan Intercepts | |||||||||

| CDP National Provider Panel | 0.799 | 0.360 | 2.223 | 9.564 | 0.811 | 0.322 | 2.515 | 11.723 | |

| PTC | 0.125 | 0.142 | 0.881 | 2.099 | 0.132 | 0.147 | 0.9 | 2.203 | |

| PPO | 0.692 | 0.139 | 4.979 | 4.846 | 0.687 | 0.146 | 4.699 | 4.456 | |

| CDP Preventive Services Covered | 0.273 | 0.346 | 0.787 | 3.262 | 0.406 | 0.310 | 1.311 | 5.869 | |

| PTC | 0.187 | 0.123 | 1.524 | 3.136 | 0.204 | 0.127 | 1.608 | 3.397 | |

| PPO | −0.018 | 0.130 | −0.138 | −0.125 | 0.037 | 0.138 | 0.266 | 0.238 | |

| CDP My Doctor Is in the Panel | 0.864 | 0.376 | 2.299 | 10.343 | 0.822 | 0.324 | 2.539 | 11.889 | |

| PTC | 1.785 | 0.137 | 13.067 | 29.970 | 1.777 | 0.140 | 12.727 | 29.558 | |

| PPO | 5.285 | 0.394 | 13.415 | 37.015 | 5.396 | 0.398 | 13.561 | 35.002 | |

| CDP No Referrals or Preauthorization | 0.61 | 0.36 | 1.71 | 7.307 | 0.80 | 0.31 | 2.58 | 11.535 | |

| PTC | 0.293 | 0.119 | 2.452 | 4.915 | 0.301 | 0.124 | 2.430 | 5.013 | |

| PPO | 0.97 | 0.115 | 8.455 | 6.790 | 0.96 | 0.122 | 7.828 | 6.219 | |

| CDP Health Plan Has No Copayments | −0.27 | 0.431 | −0.615 | −3.172 | −0.07 | 0.365 | −0.185 | −0.978 | |

| PTC | 0.381 | 0.141 | 2.705 | 6.398 | 0.373 | 0.145 | 2.567 | 6.206 | |

| PPO | −0.185 | 0.133 | −1.390 | −1.296 | −0.208 | 0.144 | −1.443 | −1.351 | |

| CDP Personal Care Account Rolls Over | 0.396 | 0.366 | 1.080 | 4.737 | 0.193 | 0.329 | 0.585 | 2.785 | |

| PTC | −0.096 | 0.135 | −0.712 | −1.612 | −0.092 | 0.136 | −0.671 | −1.522 | |

| PPO | −1.039 | 0.148 | −7.010 | −7.277 | −1.124 | 0.159 | −7.068 | −7.292 | |

| CDP Use of Online Tools | 0.999 | 0.577 | 1.731 | 11.951 | 0.884 | 0.521 | 1.696 | 12.776 | |

| PTC | 1.211 | 0.208 | 5.811 | 20.334 | 1.214 | 0.217 | 5.587 | 20.193 | |

| PPO | −2.707 | 0.524 | −5.168 | −18.957 | −2.797 | 0.629 | −4.446 | −18.143 | |

| Number of observations | 915 | 915 | |||||||

| Log-L for Choice model | −861.87 | −897.19 | |||||||

| Adjusted R-square | 0.31 | 0.28 | |||||||

Note: Estimates in bold are significant at p<.05

The next four columns include the tax-adjusted premium as well as interactions of premium with employee (or family member) chronic condition and an indicator variable for a family contract. In this model the premium coefficient is effectively identified only through variation in premiums created by differences in the employees' marginal tax rates, because the health plan intercepts control for all individually invariant plan characteristics.

To aid in interpreting the results from these models, we present marginal effects as well as coefficient estimates. Marginal effects are defined as the change in the probability of choosing a health plan (scaled times 100) as a continuous independent variable changes by one unit or a discrete independent variable changes from zero to one. An examination of the marginal effects of employee characteristics interacted with plan-specific dummy variables in Table 3 suggests that chronic illness of the employee or of family members has no effect on choice except for a greater preference for the PPO option, PreferredOne. Employees with family contracts have a greater preference for Choice Plus. Income is positively related to the selection of Definity and is the largest marginal health plan effect in the income group. Income is also positively related to selection of Choice Plus. Age has no statistically significant relationship with Definity Health choice, although the estimated coefficient is positive. Both Choice Plus and PreferredOne attract older employees.

With regard to health benefit knowledge, measured as a correct response to a quiz question on tax-exempt flexible spending accounts, we find the most knowledgeable employees selected Choice Plus, and the least knowledgeable selected PreferredOne.

Employees who chose Definity Health prefer health plans with a national provider panel and a plan that includes their physician in the panel. Employees who chose PreferredOne also preferred these health plan features. Two other positive preferences for Definity Health employees (significant at the .10 level) were that the health plan had no referrals or preauthorization requirements and the plan had online tools to manage one's health and health benefits. Choice Plus enrollees preferred a plan with no copayments and favored lower out-of-pocket expenses.

When premiums are included in the model, we find the sign of the premium coefficient is negative as expected. When premium is interacted with the presence of a chronic illness, we surprisingly find greater price sensitivity for employees and families with a chronic health condition. Premium interacted with family coverage generated a smaller marginal effect suggesting that employees with family coverage may have other family-member constraints that reduce their sensitivity to differences in health plan premiums. The dummy variable interactions are also negative, though not as large as the results in Table 3, suggesting that they may not account for all the premium variation affecting plan choice. In a conditional logit choice model that excluded the health plan intercepts (results not reported here), premium had an even larger effect on plan choice.

Comparing the effects of employee characteristics, we find only a few differences between the two models. If Definity Health had a greater take-up rate and thus a sample weight greater than .04, we may find that employees with chronic illnesses have a higher likelihood of choosing Definity Health. We observe an even larger positive relationship between chronic illness and PreferredOne plan choice when the model includes premiums.

With premium explicitly controlled, we see larger marginal effects for Definity Health choice associated with health plan features than in the intercept-only model of plan choice. The national provider panel feature and having access to my doctor continue to have strong positive relationships with the choice of Definity Health. One change is a positive and statistically significant association with choice of Definity Health for those who prefer a plan with no referral or preauthorization. Interestingly, the use of online tools, one of the hallmarks of consumer-driven health plans, does not have a very significant role in the choice of Definity Health, though it did play a significant role, with a large effect, for employees choosing Choice Plus.

An advantage of the model that includes premiums is that we can calculate explicit premium elasticity estimates, which are shown in Table 4 for Definity Health and HealthPartners. These estimates are derived using the market share of each plan and the average marginal tax rates of 39 percent and 36 percent for employees selecting Definity Health and HealthPartners, respectively. The “employee-perspective” premium elasticity shows the percentage change in the probability of choosing Definity Health as the tax-adjusted out-of-pocket premium changes by 1 percent. This elasticity is relevant for estimating the decision maker's response to a change in her out-of-pocket premium contribution. The “insurer perspective” premium elasticity shows the percentage change in the probability of Definity Health enrollment as the health plan raises its total premium by one percent. This elasticity is more useful for estimating the heightened pressure on health plans from managed competition reforms.

Table 4.

Premium Elasticity Estimates

| Employee-Only Coverage | Family Coverage | |||

|---|---|---|---|---|

| Employee Perspective | Health Plan Perspective | Employee Perspective | Health Plan Perspective | |

| Definity Health | ||||

| No chronic condition | −0.387 | −4.584 | −0.786 | −5.375 |

| Chronic condition | −0.58 | −6.876 | −1.572 | −10.749 |

| HealthPartners HMO | ||||

| No chronic condition | N/A | −2.064 | −0.155 | −2.58 |

| Chronic condition | N/A | −3.097 | −0.309 | −5.161 |

Notes:

Formula for premium elasticity: n=B(1 − P)X

B = coefficient, P = probability of choosing this plan, X = tax-adjusted out-of pocket (total) premium for employee (health plan) perspective elasticity

Marginal tax rates for employees: HealthPartners = 0.36, Definity Health = 0.39

The Definity Health elasticity estimates show that single-contract employees with chronic conditions are more price-sensitive than those without chronic conditions. We observe even larger price elasticity for employees selecting family contracts in Definity Health, with chronically ill employees or their family members having a greater premium response. We observe no single-contract employee price elasticity for HealthPartners, since there is no employee premium for the benefit. The family elasticity estimates from both the employee and insurer perspectives are less for HealthPartners than for Definity Health.

Conclusion and Limitations

The analysis in this paper provides new knowledge on preferences of employees who are offered a consumer-driven health plan for the first time. Our results do not suggest that the CDHP was disproportionately chosen by the young and the healthy. At the very least, employees who choose Definity Health appear no healthier or younger than those who chose an HMO.

We do find that income and employee preferences for several health plan features were strongly positively associated with the choice of Definity Health. Most notably, access to a panel that included a desired provider as well as the availability of a national panel of physicians and hospitals is appealing. For example, Definity Health offers access to the Mayo Clinic in Rochester, Minnesota. Only one other plan explicitly permits access to Mayo, and then at a premium nearly three times the required employee premium contribution for Definity Health. Income is a consistent factor associated with Definity Health choice, suggesting that those with the ability to easily fund the deductible in the case of emergency are more willing to choose a consumer-driven health plan. If income continues to be a factor in health plan choice, consumer-driven plans may acquire a reputation for being the choice for the “well-to-do.” However, in other survey results there was no apparent difference in consumer-perceived quality between Definity Health and other health plans, suggesting that, if higher-income individuals choose to pay more for greater provider choice, it does not appear associated with an appreciable difference in perceived quality of care.

As in many previous studies, we find that employees are sensitive to out-of-pocket premium differences among competing health plans. However, employees with chronic conditions themselves or in their family are more price-sensitive than those without chronic conditions. Our conjecture for the cause of this surprising result is that three UM plans—Definity Health, PreferredOne, and Choice Plus—featured larger provider networks and more open access to providers than did HealthPartners. If chronically ill employees and families prefer these features, they may perceive more close substitutes in the choice set than employees and families without chronic illnesses. As the number of close substitutes for a product increases, the own-price elasticity of demand rises.

Our conclusions are subject to several important limitations. The first of these concerns the generalizability of the results. We observe only employees and families who switched into a consumer-driven heath plan during its first year. No one at the UM had experience with this type of plan, which is quite different from the offerings during the prior years. One would expect that employees who chose Definity Health for themselves and their families in 2002 might be different from those who select the plan in subsequent years. We plan to continue the analysis by examining the patterns of selection into Definity Health in 2003.

Second, the study is limited by the small sample size of 430 Definity Health members. Some of the insignificant results may be due to this limitation. The small number of enrollees in Definity Health Options 1 and 2 also prevented estimation of nested logit/multinomial probit health plan choice models. A Hausman test (Hausman and McFadden 1984) indicated that we could not drop one of the alternatives without violating the assumption of “independence of irrelevant alternatives” or IIA (χ2=132.109, df=31). Therefore, our finding that chronically ill employees are more price-sensitive than those without chronic conditions may be dependent on the particular set of choices offered by the UM.

Third, our analysis of selection relies heavily on a self-reported indicator of chronic illness that counts all chronic conditions equally and classifies the whole family as having a chronic condition if only one family member has such a condition. Because of concerns about the validity of this measure, we performed three tests using the survey responses for Definity Health respondents matched to 2002 medical claims data for the respondent's contract. First, we created a count of the number of Adjusted Diagnosis Groups (ADGs) for each contract in the claims data. Each ADG is a grouping of ICD-9 diagnosis codes that are similar in terms of the severity and likelihood of persistence of the health condition treated over a relevant period of time (Weiner et al. 1991). The ADGs are also predictive of the need for health care services. Just as individuals may have multiple ICD-9 diagnosis codes, they may have multiple ADGs (up to 34). The correlation coefficient between the ADG-count variable and the survey-based chronic condition indictor was .362, which was statistically significant at p<.0001.

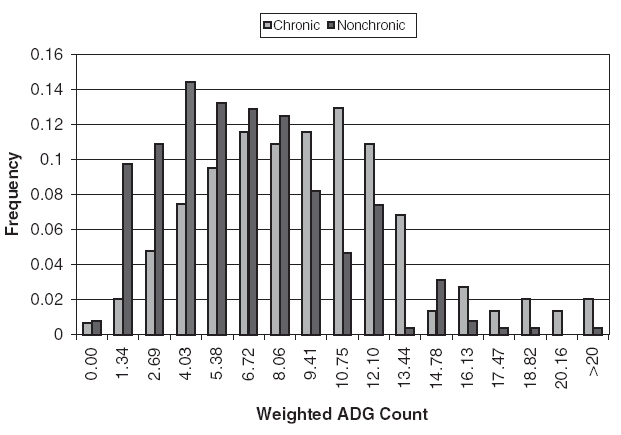

Second, we created a weighted ADG count using claims cost weights for each ADG from a large employer population (not the University of Minnesota, for which claims data were unavailable). This is a different and arguably better representation of what each family is likely to cost. The correlation coefficient between this weighted ADG count and the survey responses is .311, slightly lower than the first test but significant at p<.0001. A graph of the distribution of weighted ADGs among chronic and nonchronic respondents is shown in Figure 1. The distribution has a single peak in both populations, but the chronically ill population peaks at a higher illness burden than the nonchronic population. In addition, the weighted ADG count does not appear to be driven by unusually low- or high-cost outliers in either population.

Figure 1.

Frequency of Weighted ADG Count among Chronic and Nonchronic CDHP Respondents

Finally, we created an ADG-count variable based only on progressive and chronic diseases (ADGs 9–19 and 23–25). This measure was correlated at p<.001 with the survey-based chronic condition indicator. Thus, while the chronic condition indicator is not perfect, our tests demonstrate that it correlates highly with a conceptually and statistically valid measure of health status.

We plan to examine the choices of employees in other employed groups to test the stability of the results reported in this paper. In these groups, we will use claims data to measure illness burden, using ICD-9 diagnosis codes. Most importantly, we will address the question of whether consumer-driven health plans result in appreciable differences in cost and utilization subsequent to enrollment. This work lays the groundwork for future research by providing the first empirical examination of the health plan features most preferred by consumers considering the choice of a consumer-driven health plan. Continuing this analysis over several years might yield different results. Observing subsequent rounds of consumer health plan selection would also be desirable to examine whether early adopters of CDHPs differ from later adopters in their decision making. Our results suggest the options offered by Definity Health to the University of Minnesota did not receive favorable risk selection relative to the most popular and lowest-cost option in the first round of employee choice.

References

- Bureau of National Affairs “Employer Premiums Increase 11 Percent; Employees Likely to Pay More, Survey Says”. Health Care Policy Report. 2001;9(35):1385. [Google Scholar]

- CAHPS™ CAHPS™ 2.0, Adult Core Questionnaire. 1998. Available at http://www.ahcpr.gov/qual/cahpfact.htm.

- Christianson J, Feldman R. “Evolution in the Buyers Health Care Action Group Purchasing Initiative”. Health Affairs. 2002;22(1):76–88. doi: 10.1377/hlthaff.21.1.76. [DOI] [PubMed] [Google Scholar]

- Christianson J, Feldman R, Weiner JP, Drury P. “Early Experience with the Buyers Health Care Action Group Direct Contracting Initiative”. Health Affairs. 1999;18(6):100–14. doi: 10.1377/hlthaff.18.6.100. [DOI] [PubMed] [Google Scholar]

- Christianson J, Parente ST, Taylor R. “Defined Contribution Health Insurance Products: Development and Prospects”. Health Affairs. 2002;21(1):49–64. doi: 10.1377/hlthaff.21.1.49. [DOI] [PubMed] [Google Scholar]

- Dowd B, Feldman R. “Premium Elasticities of Health Plan Choice”. Inquiry. 1994/1995;31(4):438–44. [PubMed] [Google Scholar]

- Dowd B, Feldman R, Maciejewski M, Pauly MV. “The Effect of Tax-Exempt Out-of-Pocket Premiums on Health Plan Choice”. National Tax Journal. 2001;44(4):741–56. [Google Scholar]

- Feldman R, Christianson J, Schultz J. “Do Consumers Use Information to Choose a Health Care Provider System?”. Milbank Quarterly. 2000;78(1):47–78. doi: 10.1111/1468-0009.00161. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Feldman R, Finch M, Dowd B, Cassou S. “The Demand for Employment-Based Health Insurance Plans”. Journal of Human Resources. 1989;24(1):115–42. [Google Scholar]

- Freudenheim MH. “A New Health Plan May Raise Expenses for Student Workers”. 2001. New York Times December 5.

- Gabel J, Levitt L, Pickreign J, Whitmore H, Holve E, Rowland D, Dhont K, Hawkins S. “Job-Based Health Insurance in 2001: Inflation Hits Double Digits, Managed Care Retreats”. Health Affairs. 2001;20(5):180–6. doi: 10.1377/hlthaff.20.5.180. [DOI] [PubMed] [Google Scholar]

- Gabel JR, Lo Sasso AT, Rice T. “Consumer-Driven Health Plans: Are They More Than Talk Now?”. Health Affairs. 2002 doi: 10.1377/hlthaff.w2.395. Web exclusive. Available at http://www.healthaffairs.org/WebExclusives/2201Gabel.pdf. [DOI] [PubMed] [Google Scholar]

- Galvin R, Milstein A. “Large Employer's New Strategies in Health Care”. New England Journal of Medicine. 2002;347(12):939–42. doi: 10.1056/NEJMsb012850. [DOI] [PubMed] [Google Scholar]

- Harris K, Keane MP. “A Model of Health Plan Choice: Inferring Preferences and Perception from a Combination of Revealed Preference and Attitudinal Data”. Journal of Econometrics. 1999;89(1–2):131–57. [Google Scholar]

- Harris K, Schultz J, Feldman R. “Measuring Consumer Perceptions of Quality Differences among Competing Health Benefit Plans”. Journal of Health Economics. 2002;21(1):1–17. doi: 10.1016/s0167-6296(01)00098-4. [DOI] [PubMed] [Google Scholar]

- Hausman J, McFadden D. “Specification Tests for the Multinomial Logit Model”. Econometrica. 1984;52:1219–40. [Google Scholar]

- Iglehart JK. “Changing Health Insurance Trends”. New England Journal of Medicine. 2002;347(12):956–62. doi: 10.1056/NEJMhpr022143. [DOI] [PubMed] [Google Scholar]

- Lutz S, Henkind S. “The Web Fuels Interest in Defined Contribution”. HealthPlan. 2000;41(6):62. 64, 66. [PubMed] [Google Scholar]

- Manski CF, Lerman SR. “The Estimation of Choice Probabilities from Choice Based Samples”. Econometrica. 1977;45(8):1977–88. [Google Scholar]

- Parrish M. “When Patients Buy Their Own Health Care”. Medical Economics. 2001;(March 5):94. [PubMed] [Google Scholar]

- Robinson JC. “Renewed Emphasis on Consumer Cost Sharing in Health Insurance Benefit Design”. Health Affairs. 2002 doi: 10.1377/hlthaff.w2.139. Web exclusive. Available at http://content.healthaffairs.org/cgi/reprint/hlthaff.w2.139v1.pdf. [DOI] [PubMed] [Google Scholar]

- Schlesinger M, Druss B, Thomas T. “No exit? The Effect of Health Status on Dissatisfaction and Disenrollment from Health Plans”. Health Services Research. 1999;34(2):547–76. [PMC free article] [PubMed] [Google Scholar]

- Short PF, Taylor AK. “Premiums, Benefits, and Employee Choice of Health Insurance Options”. Journal of Health Economics. 1989;8(3):293–311. doi: 10.1016/0167-6296(89)90023-4. [DOI] [PubMed] [Google Scholar]

- Schultz JS. “Selection of Health Care Provider Systems in a Direct Contracting Model”. 2001 Doctoral Dissertation in Health Services Research, Policy, and Administration, University of Minnesota. [Google Scholar]

- Schultz J, Thiede Call K, Feldman R, Christianson J. “Do Employees Use Report Cards to Access Health Care Provider Systems?”. Health Services Research. 2001;36(3):509–30. [PMC free article] [PubMed] [Google Scholar]

- Strombom BA, Buchmueller TC, Feldstein PJ. “Switching Costs, Price Sensitivity, and Health Plan Choice”. Journal of Health Economics. 2002;21(1):89–116. doi: 10.1016/s0167-6296(01)00124-2. [DOI] [PubMed] [Google Scholar]

- Sutton H, Feldman R, Dowd B. “Disruption of a Managed Competition Environment by Low-Ball Premium Bids: The Minnesota State Employees Group Insurance Program”. North American Actuarial Journal. 2004;(April) in press. [Google Scholar]

- Trude S, Ginsburg P. Are Defined Contributions a New Direction for Employer-Sponsored Coverage? Washington, DC: Center for Studying Health System Change; 2000. Issue brief no. 32. [PubMed] [Google Scholar]

- Weiner JP, Starfield BH, Steinwachs DM, Mumford LM. “Development and Application of a Population-Oriented Measure of Ambulatory Case-Mix”. Medical Care. 1991;29(5):452–72. doi: 10.1097/00005650-199105000-00006. [DOI] [PubMed] [Google Scholar]

- Wiggins S, Emery D. “Self-Directed Health Plans: Web-Enabled Alternatives to Traditional Managed Care”. Managed Care Quarterly. 2001;9(1):33–40. [PubMed] [Google Scholar]