Abstract

Objective

To review all admissions (age > 13) to three surgical patient care centers at a single academic medical center between January 1, 1995, and December 6, 1999, for significant surgical adverse events.

Summary Background Data

Little data exist on the interrelationships between surgical adverse events, risk management, malpractice claims, and resulting indemnity payments to plaintiffs. The authors hypothesized that examination of this process would identify performance improvement opportunities overlooked by standard medical peer review; the risk of litigation would be constant across the three homogeneous patient care centers; and the risk management process would exceed the performance improvement process.

Methods

Data collected included patient demographics (age, gender, and employment status), hospital financials (hospital charges, costs, and financial class), and outcome. Outcome categories were medical (disability: <1 month, 1–6 months, permanent/death), legal (no legal action, settlement, summary judgment), financial (indemnity payments, legal fees, write-offs), and cause and effect analysis. Cause and effect analysis attempts to identify system failures contributing to adverse outcomes. This was determined by two independent analysts using the 17 Harvard criteria and subdividing these into subsystem causative factors.

Results

The study group consisted of 130 patients with surgical adverse events resulting in total liabilities of $8.2 million. The incidence of adverse events per 1,000 admissions across the three patient care centers was similar, but indemnity payments per 1,000 admissions varied (cardiothoracic = $30, women’s health = $90, trauma = $520). Patient demographics were not predictive of high-risk subgroups for adverse events or litigation. In terms of medical outcome, 51 patients had permanent disability or death, accounting for 98% of the indemnity payments. In terms of legal outcome, 103 patients received no indemnity payments, 15 patients received indemnity payments, four suits remain open, and in eight cases charges were written off ($0.121 million). To date, no cases have been adjudicated in court. Cause and effect analysis identified 390 system failures contributing to the adverse events (mean 3.0 failures per adverse event); there were 4.7 failures per adverse event in the 15 indemnity cases. Five categories of causes accounted for 75% of the failures (patient management, n = 104; communication, n = 89; administration, n = 33; documentation, n = 32; behavior, n = 23). The current medical review process would have identified 104 of 390 systems failures (37%).

Conclusions

This study demonstrates no rational link between the tort system and the reduction of adverse events. Sixty-three percent of contributing causes to adverse events were undetected by current medical review processes. Adverse events occur at the interface between different systems or disciplines and result from multiple failures. Indemnity costs per hospital day vary dramatically by patient care center (range $3.60–97.60 a day). The regionalization of healthcare is in jeopardy from the burden of high indemnity payments.

Headlines scream and pundits wag about the crisis in malpractice premiums. In West Virginia there is one lawsuit for every two practicing physicians. 1 Thirty-one percent of physicians in Pennsylvania were dropped by their liability carrier in 2001 to 2002. 2 Seventy percent of physicians in Texas’ Rio Grande Valley have a medical liability claim outstanding. 3

This crisis has expanded to affect healthcare delivery. Hospitals have discontinued high-risk services, and trauma centers have closed. 4 Physicians have retired, changed the composition of their practice, or moved to states with a favorable malpractice environment. The crisis is convoluted and solutions are complicated by the uneven burden of malpractice premiums. The burden differs dramatically between hospitals, physicians, and specialties and between states with different regulatory and legal environments. 5 This crisis is born from the complex relationship between the healthcare industry, which is responsible for ensuring patient safety, the legal system, which is responsible for protecting individual rights, and the insurance industry, which is responsible for distributing risk.

To clarify this complex relationship, we looked at our 5-year risk management experience in three surgical patient care centers. We identified adverse events and subjected them to cause and effect analysis. We looked at medical outcome, legal outcome, the cost of defense, and indemnity payments made. We hypothesized that the process would identify performance improvement opportunities overlooked by standard medical review; that the risk of litigation would be constant across the three homogeneous patient care centers; and that our risk management outcome would exceed our performance improvement outcome.

METHODS

Study Setting

The study was conducted in a single self-insured academic medical center. This enterprise has a long history of a collaborative risk management strategy. The institution is structured into patient care centers. These multidisciplinary product lines have joint physician and hospital leadership and were created to promote efficient care delivery. Patient care center management is given significant independence to execute financial goals within a strategic framework defined by the clinical enterprise. Three patient care centers were identified for this study based on the high-acuity nature of their practice: women’s health, cardiothoracic surgery, and trauma. All three patient care centers treat patients who have high probabilities of adverse events. Trauma and women’s health are service lines considered to be at risk nationally because of the insurance premium crisis. Additionally, our women’s health patient care center has a large high-risk obstetrics practice associated with the region’s only level 3 neonatal intensive care unit. The cardiothoracic product line is a relatively homogeneous product with a large semi-elective, high-acuity practice. It is associated with high resource consumption and an older population. The trauma patient care center was chosen because it is the only level 1 trauma center for a 65,000-square-mile catchment area with a well-developed regionalized trauma system.

The risk management department has been in existence for 25 years and manages a large self-insurance trust fund. Additionally, risk management is responsible for investigating incidents, determining adverse events, evaluating exposure, managing claims, supervising litigation, and structuring indemnity payments. The risk management office and the self-insurance trust represent all medical center employees, including the house staff and faculty. This system provides for a coordinated defense and a consolidated payment structure.

IRB approval was obtained before initiation of the study. Additionally, approval was obtained from the patient care center directors and the risk management office, which retained rights for manuscript approval.

Definition of Terms

Patients were stratified by employment status and financial class. Employment status was determined at the time of admission by the patient or the patient’s family, as reported to the financial counselor. Financial class was divided into insured and underinsured. Insured categories include commercial insurance, worker’s compensation, and Medicare. Underinsured patients include TennCare (Medicaid) and self-pay. Medical, legal, and financial definitions are contained in the Appendix.

Cause and Effect Analysis

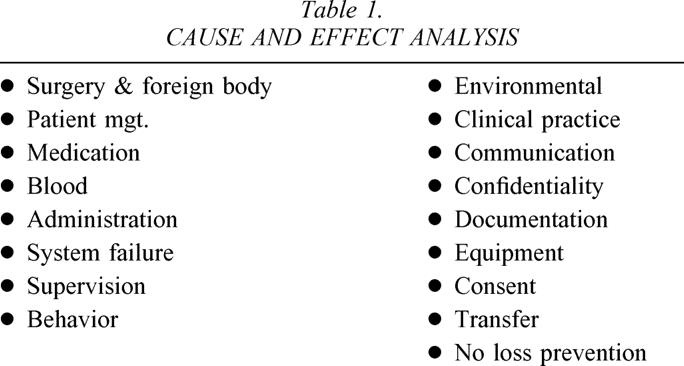

Cause and effect analysis seeks to identify relationships preceding adverse events. In this study, two independent analysts, associated with the Department of Risk Management, identified actions, events, and environmental circumstances resulting in adverse events. Contributing causes were drawn from a list of malpractice claims and description codes adopted and expanded from the Harvard Risk Management Foundation Allegation of Negligence. 6 Each reviewer presented the cause and effect analysis for every adverse event to a review team that included a claims investigator and one experienced Registered Nurse manager. Codes were aggregated into broader issues such as communication failure or documentation failure to quantify general classes of problems. Codes for each case were collected in a spreadsheet and analyzed with descriptive statistics. Statistical analysis was performed using an unpaired Student t test with significance set at P < .05. Table 1 lists the 17 major categories of cause and effect analysis.

Table 1. CAUSE AND EFFECT ANALYSIS

Study Population

Between January 1, 1995, and December 6, 1999, 32,100 patients over the age of 13 were admitted to the three patient care centers. One hundred seventy-one patients with potential adverse events and a risk management claim file were identified. After detailed review, 41 patients were excluded: no adverse events were identified in 26 patients, 11 patients were never admitted to the hospital, and 4 patients were outside the study period. This provided a study group of 130 patients who were assessed for basic demographic information and medical, legal, and financial outcome. The hospital medical record and electronic information systems were queried for additional patient and patient care center information. Patient data included length of stay, acuity, number of consults, employment status, and insurance status. Patient care center data included number of admissions and total hospital days for each patient care center over the 5-year study period.

Medical Outcome

Medical outcome was analyzed in the entire study group and by individual patient care center. Medical outcome was defined as the presence of disability, number of consultants, timing of discovery, and cause and effect analysis. Medical disability was defined by the time necessary to recover from the adverse event and stratified into less than 1 month, 1 month to 6 months, and more than 6 months, or permanent. Permanent disability included disability more than 6 months, or death.

Legal Outcome

Legal outcome was defined as that outcome associated with the claim. Potential outcomes were divided into two classes: no action and claims filed. The no action group consisted of patients with identified adverse events who did not choose to file a claim. The outcomes within the claims filed group included non-suit, settlement, summary judgment, or open-in-suit.

Financial Outcome

Financial outcome was divided into three groups: no indemnity payment, indemnity payment, and open-in-suit. No indemnity payment meant that no payment was made to the plaintiff or the hospital bill was written off. Indemnity payments represented all payments made to the plaintiff and include those payments associated with the plaintiff’s attorney fees. Open-in-suit represented four cases in which final judicial and financial outcome was pending over 3 years following identification of the adverse event. These cases were excluded from final financial outcome analysis but were included in medical and legal outcome data. Legal fees (i.e., defense costs) are reported separately and include all costs for outside counsel, consultants, and review.

Incidence data by patient care center is presented in three categories: patients with adverse events per 1,000 admissions, indemnity dollars per patient admitted, and per diem indemnity cost. The last two categories attempt to quantify the incremental institutional indemnity cost associated with maintaining the product line. For the patient care center to be viable, this incremental cost must be recaptured through some form of price increase.

RESULTS

Demographics

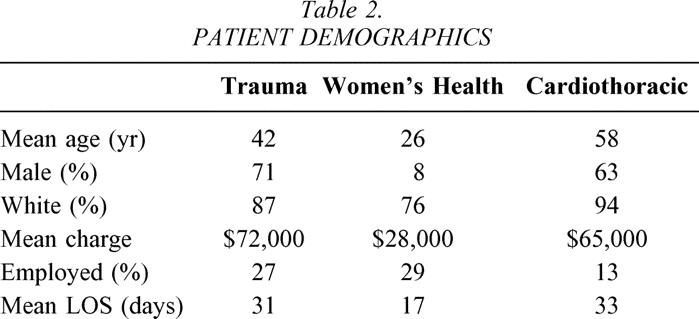

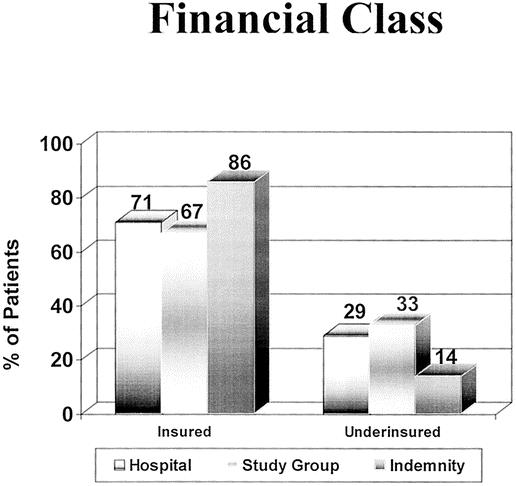

There were 32,100 admissions to the three patient care centers over the study period. One hundred thirty patients (0.4%) qualified for the study group. The demographics of the study group are defined in Table 2. The mean age in the trauma patient care center was slightly higher than expected. The financial class of the study group is depicted in Figure 1 and showed no significant differences between the study group and the hospital population over this period. This is to be expected because adverse events should be independent of insurance status. However, the indemnity group had a higher probability of being insured (86%). This suggests patient facility with the legal system, rather than medical need, was the catalyst for instigating a successful suit.

Table 2. PATIENT DEMOGRAPHICS

Figure 1. Financial class: percentage of patients either insured or underinsured in the hospital population, the study group, and the indemnity group. The indemnity group was more likely to be insured, suggesting that facility with the legal system predicts a successful suit.

Medical Outcome

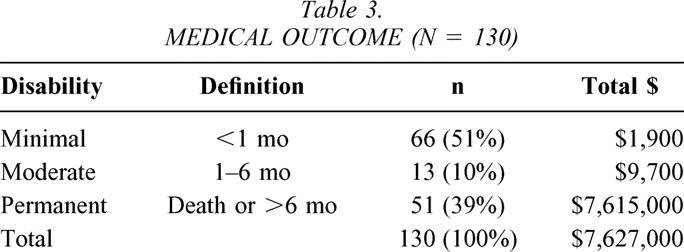

We looked at three indicators of medical outcome: number of consults, timing of discovery, and length of disability resulting from the adverse event. There were no differences in the number of consults or timing of discovery among the patient care centers. Medical disability for the study group is defined in Table 3. Fifty-one percent of the study group had minimal residual disability, defined as less than 1 month. As expected, financial liability (n = 126) varied directly with the severity of the patient’s disability. Thirty-nine percent (39%) of patients with permanent disability accounted for 98% of institutional liability.

Table 3. MEDICAL OUTCOME (N = 130)

Legal Outcome

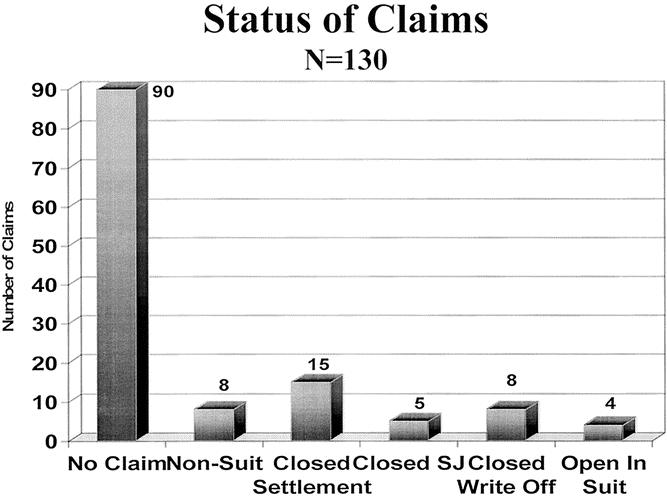

Figure 2 defines the legal resolution of the 130 patients in the study group. Remarkably, not a single patient claim was adjudicated by jury award. Ninety patients (69%) filed no claim at all and had no formal interaction with the legal system. Forty patients (31%) had some interaction with the system. Ninety percent of these cases are closed and 10% remain open-in-suit. Of the closed cases (n = 36), 13 (36%) were resolved in favor of the defense (non-suit, summary judgment), 8 (22%) were resolved by write-off, and 15 (42%) were resolved for the plaintiff by settlement. Total hospital charges for the write-off group were $121,588, with approximate hospital costs of $63,700 and legal costs of $2,935. This provides a mean soft settlement cost for the eight patients in the write-off group of $8,329 per patient.

Figure 2. Legal outcome of adverse events (n = 130). Sixty-nine percent filed no claim at all. Of the closed cases, 36% were resolved in favor of the defense, 22% resulted in write-off, and 42% were resolved for the plaintiff.

Financial Outcome

Financial outcome was divided into four groups: no payment, write-off, indemnity payment, and open-in-suit. Table 4 defines financial outcome by legal outcome in 126 closed cases. Total payments for this group were $8.2 million. Legal expenses were $425,000, or 5.2% of the total indemnity payment. Four open-in-suit cases were not included in this financial analysis. Open-in-suit represents cases where judicial and financial outcome is pending, now 3 or more years following identification of the adverse event. Because these cases continue before the court, we should not speculate on financial outcome. Therefore, the dollar numbers we present underestimate the total financial exposure to the institution.

Table 4. FINANCIAL OUTCOME, CLOSED CASES

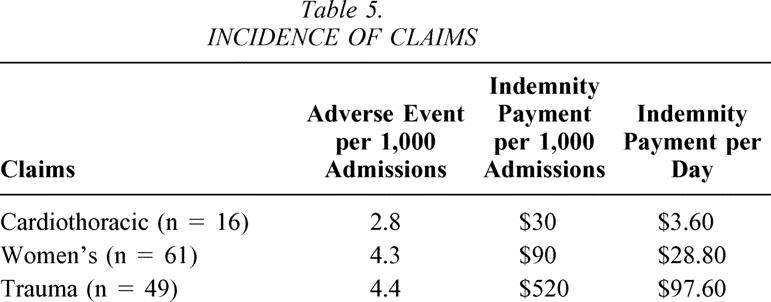

Table 5 defines, by patient care center, adverse events per 1,000 admissions, indemnity payments per admission, and indemnity payments per hospital day. While the incidences of adverse events were within the same order of magnitude, indemnity cost per admission and per diem indemnity costs to the institution across the three patient care centers varied widely (range $3.60–$97.60).

Table 5. INCIDENCE OF CLAIMS

Cause and Effect Analysis

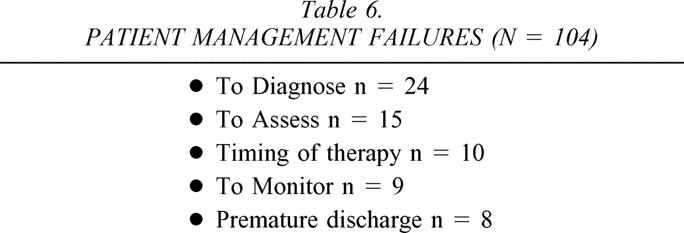

Detailed cause and effect analysis of the study group demonstrated a total of 390 system failures (mean 3.0 failures per patient). Of the 17 possible failure categories, 5 categories accounted for 72% of all failures: patient management (n = 104), communication (n = 89), administration (n = 33), documentation (n = 32), and behavior (n = 23). These five categories represented 281 failures. Table 6 describes subcategories of patient management failures. Only the 104 failures associated with patient management, out of the total of 390 system failures (37%), would be expected to be detected and discussed at standard morbidity and mortality review. Put another way, 63% of our failures were undetected by our present method of medical peer review.

Table 6. PATIENT MANAGEMENT FAILURES (N = 104)

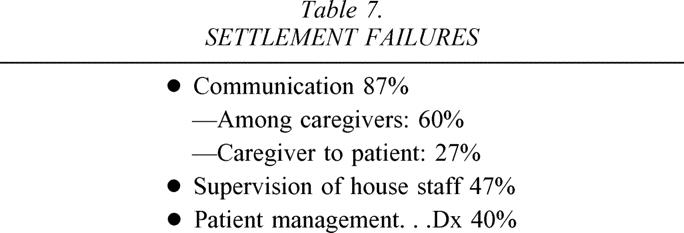

The indemnity group (n = 15) represented a total of 70 systems failures (mean 4.7), a significantly higher rate than the failure rate (3.0) in the study group overall. Table 7 reviews the major systems failures in the indemnity group. Communication was the primary failure, followed by supervision of the house staff. We were surprised to find that communication failures were predominantly between caregivers rather than caregiver to patient.

Table 7. SETTLEMENT FAILURES

DISCUSSION

It is commonly held that large jury awards, by virtue of financial penalty to an individual provider, will put the medical community on notice and will result in improved medical care. The process, however, is more complex. It includes interactions between the defense, the judicial system, the plaintiff’s bar, and the insurance industry. Defense attorneys are motivated to minimize financial payments for providers; conversely, plaintiff’s attorneys are motivated to maximize awards to their clients. In the middle is the jury, which possesses little medical expertise and is bound by statutes that vary by state. In this adversarial environment, decisions are made and dollars are often paid independent of the presence of negligence. The insurance industry performs a service that distributes provider risk over the entire provider community. Additionally, the insurance industry must estimate losses and price product such that they remain profitable. No one in this process is charged with reducing adverse events and improving the outcome of the healthcare system.

In fact, the current jury award process may provide disincentives to improving healthcare. In academic medical centers, the concentration of certain high-risk patients (trauma, high-risk obstetrics, and neonatology) into the hands of a small number of subspecialty physicians has proven to be cost-effective, to improve patient outcomes, and to enhance system efficiency. 7 Institutions with a commitment to regionalized high-risk subspecialty care have, however, inadvertently assumed the indemnity risk of concentrating these patients. In this study we quantify the dollar cost of this risk. It ranged from $3.60 per day in the cardiothoracic patient care center to $97.60 per day in the trauma patient care center. When faced with these large indemnity costs in a managed care environment that will not support price increase, the logical administrative decision is to eliminate these high-risk services.

For community hospitals the paradigm is different. Assume an institution wishes to shift dollars into its performance improvement infrastructure to reduce adverse events and malpractice premiums. One will find that premiums are insensitive to a single institution’s indemnity experience but reflect instead the community’s indemnity experience. 5 Further, the insurance market prices premiums based on an institution’s historical risk. The mathematical assessment of risk is based on volatility. Volatility is higher in cases adjudicated by jury rather than settled. Therefore, the decision to settle is not based solely on the presence of negligence but is also related to controlling claims risk and premium cost. This strategy creates a further disconnect between the judicial system and performance improvement.

Review of Salient Results

The causes of adverse events are multifactorial, often misunderstood, misanalyzed, and rarely (37%) identified by standard medical review. These failures are invariably multiple and commonly occur at the interface of complex medical systems. For example, medication errors may occur at the interface of pharmacy and the nursing staff. 8 Communication errors occur at the interface between the family and physicians 9 but, more importantly, occur commonly between professionals from different disciplines. System failures leading to adverse events and litigation are never isolated. There were a mean of 3.0 failures in the study group and 4.7 failures in the indemnity group. This suggests ample opportunity to construct meaningful interventions, if the proper structure is created. The understanding of failure leads to novel solutions, yet few institutions have the structure to collect specialty-specific data to provide specialty-specific solutions.

There were a number of surprises when we looked at legal outcomes. No case was determined by jury award. Sixty-nine percent of patients never filed a claim. Of the claims that were filed, 30% were withdrawn or dismissed before presentation to a jury. All this suggests that a vast majority of adverse events are never seen by the jury system. Consequently, it is unrealistic to expect this system to effectively improve the delivery of medical care.

Additionally, this study suggests that the current institution-wide risk management strategy that aligns physicians, staff, and the hospital is an improvement over independent representation. Defense costs were low (5.2%) and consolidated claims resulted in a high rate of settlement and lower insurance premiums. Volatility was controlled by settling high-risk claims rather than risking a jury trial and an uncontrolled award.

Our analysis of financial outcome suggests that large settlements are rare; only 12% of closed cases resulted in indemnity payments. The size of the settlement is more likely to be associated with the degree of disability than the presence of negligence. The incidence of adverse events varied among patient care centers but less so than indemnity payment per day, which differed by almost two orders of magnitude ($3.60 vs. $97.60).

We contend that these differences are hidden and go largely unrecognized by hospital administrators. These differences may be due to differences in care provided, family expectations, patient population, or risk management strategy.

This study was not designed to capture the true incidence of adverse events, nor was it designed to detect differences in patient care. Therefore, we cannot quantify care differences across patient care centers except to say that cause and effect analysis of patient management errors failed to demonstrate differences.

The concept of differing expectations is interesting. Cardiothoracic patients have, for the most part, a chronic disease, and consequently there is opportunity to manage expectations preoperatively. Women’s health, in theory, also has the opportunity to manage expectations preoperatively but is faced with two significant problems. First, social expectations for a normal baby are high, both for the patient and the jury. Unfulfilled expectations in the patient population may lead to more dissatisfaction 10 and a higher rate of claims filed. The jury’s high expectation of a good outcome is a risk factor that must be considered when taking a case to trial or when establishing settlement limits. Second, the underinsured population is growing. This provides physicians less opportunity to manage patients before delivery and increases the risk of poor outcome and unfulfilled expectations.

Expectations in the trauma population are the most difficult to manage. There is no preinjury physician-to-patient relationship, families have little understanding of the disease process, and anger frequently accompanies recovery. In many instances this anger is transferred from the perpetrator of the injury to the healthcare team.

Currently, the same risk management strategies are used across all patient care centers. This strategy bears re-examination, as high-risk services present different problems than those of low-risk services. Low-risk providers infrequently have bad outcomes and, if they occur, these unfavorable outcomes may be associated with negligence or poor interpersonal relationships. Conversely, high-risk providers, although not immune from negligence, frequently encounter bad outcomes, associated purely with the magnitude of the injury. These differing causes suggest the need for unique risk management strategies for high- and low-risk populations.

Finally, settlement decisions should not be influenced by the age or the predicted productivity of the plaintiff. Ideally, settlement discussions and jury awards should be a function of the magnitude of deviation from the standard of care, not lost productivity, unmet expectations, or courtroom theater. Under any circumstances, the dramatic differences in indemnity costs have implications for healthcare delivery. The options are clear: discontinue the high-risk service, pass the cost to the consumer, or manage the risk better. Managing the risk better will require a significant investment in performance improvement infrastructure and claims management and risk financing.

Our analysis suggests that from an institutional perspective, our risk management efforts are more sophisticated and have evolved more rapidly than our performance improvement processes. We have identified only isolated instances where indemnity payments translated into policy changes to reduce the incidence of future adverse events. The failures of medical peer review to define system failures leading to adverse events, and the failure of indemnity payments to change policy, mandate a fundamental change in our approach to these issues.

Strengths and Limitations

We acknowledge the limitations of this study. We recognize that 130 adverse events in this population represents underreporting. The database used was designed to detect cases at high risk for litigation and was sufficiently robust to identify all cases in advance of judicial inquiry. Another limitation is that we must underestimate financial liability because four cases remain open-in-suit. These cases are complex, may be adjudicated in the jury system, and will have significant associated legal expenses in addition to any individual payments required.

The strengths of this study include the availability of cause and effect information for adverse event review, a homogeneous study population, and a single institutional risk management strategy. The detail provided by cause and effect analysis has identified problems and suggested solutions that would be unobtainable using a large database. The homogeneous population of surgical patients provides information useful in managing risk at the practice level. The single institutional risk management strategy, while not unique, represents best practice in this field.

Future Directions

The ultimate goal of the healthcare system is to enhance safety, not reduce premiums. We must design policy and programs that promote safety. The judicial system cannot be expected to improve healthcare and currently provides disincentives to physicians treating patients in high-risk specialties, high-risk states, and high-risk environments. At the policy level we must encourage the development of new incentives for both physicians and hospitals—incentives that reward regionalization, innovation, and process changes that improve safety. Most importantly, the federal government must create incentives that promote the development, evaluation, and translation of information technology to the bedside.

“We must create a culture of safety within a culture of quality.” Academic medical centers must create a culture that rewards event reporting as a valued task, a culture that holds the reporter blameless for the report, but individuals accountable for the event. At the institutional level we must change our systems and redesign our work. We need to move professionals to the bedside and minimize nonclinical distractions. We must create a workplace that allows the professional to evolve from an individual who records medical information to an individual who processes medical information. We must rapidly integrate new technology that provides for bedside electronic data capture and order entry, and we must develop the software and systems that predict and prevent adverse events before they occur. We must recognize that failures occur predominantly at the interface between complex processes, and we must design analytical tools that focus on these interfaces. We must redesign our peer review process to focus on populations and not just individuals, and we must benchmark these processes to national norms.

CONCLUSIONS

This study fails to demonstrate a rational link between the tort system and the reduction of adverse medical events. Sixty-three percent of contributing causes to adverse medical events were undetected by current medical review processes. Adverse events typically result from multiple, not isolated, system failures and commonly occur at the interface of systems or disciplines. The incidence of adverse events was similar across patient care centers, but indemnity payments per admission and per hospital day varied by two orders of magnitude. The high cost of malpractice insurance is changing the delivery of healthcare in unexpected ways. Specialty centers are in jeopardy, and if they close patients will be redistributed to community providers. Care will be less centralized and less efficient, and costs will rise. The federal government must create policy incentives to reduce tort variability between states, promote capital expenditure to get informatics to the bedside, and compensate high-risk specialty providers for the high premium costs associated with regionalized care.

Standard Legal Definitions Used for This Study

Adjudication: Determination of the controversy in a court of law and pronouncement of judgment based on presented evidence

Adverse Medical Event: Injury to the patient that may have been the result of medical or surgical intervention that may prolong hospitalization, produce a disability, death or both

Claim File: File opened by the risk management staff whenever concern was expressed about an adverse event, a medical error was identified, or the patient or the patient’s family made the threat of legal action

Case Settled: Indemnity payment made before adjudication in court

Indemnity Payment: Payment that accepts whole or partial responsibility for a loss sustained by another

Non-Suit/No Case: No actual claim was filed by the patient and/or family

Open-in-Suit: The malpractice suit/claim is being actively pursued; the outcome is still pending

Summary Judgment: An entry of judgment by the court after review of claims and evidence before a trial wherein the court determines that there is no genuine issue or dispute, and that evidence is insufficient to allow such a claim. Judgment is rendered in favor of one party.

Write Off: Hospital and physician charges resulting from the hospitalization are dismissed from the responsibility of the patient and/or family

Discussion

Dr. J. Wayne Meredith (Winston-Salem, NC): This presentation and this manuscript are creative, candid, and courageous: creative in its techniques and taking advantage of its risk management groups, candid in its description of its problems, and courageous in its recommendations. This report reviewed the experience of a mature self-insured integrated enterprise-wide risk management program. They found that the awards are not related to the degree or the presence of negligence. This points out major problems in our current tort system. Our current system does not punish negligence. Our current system does not stimulate improvements in healthcare provision to patients. And our current system does not equitably compensate those who have been injured. It doesn’t even identify most of those who have been injured. The authors also found that our classical quality improvement measures, M&M conferences and those things, do not detect system design errors; they detect provider-related errors. And lastly, the authors show that interdisciplinary communication is a key factor in error reduction.

I would ask the authors to elaborate on a few things. Their manuscript is really worth reading and has lot of good recommendations in it that his presentation did not have time to make. So I want to invite him to say some of those things.

First, a question that is not answered: This process needs to be done in lots of medical centers to look at our legal system and to look at how we can improve patient safety. Can this be done in institutions that aren’t self-insured? Can this be done in institutions that don’t have enterprise-wide self-insurance programs and mature risk management programs? What do you do differently now? And what do the rest of us need to do differently? And what do you recommend for our tort system?

Dr. Hiram C. Polk, Jr. (Louisville, KY): This has been a good scientific meeting for the Southern, but I would suggest, with all due respect to the other presenters, that this is the most important paper presented at this meeting. We are indebted to Dr. Morris for having shifted his career from leadership in trauma to something that is new and unique and badly needed.

I want to make a couple of points that are not questions but emphases that need to be made from this presentation.

The issue is not professional liability; the issue is patient safety. When we talk about professional liability, it is seen as a very self-serving discussion by everyone. Talking about patient safety is the role surgeons need to take. I would say that surgery in America and surgeon organizations have been slow and not focused in beginning to address what is a front-burner public issue: patient safety.

I congratulate Dr. Morris on having done such a good job. He needs to lead more of us to contribute to the answers to this puzzle. All of us can make part of these observations, and all of us can come to many of the same kinds of conclusions, no matter what your system is.

I thought the most dramatic thing in this paper as presented this morning was the fact that there were two more systems that failed when claims were actually paid, compared to those when awards were not made. There is just a treasure trove of data in here. More importantly, all of us ought to begin to ask questions like this, not dealing with professional liability, but dealing with patient safety.

Dr. J. Alex Haller, Jr. (Baltimore, MD): Dr. Morris, I would like to ask you a few questions about your experience at Vanderbilt with risk management. You are worried that your trauma service has the poorest batting average. I am wondering if that is related to the fact that since there are multiple organ systems involved in those trauma patients, there are multiple services involved in their care. Thus, there is a greater chance for communications breakdown.

In our experience at Hopkins, we have found that the interplay of the hospital ethics committee has had an increasing impact on patient safety and quality of patient management. That surprised me at first, but as I have participated in it, many communication problems will ultimately become the focus of a family not being happy with the way they are being managed. They and the staff may ask if this is ethically appropriate, what is the next step in treatment? At this point the ethics committee may get called in consultation. In reviewing our recent experience, frequently when there is a safety problem or there has been a misadventure in management, with the participation of the ethics committee the resolution of these conflicts has often been resolved, having a disinterested party come in and has identified the miscommunication which was going on.

So my question to you is, What role does your hospital ethics committee play in your risk management process? If not, do you think it would be helpful to have such an input?

I think your paper is a very important one for us all.

Dr. Ward O. Griffen, Jr. (Frankfort, MI): Dr. Morris, I really enjoyed this paper. I didn’t get a chance to look at the manuscript, but I noticed that you didn’t mention M&M conferences in your presentation, although your title certainly was intriguing in mentioning M&M conferences. Having visited many institutions and participated in M&M conferences, I can tell you that they are quite different. In some places, they do in fact try to root out where the error was made, and they hold the individual accountable but blameless, which I think is a very good teaching method. On the other hand, there are M&M conferences in which the physicians try to find out how the disease caused the complication or the death of the patient rather than trying to figure out what really happened and what went on. My question is: cannot we improve our performance by addressing some of the issues that you have brought up in a well-structured M&M conference?

Dr. Richard J. Howard (Gainesville, FL): I also enjoyed this paper. One of the most vexing issues, it seems to me, is the reporting of adverse events, because reporting adverse events potentially leads to punishment of the reporter, with states and the country having database systems that now record some of these outcomes. In thinking about this, how do you suggest that adverse events be encouraged to be reported without punishing potentially the service, the physician, or the person who reports them?

Dr. John A. Morris, Jr. (Nashville, TN): Dr. Meredith asked, what can we do if we are not in a self-insured environment? Understand that self-insured environment is a product of the risk management function. What can you do if you are not self-insured? If you want to lower your premiums and you want to lower the amount that you pay out, get self-insured, get a consolidated strategy. That is very clear. What can you do if you don’t have that? Everything on the performance improvement side you can do, all of the things which increase safety and lower risk of adverse events. What are some of those things? Well, we talked about the culture change. But how do you get it down to practical execution steps? I think there are some things that we need to do in terms of structure. We are now looking at a very high-level committee which will be empowered by the medical center to make policy changes and to make behavioral changes. Now, whether we actually take the hard steps and implement both the restructuring of our performance improvement process and, more importantly, the execution of change remains to be seen. Perhaps that will be the subject of my next report some years from now. There are clearly things that we can do on execution.

Data capture: Electronic bedside data capture is a major thing. To believe that we had 31,000 admissions and 130 adverse events is absolutely ludicrous. We need to start capturing all adverse events in a consolidated fashion.

That brings me to one of Dr. Griffen’s points, which is, how do we change M&M? Or do we need to change M&M? M&M is a good thing. But M&M looks at individuals and not patient populations. And we need to add to M&M and make our residents understand that we are also treating populations of patients. And we need to have reports in M&M that are nationally benchmarked and say that our incidents of ventilator-associated pneumonia are in the 40th percentile or 80th percentile. That is valuable information, and we have to teach the house staff to look at things from that perspective.

Dr. Haller’s question about the ethics committee. Our ethics committee, at least in my perspective, is not helpful. What is helpful is to have a committee who is capable of guiding individual practitioners to better communication outcomes with their family. I would say parenthetically, as Dr. Haller probably knows, Gerry Hickson, who is at our institution, has made a career of looking at the doctor–patient communication side of the equation. We have a lot of information on that. My view from 100,000 feet is that that doctor-to-patient communication is more important in the lower-acuity, less intense environments, important in terms of claims filed, than the high-acuity environments that we studied here. The high-acuity environments are much more sensitive with catastrophic outcome, be that catastrophic outcome a result of negligence or be it the result of the disease process.

And finally, the question on reporting adverse events. I think we have to make a distinction about what we report internally and what we report externally. External reporting is done based on claims filed. The internal reporting, which is the most important, is the culture change that we are going to have to put in place to be able to capture that information, because a lot of this information is actually not known to the doctors. It occurs at the level of the nursing staff or it occurs in other system environments. And we need to make sure that throughout our institution we have that culture of blameless reporting.

References

- 1.Cox T. Doctors facing dilemma. Charleston Daily Mail. April 10, 2002.

- 2.Pennsylvania Medical Society press release; www.pamsmed.org.

- 3.Rivera P. Malpractice rates take a feverish leap: Texas doctors hit hard by increases, which insurers say are needed. Dallas Morning News. Jan. 20, 2002.

- 4.Booth W. Las Vegas trauma center closes as doctors quit; surgeon cite rising costs of malpractice insurance, lawsuits. A growing problem. Washington Post. July 4, 2002.

- 5.Warner J, Advanti P, Large A. Managing health care malpractice costs. The Advisory Board, June 2002.

- 6.“Malpractice Claims Description Codes” adapted from the Harvard Risk Management Foundation Allegation of Negligence.

- 7.MacKenzie EJ, Morris JA Jr, Smith G, et al. Acute hospital costs of trauma in the Untied States: Implications for regionalized systems of care. J Trauma. 1990; 30: 1096–1103. [DOI] [PubMed] [Google Scholar]

- 8.Brennan TA, Sox CM, Burstin HR. Identification of adverse events occurring during hospitalization. Ann Intern Med. 1990; 112: 221–226. [DOI] [PubMed] [Google Scholar]

- 9.Hickson GB, et al. Factors that prompted families to file medical malpractice claims following prenatal injuries. JAMA. 1992; 267: 1359–1363. [PubMed] [Google Scholar]

- 10.Pichert JW, Hickson GB, et al. Understanding the etiology of serious medical events involving children: Implications for pediatricians and their risk managers. Pediatr Ann. 1997; 26: 160–172. [DOI] [PubMed] [Google Scholar]

Footnotes

Presented at the 114th Annual Session of the Southern Surgical Association, December 1–4, 2002, Palm Beach, Florida.

Correspondence: John A. Morris, Jr., MD, Section of Surgical Sciences, Division of Trauma and Surgical Critical Care, 243 Medical Center South, 2100 Pierce Avenue, Nashville, TN 37212-3755.

E-mail: john.morris@vanderbilt.edu

Accepted for publication December 2002.