ABSTRACT

Background

The government is prohibited from directly negotiating drug prices for Medicare Part D, resulting in substantial policy debate. However, the government has an established mechanism for setting prices with pharmaceutical manufacturers for certain other federal programs - the Federal Supply Schedule (FSS).

Objective

To estimate how much could be saved nationwide if prices equivalent to the 2006 FSS were achieved for the top 200 drug formulations dispensed to seniors.

Design/Setting

Cross-sectional analysis of drug utilization patterns and costs from the nationally representative Medical Expenditure Panel Surveys (MEPS), 2003–2004, and the 2006 FSS.

Participants

Seniors who filled a prescription for any of these common drugs (n = 6,135 individuals).

Measures

Prescription expenditures were obtained from MEPS, and a price/unit was calculated in 2006 dollars. This price/unit was compared to the 2006 FSS, and a savings/unit was calculated and summed across the observed units dispensed in MEPS.

Results

The potential annual savings with FSS prices would be $21.9 billion [95% confidence interval (CI), $21.1 billion to $22.8 billion]. If FSS prices were substituted for only the top ten drugs, the annual savings would be $5.9 billion (95% CI, $5.7 billion, $6.1 billion).

Conclusions

Extension of existing price setting mechanisms to Medicare could save tens of billions of dollars if prices similar to those already achieved by other federal programs could be reached. Whether or not this is a political or economic possibility, the magnitude of these savings cannot be ignored.

KEY WORDS: medicare, pharmaceuticals, costs of care

INTRODUCTION

Federal negotiation of prescription drug prices on behalf of Medicare beneficiaries is a contentious, but timely, issue. In authorizing Medicare Part D in 2003, Congress explicitly forbade the federal government from directly negotiating prices with pharmaceutical companies.1 The rationale was that the market would lower prices and that each of the private prescription drug plans, in competition to attract more Medicare beneficiaries, would negotiate with prescription manufacturers to reduce costs.

Whether the market has truly been successful in lowering prescription drug prices to the extent that the writers of the legislation had hoped is a subject of current debate. A survey of almost 2,000 seniors in late 2006 found that 52% were saving money with Part D.2 Early nationally representative data recently released suggest a small, but appreciable, decrease in out-of-pocket spending and cost-related medication nonadherence with Part D.3,4 There is some evidence of price increases under Part D, however,5 and many critics of the non-negotiation clause point to Veterans Administration prices to show that direct negotiation by the federal government and price control statutes could result in greater savings. A report by Families USA, which looked at the top 20 drugs prescribed to seniors, found that VA prices were substantially lower than the cheapest Part D plans, with a median price difference of 58%.6

With Medicare and Medicaid spending projected to account for over 30% of the federal budget in 10 years, every possible avenue for cost savings in prescription drugs must be entertained.7 The Federal Supply Schedule (FSS) is a federal contract and list of prices for prescription drugs available for purchase by certain federal agencies, which include the VA, Department of Defense (DOD), Public Health Service (PHS), Bureau of Prisons, the District of Columbia, U.S. territorial governments, and some Indian Tribal governments.8 Drug manufacturers are effectively required to limit their FSS price to the lowest price that is charged to any private purchaser in the US, net of all rebates or other price concessions. Under the Veterans Health Care Act of 1992, drug manufacturers are required to list their brand-name drugs on the FSS for them to be covered by Medicaid. In 2003, sales under FSS contracts totaled around $4.5 billion for brand-name drugs, and costs were approximately 53% of the average wholesale price (AWP).8 Drug manufacturers are also required to sell certain drugs - about 1/3 of the drugs on the schedule - to the VA, DOD, PHS, and Coast Guard (the “Big Four”) at a price that is often even lower, the Federal Ceiling Price (FCP), which is statutorily defined rather than negotiated (approximately 50% of the AWP).8 Finally, statute determines that FSS prices are not allowed to rise faster than general inflation over the course of multi-year contracts By contrast, drug prices in the private market have grown considerably faster than the CPI.9

The FSS is publicly available and represents prices that are set through government statute and negotiation without formularies. To inform the debate about the potential savings associated with government negotiation of drug prices, we used actual prescription utilization and cost data from the nationally representative Medical Expenditure Panel Survey (MEPS) to estimate the potential savings prior to Part D if FSS prices were available to seniors.

METHODS

Data

This analysis is based on data from the 2003–2004 Medical Expenditure Panel Survey Household Component (MEPS), a nationally representative survey of the US civilian, non-institutionalized population, conducted by the Agency for Healthcare Research and Quality. Details of the survey design have been previously published.10 MEPS provides data on demographic characteristics, insurance coverage, and the utilization of health-care services for all individuals in the sampled households. Household respondents were asked to provide the names of all outpatient medications used by each household member, the names and locations of the pharmacies where each medication was obtained, and for permission to obtain records from each of the pharmacies.11 Pharmacies then provided data on total expenditures paid by all parties for the drug and the data necessary to assign a National Drug Code (NDC) to each prescription. The NDC is specific for prescription characteristics, including the manufacturer, ingredients, strength, and package size.

The Federal Supply Schedule (FSS) was obtained on 16 November 2006 from the VA website (http://www.pbm.va.gov/DrugPharmaceuticalPrices.aspx). MEPS data were merged with this list of FSS prices using the NDC, drug name, dose, form, and unit to obtain the FSS price for each drug-dose combination found in MEPS.

Study Sample

Adults who were at least 65 years of age and used at least 1 of the 200 drug formulations most often used by adults 65 and older in 2004 were included in this analysis (75% of all prescriptions dispensed for this population). We chose to study savings based on participation by all Medicare beneficiaries as a primary analysis since these data were collected prior to Part D, and therefore we could not distinguish between those who would join Part D in 2006 and those who would not. In addition, we believe an analysis of savings with FSS prices for all Medicare beneficiaries has relevance regardless of the current political feasibility of a single Medicare formulary. As a secondary data analysis, however, we did calculate savings using FSS prices for the subset of seniors with current supplemental coverage in addition to Medicare. Seniors with private supplemental coverage presumably have plans that have negotiated for the best prescription prices, allowing a comparison of prices on the FSS to prices that are already negotiated by market forces, akin to Medicare Part D.

Any two drug formulations that represented one unique drug were combined (e.g., diltiazem and diltiazem hcl). Drugs that were subsequently withdrawn from the market (i.e., rofecoxib) were excluded. In addition, aspirin was excluded because it is available over-the-counter, and insulin preparations were excluded as well because of difficulty calculating dose in MEPS. After accounting for similar formulations and exclusions, 161 unique drugs were included in this analysis, which accounted for 71% of total prescription spending among this age group.

Calculation of Prices and Potential Savings

We obtained information about the total expenditure for each drug from MEPS, including the amount spent by the individual and the amount paid by any insurance coverage. We calculated the expenditure per unit (i.e., tablet, vial, tube) for each drug in MEPS and in the FSS, in 2006 dollars. The availability of the actual drug expenditures for each product is an improvement over previous estimates of drug costs, which use a standard discount off the average wholesale price because actual expenditures are not typically available.10 Prices from the FSS were current for 2006. To inflate MEPS expenditures to 2006 dollars, we increased the 2003 expenditures by 8.4% and the 2004 expenditures by 6.1%, representing the increase in the consumer price index over those years.12 We then subtracted the FSS cost from the MEPS expenditure to get a savings per unit and multiplied this by the observed number of units purchased in MEPS to get a savings for each prescription. Savings for all prescriptions were totaled for each subject to calculate the annual per capita savings (both out-of-pocket savings plus savings to any insurance plan). We then calculated overall savings from a population perspective. The calculation using the top 200 drug formulations was the primary analysis. We also calculated the potential savings for the subgroup of the top 10 most commonly used drugs, as it may be more feasible initially to negotiate a more limited sample of drugs. Finally, as an additional sensitivity analysis, we calculated savings for the entire sample assuming varying abilities to negotiate prices down to the FSS level (i.e., prices of FSS 5%, FSS 10%). This sensitivity analysis was also done to address the concern that MEPS data may not reflect the rebates that health plans receive for drug costs.

Data Analysis

Median annual savings per person were compared across demographic groups using Wilcoxon rank sum or Kruskal-Wallis tests when appropriate. The MEPS data include sampling weights that reflect the survey design, sampling frame, and adjustments for household non-response and planned over-sampling. The weighted results therefore represent estimates for the non-institutionalized US population. All analyses were performed using SAS (version 9, SAS Institute, Inc., Cary, NC) and SUDAAN (version 9.0) and employed the appropriate weighting and survey design variables to obtain these population estimates.

RESULTS

Characteristics of the Sample

There were 150,687 prescriptions for eligible drugs. A total of 4,412 prescriptions (2.9%) could not be matched to a FSS price, and an additional 836 (0.5%) were missing a prescription quantity in MEPS. Thus, the final sample was 145,439 prescriptions and 6,135 individuals, weighted to represent 1,354,700,000 prescriptions and 60,071,166 individuals over these 2 years. In 2004, the total expenditures for these drugs were $48 billion. More than half of the sample were 65–74 years of age, and they were predominantly white, with a high school degree or less (Table 1). In addition to Medicare, 54% of the sample had supplemental insurance.

Table 1.

Characteristics of US Seniors 65 Years and Older Taking at Least One of the Top 200 Drug Formulations in 2003–2004, Included in the Medical Expenditure Panel Survey (MEPS)

| Unweighted (N) | Percentage* | |

|---|---|---|

| Total | 6,153 | |

| Age | ||

| 65–74 years | 3,230 | 52.0% |

| 75–84 years | 2,282 | 37.1% |

| >85 years | 641 | 10.8% |

| Gender | ||

| Male | 2,365 | 41.5% |

| Female | 3,788 | 58.5% |

| Race/ethnicity | ||

| White | 4,372 | 82.6% |

| Black | 753 | 8.0% |

| Hispanic | 789 | 5.7% |

| Asian or other | 239 | 3.7% |

| Education** | ||

| High school or less | 4,189 | 62.9% |

| College | 924 | 17.6% |

| Post-college | 976 | 19.5% |

| Household income** | ||

| <$12,000 | 1,183 | 13.4% |

| $12,000–$23,999 | 1,458 | 25.5% |

| $24,000–$47,999 | 1,722 | 29.2% |

| ≥$48,000 | 1,684 | 31.8% |

| Insurance | ||

| Medicare alone | 2,167 | 34.8% |

| Medicare with supplemental insurance | 2,875 | 54.3% |

| Medicare with Medicaid or other public program | 1,062 | 10.2% |

| Other*** | 49 | 0.6% |

| Chronic conditions | ||

| 0 | 3,463 | 55.7% |

| 1 | 1,535 | 24.2% |

| >=2 | 1,155 | 20.1% |

Note: Top 200 drug formulations defined by number of prescriptions, not expenditure; translates into 161 unique drugs after combining some formulations (diltiazem and diltiazem hcl) and excluding withdrawn drugs (e.g., rofexocib)

*Frequencies are weighted to represent the US population

**Sixty-four missing from education; 106 missing from household income

***Includes 26 seniors who only reported employer-sponsored insurance, 22 who were uninsured, and 1 with insurance classified as “other” in MEPS

Potential Annual Savings

The potential annual savings in drug expenditures if FSS prices were substituted for current prices is $21.9 billion [95% confidence interval (CI), $21.1 billion, $22.8 billion]. The median per capita annual savings in total expenditures is $483 (interquartile range $194 to $975). Seniors with less education and income, more chronic conditions, and older age have more savings with the substitution of FSS prices (Table 2; p < .001, p < .001, p < .001, and p = .004, respectively). For the subset of seniors who currently have supplemental coverage in addition to Medicare, using FSS prices rather than the prices they currently pay would save $11.3 billion (95% CI, $10.6 billion, $11.9 billion).

Table 2.

Potential Per Person Annual Savings in Total Drug Expenditures with Federal Supply Schedule Prices, for US Seniors 65 Years and Older*

| Median (interquartile range)** | P value*** | |

|---|---|---|

| Total | $483.46 (194.38–974.87) | |

| Age | .004 | |

| 65–74 years | 438.02 (170.40–938.04) | |

| 75–84 years | 510.79 (226.95–1,032.07) | |

| >85 years | 534.83 (242.90–988.37) | |

| Gender | .67 | |

| Male | 471.34 (196.01–945.78) | |

| Female | 491.90 (192.87–1,004.74) | |

| Race/ethnicity | .03 | |

| White | 496.66 (199.30–983.58) | |

| Black | 469.67 (187.44–983.22) | |

| Hispanic | 450.20 (177.02–916.07) | |

| Asian or other | 304.02 (147.07–868.18) | |

| Education | <.001 | |

| High school or less | 519.18 (211.27–1,048.49) | |

| College | 440.12 (186.74–944.17) | |

| Post-college | 383.20 (159.93–809.49) | |

| Household income | <.001 | |

| <$12,000 | 560.09 (235.88–1,127.15) | |

| $12,000–$23,999 | 515.44 (209.92–1,052.23) | |

| $24,000-$47,999 | 468.05 (195.25–990.16) | |

| ≥$48,000 | 430.71 (176.60–847.48) | |

| Insurance | <.001 | |

| Medicare alone | 458.28 (185.22–970.23) | |

| Medicare with supplemental insurance | 473.36 (193.65–937.32) | |

| Medicare with Medicaid or other public program | 633.00 (248.79–1,250.42) | |

| Chronic conditions | <.001 | |

| 0 | 389.91 (159.83–811.88) | |

| 1 | 590.52 (276.25–1,134.49) | |

| ≥2 | 625.90 (253.08–1,246.11) |

*Data derived from the Medical Expenditure Panel Survey and weighted to be representative of the US population

**Calculated in 2006 $

***P value testing for difference in median annual savings between the groups listed in each category

The top ten drugs used by seniors are listed in Table 3, with the associated annual savings if FSS prices were substituted for the entire sample. Atorvastatin (Lipitor) was the most commonly prescribed medication among the sample, with a national estimated savings of $1.3 billion, which represents a savings of 29% off current expenditures for Lipitor. Overall, savings from the top ten drugs using FSS prices would be approximately $5.9 billion (95% CI, $5.7 billion, $6.1 billion).

Table 3.

Top Ten Drugs Used in the US by Volume and Associated Savings with Federal Supply Schedule

| Prescription drug | Annual # prescriptions (weighted) | Current expenditures, Medical Expenditure Panel Survey* | Absolute savings with Federal Supply Schedule prices * | Percentage of current expenditure saved* |

|---|---|---|---|---|

| Atorvastatin (Lipitor) | 39,604,209 | $4,503,599,518 | $1,321,679,381 | 29.3% |

| Furosemide | 25,436,137 | 285,571,827 | 263,271,595 | 92.2% |

| Lisinopril | 23,265,084 | 1,164,407,869 | 1,061,399,316 | 91.2% |

| Hydrochlorothiazide | 22,127,830 | 210,155,282 | 182,224,109 | 86.7% |

| Atenolol | 21,679,039 | 993,571,279 | 945,249,018 | 95.1% |

| Amlodipine (Norvasc) | 19,960,498 | 1,493,847,690 | 456,753,328 | 30.6% |

| Levothyroxine (Synthroid) | 19,666,947 | 523,465,215 | 443,815,117 | 84.8% |

| Simvastatin (Zocor) | 19,224,615 | 2,358,898,147 | 662,973,114 | 28.1% |

| Metoprolol SR (Toprol XL) | 15,998,237 | 840,934,795 | 169,061,035 | 20.1% |

| Clopidogrel (Plavix) | 13,132,527 | 1,753,964,659 | 390,588,927 | 22.3% |

*All amounts are calculated in 2006 dollars

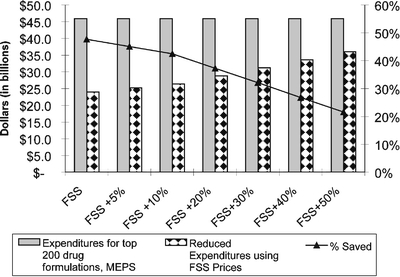

Savings with Varying Assumptions About FSS Price

Figure 1 shows the savings with varying assumptions about the success of any negotiations on drug pricing, represented as a percentage difference from the actual FSS price. For example, if prices were to reach FSS prices 5% (slightly higher than FSS prices), the amount saved would decrease slightly to $20.7 billion, which is a 45.1% savings. Similarly, if prices were to decrease only to FSS levels 50%, the amount saved would be $9.9 billion, or 21.6% of current expenditures.

Figure 1.

Sensitivity analysis, showing savings using federal supply schedule prices for seniors with varying assumptions about the government’s ability to negotiate (all in 2006 dollars).

DISCUSSION

This analysis, using nationally representative data from MEPS that captures the actual utilization of prescription drugs, suggests an approximate annual savings of $21.9 billion, or $483 per person, with the substitution of the FSS price for seniors prior to Part D. A substantial savings of over $11 billion dollars is present if FSS prices are substituted only for the subgroup of seniors with private supplemental coverage in addition to Medicare. A savings of $483 per person is a significant discount, considering that in 2004 the amount of money spent per capita for prescription drugs for those over the age of 65 was $1,550.13 Whether these savings would be passed on to patients or retained by their health plans, they would potentially leave more resources in the health-care system to treat more patients and more conditions. Even if the prices were set at 50% higher than the 2006 FSS, the savings would still be over 20% for these drugs. The magnitude of these numbers has significant implications in the debate on whether or not the government should be directly involved in setting drug prices on behalf of Medicare Part D.

To our knowledge, there have been no prior national estimates of the potential savings to Medicare if FSS prices were used for drug purchases. A report by Families USA comparing prices found in the VA with prices under various Part D plans found a 58% median difference in prices, which is consistent with the substantial savings demonstrated in this analysis.6 In addition, there is evidence that FSS prices are fairly similar to prices paid by the Canadian government,14 and prior work has compared Canadian prices to the higher current commercial US prices.15,16

There is considerable debate about whether negotiation by the federal government would actually lead to lower prices without the imposition of nationwide formulary restrictions that the public might not accept.17–19 The nonpartisan Congressional Budget Office (CBO) stated in a letter to Senator Bill Frist in January 2004 that removing the “noninterference” provision of the Medicare Modernization Act of 2003 (the section of Part D that forbids the government to directly negotiate drug prices for seniors) would have a “negligible effect on federal spending.”20 The CBO letter went on to say that for drugs that face competition with other therapeutically similar drugs, the market would be as successful as government negotiation in lowering drug prices. However, definitive empirical evidence as to how successful the market has been in lowering prices is lacking, and there is also no consensus about what a “successful” reduction in drug prices by market forces would be. The little we know about 2006 PDP drug prices comes from the Families USA study showing that prices in PDPs are not nearly as low as at the VA, and from a separate analysis released by CMS showing that drug prices in the median cost PDP are on average only 25% lower than cash prices, although significant variation exists.21 Some data suggest that prices for certain drugs have actually increased with Part D, and data from the National Health Expenditure Accounts show that overall drug prices increased in both 2005 and 2006 at 3.6 percent.5,22

The CBO did say that some savings were possible if the government could negotiate prices with manufacturers of drugs with no competition from therapeutic alternatives - drugs such as clopidogrel (Plavix).20 Our analysis quantifies some of these potential savings. Included in the list of top ten drugs used by seniors is one that has no real therapeutically equivalent competitor on the market [clopidogrel (Plavix)]. Combined savings from using FSS prices for just this one drug would total almost 400 million dollars annually. Clopidogrel is one of the medications whose price has reportedly increased in Part D.5

The ability of the government to extend prices from the federal supply schedule to the much larger population of Medicare beneficiaries is uncertain. However, the FSS is a clear example of a set of drugs available to federal purchasers that is negotiated by the government without a formulary. We believe this makes the FSS, and our analysis, very relevant to the discussion on federal negotiation of drug prices and important for moving the Medicare debate forward. While these exact FSS prices may not be negotiated for Part D, our sensitivity analysis suggests that almost $10 billion could still be saved annually if these drugs were subjected to FSS prices plus 50%. In addition, for seniors who already have private supplemental insurance in addition to Medicare, price differences with the FSS amount to billions of dollars. The magnitude of these price differences between commercial and FSS prices is striking, regardless of the economic feasibility for Medicare of this kind of negotiation. This paper estimates the savings that could exist if FSS prices were substituted for current drug prices among seniors, and it is not meant to be an exhaustive analysis of the economic complexities surrounding federal negotiation of pharmaceutical prices. The actual consequences of opening up the Federal Supply Schedule to a larger group are unknown.23 There would likely be spillover effects with higher prices for cash-paying customers and private health plans as manufacturers work to regain profits, or perhaps less capacity for research and development by pharmaceutical manufacturers. There would be administrative costs associated with federal negotiation of prices that are not modeled here, although there may also likely be savings to the manufacturers in having to negotiate only once. A full discussion of these complexities is beyond the scope of this paper.

The results of this study must be interpreted in the context of the study design and data sources. While the use of 2003–2004 data is not ideal, there is no public nationally representative data of this kind about expenditures under Part D. While market forces may have changed the prices and patterns of utilization of drugs somewhat over the 2–3-year period (between 2003–2004 and 2006), MEPS is the most recent nationally representative source of prescription expenditures available that reflects actual drug utilization patterns nationally. This allows us to use the detailed data that are available in MEPS on individual insurance, copays, the frequency of refills, the number of pills per prescription (30 vs. 90 day), etc. It will be critical once 2006 data become available to determine whether negotiation of prices in part D has saved money for seniors and for society. We do note, however, that one study described above does demonstrate that Part D prices are very much higher than VA prices - on the same order of magnitude as found in this study. Additionally, our inflation of MEPS expenditures by the consumer price index may actually underestimate true prices in 2006, since drug prices are known to increase faster than inflation - this would lead to an underestimation of savings.24 In fact, recent data have shown that prescription spending outpaced inflation by significant amounts between 2004–2006, and the number of prescriptions purchased by Medicare beneficiaries actually increased more rapidly in 2006 than in 2005.22

MEPS also unfortunately does not account for the rebates that flow from manufacturer to payor and PDP, which may lead to an overestimate of drug expenditures in MEPS. However, data on rebates are proprietary, and it is unknown how significantly they would affect overall expenditures, and for what drugs. A recent congressional report estimated that insurers in Medicare Part D received rebates from pharmaceutical manufacturers of 5% in 2006.25 A previous government estimate in 1997 reported manufacturer rebates of 7% on average.26 Basic Medicaid rebates are on average 15% of the Average Manufacturers Price (AMP); however, the AMP is also not publicly available.8 Ultimately, our sensitivity analysis shows that these rebates are unlikely to be large enough to completely remove the savings calculated in this study. Finally, FSS prices are available to those agencies that dispense their own drugs and therefore do not take into account dispensing fees, while MEPS expenditures include the cost to the pharmacy of dispensing the medicine. Although this may overestimate the savings we calculate, it also would not likely be enough to change the results of the sensitivity analysis.

While the debate about negotiation of drug prices continues, prescription spending continues to increase faster than inflation and occupies a growing percentage of our national health expenditures.9,22,27,28 The use of lower-price generic drugs through tiered benefits, shifts towards mail-order pharmacy, and the removal from the market of highly priced drugs that turned out to be dangerous have contributed to some modest slowing in the rate of growth in drug spending until recently.9 However, as rates of diabetes and other chronic diseases increase and a larger percentage of the population enters Medicare, these rates of growth may not be sustainable. The pricing of prescription drugs under Medicare Part D will be a central issue for cost containment in the future.

An annual savings of over $20 billion could be realized if FSS prices could be achieved by the federal government for the majority of drugs used by seniors in 2003–2004, and there would be substantial savings if prices were only to reach FSS levels plus 50%. Whether or not price negotiation or price setting for prescription drugs in Medicare is a political or economic possibility, the magnitude of these savings should not be ignored.

Acknowledgements

This work was supported by the National Cancer Institute (R01 CA112451) and by a National Research Service Award (T32HP11001-18). The analysis was reviewed and approved by the Institutional Review Board of Partners HealthCare.

Conflict of Interest Dr. Schneeweiss previously received research grants from Pfizer and Merck for unrelated work (on the safety of coxibs). None of the other authors have a conflict of interest.

REFERENCES

- 1.Medicare program. Medicare prescription drug benefit. Final rule. Fed Regist. 2005;70184193–585. [PubMed]

- 2.Kaiser Family Foundation/Harvard School of Public Health. Seniors and the medicare prescription drug benefit; December 2006.

- 3.Madden JM, Graves AJ, Zhang F, et al. Cost-related medication nonadherence and spending on basic needs following implementation of medicare part D. JAMA. 2008;299161922–8. [DOI] [PMC free article] [PubMed]

- 4.Goldman DP, Joyce GF. Medicare part D: a successful start with room for improvement. JAMA. 2008;299161954–5. [DOI] [PMC free article] [PubMed]

- 5.Frank RG, Newhouse JP. Should drug prices be negotiated under part d of Medicare? and if so, how? Health Affairs. 2008;27133–43. [DOI] [PubMed]

- 6.Steinberg M, Bailey K. No Bargain: Medicare Drug Plans Deliver High Prices. Washington, D.C.: Families USA; 2007 January.

- 7.Testimony of Richard G Frank, Ph.D. In: US Senate Committee on Finance. Washington, D.C.; January 11, 2007.

- 8.Congressional Budget Office. Prices for Brand-Name Drugs Under Selected Federal Programs: The Congress of the United States; 2005, June.

- 9.Smith C, Cowan C, Heffler S, Catlin A. National health spending in 2004: recent slowdown led by prescription drug spending. Health Aff (Millwood). 2006;251186–96. [DOI] [PubMed]

- 10.Haas JS, Phillips KA, Gerstenberger EP, Seger AC. Potential savings from substituting generic drugs for brand-name drugs: medical expenditure panel survey, 1997–2000. Ann Intern Med. 2005;14211891–7. [DOI] [PubMed]

- 11.Moeller JF, Stagnitti MN, Horan E, Ward P, Kieffer N, Hock E. Outpatient Prescription Drugs: Data Collection and Editing in the 1996 Medical Expenditure Panel Survey (HC-010A). Rockville, MD: Agency for Healthcare Research and Quality; 2001.

- 12.Consumer Price Index.: Federal Reserve Bank of Minneapolis.

- 13.Centers for Medicare and Medicaid Services. 2004 National Health Expenditures Accounts. Available at http://www.cms.hhs.gov/NationalHealthExpendData/downloads/2004-age-tables.pdf. Accessed May 10, 2008.

- 14.Hollis A. How cheap are Canada’s drugs really? J Pharm Sci. 2004;72215–6. [PubMed]

- 15.Anderson GF, Shea DG, Hussey PS, Keyhani S, Zephyrin L. Doughnut holes and price controls. Health Aff (Millwood). 2004:W4–396-404. Suppl Web Exclusives. [DOI] [PubMed]

- 16.Quon BS, Firszt R, Eisenberg MJ. A comparison of brand-name drug prices between Canadian-based Internet pharmacies and major US drug chain pharmacies. Ann Intern Med. 2005;1436397–403. [DOI] [PubMed]

- 17.D’Angelo G, Moffit RE. H.R. 4: A Confusing and Contradictory Prescription for Medicare Drugs. Washington, DC: The Heritage Foundation; 2007January 11.

- 18.Enthoven A, Fong K. Medicare: Negotiated Drug Prices May Not Lower Costs. Dallas, TX: National Center for Policy Analysis; 2006 December 18.

- 19.Testimony of Richard G Frank, Ph.D. In: US Senate Committee on Finance. Washington, D.C.; January 11, 2007.

- 20.Holtz-Eakin D. Letter to Senator Ron Wyden, United States Senate; March 3, 2004.

- 21.Centers for Medicare and Medicaid Services. Drug Plan Finder Analysis: Medicare PDP Savings Compared to Cash Prices. October 12, 2006. Available at http://www.cms.hhs.gov/prescriptiondrugcovgenIn/downloads/planfinderanalysis.pdf. Accessed May 1, 2008.

- 22.Catlin A, Cowan C, Hartman M, Heffler S. National health spending in 2006: a year of change for prescription drugs. Health Aff (Millwood). 2008;27114–29. [DOI] [PubMed]

- 23.United States General Accounting Office. Drug Prices: Effects of Opening Federal Supply Schedule for Pharmaceuticals are Uncertain; June 1997.

- 24.Mahan D. Sticker Shock: Rising Prescription Drug Prices for Seniors. Washington, DC: Families USA; 2004 June.

- 25.Weisman J. Costs Grow for Common Medicare Drugs. Washington Post 2007 Sunday, May 13;Sect. A10.

- 26.Department of Health and Human Services. Report to the President: Prescription Drug Coverage, Spending, Utilization, and Prices. April 2000. Available at http://aspe.hhs.gov/health/reports/drugstudy. Accessed May 1, 2008.

- 27.Poisal JA, Truffer C, Smith S, et al. Health spending projections through 2016: modest changes obscure part D’s impact. Health Aff (Millwood) 2007. [DOI] [PubMed]

- 28.Zuvekas SH, Cohen JW. Prescription drugs and the changing concentration of health care expenditures. Health Aff (Millwood). 2007;261249–57. [DOI] [PubMed]