Abstract

Objective

The impact of consumer-driven health plans (CDHPs) has primarily been studied in a small number of large, self-insured employers, but this work may not generalize to the wide array of firms that make up the overall economy. The goal of our research is to examine effects of health savings accounts (HSAs) on total, medical, and pharmacy spending for a large number of small and midsized firms.

Data Sources

Health plan administrative data from a national insurer were used to measure spending for 76,310 enrollees over 3 years in 709 employers. All employers began offering a HSA-eligible plan either on a full-replacement basis or alongside traditional plans in 2006 and 2007 after previously offering only traditional plans in 2005.

Study Design

We employ difference-in-differences generalized linear regression models to examine the impact of switching to HSAs.

Data Extraction Methods

Claims data were aggregated to enrollee-years.

Principal Findings

For total spending, HSA enrollees spent roughly 5–7 percent less than non-HSA enrollees. For pharmacy spending, HSA enrollees spent 6–9 percent less than traditional plan enrollees. More of the spending decrease was observed in the first year of enrollment.

Conclusions

Our findings are consistent with the notion that CDHP benefit designs affect decisions that are at the discretion of the consumer, such as whether to fill or refill a prescription, but have less effect on care decisions that are more at the discretion of the provider.

Keywords: Consumer-driven health plans, high deductible health insurance, health savings accounts, benefit design

Consumer-driven health plans (CDHPs) or high-deductible health plans with saving accounts remain controversial in the ongoing health care reform debate; nonetheless, CDHPs have attracted considerable attention from employers, individuals, and policy makers because of their perceived potential to reduce health care costs. Broadly speaking, CDHPs feature higher deductible levels—generally in the range of U.S.$2,000—than traditional preferred provider organization (PPO) or health maintenance organization (HMO) plans, and they are typically combined with an account for first-dollar coverage under the deductible; in general the spending account will be less than the deductible leaving a period during which the enrollee is responsible for the full cost of health care, sometimes referred to as the “doughnut hole.” By exposing enrollees to the full price of treatment options more than PPO or HMO plans, CDHPs aim for enrollees to scrutinize more carefully the cost of services relative to their (perceived) benefits.

The prevalence of CDHPs has grown markedly over the past few years in the employer-sponsored health insurance market. The most recent Kaiser Family Foundation/HRET employer health benefit survey found that 13 percent of employers offered a CDHP in 2008, up from just 7 percent in 2006; 8 percent of employees were enrolled in such plans in 2008, up from 4 percent in 2006 (Claxton et al. 2008). Recent anecdotal reports suggest that the economic downturn is causing more families to turn to high-deductible CDHPs as a means of cutting their premium expenditures (Alderman 2009). Despite the interest, there remains surprisingly little known about the effects of high-deductible health plans with spending accounts for first dollar coverage on health care use and spending, and health outcomes.

While some research exists on how CDHPs affect health care spending and utilization, traditionally the work has been focused on small samples of large, self-insured, national employers; comparatively little is known about the effect of CDHP designs across a wide spectrum of firms of varying sizes and with varying degrees of take-up. For example, there are reasons to suspect firm-specific factors such as overall benefit generosity, human resources and benefits practices, and employee communications might have a strong influence on take-up. These and other factors could have a strong influence on the findings from studies that focus on only a handful of firms. Concern over the influence of firm-specific idiosyncratic factors on estimates is reduced when the sample includes a large number of firms. The goal of our research is to examine effects of CDHP enrollment on spending using a unique administrative dataset with enrollees from over 700 small and large employers from a large national insurer. We follow two cohorts of individuals before and after employers offered a CDHP: those that switch to a CDHP and those who stay in traditional plans. The findings from our study have important implications to policy makers, health insurance purchasers such as private employers and state governments, and consumers.

BACKGROUND AND PREVIOUS LITERATURE

The 2003 Medicare Modernization Act created health savings accounts (HSAs), now the most common type of CDHP. HSAs involve the pairing of a high-deductible health insurance plan with the establishment of an account that can be funded with pretax dollars and used to pay for eligible health care expenditures. The contributions to the account may earn interest and are owned by the individual akin to a bank account and thus are portable even after workers leave their job. The Internal Revenue Service (IRS) defined HSAs as having a minimum annual deductible of U.S.$1,050 for single enrollees and U.S.$2,100 for families (in 2006), though the deductible may be higher. The total annual tax-preferred contributions to the account cannot exceed the lesser of the deductible or U.S.$2,700 for singles or U.S.$5,450 for families. HSAs should be distinguished from health reimbursement arrangements (HRAs), which were formally established by an IRS administrative ruling in the summer of 2002. The key features of HRAs are the employer's contribution of pretax dollars to an account that can be used by the enrollee, but the enrollee does not own the account and thus HRAs are not portable. Our study focuses on HSAs.

The prior studies of CDHPs have several notable gaps and weaknesses. Past work commonly is based on case studies of a handful of employers or surveys of employer and employee attitudes and experiences with regard to CDHPs (see Buntin et al. 2006; Feldman, Parente, and Christianson 2007; Wharam et al. 2007). External validity is a challenge when only examining a few employers' experiences. Another concern is the potential for favorable selection into CDHPs, which could bias findings from earlier studies. Specifically, individuals who choose to switch to a relatively new health insurance product design over familiar alternatives such as HMOs or PPOs are likely to differ on unobservable factors related to their anticipated health care utilization leading to biased inference about the effect of CDHPs. Below we discuss the conditions under which bias from such selection will and will not occur.

There remains considerable controversy about the extent to which CDHP designs affect use of health care services. Much of the literature has focused on overall spending levels. A study by Parente, Feldman, and Christianson (2004b) did a pre/post comparison of “switchers” into CDHP relative to “stayers” remaining in traditional plans within a single large employer. While the authors found that baseline year spending for CDHP enrollees was 16 percent lower than that of HMO and PPO enrollees, their results suggested that spending increased more for the CDHP group than the controls in the postyear. Follow-up work revealed that 3 years after CDHP was offered, CDHP enrollees continued to have higher spending than point of service (POS) enrollees (Feldman et al. 2007); additionally, prescription drug spending did not differ between switchers and stayers (Parente, Feldman, and Chen 2008) beyond the first year. While these findings tend to be at odds with the notion that CDHPs serve to limit spending, how much one can conclude from single employer settings is not clear. Other recent employer-specific studies by Greene et al. (2008a, 2008b) found similar results to previous analyses. Interestingly, this work also found CDHPs were not as effective for drug adherence; CDHP enrollees were more likely to discontinue antihypertensive and lipid-lowering pharmacotherapy after implementation of the CDHP (Greene et al. 2008a).

Research has also found evidence of favorable selection into CDHPs. As stated earlier, Parente, Feldman, and Christianson (2004a) found that CHDP enrollees had lower initial health spending than HMO and PPO enrollees; however, a comparison of case-mix indicators supported the notion that the CDHP enrollees were also healthier than stayers. Another study of enrollees in a Humana CDHP indicated that individuals that switched into a CDHP were significantly less likely to have a chronic condition and were more likely to self-report their health as excellent (Fowles et al. 2004). For each of the five services studied, prior year utilization by people who subsequently enrolled in the CDHP was below 60 percent of the average for the whole group. Related research at Humana revealed that, based on demographic data alone, there was a minimal difference in the risk profiles of those choosing to enroll in the CDHP versus those remaining in traditional plans (Tollen, Ross, and Poor 2004). However, when examining prior year claims data the authors found that persons choosing the CDHP were healthier than stayers. Selection issues seem clearly critical in the study of CDHPs, as they have been historically for all forms of health insurance.

DATA AND METHODS

All data were extracted from the data repository of a large national insurer that provides a full complement of traditional plan designs in addition to being the leading provider of CDHPs in the country. The repository contains linkable datasets of member, employer, medical and pharmacy claims, and plan design information. Because a critical aspect of our approach involves selecting and subdividing cohorts of individuals based on the plans that are offered to them by their employers, data extraction began with the identification of employers. We included employers that did not offer a CDHP in 2005 that then offered HSA plans on either a full-replacement basis or as an option alongside traditional plans in 2006 and 2007. Employers included commercial groups with 2–5,000 employees offering both fully insured and administrative services only (ASO) products. The benefit of including employer sizes up to 5,000 is the ability to introduce variation in benefits that we seek to study. HSAs were chosen because they were the predominant CDHP offered by employers. Study inclusion criteria required employers to offer medical and pharmacy coverage to their employees for three consecutive years (2005, 2006, and 2007) with the same plan start date, January 1 (the most common), in each year. We identified 709 employers meeting our inclusion criteria. The employers included 457 HSA full-replacement employers (all of which were fully insured), 229 fully insured HSA option firms, and 23 (large) ASO option firms.

Our goal is to estimate the relative change in total health care spending (the sum of medical and pharmacy spending by both employers and employees) associated with a switch to HSAs. We use multivariate estimators to compare the difference in spending over time between individuals who enroll in an HSA (switchers) to those who remain in a traditional plan (stayers). All employees were continuously enrolled for 3 years. Employees were excluded if aged older than 65 years, had coordination of benefits (indicating other health insurance coverage), and total allowed spending exceeded U.S.$200,000 in any calendar year.

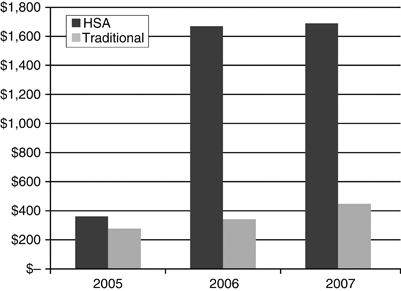

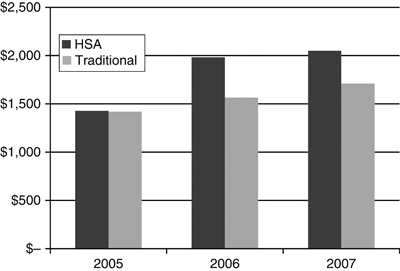

Figures 1 and 2 demonstrate the essential nature of the change in health insurance plan design that occurred coincident with enrollment in HSAs. Figure 1 indicates the substantial increase in the deductible among those who switch to the HSA: the mean deductible increases from U.S.$361 in 2005 to U.S.$1,689 in 2007. By contrast a relatively modest increase in deductibles is evident among the stayers, from U.S.$278 in 2005 to U.S.$447 in 2007. Of course it should be noted that a tax-advantaged savings account is available for HSA enrollees for first dollar coverage of health care needs. The out-of-pocket (OOP) maximum amounts (Figure 2) highlight that HSA enrollment is not necessarily synonymous with substantially higher OOP spending. HSA enrollees experience an increase in OOP maximum from U.S.$1,428 in 2005 to U.S.$2,050 in 2007, while traditional plan enrollees experience an increase from U.S.$1,420 to U.S.$1,710.

Figure 1.

Deductible Pre- and Post-HSA by Cohort, 2005–2007

Figure 2.

Out-of-Pocket Maximum Pre- and Post-HSA by Cohort, 2005–2007

Based on the differences in plan characteristics, we might expect to see pronounced effects of HSAs on spending relative to traditional plans. However, we lack two important details that limit our ability to predict the effect of a switch to HSAs: (1) we do not have information on the size of the savings account that is used for first dollar coverage and (2) we do not have information on whether or how much the employer contributes to the account. Both the account size and the employer contribution to it could mitigate the negative effect of HSA enrollment on spending. Moreover, we do not have information on how employers structured premium cost sharing for the plans offered and how it might have changed over time. Prior work has established that enrollees are quite sensitive to premium levels (Buchmueller and Feldstein 1996, 1997; Cutler and Reber 1998). Consequently, the effect of HSA enrollment on health care spending remains an empirical question.

In order to measure the overall effect of the switch to an HSA on health care spending, we employ a generalized linear model (GLM) with a log-link. This model is frequently applied to health care data because of its tractability and, given advances in personal computing, ease of estimation (Manning 1998; Mullahy 1998; Manning and Mullahy 2001;). The basic model with a log-link is

| (1) |

where Y is annual spending for person i in year t, Post is an indicator variable representing the years 2006 and 2007 (versus 2005), HSA is an indicator for whether the person is in the group that is enrolled or will enroll in an HSA, and the coefficient on the interaction term between HSA and Post reveals the difference-in-differences (DD) estimate of the effect of HSA enrollment on health care spending.1 Conveniently, with the log-link function, the coefficient estimate of interest (β3) can be interpreted directly as a multiplicative effect on total costs. The model also controls for enrollee characteristics (age, gender, region, and the type of plan in which the enrollee was enrolled in 2005—HMO, PPO, POS, exclusive provider organization (EPO), or indemnity) as well as 1-digit industry code dummies, size of the employer, the employer insurance type (full replacement, option—fully insured, option—ASO), and a year trend. The ɛ term is an idiosyncratic error.

Because there is the potential of the HSA effect to evolve with subsequent years enrolled in the plan, we also estimate a variant on equation (1) that allows for the effect of HSA enrollment to differ based on the year enrolled in the plan. For example, there could be a learning curve associated with individuals gaining comfort with a plan design they are experiencing potentially for the first time.

By, in effect, conditioning on pre-HSA enrollment spending we aim to minimize the potential selection problem that could exist if healthier employees opt to enroll in the HSA versus remaining in a traditional plan. The basic presumption of the DD model is that while the levels of spending might differ between switchers and stayers, the change in spending in the switcher group would have been the same as the stayers had the switcher group not enrolled in an HSA (the counterfactual). Counterfactual assumptions are inherently untestable, but given the rich data in our study it is possible to learn something about the validity of the quasi-experimental design by testing whether we observe different HSA effects between full-replacement enrollees, who presumably face a less voluntary switch to an HSA, and option enrollees, for whom selection is presumably most acute. Specifically we will specify a triple-difference (DDD) model to test whether the effect of HSAs differs between full-replacement enrollees and option enrollees:

| (2) |

where Full represents full replacement and now the coefficient we are primarily interested in is the three-way interactions between Post, HSA, and Full (β6): it tells us whether there is a difference in the DD estimate (in equation [1]) between full-replacement HSA enrollees and option HSA enrollees. In addition, another specification check involves estimating stratified regressions based on whether enrollees have chronic conditions in 2005. This allows us to test whether the effects of HSA enrollment are symmetric across different health statuses of enrollees.

While we lack a control group that is not exposed to CDHP, we have a group that receives only CDHP and another group that receives only a partial “dose” of CDHP, thus allowing us to estimate a true, if somewhat unconventional, intent-to-treat model. In this case, the group receiving HSAs on a full-replacement basis serves the function that a control group receiving no CDHP would serve. Specifically, we are able to estimate the treatment effect on the treated by estimating a model of the following model: spend=a+b Post+c Full+d Post×Full, where Full is an indicator for whether the person is a member of a full-replacement employer, and then scaling the d coefficient with 1−the take-up of HSA in the option group. This approach allows us to completely bypass individual-level selection as a potential source of bias because actual HSA enrollment (on an individual basis) never enters the estimation.

RESULTS

Descriptive Findings

Table 1 presents the baseline (2005) demographics of the 76,310 enrollees in employers that provided HSAs either on a full-replacement basis or as an option alongside traditional plans in 2006 and 2007 after not being offered a CDHP in 2005. Approximately one-third of the sample enrolled in an HSA in the postperiod. HSA enrollees had nearly equal gender composition and were slightly older, which is atypical relative to what is commonly seen in CDHP studies. Firm size is smaller in the HSA group primarily because a majority (56 percent) of the HSA group is comprised of full-replacement enrollees, and full replacement is far more common in small firms. Note that ASO group enrollees represent roughly half the sample overall but only 10 percent of HSA enrollees, implying that take-up was very low in the large, ASO firms (roughly 6 percent). A majority of the sample resides in the central region of the United States followed by about a quarter to a third of the sample in the southeast region. The most common industry in the sample is the service sector followed closely by finance, real estate, and insurance.

Table 1.

Baseline Demographics of HSA Switchers and Traditional Plan Stayers, 2005

| All | HSA Enrollees | Traditional Plan Enrollees | |

|---|---|---|---|

| Sample size | 76,310 | 23,587 | 52,723 |

| Female (%) | 50.8 | 50.4 | 51.0 |

| (SD) | (50.0) | (50.0) | (50.0) |

| Age | 32.9 | 33.2 | 32.8 |

| (17.7) | (17.9) | (17.6) | |

| Child under 18 (%) | 27.1 | 26.9 | 27.3 |

| (44.5) | (44.3) | (44.5) | |

| Firm size | 1,867 | 942 | 2,281 |

| (1,699) | (1,172) | (1,734) | |

| Firm type | |||

| Fully insured, full replacement | 17.3 | 56.0 | — |

| Fully insured, option | 32.1 | 34.2 | 31.2 |

| ASO, option | 50.6 | 9.8 | 68.8 |

| Region | |||

| Central | 47.6 | 62.8 | 40.9 |

| Northeast | 10.9 | 4.7 | 13.7 |

| Southeast | 29.8 | 24.2 | 32.4 |

| West | 11.6 | 8.4 | 13.0 |

| Industry (%) | |||

| Agriculture, forestry, fishing | 0.1 | 0.2 | 0.0 |

| Mining | 3.8 | 6.5 | 2.6 |

| Construction | 12.0 | 5.4 | 15.0 |

| Manufacturing | 11.8 | 7.9 | 13.5 |

| Transportation, communications, utilities | 2.4 | 3.6 | 1.9 |

| Wholesale trade | 12.0 | 8.0 | 13.8 |

| Retail trade | 12.1 | 7.0 | 14.4 |

| Insurance, real estate | 9.3 | 10.5 | 8.8 |

| Services | 33.2 | 45.7 | 26.1 |

| Public administration | 1.7 | 1.8 | 1.7 |

| Unknown | 2.6 | 3.5 | 2.2 |

ASO, administrative services only; HSA, health savings accounts.

The seeming similarity of the two groups (at least on demographics) is the result of two somewhat different samples being combined: the full-replacement group tends to be somewhat older (and less healthy) than voluntary HSA enrollees, who tend to be younger (and healthier). Table 2 presents measures of health status in the baseline (2005) year. Displayed are retrospective health risk scores that are calculated by Ingenix Episode Risk Group software. The software uses claims data grouped into episodes of care (based on ICD-9 diagnosis codes) and then calculates a risk score based on the mix of episodes. Another health status measure is an indicator for the presence of a chronic disease condition as measured by a person having select episodes (based on Ingenix software). It should be noted that half of individuals have some chronic illness and half of HSA enrollees have a chronic illness as well. Based on the measures of health risk, full-replacement enrollees were clearly less healthy than voluntary switchers. Voluntary switchers were also clearly healthier than the traditional plan stayers. This result is consistent with most of the prior literature examining the characteristics of enrollment in HSAs. Our regression models will include the type of insurance setting to control for these baseline health differences.

Table 2.

Baseline Health Status Measures of HSA Switchers and Traditional Plan Stayers, by Firm Type, 2005

| Sample Size | Retrospective Risk Score | Chronic Disease (%) | |

|---|---|---|---|

| All | 76,310 | 1.09 | 50.7 |

| HSA | 23,587 | 1.07 | 49.7 |

| Full replacement | 13,218 | 1.17 | 52.7 |

| Insured, option | 8,068 | 0.96 | 46.3 |

| ASO, option | 2,301 | 0.83 | 44.3 |

| Traditional plan | 52,722 | 1.09 | 51.1 |

| Full replacement | 0 | — | — |

| Insured, option | 16,433 | 1.07 | 52.3 |

| ASO, option | 36,290 | 1.10 | 50.6 |

ASO, administrative services only; HSA, health savings accounts.

Table 3 displays mean spending figures over time for the HSA enrollees and traditional plan stayers. Total health care spending is defined as the sum of medical (inpatient and outpatient) and pharmaceutical drug payments made by the plan and the member (employer and employee). The table also displays means of medical and pharmaceutical spending broken out separately. On average, total health care payments increased by just over 20 percent between 2005 and 2007. Medical expenditures increased over the period by 24 percent while pharmacy spending grew by roughly 10 percent. At baseline HSA enrollees were similar to traditional plan stayers in terms of overall spending: HSA enrollees spent 1.4 percent less in 2005 on average (before their enrollment in the HSA). However, total spending grew at a faster rate for traditional plan stayers relative to HSA enrollees (22 percent versus 18 percent). Medical spending was 3 percent lower for HSA enrollees and pharmacy spending was about 4 percent higher for HSA enrollees in 2005. Spending for medical services and pharmacy services grew at faster rates for traditional plan enrollees relative to HSA enrollees: 25 percent versus 22 percent for medical spending and 12.5 percent versus 7 percent for pharmacy spending over the period.

Table 3.

Descriptive Statistics of Health Care Spending by HSA Enrollment/Nonenrollment, 2005–2007

| All | HSA Enrollees | Traditional Plan Enrollees | |

|---|---|---|---|

| Sample size | 76,310 | 23,587 | 52,723 |

| 2005 | |||

| Total spending | 2,631.23 | 2,605.98 | 2,642.52 |

| (6,046.76) | (5,882.78) | (6,118.72) | |

| Medical spending | 1,952.45 | 1,910.78 | 1,971.10 |

| (5,396.24) | (5,214.17) | (5,475.68) | |

| Pharmacy spending | 678.79 | 695.22 | 671.44 |

| (1,826.41) | (1,781.64) | (1,846.05) | |

| 2006 | |||

| Total spending | 3,041.93 | 2,895.33 | 3,107.52 |

| (7,056.37) | (6,902.11) | (7,123.38) | |

| Medical spending | 2,298.24 | 2,173.21 | 2,354.17 |

| (6,321.96) | (6,136.22) | (6,402.58) | |

| Pharmacy spending | 743.72 | 722.15 | 753.36 |

| (1,982.46) | (1,942.28) | (2,000.12) | |

| 2007 | |||

| Total spending | 3,172.24 | 3,074.59 | 3,215.93 |

| (8,594.69) | (8,379.80) | (8,688.83) | |

| Medical spending | 2,421.05 | 2,330.69 | 2,461.48 |

| (7,846.83) | (7,559.87) | (7,971.60) | |

| Pharmacy spending | 751.23 | 743.93 | 754.50 |

| (2,110.87) | (2,032.27) | (2,145.11) | |

Notes. Total health care payment includes medical (inpatient and outpatient) and prescription drug payments by the member (employee/employer) and the plan. Standard deviations in parentheses.

DD Results

Table 4 displays regression results for the DD models presented in equation (1) above for total spending, medical spending, and pharmacy spending. Estimates show the log-link coefficient estimates from the GLM regressions. For total spending we observe that HSA enrollment is associated with annual spending levels that are 4.6 percent lower over the postperiod compared with those staying in traditional plans. When we break out medical (inpatient/outpatient) spending from pharmaceutical spending, we observe a negative effect of HSA enrollment on medical spending, though the estimate is not statistically significant at conventional levels. For pharmacy spending we observe that HSA enrollment is associated with annual spending levels that are 6.3 percent lower than traditional plan enrollees.

Table 4.

Difference-in-Differences Generalized Linear Model (GLM) Estimates of Health Care Spending between HSA and Traditional Plan Enrollees

| Variables | Total Spending | Medical Spending | Pharmacy Spending |

|---|---|---|---|

| HSA×Post | −0.0459* | −0.0384 | −0.0626*** |

| (0.0277) | (0.0370) | (0.0199) | |

| Post | 0.0956*** | 0.0930*** | 0.105*** |

| (0.0253) | (0.0339) | (0.0151) | |

| HSA | −0.0676 | −0.0398 | −0.147*** |

| (0.0483) | (0.539) | (0.0481) | |

| Year | 0.0685*** | 0.0873*** | 0.0100 |

| (0.0130) | (0.0171) | (0.00988) | |

| Region (Midwest reference) | |||

| Northeast | −0.0192 | −0.0118 | −0.0359 |

| (0.0475) | (0.0600) | (0.0386) | |

| South | −0.0411 | −0.0691* | 0.0407 |

| (0.0305) | (0.0384) | (0.0311) | |

| Unknown | −1.234*** | −1.263*** | −1.147*** |

| (0.0548) | (0.132) | (0.342) | |

| West | −0.0541 | −0.0378 | −0.111** |

| (0.0533) | (0.0634) | (0.0513) | |

| Female | 0.761*** | 0.901*** | 0.246*** |

| (0.0539) | (0.0601) | (0.0921) | |

| Age | 0.0379*** | 0.0378*** | 0.0384*** |

| (0.00138) | (0.00168) | (0.00161) | |

| Female × Age | −0.0103*** | −0.0127*** | −0.00112 |

| (0.00127) | (0.00143) | (0.00182) | |

| Firm size (100s) | 0.000220 | 0.000197 | 0.000661 |

| (0.00142) | (0.00167) | (0.00181) | |

| Type (Full replace reference) | |||

| Add-on (fully insured) | −0.111** | −0.0746 | −0.210*** |

| (0.0461) | (0.0465) | (0.0616) | |

| Add-on (ASO) | −0.0115 | 0.0517 | −0.191** |

| (0.0610) | (0.0620) | (0.0829) | |

Notes. N=228,930. Log-link used in GLM specification. Regressions also controls for 2005 plan type dummies (EPO, HMO, indemnity, POS, PPO) and 1-digit SIC dummies. Robust standard errors (clustered at firm level) in parentheses.

p<.01

p<.05

p<.1.

ASO, administrative services only; HSA, health savings account; HMO, health maintenance organization; POS, point of service; PPO, preferred provider organization.

Several other coefficient estimates are worthy of note. The coefficient on HSA is always negative (though only statistically significant for pharmacy spending), indicating that HSA enrollees are lower spending individuals on average. Likewise, full-replacement enrollees are generally higher spending than the two types of add-on (option) firms. Firm size has no significant effect on spending.

Table 5 displays key coefficients from GLM regressions examining the effect of separating the postperiod dummy into 2006 and 2007 to allow for a differential effect of HSA enrollment in each of the two postyears. In all cases effect sizes are not statistically different between the two follow-up years, though the general pattern of coefficient estimates suggests larger effects in 2006 than 2007.

Table 5.

Difference-in-Differences Generalized Linear Model (GLM) Estimates of Health Care Spending between HSA and Traditional Plan Enrollees, with Differential Postperiod Years

| Variables | Total Spending | Medical Spending | Pharmacy Spending |

|---|---|---|---|

| HSA×Year 2006 | −0.0570* | −0.0460 | −0.0843*** |

| (0.0302) | (0.0386) | (0.0204) | |

| HSA×Year 2007 | −0.0362 | −0.0320 | −0.0415* |

| (0.0313) | (0.0425) | (0.0234) | |

| HSA | −0.0677 | −0.0398 | −0.148*** |

| (0.0483) | (0.0539) | (0.0481) | |

| Year 2006 | 0.167*** | 0.182*** | 0.122*** |

| (0.0186) | (0.0253) | (0.0112) | |

| Year 2007 | 0.230*** | 0.266*** | 0.119*** |

| (0.0203) | (0.0271) | (0.0174) |

Notes. N=228,930. Log-link used in GLM specification. Regressions also control for region dummies, gender, age, gender × age interaction, firm size, setting (full replacement [fully insured only], fully insured add-on, ASO add-on), 2005 plan type dummies (EPO, HMO, indemnity, POS, PPO), and 1-digit SIC dummies. Robust standard errors (clustered at firm-level) in parentheses.

p<.01

**p<.05

p<.1.

ASO, administrative services only; HSA, health savings account; HMO, health maintenance organization; POS, point of service; PPO, preferred provider organization.

Sensitivity Analyses

Table 6 displays summary results from a number of alternative specifications to test the robustness of the results estimated above. Panel A presents DDD models that identify the difference in HSA enrollment spending effects between full-replacement enrollees and enrollees opting into HSA in option settings. The three-way interaction term (HSA × Post × Full Replace) is in no case statistically significant, though it is relatively large in magnitude, making it difficult to rule out economically meaningful differences in the effect of HSA enrollment on spending categories between those being switched involuntarily to HSAs and those opting to switch into an HSA.

Table 6.

Specification Tests

| Variables | Total Spending | Medical Spending | Pharmacy Spending |

|---|---|---|---|

| Panel A: Triple-difference two-part models testing for differences in HSA effect between full-replacement enrollees and add-on enrollees | |||

| HSA×Post×Full Replace | −0.0485 | −0.0430 | −0.0444 |

| (0.0417) | (0.0556) | (0.0280) | |

| HSA×Post | −0.0148 | −0.0119 | −0.0312 |

| (0.0357) | (0.0478) | (0.0275) | |

| Post | 0.0957*** | 0.0930*** | 0.105*** |

| (0.0253) | (0.0339) | (0.0151) | |

| HSA | −0.0904* | −0.0595 | −0.169*** |

| (0.0538) | (0.0620) | (0.0473) | |

| Panel B: Intent-to-Treat analysis | |||

| Post×Full Replace | −0.0611* | −0.0530 | −0.0721*** |

| (0.0321) | (0.0432) | (0.0198) | |

| Implied TOT | −0.0731 | −0.0634 | −0.0862 |

| Post | 0.0927*** | 0.0907*** | 0.1004*** |

| (0.0241) | (0.0324) | (0.0147) | |

| Full Replace (versus FI option) | 0.0856** | 0.0671 | 0.1232** |

| (0.0402) | (0.0466) | (0.0492) | |

| Panel C: Difference-in-Differences two-part model estimates of health care spending between HSA and traditional plan enrollees, for enrollees with chronic conditions in 2005 (n=116,028) | |||

| HSA×Post | −0.0393 | −0.0317 | −0.0574*** |

| (0.0272) | (0.0370) | (0.0205) | |

| Post | 0.0417 | 0.0181 | 0.102*** |

| (0.0280) | (0.0389) | (0.0147) | |

| HSA | −0.0284 | −0.00740 | −0.0788 |

| (0.0555) | (0.0633) | (0.0485) | |

| Panel D: Difference-in-Differences two-part model estimates of health care spending between HSA and traditional plan enrollees, for enrollees without chronic conditions in 2005 (n=112,902) | |||

| HSA×Post | −0.0817 | −0.0758 | −0.104*** |

| (0.0510) | (0.0592) | (0.0350) | |

| Post | 0.415*** | 0.456*** | 0.152*** |

| (0.0437) | (0.0502) | (0.0368) | |

| HSA | 0.0334 | 0.0574 | −0.147*** |

| (0.0449) | (0.0494) | (0.0521) | |

Notes. N=228,930 except where indicated. Implied treatment-on-the-treated (TOT) estimates represent scale Post×Full Replace coefficient where the scaling factor equal 1−HSA take-up in the option group (16.4%). GLM regressions with log-link also controls for region dummies, gender, age, gender × age interaction, firm size, setting (full replacement [fully insured only], fully insured add-on, ASO add-on), 2005 plan type dummies (EPO, HMO, indemnity, POS, PPO), and 1-digit SIC dummies. Robust standard errors (clustered at firm level) in parentheses.

p<.01

p<.05

p<.1.

ASO, administrative services only; GLM, generalized linear model; HMO, health maintenance organization; HSA, health savings account; POS, point of service; PPO, preferred provider organization.

In panel B we estimate the intent-to-treat model wherein we do not explicitly control for HSA enrollment. As noted above, we compare the “fully treated” group (full replacement) to the “partial dose” group (the option groups). After scaling the coefficient estimates from the regressions by 1−the HSA take-up rate in the option groups (16.4 percent) to generate the treatment-on-the-treated estimate, we observe strikingly similar estimates from the traditional approach that is potentially afflicted by individual-level selection bias and the intent-to-treat approach. The results point to roughly 7 percent reductions in total health care expenditures associated with enrollment in an HSA.

Panels C and D show results that stratify by the presence of a chronic condition in 2005. The sample size for each stratified group is roughly half the full sample. Effect sizes for those with chronic conditions are generally half those observed for individuals without chronic conditions. The Post variable estimates are much larger for those without chronic conditions, which suggests greater stability of health care utilization for persons with chronic illness.

A final set of robustness checks (not displayed) involved examining how sensitive our DD estimates are to the inclusion/exclusion of important observables. We estimated separate regressions that include the baseline (2005) retrospective risk and the chronic disease variables seen in Table 2. Both variables are highly significant predictors of any use and spending conditional on any use, but the coefficients associated with the HSA enrollment effects remained nearly unchanged (full results available upon request). It could be argued that the retrospective risk and chronic disease measures are important omitted variables and that they belong in the model (their t-statistics range from 50 to 100). We choose not to include them in our main specifications because the measures are constructed using the same claims data that are used to calculate spending, the dependent variable; hence, we are concerned about potential endogeneity biases associated with these measures.

DISCUSSION

We used data from a large national health insurance company on enrollees who beginning in 2006 are presented by their employers with either a full-replacement HSA benefit or the option of an HSA alongside traditional plan designs. The data contain enrollees in 709 employers ranging in size from 2 to 5,000, and enrollees are tracked for 3 years of continuous enrollment in order to establish the effect of switching plans beyond the first year of enrollment and still have access to pre-HSA enrollment data (2005).

Using a variety of robustness checks and alternative methodologies, our results point to three key findings. First we find that HSAs are associated with a statistically significant and economically meaningful relative decrease in spending when compared with individuals who remained in traditional plans. Overall, enrollees in HSAs spent roughly 5–7 percent less when compared with traditional health plan enrollees. There is evidence that more of the relative reduction in spending occurred in the first year of enrollment. Such a pattern could be consistent with a “benefit rush” in the year before HSA enrollment, but we do not observe that switchers spent significantly more than stayers in the year before the HSAs being offered. The relative reduction in the first year of enrollment could also be consistent with enrollees learning about their benefit design in the first year and therefore holding back on spending; alternatively, enrollees may use the first year to accumulate a substantial balance in their spending accounts in order to afford more costly procedures in subsequent years.

Second, the pattern of our results suggests that HSAs had larger relative effects on pharmacy spending than outpatient and inpatient spending. For pharmacy spending, HSA enrollees spent 6–9 percent less than traditional plan enrollees. Our findings are consistent with the notion that CDHP benefit designs affect decisions that are at the discretion of the consumer, such as whether to fill or refill a prescription, but have less effect on care decisions that are (more) at the discretion of the provider. This finding is broadly consistent with the results of the RAND Health Insurance Experiment (Newhouse 1994). In estimates that stratified by the presence of a chronic condition in the pre-HSA period, we found that HSA effects were twice as large in magnitude for those without chronic conditions. This suggests at a minimum that HSAs did not result in large, indiscriminate decreases in health care spending for those who may need it more.

Third, while there is some evidence consistent with the potential presence of favorable selection into HSAs based on the levels of spending, we provide compelling evidence to suggest that there is not selection on changes (or trends) in spending. The distinction is critical because we have longitudinal data spanning 1 year before the HSA being offered to 2 years post-HSA introduction. We believe the combination of estimates provided here represents the strongest evidence presented to date regarding the importance (or lack thereof) of selection when controlling for baseline spending. Therefore, we are comfortable concluding that our estimates represent the most convincing estimates of the effects of HSAs on health care spending. Our results diverge from earlier findings from Feldman et al. (2007) who did not find spending reductions associated with CDHP. This divergence could highlight the importance of looking at a broad array of different employers rather than a single large employer as in the previous studies.

There remain a number of noteworthy limitations of our work. First, we do not have the data to study drop out of employees from the offered benefits: all the individuals in our data are present for all 3 years of the analysis period. Hence, there may be a bias toward a healthier group of workers because of the requirement that they stay with the same firm for 3 consecutive years. Second, it remains a possibility that selection bias is present based on changes over time—our longitudinal methods cannot control for this type of selection, if it is present. In an effort to at least partly deal with this concern, in a sensitivity analysis we conducted nearest neighbor propensity score match to better balance the observable characteristics of HSA enrollees and nonenrollees in the preperiod. The point estimates for overall spending are robust to propensity score matching (details of our analysis are available by request of the authors), but the precision of our estimates worsened; point estimates suggested that propensity score matching revealed a larger estimated effect of HSA enrollment on medical spending and smaller effect on pharmacy spending, but we could not reject that the estimates differed from our nonmatched findings. Third, we do not have information on some important aspects of the benefit design, most notably the spending account and the amount contributed by the employer. Work by Lo Sasso, Helmehen, and Kaestner (2010) has shown that health care spending can be quite sensitive to employer contributions to the account. It should be noted that the fact that our study takes place within a naturalistic context using a control group comprised of non-CDHP benefit designs will tend to bias us toward finding smaller effects than are actually present if CDHP designs were compared against a static control benefit design. This is because the comparison group plan designs are getting less generous over time, the effect of which is to attenuate the estimated CDHP effect; this change was evident in Figures 1 and 2 as deductible levels and OOP maximums were increasing for stayers in non-CDHP designs. Fourth, there is the possibility of employer-level selection in the decision to offer HSAs (particularly on a full-replacement basis) in the first place. Indeed the question of what prompts an employer to consider a CDHP remains largely unknown. It is possible, for example, that prior health spending trends may motivate the decision to consider alternative benefit designs. The present study design is unable to control for such factors. Lastly, it is worth noting that our work does not claim to look at the health effects of HSA enrollment or at what type of care is reduced when individuals are enrolled in HSAs, though such outcomes represent fruitful future areas of research.

Acknowledgments

Joint Acknowledgment/Disclosure Statement: The authors would like to gratefully acknowledge comments received at the 2009 AcademyHealth Annual Research Meeting. The findings and conclusions in this document are those of the authors, who are responsible for its content, and do not necessarily represent the views of any third parties.

Disclosures: None.

Disclaimers: None.

NOTE

It might be tempting given the nonlinear models to use Ai and Norton's (2003) correction for interaction effects in nonlinear models. However, it should be noted that Puhani (2008) has observed that Ai and Norton's work on interaction effects in nonlinear models does not apply to difference-in-differences estimates of the type we are estimating.

SUPPORTING INFORMATION

Additional supporting information may be found in the online version of this article:

Appendix SA1: Author Matrix.

Please note: Wiley-Blackwell is not responsible for the content or functionality of any supporting materials supplied by the authors. Any queries (other than missing material) should be directed to the corresponding author for the article.

REFERENCES

- Ai D, Norton EC. Interaction Terms in Logit and Probit Models. Economics Letters. 2003;80:123–9. [Google Scholar]

- Alderman L. 2009. Advice to the Jobless on Getting Health Coverage. New York Times, 28, B6.

- Buchmueller TC, Feldstein PJ. Consumers' Sensitivity to Health Plan Premiums: Evidence from a National Experiment in California. Health Affairs. 1996;15(1):143–51. doi: 10.1377/hlthaff.15.1.143. [DOI] [PubMed] [Google Scholar]

- Buchmueller TC. The Effect of Price on Switching Among Health Plans. Journal of Health Economics. 1997;16(2):231–47. doi: 10.1016/s0167-6296(96)00531-0. [DOI] [PubMed] [Google Scholar]

- Buntin MB, Damberg C, Haviland A, Kapur K, Lurie N, McDevitt R, Marquis MS. Consumer-Directed Health Care: Early Evidence about Effects on Cost and Quality. Health Affairs. 2006;25(6):w516–30. doi: 10.1377/hlthaff.25.w516. [DOI] [PubMed] [Google Scholar]

- Claxton G, Gabel J, DiJulio B, Pickreign J, Whitmore H, Finder B, Jarlenski M, Hawkins S. Health Benefits in 2008: Premium Moderately Higher, While Enrollment in Consumer-Directed Plans Rises in Small Firms. Health Affairs. 2008 doi: 10.1377/hlthaff.27.6.w492. 27 (6): w492–w502. Available at http://content.healthaffairs.org/cgi/content/abstract/hlthaff.27.6.w492. [DOI] [PubMed] [Google Scholar]

- Cutler D, Reber S. Paying for Health Insurance: The Trade-Off between Competition and Adverse Selection. Quarterly Journal of Economics. 1998;113(2):433–66. [Google Scholar]

- Feldman R, Parente ST, Christianson JB. Consumer-Directed Health Plans: New Evidence on Spending and Utilization. Inquiry. 2007;44:26–40. doi: 10.5034/inquiryjrnl_44.1.26. [DOI] [PubMed] [Google Scholar]

- Fowles JB, Kind EA, Braun BL, Bertko J. Early Experience with Employee Choice of Consumer-Directed Health Plans and Satisfaction with Enrollment. Health Services Research. 2004;39(4, part 2):1141–58. doi: 10.1111/j.1475-6773.2004.00279.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Greene J, Hibbard J, Murray JF, Teutsch SM, Berger ML. The Impact of Consumer Directed Health Plans on Prescription Drug Use. Health Affairs. 2008a;27(4):1111–9. doi: 10.1377/hlthaff.27.4.1111. [DOI] [PubMed] [Google Scholar]

- Greene J, Peters E, Mertz CK, Hibbard JB. Comprehension and Choice of a Consumer Directed Health Plan: An Experimental Study. American Journal of Managed Care. 2008b;14(6):369–76. [PubMed] [Google Scholar]

- Lo Sasso AT, Helmehen LA, Kaestner R. The Effects of Consumer-Directed Health Plans on Health Care Spending. The Journal of Risk and Insurance. 2010;77(1):85–103. [Google Scholar]

- Manning WG. The Logged Dependent Variable, Heteroscedasticity, and the Retransformation Problem. Journal of Health Economics. 1998;17:283–95. doi: 10.1016/s0167-6296(98)00025-3. [DOI] [PubMed] [Google Scholar]

- Manning WG, Mullahy J. Estimating Log Models: To Transform or Not to Transform? Journal of Health Economics. 2001;20(4):461–94. doi: 10.1016/s0167-6296(01)00086-8. [DOI] [PubMed] [Google Scholar]

- Mullahy J. Much Ado about Two: Reconsidering Retransformation and Two-Part Model in Health Econometrics. Journal of Health Economics. 1998;17:247–81. doi: 10.1016/s0167-6296(98)00030-7. [DOI] [PubMed] [Google Scholar]

- Newhouse JP The Insurance Experiment Group. Free for All? Lessons from the RAND Health Insurance Experiment. Cambridge, MA: Harvard University Press; 1994. [Google Scholar]

- Parente ST, Feldman R, Christianson JB. Evaluation of the Effect of a Consumer-Driven Health Plan on Medical Care Expenditures and Utilization. Health Services Research. 2004a;39(4, part 2):1189–210. doi: 10.1111/j.1475-6773.2004.00282.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Parente ST. Employee Choice of Consumer-Driven Health Insurance in a Multiplan, Multiproduct Setting. Health Services Research. 2004b;39(4, part 2):1091–112. doi: 10.1111/j.1475-6773.2004.00275.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Parente ST, Feldman R, Chen S. Effects of a Consumer Driven Health Plan on Pharmaceutical Spending and Utilization. Health Services Research. 2008;43(5):1542–56. doi: 10.1111/j.1475-6773.2008.00857.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Puhani PA. 2008. The Treatment Effect, the Cross Difference, and the Interaction Term in Nonlinear “Difference-in-Differences” Models. IZA Discussion Paper Series 3478, IZA.

- Tollen LA, Ross MN, Poor S. Risk Segmentation Related to the Offering of a Consumer-Directed Health Plan: A Case Study of Humana Inc. Health Services Research. 2004;39(4, part 2):1167–88. doi: 10.1111/j.1475-6773.2004.00281.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Wharam JF, Landon BE, Galbraith AA, Kleinman KP, Soumerai SB, Ross-Degnan D. Emergency Department Use and Subsequent Hospitalizations among Members of a High-Deductible Health Plan. Journal of American Medical Association. 2007;297(10):1093–102. doi: 10.1001/jama.297.10.1093. [DOI] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.