Abstract

Genes can affect behaviour towards risks through at least two distinct neurocomputational mechanisms: they may affect the value assigned to different risky options, or they may affect the way in which the brain adjudicates between options based on their value. We combined methods from neuroeconomics and behavioural genetics to investigate the impact that the genes encoding for monoamine oxidase-A (MAOA), the serotonin transporter (5-HTT) and the dopamine D4 receptor (DRD4) have on these two computations. Consistent with previous literature, we found that carriers of the MAOA-L polymorphism were more likely to take financial risks. Our computational choice model, rooted in established decision theory, showed that MAOA-L carriers exhibited such behaviour because they are able to make better financial decisions under risk, and not because they are more impulsive. In contrast, we found no behavioural or computational differences among the 5-HTT and DRD4 polymorphisms.

Keywords: neuroeconomics, behavioural genetics, monoamine oxidase-A, risk-taking, decision-making

1. Introduction

Recent research using twin-genetic studies has shown that some of the variation across people in their willingness to take risks can be attributed to heritability [1–3]. Additional work has begun to show associations between specific genes and financial risk-taking behaviour [4–7]. Although these studies have been very valuable in identifying particular genes that might be associated with risk-taking behaviour, they have not been able to identify the neurocomputational mechanisms that mediate the impact of genes on behaviour. This is an important shortcoming since a growing body of work in behavioural neuroscience and neuroeconomics has shown that there might be multiple mechanisms through which genes could affect risk-taking behaviour. In particular, genes may affect behaviour by changing the value assigned to different risky options (ROs) [8,9], or they may affect behaviour by changing the way in which the brain adjudicates between the options based on their values [10].

In this paper, we shed some light on how genes affect the psychological processes associated with risk-taking behaviour by combining tools from behavioural genetics, neuroeconomics and experimental economics. In particular, we use experimental choice data to estimate well-parameterized computational models of financial behaviour under risk that allow us to test for the impact the genes encoding for monoamine oxidase-A (MAOA), the serotonin transporter (5-HTT) and the dopamine D4 receptor (DRD4) has on the two computations described above. Employing a computational model allows us to isolate the underlying psychological mechanisms that contribute to choice heterogeneity across these genes. Consistent with previous results, we find that a specific polymorphism of the MAOA gene is associated with an increased propensity to take financial risk. Our computational modelling approach also allowed us to identify the specific mechanism responsible for this increased appetite for risk, which allows for an improved interpretation of previous behavioural genetic results.

We focus on these three genes because they have been the subject of various previous behavioural genetic studies, and because much of the behavioural neuroscience literature points to an important role of the serotonergic, dopaminergic and noradrenergic systems in decision-making [11–15].

MAOA is an enzyme that regulates the catabolism of monoamines, including serotonin, dopamine, norepinephrine and epinephrine. These monoamines function as neurotransmitters in the central nervous system. Expression of MAOA in the brain has been shown to be influenced by the variable number of tandem repeats (VNTRs) in the MAOA gene [16]. In particular, carriers of the 3.5 or 4 repeats (MAOA-H) allele exhibit higher expression of the enzyme, whereas carriers of the 2, 3 or 5 repeats (MAOA-L) allele are associated with lower enzymatic expression. The low-activity variant of the MAOA gene has been shown to contribute to aggressive and impulsive behaviour in mice and humans [17,18]. At the neuroanatomical level, MAOA-L carriers show lower activity in regulatory prefrontal areas and increased functional connectivity between vmPFC and amygdala regions [19,20]. In addition, genetic variation in the MAOA gene has also been linked to a susceptibility to psychiatric diseases, including pathological gambling [21].

The serotonin transporter (5-HTT) encodes a protein responsible for the reuptake of serotonin at the synaptic cleft. A short variant has been associated with lower transcriptional efficiency of the gene promoter and higher levels of anxiety, harm-avoidance and financial risk-aversion [5,22,23]. A long variant of the gene is associated with higher transcriptional efficiency and thus higher reuptake of serotonin into the presynaptic neuron. The serotonin transporter is also the target of many anti-depressant drugs that act to inhibit the reuptake of 5HT in order to prolong neuronal firing and serotonin transmission.

The DRD4 gene influences the function of dopamine D4 receptors, for which a particular repeat sequence leads to functional differences in ligand binding. This gene contains a 48 bp VNTR in exon III that contains 2–11 repeats; carriers of the 7-repeat allele have been shown to require higher levels of dopamine to produce a response of similar magnitude to those without the 7-repeat allele [24]. Behaviourally, carriers of the 7-repeat allele score higher on novelty-seeking personality tests and also exhibit higher rates of pathological gambling [25,26]. A recent study of an all-male population has also shown that carriers of the 7-repeat allele are willing to take more financial risk in an investment experiment [4], and a similar mixed-gender experiment confirms these results [5].

2. Results

Ninety male subjects were asked to make choices between 140 different pairs of monetary gambles. Each pair contained a certain option (CO) involving a payout of $c with 100 per cent probability, and an RO involving a gain $g and a loss $l with equal probability (see §4 for details). Subjects cared about their choices because at the end of the experiment, one trial was selected at random and the payouts associated with the selected option were implemented. We failed to obtain successful genotyping on six subjects, and one additional subject was excluded because ex-post debriefing showed that he did not understand the instructions. As a result, our effective sample size is n = 83.

(a). Basic behavioural results

We compared the frequency with which the RO was chosen by the different genetic groups (figure 1). MAOA-L carriers accepted the RO in 41 per cent of trials while MAOA-H carriers accepted 36 per cent of the ROs (n = 83, t = 1.70, p < 0.046, one-tailed). However, the DRD4 and 5-HTT polymorphisms were not associated with differences in the propensity to accept the RO. DRD4 7R+ carriers accepted 39 per cent of the ROs, while non-carriers accepted 38 per cent of the time (n = 83, t = 0.60, p = 0.27, one-tailed). Subjects that were homozygous for the short allele of the 5-HTT gene accepted 37 per cent of ROs, while carriers of the long variant had a 39 per cent acceptance rate (n = 83, t = −0.66, p = 0.26, one-tailed). We also examined a different categorization of the 5-HTT genotype and found that carriers of the short allele and those that were homozygous for the long allele both accepted the RO 38 per cent of the time (n = 83, p = 0.58, one-tailed). One-tailed test statistics were used for these basic behavioural tests because multiple previous studies have shown that these polymorphisms are associated with increased risk-taking.

Figure 1.

Choice of the risky option by the genetic group. MAOA-L carriers accepted the risky optional significantly more often than MAOA-H carriers: 41.2 versus 36.3% (p = 0.046). Differences in the acceptance rates for the 5-HTT and DRD4 polymorphisms were not significant. Forty-six per cent of the risky options in our design had a positive net expected value.

(b). Basic computational phenotype

In order to investigate the psychological mechanisms through which the MAOA gene affects the propensity to take financial risks, we estimated the parameters of a linear prospect theoretic model for each of the subjects based on their choices. The use of this model is justified by the fact that a growing body of behavioural and neuroimaging evidence suggests that most individuals make risky choices by first assigning a value to the different lotteries according to the rules of prospect theory (PT) [8,27–29], and then comparing those values to make a choice.

We assumed that subjects evaluated the gambles using a simple linear version of the PT in which the utility of taking the RO is given by

and the utility of taking the CO is given by

Here, g denotes the gain associated with the RO, l denotes the loss, p denotes the probability of the positive pay-off and λ > 0 is a parameter measuring the relative value that the individual assigns to gains and losses. Note that most PT models also assume that probabilities are weighted non-linearly [27,29]. However, since our study only considers 50 : 50 gambles, and previous studies have found that the probability distortion at p = 0.5 is small [30], we ignore this aspect of the theory.

We assume that the choices are a stochastic function of values that is described by the softmax function:

where a is the inverse-temperature parameter that controls the quality of the decision-making process: when a = 0 subjects, choose both options with equal probability regardless of their associated underlying values; as a increases, the probability of choosing the option associated with the largest value increases.

The model has two free parameters for each subject, λ and a, which we estimated using maximum likelihood (see §4 for details). For technical reasons described in electronic supplementary material, Methods, we were able to successfully estimate all of the parameters for the two computational models discussed in the paper for 64 of the 83 subjects. For this reason, all of the computational results here and below are limited to this smaller sample. The estimate of λ was 1.52 ± 0.11 (mean ± s.e.). The estimate of a was 3.06 ± 0.60; see electronic supplementary material, table S2, for a full list of the individual estimates. Forty-one subjects were significantly loss averse (λ > 1), 21 subjects were loss neutral and two subjects were significantly loss seeking (λ < 1). The average level of λ is similar to that found in other behavioural studies of loss aversion [30,31].

Note the relationship between the parameters of the model and the psychological processes that affect choice. The coefficient of loss aversion λ measures the relative value placed on potential gains and losses. When λ is low, subjects engage in risk-taking behaviour by overvaluing gains relative to losses. The opposite is true for high λ. As a result, this coefficient is a good indicator of the impact that the valuation process has on risk-taking. In contrast, the coefficient a measures the facility with which subjects are able to choose the option with the highest value. Thus, a is a good measure of the performance of the comparison or choice processes.

(c). Genetic effects on the valuation process

We first investigated the extent to which the impact of the genetic polymorphisms on risk-taking behaviour can be explained by changes in the valuation process. We did this by first regressing the individually estimated loss-aversion parameters on each gene polymorphism, including controls for ethnicity and school attended. We found no significant results for MAOA (n = 64, t = −1.33, p = 0.19, two-tailed), DRD4 (n = 64, t = −0.09, p = 0.93, two-tailed) or 5-HTT (n = 64, t = 0.22, p = 0.82, two-tailed). We then ran a multivariate specification by including all three gene polymorphisms in the same model (which also included the ethnicity and schooling controls) and found no significant effects for MAOA (t = −1.33, p = 0.19, two-tailed), DRD4 (t = −0.03, p = 0.98, two-tailed) or 5-HTT (t = 0.31, p = 0.76, two-tailed). Finally, because the multiplicative nature of the loss-aversion parameter may bias the estimate of the mean, as a robustness check we also ran a version of the multivariate specification using log(λ) as the independent variable. Again, we found no significant effects for MAOA (t = −0.92, p = 0.36, two-tailed), DRD4 (t = −0.06, p = 0.95, two-tailed) or 5-HTT (t = 0.43, p = 0.67, two-tailed).

(d). Genetic effects on the choice process

We then investigated the extent to which the impact of the genetic polymorphisms on risk-taking behaviour can be explained by changes in the comparison process. We did this by regressing the individual fit of the inverse-temperature parameters on each gene polymorphism controlling for ethnicity and school population. We found no significant effects for MAOA (n = 64, t = −0.47, p = 0.64, two-tailed), DRD4 (n = 64, t = 0.66, p = 0.51, two-tailed) or 5-HTT (n = 64, t = −0.84, p = 0.40, two-tailed). The multivariate specification including all three polymorphisms and controls also failed to find significant effects for MAOA (t = −0.40, p = 0.69, two-tailed), DRD4 (t = 0.44, p = 0.66, two-tailed) and 5-HTT (t = −0.64, p = 0.53, two-tailed).

(e). Advanced computational phenotype

Since our basic behavioural results show a statistically significant difference in risk-taking behaviour for MAOA that could not be explained by the simple computational model described above, we decided to complicate the model slightly by allowing for the inverse-temperature parameter to differ for choices in which the gamble had positive net expected utility and those that had negative net expected utility. In particular, we used the same equations to model the valuation of the RO and CO, but we allowed for an asymmetric stochastic choice function:

|

and

|

The selection of this specification was motivated by the fact that, under the estimates of the basic model, on average, subjects rejected a higher percentage (93.3%) of gambles among those with negative expected utility than they accepted (85.4%) with positive expected utility (n = 64, t = −4.43, p < 0.001, two-tailed). This suggested that subjects might be using a different comparison process when making choices between these two types of risks.

As before, we estimated the individual model parameters using maximum likelihood (see electronic supplementary material, table S3 and figure S3 for a description of the individual fits). The estimate of λ was 1.49 ± 0.10. The median estimates of a+ and a− were 1.97 and 2.25, respectively (see the electronic supplementary material for discussion on technical issues related to the estimation of these two inverse-temperature parameters and a justification for the use of the median statistic to describe the population.) The Bayesian information criterion value for the unconstrained and constrained (a− = a+) models were 5022 and 5058, respectively, indicating a better fit when allowing for asymmetric temperature parameters.

(f). Genetic effects on the comparator process of advantageous and disadvantageous risks

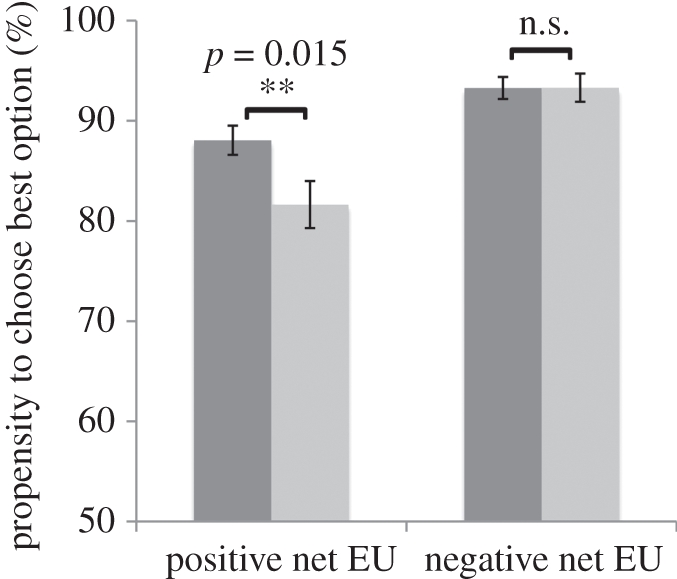

Figure 2 displays logistic fits to the average group choices for each MAOA group, allowing for different slopes in the positive and negative EU domains. The net utility for each gamble was computed using the model fits from the advanced computational model. Note that the logit curve summarizes the performance of the comparator process by relating the net utility of the RO to the probability that it is chosen as steeper slopes of the logistic curve corresponding to higher rates of optimal decision-making. The figure shows that there were no differences when the RO had a lower value than the CO, but that there was a systematic difference when this was not the case: MAOA-L carriers chose the optimal action more often than MAOA-H carriers when faced with advantageous risk. A formal statistical test confirmed the difference between the two groups (figure 3): MAOA-L carriers accepted the RO 6.4 per cent more often than MAOA-H carriers (n = 64, t = 2.49 p = 0.015, two-tailed) when the RO had a positive net expected utility, but there was no significant difference in acceptance rates over the negative EU domain (n = 64, t = 0.51, p = 0.62, two-tailed), in both cases controlling for ethnicity. Because the latter conclusion was justified by rejection of the null, we subsequently ran a more conservative statistical test by estimating the interaction effect between the MAOA genotype and a dummy for positive EU gambles; we found a positive coefficient on the interaction term, consistent with our previous test, although the result was slightly weaker (n = 64, t = 1.95, p = 0.056, two-tailed). Note that our statistical test was constructed by integrating under each of the choice curves in the positive and negative EU domains, and thus acts as a non-parametric test of group differences between the a+ and a− parameters. Similar analyses for DRD4 and 5-HTT did not reveal any significant differences in choice behaviour.

Figure 2.

Propensity to choose the RO as a function of its net expected utility (using individually fitted PT parameters). The single solid black curve in the negative net EU domain indicates there was no difference in acceptance rates across the MAOA polymorphism when the net EU was negative. However, the two dashed curves in the positive net EU domain show there was a systematic difference in the propensity to accept the RO: MAOA-L carriers (black) accepted the risky offer significantly more often than MAOA-H carriers (grey). Net EU is partitioned into bins of length 0.5 and the average group acceptance rate within each bin is displayed for MAOA-L and MAOA-H.

Figure 3.

Propensity to choose the option with the highest expected utility as a function of the MAOA polymorphism. Dark grey bars, MAOA-L; light grey bars, MAOA-H.

3. Discussion

The computational approach used in the paper allowed us to conclude that MAOA-L carriers are more likely to take a financial risk than their MAOA-H counterparts, but only when it is advantageous to do so given their preferences over risk. For disadvantageous gambles, there was no difference between the two groups. This suggests that MAOA-L carriers perform better in the case of risky financial decision-making because they exhibit an improved ability to select the optimal response when it is advantageous. Contrary to previous findings in the literature [4,5], we found no significant differences in either gambling tendencies or the computations associated with valuation or choice for the 5-HTT and DRD4 genes.

Our results for MAOA are consistent with previous related behavioural genetic studies, although our computational approach provides novel insights about the mechanism through which this gene influences risky financial choice. Previous studies have found that MAOA-L carriers are more likely to exhibit aggressive and risky behaviour [6,18,19,21]. Contrary to previous discussion in the literature [6,19,21], our results show that these behavioural patterns are not necessarily counterproductive [19,21], since in the case of financial choice these subjects engage in more risky behaviour only when it is advantageous to do so. This provides a cautionary tale on the interpretation of previous behavioural results related to MAOA, and on the common practice in the literature of relating genes to behaviour without specifying and estimating a computational phenotype.

The fact that the MAOA gene influences the catabolism of monoamines (such as serotonin, dopamine, norepinephrine and epinephrine) also allows us to connect our findings with various other strands of the literature. Previous neuroscience studies have shown that humans with higher levels of norepinephrine typically choose the action carrying the highest immediate reward [11,15]. Our results are consistent with this claim as monoamine oxidase is responsible for the catabolism of norepinephrine, and low activity carriers of MAOA will tend to have lower enzymatic activity and thus increased levels of norepinephrine. A recent study that examined the cognitive effects of norepinephrine in mice found that pharmacologically manipulating norepinephrine levels downward resulted in decreased ‘immediate performance accuracy’ [32], which is also consistent with our finding that MAOA affects the temperature parameters that control the accuracy of choices.

Monoamine oxidase also plays a role in breaking down dopamine. Therefore, dopaminergic transmission might also play a role in the computational phenotype identified here. Consistent with our findings, a recent study in which in vitro dopaminergic levels were experimentally manipulated through L-DOPA and the impact on optimal choice behaviour was measured [33] found that increased dopamine levels lead to more optimal choices in a simple learning task.

The fact that we failed to find behavioural or computational differences between the 5-HTT and DRD4 genotypes is also consistent with the previous literature. Some recent studies have found significant effects of both of these genes on financial risk-taking behaviour [4,5], but other studies have failed to replicate these results. For example, a recent fMRI study found a significant effect of 5-HTT on the framing-induced choice biases, but it failed to find a link between the 5-HTT polymorphism and financial risk-taking [34]. Another study also failed to find any 5-HTT associations between risk attitudes over the gain and loss domains [35]. The DRD4 gene has also been implicated in impulsive behaviour and novelty-seeking in a variety of studies [25,26], but these results have also not been consistently replicated [36,37]. In particular, a larger meta-analysis does not find a significant association between the DRD4 polymorphism and impulsive or risky behaviour [38]. One potential reason for our failure to identify a significant effect of 5-HTT on financial risk-taking is limited statistical power for this gene: the distribution of the key polymorphism was unbalanced in our subject population, with only 27 per cent homozygous for the short allele.

As with any behavioural genetic study, it is also important to pay close attention to the behavioural specificity of the phenotype we define. It is possible that the phenotypic difference we find for the MAOA-L polymorphism may arise from a more general cognitive effect, such as intelligence or numerical ability. We do not have a sufficient battery of controls that can definitively rule out these broader psychological mechanisms nor do we have controls for potential environmental variables (e.g. income) that could interact with the MAOA gene to produce the effect. However, one advantage of estimating a computational phenotype is that it allows us to precisely identify the parameter that is driving the heterogeneity in choice within the model. If this heterogeneity were driven by a more general cognitive or environmental variable, then this mechanism should also mediate choice behaviour in a manner consistent with our asymmetric result on optimal action selection.

Our results suggest several natural directions for further research. First, future studies should investigate the neurochemical basis of decision-making to understand the quantitative relationship between norepinephrine, dopamine, monoamine oxidase and optimal choice. Our results provide support for the hypothesis that higher levels of norepinephrine and dopamine correspond to a greater level of action selection optimality, but further research must be conducted to fully understand this relationship [11]. Second, our results indicate the need for future genetic studies to specify a computational phenotype that separates the valuation and choice processes, as subjects with similar preferences might still make very different choices.

4. Material and methods

(a). Subjects

Ninety male subjects, aged 19 to 27, participated in the study. Subjects were students at Caltech (59) or at a nearby community college. We restricted our population to males to avoid gender as a confounding factor and to avoid difficulties in the analysis of the MAOA gene (males carry only one allele while females carry two). Subjects' self-reported ethnicity was as follows: 53 Caucasian, 13 Latin/Hispanic, nine Indian, three African-American, three Asian and nine other. However, we failed to obtain successful genotyping on six subjects, and one additional subject was excluded because ex-post debriefing showed that he did not understand the instructions. As a result, our effective sample size is n = 83. The study was approved by Caltech's Human Subjects Committee.

(b). Behavioural task

Subjects received $25 for participating in the study. They were allowed to risk part of these funds during the following decision-making task. In each trial, they were shown a pair of gambles and had to choose one of them. One option involved certain non-negative pay-offs (e.g. gain $0 with probability 100%). We refer to it as the CO. The other option involved a 50 : 50 gamble between a gain and a loss (e.g. winning $7 and losing $4 with equal probability). We refer to it as the risky option (RO). Subjects made decisions in 140 different trials without feedback on a private computer. The order of the choices was randomized within subjects. Electronic supplementary material, table S1, lists the entire set of pay-offs used.

Both options were displayed simultaneously on the screen until the subject made a decision. Subjects made a decision using a 5-point scale: 1 = strongly reject the risk option, 2 = weakly reject the RO, 3 = indifferent between both options, 4 = accept the RO, 5 = strongly accept the RO. For the purpose of the computational analysis, the responses were collapsed into a binary response (with 5 and 4 coded as accept, 1 and 2 coded as reject, and 3's allocated randomly to the two conditions). To make sure that we did not lose information when collapsing the choice data into binary responses, we estimated an ordered logistic regression and found that 95% confidence intervals (CI) for the interior cutpoints (responses 2, 3 and 4) overlapped. This suggests that using the 5-point scale would not add significant information to the behavioural and genetic analyses performed in the paper. Subjects failed to enter a response in 4 per cent of the trials, which were excluded from further analyses. Subjects cared about the choices because one trial was selected at random at the end of the experiment and his choice for that trial was implemented. Average earnings were $28.

(c). Genotyping

Genetic data was collected from each subject using an Oragene DNA OG-500 saliva collection kit. Six subjects were unsuccessfully genotyped for one or more genes and were dropped from all genetic analyses.

5-HTTLPR was identified as follows. The forward primer was labelled with 6FAM-5′-GGC GTTGCC GCT CTG AAT GC-3′, the reverse primer was unlabelled 5′-GAG GGA CTGAGC TGG ACA ACC AC-3′, which yielded 484 bp (short) and 527 bp (long) fragments. Polymerase chain reaction (PCR) was performed in a total volume of 25 µl, containing 50 ng of DNA; 1 µl of each primer (10 µM stock); 1.5 µl of (25 mM) MgCl2; 2 per cent DMSO (v/v); 2.5 U Amplitaq Gold DNA polymerase (Applied Biosystems, Foster City, CA, USA); 2 µl of Deaza dNTP (2 mM each dATP, dCTP, dTTP, 1 mM dGTP, 1 mM deaza-dGTP). Cycling conditions consisted of (i) an initial 12 min denaturation at 94°C, (ii) eight cycles with denaturation for 30 s at 94°C, varied annealing temperatures consisting of 30 s at 66°C (two cycles), then 65°C (three cycles), then 64°C (three cycles), followed by hybridization for 1 min at 72°C, (iii) 35 cycles with an annealing temperature of 63°C and the same denaturation and hybridization parameters, and (iv) a final extension for 20 min at 72°C.

MAOA was identified as follows. The forward primer was labelled with VIC-5′-ACAGCCTGACCGTGGAGAAG-3′, the reverse primer was unlabelled 5′-GAACGGACGCTCCATTCGGA-3′. PCR was performed in a total volume of 10 µl, containing 25 ng of DNA, 0.5 µl of each primer (10 µM stock), 10× PCR buffer 0.8 µl, dNTP 0.8 µl, DMSO 0.8 µl, 25 mM MgCl2 0.8 µl and 0.064 µl of Amplitaq Gold (Applied Biosystems). Cycling conditions consisted of (i) an initial 12 min denaturation at 95°C and (ii) 35 cycles of 94°C for 30 s, 59°C for 30 s, 72°C for 2 min.

DRD4 was identified as follows. The forward primer was labelled with VIC-5′-AGG ACC CTC ATG GCC TTG-3′, the reverse primer was unlabelled 5′-GCG ACT ACG TGG TCT ACT CG-3′. PCR was performed in a total volume of 10 µl, containing 25 ng of DNA, 0.5 µl of each primer (10 µM stock), Takara LA Taq 0.1 µl, 5 µl 2× GC Buffer II and 1.6 µl dNTP. Cycling conditions consisted of (i) an initial 1 min denaturation at 95°C, (ii) 30 cycles of 94°C for 30 s, 62°C for 30 s, 72°C for 2 min, and (iii) 72°C for 5 min. In all cases, the PCR products were electrophoresed on an ABI 3730 DNA analyzer (Applied Biosystems) with an LIZ1200 size standard (Applied Biosystems), and data collection and analysis used Genemapper software (Applied Biosystems).

(d). Genotype equilibrium

Allele and genotype frequencies are given in electronic supplementary material, tables S4–S7. A Pearson χ2-test failed to reject the null hypothesis that the 5-HTT gene was in Hardy–Weinberg equilibrium (HWE) in our subject pool (χ2 = 0.98, d.f. = 1, p > 0.32). Since males possess only one allele of the MAOA gene, HWE is trivially satisfied. Finally, because of its multiple allele structure [39], we used a Markov Chain Monte Carlo method to test the null hypothesis that DRD4 was in HWE. The test failed to reject the null hypothesis (p = 0.689).

(e). Computational phenotype

The parameters for the two computational models described in §2 were estimated by optimizing the nonlinear likelihood function using the Nelder–Mead simplex method [40], as implemented in Matlab (2008b). We computed standard errors for the estimated parameters using parametric bootstrapping with a re-sampling size of 500. For each subject, we estimated individual parameters from the choice data and then used the estimates to generate a set of 500 pseudosamples of choice data. We then used the same MLE procedure described above to estimate the parameters in each of the pseudosamples. The standard error of the parameter estimate was then estimated by the standard deviation of this set of samples.

We assessed the model fit of the unconstrained computational model by computing the per cent of choices correctly predicted for each subject at individually fitted parameter values, which was 88.8 per cent on average.

For technical reasons explained in the electronic supplementary material, we failed to estimate one or more model parameters for 19 out of 83 subjects. The computational results described in the paper only apply to the 64 subjects for which all parameters were estimated successfully.

A potentially important simplification used in the computational models is the linearity of the value function. We tested the robustness of this assumption by estimating a nonlinear version of the simple prospect theoretic model given by the following three equations:

| 4.1 |

| 4.2 |

and

| 4.3 |

This model contains an additional parameter that allows for the possibility that value might be a nonlinear function of the pay-offs. We estimated the model using the same MLE procedure described above. However, owing to insufficient concavity of the likelihood function, we failed to successfully estimate parameters for five additional subjects that we were able to estimate the model for under the constraint ρ = 1. Of the remaining subjects, average estimates of λ, ρ and a were 1.51, 1.03 and 2.95, respectively. We ran a likelihood ratio test for each individual under the null hypothesis that ρ = 1, and determined that we could reject a linear value function in 46 of 65 subjects at the 5 per cent significance level. Furthermore, a t-test on the distribution of the unconstrained estimates of ρ did not reject the null hypothesis that the average value of ρ in the population is 1 (p = 0.29). Because of the lack of heterogeneity in ρ, and because including this extra parameter did not significantly improve the model fit, we focused the analysis in the paper on the simple and advanced versions of the linear PT model.

Acknowledgements

Financial support from Betty and Gordon Moore Foundation (A.R., C.C.) is gratefully acknowledged.

References

- 1.Cesarini D., Johannesson M., Lichtenstein P., Sandewall Ö., Wallace B. 2010. Genetic variation in financial decision-making. J. Finance 65, 1725–1754 10.1111/j.1540-6261.2010.01592.x (doi:10.1111/j.1540-6261.2010.01592.x) [DOI] [Google Scholar]

- 2.Cesarini D., Dawes C. T., Johannesson M., Lichtenstein P., Wallace B. 2009. Genetic variation in preferences for giving and risk taking*. Q. J. Econ. 124, 809–842 10.1162/qjec.2009.124.2.809 (doi:10.1162/qjec.2009.124.2.809) [DOI] [Google Scholar]

- 3.Zhong S., Chew S. H., Set E., Zhang J., Xue H., Sham P. C., Ebstein R. P., Israel S. 2009. The heritability of attitude toward economic risk. Twin Res. Hum. Genet. 12, 103–107 10.1375/twin.12.1.103 (doi:10.1375/twin.12.1.103) [DOI] [PubMed] [Google Scholar]

- 4.Dreber A., Apicella C. L., Eisenberg D. T. A., Garcia J. R., Zamore R. S., Lum J. K., Campbell B. 2009. The 7R polymorphism in the dopamine receptor D4 gene (DRD4) is associated with financial risk taking in men. Evol. Hum. Behav. 30, 85–92 10.1016/j.evolhumbehav.2008.11.001 (doi:10.1016/j.evolhumbehav.2008.11.001) [DOI] [Google Scholar]

- 5.Kuhnen C. M., Chiao J. Y. 2009. Genetic determinants of financial risk taking. PLoS ONE 4, e4362. 10.1371/journal.pone.0004362 (doi:10.1371/journal.pone.0004362) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Zhong S., Israel S., Xue H., Ebstein R. P., Chew S. H. 2009. Monoamine oxidase A gene (MAOA) associated with attitude towards longshot risks. PLoS ONE 4, e8516. 10.1371/journal.pone.0008516 (doi:10.1371/journal.pone.0008516) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Roe B. E., Tilley M. R., Gu H. H., Beversdorf D. Q., Sadee W., Haab T. C., Papp A. C. 2009. Financial and psychological risk attitudes associated with two single nucleotide polymorphisms in the nicotine receptor (CHRNA4) gene. PLoS ONE 4, e6704. 10.1371/journal.pone.0006704 (doi:10.1371/journal.pone.0006704) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.Tom S. M., Fox C. R., Trepel C., Poldrack R. A. 2007. The neural basis of loss aversion in decision-making under risk. Science 315, 515–518 10.1126/science.1134239 (doi:10.1126/science.1134239) [DOI] [PubMed] [Google Scholar]

- 9.Tobler P. N., O'Doherty J. P., Dolan R. J., Schultz W. 2007. Reward value coding distinct from risk attitude-related uncertainty coding in human reward systems. J. Neurophysiol. 97, 1621–1632 10.1152/jn.00745.2006 (doi:10.1152/jn.00745.2006) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.Rangel A., Camerer C., Montague P. R. 2008. A framework for studying the neurobiology of value-based decision making. Nat. Rev. Neurosci. 9, 545–556 10.1038/nrn2357 (doi:10.1038/nrn2357) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 11.Doya K. 2002. Metalearning and neuromodulation. Neural Netw. 15, 495–506 10.1016/S0893-6080(02)00044-8 (doi:10.1016/S0893-6080(02)00044-8) [DOI] [PubMed] [Google Scholar]

- 12.Schultz W. 2007. Behavioral dopamine signals. Trends Neurosci. 30, 203–210 10.1016/j.tins.2007.03.007 (doi:10.1016/j.tins.2007.03.007) [DOI] [PubMed] [Google Scholar]

- 13.Daw N. D., Kakade S., Dayan P. 2002. Opponent interactions between serotonin and dopamine. Neural Netw. 15, 603–616 10.1016/S0893-6080(02)00052-7 (doi:10.1016/S0893-6080(02)00052-7) [DOI] [PubMed] [Google Scholar]

- 14.Aston-Jones G., Cohen J. D. 2005. An integrative theory of locus coeruleus-norepinephrine function: adaptive gain and optimal performance. Annu. Rev. Neurosci. 28, 403–450 10.1146/annurev.neuro.28.061604.135709 (doi:10.1146/annurev.neuro.28.061604.135709) [DOI] [PubMed] [Google Scholar]

- 15.Ishii S., Yoshida W., Yoshimoto J. 2002. Control of exploitation-exploration meta-parameter in reinforcement learning. Neural Netw. 15, 665–687 10.1016/S0893-6080(02)00056-4 (doi:10.1016/S0893-6080(02)00056-4) [DOI] [PubMed] [Google Scholar]

- 16.Sabol S. Z., Hu S., Hamer D. 1998. A functional polymorphism in the monoamine oxidase A gene promoter. Hum. Genet. 103, 273–279 10.1007/s004390050816 (doi:10.1007/s004390050816) [DOI] [PubMed] [Google Scholar]

- 17.Shih J. C., Chen K. 1999. MAO-A and -B gene knock-out mice exhibit distinctly different behavior. Neurobiology (Bp) 7, 235–246 [PubMed] [Google Scholar]

- 18.McDermott R., Tingley D., Cowden J., Frazzetto G., Johnson D. D. P. 2009. Monoamine oxidase A gene (MAOA) predicts behavioral aggression following provocation. Proc. Natl Acad. Sci. USA 106, 2118–2123 10.1073/pnas.0808376106 (doi:10.1073/pnas.0808376106) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 19.Meyer-Lindenberg A., et al. 2006. Neural mechanisms of genetic risk for impulsivity and violence in humans. Proc. Natl Acad. Sci. USA 103, 6269–6274 10.1073/pnas.0511311103 (doi:10.1073/pnas.0511311103) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.Buckholtz J. W., et al. 2008. Genetic variation in MAOA modulates ventromedial prefrontal circuitry mediating individual differences in human personality. Mol. Psychiatry 13, 313–324 10.1038/sj.mp.4002020 (doi:10.1038/sj.mp.4002020) [DOI] [PubMed] [Google Scholar]

- 21.Ibanez A., Perez de Castro I., Fernandez-Piqueras J., Blanco C., Saiz-Ruiz J. 2000. Pathological gambling and DNA polymorphic markers at MAO-A and MAO-B genes. Mol. Psychiatry 5, 105–109 10.1038/sj.mp.4000654 (doi:10.1038/sj.mp.4000654) [DOI] [PubMed] [Google Scholar]

- 22.Lesch K. P., et al. 1996. Association of anxiety-related traits with a polymorphism in the serotonin transporter gene regulatory region. Science 274, 1527–1531 10.1126/science.274.5292.1527 (doi:10.1126/science.274.5292.1527) [DOI] [PubMed] [Google Scholar]

- 23.Canli T., Lesch K. P. 2007. Long story short: the serotonin transporter in emotion regulation and social cognition. Nat. Neurosci. 10, 1103–1109 10.1038/nn1964 (doi:10.1038/nn1964) [DOI] [PubMed] [Google Scholar]

- 24.Asghari V., Sanyal S., Buchwaldt S., Paterson A., Jovanovic V., Van Tol H. H. M. 1995. Modulation of intracellular cyclic AMP levels by different human dopamine D4 receptor variants. J. Neurochem. 65, 1157–1165 10.1046/j.1471-4159.1995.65031157.x (doi:10.1046/j.1471-4159.1995.65031157.x) [DOI] [PubMed] [Google Scholar]

- 25.Ebstein R. P., et al. 1996. Dopamine D4 receptor (D4DR) exon III polymorphism associated with the human personality trait of novelty seeking. Nat. Genet. 12, 78–80 10.1038/ng0196-78 (doi:10.1038/ng0196-78) [DOI] [PubMed] [Google Scholar]

- 26.Perez de Castro I., et al. 1997. Genetic association study between pathological gambling and a functional DNA polymorphism at the D4 receptor gene. Pharmacogenetics 7, 345–348 [PubMed] [Google Scholar]

- 27.Kahneman D., Tversky A. 1979. Prospect theory: an analysis of decision under risk. Econometrica 47, 263–291 10.2307/1914185 (doi:10.2307/1914185) [DOI] [Google Scholar]

- 28.Hsu M., Krajbich I., Zhao C., Camerer C. F. 2009. Neural response to reward anticipation under risk is nonlinear in probabilities. J. Neurosci. 29, 2231–2237 10.1523/JNEUROSCI.5296-08.2009 (doi:10.1523/JNEUROSCI.5296-08.2009) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 29.Tversky A., Kahneman D. 1992. Advances in prospect theory: cumulative representation of uncertainty. J. Risk Uncertainty 5, 297–323 10.1007/BF00122574 (doi:10.1007/BF00122574) [DOI] [Google Scholar]

- 30.Bateman I., Kahneman D., Munro C., Starmer C., Sugden R. 2005. Testing competing models of loss aversion: an adversarial collaboration. J. Public Econ. 89, 1561–1580 10.1016/j.jpubeco.2004.06.013 (doi:10.1016/j.jpubeco.2004.06.013) [DOI] [Google Scholar]

- 31.Sokol-Hessner P., Hsu M., Curley N. G., Delgado M. R., Camerer C. F., Phelps E. A. 2009. Thinking like a trader selectively reduces individuals' loss aversion. Proc. Natl Acad. Sci. USA 106, 5035–5040 10.1073/pnas.0806761106 (doi:10.1073/pnas.0806761106) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 32.Luksys G., Gerstner W., Sandi C. 2009. Stress, genotype and norepinephrine in the prediction of mouse behavior using reinforcement learning. Nat. Neurosci. 12, 1180–1186 10.1038/nn.2374 (doi:10.1038/nn.2374) [DOI] [PubMed] [Google Scholar]

- 33.Pessiglione M., Seymour B., Flandin G., Dolan R. J., Frith C. D. 2006. Dopamine-dependent prediction errors underpin reward-seeking behaviour in humans. Nature 442, 1042–1045 10.1038/nature05051 (doi:10.1038/nature05051) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 34.Roiser J. P., de Martino B., Tan G. C. Y., Kumaran D., Seymour B., Wood N. W., Dolan R. J. 2009. A genetically mediated bias in decision making driven by failure of amygdala control. J. Neurosci. 29, 5985–5991 10.1523/JNEUROSCI.0407-09.2009 (doi:10.1523/JNEUROSCI.0407-09.2009) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35.Zhong S., Israel H., Xue P. C., Sham S., Ebstein R. P., Chew S. H. 2009. A neurochemical approach to valuation sensitivity over gains and losses. Proc. R. Soc. B 276, 4181–4188 10.1098/rspb.2009.1312 (doi:10.1098/rspb.2009.1312) [DOI] [PMC free article] [PubMed] [Google Scholar]

- 36.Lusher J. M., Chandler C., Ball D. 2001. Dopamine D4 receptor gene (DRD4) is associated with novelty seeking (NS) and substance abuse: the saga continues. Mol. Psychiatry 6, 497–499 10.1038/sj.mp.4000918 (doi:10.1038/sj.mp.4000918) [DOI] [PubMed] [Google Scholar]

- 37.Kreek M. J., Nielsen D. A., Butelman E. R., LaForge K. S. 2005. Genetic influences on impulsivity, risk taking, stress responsivity and vulnerability to drug abuse and addiction. Nat. Neurosci. 8, 1450–1457 10.1038/nn1583 (doi:10.1038/nn1583) [DOI] [PubMed] [Google Scholar]

- 38.Schinka J. A., Letsch E. A., Crawford F. C. 2002. DRD4 and novelty seeking: results of meta-analyses. Am. J. Med. Genet. 114, 643–648 10.1002/ajmg.10649 (doi:10.1002/ajmg.10649) [DOI] [PubMed] [Google Scholar]

- 39.Guo S. W., Thompson E. A. 1992. Performing the exact test of Hardy–Weinberg proportion for multiple alleles. Biometrics 48, 361–372 10.2307/2532296 (doi:10.2307/2532296) [DOI] [PubMed] [Google Scholar]

- 40.Lagarias J. C., Reeds J. A., Wright M. H., Wright P. E. 1998. Convergence properties of the Nelder–Mead simplex method in low dimensions. SIAM J. Optim. 9, 112–147 10.1137/S1052623496303470 (doi:10.1137/S1052623496303470) [DOI] [Google Scholar]