Abstract

The two-phase design has recently received attention in the statistical literature as an extension to the traditional case-control study for settings where a predictor of interest is rare or subject to missclassification. Despite a thorough methodological treatment and the potential for substantial efficiency gains, the two-phase design has not been widely adopted. This may be due, in part, to a lack of general-purpose, readily-available software. The osDesign package for R provides a suite of functions for analyzing data from a two-phase and/or case-control design, as well as evaluating operating characteristics, including bias, efficiency and power. The evaluation is simulation-based, permitting flexible application of the package to a broad range of scientific settings. Using lung cancer mortality data from Ohio, the package is illustrated with a detailed case-study in which two statistical goals are considered: (i) the evaluation of small-sample operating characteristics for two-phase and case-control designs and (ii) the planning and design of a future two-phase study.

Keywords: operating characteristics, power, simulation, study design

1. Introduction

Researchers have at their disposal a wide variety of study designs with which to identify and assess associations between predictors and outcomes. In epidemiology, the case-control design is a mainstay of observational research for binary outcomes (Prentice and Pyke 1979; Breslow and Day 1980). While the design provides an efficient framework for investigating a rare outcome, gains over simple random sampling may be lost if the predictor or exposure of interest is also rare. For the setting where the exposure is binary, White (1982) proposed using the two-phase design as a means to improving efficiency (Neyman 1938). In this context, the design stratifies the population jointly on the outcome and exposure, resulting in four phase I strata. From each of these, a sample is drawn with additional exposure/confounder information retrospectively ascertained. Similar to the case-control design, efficiency gains arise due to the over-sampling of a rare sub-population (particularly exposed cases). Over the past 25 years the statistical literature has built on this (and other) work, to provide a comprehensive methodological treatment of the two-phase design; key recent references include Breslow and Holubkov (1997a), Scott and Wild (1997) and Breslow and Chatterjee (1999).

Despite the potential for substantial efficiency gains relative to a case-control design, the two-phase design has not been widely adopted. To illustrate this, and motivated by our work in epidemiologic applications, we recently conducted a survey of five top-line epidemiological/medical journals (American Journal of Epidemiology, Epidemiology, International Journal of Epidemiology, New England Journal of Medicine and Journal of the American Medical Association). Of the 4,792 studies published between 2002 and 2007, 816 used the case-control design; only one specifically employed the two-phase design. The lack of uptake may be due, in part, to a paucity of general-purpose, readily-available software for (i) the analysis of two-phase designs and (ii) the evaluation of small-sample operating characteristics, such as bias and power.

In this article we introduce and provide an overview of a new R (R Development Core Team 2011) package, osDesign, that contains a suite of functions useful when designing and analyzing two-phase and case-control studies. The package is available from the Comprehensive R Archive Network at http://CRAN.R-project.org/package=osDesign. In Section 2 we provide a brief review of the two-phase design including notation, an overview of estimation/inference techniques and a summary of the published literature on design considerations. Section 3 outlines a proposed simulation-based algorithm for evaluating small-sample operating characteristics of two-phase and case-control designs, implemented in the osDesign package. Sections 4, 5, and 6 illustrate the package with a detailed case-study using lung cancer mortality data from Ohio. Section 7 briefly discusses the trade-off between computing time and accuracy inherent to simulation-based estimation. Finally, Section 8 concludes with a brief summary and areas for further work.

2. The two-phase design

Let Y be the binary outcome under investigation and X a vector of explanatory variables which will generally include the exposure of interest as well as confounders and effect modifiers. Suppose the relationship between Y and X is characterized via the logistic regression model:

| (1) |

In the context of this work, the primary statistical task is to perform estimation and inference with respect to the vector of exposure-specific log odds ratios, βx. The rest of this section outlines the general two-phase sampling scheme and corresponding likelihood, presents an overview of estimation and inference techniques, and reviews the literature and available software for designing two-phase studies.

2.1. Data collection scheme

Initially, suppose N individuals from the population of interest are observed. These data can either be a complete enumeration of the observable population or a large sample drawn cross-sectionally, prospectively or retrospectively (Breslow and Holubkov 1997b). In addition to outcome status, some additional information is available for all N observed individuals; using this information a stratification variable, denoted by S and taking on one of K levels is constructed. For example if sex and age information is available, S could be constructed by either taking sex alone or categorizing age or some combination of both.

The cross-classification by Y and S is referred to as the phase I data and yields N0k controls and N1k cases in the k-th stratum of S, k = 1,…, K; Table 1 summarizes the notation.

Table 1.

Notation for the phase I data.

| S = 1 | S = 2 | … | 5 = K | S = K | |

|---|---|---|---|---|---|

| Y = 0 | N10 | N02 | … | N0K | N0 |

| Y = 1 | N11 | N12 | … | N1K | N1 |

Given the phase I cross-classification in Table 1, phase II involves drawing nyk individuals at random from the Nyk in each of the 2K outcome by stratum combinations. Note, when there is no stratification (or, equivalently, K = 1) Table 1 is analogous to a case-control sampling frame for the phase I population/sample.

For each individual sampled at phase II, detailed exposure/confounder information is (restro-spectively) obtained resulting in the covariate vectors xyki, for i = 1,…, nyk. The set of n = Σy Σk nyk covariate vectors are collectively referred to as the phase II data.

2.2. Two-phase likelihood

The observed data in a two-phase study consist of two sets of random quantities: the 2K phase I counts, {Nyk; y = 0, 1, k = 1,…, K}, and the n phase II covariate vectors, {xyki; y = 0, 1, k = 1,…, K, i = 1,…, nyk}. When the phase I data arise via a prospective sample from the underlying population Scott and Wild (1991) showed that the likelihood for the two-phase design consists of two sets of contributions, for the phase I counts and phase II data:

| (2) |

The primary challenge in performing estimation and inference based on (2) is accounting for the retrospective nature of the data collection at phase II. Following similar arguments to those developed for the analysis of case-control studies (Prentice and Pyke 1979), the retrospective phase II contribution can be re-parameterized to give two components: a parametric prospective component for the outcome data and a non-parametric component for the marginal exposure distribution (Holubkov 1995). This induces a series of constraints on the βx parameter space, however, which must be accounted for when performing estimation and inference. When the phase I data are obtained retrospectively, via a case-control scheme, Holubkov (1995) showed that the two-phase likelihood takes on a similar form as (2) but with the prospective P(Y = y|S = k) terms in the phase I contribution replaced by retrospective P(S = k|Y = y) terms. Re-parameterization of these latter terms induces a second series of constraints, although estimation and inference for the two types of two-phase designs is asymptotically equivalent (Breslow and Holubkov 1997a; Breslow and Chatterjee 1999).

2.3. Estimation and inference

The key advantage of re-parameterizing the two-phase likelihood is that it is then directly expressed in terms of the prospective model (1), the model of scientific interest. However, as noted, the re-parameterization induces a series of constraints on the parameter space for the regression coefficients {β0, βx}; one set for each phase of data collection that is retrospective. Three estimators have been proposed for the analysis of two-phase data: weighted likelihood (WL), pseudo- or profile likelihood (PL) and maximum likelihood (ML). While each is consistent and asymptotically normally distributed, the estimators differ in the extent to which the phase I and phase II constraints are satisfied: ML satisfies both, PL satisfies the phase I constraints and WL ignores both. A consequence is that the estimators differ in their efficiency properties (Breslow and Chatterjee 1999). Throughout, we assume the following conditional independence assumption holds: P(Y = 1|X = x, S = k) = P(Y = 1|X = x). This will hold, for example, when S is an element of X or a surrogate for one or more of the elements in X, with accuracy that does not depend on Y. We note that, while consistency and asymptotic normality of the PL and ML estimators require this assumption, it is not required by the WL estimator.

In the literature, two approaches to standard error estimation have appeared. In both approaches is decomposed into phase I and phase II contributions. The phase I contribution estimates the variance in if full data were available for all N subjects. The phase II contribution is the variance added by incomplete measurement of X. The phase II contribution is always estimated by a `sandwich' formula based on the Horvitz-Thompson variance estimator (Horvitz and Thompson 1952). Approaches for the phase I contribution differ in whether they assume model (1) is correctly specified. When model (1) is correct, the second derivative of the weighted log-likelihood estimates the Fisher information for with complete data, so its inverse estimates the variance of . If model (1) is not assumed to be correct, an empirical weighted sandwich estimator can be used for the phase I contribution. Breslow and Holubkov (1997b) provide a detailed description of each estimator, expressions for estimators of their standard errors, as well as algorithms for their implementation.

As is well known, the sandwich and information-based standard error estimators for logistic regression tend to be very similar unless the data set is very small or the model is grossly misspecified. As such, the choice between model-based and model-robust standard error estimators tends not to be of practical importance. Based, in part, on the work of Breslow and Holubkov (1997b), the osDesign evaluates operating characteristics using empirical standard error estimates for the WL estimator and model-based standard error estimates for the PL and ML estimators.

2.4. Design considerations

While methods for estimation and inference are well-developed, to date there is a paucity of published literature specifically on design considerations for two-phase studies. As such, there is little in the literature to provide guidance to the practicing researcher on settings where a two-phase study would be useful and on how to design such a study. In the setting of a binary outcome and binary exposure, White (1982) noted that efficiency may be optimized by making all phase two sample sizes, nyk, as equal as possible. Reilly (1996) considered optimal sampling strategies for two-stage methods using the mean-score method (equivalent to WL; Reilly and Pepe 1995), while, in the setting of categorical exposure/confounder variables, Schaubel, Hanley, Collet, Bolvin, Sharpe, Morrison, and Mao (1997) presented methods for determining the phase II sample size based on PL estimation. More recently, Hanley, Csizmadi, and Collet (2005) exploited a rearrangement of the variance for the PL estimator to permit an investigation of sample size requirements when confounders are qualitative.

Outside the context of regression problems, Jinn, Sedransk, and Smith (1987) consider optimal phase I and II sample sizes when one is interested in estimating the age distribution of a population, while Shrout and Newman (1989) and Erkanli, Soyer, and Angold (1998) consider estimation of the prevalence of a rare outcome.

Breslow and Chatterjee (1999) considered design issues in the two-phase studies framework, with an application to Wilms tumor prognosis, focusing on choosing the phase I sampling fractions. As with White (1982), they found that choosing the sampling fractions to achieve approximate equal numbers within each of the phase I strata (referred to as a balanced design) yielded efficiency gains over stratification based on outcome or phase I covariates alone. In the setting of binary exposure for which an error-prone surrogate is observed at phase I, McNamee (2005) compared a balanced design to the theoretically optimal design, and found the former to perform well in a broad range of settings. However, in more general settings (i.e., outside a binary exposure), it is unclear that the `one-size-fits-all' approach of a balanced design will be optimal. Further, deciding how to choose the phase I stratification variable, important when faced with several options, has not been adequately addressed.

2.5. Software

Beyond the lack of practical guidance on how to design a two-phase study, there is also a lack of convenient, general-purpose software for analyzing data arising from a two-phase design as well as for evaluating small-sample operating characteristics, such as power. Two notable exceptions are reported by Reilly and Salim (2005) and Schill, Wild, and Pigeot (2007). The former facilitates optimal design when the mean-score method is taken as the analytic approach and is implemented in several statistical packages including R, S-PLUS and Stata. The latter is implemented as a stand-alone application and permits the use of ML, although is restricted to settings with categorical covariates.

3. Evaluating operating characteristics via simulation

Approaches to evaluating operating characteristics of statistical procedures/methods, such as bias, efficiency/uncertainty and power, can broadly be grouped into two classes: formula-based and Monte Carlo or simulation-based. Formula-based approaches rely on closed form expressions for an estimator or a hypothesis test and have been developed in a broad range of settings (e.g., van Belle 2008). Unfortunately, however, formulae are unavailable in many settings that are common to statistical practice. In the context of two-phase studies, general closed-form expressions are unavailable for any of the estimators outlined in Section 2.3. Further, standard error estimators are generally complex, particularly as functions of the key elements for design consideration (the phase I stratification variable, S, and the phase II sample size, n). Finally, formulae-based evaluation of operating characteristics typically rely on asymptotic approximations to some sampling distribution, which may not work well in small-sample situations.

Monte Carlo or simulation-based methods provide a flexible, all-purpose approach to investigating small- and large-sample properties of statistical procedures (e.g., Robert and Casella 2004). In principle, one can implement a simulation in any setting, with the challenge being the proper accounting of all the necessary details. The key purpose, and contribution, of the osDesign package is to provide a convenient, easy-to-use framework for conducting simulation-based investigations of case-control and two-phase designs.

3.1. Algorithm

Both case-control and two-phase designs employ retrospective, outcome-dependent sampling schemes. As such, the explanatory variables X, or some subset, are the random quantities generated by each design. This is in contrast to the typical prospective model specification, where the outcome Y is viewed as the random quantity (see model (1), for example, which conditions on X). Simulating a retrospective, outcome-dependent sampling scheme while accommodating a prospective model specification requires care. Additionally ensuring that the simulation adequately reflects the two sources of uncertainty (i.e., sampling variability at phase I and at phase II) also requires care. One approach is to derive the induced retrospective likelihood, given by (2), and sample directly. This requires accurate accounting of the phase I and II constraints (see Section 2.2), which is complex. The approach we take is conceptually far simpler, as outlined in the following algorithm:

-

(i)

For the population of interest (i.e., the population to which the research will generalize), specify the marginal exposure distribution, P (X = x).

-

(ii)

Specify values for the regression coefficients in model (1), β0 and βx.

-

(iii)

Apply model (1) to a `population' of size N with a marginal exposure distribution specified in step (i). Specifically, for each of the N individuals generate a random Bernoulli outcome with their exposure-specific outcome probability (1).

-

(iv)

Stratify the simulated population according to the case-control or two-phase design under consideration, yielding the phase I data (as in Table 1).

-

(v)

For each of the resulting 2K strata, `sample' nyk individuals by drawing (without replacement) from the Nyk individuals previously generated. Since each of the N individuals in the population were initially characterized on the basis of their vector of explanatory variables (steps (i) and (iii)) one can then retrospectively `observe' their value for X. These collectively form the phase II data.

-

(vi)

Evaluate and record the WL, PL and ML estimators as well as the corresponding estimated standard errors, denoted and , respectively.

-

(vii)

Repeat steps (iii) to (vi) B times.

While we believe this algorithm to be conceptually simpler than characterizing and sampling from the retrospective sampling distribution, we note that steps (i) and (ii) will, in general, not be trivial, requiring careful thought and consultation with the subject-matter experts.

3.2. Simulation functions

The core functions for evaluating operating characteristics and estimating statistical power under the two-phase design are tpsSim() and tpsPower(); analogous functions for the case-control design are ccSim() and ccPower(). For each function, a detailed help file is provided as part of the osDesign package. Briefly, a simulation is conducted using the algorithm outlined in Section 3.1. For each of B simulated datasets, five estimators of βx are evaluated: the complete data ML estimate (i.e., based on complete information on all covariates for all N individuals and denoted CD), the case-control ML estimate (denoted CC) and the three two-phase estimators of Section 2.3 (WL, PL and ML). Evaluation of the CD and CC estimators is via the glm() function within R. The three two-phase estimators are implemented via a function tps(), originally written by Chatterjee and Breslow for S-PLUS, adapted for R and included as part of the osDesign package. Finally, while users can extract output directly from objects created by function in the osDesign package, plotPower() provides functionality for graphically presenting estimates of power from tpsPower() and ccPower().

The core functions automatically compute a series of operating characteristics for each of the five estimators (CD, CC, WL, PL and ML). Some of the simulated datasets may result in a failure to converge, particularly when the phase II sample size is small and/or the choice of phase I stratification variable yields sparse cells (e.g., when K is large). If there are such failures, output from each of the functions additionally returns the number of failures, with the evaluation of the operating characteristics based solely on the subset of B simulated datasets that converged.

4. Example: Lung cancer in Ohio

To illustrate the functionality of the osDesign package, we present a detailed case study using a dataset on lung cancer mortality. Specifically, we (i) estimate small-sample operating characteristics of the WL, PL and ML estimators, under various two-phase designs and (ii) examine design considerations in the context of planning a future two-phase study. Prior to doing so, we provide a brief description of the data and discuss how one specifies the underlying model/design of interest.

4.1. Marginal exposure distribution

The case study examines data on lung cancer mortality from the US state of Ohio. Specifically, the data consist of aggregated population estimates and lung cancer death counts for 55–84 year olds in 1988. The counts are available by 10-year age bands, sex and race and were obtained from the National Center for Health Statistics Compressed Mortality File. A more comprehensive dataset, providing counts further stratified by county as well as for the years 1968 to 1988, is described by Xia and Carlin (1998). The data for this case study are provided as part of the osDesign package:

R> library(“osDesign”)

R> data(“Ohio”)

R> Ohio

| Age | Sex | Race | N | Death | |

| 1 | 0 | 0 | 0 | 429617 | 1025 |

| 2 | 0 | 0 | 1 | 48382 | 172 |

| 3 | 0 | 1 | 0 | 476170 | 507 |

| 4 | 0 | 1 | 1 | 54662 | 81 |

| 5 | 1 | 0 | 0 | 319387 | 1477 |

| 6 | 1 | 0 | 1 | 29972 | 182 |

| 7 | 1 | 1 | 0 | 408229 | 733 |

| 8 | 1 | 1 | 1 | 38767 | 62 |

| 9 | 2 | 0 | 0 | 139050 | 768 |

| 10 | 2 | 0 | 1 | 11610 | 100 |

| 11 | 2 | 1 | 0 | 244965 | 391 |

| 12 | 2 | 1 | 1 | 19366 | 35 |

Age is coded as 0/1/2 for the 55–64/65–74/75–84 year groups, Sex is coded as 0/1 for male/female and Race is coded as 0/1 for white/non-white. The columns labelled N and Death provide the population counts and number of lung cancer deaths, respectively. Jointly, the first four columns of the Ohio dataset form the marginal exposure distribution (across N = 2,220,177 individuals), required in step (i) of the simulation algorithm outlined in Section 3.1.

4.2. Model specification

For both the two-phase and case-control designs, the target of estimation and inference is some logistic regression model for the binary outcome Y. Let A1 be a binary indicator of whether or not an individual's age is between 65 and 74 years, and A2 a binary indicator of whether or not the age is between 75 and 84 years. Further, let S be a binary indicator of sex and R a binary indicator of race (both coded as in the Ohio data). Finally, let Y = 0/1 be a binary indicator of lung cancer mortality status. We consider the following two logistic models for π = P(Y = 1| A1, A2, S, R):

| (3) |

| (4) |

Model (3) consists solely of main effects for each of the three explanatory variables while model (4) further incorporates an interaction term between sex and race.

Specification of a logistic model within the osDesign package is achieved via a `design matrix', denoted by the generic argument X. The first column of the design matrix consist of 1's (specifically for the intercept parameter) while each subsequent column represents an individual predictor. The coding of each predictor column follows the same convention of having a referent group coded as 0 and subsequent categories as increasing integers. The induced model specification is then obtained via an application of the factor() function to each column of X and concatenated to construct an R formula object for use in either the glm() or tps() functions. This process can be reversed to construct the appropriate design matrix for any given model. For example, the specifications corresponding to models (3) and (4) are

R> XM <- cbind(Int = 1, Ohio[, 1:3])

R> XI <- cbind(XM, SbyR = XM[, 3] * XM[, 4])

R> XM

| Int | Age | Sex | Race | |

| 1 | 1 | 0 | 0 | 0 |

| 2 | 1 | 0 | 0 | 1 |

| 3 | 1 | 0 | 1 | 0 |

| 4 | 1 | 0 | 1 | 1 |

| 5 | 1 | 1 | 0 | 0 |

| 6 | 1 | 1 | 0 | 1 |

| 7 | 1 | 1 | 1 | 0 |

| 8 | 1 | 1 | 1 | 1 |

| 9 | 1 | 2 | 0 | 0 |

| 10 | 1 | 2 | 0 | 1 |

| 11 | 1 | 2 | 1 | 0 |

| 12 | 1 | 2 | 1 | 1 |

It is important to note that XM and XI do not correspond to the standard definition of a design matrix. In both models (3) and (4), for example, the age variable is included via two dummy variables (with corresponding regression coefficients, βA1 and βA2); in a standard design matrix these would be represented by two separate columns as follows:

R> cbind(Int = 1, Age1 = as.numeric(Ohio[, 1] == 1), + Age2 = as.numeric(Ohio[, 1] == 2), Ohio[, 2:3])

While the osDesign package currently allows arbitrary categorical variables in the specification of the underlying logistic model, continuous predictors are not accommodated at this time. As we expand upon below, the approach taken for the osDesign package permits the straightforward specification of the phase I stratification variable, S, in terms of the columns of X. An additional advantage is the representation of data as aggregated counts (i.e., binomial outcomes); accommodating continuous explanatory variables precludes aggregation and, for large phase I datasets such as the Ohio data, could dramatically increase the computational burden for each repetition of the simulation. We do note, however, that the tps() function, used for the analysis of data arising from a two-phase design, does accommodate continuous exposures in the model of interest.

Given a model of interest, step (ii) of the algorithm in Section 3.1 requires specification of the `true' values for regression coefficients. For both models (3) and (4), we take these from fits to the complete data:

R> fitM <- glm(cbind(Death, N – Death) ~ factor(Age) + Sex + Race, + data = Ohio, family = binomial)

R> summary(fitM)

…

Coefficients:

| Estimate | Std. Error | z value | Pr(>|z|) | ||

| (Intercept) | −5.96210 | 0.02572 | −231.769 | < 2e-16 | *** |

| factor(Age)1 | 0.59538 | 0.03118 | 19.097 | < 2e-16 | *** |

| factor(Age)2 | 0.68796 | 0.03671 | 18.738 | < 2e-16 | *** |

| Sex | −1.00412 | 0.02879 | −34.878 | < 2e-16 | *** |

| Race | 0.28303 | 0.04238 | 6.678 | 2.42e-11 | *** |

R> fitI <- glm(cbind(Death, N – Death) ~ factor(Age) + Sex * Race, + data = Ohio, family = binomial)

R> summary(fitI)

…

Coefficients:

| Estimate | Std. Error | z value | Pr(>|z|) | ||

| (Intercept) | −5.97008 | 0.02599 | −229.722 | < 2e-16 | *** |

| factor(Age)1 | 0.59547 | 0.03118 | 19.099 | < 2e-16 | *** |

| factor(Age)2 | 0.68752 | 0.03672 | 18.724 | < 2e-16 | *** |

| Sex | −0.97979 | 0.03045 | −32.182 | < 2e-16 | *** |

| Race | 0.35097 | 0.05024 | 6.986 | 2.84e-12 | *** |

| Sex:Race | −0.22213 | 0.09362 | −2.373 | 0.0177 | * |

4.3. Design choice

A key defining feature of the two-phase design is that one has access to complete data on a subset of data elements for all individuals in the phase I population/sample (see Section 2.1). Additional data collection efforts are required to obtain complete information on all data elements from a sub-sample; hence the phase II data. Of course, the nature of the available phase I information dictates which elements require collection at phase II. For the Ohio lung cancer data, given three predictors, Table 2 provides the 8 potential designs. Note design #1 has complete information on all individuals at phase I and is, therefore, referred to as the `complete data' design. Design #2 only has access to outcome information at phase I and is consequently the traditional case-control study. Designs #3 to #8 denote the 6 remaining potential two-phase designs. For each design, the third and fourth columns provide the number of phase I strata and the data elements requiring collection at phase II, respectively.

Table 2.

Data availability scenarios for hypothetical two-phase studies of the Ohio lung cancer mortality example

| Design | Elements available at phase I | Number of phase I strata | Elements requiring collection at phase II |

|---|---|---|---|

| 1a | Y, Age, Sex, Race | 24 | NA |

| 2b | Y | 2 | Age, Sex, Race |

| 3 | Y, Age | 6 | Sex, Race |

| 4 | Y, Sex | 4 | Age, Race |

| 5 | Y, Race | 4 | Age, Sex |

| 6 | Y, Age, Sex | 12 | Race |

| 7 | Y, Age, Race | 12 | Sex |

| 8 | Y, Sex, Race | 8 | Age |

equivalent to a complete data design

equivalent to a case-control design

5. Small-sample operating characteristics

Section 4 illustrated the how to specify key quantities, required by the core functions in the osDesign package. In this section we continue the case study and illustrate the use of the package to estimate small-sample operating characteristics for the two-phase and case-control designs.

5.1. A single two-phase design

To illustrate the evaluation of small-sample operating characteristics, consider the two-phase design for which age information is available at phase I (i.e., design #3 in Table 2). Table 3 provides the phase I stratification for the Ohio data.

Table 3.

Phase I data for the Ohio lung cancer mortality data, where S represents the three-level age variable described in Section 4.1.

| S = 1 | S = 2 | S = 3 | ||

|---|---|---|---|---|

| Y = 0 | 1,007,046 | 793,901 | 413,697 | 2,220,177 |

| Y = 1 | 1,785 | 2,454 | 1,294 | 5,533 |

Given these phase I data, additional data collection efforts are required to obtain information on sex and race. To this end, suppose sufficient resources exist to obtain such information on n = 300 individuals at phase II; allocating these equally across the 6 strata yields a balanced design for which nyk = 50, for y = 0, 1 and k = 1, 2, 3.

As outlined in Section 3.2, the core function for evaluating operating characteristics of estimators for such a two-phase design is tpsSim(). In the present context, the basic command for running the simulation is:

R> ocAge <- tpsSim(B = 10000, betaTruth = fitM$coef, X = XM, N = Ohio$N, + strata = 2, nII0 = c(50, 50, 50), nII1 = c(50, 50, 50), + betaNames = c(“Int”, “Age1”, “Age2”, “Sex”, “Race”), monitor = 100)

While greater detail on the usage of the tpsSim() function is provided by the corresponding help file, we briefly highlight three of the arguments. Firstly, the `strata' argument specifies the choice of the phase I stratification variable by referring to the columns of the design matrix X. For example, in the above sample code, `strata = 2' refers to the second column of XM (i.e., the column representing the three-level age variable). One could similarly stratify on sex or race by specifying `strata = 3' or `strata = 4', respectively. In some settings, information may be available at phase I on more than one exposure variable. For example, suppose sex and race information were available on all 2,220,177 individuals, with age requiring collection at phase II (design #8 in Table 2). Taking S to be sex and race jointly, the appropriate argument would be `strata = c(3, 4)', indicating the third and fourth columns of XM.

Secondly, the `nII0' and `nII1' arguments provide the phase II control and case sample sizes, respectively. While the above code corresponds to a balanced design (i.e., the same number of phase II samples drawn from the 6 phase I strata), these arguments can be easily modified to specify any phase II design with the caveat that each of the nyk > 0. For example, one could specify an unbalanced design that over-samples individuals who are 75–84 years of age by setting `nII0 = c(25, 25, 100)' and `nII1 = c(25, 25, 100)'.

Finally, the `monitor' argument can be used to provide an update of the progress of the simulation, as the B datasets are generated and evaluated. In the above example a brief message is printed every 100 repetitions. The default is monitor = NULL; in this case no output is provided as the simulation progresses.

Once the simulation is completed, various operating characteristics are automatically evaluated and stored in an object of class `tpsSim()'. Many of the operating characteristics, such as bias, power, coverage probability are standard; the help files provide a detailed list. One operating characteristic we highlight here is the ratio of the standard error for a particular estimator, relative to the standard error of some referent estimator, multiplied by 100:

This quantity is closely related to the usual relative efficiency (a ratio of variances, rather than standard errors) and is referred to as the relative uncertainty. The appeal of this operating characteristic arises from its' interpretability in terms of the expected width of Wald-based confidence intervals. For example, suppose the relative uncertainty is estimated to be 82.3: Wald-based confidence intervals are expected to be approximately 82.3% tighter than those for the referent estimator, indicating lower uncertainty (or, equivalently, greater statistical efficiency) and greater power to detect a non-zero association. While the default in the osDesign package is to calculate the relative uncertainty with respect to the case-control estimator, an alternative choice can be made using the referent argument.

The following provides the basic output from the ocAge object (using a generic print function):

R> ocAge

Number of simulations, B: 10000

Phase I stratification variable(s): Age

Sample size at Phase I: 2220177

Sample size at Phase II sample size:

controls, nII0: 50 50 50

cases, nII1: 50 50 50

Sample size for the case-control design, nCC: 150 150

'True' regession coefficients, betaTruth:

| Int | −5.9620986 |

| Age1 | 0.5953782 |

| Age2 | 0.6879627 |

| Sex | −1.0041234 |

| Race | 0.2830300 |

Mean percent bias

| Int | Age1 | Age2 | Sex | Race | |

| CD | 0.0 | −0.1 | −0.1 | 0.1 | 0.0 |

| CC | NA | 2.6 | 3.0 | 2.3 | 7.1 |

| TPS-WL | −0.1 | 1.3 | 0.3 | 3.4 | 13.4 |

| TPS-PL | −0.1 | 0.0 | 0.5 | 2.0 | 6.3 |

| TPS-ML | −0.1 | 0.0 | 0.5 | 2.0 | 6.3 |

95% coverage probability

| Int | Age1 | Age2 | Sex | Race | |

| CD | 95.0 | 94.7 | 95.1 | 94.8 | 95.1 |

| CC | NA | 94.5 | 94.7 | 94.5 | 95.1 |

| TPS-WL | 95.1 | 96.9 | 96.2 | 94.5 | 94.9 |

| TPS-PL | 94.8 | 97.0 | 95.6 | 94.5 | 95.5 |

| TPS-ML | 94.8 | 97.0 | 95.6 | 94.5 | 95.5 |

Relative uncertainty

| Int | Age1 | Age2 | Sex | Race | |

| CD | NA | 11.0 | 10.8 | 11.6 | 10.0 |

| CC | NA | 100.0 | 100.0 | 100.0 | 100.0 |

| TPS-WL | NA | 42.9 | 37.0 | 104.0 | 110.7 |

| TPS-PL | NA | 30.3 | 27.3 | 98.3 | 99.3 |

| TPS-ML | NA | 30.3 | 27.3 | 98.3 | 99.3 |

From a substantive perspective, both the PL and ML estimators for the two-phase design generally exhibit reduced small-sample bias compared to both the case-control and two-phase WL estimators. For example, based on a phase II sample size of n = 300, the mean percent bias for the estimator of the race effect βR is approximately 6.3% for both the PL and ML estimators; the corresponding small-sample percent biases for the CC and WL estimators are approximately 7.1% and 13.4%, respectively. That the coverage probabilities are all close to their nominal levels, together with the relatively small bias, indicates that standard errors are well estimated across all five estimators. Finally, compared to a standard case-control design, all three two-phase estimators for the intercept and two age coefficients (β0, βA1, and βA2) exhibit substantially reduced uncertainty illustrating the fundamental utility of exploiting the phase I age information. While the two-phase WL estimator exhibits somewhat increased uncertainty for both the sex and race main effects (approximately 104% for βS and 111% for βR) there appear to be no trade-offs for PL and ML two-phase estimators.

5.2. Comparing specific designs

In some settings, researchers may have access to information on multiple covariates at phase I. For example, suppose sex and race information is available and the purpose of phase II is to facilitate collection of age information. In this setting, there are three potential phase I stratification schemes: (i) sex alone, (ii) race alone and (iii) sex and race jointly (designs #4, #5 and #8 in Table 2, respectively). The following commands can be used to investigate these three designs when interest lies in model (4) and sufficient resources exist to collect n = 200 samples at Phase II sample size:

R> ocInterS <- tpsSim(B = 50000, betaTruth = fitI$coef, X = XI, N = Ohio$N, + strata = 3, nII0 = c(50, 50), nII1 = c(50, 50))

R> ocInterR <- tpsSim(B = 50000, betaTruth = fitI$coef, X= XI, N = Ohio$N, + strata = 4, nII0 = c(50, 50), nII1 = c(50, 50))

R> ocInterSR <- tpsSim(B = 50000, betaTruth = fitI$coef, X = XI, N = Ohio$N, + strata = c(3, 4), nII0 = c(25, 25, 25, 25), nII1 = c(25, 25, 25, 25))

Table 4 provides estimates of small sample percent median bias for the main effect for sex, βS, and the interaction term, βSR. We see that, in terms of small-sample bias, estimation of βS under either two-phase design that stratifies on sex (either alone or jointly with race) is superior to that under the case-control design. Interestingly, estimation of βS under the two-phase design that stratifies solely on race is no better in terms of bias than the case-control design. Small-sample estimation of both parameters is generally superior under each of the two-phase designs than under the case-control design. This is particularly the case for the βSR parameter; compare 38.7% bias to 1.1%, 1.4% and 0.6% under the ML estimator for the three two-phase designs.

Table 4.

Percent median bias for estimation of βS and βSR in model (4), under various design/estimator combinations. Estimates are based on B = 10,000 simulated datasets.

| Design | Sex main effect, βS |

Interaction, βSR |

||||

|---|---|---|---|---|---|---|

| WL | PL | ML | WL | PL | ML | |

| Complete data | - | - | 0.0 | - | - | 0.6 |

| Case-control designa | - | - | 1.7 | - | - | 38.7 |

| Two-phase design | ||||||

| Sexb | 1.4 | 0.1 | 0.1 | 5.7 | 2.7 | 1.1 |

| Raceb | 6.3 | 2.9 | 2.9 | −15.5 | 1.4 | 1.4 |

| Sex and Race jointlyc | 0.9 | −0.4 | −0.4 | −5.7 | 0.6 | 0.6 |

balanced case-control design with n0 = n1 = 100,

Balanced two-phase design with nyk = 50 for y = 0,1 and k = 0,1,

Balanced two-phase design with nyk = 25 for y = 0,1 and k = 0,1, 2, 3

5.3. All two-phase designs

Beyond comparing specific two-phase designs, it may be of interest to investigate the relative performance of all possible designs based on the X argument. This is achieved by specifying `strata = 0'. Since the number of phase I strata will differ across the designs (see Table 2), an exhaustive comparison is restricted to balanced designs and hence only requires specification of the overall phase II sample sizes (n0, n1), via the nII argument. Note, researchers interested in investigating unbalanced designs can do so using the tpsSim() function and modifying the nII0 and nII1 arguments.

The following provides the basic command for running the simulation, taking n0 = n1 = 250, along with abbreviated output restricted to relative uncertainty:

R> ocAll <- tpsSim(B = 10000, betaTruth = fitM$coef, X = XM, N = Ohio$N, + strata = 0, nII = c(250, 250), monitor = 100)

R> ocAll

Number of simulations, B: 10000

Phase I stratification variable(s):

- All combinations of

- 2 : Age

- 3 : Sex

- 4 : Race

Sample size at Phase I: 2220177

Sample size at Phase II, nII=c(nII0, nII1): 250 250

Sample size for the case-control design, nCC: 250 250

…

Relative uncertainty

| Int | Age1 | Age2 | Sex | Race | ||

| CD | NA | 14.7 | 14.2 | 14.7 | 13.4 | |

| CC | NA | 100.0 | 100.0 | 100.0 | 100.0 | |

| TPS-WL | 2 | NA | 42.3 | 36.5 | 102.7 | 109.4 |

| 3 | NA | 103.7 | 104.6 | 31.8 | 107.2 | |

| 4 | NA | 128.3 | 134.5 | 132.2 | 29.7 | |

| 23 | NA | 19.8 | 17.6 | 18.6 | 108.5 | |

| 24 | NA | 49.8 | 43.6 | 128.8 | 25.4 | |

| 34 | NA | 130.9 | 132.0 | 37.8 | 20.3 | |

| TPS-PL | 2 | NA | 31.2 | 28.5 | 98.4 | 101.0 |

| 3 | NA | 96.4 | 96.5 | 23.5 | 98.4 | |

| 4 | NA | 98.7 | 101.7 | 100.6 | 22.1 | |

| 23 | NA | 17.4 | 16.2 | 16.0 | 96.8 | |

| 24 | NA | 34.9 | 32.9 | 98.0 | 20.3 | |

| 34 | NA | 95.8 | 98.6 | 29.2 | 17.6 | |

| TPS-ML | 2 | NA | 31.2 | 28.5 | 98.4 | 101.0 |

| 3 | NA | 96.4 | 96.5 | 23.5 | 98.4 | |

| 4 | NA | 98.7 | 101.7 | 100.6 | 22.1 | |

| 23 | NA | 16.5 | 15.7 | 15.8 | 101.1 | |

| 24 | NA | 33.0 | 30.1 | 98.9 | 20.0 | |

| 34 | NA | 96.5 | 99.5 | 25.2 | 17.1 |

As the phase I stratification schemes for each of the two-phase designs are identified in terms of the columns of the design matrix XM (see the left-hand most column of the output above), a key is provided to remind the user of the variables to which they correspond (see the top of the table). So, for example, the two-phase design that jointly stratified on age and race corresponds to the results for the `24' design.

From the output, it is clear that efficiency gains for any given coefficient depend heavily on the choice of phase I stratification variable. While it is well-known that stratification schemes that involve a specific explanatory variable result in efficiency gains (i.e., reduced uncertainty relative to a balanced case-control design) for the corresponding coefficient (e.g., Breslow and Chatterjee 1999), the output from tpsSim() provides a direct quantitative assessment of these gains in small-sample settings.

5.4. Case-control sampling at phase I

As mentioned in Section 2.1, the phase I sample may arise via one of several different sampling schemes. The `cohort' argument in the tpsSim() function indicates the sampling scheme for the phase I data: `cohort = TRUE' is the default and is appropriate if the phase I data are a complete enumeration or a large prospective sample; `cohort = FALSE' indicates the phase I data were collected via a case-control scheme. When the phase I data are taken to arise from a case-control scheme, the `NI' = {N0, N1} argument is used to specify the number of controls and cases observed at phase I, respectively. Note, the N argument is still required, in that it specifies the underlying population from which the phase I case-control sample is drawn (i.e., the phase I sample may not be a complete enumeration of the population). The following provides an example of code where the phase I data arise from a case-control study with N0 = N1 = 5,000:

R> ocAge <− tpsSim(B = 10000, betaTruth = fitM$coef, X = XM, N = Ohio$N, + strata = 2, cohort = FALSE, NI = c(5000, 5000), nII0 = c(50, 50, 50), + nII1 = c(50, 50, 50), betaNames = c(“Int”, “Age1”, “Age2”, “Sex”, + “Race”), monitor = 100)

5.5. Traditional case-control designs

Researchers may not always have access to suffcient information to consider a two-phase design or may solely be interested in the case-control design. osDesign also provides functionality for evaluating the operating characteristics of the traditional case-control design, via the ccSim() function. One key difference between the ccSim() and tpsSim() functions is that the former does not require specification of the stratification variable. To provide some flexibility in the range of case-control designs considered, ccSim() permits the investigation of alternative balances between the number controls and number of cases sampled. Specifically, an additional argument `r' represents the control-to-case ratio from the nCC sampled. The following illustrates the use of the the function along with abbreviated output:

R> resultsCC <- ccSim(B = 10000, betaTruth = fitM$coef, X = XM, N = Ohio$N, + nCC = 500, r = c(0.67, 1.5), betaNames = c(“Int”, “Age1”, “Age2”, + “Sex”, “Race”), monitor = 100)

R> resultsCC

…

Mean percent bias

| Int | Age1 | Age2 | Sex | Race | ||

| CD | 0 | 0.0 | 0.0 | 0.0 | −0.3 | |

| CC | r = 1 | NA | 1.4 | 1.5 | 0.9 | 1.3 |

| CC | r = 0.67 | NA | 1.0 | 1.6 | 1.1 | 4.7 |

| CC | r = 1.5 | NA | 1.3 | 1.2 | 1.3 | −1.5 |

…

Relative uncertainty

| Int | Age1 | Age2 | Sex | Race | ||

| CD | NA | 14.7 | 14.3 | 15.1 | 13.2 | |

| CC | r = 1 | NA | 100.0 | 100.0 | 100.0 | 100.0 |

| CC | r = 0.67 | NA | 101.6 | 100.2 | 103.2 | 102.8 |

| CC | r = 1.5 | NA | 101.2 | 102.1 | 104.2 | 100.2 |

As with the tpsSim() function, ccSim() automatically includes a balanced case-control design (r = 1) in the list of designs for which operating characteristics are estimated. This balanced design is used as the referent in evaluation of relative uncertainty.

6. Power calculations for study design

Section 5 focused on evaluating general small-sample operating characteristics. Another important task, for which the osDesign package provides practical assistance, is the planning and designing of future studies. In this section we illustrate the use of osDesign to examine the impact of alternative phase I stratification schemes, estimate and present power for both the two-phase and case-control designs, and modify the anticipated effect size to be detected.

6.1. Expected phase I strata

In most practical settings, the focus of study design considerations will be on the anticipated effect sizes, βx, and phase II sample size, n. Depending on the nature of the availability of phase I information, researchers may also have options with respect to the phase I stratification. Each of these choices have ramifications for the power of the design and will require detailed communication between the statistician and collaborators. To aid this communication, the phaseI() function provides the expected phase I counts based on the assumed marginal exposure distribution, logistic model, overall sample size and stratification variable. For example, taking S to be race for the main effects only model yields:

R> phaseI(betaTruth = fitM$coef, X = XM, N = Ohio$N, strata = 4)

Expected Phase I counts:

| N0k | N1k | |

| Race = 0 | 2012517 | 4901 |

| Race = 1 | 202127 | 632 |

Additionally stratifying on age yields:

R> phaseI(betaTruth = fitM$coef, X = XM, N = Ohio$N, strata = c(2, 4))

Expected Phase I counts:

| N0k | N1k | ||

| Age = 0 | Race = 0 | 904235 | 1552 |

| Age = 0 | Race = 1 | 102811 | 233 |

| Age = 1 | Race = 0 | 725434 | 2182 |

| Age = 1 | Race = 1 | 68467 | 272 |

| Age = 2 | Race = 0 | 382848 | 1167 |

| Age = 2 | Race = 1 | 30849 | 127 |

Given phase II sample sizes, the phaseI() function also calculates the expected sampling probabilities for each of the 2K phase I stratum. For example, stratifying on age alone and sampling nyk = 100 from each of the 6 phase I strata, yields:

R> phaseI(betaTruth = fitM$coef, X = XM, N = Ohio$N, strata = 2, + nII0 = rep(100, 3), nII1 = rep(100, 3)

Expected Phase I counts:

| N0k | N1k | |

| Age = 0 | 1007046 | 1785 |

| Age = 1 | 793901 | 2454 |

| Age = 2 | 413697 | 1294 |

Phase II sample size:

| nII0k | nII1k | |

| Age = 0 | 100 | 100 |

| Age = 1 | 100 | 100 |

| Age = 2 | 100 | 100 |

Expected Phase II sampling probabilities:

| p0k | p1k | |

| Age = 0 | 0.000099 | 0.056022 |

| Age = 1 | 0.000126 | 0.040750 |

| Age = 2 | 0.000242 | 0.077280 |

Finally, phaseI() also permits the calculation expected counts under a case-control sampling scheme for the phase I data via the cohort and NI arguments:

R> phaseI(betaTruth = fitM$coef, X = XM, N = Ohio$N, strata = 4, + cohort = FALSE, NI = c(5000, 5000))

Expected Phase I counts:

| N0k | N1k | |

| Race = 0 | 4544 | 4429 |

| Race = 1 | 456 | 571 |

6.2. Power for a two-phase study

When planning a study, the two-phase design is a useful option when additional information, beyond outcome status, is available on all members of the population or a large cross-sectional, cohort or case-control sub-sample (see Section 2.1). For a hypothetical study of lung cancer mortality in Ohio, suppose the only information available at phase I is outcome and race; further data collection efforts are required to obtain information on age and sex. In this specific setting, one could consider planning a case-control study that ignores the available race information or incorporate race into the sampling scheme via a two-phase design; Figure 1 quantifies the differences in power between the two designs. Each sub-plot provides estimated power curves for one of the log-odds ratio coefficients in Model (3), as a function of the phase II sample size n. Shown are curves for the case-control ML estimator and three two-phase estimators for a balanced design with S taken to be race. The calculations and figure were produced using the tpsPower() and plotPower() functions:

R> powerRaceTPS <- tpsPower(B = 10000, betaTruth = fitM$coef, X = XM, + N = Ohio$N, strata = 4, nII = seq(from = 100, to = 1000, by = 100))

R> par(mfrow = c(2, 2))

R> plotPower(powerRaceTPS, coefNum = 2, + xAxis = seq(from = 100, to = 1000, by = 100), + main = expression(“Age effect (65–74 vs. 55–64 years), ” * beta[A1]), + legendXY = c(800, 60))

R> plotPower(powerRaceTPS, coefNum = 3, + xAxis = seq(from = 100, to = 1000, by = 100), + main = expression(“Age effect (75–84 vs. 55–64 years), ” * beta[A2]), + legendXY = c(800, 60))

R> plotPower(powerRaceTPS, coefNum = 4, + xAxis = seq(from = 100, to = 1000, by = 100), + main = expression(“Sex effect, ” * beta[S]), legendXY = c(800, 60))

R> plotPower(powerRaceTPS, coefNum = 5, + xAxis = seq(from = 100, to = 1000, by = 100), + main = expression(“Race effect, ” * beta[R]), legendXY = c(800, 60))

Figure 1.

Power for each of the four main-effects regression coefficients in Model (3), under a case-control design and a balanced two-phase design where the phase I stratification variable, S, is taken to be race. Power estimates are based on B = 10,000 simulated datasets.

From Figure 1 there are clear, substantial power gains for the race effect when one adopts the two-phase design compared to a case-control design. When n = 200, the power to detect βR = 0.283 is approximately 8% under the case-control design and increases to approximately 78% for the PL and ML estimators under the two-phase design. Doubling the sample size increases the power for the two-phase estimators to 95%, while the case-control estimator increases to 12%.

Interestingly, there appears to be a trade-off with the two-phase WL estimator. For example, when n = 400, the WL estimator exhibits approximately 68% power for the race effect. While this is considerably higher than the case-control estimator, the power for the two age effects is lower than under the case-control design. This phenomenon is likely dependent on the interplay between the outcome and the joint marginal exposure/confounder distribution. While beyond the scope of this paper, the osDesign could be be used to investigate this phenomenon. Specifically, a simulation study could be designed that examines differing structures for the joint marginal exposure/confounder distribution and the extent to which specific choices of phase I stratification variable(s) reproduce the phenomenon.

6.3. Comparing two-phase designs

While Figure 1 presents power estimates for the case-control ML estimator and the three two-phase estimators for a single two-phase design, it may also be of interest to compare different designs. Figure 2 provides estimates of power for each of the four main effects in Model (3) based on ML estimation for three designs: (i) a two-phase design with S taken to be race, (ii) a two-phase design with S taken to be sex and (iii) a case-control design. We find that, at least for these examples, power gains under a two-phase design are primarily obtained for the coefficient corresponding to the covariate that is stratified upon. That is, for the age coefficients, βA1 and βA2, there is little to be gained (in terms of power) by employing a two-phase design that stratifies either on race or sex.

Figure 2.

Power for each of the four main-effects regression coefficients in Model (3) based on ML estimation for three designs: (i) a two-phase design with S taken to be race, (ii) a two-phase design with S taken to be sex and (iii) a case-control design. Power estimates are based on B = 10,000 simulated datasets.

The following provides the code used to generate the upper-left-hand sub-figure of Figure 2.

R> powerSexTPS <- tpsPower(B = 10000, betaTruth = fitM$coef, X = XM, + N = Ohio$N, strata = 3, nII = seq(from = 100, to = 1000, by = 100))

R> nLvls <- length(powerSexTPS$nII)

R> plotPower(powerRaceTPS, coefNum = 2, include = “ML”, + xAxis = seq(from = 100, to = 1000, by = 100), + main = expression(“Age effect (65–74 vs. 55–64 years), ” * beta[A1]))

R> lines(powerSexTPS$nII, powerSexTPS$power[(5 + c(0:(nLvls − 1)) * 4), 2], + lwd = 2, lty = 2, pch = 2, type = “o”)

R> lines(powerSexTPS$nII, powerSexTPS$power[(2 + c(0:(nLvls − 1)) * 4), 2], + lwd = 2, lty = 3, pch = 3, type = “o”)

R> legend(650, 65, c(“TPS: Race”, “TPS: Sex”, “Case-control”), + lwd = c(2, 2, 2), lty = c(1, 2, 3), pch = c(1, 2, 3))

6.4. Power for case-control studies

Just as the osDesign package provides a function dedicated to estimating operating characteristics of the traditional case-control design, the package also provides functionality for planning a case-control study via the ccPower() function. The following sample code examines the impact of the sample size on power for the components of Model (3) based on a balanced case-control design (i.e., r = 1).

R> powerCC <- ccPower(B = 10000, betaTruth = fitM$coef, X = XM, N = Ohio$N, + r = 1, nCC = seq(from = 100, to = 500, by = 50))

R> par(mfrow = c(2, 2))

R> plotPower(powerCC, coefNum = 2, + xAxis = seq(from = 100, to = 500, by = 100), + main = expression(“Age effect (65–74 vs. 55–64 years), ” * beta[A1]))

R> plotPower(powerCC, coefNum = 3, + xAxis = seq(from = 100, to = 500, by = 100), + main = expression(“Age effect (75–84 vs. 55–64 years), ” * beta[A2]))

R> plotPower(powerCC, coefNum = 4, + xAxis = seq(from = 100, to = 500, by = 100), + main = expression(“Sex effect, ” * beta[S]))

R> plotPower(powerCC, coefNum = 5, + xAxis = seq(from = 100, to = 500, by = 100), + main = expression(“Race effect, ” * beta[R]))

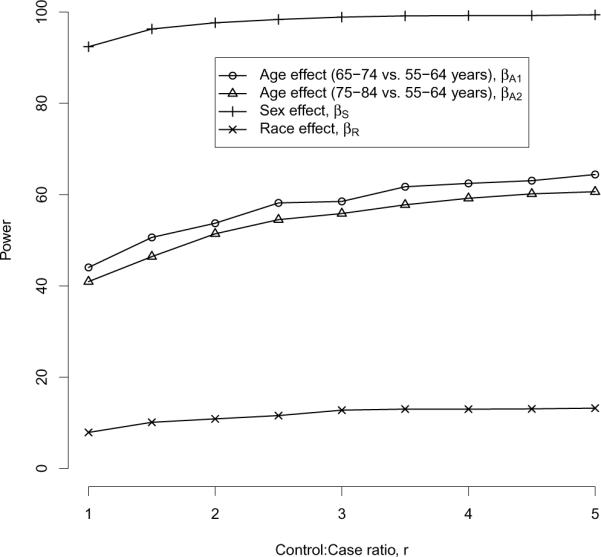

Figure 3 provides the resulting power curve estimates. Note these are the same estimates of power indicated by the `CC' curves in Figure 1; in situations where solely case-control designs are being considered, such plots may be useful. In addition to investigating the impact of increasing the overall sample size, n, researchers may be interested in investigating the benefits of sampling additional controls. Figure 4 provides estimates of power for case-control designs where the number cases is fixed at n1 = 100 and the number of controls is set to be n0 = n1 × r for r between 1 and 5. The following provides sample code used to generate the power estimates as well as Figure 4.

Figure 3.

Power for each of the four main-effects regression coefficients in Model (3), under a traditional balanced case-control design. Power estimates are based on B = 10,000 simulated datasets.

Figure 4.

Power for each of the four main-effects regression coefficients in Model (3), under a case-control design with r:1 matching. For each setting, the number of cases is fixed at n1 = 100. Power estimates are based on B = 10,000 simulated datasets.

R> powerCC100 <- ccPower(B = 10000, betaTruth = fitM$coef, X = XM, + N = Ohio$N, r = 1, nCC = 200)

R> powerCC150 <- ccPower(B = 10000, betaTruth = fitM$coef, X = XM, + N = Ohio$N, r = 1.5, nCC = 250)

R> powerCC200 <- ccPower(B = 10000, betaTruth = fitM$coef, X = XM, + N = Ohio$N, r = 2, nCC = 300) …

R> powerCC450 <- ccPower(B = 10000, betaTruth = fitM$coef, X = XM, + N = Ohio$N, r = 4.5, nCC = 550)

R> powerCC500 <- ccPower(B = 10000, betaTruth = fitM$coef, X = XM, + N = Ohio$N, r = 5, nCC = 600)

R> powerCCr <- rbind( + powerCC100$power[2, -1], … + powerCC500$power[2, -1])

R> plot(c(1, 5), c(0, 100), xlab = “Control:Case ratio, r”, ylab = “Power”, + axes = FALSE, type = “n”)

R> axis(1, at = seq(from = 1, to = 5, by = 1))

R> axis(2, at = seq(from = 0, to = 100, by = 20))

R> lines(seq(from = 1, to = 5, by = 0.5), powerCCr[, 1], lwd = 2, + type = “o”, pch = 1)

R> lines(seq(from = 1, to = 5, by = 0.5), powerCCr[, 2], lwd = 2, + type = “o”, pch = 2)

R> lines(seq(from = 1, to = 5, by = 0.5), powerCCr[, 3], lwd = 2, + type = “o”, pch = 3)

R> lines(seq(from = 1, to = 5, by = 0.5), powerCCr[, 4], lwd = 2, + type = “o”, pch = 4)

R> legend(2, 90, c( + expression(”Age effect (65–74 vs. 55–64 years), ” * beta[A1]), + expression(”Age effect (75–84 vs. 55–64 years), ” * beta[A2]), + expression(”Sex effect, ” * beta[S]), + expression(”Race effect, ” * beta[R])), lwd = rep(2, 4), pch = 1:4)

Finally, as a reminder, we note that power for unbalanced case-control studies can be investigated by modifying the `r' argument in either the ccSim() or ccPower() functions.

6.5. Modifying anticipated effect sizes

The power calculations presented in Figures 1 and 3 are for effect sizes equal to the `true' coefficient values obtained from a fit of the complete data (see Section 4.2). When conducting sample size/power calculations it is often of interest to characterize power at alternative levels of the strength of the anticipated association. This is achieved by modifying the betaTruth argument, which represents the vector (β0, βx) in the notation of model (1). Modifying any of the components of βx, however, will have consequences for the expected number of cases. For example, suppose the two age coefficients were reduced in magnitude by 50%, to give:

R> newBetaM <- fitM$coef

R> newBetaM[2:3] <- newBetaM[2:3] * 0.5

R> phaseI(betaTruth = newBetaM, X = XM, N = Ohio$N, strata = c(2, 4))

Expected Phase I counts:

| Y=0 | Y=1 | ||

| Age = 0 | Race = 0 | 904235 | 1552 |

| Age = 0 | Race = 1 | 102811 | 233 |

| Age = 1 | Race = 0 | 725995 | 1621 |

| Age = 1 | Race = 1 | 68536 | 203 |

| Age = 2 | Race = 0 | 383186 | 829 |

| Age = 2 | Race = 1 | 30886 | 90 |

Compared with the expected counts based on `betaTruth=fitM$beta', there are 1,006 fewer expected cases or, equivalently, a decrease in the outcome prevalence from 2.49 to 2.04 per 1,000. In most applied settings, the overall outcome prevalence in the population will be well-known and, in particular, fixed. Hence, it is important to ensure that the outcome prevalence is held constant across various scenarios for βx. One approach to achieving this is to fix β0 so that the overall (expected) prevalence is held at some specified level; the function beta0() calculates the appropriate value of β0 given βx, the marginal exposure distribution and outcome prevalence (represented by the rhoY argument):

R> fitM$coef1]

(Intercept) −5.962099

R> newBetaM[1] <- beta0(betaX = newBetaM[-1], X = XM, N = Ohio$N, + rhoY = sum(Ohio$Death)/sum(Ohio$N))

R> newBetaM[1]

(Intercept) −5.760943

Using the modified `newBetaM' in the tpsSim() and tpsPower() functions (as well as the ccSim() and ccPower() functions) permits the investigation of operating characteristics under various alternative effect sizes, while retaining comparability in terms of the underlying overall outcome prevalence.

7. Run times and Monte Carlo error

As outlined in Section 3, osDesign estimates operating characteristics of both two-phase and case-control designs via simulation. In practice, the use of simulation involves a trade-off between the time the simulation takes to run and the uncertainty of the estimates. The latter arises from sampling variability due to the finite choice of B and is often referred to as Monte Carlo error (MCE, Metropolis and Ulam 1949). This form of uncertainty is analogous to the usual form of sampling variability measured by standard errors; as one increases B (the `simulation sample size'), the longer it takes to run the simulation but the more accurate the results will be. Each of the examples in this manuscript, as well as those in the osDesign package, use B = 10,000. Table 5 provides run times for selected function calls presented in this manuscript, for several common choices of B. Each are based on an Apple iMac with dual core 3.6 GHz Intel Core i5 processors and 8Gb of memory, running Mac OS X 10.6.7. Further, throughout, version 1.3 of the osDesign package was used in R version 12.2.2.

Table 5.

Run times, in minutes, for select calls presented in the manuscript.

| Function call | Manuscript sub-section | Distinct designsa | Simulation sample size, B | ||||

|---|---|---|---|---|---|---|---|

| TP | CC | CD | 500 | 1,000 | 10,000 | ||

| ocAge <- tpsSim() | 5.1 | 1 | 1 | 1 | 0.28 | 0.58 | 5.95 |

| ocAll <- tpsSim() | 5.3 | 6 | 1 | 1 | 1.45 | 2.93 | 27.92 |

| powerRaceTPS <- tpsPower() | 6.2 | 9 | 9 | 1 | 2.48 | 4.87 | 49.83 |

| powerCC <- ccPower() | 6.3 | 0 | 9 | 1 | 0.38 | 0.77 | 7.60 |

Number of distinct two-phase (TP), case-control (CC) and complete data (CD) designs evaluated during each repetition.

Clearly, as B increases the time taken to run the simulation increases and since the underlying functions are based on a loop, they increase somewhat linearly with B. A simple strategy could be to run a small number of repetitions, say B = 500, to help choose the details of the broader simulation and then present final based on a larger value (as we have done). More generally, Koehler, Brown, and Haneuse (2009) provide an overview of MCE as well as simple approaches to estimating MCE in a broad range of settings. Further, given a desired level of accuracy (or uncertainty), they develop a graphical technique for determining the value of B. Their methods have been implemented in the MCE package (Koehler and Haneuse 2010) for R.

8. Summary

Although the two-phase design is well-established in the statistical literature, researchers have been slow to adopt the design as an efficient alternative to the traditional case-control design. A key factor in the lack of uptake may be the paucity of flexible, convenient software for (i) analyzing data that arises from a two-phase design, (ii) estimating small-sample operating characteristics of various designs and (iii) planning a two-phase study. The osDesign package for R provides a suite of functions that help fill this gap. The focus of this paper is the functionality of the osDesign package and we have not sought to provide general guidelines to researchers. We believe, however, that the Ohio lung cancer example may serve as a useful template to researchers as they plan their own studies (both for design purposes and the investigation of small-sample operating characteristics).

Compared to existing software, the strengths of the package include the ability to simultaneously investigate case-control and two-phase designs that vary in terms of the variable(s) determining the phase I stratification and case-control/phase II sample size; user-friendly output (both tabular and graphical) is returned for a broad range of small-sample operating characteristics. Further, functions tpsSim() and ccSim() both permit the investigation of unbalanced two-phase and case-control designs, respectively.

As outlined in Section 4.2, osDesign uses a design matrix, denoted X, for the specification of the underlying logistic model and the phase I stratification. While easy-to-use and flexible, in terms of being able to specify arbitrary design matrixes that involve categorical covariates, an important limitation is that continuous covariates are currently not accommodated. Although such covariates could not be directly used for the phase I stratification, they are often collected at phase II and included in models. However, we note that this limitation is specific to the evaluation of operating characteristics. For the analysis of data arising from a two-phase design, osDesign includes the tps() function for which there is no restriction on the covariates. While large-sample properties of the WL, PL and ML estimators are well-established in the literature, a number of real life data scenarios and design issues deserve further investigation. Within the contexts of their own scientific studies, for example, researchers may be interested in understanding small-sample properties of the various estimators. These may include characterizing the performance of the estimators when the stratification variable is subject to varying degrees of non-differential error (i.e., the conditional independence assumption of Section 2.3 does not hold) or when the model is misspecified (e.g., Breslow and Chatterjee 1999). We are currently working on extending the osDesign package to permit the investigation of these scenarios. Other avenues for extending the package that we are currently pursing include accommodating continuous exposures as well as providing functions for a broader range of outcome-dependent designs: case-control studies where all cases are sampled and controls are sampled until some pre-determined threshold for power is achieved; nested case-control designs (Oakes 1981; Langholz and Borgan 1995); and case-cohort designs (Prentice 1986).

Acknowledgments

We are grateful to an Associate Editor and two reviewers for their thoughtful and constructive comments. This research was supported by grants R01 CA125081 and R03 CA135671 from the National Institutes of Health.

References

- Breslow NE, Chatterjee N. Design and Analysis of Two-Phase Studies with Binary Outcomes Applied to Wilms' Tumor Prognosis. Applied Statistics. 1999;48:457–468. [Google Scholar]

- Breslow NE, Day NE. Statistical Methods in Cancer Research (Vol. 1): The Analysis of Case-Control Studies. World Health Organization; 1980. Distribution and Sales Service. [PubMed] [Google Scholar]

- Breslow NE, Holubkov R. Maximum Likelihood Estimation of Logistic Regression Parameters Under Two-Phase, Outcome-Dependent Sampling. Journal of the Royal Statistical Society B. 1997a;59:447–461. [Google Scholar]

- Breslow NE, Holubkov R. Weighted Likelihood, Pseudo-Likelihood and Maximum Likelihood Methods for Logistic Regression Analysis of Two-Stage Data. Statistics in Medicine. 1997b;16:103–116. doi: 10.1002/(sici)1097-0258(19970115)16:1<103::aid-sim474>3.0.co;2-p. [DOI] [PubMed] [Google Scholar]

- Erkanli A, Soyer R, Angold A. Optimal Bayesian Two-phase Designs. Journal of Statistical Planning and Inference. 1998;66:175–191. [Google Scholar]

- Hanley J, Csizmadi I, Collet J. Two-Stage Case-Control Studies: Precision of Parameter Estimates and Considerations in Selecting Sample Size. American Journal of Epidemiology. 2005;162:1225–1234. doi: 10.1093/aje/kwi340. [DOI] [PubMed] [Google Scholar]

- Holubkov R. Ph.D. thesis. University of Washington; Seattle: 1995. Maximum Likelihood Estimation in Two-Stage Case-Control Studies. [Google Scholar]

- Horvitz D, Thompson D. A Generalization of Sampling Without Replacement from a Finite Universe. Journal of the American Statistical Association. 1952;47:663–685. [Google Scholar]

- Jinn J, Sedransk J, Smith P. Optimal Two-Phase Stratified Sampling for Estimation of the Age Composition of a Fish Population. Biometrics. 1987;43:343–353. [Google Scholar]

- Koehler E, Brown E, Haneuse S. On the Assessment of Monte Carlo Error in Simulation-Based Statistical Analyses. The American Statistician. 2009;62:155–162. doi: 10.1198/tast.2009.0030. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Koehler E, Haneuse S. MCE: Tools for Evaluating Monte Carlo Error. R package version 1.1. 2010. URL http://CRAN.R-project.org/package=MCE. [Google Scholar]

- Langholz B, Borgan O. Counter-Matching: A Stratified Nested Case-Control Sampling Method. Biometrika. 1995;82:69–79. [Google Scholar]

- McNamee R. Optimal Design and Efficiency of Two-Phase Case-Control Studies with Error-Prone and Error-Free Exposure Measures. Biostatistics. 2005;6:590–603. doi: 10.1093/biostatistics/kxi029. [DOI] [PubMed] [Google Scholar]

- Metropolis N, Ulam S. The Monte Carlo Method. Journal of the American Statistical Association. 1949;44:335–341. doi: 10.1080/01621459.1949.10483310. [DOI] [PubMed] [Google Scholar]

- Neyman J. Contribution to the Theory of Sampling Human Populations. Journal of the American Statistical Association. 1938;33:101–116. [Google Scholar]

- Oakes D. Survival Times: Aspects of Partial Likelihood. International Statistical Review. 1981;49:235–264. [Google Scholar]

- Prentice RL. A Case-Cohort Design for Epidemiologic Cohort Studies and Disease Prevention Trials. Biometrika. 1986;73:1–11. [Google Scholar]

- Prentice RL, Pyke R. Logistic Disease Incidence Models and Case-Control Studies. Biometrika. 1979;66:403–411. [Google Scholar]

- R Development Core Team . R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing; Vienna, Austria: 2011. ISBN 3-900051-07-0, URL http://www.R-project.org/ [Google Scholar]

- Reilly M. Optimal Sampling Strategies for Two-Stage Studies. American Journal of Epidemiology. 1996;143:92–100. doi: 10.1093/oxfordjournals.aje.a008662. [DOI] [PubMed] [Google Scholar]

- Reilly M, Pepe M. A Mean-Score Methods for Missing and Auxiliary Covariate Data in Regression Models. Biometrika. 1995;82:299–314. [Google Scholar]

- Reilly M, Salim A. Designing Optimal Two-Stage Epidemiological Studies. In: Berger M, Wong WK, editors. Applied Optimal Designs. John Wiley & Sons; New York: 2005. [Google Scholar]

- Robert C, Casella G. Monte Carlo Statistical Methods. 2nd edition Springer-Verlag; New York: 2004. [Google Scholar]

- Schaubel D, Hanley J, Collet JP, Bolvin JF, Sharpe C, Morrison H, Mao Y. Two-Stage Sampling for Etiologic Studies; Sample Size and Power. American Journal of Epidemiology. 1997;146:450–458. doi: 10.1093/oxfordjournals.aje.a009298. [DOI] [PubMed] [Google Scholar]

- Schill W, Wild P, Pigeot I. A Planning Tool for Two-Phase Case-Control Studies. Computer Methods and Programs in Biomedicine. 2007;88:175–181. doi: 10.1016/j.cmpb.2007.08.002. [DOI] [PubMed] [Google Scholar]

- Scott A, Wild C. Fitting Logistic Models in Stratified Case-Control Studies. Biometrics. 1991;47:497–510. [Google Scholar]

- Scott AJ, Wild CJ. Fitting Regression Models to Case-control Data by Maximum Likelihood. Biometrika. 1997;84:57–71. [Google Scholar]

- Shrout PE, Newman SC. Design of Two-Phase Prevalence Studies of Rare Disorders. Biometrics. 1989;45:549–555. [PubMed] [Google Scholar]

- van Belle G. Statistical Rules of Thumb. 2nd edition John Wiley & Sons; Hoboken: 2008. [Google Scholar]

- White JE. A Two Stage Design for the Study of the Relationship Between a Rare Exposure and a Rare Disease. American Journal of Epidemiology. 1982;115:119–128. doi: 10.1093/oxfordjournals.aje.a113266. [DOI] [PubMed] [Google Scholar]

- Xia H, Carlin B. Spatio-Temporal Models with Errors in Covariates: Mapping Ohio Lung Cancer Mortality. Statistics in Medicine. 1998;17:2025–2043. doi: 10.1002/(sici)1097-0258(19980930)17:18<2025::aid-sim865>3.0.co;2-m. [DOI] [PubMed] [Google Scholar]