Abstract

Background

Health information technology (HIT) certification and meaningful use are interventions encouraging the adoption of electronic health records (EHRs) in the USA. However, these initiatives also constitute a significant intervention which will change the structure of the EHR market.

Objective

To describe quantitatively recent changes to both the demand and supply sides of the EHR market.

Materials and methods

A cohort of 3447 of hospitals from the HIMSS Analytics Database (2006–10) was created. Using hospital referral regions to define the local market, we determined the percentage of hospitals using paper records, the number of vendors, and local EHR vendor competition using the Herfindahl–Hirschman Index. Changes over time were assessed using a series of regression equations and geographic information systems analyses.

Results

Overall, there was movement away from paper records, upward trends in the number of EHR vendors, and greater competition. However, changes differed according to hospital size and region of the country. Changes were greatest for small hospitals, whereas competition and the number of vendors did not change dramatically for large hospitals.

Discussion

The EHR market is changing most dramatically for those least equipped to handle broad technological transformation, which underscores the need for continued targeted support. Furthermore, wide variations across the nation indicate a continued role for states in the support of EHR utilization.

Conclusion

The structure of the EHR market is undergoing substantial changes as desired by the proponents and architects of HIT certification and meaningful use. However, these transformations are not uniform for all hospitals or all the country.

Keywords: Electronic health records, healthcare markets, vendors, American recovery and reinvestment act, health policy

Background and significance

After a long period of lagging adoption1 and perceived market shortcomings,2 3 the electronic health record (EHR) marketplace in the USA has received two radical shocks within a short period of time. First, is the introduction of health information technology (HIT) certification intended to alleviate the concerns of EHR buyers faced with expensive, but uncertain technology decisions by creating a class of products that has been independently and objectively tested for specific capabilities.4–6 While HIT certification effectively intervened on the supply side of the EHR market, the meaningful use criteria were even more far reaching. Introduced as part of the Health Information Technology for Economic and Clinical Health (HITECH) portion of 2009's American Recovery and Reinvestment Act, meaningful use constituted an estimated $27 billion federal intervention to encourage EHR adoption.7 At its foundation, meaningful use provides a financial incentive to buy an EHR. However, as the former national coordinator for health information technology David Blumenthal stated, ‘The incentive program is not only about paying providers, it is about transforming the marketplace.’8 He went on to identify such desired changes as new companies in the marketplace and increased competition. The current national coordinator has echoed these comments about changing the marketplace.9 10

Several indicators do reflect a changing marketplace. Adoption of EHR is increasing11 and a substantial proportion of providers and hospitals report specifically seeking the EHR incentive payments.12 However, while this is evidence of healthcare's change from a paper to an electronic world, these indicators do not detail the type of fundamental marketplace changes envisioned by policy makers and HIT proponents. Likewise, the Office of the National Coordinator notes the substantial number of vendors with certified EHR products as evidence of increased competition.13 Again, while this is a suggestive indicator, measures of competition exist that would provide a better description of whether the EHR marketplace had changed since the introduction of important HIT policies. Understanding the extent and nature of changes in the EHR market is relevant to policy. Meaningful use and certification represent the single largest government intervention in a multi-billion dollar market, a source of significant ongoing costs for public and private institutions, and a policy that will ultimately change the daily operations of healthcare and public health organizations across the country.

Objective

In this paper, we quantitatively describe recent changes to both the demand and the supply sides of the EHR market using hospitals' reported technology purchases. Specifically, we examine the pace of EHR adoption by hospitals and trends in the vendor penetration and vendor competition of the EHR market over the period of certification and meaningful use. By focusing on the presence of EHR vendors as a market measure, we are better able to investigate whether or not the EHR marketplace is changing to the degree, and in the ways, expected by the architects of federal policy.

In addition, descriptions of the EHR vendor market are usually limited to division by type of service (ie, inpatient, ambulatory, or emergency department). To varying degrees, this is the practice of certifying bodies, the Office of the National Coordinator, industry trade groups, market consultants, and industry publications.14–18 While helpful, this approach includes only the relevant product dimension of a market. Our analysis incorporates the dimension of geography into the concept of EHR vendor markets, which is a new perspective. This represents the first comprehensive description of the changing structure of the EHR marketplace for hospitals in the USA during a period of intense policy intervention.

Materials and methods

Data

We created a cohort of 3447 non-federally operated, general medical and short-term acute care hospitals from the HIMSS Analytics Database for the years 2006–10. The HIMSS Analytics Database includes annual survey data on hospitals' use of specific information technology (IT) applications and the respective application vendors. HIMSS Analytics contacts chief information officers or designees for the IT variables and has collected this information since 2005. The HIMSS Analytics Database has been used in numerous scientific and market research publications on IT staffing, IT adoption, EHR adoption, and costs. HIMSS Analytics does not publish survey response rates, but reports that only 2% of hospitals refuse to participate.

For each hospital, we identified (1) if the facility had an EHR and (2) the name of the vendor supplying the technology. First, we defined the EHR solely in terms of a clinical data repository that was live and operational, in the process of installation, or under contract. HIMSS Analytics defines a clinical data repository as ‘a centralized database that allows organizations to collect, store, access, and report clinical, administrative, and financial information collected from various applications within or across the healthcare organization that provides healthcare organizations an open environment for accessing/viewing, managing, and reporting enterprise information.’ While a clinical data repository is clearly not a fully functioning EHR, it is a necessary component of the most current conceptualization of the EHR,19 20 and more importantly it provides a consistent measure of EHR vendor choice for the hospital cohort before and after the changes instituted by the HITECH Act in our secondary dataset. Next, our interest lay in what vendor the hospital had chosen and not if the hospital had made effective use of the EHR. Therefore, we considered the hospital had selected the vendor if the EHR product was live and operational, in the process of installation, or under contract. As a result, the stage of adoption or implementation did not matter, because in each instance the vendor could legitimately be present in the market. We excluded vendors of clinical data repositories designated as ‘to be replaced’ because the hospital had already made the decision to discontinue their use. The number of vendors (excluding self-developed systems) reported each year ranged from 34 to 38. The cohort included hospitals located in the 50 states and the District of Columbia with complete information on EHR vendors each year. As a result, the cohort represented between 74% and 78% of hospitals with the aforementioned characteristics included annually in the HIMSS Analytics Database.

Measures

We used the Dartmouth Atlas' Hospital Referral Regions (HRRs) to define the local geographical EHR market.21 HHRs divide the country into the distinct areas based on hospitals' performance of major cardiovascular and neurosurgical procedures22 and have been used to define the market area for healthcare in numerous health services research studies (eg, Chen et al,23 Mittler et al 24). In order to keep market areas constant over time, we assigned all hospitals to their 2007 HRRs. Three measures describe the EHR markets for each study year: percentage of hospitals using paper records, number of vendors, and EHR vendor competition. Hospitals without an automated clinical data repository and those which had not yet entered a contract with a vendor were classified as having paper medical records. For each year we counted the number of vendors with products in use in the market. Last, we measured the EHR market concentration at the hospital level using the Herfindahl–Hirschman Index (HHI), which is the sum of each vendor's market share squared.25 In this context, the HHI constitutes the weighted average of each vendor's market share within the HRR. Increasing HHI values indicate a move toward EHR market concentration, whereas decreasing HHI scores demonstrate increasing competition. In addition, each year a small number of hospitals (between 7 and 16) reported using two different EHR systems in tandem. We included both vendors in our HHI calculations, because each vendor could claim those hospitals as customers, and the use of two different systems does not conflict with our policy-based research question. Paper records were not considered as a product choice and therefore excluded from the HHI calculation.

Analysis

We calculated the means of these three measures at the HRR level for each year. Because organizational size has been an important predictor of EHR adoption26 and vendors often market their products by hospital size, we stratified each measure by the hospital's 2009 bed size: small (≤99 beds), medium (100–249 beds), and large (≥250 beds). While, these categories match existing popular reports on the EHR market,18 they should not be viewed as mutually exclusive for EHR vendors. An EHR vendor may be represented in any or all of the size-stratified measures.

A series of fixed-effects and random-effects regression equations described the changes in the annual averages of vendors, vendor competition, and percentage of hospitals using paper records at the HRR level. First, we examined if the measures in subsequent years were statistically different from those in the base year 2006 using ordinary least-squares regression, including dichotomous indicators for the year 2007–10 with cluster-robust standard errors. Second, to determine the average annual change, we obtained the slope of time regressed on each of the three dependent variables using random-intercept linear models with an unstructured variance–covariance structure.27 Third, we tested whether the pace of EHR market changes was statistically different among small, medium, and large hospitals. We estimated random intercept regression models, separately for each outcome measure, which included an interaction term between linear trend and hospital size. These coefficients served as a test of whether the trends in the number of vendors, competition, and paper record usage differ by hospital size.

We used geographic information system analysis to visualize changes and differences by geography in the EHR market. Using ArcGIS 9.3.1 (ESRI, Redlands, California, USA), we mapped the absolute change in the number of vendors and the HHI during the study period and the percentage of hospitals still using paper records in 2010 by HRR.

Results

Most hospitals in the cohort were private not-for-profit (65.9%) followed by public hospitals (18.1%) and private for-profit hospitals (16.0%). Hospitals were slightly larger than the entire population of general medical and surgical hospitals reported in the annual American Hospital Association survey (χ2=129.02; ρ<0.05). The percentage of hospitals in the cohort with at least 250 beds was 27.6%, 35.8% were medium-sized hospital, and hospitals with fewer than 100 beds made up 36.6% of the cohort.

Trends for all hospitals

Trends in the number of vendors, competition, and reliance on paper records in the EHR market are displayed in table 1. Between 2006 and 2010 the general trend was toward more vendors in a market, more vendor competition, and reductions in paper medical records. For all three measures, the overall time trends were statistically significant at the p<0.01 level (see the ‘Linear slope’ column). Specifically, the average market in 2006 had 3.70 different vendors with an EHR operational or under contract in a hospital. In 2010, the average had increased to 4.22 vendors. For vendor competition, the average HHI decreased by 3.5 points between 2006 and 2010, signaling greater vendor competition within HRRs. However, for the HHI measure, no significant changes from the 2006 baseline occurred until 2009 and 2010 when the meaningful use standards were in effect. Lastly, the percentage of hospitals relying on paper records in each market decreased from nearly one in four to <1 in 10.

Table 1.

Changes in the US electronic health record market, 2006–10¶

| Market measures at the hospital referral region level | 2006 | 2007 | 2008 | 2009 | 2010 | Linear slope |

| Mean (SD) | Mean (SD) | Mean (SD) | Mean (SD) | Mean (SD) | β (95% CI) | |

| All hospitals | ||||||

| Number of vendors | 3.70 (2.00) | 4.00 (2.10) | 4.07 (2.10)* | 4.21 (2.14)§ | 4.22 (2.17)§ | 0.12 (0.10 to 0.14)‡ |

| HHI** †† | 41.81 (21.56) | 39.82 (20.67) | 39.74 (20.65) | 38.37 (19.86)* | 38.28 (19.59)* | −1.02 (−1.30 to −0.75)‡ |

| % Hospitals using paper | 23.06 (21.47) | 15.21 (17.73)§ | 12.47 (15.73)§ | 8.28 (13.82)§ | 7.62 (12.68)§ | −3.78 (−4.13 to −3.43)‡ |

| Small hospitals (≤99 beds) | ||||||

| Number of vendors | 1.96 (1.40) | 2.16 (1.43) | 2.25 (1.48)* | 2.43 (1.58)§ | 2.48 (1.62)§ | 0.13 (0.11 to 0.15)‡ |

| HHI | 64.29 (29.12) | 62.46 (28.64) | 62.47 (29.14) | 59.74 (29.50)† | 59.23 (29.39)† | −1.94 (−2.40 to −1.48)‡ |

| % Hospitals using paper | 35.25 (33.97) | 26.13 (31.02)§ | 22.68 (29.40)§ | 16.97 (26.03)§ | 16.14 (25.38)§ | −4.74 (−5.44 to −4.05)‡ |

| Medium hospitals (100–249 beds) | ||||||

| Number of vendors | 2.23 (1.51) | 2.44 (1.57) | 2.44 (1.52)† | 2.59 (1.53)§ | 2.59 (1.57)§ | 0.09 (0.07 to 0.10)‡ |

| HHI | 62.05 (29.45) | 58.99 (1.54) | 58.63 (28.31) | 56.77 (28.26)* | 57.15 (28.44)* | −1.58 (−1.96 to −1.21)‡ |

| % Hospitals using paper | 18.70 (25.57) | 9.62 (18.79)§ | 7.77 (16.63)§ | 3.44 (10.89)§ | 2.98 (9.41)§ | −3.76 (−4.25 to −3.28)‡ |

| Large hospitals (≥ 250 beds) | ||||||

| Number of vendors | 2.16 (1.35) | 2.20 (1.45) | 2.21 (1.49) | 2.20 (1.43) | 2.22 (1.43) | 0.03 (0.01 to 0.04)‡ |

| HHI | 65.35 (29.83) | 65.08 (29.88) | 65.47 (30.18) | 64.99 (29.75) | 65.06 (29.63) | −0.44 (−0.71 to −0.18)‡ |

| % Hospitals using paper | 11.25 (24.45) | 6.28 (19.69)§ | 2.86 (12.89)§ | 0.66 (6.86)§ | 0.68 (6.92)§ | −2.68 (−3.14 to −2.21)‡ |

Statistically significantly different from 2006 (base year) at the 95% level.

Statistically significantly different from 2006 (base year) at the 90% level.

Statistically significant slope at the 99% level.

Statistically significantly different from 2006 (base year) at the 99% level.

Based on the vendors supplying data from a clinical repository that was live and operational, in the process of installation, or under contract centralized data repositories to hospitals.

Herfindahl–Hirschman Index.

Paper records were excluded in the HHI calculation.

HHI, Herfindahl–Hirschman Index.

Trends by hospital size

Recent year-to-year changes in the EHR market varied by hospital size (table 1). While for small, medium, and large hospitals the direction of the general trends in the number of vendors and competition was statistically significant and similar, the magnitude of the changes was not. In addition, we found that the pace of EHR market changes was statistically different (p<0.01) across the categories of hospital size (see online technical appendix for complete regression table).

Changes in the market place in general were most dramatic for small hospitals with fewer than 100 beds. These hospitals saw the largest absolute gains in numbers of vendors in the market and the largest increases in competition. In 2006, an HRR on average had fewer than two (1.96) vendors with EHRs in small hospitals. By 2010, the average had increased to 2.48. Similarly, over the study period, the HHI decreased by an average of 1.94 points, signaling a trend toward more competition. Small hospitals also had a statistically significant reduction in use of paper records from 35.25% to 16.14%.

The trends toward more competition and increased vendor presence in the market were also statistically significant for medium sized hospitals. However, the absolute gain in vendors and HHI reduction (ie, greater competition) was not as large as among the small hospitals. In addition, during the study period, the percentage of hospitals relying on paper records declined from 18.70% to 2.98%. On average, the use of paper records among medium-sized hospitals fell by 3.76 percentage points a year during the study period.

The EHR market has not changed dramatically for large hospitals in the number of vendors and HHI in the HRR. Despite a small statistically significant upward trend over the entire study period, changes in the average number of vendors in each HRR were not statistically different between 2006 and 2010. The average number of vendors in the HRR for large hospitals remained around 2.2. Likewise, the large hospitals witnessed a trend toward more competition over the entire study period. However, these changes were not enough to make the HHI in 2010 statistically different from its value in 2006. Nevertheless, as with the small and medium-sized hospitals, the percentage of hospitals in the cohort without an EHR substantially reduced from 11.25% in 2006 to <1% in 2010.

Trends by geography

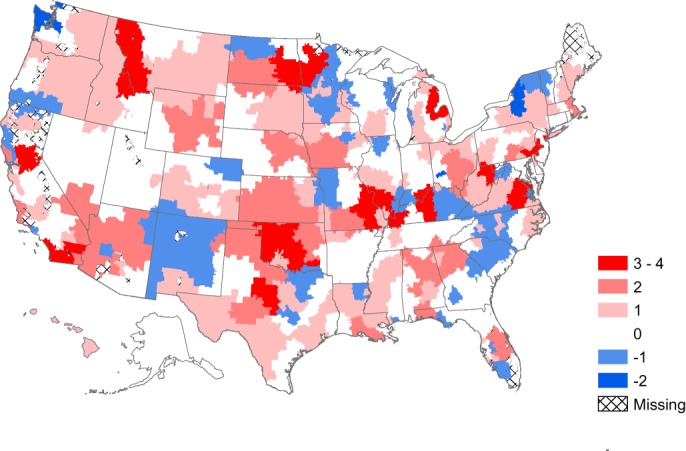

Figure 1 describes the change at the HRR level in the total number of vendors with EHRs operational, being installed, or under contract at a hospital. The first notable feature of this change-map is that not every HRR in the country saw an increase in EHR vendors. No change in the absolute number of vendors occurred in 42.0% of HRRs and several HRRs (13.1%) saw a decrease in the number of vendors during this time. The lack of change in the number of vendors present occurred in almost all of the HRRs included in Arkansas, Nevada, Utah, and Tennessee. In contrast, increasing vendor numbers were noticeable for HRRs in Alabama, Hawaii, Idaho, Kansas, Montana, Nebraska, Ohio, Oklahoma, and Wyoming.

Figure 1.

Change in the number of electronic health record vendors within healthcare referral regions, 2006–10.

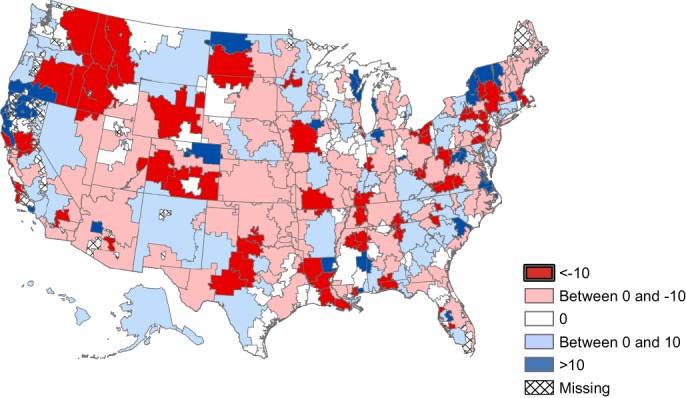

Of the 305 HRRs represented in the cohort, competition increased in half (49.5%) of the markets from 2006 to 2010 (figure 2). In these markets, the mean HHI decreased by 13.4 points (SD=1.26). In 23.3% of markets, the level of competition did not change. The HHI increased in 27.2% of the markets, signaling a move toward less competition.

Figure 2.

Change in the Herfindahl–Hirschman Index for the electronic health record market at the healthcare referral region level, 2006–10.

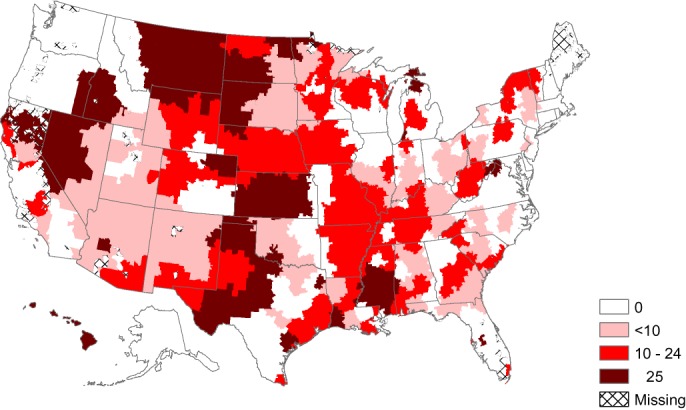

Figure 3 displays the percentage of hospitals by HRR using paper medical records in 2010. Clearly, some markets have made greater progress toward electronic record keeping than others. Specifically, healthcare markets where all hospitals had converted to electronic records tended to be on the coasts with higher persistence of paper in the Midwest and West. Also, the map illustrates that markets in which more than one in four hospitals still used paper records tended to be in very rural areas (eg, the western Dakotas, southern Mississippi, western Kansas, the Texas Panhandle, and northern Nevada).

Figure 3.

Percentage of hospitals relying on paper records at the healthcare referral region level, 2010.

Discussion

The structure of the EHR market is undergoing substantial changes. The trend in the number of vendors in each market is upwards. Most markets are becoming less concentrated and hospitals of all sizes are abandoning paper records. While this will be welcome news for EHR advocates, our analysis showed significant variations in the structure and changes in the EHR market in the USA since the introduction of certification and meaningful use. These variations highlight the particular challenges of small hospitals, the potential limits of these interventions to bring about market change, and the continuing roles for the states in HIT policy. Furthermore, our results provide important insights into the formulation of future health technology and EHR policies and suggest future lines of inquiry.

First, our results raise concerns about the performance and functioning of small hospitals. The EHR market showed the greatest change for the group of hospitals that need the most help. By most measures small hospitals are less IT savvy than larger hospitals. Small hospitals invest less in equipment and technology,28 are more likely to outsource key technical support functions,29 have more concerns about the capabilities of their IT staff,30 and their chief information officers have less training, are less experienced,31 and less often members of the executive team.32 Furthermore, small hospitals are more likely to employ a single vendor strategy, making their technology decisions all the more important, because that strategy has an effect on the entire organization.33 While rural and critical access hospitals are already targeted for specific assistance by regional extension centers, a broader geographical focus many be necessary to ensure the success of EHR adoption by small hospitals. Alternatively, strategic partnerships between hospitals may help smaller organizations ensure they have the technical expertise to navigate the changing and complex HIT market.34

Second, the changes in the EHR market for large hospitals are not readily apparent from summary measures of competition. Overall indicators of the EHR market suggest little change, on average. However, that stability appears to be a product of the dominance of the top five EHR vendors in the large hospital market, which counted 75–80% of all large hospitals as customers from year to year. The high baseline clinical data repository usage among large hospitals contributes further to the apparent stability by reducing the number of opportunities for vendors seeking customers among organizations switching away from a paper environment. As a result, the variation in the large hospital EHR market occurred among those vendors with fewer customers. The entrance and exits of these less common vendors tended to balance out annually and therefore did not result in substantial changes to our measures of competition.

Even with an overall shift toward EHR adoption, our examination showed that some individual markets experienced a decrease in the number of vendors present and a shift toward more concentration. This illustrates the explanatory power added by the inclusion of geography in the analysis. Beyond describing local variation, a comparison of all three maps shows that some of the changes in competition were not due to the entry of new vendors in the market, but due to a change in the number of customers for the existing vendors. For example, the number of vendors in central Arkansas did not change, but competition decreased, indicating that one of the existing EHR vendors simply gained market share. Conversely, portions of Utah saw a move toward greater competition without increases in the number of vendors. The primary implication of these regional variations is that changes in the marketplace, despite initiatives originating at the federal level, are not occurring uniformly or even in the same direction. We believe that this type of regional variation leaves open the potential need for the states to help shape local EHR markets. Current federal policies dominate HIT discussions and justifiably so, given their unprecedented scope and scale. However, several states have been very active in the support of HIT,35 and how states interact or augment federal policy is an avenue for future inquiry. At the very least, state level policy makers must not assume that all hospitals in their state will respond similarly to nationwide initiatives.

These results call for targeted HIT policies to be considered. In many respects, certification and meaningful use are essentially uniformly applied policy interventions. Putting aside the obvious and critical distinctions between EHRs for the inpatient and ambulatory settings, because it focuses on the capabilities of the technology and not the adopting organization, certification affects the entire hospital sector and country without any distinctions of organizational size, technological capabilities, or local environment. Likewise, while meaningful use contains both Medicare and Medicaid mechanisms and special considerations for critical access hospitals, all hospitals that become meaningful users are financially incentivized and will use EHRs that have to meet a common set of stage 1 requirements. However, the organizations adopting EHRs, vendor presence, competition, or geography of the markets described here are not changing uniformly. More targeted interventions may be required to ensure widespread transformation across all segments of the EHR market. For example, the current financial incentives and timelines did not favor an organization wishing to switch entirely to EHR products, which would definitely encourage changes in the market. Instead the clearest path for hospitals using paper was to buy and implement a certified EHR quickly, and for those using an existing non-certified EHR system was to wait for upgrades to a certified system from their current vendor (effectively all existing vendors have had their products certified). This latter option does not fundamentally alter the EHR market, and the former may not increase competition or the number of vendors in use as this analysis has demonstrated. Specific support or increased time to assist with switching costs, targeted state interventions, or additional support for hospitals to build in-house technical expertise could change the way in which hospitals select their certified EHR.

Lastly, our findings suggest both retrospective and forward-looking research questions. In view of the changes that have already transpired, this study justifies the needs for a formal evaluation of the effects of certification and meaningful use on the EHR market. Determining what role these policies have had in market change will be a complement to the current evaluations focusing on overall EHR adoption and on meeting meaningful use objectives.11 36 However, a quantitative evaluation of the effect of these interventions will require more historical data and consideration of many more determinants, including the influence of state policies. We expect that still more changes in the EHR market will take place. Market demand may shift again in response to the practice of regional extension centers of releasing preferred or recommended lists of EHR vendors. Although the work of regional extension centers is more targeted toward primary care physicians and even federally qualified health centers, these lists may serve as a constraining factor within states and regions.

Limitations

As noted already, the purpose of this study was not a formal evaluation of the effects of certification and meaningful use. Therefore, the observed trends may be due to other factors. Undoubtedly, mergers and acquisitions and hospitals abandoning self-developed systems in favor of a vendor-provided solution might explain some changes. However, that type of IT strategy change is not common. Also, because we did not specifically examine the role of state policies, we are unable to determine whether regional variation might be explained by the presence of supportive state policies or even by unique factors within areas. In addition, our analysis most likely does not count the whole number of EHRs vendors with products operational or under contract, because we used a basic measure of the EHR in order to be consistent across the study period. However, this measure excludes the possibility of a hospital using a modular EHR strategy, which would entail contracting with multiple vendors for services. Our analysis did not examine the quality, reputation, or long-term viability of any of the vendors in the marketplace, which has been a concern.37 Today, 65% of vendors with certified EHRs have fewer than 50 employees.38 Also, the generalizability of this study is limited as we looked only at hospitals and not ambulatory care providers or the growing service areas of long-term care and rehabilitation.

Our analysis only examined whether or not the EHR market was changing as envisioned by the architects of current federal policy and not whether hospitals were achieving meaningful use. Clearly, current federal policies intervened in the market with the ultimate objectives of innovation and other benefits.8 39 However, we have not examined whether any of those expected outcomes of changing the EHR market through meaningful use and certification actually occurred or if these changes were beneficial. Thus our analysis does not answer the following critical policy questions: Are more vendors in the market place good for hospitals and other healthcare organizations? Are these new vendors creating more innovative products? Are increases in competition changing product pricing? Our analysis does, however, demonstrate that questions such as these are all the more relevant as the EHR market is undergoing significant change.

Conclusions

The structure of the EHR market is undergoing substantial changes as desired by the proponents and architects of health information technology certification and meaningful use. However, these transformations are not uniform for all hospitals or all parts of the country. A comprehensive description, including products, buyers, and geography, better explains how the market is functioning, which in turn stimulates the reformulation of key policy questions and how they will be evaluated.

Supplementary Material

Acknowledgments

The author's thank Jose Millan for his cartography skills and HIMSS Analytics™ for access to the data.

Footnotes

Contributors: JV conceived the research question, analyzed the data, and led the drafting of the manuscript. JY led the regression analyses and drafted the manuscript. BHB led the geographic analysis and drafted the manuscript. All authors approved the final version of the manuscript.

Competing interests: None.

Ethics approval: Georgia Southern University institutional review board.

Provenance and peer review: Not commissioned; externally peer reviewed.

References

- 1. Ford EW, Menachemi N, Phillips MT. Predicting the adoption of electronic health records by physicians: when will health care be paperless? J Am Med Inform Assoc 2006;13:106–12 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2. Kleinke JD. Dot-Gov: market failure and the creation of a national health information technology system. Health Aff 2005;24:1246–62 [DOI] [PubMed] [Google Scholar]

- 3. Middleton B. Achieving U.S. health information technology adoption: the need for a third hand. Health Aff 2005;24:1269–72 [DOI] [PubMed] [Google Scholar]

- 4. Certification Commission for Health Information Technology. Organization and Governance. 2011. http://www.cchit.org/about/organization (accessed 8 Aug 2011). [Google Scholar]

- 5. Classen DC, Avery AJ, Bates DW. Evaluation and certification of computerized provider order entry systems. J Am Med Inform Assoc 2007;14:48–55 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6. Office of the National Coordinator for Health Information Technology Goals Of Strategic Framework. 2004. http://www.hhs.gov/healthit/goals.html (accessed 18 Nov 2010). [Google Scholar]

- 7. Department of Health & Human Services Medicare and Medicaid Programs; Electronic Health Record Incentive Program; Proposed Rule. Fed Regist 2010;75:1844–2011 [PubMed] [Google Scholar]

- 8. Blumenthal D. HIMSS'11 Keynote Address. Orlando, FL: HIMSS'11, 2011 [Google Scholar]

- 9. Conn J. New ONC head Mostashari Outlines His Priorities. 2011. http://www.modernhealthcare.com/article/20110413/NEWS/304139950 (accessed 10 Oct 2011). [Google Scholar]

- 10. Brady D. Farzad Mostashari on Digitizing Health Records. 2011. http://www.businessweek.com/magazine/farzad-mostashari-on-digitizing-health-records-09222011.html (accessed 10 Oct 2011). [Google Scholar]

- 11. Jha AK, DesRoches CM, Kralovec PD, et al. A progress report on electronic health records in U.S. Hospitals. Health Aff 2010;29:1951–7 [DOI] [PubMed] [Google Scholar]

- 12. US Department of Health & Human Services Surveys Show Significant Proportions Of Hospitals And Doctors Already Plan To Adopt Electronic Health Records And Qualify For Federal Incentive Payments. 2011. http://www.hhs.gov/news/press/2011pres/01/20110113a.html (accessed 25 Oct 2011). [Google Scholar]

- 13. The Office of the National Coordinator for Health Information Technology Adoption and Meaningful Use Of Electronic Health Records Support Programs Carried Out Under HITECH. 2011. http://healthit.hhs.gov/portal/server.pt/gateway/PTARGS_0_0_4381_1238_15609_43/http%3B/wci-pubcontent/publish/onc/public_communities/p_t/resources_and_public_affairs/fact_sheets/fact_sheets_portlet/files/aspa_0386_20110525_onc_fs_meaningful_use_v01.pdf (accessed 11 Aug 2011). [Google Scholar]

- 14. The Office of the National Coordinator for Health Information Technology. Certifed Health IT Product List. 2010. http://onc-chpl.force.com/ehrcert [Google Scholar]

- 15. Healthcare Information & Management Systems Society. HIMSS Online Buyer's Guide. 2012. http://onlinebuyersguide.himss.org/ [Google Scholar]

- 16. Certification Commission for Health Information Technology. CCHIT Certified® Products. 2012. http://www.cchit.org/products/cchit [Google Scholar]

- 17. Brown N. Driving EMR adoption: making EMRs a Sustainable, Profitable Investment. Health Manag Technol 2005;26:48–7 [PubMed] [Google Scholar]

- 18. Black Book Rankings Top EHR & EMR Vendors. 2011. http://www.blackbookrankings.com/ [Google Scholar]

- 19. Amarasingham R, Plantinga L, Diener-West M, et al. Clinical information technologies and inpatient outcomes: a multiple hospital study. Arch Intern Med 2009;169:108–14 [DOI] [PubMed] [Google Scholar]

- 20. DesRoches CM, Campbell EG, Rao SR, et al. Electronic health records in ambulatory care—a national survey of physicians. N Engl J Med 2008;359:50–60 [DOI] [PubMed] [Google Scholar]

- 21. The Trustees of Dartmouth College The Dartmouth Atlas of Health Care. 2011. http://www.dartmouthatlas.org/tools/downloads.aspx (accessed 13 Aug 2011). [Google Scholar]

- 22. Dartmouth Medical School CfECS The Dartmouth Atlas of Health Care 1998. Chicago, IL: American Hospital Publishing, Inc., 1998 [PubMed] [Google Scholar]

- 23. Chen J, Krumholz HM, Wang Y, et al. Differences in patient survival after acute myocardial infarction by hospital capability of performing percutaneous coronary intervention: implications for regionalization. Arch Intern Med 2010;170:433–9 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 24. Mittler JN, Landon BE, Fisher ES, et al. Market variations in intensity of medicare service use and beneficiary experiences with care. Health Serv Res 2010;45:647–69 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 25. Santerre RE, Neun SP. Health Economics: Theories, Insights, and Industry Studies. 4th edn Manson, OH: Thomson South-Western, 2007 [Google Scholar]

- 26. Kazley AS, Ozcan YA. Organizational and environmental determinants of hospital EMR adoption: a National study. J Med Syst 2007;31:375–84 [DOI] [PubMed] [Google Scholar]

- 27. Rabe-Hesketh S, Skrondal A. Multilevel and Longitudinal Modeling Using Stata. 2nd edn College Station, Tx: Stata Press, 2008 [Google Scholar]

- 28. Li L, Benton WC. Hospital technology and nurse staffing management decisions. J Operations Manag 2006;24:676–91 [Google Scholar]

- 29. Menachemi N, Burke D, Diana M, et al. Characteristics of hospitals that outsource information system functions. J Healthc Inf Manag 2005;19:63–9 [PubMed] [Google Scholar]

- 30. Schoenman J. Small, Stand-Alone, and Struggling: The Adoption Of Health Information Technology By Rural Hospitals: NORC Walsh Center for Rural Health Analysis. Chicago, IL: The Walsh Center for Rural Health Analysis, 2007 [Google Scholar]

- 31. Burke D, Menachemi N, Brooks R. Health care CIOs: assessing their fit in the organizational hierarchy and their influence on information technology capability. Health Care Manag (Frederick) 2006;25:167–72 [DOI] [PubMed] [Google Scholar]

- 32. Scottsdale Institute-HIMSS Analytics Healthcare The Changing Landscape of Healthcare IT Management and Governance. Chicago, IL: HIMSS Analytics, 2005 [Google Scholar]

- 33. Burke DE, Yu F, Au D, et al. Best of breed strategies: hospital characteristics associatecd with organizational HIT strategy. J Healthc Inf Manag 2009;23:46–51 [PubMed] [Google Scholar]

- 34. Goodman KW, Berner ES, Dente MA, et al. Challenges in ethics, safety, best practices, and oversight regarding HIT vendors, their customers, and patients: a report of an AMIA special task force. J Am Med Inform Assoc 2011;18:77–81 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 35. Mertz K. Health Information Technology 2007 and 2008 State Legislation. Washington, DC: National Conference of State Legislatures, 2008 [Google Scholar]

- 36. Hogan SO, Kissam SM. Measuring meaningful use. Health Aff 2010;29:601–6 [DOI] [PubMed] [Google Scholar]

- 37. Middleton B, Hammond WE, Brennan PF, et al. EHR adoption: how to get there from here. Recommendations based on the 2004 ACMI Retreat. J Am Med Inform Assoc 2005;12:13–19 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 38. Office of the National Coordinator for Health Information Technology Electronic health record (EHR) certification program. 2011. http://healthit.hhs.gov/portal/server.pt/document/953720/ehr_certification_program_data_sheett_pdf (accessed 29 Aug 2011). [Google Scholar]

- 39. Zigmond J. Mostashari: efficient market is biggest driver of innovation. 2011. http://www.modernhealthcare.com/article/20110427/NEWS/304279988/ [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.