The experiences of insured cancer patients requesting copayment assistance and the impact of health care expenses on well-being and treatment are examined. Insured patients undergoing cancer treatment and seeking copayment assistance were found to experience considerable subjective financial burden and were found to alter care to defray out-of-pocket expenses.

Keywords: Neoplasms, Cost, Chemotherapy, Indigency, Medical, Quality of health care, Financial support

Learning Objectives

Describe the experiences of insured cancer patients requesting copayment assistance in order to better understand the challenges of underinsurance.

Describe the impact of costs on the well being of insured cancer patients.

Evaluate the impact of costs on the treatment received by insured cancer patients.

Abstract

Purpose.

Cancer patients carry rising burdens of health care-related out-of-pocket expenses, and a growing number of patients are considered “underinsured.” Our objective was to describe experiences of insured cancer patients requesting copayment assistance and to describe the impact of health care expenses on well-being and treatment.

Methods.

We conducted baseline and follow-up surveys regarding the impact of health care costs on well-being and treatment among cancer patients who contacted a national copayment assistance foundation along with a comparison sample of patients treated at an academic medical center.

Results.

Among 254 participants, 75% applied for drug copayment assistance. Forty-two percent of participants reported a significant or catastrophic subjective financial burden; 68% cut back on leisure activities, 46% reduced spending on food and clothing, and 46% used savings to defray out-of-pocket expenses. To save money, 20% took less than the prescribed amount of medication, 19% partially filled prescriptions, and 24% avoided filling prescriptions altogether. Copayment assistance applicants were more likely than nonapplicants to employ at least one of these strategies to defray costs (98% vs. 78%). In an adjusted analysis, younger age, larger household size, applying for copayment assistance, and communicating with physicians about costs were associated with greater subjective financial burden.

Conclusion.

Insured patients undergoing cancer treatment and seeking copayment assistance experience considerable subjective financial burden, and they may alter their care to defray out-of-pocket expenses. Health insurance does not eliminate financial distress or health disparities among cancer patients. Future research should investigate coverage thresholds that minimize adverse financial outcomes and identify cancer patients at greatest risk for financial toxicity.

Implications for Practice:

The number of insured patients is increasing, but insured patients are paying more out of pocket for cancer care due to increased cost sharing. As a result, the number of underinsured cancer patients is increasing. Patients are faced with greater out-of-pocket health care costs, but treatment decision making is often made without consideration of these expenses. In our study, insured patients undergoing cancer treatment and seeking copayment assistance experienced considerable subjective financial burden, and they altered care to defray out-of-pocket expenses. Health insurance does not eliminate financial distress or health disparities among cancer patients. Financial distress or “financial toxicity” as a result of disease or treatment decisions might be considered analogous to physical toxicity and might be considered a relevant variable in guiding cancer management. Understanding how and among whom to best measure financial distress is critical to the design of future interventional studies.

Introduction

Cancer treatment has made remarkable strides, yielding improvements in patient outcomes, but those improvements have come at increasing costs [1]. As health care costs increase, insurers have shifted some of the cost burden to patients through higher deductibles, rising copayments, and coinsurance, resulting in higher out-of-pocket expenses [2]. These out-of-pocket–related expenses are higher among patients with cancer than among patients with other conditions [3, 4]. As a result of growing expenses, even patients with insurance may require financial assistance from government or nonprofit national copayment assistance organizations to guarantee access to therapy and to mitigate the financial burden of cancer care [5]. Though the number of insured patients is estimated to increase in the era of the Affordable Care Act, rising out-of-pocket costs dispute the adequacy of insurance for providing affordable cancer care [6, 7]. Patients who carry insurance but still pay a significant portion of health care costs out of pocket are considered underinsured [1].

In the context of increasing health care costs, we sought to better understand the degree of financial hardship and the impact of cancer costs on the well-being of underinsured cancer patients. Out-of-pocket expenses are one measure of underinsurance, particularly when those expenses impact patient well-being, treatment choices, or outcomes [8, 9]. We can view the adverse impacts of out-of-pocket health care costs as a form of treatment-related toxicity, or “financial toxicity.” As with physical toxicity resulting from cancer treatment, certain patients might be predisposed to greater financial toxicity than others. Though prior work has investigated the burden of out-of-pocket expenses among cancer patients, we sought to specifically evaluate the prevalence and impact of financial toxicity among a high-risk group of patients who had applied for copayment assistance to better understand the challenges posed by underinsurance. Hence, we conducted an exploratory pilot study to evaluate the degree of objective financial burden and subjective financial burden among insured cancer patients seeking copayment assistance through a national nonprofit foundation and among a comparison cohort of patients with cancer recruited at our academic medical center.

Materials and Methods

Participants

Eligible participants were patients with solid tumors actively receiving chemotherapy or hormonal therapy. Participants were recruited from two sources: the HealthWell Foundation, a 501(c)(3) nonprofit organization that assists patients with prescription drug copayments, coinsurance, and premium payments, and Duke University Medical Center. Patients were referred to HealthWell by their health care providers, other copayment assistance foundations, reimbursement hotlines, pharmacies, or social workers [10]. Between June 2010 and May 2011, HealthWell staff asked patients who contacted the Foundation for financial assistance if they were interested in participating in cost-related research. Potential participants were informed that receipt of financial assistance from HealthWell would be independent of their decision to participate in research. For those who agreed, HealthWell forwarded contact information to investigators at Duke, who then contacted patients for eligibility screening. A convenience sample of adult patients receiving chemotherapy or endocrine therapy for solid tumors at Duke University Medical Center were recruited by physician referral during routine clinic visits; the primary intent of enrolling these patients was to provisionally compare the subjective financial experience and objective financial burden among a cohort of patients seeking copayment assistance with those of an unselected sample of patients at an academic cancer center. A minority of patients recruited at Duke reported seeking copayment assistance and they were analyzed as part of the copayment assistance cohort. We conducted a sensitivity analysis comparing HealthWell participants with Duke participants (regardless of copayment application status) and found no notable differences in results.

Study Design

This was an exploratory, observational study of self-reported, treatment-related costs (objective financial burden) and patient-reported subjective financial burden among patients with cancer seeking copayment assistance. All participants completed a baseline survey at the time of enrollment assessing sociodemographics and strategies used to cope with out-of-pocket expenses. Questions pertaining to cost-coping strategies were based on a study by Schrag et al. [11].

Beginning 1 month after the baseline survey, participants completed monthly cost diaries for up to 4 months. Initially, the study included four weekly cost diaries for the first month, followed by three monthly diaries. As a result of low participation in the weekly diary component and perceived burden on participants, we amended the study design to four monthly diaries. Patients were asked to estimate their monthly cancer-related out-of-pocket expenses (objective financial burden), including prescription and nonprescription medications, doctor visit copayments, insurance premiums, travel, special diets, alternative therapies, devices and equipment, time off work, and other services, such as child care. Insurance premiums were included in the calculation of out-of-pocket expenses, consistent with a landmark survey on health care expenses and underinsurance [1].

The baseline survey and cost diary items were developed and piloted in focus groups of patients undergoing cancer treatment at Duke. All surveys were completed either online or on paper, based on participant preference. Duke University Health System's Institutional Review Board approved this study.

Statistical Analyses

Descriptive statistics summarized sociodemographics, disease and treatment characteristics, out-of-pocket expenses, and cost-coping strategies. Costs related to travel were estimated by multiplying miles traveled for cancer care by $0.51, the 2011 mileage reimbursement rate set by the Internal Revenue Service. We used the following equation to determine indirect costs resulting from lost wages: [(hours worked if healthy) − (hours actually worked)] × federal minimum wage of $7.25.

We estimated the proportion of underinsured participants by first converting annual income to a monthly income range (e.g., $40,000–$59,999/year was converted to $3333–$4999/month). For patients who reported income in either the “less than $20,000/year” or “greater than $60,000/year” categories, we assumed $20,000 or $60,000, respectively, as their annual income. We then divided the median out-of-pocket expenses reported by each participant by high and low values of their monthly income range. Similar methods have been used previously to report proportion of income spent on health care [12]. We calculated the proportion of underinsured patients, with underinsurance defined as insured patients who spend at least 10% of their annual household income out of pocket on health care [1].

χ2 tests were used to assess differences between patients who applied for copayment assistance and those who did not. Logistic regression was used to assess the relationship between sociodemographics and subjective financial burden. Variables were selected for inclusion in multivariate models using a combination of the statistical selection criterion of p < .25 in unadjusted analyses and clinical relevance. A p value < .05 in the final model was considered statistically significant. Pearson correlations were calculated to determine the degree of correlation between the use of cost-coping strategies and subjective financial burden.

Results

Cohort Characteristics

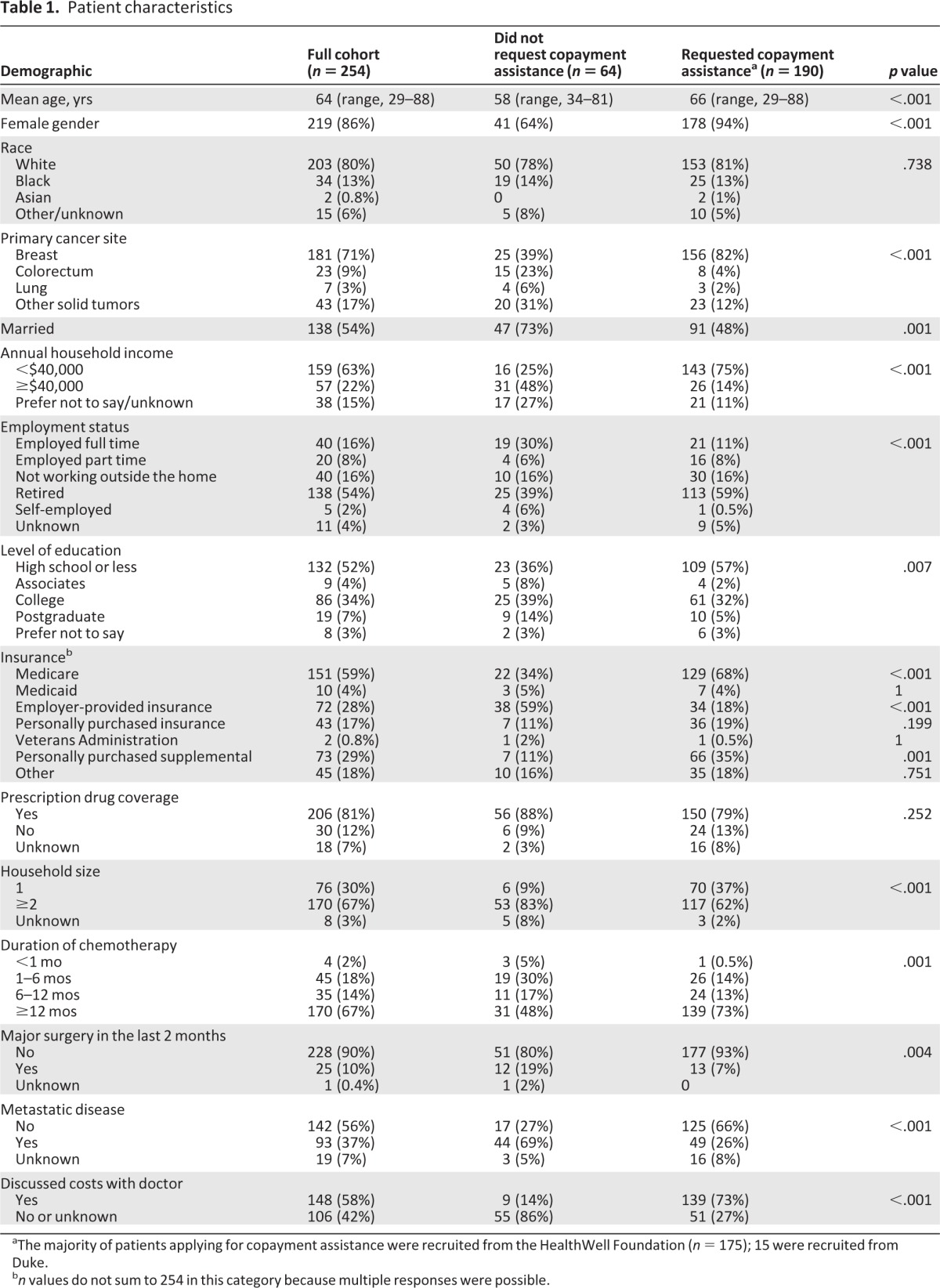

Between July 2010 and July 2011, among 677 eligible patients, 258 agreed to participate and completed baseline surveys, representing a response rate of 38% (Fig. 1). Nonresponders included those who declined to participate and those who agreed but did not complete a baseline survey. Four uninsured participants were excluded from this analysis, which focused on insured participants, thereby resulting in an effective sample size of 254. Participants were enrolled nationwide (Fig. 2), with 175 (68%) recruited via HealthWell and the remainder recruited at Duke. The mean and median age was 64 years (Table 1). Eighty percent were white, 86% were women, and 71% had breast cancer. Overall, 81% carried prescription drug coverage. Fifty-eight percent reported discussing costs with their doctor.

Figure 1.

Derivation of cohorts. (A): Derivation of HealthWell study cohort. (B): Derivation of Duke study cohort. Although ineligibility reason was not recorded, the only eligibility criterion was actively receiving hormonal therapy or chemotherapy.

Figure 2.

Participants by state.

Table 1.

Patient characteristics

aThe majority of patients applying for copayment assistance were recruited from the HealthWell Foundation (n = 175); 15 were recruited from Duke.

bn values do not sum to 254 in this category because multiple responses were possible.

One hundred ninety (75%) participants applied for prescription drug copayment assistance. Among copay applicants, 174 (92%) were enrolled via HealthWell. As described in Table 1, participants who applied for copayment assistance differed in many regards from those who did not apply.

Out-of-Pocket Expenses

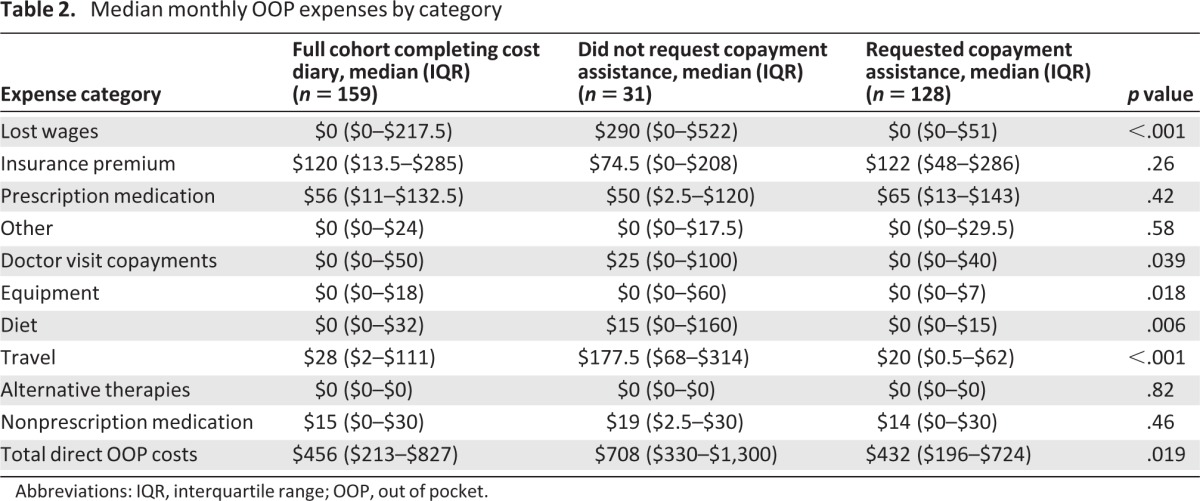

Sixty-three percent of participants completed a baseline survey and at least one cost diary, 32% completed two diaries, 20% completed three diaries, and 13% of patients completed a baseline survey and all four cost diaries. Cost calculations focused on the 159 (63%) participants who completed at least one cost diary. Excluding indirect costs, participants spent a median of $456/month (interquartile range, $213–$827) out of pocket on cancer care-related expenses. Table 2 lists the median amount spent per category of expense. The median proportion of income spent out of pocket did not differ significantly between copayment applicants (17%; range, 8%–35%) and nonapplicants (15%; range, 6%–28%; p = .31).

Table 2.

Median monthly OOP expenses by category

Abbreviations: IQR, interquartile range; OOP, out of pocket.

Per an accepted definition of underinsurance (insured patients who spend greater than 10% of their annual household income out of pocket on health care [1]), 55% of those completing cost diaries were underinsured, compared with 22% of all U.S. adults [1]. In a sensitivity analysis using a more conservative 20%-of-income threshold, 35% of participants were underinsured, compared with 13% of U.S. adults, using this higher threshold [3]. However, copayment assistance applicants were more likely than nonapplicants to be underinsured using the 10% threshold (59% vs. 39% underinsured; p = .042), but not using the 20% threshold (38% vs. 26% underinsured; p = .055).

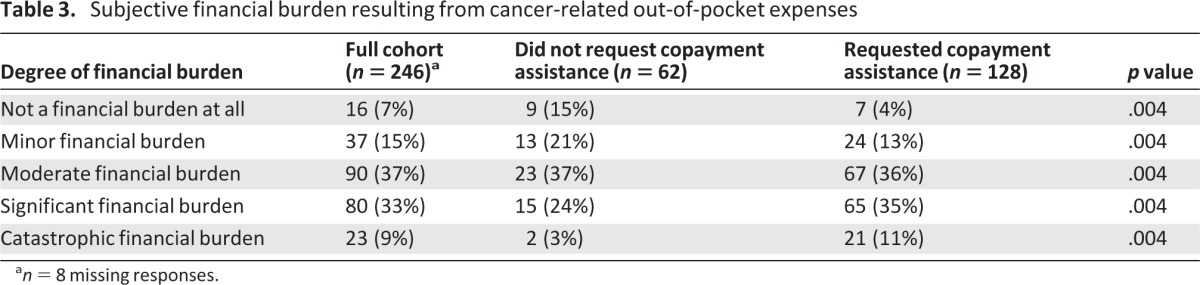

Participants reported their subjective financial burden resulting from cancer-related out-of-pocket expenses (Table 3). Among the 250 participants who responded to this item, 42% reported a significant or catastrophic burden. χ2 analysis revealed that, compared with nonapplicants, copayment assistance applicants were more likely to report a higher financial burden (Table 3) (p = .004). Figure 3 presents a multivariate analysis assessing the characteristics associated with a high financial burden. In an adjusted analysis, older age and a smaller household size were associated with less financial burden. Applying for copayment assistance and communicating with physicians about the cost of care were associated with greater subjective financial burden.

Table 3.

Subjective financial burden resulting from cancer-related out-of-pocket expenses

an = 8 missing responses.

Figure 3.

Characteristics associated with greater financial burden in an adjusted multivariate analysis (n = 195). Variables considered in the univariate analysis included gender, application for copayment assistance, presence of metastatic disease, education, age, income (excluded from the multivariate analysis because of 15% missing), race, marital status, employment, household size, recent major surgery, communication with doctor about costs, insurance type, out-of-pocket payments for health insurance, presence of prescription drug coverage, and duration of chemotherapy.

Abbreviations: CI, confidence interval; OR, odds ratio.

Subjective Financial Burden and Well-Being

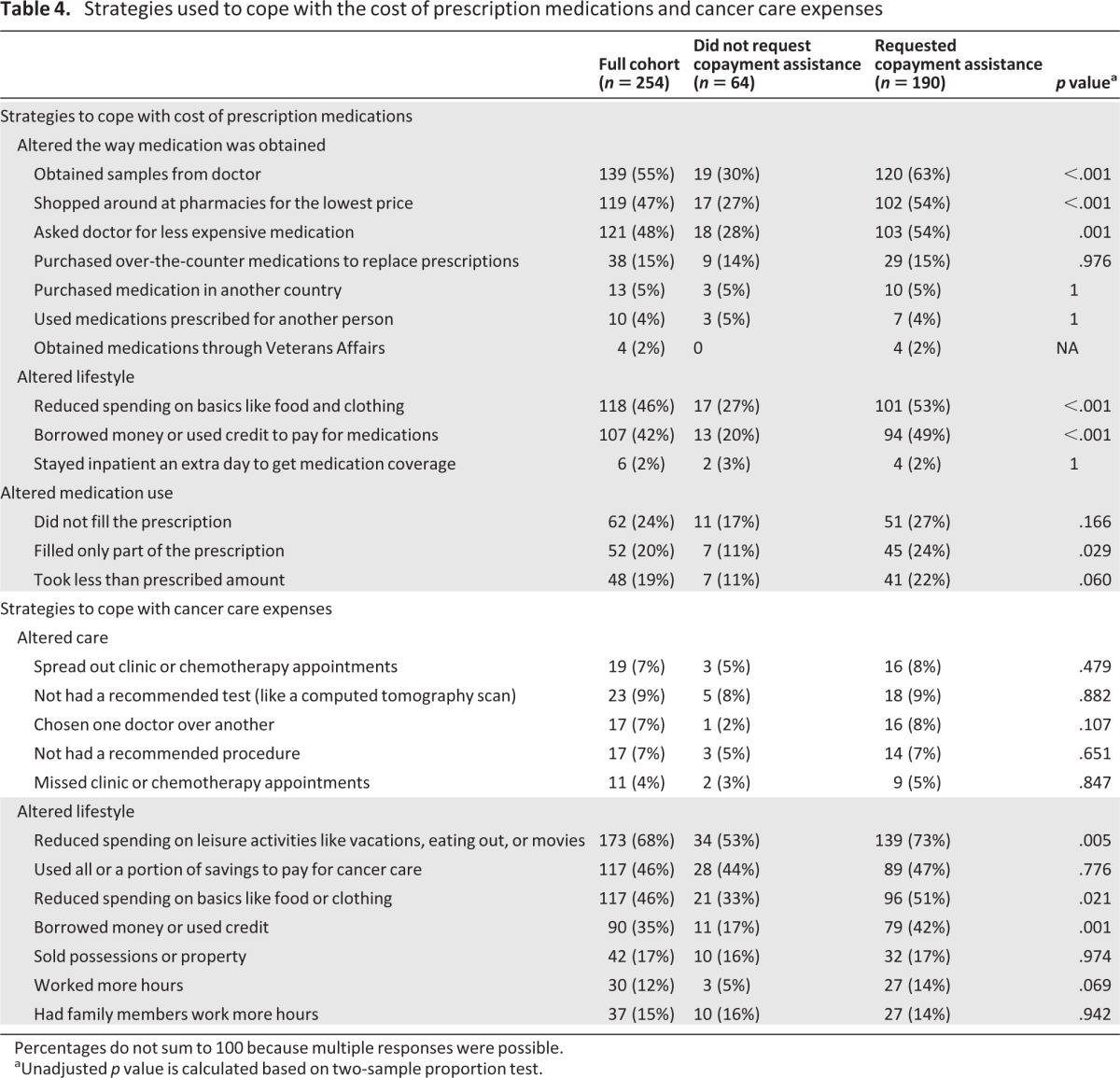

Participants altered their lifestyles to afford prescription medications and cancer care in general (Table 4). Overall, 68% cut back on leisure activities, 46% reduced spending on basics like food and clothing, 46% used their savings, and 17% sold possessions or property, all to help defray cancer care-related out-of-pocket expenses. Copayment assistance applicants were more likely than nonapplicants to employ at least one strategy to cope with costs (98% vs. 78%; p < .001). Among those who employed at least one strategy, copayment assistance applicants were more likely to reduce spending on leisure activities (p = .005), reduce spending on food or clothing (p = .021), and borrow money or use credit (p = .001).

Table 4.

Strategies used to cope with the cost of prescription medications and cancer care expenses

Percentages do not sum to 100 because multiple responses were possible.

aUnadjusted p value is calculated based on two-sample proportion test.

Using cost-coping strategies to help pay for cancer care was positively correlated with reporting a high subjective financial burden (r = 0.49; p < .01). We further examined this correlation by focusing on each individual coping strategy (supplemental online Table 1). All strategies except “Worked more hours to help pay for your cancer care” were associated with high subjective financial burden.

Subjective Financial Burden and Quality of Care

As one of many strategies used to alleviate the financial burden of cancer care, participants reported noncompliance with care (Table 4). Overall, 20% took less than the prescribed amount of medication, 19% filled only part of a prescription, and 24% avoided filling prescriptions at all. A smaller portion of patients avoided procedures (7%) or tests (9%) because of costs. Seven percent spread out chemotherapy or clinic appointments, and 4% skipped appointments to save money.

Discussion

This study provides a timely window into the financial impact of cancer care, with a particular focus on insured patients who applied for copayment assistance. In this select cohort of high-risk patients, participants experienced high subjective financial burden and altered their lifestyles and care to defray out-of-pocket expenses.

These data provide one of the first evaluations of the negative personal financial impact of cancer care among the underinsured—a concept we call “financial toxicity.” Though we found substantial potential for financial toxicity among patients with cancer, it was not seen exclusively among those who sought copayment assistance. The broader range of patients at risk for subjective financial burden suggests a need to better assess cancer-related financial hardship and to expand educational interventions targeted to both clinicians and patients.

Who Is at Risk for Financial Burden?

Recent studies have detailed the burden of health care-related out-of-pocket expenses [3, 4, 8, 9, 12–14]. Our study is among the first to evaluate the subjective financial burden and cost-related experiences of insured cancer patients who applied for copayment assistance. Consistent with recent evidence, we found that younger patients and those with larger households were at greater risk for financial burden. As would be expected, applying for copayment assistance was also associated with greater subjective financial burden. However, the median proportion of income spent out of pocket did not differ significantly between copayment applicants and nonapplicants. This suggests that measuring out-of-pocket expenses as a proportion of income might not be sufficient to capture objective financial burden, and some subjective assessment should also be considered to identify patients who may benefit from intervention.

How Do Expenses Impact Patient Well-Being?

Participants struggling to pay for their cancer treatment altered their lifestyles considerably to defray out-of-pocket expenses. Our results are consistent with the limited literature addressing how out-of-pocket expenses impact cancer patients' lives [9, 15]. We found that copayment assistance applicants were more likely than nonapplicants to employ at least one lifestyle-altering strategy to cope with costs. However, the direction of the association is unclear, and we did not directly assess the reason for seeking copayment assistance at the time of application. Given that copayment assistance is a poorly understood support mechanism, further work is needed to assess the triggers for requesting assistance and the outcomes associated with receiving (or not receiving) assistance.

The similarities and differences among participants in terms of which cost-saving strategies were employed provide meaningful insights into how patients alter their behavior when confronted with high out-of-pocket health care costs. Both copayment applicants and nonapplicants were equally likely to sell possessions, work longer hours, have family members work longer hours, and use their savings; these behaviors are particularly meaningful because the median age for all participants approached retirement age. However, copayment assistance applicants were more likely than nonapplicants to reduce spending on food, clothing, and leisure activities to help pay for care. This pattern of coping strategies suggests that, as financial burden increases, patients work more and exhaust savings before cutting back on daily expenses. Furthermore, all cost-coping strategies except “Worked more hours to help pay for your cancer care” were associated with high subjective financial burden. This exploratory analysis suggests that, for some patients, cutting back on leisure activities to pay for cancer care might be as distressing as spending savings. Future research should address how patients prioritize lifestyle changes and alter financial behaviors in the face of significant out-of-pocket expenses.

How Do Expenses Impact Cancer Treatment?

Participants reported taking less medication than prescribed, replacing prescription medications with over-the-counter drugs, and taking medications prescribed for others in order to defray costs. A minority of participants reported skipping appointments or declining procedures because of costs. These findings confirm a disturbing link between costs and medication compliance [9, 16]. Our results suggest that the risk for noncompliance is not isolated to patients applying for drug copayment assistance. To the extent that cost sharing is intended to boost patient-directed decision making in health care and increase the value of health care, these findings suggest a potential for unintended adverse consequences that may result in higher downstream health care costs [17].

Our data suggest that the costs of care are insufficiently addressed in discussions between patients and physicians; over one quarter of copayment applicants did not discuss costs with their doctor. Our sample is saturated with those applying for financial assistance, which in turn was associated with a higher likelihood of discussing costs with a doctor. In the general population, in which the rates of financial assistance application are lower, costs might be discussed at a lower rate than those described in our study. Given the high levels of financial burden identified in our study population, our data might underestimate the number of patients who do not discuss the costs of cancer care in the clinic. Of note, we did not ask participants if they wanted to discuss costs or if they wanted costs to play a role in treatment decision making. Research suggests that oncologists feel that the costs of care are important, but that they are poorly prepared to discuss costs with patients in the clinic. Our findings—in conjunction with calls from the American Society of Clinical Oncology to address the costs of cancer care in the clinic—suggest a need for further efforts at clinician education in this area [18].

What little is known about patient preferences regarding cost discussions is based on the general medicine literature [19], but those findings might not apply to cancer treatment. In treating hypertension, for example, patients are more willing to modify treatment based on costs because a broad cost spectrum of drugs is available to treat hypertension. However, for any given tumor type, a broad spectrum of anticancer therapies is not necessarily available to patients and providers, so the same willingness to alter treatment might not apply [20, 21]. Future studies should address patients' willingness to include out-of-pocket costs in treatment decision making and patients' understanding of the potential implications of doing so.

Our findings are subject to limitations. There are several sources of bias that may limit the generalizability of this study. First, we recruited the majority of patients through the HealthWell Foundation. This population is not representative of all adult patients with cancer, and as shown through comparison with Duke clinic patients, it does not represent all patients who are underinsured or facing financial hardship. However, this limited sample does provide one of the first windows into the demographics and financial experiences of patients with cancer seeking copayment assistance. Similarly, the Duke participants were selected as a convenience sample to allow for comparison between patients applying to HealthWell and an unselected population, but they are not representative of patients seeking oncology care in the community setting, or even of all patients seeking care at academic cancer centers. However, the fact that financial hardship and underinsurance were prevalent even in this select population suggests that the financial challenges identified here are likely to be widespread.

In terms of the broader generalizability of our sample, Duke study participants were similar to all Duke Cancer Center patients receiving treatment in terms of age, race, and insurance type (Sarah Bacik, personal communication, 2012). HealthWell participants were predominantly white women with breast cancer. They had a mean age of 66 years. HealthWell reports that the average age of applicants is >65 years, and 67% of those applying for assistance are women [10]. Assistance is provided on the basis of specific diseases, not cancer in general. At the time of our study, HealthWell had funds to support patients with breast, colorectal, and lung cancer but not prostate cancer; this may have contributed to the gender and disease imbalance in our sample.

In addition, the baseline survey response rate was 38%, which introduces the possibility of nonresponse bias. However, this exploratory study on personal finances focused on elderly cancer patients facing financial hardship. Surveying low-income or financially distressed populations is challenging, as evidenced by the low response rates of other survey studies focused on these populations [9, 22, 23].

Our sample was enriched with underinsured patients, though one in five adults in the U.S. is underinsured [1]. Although not all patients in our sample met some of the conventional definitions of underinsurance, these data are among the first to evaluate how insured cancer patients manage financial burdens. Not all patients completed a cost diary: 63% of respondents completed at least one monthly cost diary and only 13% completed all four. Those who did not were more likely to be older, have Medicare, and have received financial assistance. This suggests that our measured out-of-pocket expenses are possibly underestimated. Our subjective measure of financial burden was not validated. It was piloted, and high financial burden was correlated with the use of cost-saving strategies. Finally, reported costs might have included those incurred from health care unrelated to cancer, but participants were directed to limit their cost reporting to cancer care-related costs. This study focused on costs related to cancer care, but copayment assistance foundations provide funds for treatment of other chronic illnesses [10]. Future research should investigate whether or not the concept of financial toxicity also applies to the treatment of other chronic diseases.

Conclusion

Insured patients undergoing cancer treatment and seeking copayment assistance experience a considerable subjective financial burden. They may exhaust their savings, take on excessive debt, and face choices between health care and other basic necessities to save money. Insured patients who did not apply for copayment assistance also faced financial hardship, suggesting that those applying for financial assistance represent the tip of the iceberg of patients with financial difficulties. Financial distress or “financial toxicity” as a result of disease or treatment decisions might be considered analogous to physical toxicity and might be considered a relevant variable in guiding cancer management. Understanding how and among whom to best measure financial distress is critical to the design of future interventional studies. This pilot study is the first to assess financial distress among insured patients applying for copay assistance. Our data suggest that copayment assistance applicants are enriched for, but not the exclusive bearers of, financial distress. These data also confirm the feasibility of measuring financial distress among copayment assistance applicants, with potential relevance to fields outside oncology. These data will support the design of a study assessing the differential impact of financial distress on treatment-related decision making throughout the continuum of cancer care.

See www.TheOncologist.com for supplemental material available online.

This article is available for continuing medical education credit at CME.TheOncologist.com.

Supplementary Material

Acknowledgments

We gratefully acknowledge data collection and management assistance provided by Greg Samsa, Ph.D., Robin Fowler, Devdutta Warhadpande, Agbessi Gblokpor, and Joe Kelly.

This manuscript was presented in part as an oral presentation at the 2011 American Society of Clinical Oncology Annual Meeting, Chicago, IL.

This study was funded by the HealthWell Foundation.

Footnotes

EDITOR'S NOTE: See the related editorial on pages 347–349 of this issue.

Author Contributions

Conception/Design: S. Yousuf Zafar, Jeffrey M. Peppercorn, Deborah Schrag, Donald H. Taylor, Amy P. Abernethy

Provision of study material or patients: S. Yousuf Zafar, Jeffrey M. Peppercorn, Deborah Schrag

Collection and/or assembly of data: S. Yousuf Zafar, Amy M. Goetzinger, Xiaoyin Zhong, Amy P. Abernethy

Data analysis and interpretation: S. Yousuf Zafar, Jeffrey M. Peppercorn, Deborah Schrag, Donald H. Taylor, Amy M. Goetzinger, Xiaoyin Zhong, Amy P. Abernethy

Manuscript writing: S. Yousuf Zafar, Jeffrey M. Peppercorn, Deborah Schrag, Donald H. Taylor, Amy M. Goetzinger, Xiaoyin Zhong, Amy P. Abernethy

Final approval of manuscript: S. Yousuf Zafar, Jeffrey M. Peppercorn, Deborah Schrag, Donald H. Taylor, Amy M. Goetzinger, Xiaoyin Zhong, Amy P. Abernethy

Disclosures

S. Yousuf Zafar: Genentech (H); HealthWell Foundation (RF); Jeffrey M. Peppercorn: GlaxoSmithKline (E [spouse]); Genentech (C/A); Novartis (RF); Ownership Interest: GlaxoSmithKline (OI [spouse]); Amy P. Abernethy: Orange Leaf Associates, Advoset (E); Novartis, Pfizer (C/A); Pfizer, Helsinn, Amgen, Kanglaite, Alexion, Biovex, DARA, MiCo (RF). The other authors indicated no financial relationships.

Section editor: Thomas G. Roberts, Jr.: Farallon Capital Management LLC (E)

Reviewer “A”: None

(C/A) Consulting/advisory relationship; (RF) Research funding; (E) Employment; (H) Honoraria received; (OI) Ownership interests; (IP) Intellectual property rights/inventor/patent holder; (SAB) Scientific advisory board

References

- 1.Schoen C, Doty MM, Robertson RH, et al. Affordable Care Act reforms could reduce the number of underinsured US adults by 70 percent. Health Aff (Millwood) 2011;30:1762–1771. doi: 10.1377/hlthaff.2011.0335. [DOI] [PubMed] [Google Scholar]

- 2.Goldman DP, Joyce GF, Zheng Y. Prescription drug cost sharing: Associations with medication and medical utilization and spending and health. JAMA. 2007;298:61–69. doi: 10.1001/jama.298.1.61. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.Bernard DS, Farr SL, Fang Z. National estimates of out-of-pocket health care expenditure burdens among nonelderly adults with cancer: 2001 to 2008. J Clin Oncol. 2011;29:2821–2826. doi: 10.1200/JCO.2010.33.0522. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Langa KM, Fendrick AM, Chernew ME, et al. Out-of-pocket health-care expenditures among older Americans with cancer. Value Health. 2004;7:186–194. doi: 10.1111/j.1524-4733.2004.72334.x. [DOI] [PubMed] [Google Scholar]

- 5.Rajurkar SP, Presant CA, Bosserman LD, et al. A copay foundation assistance support program for patients receiving intravenous cancer therapy. J Oncol Pract. 2011;7:100–102. doi: 10.1200/JOP.2010.000112. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Sheils JF, Haught R. Without the individual mandate, the Affordable Care Act would still cover 23 million; premiums would rise less than predicted. Health Aff (Millwood) 2011;30:2177–2185. doi: 10.1377/hlthaff.2011.0708. [DOI] [PubMed] [Google Scholar]

- 7.Virgo KS, Burkhardt EA, Cokkinides VE, et al. Impact of health care reform legislation on uninsured and Medicaid-insured cancer patients. Cancer J. 2010;16:577–583. doi: 10.1097/PPO.0b013e31820189cb. [DOI] [PubMed] [Google Scholar]

- 8.Shankaran V, Jolly S, Blough D, et al. Risk factors for financial hardship in patients receiving adjuvant chemotherapy for colon cancer: A population-based exploratory analysis. J Clin Oncol. 2012;30:1608–1614. doi: 10.1200/JCO.2011.37.9511. [DOI] [PubMed] [Google Scholar]

- 9.Markman M, Luce R. Impact of the cost of cancer treatment: An internet-based survey. J Oncol Pract. 2010;6:69–73. doi: 10.1200/JOP.091074. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 10.HealthWell Foundation. HealthWell Foundation 2010 Annual Report. [Accessed February 7, 2012]. Available at: http://www.healthwellfoundation.org/sites/default/files/HWF%202010%20Annual%20Report.pdf.

- 11.Schrag D, Naughton M, Kesselheim A, et al. Clinical trial participants' strategies for coping with prescription drug costs: A companion study to CALGB 80405. J Clin Oncol. 2009;27(suppl 15):9503. [Google Scholar]

- 12.Lauzier S, Levesque P, Drolet M, et al. Out-of-pocket costs for accessing adjuvant radiotherapy among Canadian women with breast cancer. J Clin Oncol. 2011;29:4007–4013. doi: 10.1200/JCO.2011.35.1007. [DOI] [PubMed] [Google Scholar]

- 13.Longo CJ, Deber R, Fitch M, et al. An examination of cancer patients' monthly ‘out-of-pocket’ costs in Ontario, Canada. Eur J Cancer Care (Engl) 2007;16:500–507. doi: 10.1111/j.1365-2354.2007.00783.x. [DOI] [PubMed] [Google Scholar]

- 14.Arozullah AM, Calhoun EA, Wolf M, et al. The financial burden of cancer: Estimates from a study of insured women with breast cancer. J Support Oncol. 2004;2:271–278. [PubMed] [Google Scholar]

- 15.Hanratty B, Holland P, Jacoby A, et al. Financial stress and strain associated with terminal cancer—a review of the evidence. Palliat Med. 2007;21:595–607. doi: 10.1177/0269216307082476. [DOI] [PubMed] [Google Scholar]

- 16.Neugut AI, Subar M, Wilde ET, et al. Association between prescription co-payment amount and compliance with adjuvant hormonal therapy in women with early-stage breast cancer. J Clin Oncol. 2011;29:2534–2542. doi: 10.1200/JCO.2010.33.3179. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.Rosenthal MB. What works in market-oriented health policy? N Engl J Med. 2009;360:2157–2160. doi: 10.1056/NEJMp0903166. [DOI] [PubMed] [Google Scholar]

- 18.Meropol NJ, Schrag D, Smith TJ, et al. American Society of Clinical Oncology guidance statement: The cost of cancer care. J Clin Oncol. 2009;27:3868–3874. doi: 10.1200/JCO.2009.23.1183. [DOI] [PubMed] [Google Scholar]

- 19.Alexander GC, Casalino LP, Meltzer DO. Patient-physician communication about out-of-pocket costs. JAMA. 2003;290:953–958. doi: 10.1001/jama.290.7.953. [DOI] [PubMed] [Google Scholar]

- 20.Hofstatter EW. Understanding patient perspectives on communication about the cost of cancer care: A review of the literature. J Oncol Pract. 2010;6:188–192. doi: 10.1200/JOP.777002. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 21.Kim P. Cost of cancer care: The patient perspective. J Clin Oncol. 2007;25:228–232. doi: 10.1200/JCO.2006.07.9111. [DOI] [PubMed] [Google Scholar]

- 22.Gibson PJ, Koepsell TD, Diehr P, et al. Increasing response rates for mailed surveys of Medicaid clients and other low-income populations. Am J Epidemiol. 1999;149:1057–1062. doi: 10.1093/oxfordjournals.aje.a009751. [DOI] [PubMed] [Google Scholar]

- 23.Kaiser Family Foundation. Spotlight on Uninsured Parents: How a Lack of Coverage Affects Parents and Their Families. [Accessed March 28, 2012]. Available at http://www.kff.org/uninsured/upload/7662.pdf.

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.