Abstract

Introduction:

Because cigarette price minimization strategies can provide substantial price reductions for individuals continuing their usual smoking behaviors following federal and state cigarette excise tax increases, we examined independent price reductions compensating for overlapping strategies. The possible availability of larger independent price reduction opportunities in states with higher cigarette excise taxes is explored.

Methods:

Regression analysis used the 2006–2007 Tobacco Use Supplement of the Current Population Survey (N = 26,826) to explore national and state-level independent price reductions that smokers obtained from purchasing cigarettes (a) by the carton, (b) in a state with a lower average after-tax cigarette price than in the state of residence, and (c) in “some other way,” including online or in another country. Price reductions from these strategies are estimated jointly to compensate for known overlapping strategies.

Results:

Each strategy reduced the price of cigarettes by 64–94 cents per pack. These price reductions are 9%–22% lower than conventionally estimated results not compensating for overlapping strategies. Price reductions vary substantially by state. Following cigarette excise tax increases, the price reduction available from purchasing cigarettes by cartons increased. Additionally, the price reduction from purchasing cigarettes in a state with a lower average after-tax cigarette price is positively associated with state cigarette excise tax rates and border state cigarette excise tax rate differentials.

Conclusions:

Findings from this large, nationally representative study of cigarette smokers suggest that price reductions are larger in states with higher cigarette excise taxes, and increase as cigarette excise taxes rise.

INTRODUCTION

Raising cigarette prices, primarily through taxation, decreases the prevalence of tobacco use (Chaloupka, 1999; Chaloupka, Cummings, Morley, & Horan, 2002; Chaloupka & Warner, 1999; Farrelly, 2009; Frieden et al., 2005; Levy, Cummings, & Hyland, 2000). This decrease may be a result of some potential smokers choosing not to smoke and more successful quit attempts among current smokers (Chaloupka et al., 2002; Chaloupka & Warner, 1999; Frieden et al., 2005; Hyland et al., 2005, 2006; Levy et al., 2000; Lewitt & Coate, 1982; Licht et al., 2011; McGoldrick & Boonn, 2010). Unfortunately, not all smokers will respond beneficially to tax increases, and some will continue their usual smoking behaviors by either using compensatory price minimization strategies (Choi, Hennrikus, Forster, & St Claire, 2012; DeCicca, Kenkel, & Liu, 2010; Fong et al., 2006; Frieden et al., 2005; Goolsble, Lovenheim, & Slemrod, 2010; Hyland, Higbee, Bauer, Giovino, & Cummings, 2004; Hyland et al., 2005, 2006; Licht et al., 2011; Pesko, Kruger, & Hyland, 2012; U.S. Department of Health and Human Services, 2000; White, Gilpin, White, & Pierce, 2005) or paying higher prices. Use of price minimization strategies, thus, mitigates the positive public health impact of cigarette price increases. Such strategies include purchasing discount or deep discount brands, utilizing price promotions such as coupons, purchasing in cartons, purchasing from low or untaxed sources, and purchasing roll-your-own cigarettes (Frieden et al., 2005; Hanewinkel & Isensee, 2007; Hanewinkel, Radden, & Rosenkranz, 2008; Hyland et al., 2005, 2006; Kengganpanich, Termsirikulchai, & Benjakul, 2009; Licht et al., 2011; Luk et al., 2009; Shelley, Cantrell, Moon-Howard, Ramjohn, & VanDevanter, 2007).

Recently, policies have been enacted in an attempt to combat price minimization behavior, such as the Prevent All Cigarette Trafficking (PACT) Act in 2010 that restricts the delivery of cigarettes through the mail (Ribisl, Williams, Gizlice, & Herring, 2011) or individual state agreements with Native American reservations regarding the collection of state excise taxes (Samuel, Ribisl, & Williams, 2012). Other recent proposals include expanding minimum per pack price laws (inclusive of price promotions; Centers for Disease Control and Prevention, 2010; Feighery, Ribisl, Schleicher, Zellers, & Wellington, 2005) and harmonizing excise taxes across U.S. states to reduce bootlegging (Cnossen, 2006).

The prevalence of using cigarette price minimization strategies has been extensively studied and has informed the policy debate surrounding cigarette prices. However, the magnitude of price reductions smokers may realize through price minimization strategies has been less studied.

Several studies have provided mean price comparisons paid by smokers practicing a strategy compared with those not practicing the same. One study found a mean in-state price reduction resulting from buying cigarettes in cartons instead of separate packs of $0.98 cents per pack in 2003 and $1.10 per pack in 2006–2007. This study also found border state cigarette price reductions of $1.29 per pack in 2003 and $1.40 per pack in 2006–2007 compared with in-state pack purchases (DeCicca et al., 2010). Licht and colleagues (2011) found mean price reductions of $1 per pack for purchases made from low/untaxed sources, $1 per pack for discount brand cigarettes, and $1.20 per pack for carton purchases using data from the International Tobacco Control (ITC) project. Data from Western New York State (2002–2003) indicated that smokers could realize a price reduction of $2.89 per pack by purchasing cigarettes on an Indian reservation instead of a small, off-reservation tobacco outlet (Hyland et al., 2004). An additional study completed in California (2002) controlled for variation arising from uncontrolled price minimization strategies correlated with sociodemographic and smoking characteristics to estimate price reductions obtained from single strategies. These price reduction estimates ranged from $0.36 to $1.01 a pack for each of five strategies (White et al., 2005).

These studies suggest that large price reductions can be obtained from using cigarette price minimization strategies. However, these studies did not estimate price reductions from individual strategies while controlling for overlapping strategies. Given that individuals are likely to practice multiple price minimization strategies concurrently (Choi et al., 2012; Licht et al., 2011; White et al., 2005), price reductions may be overestimated for any individual strategy if not controlling for overlapping strategies. Independent estimates of the price reductions, which compensate for overlapping strategies where possible, are important to provide more accurate information in the ongoing policy debates surrounding cigarette price minimization strategies.

This study builds upon earlier methodologies by using multivariate regression analyses to investigate the independent price reductions attributable to commonly used price minimization strategies and explores how these independent price reduction estimates are impacted by cigarette excise tax increases. We used nationally representative cross-sectional data to provide both national and state-level estimates of the price reductions from purchasing cigarettes in cartons, across state borders, and through “other” means, such as purchases made online or in another country.

METHODS

Data Description

The national and state representative Tobacco Use Supplement of the Current Population Survey (TUS-CPS), sponsored by the National Cancer Institute, is used in this analysis. The cross-sectional data were collected in May 2006, August 2006, and January 2007. The data contain detailed information on smoking status, sociodemographic characteristics, and the number of cigarettes smoked per day. Daily and nondaily smokers are included. A unique feature of the data source is the ability to use its state-level representation and large number of respondents to calculate estimates for all 50 states and the District of Columbia.

Smokers were asked “Do you USUALLY buy your cigarettes by the pack or by the carton?” Following, smokers reported how much they paid for the last pack or carton of cigarettes bought (after use of discounts or coupons). Individuals stating that they usually purchase cigarettes by the carton were asked, “What price did you pay for the LAST CARTON of cigarettes you bought? Please report the cost after using discounts or coupons.” The total price paid for cartons was divided by 10 to obtain per pack price information. Respondents who reported usually purchasing both packs and cartons were only asked for the price paid for the last pack of cigarettes purchased.

Smokers were asked “Did you buy your LAST [pack or carton] of cigarettes in [respondent’s state of residence] or in some other state?” to determine the location of their last purchase. Possible selections were as follows: in state of residence, in a different state, or bought some other way (Internet or other country) as their answer.

TUS-CPS observations were excluded for respondents younger than 18 years of age, proxy respondents, nonsmokers, smokers who have not smoked during the prior 30 days, smokers with missing daily cigarette information or price data, smokers with cigarette purchase prices that fell below the combined federal and state excise taxes at the time of purchase, and smokers with self-reported cigarette prices that were above $8 per pack. The upper bound for cigarette prices was selected in an attempt to normalize the distribution. After these exclusions, the number of observations used in the analysis was 26,826. Descriptive statistics are provided in Table 1.

Table 1.

Descriptive Statistics and Ordinary Least Squares Regression Results of Price Reductions for Cigarette Price Minimization Strategies, National Estimates (N = 26,826)

| Variables | Weighted means | Coefficient (cents)a,b | 95% CI |

|---|---|---|---|

| Dependent | |||

| Price per pack | $3.62 | ||

| Independent | |||

| Cigarette price minimization strategy | |||

| Carton | 29.33% | −68*** | −71, −65 |

| Out-of-state purchase | 3.52% | −83*** | −91, −75 |

| Other purchase | 0.30% | −94*** | −128, −60 |

| Sex | |||

| Men (ref) | 53.93% | 0 | − |

| Women | 46.07% | −1 | −3, 1 |

| Age, years | |||

| 18–24 (ref) | 14.90% | 0 | − |

| 25–44 | 42.14% | −9*** | −13, −6 |

| 45–64 | 36.17% | −21*** | −24, −17 |

| 65+ | 6.79% | −17*** | −23, −11 |

| Race/ethnicity | |||

| White, non-Hispanic (ref) | 75.97% | 0 | − |

| Black, non-Hispanic | 10.60% | 21*** | 17, 25 |

| Hispanic | 8.67% | 20*** | 15, 26 |

| Other, non-Hispanic | 4.75% | 10*** | 5, 15 |

| Education | |||

| Less than high school (ref) | 18.36% | 0 | − |

| High school degree only | 39.90% | 2 | −1, 6 |

| More than high school | 41.74% | 10*** | 7, 13 |

| Family income (annual) | |||

| <$25,000 (ref) | 37.06% | 0 | − |

| $25,000–$49,999 | 22.34% | 8*** | 5, 11 |

| $50,000–$74,999 | 16.75% | 10*** | 6, 13 |

| >$74,999 | 15.12% | 23*** | 19, 26 |

| Missing data | 8.73% | 12*** | 7, 16 |

| Employment status | |||

| Employed (ref) | 68.15% | 0 | − |

| Unemployed | 6.60% | 0 | −4, 5 |

| Students/homemaker | 9.59% | −3 | −12, 7 |

| Other (not in labor force) | 15.66% | −16*** | −25, −7 |

| Work sector | |||

| White collar (ref) | 34.65% | 0 | − |

| Service | 24.89% | −4* | −7, −1 |

| Blue collar | 14.94% | −4** | −7, −1 |

| Other | 25.52% | −2 | −11, 7 |

| Smoking frequency | |||

| Every day smoker (ref) | 82.76% | 0 | − |

| Some day smoker | 17.24% | 2 | −2, 6 |

| Smoking intensity (number of cigarettes) | |||

| <6 cigarettes per day (ref) | 19.42% | 0 | − |

| 6–14 cigarettes per day | 29.42% | −5* | −9, −1 |

| >14 cigarettes per day | 51.16% | −8*** | −12, −4 |

| Constant | 24 | −11, 60 | |

Note. CI = confidence interval.

aIn this regression, average cigarette price data were included to control for variation in cigarette prices from changing state excise tax rates and other costs associated with transporting and selling cigarettes. State fixed effects were included to control for such things as variation in cigarette prices from proximity to other states, Indian reservations, and county and municipal taxes. Month fixed effects were included to control for variation associated with prices depending on month. All of these coefficients are omitted from this table for space considerations.

bIn unreported results, this model was alternatively estimated adding interaction variables between carton purchases and the other two price minimization strategies. The coefficients on these two interaction variables provide the additional savings associated with practicing the strategies simultaneously. The full savings were $1.59 for purchasing cartons in a state with a lower average after-tax cigarette price and were $1.80 by purchasing cartons in some other way.

*Significant at 5% level; **Significant at 1% level; ***Significant at .1% level.

Reported use (yes or no) of three cigarette price minimization strategies was based on respondents’ last purchase of a typical quantity: (1) usually purchasing cigarettes by the carton, (2) purchasing cigarettes in a state with a lower average after-tax cigarette price than in the state of residence, and (3) purchasing cigarettes in “some other way,” including Internet purchases and purchases made in other countries. Strategies 2 and 3 are mutually exclusive, but can be practiced with or without strategy 1.

Tax Burden on Tobacco (TBOT) cigarette price data were used to determine if the respondent made the purchase in a state with a lower average price compared with their state of residence (Orzechowski and Walker, 2011; Table 13B). This state-level price is inclusive of generic cigarettes, state and federal excise taxes, and some local taxes. Adjustments were made to TBOT cigarette prices for changes in state excise taxes occurring mid-quarter. In these instances, the weighted proportion of the increased cigarette excise tax was first removed from the TBOT average state price for that quarter. If the interview month was after the state excise tax increase came into effect, then the full state excise tax increase was added back to the adjusted TBOT price. This approach for determining the purchase of cigarettes in a state with a lower average after-tax cigarette price was used previously (Pesko et al., 2012).

State cigarette excise tax rates were also used (Orzechowski and Walker, 2011; Table 6). To explore tax rate differentials across state borders, border states were identified for each state, and the mean cigarette excise taxes in these border states was computed. The border state cigarette excise tax rate was subtracted from the in-state cigarette excise tax rate to determine the differential.

Estimation

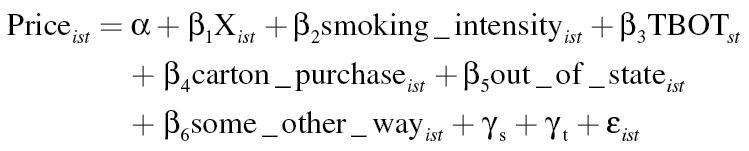

The dependent variable, cost per pack after use of any price promotions, is estimated by the following model:

|

The subscript i refers to the individual, s to the state, and t to the month that the survey was conducted. X

ist represents demographic controls and includes indicator variables for the following: sex, age (18–24, 25–44, 45–64, and ≥65), race/ ethnicity (White non-Hispanic, Black non-Hispanic, Hispanic, and other non-Hispanic), education (less than high school, high school only, and more than high school), employment status (employed, unemployed, student or homemaker, and other nonlabor force), work sector (white collar, blue collar, service, other), and family income (≤$24,999, $25,000–$49,999, $50,000–$74,999, ≥$75,000, and missing). The matrix smoking_intensityist includes indicator variables for daily smoking status (daily vs. some days over past 30 days), and for number of cigarettes smoked on smoking days (<6 cigarettes, 6–14 cigarettes, and >14 cigarettes). State fixed effects,  are included to further control for accessibility of Indian reservation purchases, and other state-varying characteristics such as antismoking sentiment. Survey month fixed effects,

are included to further control for accessibility of Indian reservation purchases, and other state-varying characteristics such as antismoking sentiment. Survey month fixed effects,  are included to control for seasonal variation in the use of explored price minimization strategies. Finally, TBOT cigarette price data were included to control for different cigarette prices within states and cigarette price differences between states.

are included to control for seasonal variation in the use of explored price minimization strategies. Finally, TBOT cigarette price data were included to control for different cigarette prices within states and cigarette price differences between states.

Indicator variables are constructed for use of the three cigarette price minimization strategies (carton_purchaseist, some_other_wayist, and out_of_stateist). These variables are included in multivariate regression analysis jointly in the regular specification, but also as standalone variables in a sensitivity analysis specification. Including the three independent variables in the same model (i.e., joint estimation) yields estimates of the independent price reductions produced by each strategy after controlling for the simultaneous use of strategies.

Ordinary least squares (OLS) regression analysis is used to estimate the model. Statistically significant negative coefficients for the price minimization strategies suggest that individuals practicing these strategies are reducing prices by the amounts given by the coefficients (in cents) compared with the reference group. Sociodemographic and smoking characteristic variables are included in this model to help control for additional savings from uncontrolled price minimization strategies and reporting bias. Uncontrolled strategies are thought to include (a) purchasing discount or deep discount cigarettes, (b) using coupons or other price promotions, and (c) purchasing cigarettes from no- or low-tax sources besides other states or countries.

This study also explores the impact of cigarette excise tax increases on independent price reductions from price minimization strategies. This analysis takes advantage of various cigarette excise tax increases occurring between the three TUS-CPS waves. Between the first wave (May 2006) and the second wave (August 2006), cigarette excise taxes increased in Vermont ($0.60), Alaska ($0.20), New Jersey ($0.175), and North Carolina ($0.05). Between the second wave (August 2006) and the third wave (January 2007), cigarette excise taxes increased in South Dakota ($1.00), Texas ($1.00), Arizona ($0.82), and Hawaii ($0.20). For this analysis, the estimation equation is similar to that used in Table 1, except that the TBOT state cigarette price is replaced with the cigarette excise tax increase, ranging from $0.05 to $1.00 for these eight states. For all other states, the cigarette excise tax increase is zero, indicating no tax increase occurred during this time period. An interaction between this cigarette excise tax variable and use of price minimization strategies investigates whether independent price reductions changed as a result of cigarette excise taxes.

The state representativeness of the TUS-CPS was used to compute state-level estimates of independent price reductions from the known cigarette price minimization strategies. First, interaction terms were added to the base model between the three cigarette price minimization strategies and all state fixed effects. Joint Wald F-statistics were computed to test the null hypothesis that state-level estimates of the three strategies are not differentiable from national estimates. The null hypothesis was rejected for all three strategies (all p < .001), suggesting that computing state-level estimates of the price reductions for all three strategies jointly is appropriate at the state level. However, out of concern for limited sample size at the state level, these results were only reported for states where at least 30 respondents practiced the respective strategy. State-level results are reported for all states and the District of Columbia for carton purchases, but are only reported for 15 states and the District of Columbia for purchasing cigarettes in a state with a lower average after-tax cigarette price. Due to insufficient sample sizes, state-level results are not reported for the third strategy of interest, purchasing cigarettes in “some other way” although this strategy remains controlled for to obtain independent price reduction estimates for the other reported strategies.

All analyses were completed using SAS version 9.3. National population estimates were based on the CPS sample weights for self-report interviews. Final weights were adjusted with replicate weights provided by the National Cancer Institute with a balanced repeated replication and Fay’s adjustment factor of 0.5 (Behm, Kabir, Connolly, & Alpert, 2012).

RESULTS

Table 1 provides full OLS regression results. The average cost per pack was $3.62 from May 2006 to January 2007. The independent price reductions (per pack) obtained from cigarette price minimization strategies were $0.68 for purchasing cigarettes in cartons, $0.83 for purchasing cigarettes in a state with a lower average after-tax cigarette price, and $0.94 for purchasing cigarettes in some other way, such as over the Internet or in another country. These independent price reductions represent an 18.8%, 23.0%, and 26.0% reduction from the average cost per pack for each of these strategies, respectively (all p < .001).

Combining multiple strategies may yield additional price reductions. The additive properties of OLS suggest reductions of $1.51 per pack ($0.68 + $0.83) by purchasing cartons in a state with a lower average after-tax cigarette price, and $1.62 per pack ($0.68 + $0.94) by purchasing cartons in some other way (online or in another country). In unreported results, interaction variables between carton purchases and the other two price minimization strategies were added to the previously estimated model. Results from the interaction model suggest higher but similar reductions of $1.59 by purchasing cartons in a state with a lower average cigarette price and $1.80 by purchasing cartons in some other way.

The coefficients on sociodemographic characteristics in Table 1 provide evidence of population subgroups that may be practicing uncontrolled price minimization strategies more frequently. After simultaneously adjusting for the known price minimizing strategies above, sociodemographic variables that were associated with other price reductions included being older, White, lower educated, and lower income earning. Compared with young adults aged 18–24, individuals aged 25–44 reported saving 9 cents per pack, individuals aged 45–64 reported saving 21 cents per pack, and individuals 65 and older reported saving 17 cents per pack (all p < .001). Whites experienced other price reductions of 21 cents compared with Blacks, 20 cents compared with Hispanics, and 10 cents compared with other races (all p < .001). The lowest income individuals realized other price reductions of 23 cents per pack compared with those with a family income of $75,000 or more (p < .001). Additionally, individuals that smoke more than 14 cigarettes daily realized other price reductions of 8 cents compared with those smoking less than 6 cigarettes daily (p < .001).

As hypothesized, the independent price reductions from each of these strategies is smaller than the price reductions estimated if each strategy is investigated separately, likely due to individuals practicing overlapping strategies (Table 2). Separately estimating price minimization strategies for carton purchases, out-of-state purchases, and other purchases suggests “per pack” reductions of $0.75 by purchasing cigarettes in cartons, $1.06 by purchasing in a state with a lower average after-tax cigarette price, and $1.20 by purchasing cigarettes some other way (all p < .001). The independent price reduction estimates obtained in the model in which all three strategies are included jointly are 9% (p < .001), 22% (p < .001), and 22% lower than these estimates, respectively.

Table 2.

Comparison of Joint (i.e., Independent) and Separate Ordinary Least Squares Regression Estimates of Per Pack Price Reductions

| Cigarette price minimization strategy | Separate model (non-independent effects)a | Joint model (independent effects)a,b | Percent changec | ||

|---|---|---|---|---|---|

| Coefficient | 95% CI | Coefficient | 95% CI | ||

| Carton purchase | −75*** | (−78, −72) | −68*** | (−71, −65) | −9%*** |

| Out-of-state purchase | −106*** | (−115, −98) | −83*** | (−91, −75) | −22%*** |

| Other purchase | −120*** | (−160, −80) | −94*** | (−128, −60) | −22% |

Note. CI = confidence interval

aAll models (joint and separate) were adjusted for sociodemographic characteristics, smoking characteristics, state fixed effects, survey month fixed effects, and average cigarette prices.

bData also presented in Table 1.

cCalculated as ((Coefficient [joint model] – coefficient [separate model]) / (coefficient [separate model])) × 100%.

***Significant at .1% level.

Sensitivity analysis was conducted by not including smoking intensity in the national model of independent price reductions. Results showed an insignificant change in the coefficients for independent price reductions of at most 2 cents, suggesting that potential endogeneity between smoking intensity and cost per pack is not influencing the results. Additionally, sensitivity analysis was conducted by removing the TBOT cigarette price variable from the regression analysis. Price reduction estimates for each price minimization strategy were not statistically different from the standard independent price reduction estimates, suggesting little impact of controlling for different cigarette prices within states and cigarette price differences between states.

Table 3 provides evidence that the eight cigarette excise tax increases occurring during the survey period increased price reduction savings. The results suggest that the increases in cigarette excise taxes had a 97% (p < .001) pass-through rate to cigarette prices in these states, which is slightly higher than a 90% pass-through rate found in a recent study using similar controls (Harding, Leibtag, & Lovenheim, 2012; Table 2, column 4). The independent price reduction estimates for the three strategies are not statistically different from those presented in Table 1. Finally, the interaction of the cigarette excise tax increase and the independent price reduction estimate suggests that the market reacted to eight cigarette excise tax increases by creating larger price reduction opportunities of between $0.17 and $0.44 for each of the three strategies although only the $0.17 increase in the price reduction from purchasing cigarettes by the carton was statistically significant. These results suggest that while cigarette excise tax increases are effective in raising the price of cigarettes (97% pass-through), the full increase in prices may be avoided by the increases in price reductions due to price minimization strategies.

Table 3.

Ordinary Least Squares Regression Results of Cigarette Excise Tax Increases and Per Pack Price Reductions

| Variables | Coefficient (cents)a | 95% CI coefficient (cents) |

|---|---|---|

| Dependent | ||

| Price per pack | ||

| Independent | ||

| State cigarette excise tax increase | 0.97*** | 0.87, 1.08 |

| Cigarette price minimization strategy | ||

| Carton | −68*** | −71, −65 |

| Out-of-state purchase | −81*** | −89, −73 |

| Other purchase | −89*** | −129, −49 |

| Interaction variables | ||

| Carton × state cigarette excise tax increase | −17* | −33, −1 |

| Out-of-state purchase × state cigarette excise tax increase | −44 | −97, 10 |

| Other purchase × state cigarette excise tax increase | −32 | −103, 38 |

Note. CI = confidence interval.

aAll independent variables used in Table 1, with the exception of state price, are also controlled for in this regression. All of these coefficients are omitted from this table for space considerations.

*Significant at 5% level; ***significant at .1% level.

State-Level Estimation Results

State-level independent price reduction estimates from carton purchasing and purchasing cigarettes from a state with a lower average after-tax cigarette price are reported for all states for carton purchasing and 16 states (including the District of Columbia) for the strategy of purchasing cigarettes in a state with a lower average after-tax cigarette price (all p < .05; Table 4). Residents of at least four states may have access to carton sources that provide independent price reductions of greater than $1 per pack, including New York ($1.35), Washington ($1.11), Oklahoma ($1.08), and Massachusetts ($1.02). Residents from Indiana reported the lowest independent price reductions from carton purchases ($0.19).

Table 4.

Ordinary Least Squares Regression Results of Price Reductions for Cigarette Price Minimization Strategies, State Estimates

| Stateb,d | Average cigarette excise tax rate | Average cigarette excise tax rate in border states | Carton coefficient (cents) | 95% CI | Out-of-state purchase coefficient (cents)c | 95% CI |

|---|---|---|---|---|---|---|

| Dependent variable: Price per pack | ||||||

| United Statesa | 91 | 87 | −68*** | −71, −65 | −83*** | −91, −75 |

| Alabama | 43 | 30 | −45*** | −61, −30 | ||

| Alaska | 173 | −51*** | −79, −23 | |||

| Arizona | 148 | 85 | −93*** | −114, −71 | ||

| Arkansas | 59 | 51 | −54*** | −68, −39 | −33*** | −49, −18 |

| California | 87 | 125 | −81*** | −90, −71 | ||

| Colorado | 84 | 104 | −62*** | −75, −49 | ||

| Connecticut | 151 | 155 | −42*** | −62, −21 | ||

| Delaware | 55 | 158 | -52*** | −64, −40 | ||

| District of Columbia | 100 | 60 | −72*** | −104, −39 | −70*** | −91, −48 |

| Florida | 34 | 39 | −76*** | −87, −65 | ||

| Georgia | 37 | 29 | −60*** | −72, −48 | ||

| Hawaii | 147 | −89*** | −115, −64 | |||

| Idaho | 57 | 141 | −63*** | −80, −45 | ||

| Illinois | 98 | 43 | −89*** | −110, −68 | −70*** | −95, −46 |

| Indiana | 56 | 121 | −19* | −35, −3 | ||

| Iowa | 34 | 82 | −61*** | −76, −46 | ||

| Kansas | 79 | 60 | −68*** | −81, −54 | ||

| Kentucky | 30 | 68 | −63*** | −75, −50 | ||

| Louisiana | 36 | 64 | −54*** | −71, −36 | ||

| Maine | 200 | 80 | −69*** | −86, −52 | −130*** | −152, −108 |

| Maryland | 100 | 93 | −65*** | −77, −53 | −55*** | −70, −40 |

| Massachusetts | 151 | 151 | −102*** | −132, −72 | ||

| Michigan | 200 | 93 | −57*** | −71, −43 | −126*** | −155, −97 |

| Minnesota | 149 | 62 | −49*** | −68, −31 | −68*** | −102, −35 |

| Mississippi | 18 | 36 | −45*** | −68, −23 | ||

| Missouri | 17 | 63 | −69*** | −79, −58 | ||

| Montana | 170 | 62 | −38*** | −55, −21 | ||

| Nebraska | 64 | 48 | −49*** | −65, −32 | −34** | −58, −9 |

| Nevada | 80 | 99 | −89*** | −106, −71 | ||

| New Hampshire | 80 | 162 | −66*** | −79, −53 | ||

| New Jersey | 254 | 141 | −45** | −72, −18 | −190*** | −230, −150 |

| New Mexico | 91 | 89 | −96*** | −121, −70 | ||

| New York | 150 | 166 | −135*** | −166, −105 | −96*** | −130, −62 |

| North Carolina | 33 | 25 | −72*** | −85, −59 | ||

| North Dakota | 44 | 144 | −60*** | −74, −46 | ||

| Ohio | 125 | 112 | −25*** | −35, −16 | −97*** | −110, −83 |

| Oklahoma | 103 | 63 | −108*** | −125, −91 | ||

| Oregon | 118 | 108 | −49*** | −60, −37 | ||

| Pennsylvania | 135 | 144 | −45*** | −57, −33 | −87*** | −107, −67 |

| Rhode Island | 246 | 151 | −57*** | −79, −35 | −91*** | −113, −68 |

| South Carolina | 7 | 35 | −67*** | −79, −54 | ||

| South Dakota | 86 | 96 | −59*** | −73, −46 | −63*** | −89, −37 |

| Tennessee | 20 | 33 | −55*** | −70, −40 | ||

| Texas | 72 | 69 | −75*** | −87, −62 | ||

| Utah | 69 | 104 | −66*** | −83, −48 | ||

| Vermont | 159 | 146 | −86*** | −104, −67 | −99*** | −120, −78 |

| Virginia | 30 | 42 | −68*** | −82, −54 | ||

| Washington | 203 | 103 | −111*** | −130, −91 | −144*** | −172, −117 |

| West Virginia | 55 | 97 | −34*** | −48, −19 | ||

| Wisconsin | 77 | 132 | −28*** | −44, −12 | ||

| Wyoming | 60 | 83 | −67*** | −79, −56 | ||

Note. CI = confidence interval.

aNational cigarette excise tax rates are those experienced by smokers.

bEach line shows estimates obtained from different state-level regressions.

cOnly estimates from states with more than 30 observations for the price minimization strategy of purchasing cigarettes in a state with a lower average after-tax cigarette price are reported.

dAverage cigarette price data were included in regressions to control for variation in cigarette prices from changes at the state level. Month fixed effects were included to control for variation associated with prices depending on month. All other previously used cigarette price minimization strategies, sociodemographic characteristics, and smoking characteristics are also controlled for.

*Significant at 5% level; **significant at 1% level; ***significant at .1% level.

Coefficients on out-of-state purchases ranged from $0.33 to $1.90. The states with the largest potential out-of-state price reductions include New Jersey ($1.90), Washington ($1.44), and Maine ($1.30). Washington is unique in that it is the only state having price reduction estimates for both cheaper out-of-state purchases and carton purchases greater than $1 per pack, with suggested price reduction for Washington residents practicing both strategies simultaneously being $2.55 per pack.

Associations between state-level price reduction estimates and cigarette excise taxes were investigated (Table 5). As expected, smokers in states with higher cigarette excise taxes obtained larger price reductions (lower prices) for purchasing out of state compared with smokers residing in lower cigarette excise tax states. Additionally, the difference between in-state cigarette excise taxes and the average of the cigarette excise taxes in border states was associated with larger price reductions (lower prices) for out-of-state purchases. The analysis suggests that the presence of $1 in cigarette excise taxes is associated with state-level price reduction opportunity of $1.27 by purchasing out-of-state. While associations between the price reduction strategy of carton purchasing and state-level cigarette excise tax rates had the same negative sign (suggesting lower prices from the strategy with higher cigarette excise taxes), these associations were not statistically significant.

Table 5.

Univariate Associations Between Cigarette Excise Tax Rates and State-Level Price Reduction Estimates

| Dependent variables | ||||||

|---|---|---|---|---|---|---|

| Carton price reduction estimate | Out-of-state price reduction estimate | |||||

| Coefficient | 95% CI | N | Coefficient | 95% CI | N | |

| In-state average cigarette excise tax rate | −0.07 | (−0.44, 0.59) | 49 | −1.27*** | (−1.70, −0.85) | 16 |

| Difference between in-state and border state average cigarette excise tax rates | −0.23 | (−0.69, 0.23) | 51 | −0.78** | (−1.30, −0.25) | 16 |

Note. CI = confidence interval.

**Significant at 1% level; ***significant at .1% level.

DISCUSSION

This article describes the potential price reductions smokers obtained from using three important price minimization strategies. In addition, this article highlights the importance of controlling for overlapping price minimization strategies to avoid over-predicting price reductions that smokers may obtain by using multiple strategies simultaneously. However, even after controlling for such overlap, large independent price reductions were still observed—$0.68 due to purchasing cigarettes by the carton, $0.83 due to purchasing cigarettes out of state, and $0.94 due to purchasing cigarettes in “some other way.” State-level analysis suggests independent price reductions vary substantially by state and are higher in states with higher cigarette excise taxes.

Unexplored price minimization strategies, such as the use of discount or deep discount cigarettes, may be responsible for the variation in average cigarette prices among subgroups after controlling for known strategies. For example, older individuals reported paying, on average, between 9 and 21 cents less per pack compared with younger individuals, likely explained by the fact that younger individuals may be more likely to purchase major brand cigarettes rather than discount brands (O’Connor, 2005). Similarly, individuals of low socioeconomic status (both low education attainment and low income) appear more likely to practice some uncontrolled price minimization strategies, which may include purchasing discount or deep discount cigarettes. This finding helps to rectify a discrepancy in the literature regarding if low socioeconomic status individuals practice cigarette price minimization strategies less frequently (Pesko et al., 2012) or more frequently than high socioeconomic status individuals (Choi et al., 2012; Licht et al., 2011). Including usage of discounted cigarettes is important in future research that analyzes the use of cigarette price minimization strategies by age or socioeconomic status.

This research found that the size of independent price reductions was responsive to changes in cigarette excise taxes across time and in cigarette excise tax differences across states. Following cigarette excise tax increases, the price reduction available from purchasing cigarettes by cartons increased. Additionally, the price reduction from purchasing cigarettes in a state with a lower average after-tax cigarette price is positively associated with state cigarette excise tax rates and border state cigarette excise tax rate differentials. This finding highlights the diluting impact of cigarette price minimization strategies in raising the price of cigarettes through cigarette excise taxes.

There are three primary limitations of this article. The first is that the TUS-CPS does not collect information on other important price minimization strategies that may also reveal large price reductions. However, all three of the strategies used in these data are noteworthy for their ability to provide smokers with substantial price reduction outlets. Future surveys on tobacco use should collect information on all strategies used by smokers, including purchasing discount or deep discount brands, using price promotions such as coupons, purchasing in cartons, and purchasing from low or untaxed sources (e.g., black market, out of state, Indian reservations) in order to comprehensively track changes in price reductions and prevalence of price minimization strategies over time or correlating use of these strategies with cessation.

Second, the data used to obtain these estimates were collected in 2006–2007. Therefore, the price reduction estimates presented here should be interpreted cautiously as tobacco control policies, among other factors, have changed from the time of these data collection. Additionally, these data are based on self-report and may be subject to recall error or response biases.

Finally, our reported price per unit of tobacco does not include additional costs associated with obtaining the tobacco products, such as those associated with transportation. These may be particularly important for Indian reservation or out-of-state purchases as smokers using these strategies may seek higher price differentials to recover these additional costs. However, measurement of these additional costs would not be practical or feasible in a large-scale population-based study such as the TUS-CPS.

Policy makers and public health officials should monitor not just the prevalence of cigarette price minimization strategies, but also the independent price reduction that the strategies provide. To encourage smoking prevention and cessation, policies should be promoted to reduce opportunities to minimize the price of cigarettes. This research in particular notes the benefit of harmonizing excise taxes to reduce the opportunity of individuals to purchase cheaper cigarettes out of state. Other policy options include expanding minimum per pack price laws (inclusive of price promotions) and expanding state-level negotiations with Indian reservations for collecting state excise taxes.

FUNDING

The work was supported in part by the National Cancer Institute and the National Institutes of Health (25CA113951) to A.S.L.

The content is solely the responsibility of the authors and does not represent the official views of the National Cancer Institute or the National Institutes of Health.

DECLARATION OF INTERESTS

None declared.

ACKNOWLEDGMENTS

Frank Chaloupka, Marina Reppucci, and Katherine Klem provided assistance with this project.

REFERENCES

- Behm I., Kabir Z., Connolly G. N., Alpert H. R. (2012). Increasing prevalence of smoke-free homes and decreasing rates of sudden infant death syndrome in the United States: An ecological association study. Tobacco Control, 21, 6–11.10.1136/tc.2010.041376 [DOI] [PubMed] [Google Scholar]

- Centers for Disease Control and Prevention (2010). State cigarette minimum price laws—United States, 2009. MMWR Morbidity and Mortality Weekly Report, 59, 389–392 [PubMed] [Google Scholar]

- Chaloupka F. J. (1999). Curbing the epidemic: Governments and the economics of tobacco control. The World Bank. Tobacco Control, 8, 196–201 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Chaloupka F. J., Cummings K. M., Morley C. P., Horan J. K. (2002). Tax, price and cigarette smoking: Evidence from the tobacco documents and implications for tobacco company marketing strategies. Tobacco Control, 11(Suppl. 1)I62–I72 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Chaloupka F. J., Warner K. E. (1999). The economics of smoking National Bureau of Economic Research Working Paper Series Retrieved from www.nber.org/papers/w7047

- Choi K., Hennrikus D., Forster J., St Claire A. W. (2012). Use of price-minimizing strategies by smokers and their effects on subsequent smoking behaviors. Nicotine & Tobacco Research, 14, 864–870.10.1093/ntr/ntr300 [DOI] [PubMed] [Google Scholar]

- Cnossen S. A. (2006). Tobacco taxation in the European Union CESifo Working Paper Series. Munich: CESifo Group Munich; [Google Scholar]

- DeCicca P., Kenkel D. S., Liu F. (2010). Who pays cigarette taxes? The impact of consumer price search. National Bureau of Economic Research Working Paper Series. Retrieved from www.nber.org/papers/w15942 [Google Scholar]

- Farrelly M. C. (2009). Monitoring the tobacco use epidemic V: The environment: factors that influence tobacco use. Preventive Medicine, 48(Suppl. 1)S35–43.10.1016/j.ypmed.2008.10.012 [DOI] [PubMed] [Google Scholar]

- Feighery E. C., Ribisl K. M., Schleicher N. C., Zellers L., Wellington N. (2005). How do minimum cigarette price laws affect cigarette prices at the retail level? Tobacco Control, 14, 80–85.10.1136/tc.2004.008656 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Fong G. T., Cummings K. M., Borland R., Hastings G., Hyland A., Giovino G. A., … Thompson M. E. (2006). The conceptual framework of the International Tobacco Control (ITC) Policy Evaluation Project. Tobacco Control, 15(Suppl. 3)iii3–11.10.1136/tc.2005.015438 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Frieden T. R., Mostashari F., Kerker B. D., Miller N., Hajat A., Frankel M. (2005). Adult tobacco use levels after intensive tobacco control measures: New York City, 2002–2003. American Journal of Public Health, 95, 1016–1023.10.2105/AJPH.2004.058164 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Goolsble A., Lovenheim M. F., Slemrod J. (2010). Playing with fire cigarettes, taxes, and competition from the Internet. American Economic Journal: Economic Policy, 2, 131–154.10.1257/Pol.2.1.131 [Google Scholar]

- Hanewinkel R., Isensee B. (2007). Access to cheaper cross-border cigarettes may decrease smoking cessation intentions in Germany. Tobacco Control, 16, 70–71.10.1136/tc.2006.016600 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Hanewinkel R., Radden C., Rosenkranz T. (2008). Price increase causes fewer sales of factory-made cigarettes and higher sales of cheaper loose tobacco in Germany. Health Economics, 17, 683–693.10.1002/hec.1282 [DOI] [PubMed] [Google Scholar]

- Harding M., Leibtag E., Lovenheim M. F. (2012). The heterogeneous geographic and socioeconomic incidence of cigarette taxes: Evidence from Nielsen Homescan Data. American Economic Review: Economic Policy, 4, 169–198.10.1257/Pol.4.4.169 [Google Scholar]

- Hyland A., Bauer J. E., Li Q., Abrams S. M., Higbee C., Peppone L., Cummings K. M. (2005). Higher cigarette prices influence cigarette purchase patterns. Tobacco Control, 14, 86–92.10.1136/tc.2004.008730 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Hyland A., Higbee C., Bauer J. E., Giovino G. A., Cummings K. M. (2004). Cigarette purchasing behaviors when prices are high. Journal of Public Health Management and Practice, 10, 497–500 [DOI] [PubMed] [Google Scholar]

- Hyland A., Laux F. L., Higbee C., Hastings G., Ross H., Chaloupka F. J., … Cummings K. M. (2006). Cigarette purchase patterns in four countries and the relationship with cessation: Findings from the International Tobacco Control (ITC) Four Country Survey. Tobacco Control, 15(Suppl. 3)iii59–64.10.1136/tc.2005.012203 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Kengganpanich M., Termsirikulchai L., Benjakul S. (2009). The impact of cigarette tax increase on smoking behavior of daily smokers. Journal of the Medical Association of Thailand, 92(Suppl. 7)S46–53 [PubMed] [Google Scholar]

- Levy D. T., Cummings K. M., Hyland A. (2000). Increasing taxes as a strategy to reduce cigarette use and deaths: Results of a simulation model. Preventive Medicine, 31, 279–286.10.1006/pmed.2000.0696 [DOI] [PubMed] [Google Scholar]

- Lewitt E. M., Coate D. (1982). The potential for using excise taxes to reduce smoking. Journal of Health Economics, 1, 121–145 [DOI] [PubMed] [Google Scholar]

- Licht A. S., Hyland A. J., O’Connor R. J., Chaloupka F. J., Borland R., Fong G. T., … Cummings K. M. (2011). How do price minimizing behaviors impact smoking cessation? Findings from the International Tobacco Control (ITC) Four Country Survey. International Journal of Environmental Research and Public Health, 8, 1671–1691.10.3390/ijerph8051671 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Luk R., Cohen J. E., Ferrence R., McDonald P. W., Schwartz R., Bondy S. J. (2009). Prevalence and correlates of purchasing contraband cigarettes on First Nations reserves in Ontario, Canada. Addiction, 104, 488–495.10.1111/j.1360-0443.2008.02453.x [DOI] [PubMed] [Google Scholar]

- McGoldrick D. E., Boonn A. V. (2010). Public policy to maximize tobacco cessation. American Journal of Preventive Medicine, 38(Suppl. 3)S327–332.10.1016/j.amepre.2009.11.017 [DOI] [PubMed] [Google Scholar]

- O’Connor R. J. (2005). What brands are US smokers under 25 choosing? Tobacco Control, 14, 213.10.1136/tc.2004.010736 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Orzechowski and Walker (2011). Tax burden on tobacco (Vol. 45). Arlington, VA: Author; [Google Scholar]

- Pesko M. F., Kruger J., Hyland A. (2012). Cigarette price minimization strategies used by adults. American Journal of Public Health, 102, e19–21.10.2105/ajph.2012.300861 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Ribisl K. M., Williams R. S., Gizlice Z., Herring A. H. (2011). Effectiveness of state and federal government agreements with major credit card and shipping companies to block illegal Internet cigarette sales. PLoS One, 6, e16754.10.1371/journal.pone.0016754 [DOI] [PMC free article] [PubMed] [Google Scholar]

- Samuel K. A., Ribisl K. M., Williams R. S. (2012). Internet cigarette sales and Native American sovereignty: Political and public health contexts. Journal of Public Health Policy, 33, 173–187.10.1057/jphp.2012.4 [DOI] [PubMed] [Google Scholar]

- Shelley D., Cantrell M. J., Moon-Howard J., Ramjohn D. Q., VanDevanter N. (2007). The $5 man: The underground economic response to a large cigarette tax increase in New York City. American Journal of Public Health, 97, 1483–1488.10.2105/AJPH.2005.079921 [DOI] [PMC free article] [PubMed] [Google Scholar]

- U.S. Department of Health and Human Services (2000). Reducing tobacco use: A report of the surgeon general. Atlanta, GA: Author; [Google Scholar]

- White V. M., Gilpin E. A., White M. M., Pierce J. P. (2005). How do smokers control their cigarette expenditures? Nicotine & Tobacco Research, 7, 625–635.10.1080/14622200500184333 [DOI] [PubMed] [Google Scholar]