Abstract

ObjectiveTo estimate the effects of changes in Medicare inpatient hospital prices on hospitals’ overall revenues, operating expenses, profits, assets, and staffing.

Primary Data SourceMedicare hospital cost reports (1996–2009).

Study DesignFor each hospital, we quantify the year-to-year price impacts from changes in the Medicare payment formula. We use cumulative simulated price impacts as instruments for Medicare inpatient revenues. We use a series of two-stage least squares panel data regressions to estimate the effects of changes in Medicare revenues among all hospitals, and separately among not-for-profit versus for-profit hospitals, and among hospitals experiencing real price increases (“gainers”) versus decreases (“losers”).

Principal FindingsMedicare price cuts are associated with reductions in overall revenues even larger than the direct Medicare price effect, consistent with price spillovers. Among not-for-profit hospitals, revenue reductions are fully offset by reductions in operating expenses, and profits are unchanged. Among for-profit hospitals, revenue reductions decrease profits one-for-one. Responses of gainers and losers are roughly symmetrical.

ConclusionsOn average, hospitals do not appear to make up for Medicare cuts by “cost shifting,” but by adjusting their operating expenses over the long run. The Medicare price cuts in the Affordable Care Act will “bend the curve,” that is, significantly slow the growth in hospitals’ total revenues and operating expenses.

Keywords: Medicare, hospitals, health care costs, payment

Congress, when faced with pressure to slow Medicare spending growth, has typically responded by reducing prices paid to providers. The Balanced Budget Act of 1997 (BBA97), for example, cut prices for hospitals and other providers. More recently, the Affordable Care Act of 2010 (ACA) permanently slowed the default growth in Medicare prices for nearly all providers (except physicians) by about 1 percentage point a year. These “cuts” do not actually reduce prices in nominal terms, but prices will be lower under the ACA than they would have been otherwise, and prices will grow more slowly than input prices.

Policy makers’ views on Medicare price cuts diverge sharply. Some view them as unpleasant but the best option for controlling Medicare spending and clearly preferable to increasing the eligibility age or beneficiary cost sharing. Others view them as ineffective in controlling Medicare spending, price-increasing for private payers, and potentially harmful to beneficiaries’ access to care (House Budget Committee 2012). Richard Foster, the former Medicare actuary, viewed the ACA price cuts as unrealistic, saying they “will not be viable in the long range” (Medicare Trustees 2012, p. 277). Foster testified that, because of the ACA, “roughly 15 percent of [medical facilities] would become unprofitable within the 10-year projection period” (Foster 2011).

The wide range of views on Medicare price cuts partly reflects our limited understanding of what happens when Medicare prices grow slowly. In the hospital sector, the effects of slow price growth on hospital operations depend on a hospital’s ability to (1) make up for lost revenues by increasing private prices or adjusting output mix and (2) adjust its cost structure. If hospitals can somehow make up for lost Medicare revenues, then operating expenses would not need to be cut. However, if lost revenues cannot be made up, then the question is whether hospitals are willing and able to reduce their operating expenses. Hospitals may have to reduce total output if marginal cost is increasing, or reduce fixed costs by scaling back its capacity and staffing, or even close. In addition, quality of care may have to be altered depending on how much price and cost are affected.

The impacts of Medicare price cuts might differ depending on ownership. For-profit hospitals, compared to not-for-profit or government hospitals, are more likely to minimize operating costs. In that case, we would expect Medicare price cuts to reduce profits at for-profit hospitals but not necessarily at other hospitals (Medicare Payment Advisory Commission 2012, p. 61).

Most of the existing literature focuses on short-run impacts of one-time Medicare policy changes. In this study, we take advantage of the fact that Congress has made a series of Medicare payment policy changes that have kept Medicare price growth below inflation for most hospitals since the mid-1990s. We use variation among hospitals and over time in the cumulative impact of those payment policy changes to better understand what we might expect under the ACA.

Background

What Is the Medicare Price, and How Does It Change over Time?

The majority of hospitals are paid by Medicare using the inpatient prospective payment system (IPPS). Under the IPPS, the Centers for Medicare & Medicaid Services (CMS) calculate a national “base rate,” or standard price per discharge. Historically, the default year-to-year increase in the national base rate has equaled an index of the inflation in hospital wages and the prices that hospitals pay for land, equipment, and so on (the “hospital market basket index”). Congress has, however, reduced the update below the market basket index in several years, and the ACA reduces future updates to account for economy-wide increases in productivity.1 CMS then adjusts the national base rate based on local hospital wages, rural location, size, medical residents, and share of low-income patients. The price for a specific discharge equals the hospital-specific base rate multiplied by a casemix adjustment based on diagnoses and procedures (Medicare Payment Advisory Commission 2007).

Every component of the IPPS has been updated over time, and nearly all updates have had disproportionate impacts on certain types of hospitals. For example, the BBA97 reduced extra payments for teaching hospitals by 30 percent. As a result of changes in payment policy, some hospitals have faced a series of large Medicare price cuts, others have faced small cuts, and a few have received price increases.

Previous Literature

Previous studies have examined two types of hospital responses to tightening of Medicare payment policy. The first is the effect of Medicare price cuts on the prices paid by private health plans. It is widely believed that hospitals “cost shift,” that is, respond to Medicare price cuts by increasing private prices. However, Frakt (2011), based on a comprehensive literature review, cautions that the evidence is mixed, and that “cost shifting can and has occurred, but usually at a relatively low rate.” More recently, White (2013) finds, contrary to the cost shifting story, that Medicare price cuts lead to lower private prices.

The second type of response is hospitals adjusting their operations, and here the evidence is clearer. Feder, Hadley et al. (1987) studied the effects of Medicare’s switch in the early 1980s from cost reimbursement to the IPPS. Hospitals responded by reducing length of stay and operating expenses per case, more so among hospitals facing the greatest revenue constraints. In a follow-up study, Hadley, Zuckerman et al. (1989) showed that hospitals continued to respond to constrained Medicare revenues by reducing length of stay and operating expenses per case. Cutler (1998) showed that Medicare price cuts occurring between 1985 and 1990 appeared to be offset by increased revenues from other payers (“cost shifting”), whereas Medicare price cuts between 1990 and 1995 resulted in hospitals reducing their operating expenses (“cost cutting”). Cutler attributes the change in hospital responses to a switch in insurance arrangements from passive indemnity plans to managed care plans that actively negotiated prices. Bazzoli, Lindrooth et al. (2004/5) measure the short-term effects of Medicare price changes following the BBA97, and they find that hospitals facing the largest Medicare price cuts reduced staffing and operating expenses per case. Profits were unaffected, implying that lost revenues were fully offset by reduced operating expenses. Dafny (2005) studied the impact of a change in 1988 in the algorithm for assigning patients to diagnosis-related groups (DRGs). She found that hospitals that received a windfall price boost tended to increase their costs per Medicare discharge, and that the increased costs were spread among all DRGs, not just those that generated the increased revenues. Wu and Shen (2011) also find that Medicare price cuts lead to reduced staffing and operating expenses, and they tie these reductions to increases in patient mortality rates. Dranove et al. (2013) examine a different type of negative financial shock to hospitals—investment losses from the stock market downturn in 2008—and find that hospitals adjusted by scaling back unprofitable services and reducing investment in information technology.

This study combines some of the strengths of the previous analyses. Like Dafny (2005), it identifies specific, legislated changes in Medicare payment policy and uses their differential impacts as a source of statistical identification. And, like Feder, Hadley et al. (1987), it takes the perspective of the entire hospital, including Medicare and non-Medicare patients and inpatient and outpatient operations.

This study is unique in its length and recent time frame (1996 through 2009). That period is relevant to the current policy environment because it starts after hospitals had fully adjusted to the IPPS and after the shift to managed care, and includes the BBA97. The time frame is also long enough to allow hospitals to fully adjust their operations. This study also differs from most previous studies in its comparison of gainers versus losers and its comparison of not-for-profit, for-profit, and government facilities.

Methodology

Our main analyses are panel data regressions with the hospital-year as the unit of observation. We include hospital-and year-fixed effects and market-level economic and demographic controls, and we weight our analyses by each hospital’s total output (“discharge equivalents,” described below).2 We use two-stage least squares (2SLS) models, rather than ordinary least squares (OLS), because of the endogeneity of the observed Medicare inpatient price.

Measuring Hospital Output

All of our outcomes—revenues, operating expenses, profits, assets, and staffing—are measured for the entire hospital, including inpatient and outpatient services and Medicare and non-Medicare patients. We wanted to measure each of these outcomes per unit of hospital output to normalize for the scale of operations, which requires some measure of output. Discharges are a natural measure of the volume of output of inpatient services, but the volume of output of outpatient services is more difficult to measure. Outpatient visits are one possibility, but what constitutes a visit is so highly variable as to be nearly meaningless. Therefore, following the adjusted-day concept developed by the American Hospital Association (AHA), we developed the “discharge equivalent” (DCEQ) as our measure of hospital output. DCEQ equals inpatient hospital discharges multiplied by the ratio of total operating expenses over inpatient hospital operating expenses.3 Formally,

| (1) |

where  equals total inpatient discharges at hospital h in year T,

equals total inpatient discharges at hospital h in year T,  equals inpatient operating expenses, and

equals inpatient operating expenses, and  equals total operating expenses. DCEQh,t is used as a denominator for all of the hospital-wide variables.

equals total operating expenses. DCEQh,t is used as a denominator for all of the hospital-wide variables.

Outcomes of Interest

The first set of outcomes of interest include revenues (i.e., revenue from providing patient services, after discounts and contractual allowances), operating expenses (i.e., the costs incurred by the hospital in providing patient care), and profits (i.e., operating income, or the excess of revenues over operating expenses), all measured in real 2009 dollars per DCEQ. Operating expenses are further broken into personnel expenses and non-personnel expenses (rent, equipment, supplies, etc.). By definition, profits equal revenues minus expenses.

The second set of outcomes are the levels of current assets (“cash,” accounts receivables, and other current assets) and the change over the prior year’s total gross fixed assets (i.e., plant, property, and equipment). The third set of outcomes is staffing, measured using full-time equivalents (FTEs). We measure all staff, as well as registered nurses (RNs), licensed practical nurses/licensed vocational nurses, and medical residents. Assets are inflated to 2009, and both assets and staffing are measured per DCEQ.

Policy-Driven Changes in Medicare Inpatient Prices—Six Instruments

Conceptually, we asked the following: Suppose a hospital provided exactly the same set of Medicare inpatient services in year t as in t-1, and that its operating expenses (wages, rent, etc.) grew with the hospital market basket index. How much of a year-to-year financial gain or loss would the hospital experience on those Medicare inpatient services due to changes in Medicare payment policy relative to its overall operations? This follows a large literature (Cutler 1998; Shen 2003; Dafny 2005; Wu 2010).

To construct our six instruments, we started with each element of the Medicare payment formula set to year t-1, and then we changed each element of the payment formula one by one while holding constant the services provided and the mix of patients treated. These six elements are as follows: (1) the standardized payment amounts; (2) the reassignment of hospitals to large urban areas; (3) the reassignment of hospitals to different metropolitan areas (i.e., not where the hospital is physically located); (4) the formula for indirect medical education payments; (5) the formula for disproportionate share hospital payments; and (6) the designation of hospitals as a sole community hospital or Medicare dependent hospital (SCH/MDH), and the formula for SCH/MDH payment boosts.

Formally,

| (2) |

equals the change in the Medicare inpatient price due to policy change p from year t-1 to t in hospital h, inflated to 2009 using the hospital market basket index. An example for a specific hospital (Medicare provider number 010001) is provided in the Appendix.

We then calculate the accumulated policy-driven price change from 1996 through each year, T:

| (3) |

Our goal is to measure the impact of Medicare inpatient payment policy changes on hospital operations overall, including Medicare and non-Medicare patients and inpatient and outpatient services. Therefore, we scale the Medicare payment changes using a Medicare-to-total-discharge ratio, following the literature (Hadley, Zuckerman et al. 1989; Staiger and Gaumer 1992; Cutler 1998; Shen 2003). We extend that concept also to reflect inpatient care as a share of the hospital’s total output. To do this, we multiplied the accumulated policy-driven changes in the Medicare inpatient price by inpatient Medicare discharges as a share of DCEQs in 1996:

| (4a) |

This is equivalent to multiplying the accumulated price changes by two scaling factors: (1) Medicare inpatient discharges as a share of total discharges in 1996 and (2) inpatient hospital operating expenses as a share of total operating expenses in 1996:

|

(4b) |

Note that we fix the number of Medicare discharges and DCEQ at their 1996 values to avoid including potential endogenous hospital behavioral responses in our instruments. For example, if a hospital reduces its share of Medicare patients due to Medicare price reductions, that behavioral response will not affect the calculation of the Medicare price instruments.

First-Stage Estimation

The first stage of our 2SLS model is:

|

(6) |

where h indexes hospitals; t indexes years; div indexes Census division;  is Medicare inpatient revenue per DCEQ, inflated to 2009;

is Medicare inpatient revenue per DCEQ, inflated to 2009;  is the accumulated impact of payment policy p per DCEQ, inflated to 2009; Xh,t is a set of time-variant hospital characteristics (case mix, and the local wage index); ZMSA,t is a set of time-variant characteristics of the market in which the hospital is located (share of the population receiving food stamps, share of the population in poverty, unemployment rate); ϕh is a set of hospital-fixed effects; φdiv,t is a set of Census division year-fixed effects; γp is a set of estimated coefficients on the Medicare price instruments; and ιh,t is a residual. The estimated coefficients from the first-stage regression are reported in the Appendix Table.

is the accumulated impact of payment policy p per DCEQ, inflated to 2009; Xh,t is a set of time-variant hospital characteristics (case mix, and the local wage index); ZMSA,t is a set of time-variant characteristics of the market in which the hospital is located (share of the population receiving food stamps, share of the population in poverty, unemployment rate); ϕh is a set of hospital-fixed effects; φdiv,t is a set of Census division year-fixed effects; γp is a set of estimated coefficients on the Medicare price instruments; and ιh,t is a residual. The estimated coefficients from the first-stage regression are reported in the Appendix Table.

Second-Stage Estimation

In the second stage, we use the predicted Medicare inpatient revenue per DCEQ from the first-stage regression to measure the impact of changes in Medicare revenues on hospital financial condition and staffing. The second-stage model is as follows:

| (6) |

where  is the outcome of interest at hospital h in year t.

is the outcome of interest at hospital h in year t.

Additional Controls

Our panel data analysis includes hospital-fixed effects and Census division year-fixed effects to control for the effects of fixed hospital characteristics and time market-specific factors on hospital costs, which allows us to be parsimonious in the use of additional controls. We include two time-variant hospital characteristics that we expect to be strongly and positively related to the Medicare inpatient price—the Medicare case mix index and the hospital-specific wage index—and we also include hospital market concentration. We include three market-level economic controls that are not directly related to hospital operations but that capture general economic conditions: the share of the population receiving food stamps, the share of the population in poverty, and the share of the labor force unemployed.

Subgroup Analyses

We wanted to measure effects separately for different ownership types (not-for-profit, for-profit, and government), and for gainers versus losers. To do this in a 2SLS framework, we created sets of endogenous variables that were interacted with subgroup dummies, and we created sets of instruments that were similarly interacted with subgroup dummies. For example, in the gainers versus losers analysis, we used 2 endogenous variables (Medicare price per DCEQ*gainer and Medicare price per DCEQ*loser) and 12 instruments.

Data Sources

All financial outcomes are from the Medicare hospital cost reports (HCRs). The reporting periods for HCRs differ depending on each hospital’s fiscal year. We allocated totals from each HCR to each calendar year based on the share of the calendar year covered by the HCR. Staffing is from the AHA annual survey—those data were only available for 1996–2007. The simulation of the impact of Medicare payment policy changes uses various sources from CMS described in White (2013). That simulation uses the HCRs, the impact file, the provider-specific file, and regulations published in the Federal Register and the Code of Federal Regulations.

We start with the universe of Medicare-certified short-stay hospitals active at any point from 1996 through 2009 (n = 5,529)—over that period, those facilities provided 160 million Medicare discharges and 480 million total discharges. We then apply several exclusion criteria. The first excludes “critical access” hospitals (CAHs) and hospitals that converted at some point to become a CAH (n = 1,245). CAHs are small, rural hospitals that have been permitted to switch back from the IPPS to cost reimbursement. CAHs were excluded because the choice of whether and when to convert to CAH status is likely driven by financial considerations, which would introduce endogeneity into the analysis. Although a large number of hospitals are CAHs, they only account for 4 percent of Medicare discharges. We also exclude all hospitals in Maryland, where rates for Medicare patients are set by its rate-setting commission under a CMS waiver, and all hospitals that had extreme values either for the Medicare inpatient price or net patient revenue, operating expenses, profits, current assets, or fixed assets (n = 1,589).4 Lastly, the sample further reduced down to hospitals that had valid data to simulate at least one of the six IVs for all the years. The final sample comprises 2,043 hospitals between 1996 and 2009, for a total of 25,284 hospital-years, representing 52 percent of total DCEQs. All regressions are performed using the Stata “xtivreg2” command and are weighted by DCEQh,t. Standard errors account for clustering at the hospital level using the “robust cluster()” command.

Results

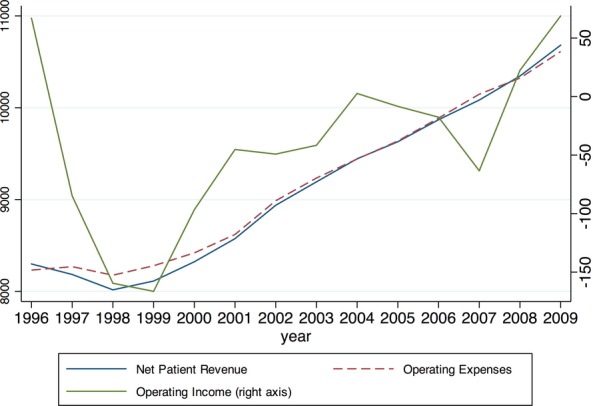

Figure 1 shows the national trends in revenues, operating expenses, and profits per DCEQ over the study period, all inflated to 2009. By far the most significant Medicare policy change affecting hospitals’ revenues was the BBA97. In the years after the BBA97 cuts, real revenues per DCEQ declined sharply, as did profits. Over the 2000s, real profits per DCEQ gradually returned to pre-BBA97 levels, due to a combination of more stable Medicare payment policy and slow growth in operating expenses.

Figure 1.

Trends in Revenues, Operating Expenses, and Profits. (Source: Author’s analysis)

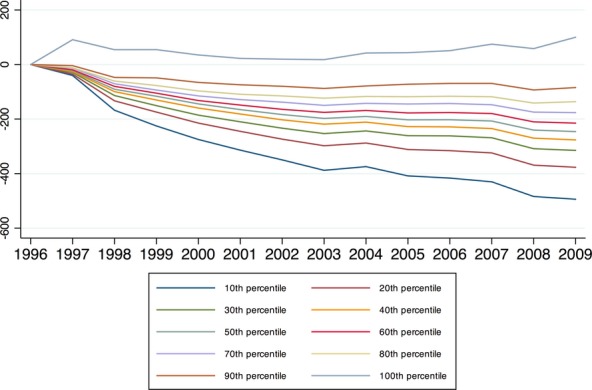

Figure 2 categorizes hospitals into deciles by the ultimate accumulated Medicare payment impact per DCEQ between 1996 and 2009 and graphs the cumulative Medicare payment impact through each year (i.e., the sum of our six instruments). Medicare inpatient payment policy has been tightened several times, with effects that have varied widely. Although most hospitals experienced policy-driven declines in real Medicare inpatient revenues over the study period, some experienced larger declines than others, and some experienced policy-driven increases. The median hospital experienced a cumulative Medicare inpatient price cut of about $250 per DCEQ, which is roughly 2.5 percent of total revenues. The second important point from Figure 2 is that Medicare payment impacts on hospitals persist over time—hospitals that faced the greatest payment cuts in 1997 were also the ones that faced the largest negative impact throughout the study period.

Figure 2.

Accumulated Medicare Payment Policy Impacts, 1996–2009. (Source: Authors’ calculations)

Table 1 describes the differences between hospitals that experienced larger versus smaller accumulated Medicare price cuts. We divide hospitals into three groups based on the accumulated policy-driven changes in Medicare inpatient revenues per DCEQ from 1996 to 2009: large cut (bottom quartile), medium cut (middle two quartiles), and small cut or increase (top quartile). The hospitals that were most negatively affected by Medicare policy changes (column 2) differ from other hospitals: they tended to receive higher Medicare prices and higher overall revenues per DCEQ in 1996, they are almost all in urban areas, and they are much more likely to be teaching hospitals and somewhat more likely to be not-for-profit ones. The hospitals that were the least negatively impacted (column 4) tended to be located in rural areas, and almost none were teaching hospitals. Changes in standardized amounts are the primary factor that differentiates large-versus small-cut hospitals, with MSA reclassifications and IME payments playing secondary roles.

Table 1.

Hospital Revenues, Operating Expenses, and Profits, 1996–2009

| Hospitals Grouped by Accumulated Policy-Driven Change in Medicare Revenue per Discharge Equivalent (DCEQ), 1996–2009 | ||||

|---|---|---|---|---|

| All Hospitals | Low | Med | High | |

| Accumulated policy-driven change in Medicare inpatient revenue per Medicare discharge | −763 | −1,021 | −769 | −291 |

| Accumulated policy-driven change in Medicare inpatient revenue per DCEQ | −166 | −267 | −152 | −32 |

| Components of policy-driven change in Medicare revenue per DCEQ | ||||

| Standardized amount | −164 | −228 | −150 | −94 |

| Urban-rural reclassification | −2 | −4 | −2 | 1 |

| MSA reclassification | 14 | 2 | 8 | 52 |

| Indirect medical education | −14 | −32 | −7 | −2 |

| Disproportionate share hospital | −2 | −6 | −2 | 6 |

| Sole community hospital/Medicare dependent hospital | 1 | 0 | 0 | 4 |

| Medicare inpatient revenue per Medicare discharge, 1996 | 11,078 | 12,997 | 10,756 | 8,743 |

| Average annual growth, 1996–2009 (%) | −0.4 | −0.8 | −0.4 | 0.3 |

| Medicare inpatient revenue per DCEQ, 1996 | 2,463 | 3,480 | 2,174 | 1,603 |

| Average annual growth, 1996–2009 (%) | −1.3 | −2.3 | −0.8 | 0.0 |

| Revenue per DCEQ, 1996 | 9,266 | 11,350 | 8,760 | 7,227 |

| Average annual growth, 1996–2009 (%) | 1.7 | 0.9 | 2.0 | 2.8 |

| Operating expenses per DCEQ, 1996 | 9,189 | 11,410 | 8,623 | 7,098 |

| Average annual growth, 1996–2009 (%) | 1.7 | 0.9 | 2.1 | 2.8 |

| Profit per DCEQ, 1996 | 77 | −61 | 137 | 130 |

| Average annual growth, 1996–2009 (%) | −0.1 | 1.8 | 0.7 | −2.0 |

| Hospital characteristics (1995–2009) | ||||

| Teaching (%) | 12 | 30 | 6 | 1 |

| Ownership (%, number of hospitals in parentheses) | ||||

| Not-for-profit | 76 (1,553) | 83 (397) | 75 (791) | 68 (344) |

| For-profit | 11 (221) | 9 (45) | 11 (116) | 13 (64) |

| Government | 13 (270) | 8 (38) | 14 (148) | 20 (100) |

| Patient mix (share of discharges, %) | ||||

| Medicare | 37 | 39 | 36 | 39 |

| Medicaid | 14 | 13 | 15 | 16 |

| Other | 49 | 48 | 50 | 45 |

| Outpatient gross revenue as a share of total gross revenue (%) | 39 | 33 | 39 | 46 |

| Population characteristics (2000) | ||||

| Urban (%) | 85 | 98 | 90 | 45 |

| Poverty (%) | 13 | 13 | 12 | 14 |

| Number of hospitals | 2,044 | 480 | 1,055 | 508 |

| Number of DCEQs, 1996–2009 (100s of millions) | 4.1 | 1.2 | 2.3 | 0.7 |

Note. Revenues, operating expenses, and profits are inflated to 2009 using the CMS hospital market basket index. All means are weighted by the number of discharge equivalents (DCEQ).

Source: Authors’ calculations.

The most adversely impacted hospitals experienced the slowest growth in Medicare revenues—this is as expected, and merely confirms the relevance of our instruments. The most adversely impacted hospitals also had the slowest growth in overall net revenues and the slowest growth in operating expenses. These descriptive findings suggest that hospitals facing large Medicare cuts do not make up for lost Medicare revenues with increased revenues from other payers—if they did, their overall revenue trends would be similar to other hospitals. The most adversely impacted hospitals started the period with the smallest profits, and their profits fell, on average, over the period. The most favorably impacted hospitals, in contrast, started with higher profits and experienced increases in profits. The levels and trends in profits suggest that changes in Medicare payment policy exacerbated, rather than corrected, pre-BBA97 disparities in profits among hospitals.

The first-stage regression results, shown in Table S1, indicate that the excluded instruments are strong predictors of Medicare inpatient revenues per DCEQ (the f-statistic is 37.2). The 2SLS regression results are presented in Table 2. The regression coefficients in Table 2 represent the dollar change in each financial outcome per DCEQ in response to a $1 policy-driven change in Medicare inpatient revenues per DCEQ. In the main results (“all hospitals”), a $1 reduction in Medicare inpatient revenues is associated with a $1.55 reduction in overall net patient revenues. This finding suggests that hospitals do not recoup lost Medicare revenues through cost shifting, and, in fact, a loss of Medicare revenue appears to have a negative spillover effect on total revenues. This finding is consistent with inpatient price spillovers, from Medicare to the privately insured, as reported in White (2013).

Table 2.

Estimated Effects on Hospital Finances of Policy-Driven Changes in Medicare Inpatient Revenue (standard errors in parentheses)

| Dependent Variables ($) | ||||||||

|---|---|---|---|---|---|---|---|---|

| Revenues | Operating Expenses | Profits | Personnel Expenses | Non-Personnel Expenses | Current Assets (cash) | Accumulation of Fixed Assets | ||

| Estimated effect of a $1 reduction in Medicare inpatient revenues | ||||||||

| All hospitals | −1.55*** (0.235) | −1.40*** (0.219) | −0.15 (0.102) | −0.82*** (0.130) | −0.59*** (0.137) | 0.00 (0.323) | −1.25*** (0.231) | |

| For-profit versus not-for-profit | ||||||||

| For-profit | −4.73*** (0.809) | −3.70*** (0.739) | −1.03*** (0.284) | −1.58*** (0.333) | −2.12*** (0.486) | −2.41*** (0.656) | −3.72*** (0.828) | |

| Government | −1.37 (0.858) | −0.95 (0.882) | −0.42 (0.424) | −0.35 (0.506) | −0.60 (0.690) | −0.08 (1.132) | −0.32 (0.941) | |

| Not-for-profit (NFP) | −1.04***(0.266) | −1.02*** (0.251) | −0.02 (0.113) | −0.74*** (0.154) | −0.28* (0.156) | 0.47 (0.387) | −0.80*** (0.278) | |

| Difference, for-profit relative to NFP | −3.69*** (0.855) | −2.65***(0.769) | −1.04*** (0.315) | −0.81** (0.363) | −1.84*** (0.515) | −2.88*** (0.745) | −2.80*** (0.881) | |

| Difference, government relative to NFP | −0.41 (0.877) | −0.06 (0.899) | −0.35 (0.430) | 0.35 (0.530) | −0.41 (0.692) | −0.58 (1.178) | 0.36 (0.952) | |

| Gainers versus Losers | ||||||||

| Estimated effect of a $1 increase in Medicare inpatient revenues | ||||||||

| Gainer hospitals | 1.87*** (0.231) | 1.22*** (0.193) | 0.65*** (0.136) | 0.49*** (0.155) | 0.73*** (0.165) | −1.27*** (0.303) | 0.88*** (0.218) | |

| Estimated effect of a $1 reduction in Medicare inpatient revenues | ||||||||

| Loser hospitals | −1.64*** (0.233) | −1.45*** (0.221) | −0.20** (0.097) | −0.82*** (0.130) | −0.62*** (0.136) | −0.04 (0.323) | −1.28*** (0.230) | |

| Difference, gainers relative to losers | 0.21 (0.260) | −0.23 (0.227) | 0.44*** (0.151) | −0.38*** (0.144) | 0.15 (0.166) | −1.27*** (0.376) | −0.45* (0.254) | |

| Observations | 25,284 | 25,284 | 25,284 | 25,287 | 25,284 | 25,287 | 25,287 | |

Note.

p < .01,

p < .05,

p < .1.

Estimated effects are from regressions of the financial outcomes (measured in dollars per discharge equivalent) on Medicare inpatient revenues (also measured in dollars per discharge equivalent). The unit of analysis is the hospital-year (1996–2009). Each cell represents a separate regression analysis, and reports the estimated coefficient on Medicare inpatient revenues per discharge equivalent (DCEQ) from a two-stage least squares regression. Gainers are defined as cumulative change from 1996 to 2009 in Medicare inpatient revenue per DCEQ greater than or equal to 0. Medicare inpatient revenues and all outcomes are all inflated to 2009 using the CMS hospital market basket index. All regressions include hospital-and year-fixed effects and market controls (coefficients not shown), and are weighted by DCEQ.

Source: Authors’ calculations.

Of the $1.55 reduction in net patient revenue, 90 percent ($1.40) is offset by reduced operating expenses (p < .01), and $0.15 appears as lost profits (not statistically significant). About three-fifths of the reduction in operating expenses is accomplished through reductions in personnel costs, with the remainder through non-personnel costs. Reduced Medicare inpatient revenues are not associated with any changes in current assets (“cash”) but are associated with large reductions in the accumulation of fixed assets.

The middle panel of Table 2 reports separate results for gainer hospitals versus loser hospitals. In general, losers’ responses to changes in Medicare revenues were symmetrical to gainers’ responses, though generally larger. One interesting difference between gainers and losers is that gainers retained a relatively large share of revenue increases as profits ($0.65 in profit out of $1.87 in revenues).

The results in Table 3 indicate that staffing is very responsive to Medicare revenue changes. For each $100,000 reduction in Medicare inpatient revenues, a hospital reduces its total staff by 1.69 FTEs. Of that staffing reduction, one-fifth is RNs (0.31 FTEs). Losers appear to cut staff more than gainers add staff, which is consistent with the finding that gainers retained more of the revenue increase as profits.5

Table 3.

Estimated Effects on Hospital Staffing of Policy-Driven Changes in Medicare Inpatient Revenue (standard errors in parentheses)

| Dependent Variables (full-time equivalents [FTEs]) | |||||

|---|---|---|---|---|---|

| Registered Nurses | Licensed Practical Nurses/Licensed Vocational Nurses | Medical Residents | All Staff | ||

| Estimated effect of a $100,000 reduction in Medicare inpatient revenues | |||||

| All hospitals | −0.31*** (0.054) | −0.06*** (0.012) | −0.02* (0.012) | −1.69*** (0.180) | |

| For-profit versus not-for-profit | |||||

| For-profit | −0.44** (0.195) | −0.06 (0.043) | −0.00 (0.034) | −2.47*** (0.787) | |

| Government | 0.19 (0.219) | −0.12*** (0.040) | −0.03 (0.103) | −0.98 (0.761) | |

| Not-for-profit (NFP) | −0.33*** (0.062) | −0.05*** (0.015) | −0.02 (0.016) | −1.62*** (0.214) | |

| Difference, for-profit relative to NFP | −0.10 (0.209) | 0.00 (0.048) | 0.01 (0.042) | −0.83 (0.848) | |

| Difference, government relative to NFP | 0.49** (0.227) | −0.07* (0.043) | 0.00 (0.103) | 0.49 (0.792) | |

| Gainers versus Losers | |||||

| Estimated effect of a $100,000 increase in Medicare inpatient revenues | |||||

| Gainers | 0.42*** (0.056) | −0.02 (0.018) | 0.06*** (0.018) | 0.94*** (0.315) | |

| Estimated effect of a $100,000 reduction in Medicare inpatient revenues | |||||

| Losers | −0.33*** (0.055) | −0.06*** (0.013) | −0.02* (0.012) | −1.70*** (0.183) | |

| Difference (gainers relative to losers) | 0.01 (0.097) | −0.07*** (0.022) | 0.04** (0.018) | −0.86*** (0.269) | |

| Observations | 21,375 | 21,375 | 21,375 | 21,375 | |

Note.

p < .01,

p < .05,

p < .1.

Estimated effects are from regressions of the financial outcomes (measured in dollars per discharge equivalent) on Medicare inpatient revenues (also measured in dollars per discharge equivalent). The unit of analysis is the hospital-year (1996–2009). Each cell represents a separate regression analysis and reports the estimated coefficient on Medicare inpatient revenues per discharge equivalent (DCEQ) from a two-stage least squares regression multiplied by 100,000. Gainers are defined as cumulative change from 1996 to 2009 in Medicare inpatient revenue per DCEQ greater than or equal to 0. Medicare inpatient revenues are all inflated to 2009 using the CMS hospital market basket index. All regressions include hospital-and year-fixed effects and market controls (coefficients not shown), and are weighted by DCEQ.

Source: Authors’ calculations.

The bottom panels of Tables 2 and 3 report results separately by hospital ownership status. Not-for-profit hospitals’ profits were unchanged by Medicare revenue losses, because their lost revenues were fully offset by reductions in operating expenses. For-profit hospitals were generally more affected by, and more responsive to, reductions in Medicare revenues than not-for-profit hospitals. For-profits reduced operating expenses more aggressively than not-for-profits but faced even larger reductions in revenues, suggesting a fairly major contraction in the intensity of services provided. The net result for for-profits was a reduction in profits roughly equal to the reduction in Medicare revenues. Government hospitals appear to be generally less responsive to the loss of Medicare revenues in their staffing levels and personnel expenses.

To understand the likely impact of the ACA, we simulated the impact of an 11 percent reduction in real Medicare prices—this equals the accumulated effect over 10 years of a 1.1 percent cut per year, which is roughly equal to the productivity adjustments in the ACA. In 2009, average Medicare payment per DCEQ is $1,884, so an 11 percent reduction is $207 dollars—this is similar in magnitude to the accumulated cuts experienced by the median hospital from 1996 to 2009. Based on our regression results, that cut would lead to $321 reduction in net patient revenue per DCEQ, $290 in operating expenses per DCEQ, and $30 in profits per DCEQ. If profits per DCEQ were adjusted downward by $30, the share of hospitals operating at a loss would increase by roughly 15 percentage points, from 10 percent to 25 percent.

Discussion

Based on hospitals’ responses to the BBA97 and subsequent tinkering, several conclusions are apparent. First, hospitals’ total revenues will drop under the ACA by more than we would expect based just on the Medicare price changes. This finding is consistent with the price spillovers from Medicare to the privately insured reported in White (2013). Second, hospitals will not simply go about their business as usual—about 90 percent of lost revenues will be offset by reduced operating expenses, accomplished mainly through savings on personnel, but also through savings on non-personnel costs. Third, hospitals will delay or forgo capital improvements. There are two broad viewpoints on hospitals’ revenues and financial condition. One viewpoint is that hospitals’ operating expenses and output are inflexible and determined by factors beyond the hospital’s control. In that view of the world, hospitals facing Medicare cuts must either recoup lost revenues from private payers or go out of business. Stensland, Gaumer et al. (2010) offer a different viewpoint, which is that hospitals’ operating expenses are fairly flexible and can expand or contract depending on resource availability. The results of this analysis clearly support the second viewpoint and the idea that hospitals tighten, or loosen, their belts as needed.

The fact that hospitals’ operating expenses are flexible has several implications. The first is that the ACA price cuts will help bend the hospital spending curve downward and, conversely, repealing those price cuts would bend it back upward. Over the long run, Medicare price cuts do not result in hospitals shifting costs to other payers or to more-profitable services; they instead constrain overall operations and resource use. Second, our results support the view of hospitals, not as typical cost-minimizing firms, but as revenue-seekers who adjust costs, and quality, up or down so as to roughly equal whatever revenues they manage to obtain. Newhouse (1970) describes the hospital industry as aspiring to a “Cadillac” level of quality. Our results suggest that hospitals, if forced to, will instead turn out Buicks. The third implication is that hospitals’ ability to increase productivity is not known because it has not really been tested. If hospitals were cost minimizers, then we could use historical data on expenses and output to measure productivity growth, and we could safely assume that productivity growth was at or near its maximum. However, hospitals are not cost minimizers, so historical data do not reflect maximum productivity growth, and they instead reflect the trends in available revenues. Although Medicare payment policy has been relatively tight since the mid-1990s, hospitals have extracted price increases from private plans well in excess of trends in input prices, which likely drove up overall operating expenses and drove down measured productivity growth.

These findings are mixed news for supporters of the ACA. From a financial standpoint, the ACA cuts clearly will help bend the hospital spending curve downward, both for Medicare and for other payers as well. The claim that large numbers of hospitals will be driven to insolvency by the ACA cuts appears to hold true only for for-profit hospitals—not-for-profit hospitals, over the period examined, fully adjusted their operating expenses to match their newly constrained revenues. Hospitals’ operations will clearly have to adjust in coming years to a more constrained revenue environment. If hospitals can manage to maintain or improve their quality of care, then the result will be improved efficiency.

Acknowledgments

Joint Acknowledgment/Disclosure Statement: The authors gratefully acknowledge the National Institute for Health Care Reform (http://www.nihcr.org) and the assistance of a Technical Advisory Panel (Herbert Wong, Stephanie Cameron, Jack Hadley, Tracy Yee, James Reschovsky, and Jeff Stensland) and two anonymous reviewers. The TAP provided insight and feedback on an earlier draft of this publication. The views expressed in this paper are the authors’ and should not be interpreted as those of the TAP or the employers of the member of the TAP.

Disclosures

None.

Disclaimers

None.

Notes

CMS’s estimate of the 10-year average increase in multifactor productivity was 1.0 percent in 2011, and 0.7 percent in 2012—both of these are lower than the long-run average, due to negative productivity growth during the Great Recession.

We weight our analyses by hospital output for two reasons. First, financial data reported by large hospitals are likely of higher quality (i.e., less subject to misreporting error) than data reported by small hospitals. Second, we wanted our results to be interpretable as reflecting industry-wide responses. We performed unweighted regressions as an alternative specification test, and we obtained results generally similar to our weighted results (see Appendix).

DCEQ is similar to the “adjusted admission” used by Bazzoli et al. (2004/5) in that it combines inpatient and outpatient volume. DCEQ differs from adjusted admissions in that it uses operating expenses, rather than gross revenues, to measure inpatient output relative to outpatient output.

An extreme value was defined as being outside a percentile range in a given year (1st–99th for the Medicare price, and 2nd–98th for total net revenues per discharge equivalent), or changing from 1 year to the next by a factor of less than 0.5 or more than 2.

Dranove et al. (2013) examine the effects of stock market losses on hospitals’ staffing and find no effects. The difference between our staffing results and theirs may be due to differences in the nature of the financial shocks (a reduction in payment rates vs a reduction in assets). Also, because Garthwaite examine a relatively recent event, their data may not have included a long enough post-period to detect staffing adjustments.

Supporting Information

Additional Supporting Information may be found in the online version of this article:

Author Matrix.

Table S1: First-Stage Regression Coefficients (dependent variable: Medicare inpatient revenue per discharge equivalent [DCEQ], standard errors in parentheses).

Table S2: Illustration of Calculation of Six Instruments: Southeast Alabama Medical Center (Medicare provider number: 010001).

Table S3: Estimated Effects on Hospital Finances of Policy-Driven Changes in Medicare Inpatient Revenue (standard errors in parentheses), Unweighted Regressions.

Table S4: Estimated Effects on Hospital Staffing of Policy-Driven Changes in Medicare Inpatient Revenue (standard errors in parentheses), Unweighted Regressions.

References

- Bazzoli GJ, Lindrooth RC, Hasnain-Wynia R, Needleman J. The Balanced Budget Act of 1997 and U.S. Hospital Operations. Inquiry. 2004;41(4):401–17. doi: 10.5034/inquiryjrnl_41.4.401. /5. “. [DOI] [PubMed] [Google Scholar]

- Cutler DM. Cost Shifting or Cost Cutting? The Incidence of Reductions in Medicare Payments. Tax Policy and the Economy. 1998;12(1):1–27. [Google Scholar]

- Dafny LS. How Do Hospitals Respond to Price Changes? American Economic Review. 2005;95(5):1525–47. doi: 10.1257/000282805775014236. [DOI] [PubMed] [Google Scholar]

- Dranove D, Garthwaite C, Ody C. How Do Hospitals Respond to Negative Financial Shocks? The Impact of the 2008 Stock Market Crash. Cambridge, MA: NBER; 2013. [Google Scholar]

- Feder J, Hadley J, Zuckerman S. How Did Medicare’s Prospective Payment System Affect Hospitals? New England Journal of Medicine. 1987;317(14):867–73. doi: 10.1056/NEJM198710013171405. [DOI] [PubMed] [Google Scholar]

- Foster RS. The Estimated Effect of the Affordable Care Act on Medicare and Medicaid Outlays and Total National Health Care Expenditures. Testimony before the House Committee on the Budget; 2011. [Google Scholar]

- Frakt AB. How Much Do Hospitals Cost Shift? A Review of the Evidence. Milbank Quarterly. 2011;89(1):90–130. doi: 10.1111/j.1468-0009.2011.00621.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Hadley J, Zuckerman S, Feder J. Profits and Fiscal Pressure in the Prospective Payment System: Their Impacts on Hospitals. Inquiry. 1989;26:354–65. [PubMed] [Google Scholar]

- House Budget Committee. The Path to Prosperity: A Blueprint for American Renewal. Washington, DC: 2012. [Google Scholar]

- Medicare Payment Advisory Commission. Hospital Acute Inpatient Services Payment System. Washington, DC: 2007. Payment Basics. [Google Scholar]

- Medicare Payment Advisory Commission. Medicare Payment Policy. Washington, DC: 2012. [Google Scholar]

- Medicare Trustees. 2012 Annual Report of the Boards of Trustees of the Federal Hospital Insurance And Federal Supplementary Medical Insurance Trust Funds. Washington, DC: 2012. [Google Scholar]

- Newhouse JP. Toward a Theory of Nonprofit Institutions: An Economic Model of a Hospital. American Economic Review. 1970;60(1):64–74. [Google Scholar]

- Shen Y-C. The Effect of Financial Pressure on the Quality of Care in Hospitals. Journal of Health Economics. 2003;22(2):243–69. doi: 10.1016/S0167-6296(02)00124-8. [DOI] [PubMed] [Google Scholar]

- Staiger D, Gaumer GL. The Impact of Financial Pressure on Quality of Care in Hospitals: Post-Admission Mortality under Medicare’s Prospective Payment System. Cambridge, MA: Abt Associates, Inc; 1992. [Google Scholar]

- Stensland J, Gaumer ZR, Miller ME. Private-Payer Profits Can Induce Negative Medicare Margins. Health Affairs. 2010;29(5):1045–51. doi: 10.1377/hlthaff.2009.0599. [DOI] [PubMed] [Google Scholar]

- White C. Contrary To Cost-Shift Theory, Lower Medicare Hospital Payment Rates for Inpatient Care Lead to Lower Private Payment Rates. Health Affairs. 2013;32(5):935–43. doi: 10.1377/hlthaff.2012.0332. [DOI] [PubMed] [Google Scholar]

- Wu VY. Hospital Cost Shifting Revisited: New Evidence from the Balanced Budget Act of 1997. International Journal of Health Care Finance and Economics. 2010;10(1):61–83. doi: 10.1007/s10754-009-9071-5. [DOI] [PubMed] [Google Scholar]

- Wu VY, Shen Y-C. The Long-Term Impact of Medicare Payment Reductions on Patient Outcomes. Cambridge, MA: NBER; 2011. NBER Working Paper. [DOI] [PMC free article] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Author Matrix.

Table S1: First-Stage Regression Coefficients (dependent variable: Medicare inpatient revenue per discharge equivalent [DCEQ], standard errors in parentheses).

Table S2: Illustration of Calculation of Six Instruments: Southeast Alabama Medical Center (Medicare provider number: 010001).

Table S3: Estimated Effects on Hospital Finances of Policy-Driven Changes in Medicare Inpatient Revenue (standard errors in parentheses), Unweighted Regressions.

Table S4: Estimated Effects on Hospital Staffing of Policy-Driven Changes in Medicare Inpatient Revenue (standard errors in parentheses), Unweighted Regressions.