Abstract

Objective

Describe the trends in enrollment and renewal in the Alabama Children's Health Insurance Plan (CHIP), ALL Kids, since its creation in 1998, and to estimate the effect that an annual premium increase, along with coincident increases in service copays, had on the decision to renew participation.

Background:

Unlike many other CHIP programs, ALL Kids is a standalone program that provides year long enrollment and contracts with the state's Blue Cross and Blue Shield program for its network of providers and its provider fee structure. In October 2003 premiums for individual coverage were increased by $50 per year and copays by $1 to $3 per visit.

Population Studied

This study is based upon a sample of 569,650 person-year observations of 230,255 children enrolled in the ALL Kids program between 1999 and 2009.

Study Design

The study models enrollment as a time series of cross section renewal decisions and specifies a series of linear probability regression models to estimate the effect of changes in the premium shift on the decision to renew. A second analysis includes interaction effects of the premiums shift with demographics, health status, income and previous enrollment to estimate differential response across subgroups.

Principal Findings

The increases in premiums and copays are estimated to have reduced program renewals by 6.1 to 8.3 percent depending upon how much time one allows for families to renew. Families with a child who has a chronic condition were more likely to renew coverage. However, those with chronic conditions, African-Americans and those with lower family incomes were more price-sensitive.

Conclusions

An increase in annual premiums and visit copays had a modest impact on program reenrollment with effects comparable to those found in Florida, New Hampshire, Kansas and Arizona, but smaller than those in Kentucky and Georgia.

Keywords: CHIP, Insurance, Premiums, Enrollment, State Programs, Plan Participation, Health Economics, Medicaid, Alabama, Retention

The purpose of this paper is two-fold: first, to describe the trends in enrollment and renewal in the Alabama Children's Health Insurance Plan (CHIP), ALL Kids, since its creation in 1998, and second, to estimate the effect that the annual premium increase, along with coincident increases in service copays, had on the decision to renew. The analysis also explores differences in renewal behavior across enrollee characteristics with particular attention given to the effects of children's health status and family income. All Kids is somewhat unusual in that it is a standalone program with an annual rather than monthly premium, and it uses the state's Blue Cross Blue Shield network of providers and provider payment structures rather than those of Medicaid. Using data on reenrollment over the 1999 to 2009 period, we find that a $50 increase in annual premiums together with a $1 to $3 increase in per visit copays decreased enrollment by 6.1 to 8.3 percent, depending upon how much time one allows for children to be reenrolled. Families with a child who has a chronic condition were more likely to renew coverage. However, those with chronic conditions, African-Americans and those with lower family incomes were more price-sensitive.

Background

ALL Kids was established in October 1998 as a stand-alone program, independent of Alabama Medicaid. It is one of 17 states in 2012 that have CHIPs that are separate from the state Medicaid program. ALL Kids provides coverage to children through age 18 with family incomes between 100 and 200 percent of the Federal Poverty Level (FPL). In October 2009, eligibility was expanded to those with family incomes up to 300 percent of the FPL. Unlike Alabama Medicaid, which contracts with specific providers for services, establishes its own fee schedules, and has annual limits on the volume of service a recipient may use, ALL Kids contracts with Blue Cross and Blue Shield of Alabama (BCBS) to use its network of providers and to pay BCBS negotiated fees. BCBS also serves as the claims administrator for the ALL Kids program.

While many states employed a monthly per child premium structure, Alabama did not. Instead, it assessed an annual premium with an implicit 12 month insurance period. From the inception of the program, there have been two premium rates. There was initially no premium for children with family incomes between 101 and 150 percent of the FPL. Families with incomes between 151 and 200 percent paid an annual premium of $50 per child with $150 maximum per family. There were copayments associated with the use of many health services for those in the upper premium category. Beginning in October 2003, new higher premiums were introduced. Those with family incomes between 101 and 150 percent of the FPL faced a $50 annual premium per child with a $150 family maximum. Those with incomes between 151 and 200 percent of the FPL paid a $100 annual premium per child with a $300 per family maximum. At the same time, copayments increased as well. For example, non-preventive service office visits increased from $0 to $3 for those below the FPL and from $3 to $5 for those between 101 and 150 percent of the FPL. Copayments for branded prescription drugs increased from $0 to $3 and $3 to $5 for lower and higher income groups. Copayments for generic drugs increased from $0 to $1 and $1 to $2, respectively, for the two groups. For a more detailed description and analysis of the copay changes see Sen et al. (2012). When eligibility was raised in October of 2009, the program simply extended the premium and copays in the higher category to those with family incomes of up to 300 percent of the FPL.

As of January 2008, 38 states charged premiums for at least some participants in the CHIP programs in their states (Cohen-Ross et al., 2008). The states have undertaken these steps in an effort to ease the financial burden on state budgets. However, there has been ongoing concern that the premium contributions have the effect of limiting access to the programs among needy families. Artiga and O'Malley (2005) summarized the early literature that attempted to quantify the enrollment response to higher premiums. These studies, many of which found evidence of strong premium sensitivity, typically relied on simple pre-post comparisons of enrollment, or were based on surveys of program participants.

A series of studies using data from six states have rigorously attempted to estimate the effects of the introduction or expansion of CHIP premiums on continued participation. Much of this work has been undertaken by Marton and colleagues. In perhaps the most comprehensive work, Marton and Talbert (2010) examined the effects of the introduction of a $20 per child per month ($240 per year) premium on those participating in the Kentucky CHIP program. The premium contribution was introduced in 2003, and was applicable to those with family incomes between 151 and 200 percent of the FPL. Using enrollment data from the December 2001 through August 2004 period, they found that, controlling for other factors, the higher premium was associated with an 8.3 percent reduction in the probability of renewing in the 3 months following the increase. However, many of these children were able to enroll in the Kentucky Medicaid program. If this option was ignored, the probability of not renewing doubled to approximately 16 percent. They also found that there were no meaningful differences in premium effects among those with and without various health conditions.

Marton's findings with respect to the Kentucky program vary a bit across his studies, largely because of somewhat different empirical specifications. Marton, Ketsche, & Zhou (2010) found that the probability of exiting to uninsured status was 10.3 percent while the total effect was a 16 percent reduction. Kenney, Marton, McFeeters, and Costich (2007) and Kenney, Allison, Costich, Marton, and McFeeters (2006–2007) found that the new premium reduced enrollment in the premium paying group by 18 percent.

Because Kentucky imposes a monthly premium, Marton and his colleagues employ a proportional hazard model to examine the probability of maintaining enrollment each month. Two alternative hazards are considered: Dropping out of public coverage entirely, or dropping out of the CHIP program, but being newly enrolled in the Medicaid program. This approach was followed in the other state studies reported below.

To comply with the federal CHIP requirements, in 1998 Florida had to reduce its earlier demonstration program monthly premium contribution from a range of premiums based on family income to a single contribution level of $15 per month for those below 200 percent of the FPL. Shenkman et al. (2002) found that, at the mean level of premium changes, a $5 lower monthly ($60 annual) premium was associated with a 2 to 3 percent lower probability of disenrolling.

Georgia increased its CHIP premium contribution in mid 2004. Previously, the rates ranged from $10 to $20 per month for those between 151 and 235 percent of the FPL. They were increased to between $20 and $70 ($240 to $840 per year). Marton et al. (2010) found a short run probability of exit of 18.3 percent, with 14.1 percent exiting to uninsured status.

In Arizona a $10 monthly ($120 annual) premium contribution was newly required of those below 150 percent of the FPL. This was introduced in mid-2004. Kenney et al. (2007) used enrollment data from the July 2001 through December 2005 period and concluded that the premium reduced enrollment by about 5 percent.

In a study of Kansas and New Hampshire (as well as Kentucky) CHIP programs, Kenney et al. (2006–2007) used time series regression analysis as well as proportional hazard models. Kansas raised its premium contributions from $10 to $30 and then back to $20 per month ($240 per year) in 2003 for those with family incomes between 151 and 175 percent of the FPL. It changed from $25 to $45 and then back to $30 for those between 176 and 200 percent of the FPL. The time series estimates implied that Kansas caseloads were reduced by 4.1 percent. New Hampshire raised monthly premium contributions in January of 2003. Those with incomes between 185 and 249 percent of the FPL saw contributions increase from $20 to $25 per month and those in the 250 to 300 percent of the FPL income range saw monthly premiums increase from $40 to $45 (an increase of $60 per year). Kenney et al. (2006–2007) reported that New Hampshire caseloads fell by 3.7 percent, other things equal.

It is clear from these studies that premium contributions do affect enrollment. The individual study findings do not lend themselves to direct comparisons, in part due to the disparate nature of the changes and levels of the premium contributions and the income ranges of those affected. However, a rough consensus suggests that over the range of annual premium increases considered, enrollment declines were in the range of 3 to 5 percent, ignoring transfers to Medicaid, with larger reductions of 8 to 18 percent in Georgia and Kentucky.

Our study extends this line of research by considering another state program, Alabama's ALL Kids. This program differs from many others in two respects. First, the program stands alone, distinct from the state Medicaid program. ALL Kids uses the large Blue Cross Blue Shield of Alabama network of providers and pays the provider rates negotiated by BCBS. As a result, more providers may be willing to treat ALL Kids enrollees than Medicaid recipients. Second, the ALL Kids program assesses a single annual premium per child. As a result, the proportional hazards model used in the foregoing studies is less appropriate. In this program, children are deemed to have 12 months of coverage, at least until their 19th birthday, and are typically removed from the program only for non-payment of the prior year's premium or for failing to meet income eligibility at the time of renewal. Both of these features would suggest that increases in premium contributions comparable to those in other states would have smaller impacts on enrollment.

Methods

The data for this study come from the Alabama ALL Kids program. Information regarding the enrollment periods of children enrolled in ALL Kids was obtained from enrollment history records managed by BCBS. Demographic information, including age, gender, and ZIP code were included with the same BCBS data on enrollee history. Race and FPL information was obtained from the ALL Kids administrative files. Measures of health status were constructed from the program's claims data administered by BCBS.

Enrollment years were the units of analysis, and included enrollment initiated at the start of the ALL Kids program on October 1, 1998 through November 30, 2009 (646,983 observations among 252,381 children). Observations among children having an enrollment period associated with the “no fee” group after October 1, 2003 were excluded, as they would not be affected by any premium changes (6,767 observations, 891 children). Children whose enrollment was in good standing and on-going as of December 1, 2009 were excluded, because renewal decisions are not made until the enrollment expires (67,123 observations/children). The remaining 569,650 observations among 230,255 children were included in the analysis.

Because of the annual nature of ALL Kids enrollment periods, we model enrollment as a time series of cross section renewal decisions and specify a series of linear probability regression models to estimate the effect of changes in the premium contribution on the decision to renew. We also experimented with logistic regression models. However, the parameter estimates of the linear probability model were virtually identical to the marginal effects derived from the logit analysis. Moreover, we also test for differences in premium responsiveness across a number of subgroups of enrollees. The interpretation of interaction terms in logistic regressions is problematic (Ai & Norton, 2003) and exceeds the capacity of Stata software when multiple interaction terms are included in the empirical model.1

The unit of observation is the child-specific enrollment year renewal decision. A child initially enrolled in 2000, and renewed in 2001, 2002, and 2003, but not subsequently would appear in the data with four renewal decisions: 2001 through 2004.

The model takes the general form:

| (1) |

RE is the decision to renew by person i in year t. Premium Shift is a dichotomous variable, taking the value “1” if the child is subject to the higher premium and copays instituted at the time of renewal after October 1, 2003. Because the premium and copay increases were instituted simultaneously, we are not able to estimate the independent effect of the premium on enrollment.

Demographics consist of a vector of age, gender, and race characteristics of person i in year t; male is the reference group. African American and Other are included with White as the reference group. Demographic variables are included to identify differences in renewal probabilities by age, gender, and race.

Health Status is a vector including a dichotomous variable, taking the value 1 if the child was admitted to a hospital in the prior enrollment period, and a second variable taking the value 1 if the child had any claims with a diagnosis code for a chronic condition. Chronic conditions include diagnoses such as asthma and diabetes. A complete listing of the conditions together with their ICD-9 codes is found in the Appendix. We include these measures to examine the extent to which an acute or ongoing health condition affects the probability of renewal. They are drawn from AHRQ (2007) measures of pediatric quality, and have been used in an analysis of the effects of ALL Kids on the health of children with chronic conditions; see Becker et al. (2011).

FPL is a dichotomous variable, taking the value 1 if the child's family income in year t was in the 151 to 200 percent range of the Federal Poverty Line. Children in families with a somewhat higher income, the 151 through 200 percent of the FPL, may be more likely to have their enrollment renewed.

Prior enrollment is a dichotomous variable, taking the value 1 if the child had been enrolled in ALL Kids prior to the current period. This variable is intended to capture the effect of experience with the ALL Kids program on renewal.

Location is a series of dichotomous variables, indicating the residence of the child in a large or small rural town, an isolated area, or whether the child's residence was unknown. Children residing in an urban residence are the reference group.2 This vector is included to identify any differences in enrollment associated with distance from clinical providers, or differential propensity to use services across areas of increasing remoteness. Finally, a time trend variable is included to account for underlying systematic trends in knowledge or access that may affect renewal decisions.

In a second set of specifications, we include interaction effects of the premium shift with demographics, health status, FPL, and previous enrollment period. These specifications allow us to test formally whether the premium shift had differential effects on those of differing characteristics. We are particularly interested in whether higher premiums/copays differentially affected the renewal decisions of families of children with chronic conditions.

Finally, the timing of renewal is somewhat problematic. Many people renew their ALL Kids coverage immediately, so there is no gap in coverage. Others, for whatever reason, may not renew for several months. CMS requests renewal information at six months. To account for this, we estimate a series of regressions using alternative times for renewal: immediate, within 6 months, and within 12 months. We also estimate, but do not report, equations for 1 and 3 months. In general, one would anticipate larger effects of the premium shift when the immediate measure of renewal is used and progressively smaller effects as later renewals are allowed. We focus our attention on the 12 month results, however.

Findings

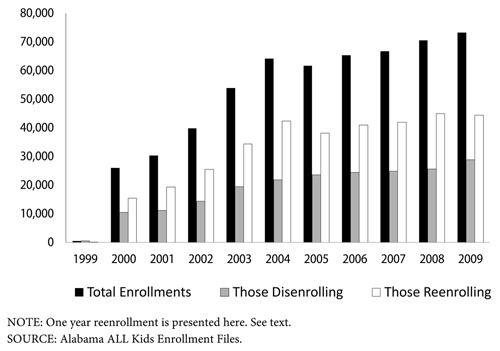

Exhibit 1 presents the trends in ALL Kids disenrollment, renewal and total enrollment over the 1999 to 2009 period. In 2000, there were over 25,900 total enrollees and the number of enrollees increased every year, except in 2005 when it fell modestly. By 2009, the end of our analysis period, there were over 73,200 enrollees. Over the study period, the proportion of children who were immediately renewed was very stable, ranging from a low of 60 percent in 2000 to a high of 66 percent in 2004 (mean = 62.9 percent). The percentage renewing increased with the time window we allowed to determine a renewal, rising from 48 percent immediately to 56.0 percent at 1 month, 58.2 percent at 3 months, 59.8 percent at 6 months and 62.9 percent at 12 months (data not shown). This is consistent with the evidence in other states. Dick et al. (2002) report enrollment survival probabilities at 12 months, for New York and Kansas CHIP programs, as between 65 and 70 percent. Using a sample of Current Population Survey data from 34 states, Sommers (2005) found an annual average drop-out rate, for children in both CHIP and Medicaid programs, of 12.6 percent.

Exhibit 1. ALL Kids Enrollment by Year.

Analyses

Exhibit 2 presents the means and standard deviations of the primary variables used in our regression analyses. Among the 569,650 enrollment-year observations in our sample, 63 percent of these observations faced the higher premiums and copays. Typically, two-thirds of the enrollment came from those with family incomes in the 101 to 150 percent of the FPL with the remainder of family incomes between 151 and 200 percent of the FPL. Approximately 60 percent of the enrollees were White and another third were African American. The average child was nearly 11 years old and was in the ALL Kids program for over 2.7 years (data not shown). Twenty-two percent had a chronic condition and 4.3 percent had been hospitalized in the enrollment year.

Exhibit 2. Means and Standard Deviations of Primary Variables Used in Analysis.

| Mean | Std Deviation | |

|---|---|---|

| 12 Month Renewal | 0.63 | 0.48 |

| 6 Month Renewal | 0.61 | 0.49 |

| Immediate Renewal | 0.56 | 0.50 |

| Premium Shift | 0.63 | 0.48 |

| Age | 11.05 | 4.75 |

| Female | 0.49 | 0.50 |

| Male (Reference Group) | 0.51 | 0.50 |

| African-American | 0.34 | 0.47 |

| Other Race | 0.05 | 0.23 |

| White (Reference Group) | 0.60 | 0.49 |

| Inpatient Use | 0.04 | 0.20 |

| Chronic Condition | 0.22 | 0.41 |

| Previous Enrollment | 0.60 | 0.49 |

| 151-200% Federal Poverty Line (FPL) | 0.36 | 0.48 |

| 101-150% FPL (Reference Group) | 0.64 | 0.48 |

| Large Town | 0.13 | 0.33 |

| Small Town | 0.13 | 0.33 |

| Isolated Area | 0.10 | 0.30 |

| Missing Rural | 0.01 | 0.11 |

| Urban | 0.64 | 0.48 |

| Time Trend | 7.47 | 2.75 |

SOURCE: Alabama ALL Kids Enrollment and Claims Files.

The initial regression results are reported in Exhibit 3. Regardless of how widely one defines the window during which a child's coverage may be renewed, it is clear that the shift to a $50 higher premium and coincident increases in copays were associated with a reduced probability of renewing, other things equal. The premium shift is estimated to have reduced renewal by 6.1 percent annually. As expected, the decline in renewals is ameliorated if one allows a longer time period for families to renew their child's coverage; the effect is over one-third larger if only immediate renewals are considered.

Exhibit 3. Analysis of Renewal, 2000–2009.

| Immediate Renewal | Renewal within 6 Month of Contract End | Renewal within 12 Months of Contract End | |

|---|---|---|---|

|

|

|||

| Premium Shift | -0.083*** (0.0024) |

-0.069*** (0.0024) |

-0.061 *** (0.0024) |

| Age | -0.0059 *** (0.00014) |

-0.0073 *** (0.00013) |

-0.0080 *** (0.00013) |

| Female | 0.0018 (0.0014) |

0.0028 (0.0014) |

0.0034 *** (0.0014) |

| African American | -0.019*** (0.0016) |

-0.0095*** (0.0015) |

-0.0069 *** (0.0015) |

| Other Race | -0.062 *** (0.0033) |

-0.062 *** (0.0032) |

-0.063 *** (0.0032) |

| Inpatient use | -0.026*** (0.0032) |

-0.029*** (0.0031) |

-0.033 *** (0.0031) |

| Chronic Condition | 0.14 *** (0.0016) |

0.14 *** (0.0015) |

0.14 *** (0.0015) |

| Previous Enrollment | 0.16 *** (0.0015) |

0.16 *** (0.0015) |

0.16 *** (0.0014) |

| 151-200% FPL | 0.044*** (0.0015) |

0.043*** (0.0014) |

0.042 *** (0.0014) |

| Large Town | -0.0023 (0.0022) |

-0.0070 *** (0.0021) |

-0.0086 *** (0.0021) |

| Small Town | -0.0040 * (0.0023) |

-0.0080 *** (0.0021) |

-0.0096 *** (0.0021) |

| Isolated Area | 0.0056*** (0.0025) |

0.0022 (0.0023) |

-0.000041 (0.0023) |

| Missing Rural | -0.094*** (0.0061) |

-0.11*** (0.0061) |

-0.12 *** (0.0060) |

| Time Trend | 0.0066*** (0.00043) |

0.0028*** (0.00043) |

0.00093*** (0.00042) |

| Constant | 0.55*** (0.0032) |

0.57*** (0.0028) |

0.60 *** (0.0028) |

| R2 | 0.044 | 0.047 | 0.048 |

| Observations | 569,650 | 569,650 | 569,650 |

Standard errors are in parentheses.

*, **, and *** indicates statistical significance at the 90, 95 and 99 percent confidence intervals, respectively.

Each model reports robust standard errors clustered on the individual.

SOURCE: Alabama ALL Kids Enrollment and Claims Files.

Not surprisingly, children are less likely to have their enrollment renewed as they become older. African American children were only slightly less likely to have their enrollment renewed within the 12 month period, but based on the regression results, were nearly 2 percent less likely to renew immediately relative to Whites. While there is a large negative effect (6.3 percent) of “Other race,” this must be interpreted with caution, because it includes those children for which race was not reported.

Children with chronic conditions were approximately 14 percent more likely to have their enrollment renewed. However, those who had had a recent hospitalization were 3.3 percent less likely to have their enrollment renewed.

Those who had previous ALL Kids enrollment were 16 percent more likely to renew. Those in the higher income threshold of eligibility were 4 percent more likely to renew. Those children residing in remote rural areas of the state were slightly more likely to renew immediately, but this effect dissipated with a longer enrollment window.

It is conceivable that the premium shift may have a differential effect on subgroups of subscribers. To address this issue we interacted the shift variable with the demographic, health status, enrollment period, and FPL variables. The results of this analysis are reported in Exhibit 4

Exhibit 4. Analysis of Differential Effects of Premium Shift, 2000–2009.

| Immediate Renewal | Renewal within 6 Months of Contract End | Renewal within 12 Months of Contract End | |

|---|---|---|---|

|

|

|||

| Premium Shift (PS) | -0.062***(0.0047) |

-0.042***(0.0047) |

-0.035***(0.0046) |

| Age | -0.0017***(0.00023) |

-0.0028***(0.00022) |

-0.0035***(0.00022) |

| PS X Age | -0.0067***(0.00029) |

-0.0072***(0.00029) |

-0.0072***(0.00029) |

| Female | -0.0027 (0.0022) |

-0.00075 (0.0021) |

-0.00015 (0.0021) |

| PS X Female | 0.0069*** (0.0027) |

0.0052*** (0.0026) |

0.0053*** (0.0027) |

| African American | 0.00057 (0.0024) |

0.0078*** (0.0023) |

0.0086*** (0.0023) |

| PS X African American | -0.029*** (0.0029) |

-0.026*** (0.0028) |

-0.024*** (0.0028) |

| Other Race | -0.10*** (0.0052) |

-0.11*** (0.0051) |

-0.11*** (0.0051) |

| PS X Other Race | 0.059*** (0.0063) |

0.070*** (0.0061) |

0.072*** (0.0060) |

| Inpatient use | -0.036*** (0.0050) |

-0.038*** (0.0049) |

-0.043*** (0.0049) |

| PS X Inpatient | 0.016*** (0.0065) |

0.014*** (0.0064) |

0.015*** (0.0063) |

| Chronic Condition | 0.16*** (0.0026) |

0.17*** (0.0024) |

0.17*** (0.0023) |

| PS X Chronic | -0.036***(0.0032) |

-0.042***(0.0029) |

-0.044***(0.0029) |

| Previous Enrollment | 0.11*** (0.0022) |

0.11*** (0.0022) |

0.11*** (0.0022) |

| PS X Previous Enroll | 0.076*** (0.0029) |

0.086*** (0.0029) |

0.086*** (0.0028) |

| FPL 151-200% | 0.074*** (0.0023) |

0.062*** (0.0023) |

0.160*** (0.0022) |

| PS X FPL | 0.047*** (0.0029) |

0.031*** (0.0028) |

0.028*** (0.0028) |

| Large Town | -0.0019 (0.0022) |

-0.0066*** (0.0021) |

-0.0081 (0.0021) |

| Small Town | -0.0038 (0.0022) |

-0.0078*** (0.0021) |

-0.0093*** (0.0021) |

| Isolated Area | 0.0058*** (0.0025) |

0.0023 (0.0023) |

0.00013 (0.0023) |

| Missing Rural | -0.094*** (0.0061) |

-0.11*** (0.0060) |

-0.12*** (0.0059) |

| Time Trend | 0.0075*** (0.00044) |

0.0042*** (0.00047) |

0.0021*** (0.00043) |

| Constant | 0.429*** (0.0038) |

0.52*** (0.0037) |

0.67*** (0.0054) |

| R2 | 0.047 | 0.051 | 0.051 |

| Observations | 569,650 | 569,650 | 569,650 |

Standard errors are in parentheses.

*, **, and *** indicates statistical significance at the 90, 95 and 99 percent confidence intervals, respectively.

Each model reports robust standard errors clustered on the individual.

SOURCE: Alabama ALL Kids Enrollment and Claims Files.

The simple analysis found that African Americans were slightly less likely to renew than Whites. However, they were substantially more price sensitive; the premium shift reduced annual renewals among African Americans by 5.9 percent compared to 3.5 percent for Whites. Parents of girls were slightly less price sensitive than those for boys. Parents of older children also were slightly more price sensitive.

Families with children who had been hospitalized in the last year were less sensitive to premium increases than families overall. They were only about three-fifths as responsive to the higher premiums. Those families with a child who had a chronic condition were substantially more price sensitive than those families who were without such conditions. The premium shift resulted in a 7.9 percent lower probability of their renewing within 12 months compared to a 3.5 percent probability for families with no chronic conditions. However, since children with a chronic condition have a 17 percent higher base probability of renewal, in spite of their greater sensitivity to the price increase, on net they remain more likely to have their coverage renewed than those without chronic conditions, even after the premium increase. Those who had been previously enrolled in ALL Kids in the prior year and those in the higher income group (150– 200% of the FPL) were less price sensitive than others.

Discussion

This paper has analyzed the effects of premium contributions on renewal in the Alabama Children's Health Insurance Program, ALL Kids. That program raised premiums by $50 per child per year in 2003 and simultaneously raised copayments, typically by $1 to $3. We estimate that the increases reduced renewal in the program by between 6.1 to 8.3 percent depending upon how much time one allows for families to renew. This effect is relatively modest and consistent with the effects found for Florida, New Hampshire, Kansas and Arizona, but smaller than those found for Kentucky and particularly Georgia.

Consistent with earlier work, we find that families with a child who has a chronic condition were more likely to renew coverage, as were those who had greater experience with the program. However, we found that families of children with chronic conditions were somewhat more price sensitive when faced with higher premiums and copays. Similarly, African Americans and those with lower family incomes were more sensitive to premium contributions and copays than were Whites or higher income eligible groups.

This study is not without limitations. Two are particularly noteworthy. First, we were not able to link ALL Kids data with state Medicaid data. Thus, we were unable to investigate the extent to which children transition from ALL Kids to Medicaid rather than becoming uninsured. In addition, we are unable to explore the extent to which rising family incomes lead children to move from Medicaid to ALL Kids. Linking these data files would provide an opportunity to investigate how well the state's integrated enrollment processes for the two programs prevent children from falling between the cracks.

Second, we know very little about the family structure of the children enrolled in ALL Kids. It proved difficult to even identify the number of siblings covered by the program, much less whether the child lives in a two parent household, with his/her mother or father, grandparent, or in some other living arrangement. Such information would allow an investigation of the extent to which family structure affects the availability of public coverage, and the extent to which transitions in family structure affect program participation.

This study found that a $50 increase in annual ALL Kids premiums, together with modest increases in service copayments, was associated with a 3.9 to 2.4 percent decrease in renewal depending upon how large of a window one allows for observing renewals. These results reinforce the findings of other studies showing that even small changes in enrollee out-of-pocket costs can affect enrollment. Because ALL Kids is a stand-alone program, independent of Medicaid, our study helps generalize to the 17 other stand-alone programs. CHIP programs in Mississippi, Pennsylvania, Texas, or Washington may experience similar results.

Appendix A.

| Disease/Condition | 3-Digit ICD9 Code(s) |

|---|---|

| Human immunodeficiency virus [HIV] | 042 |

| Neoplasms (malignant) | 140-208 |

| Diabetes mellitus (or secondary diabetes mellitus) | 249, 250 |

| Cystic fibrosis | 277 |

| Hereditary hemolytic anemia or aplastic anemia and other bone marrow failure syndromes | 282, 284 |

| Coagulation defects | 286 |

| Schizophrenic disorders | 295 |

| Pervasive developmental disorders | 299 |

| Infantile cerebral palsy | 343 |

| Epilepsy and recurrent seizures | 345 |

| Muscular dystrophy | 359 |

| Hearing loss | 389 |

| Diseases of the circulatory system | 390-459 |

| Chronic rheumatic heart disease | 393-398 |

| Hypertensive disease | 401-405 |

| Ischemic heart disease | 410-414 |

| Other forms of heart disease | 420-429 |

| Heart failure | 428 |

| Disease of the arteries, arterioles, and capillaries | 440-449 |

| Asthma† | 493 |

| Rheumatoid arthritis and other inflammatory polyarthropathies | 714 |

| Congenital anomalies | 740-759‡ |

| Heart defects | 745 |

| Spina bifida | 741 |

| Birth trauma | 767 |

| Spinal cord injury | 950-957 |

Required a minimum of three primary diagnoses over three enrollment periods;

Excluding cleft lip and palate, ICD9: 749.

SOURCE: Alabama ALL Kids Pediatric Health History Intake Form.

Footnotes

See: CRMportols Inc., “Interaction Terms Vs. Interaction Effects in Logistic and Probit Regression,” (2006), http://www.crmportals.com/crmnews/Interaction%20term%20vs.%20interaction%20effect%20in%20logit%20and%20probit%20models.pdf

The measure of rurality used the Rural Urban Commuting Area (RUCA) categorization A as developed by the WWAMI Rural Health Research Center, which was approximated by use of ZIP code data (http://depts.washington.edu/uwruca/ruca-uses.php)

Financial Disclosure: This project was funded by a contract from the Alabama Department of Public Health, Bureau of Children's Health Insurance. The findings and conclusions herein are solely those of the authors and do not necessarily reflect those of the Alabama Department of Public Health or the University of Alabama at Birmingham.

References

- AHRQ (Agency for Health Care Research and Quality) Measures of Pediatric Health Care Quality based on Hospital Administrative Data: The Pediatric Quality Indicators. Rockville, MD: U.S. Department of Health and Human Services; 2006. [Google Scholar]

- Ai C, Norton EC. Interaction Terms in Logit and Probit Models. Economics Letters. 2003;80:123–129. doi: 10.1016/S0165-1765(03)00032-6. [DOI] [Google Scholar]

- Artiga S, O'Malley M. Increasing Premiums and Cost Sharing in Medicaid and SCHIP: Recent State Experiences. Menlo Park, CA: Kaiser Family Foundation Medicaid and the Uninsured Issue Paper; 2005. May, [Google Scholar]

- Becker DJ, Blackburn J, Kilgore ML, Morrisey MA, Sen B, Caldwell C, Menachemi N. Continuity of Insurance Coverage and Ambulatory Sensitive ED Visits/Hospitalizations: Evidence from the Children's Health Insurance Program. Clinical Pediatrics. 2011;50(10):963–973. doi: 10.1177/0009922811410229. [DOI] [PubMed] [Google Scholar]

- Dick AW, Allison RA, Haber SG, Brach C, Shenkman E. Consequences of States' Policies for SCHIP Disenrollment. Health Care Financing Review. 2002;23(3):65–88. [PMC free article] [PubMed] [Google Scholar]

- Kenney G, Allison RA, Costich JF, Marton J, McFeeters J. Effects of Premium Increases on Enrollment in SCHIP: Findings from Three States. Inquiry. 2006-2007;43(4):378–392. doi: 10.5034/inquiryjrnl_43.4.378. [DOI] [PubMed] [Google Scholar]

- Kenney G, Marton J, McFeeters J, Costich J. Assessing Potential Enrollment and Budgetary Effects of SCHIP Premiums: Findings from Arizona and Kentucky. Health Services Research. 2007;42(6, part II):2354–2372. doi: 10.1111/j.1475-6773.2007.00772.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Marton J, Ketsche PG, Zhou M. SCHIP Premiums, Enrollment, and Expenditures: A Two State, Competing Risk Analysis. Health Economics. 2010;19(7):772–791. doi: 10.1002/hec.1514. [DOI] [PubMed] [Google Scholar]

- Marton J, Talbert JC. CHIP Premiums, Health Status, and the Insurance Coverage of Children. Inquiry. 2010;47(3):199–214. doi: 10.5034/inquiryjrnl_47.03.199. [DOI] [PubMed] [Google Scholar]

- Ross DC, Horn A, Marks C. Health Coverage for Children and Families in Medicaid and SCHIP: State Efforts Face New Hurdles. Menlo Park, CA: Kaiser Family Foundation Medicaid and the Uninsured; 2008. Issue Paper. [Google Scholar]

- Sen B, Blackburn J, Morrisey MA, Kilgore ML, Backer DJ, Caldwell C, Menachemi N. Did Copayment Changes Reduce Health Service Usage among CHIP Enrollees: Evidence from Alabama. Health Services Research. 2012 doi: 10.1111/j.1475-6773.2012.01384.x. forthcoming. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Shenkman EA, Vogel B, Boyett JM, Naff R. Disenrollment and Re-enrollment Patterns in a SCHIP. Health Care Financing Review. 2002;23(3):47–63. [PMC free article] [PubMed] [Google Scholar]

- Sommers BD. From Medicaid to Uninsured: Drop-Out among Children in Public Insurance Programs. Health Services Research. 2005;40(1):59–78. doi: 10.1111/j.1475-6773.2005.00342.x. [DOI] [PMC free article] [PubMed] [Google Scholar]