Abstract

Context

Medicare Part C, or Medicare Advantage (MA), now almost 30 years old, has generally been viewed as a policy disappointment. Enrollment has vacillated but has never come close to the penetration of managed care plans in the commercial insurance market or in Medicaid, and because of payment policy decisions and selection, the MA program is viewed as having added to cost rather than saving funds for the Medicare program. Recent changes in Medicare policy, including improved risk adjustment, however, may have changed this picture.

Methods

This article summarizes findings from our group's work evaluating MA's recent performance and investigating payment options for improving its performance even more. We studied the behavior of both beneficiaries and plans, as well as the effects of Medicare policy.

Findings

Beneficiaries make “mistakes” in their choice of MA plan options that can be explained by behavioral economics. Few beneficiaries make an active choice after they enroll in Medicare. The high prevalence of “zero-premium” plans signals inefficiency in plan design and in the market's functioning. That is, Medicare premium policies interfere with economically efficient choices. The adverse selection problem, in which healthier, lower-cost beneficiaries tend to join MA, appears much diminished. The available measures, while limited, suggest that, on average, MA plans offer care of equal or higher quality and for less cost than traditional Medicare (TM). In counties, greater MA penetration appears to improve TM's performance.

Conclusions

Medicare policies regarding lock-in provisions and risk adjustment that were adopted in the mid-2000s have mitigated the adverse selection problem previously plaguing MA. On average, MA plans appear to offer higher value than TM, and positive spillovers from MA into TM imply that reimbursement should not necessarily be neutral. Policy changes in Medicare that reform the way that beneficiaries are charged for MA plan membership are warranted to move more beneficiaries into MA.

Keywords: Medicare, managed care, payment policy, health care costs

Part C of Medicare, now known as Medicare Advantage (MA), began in 1985 with only 2% of beneficiaries enrolled, but it is no longer a small part of Medicare, as 28% of beneficiaries have now chosen MA rather than traditional Medicare (TM).1–3 Despite this seeming success in the marketplace, many health policy analysts view MA as a policy failure.1 In part, this is because in the past the program attracted favorable risks, and the primitive risk adjustment in place in the 1990s, along with the beneficiaries’ ability to change plans monthly, resulted in Medicare's paying more for the enrollees in MA than it would have paid for them in TM.4–12 Starting in 1998, the overpayment increased even further with the introduction of floors on MA plan reimbursement in low-spending TM counties and subsequent updates to reimbursement that favored MA.13–15

Two reasons could justify higher reimbursement for MA plans. The first is a pay-for-performance idea, that quality could be better in MA. Historically, however, there was almost no evidence regarding the quality of care in MA relative to that in TM. Lacking such evidence, the general assumption was that the quality was similar, in part because MA beneficiaries generally received care from the same physicians and hospitals as TM beneficiaries did. (Kaiser Permanente, which has somewhat less than 10% of MA enrollees, is an exception.) If anything, many were concerned about MA's possibly lower quality from stinting or underuse because of the inherent incentives in the capitation that MA plans received. These concerns led to a policy allowing beneficiaries to disenroll from their MA plan at the end of any month if they were dissatisfied and to the introduction of patient protection legislation for HMOs in 35 states’ commercial markets between 1997 and 1999.16

Second, higher payments to MA plans might be justified if higher MA penetration improved practice patterns in TM. There is, in fact, evidence that higher HMO penetration, in both Medicare and commercial, has positive spillovers.17–21 But at the time these studies were conducted, more than a decade ago, the great bulk of HMO enrollees were not in Medicare because they were under age 65 and still had commercial insurance. Since then, the MA program has grown substantially, and HMOs have advanced their medical management techniques. TM's technology and patterns of care have changed as well, leaving open the question of the current nature and magnitude of any MA-to-TM spillovers.

Medicare regulations are designed to ensure that the higher MA (relative to TM) reimbursement will pass through to beneficiaries in the form of lower premiums or additional benefits. Although Medicare's ability to monitor any pass-through is imperfect, competition among plans reinforces the regulation. Partly as a result of excess reimbursement, many plans are so-called zero-premium plans, charging no premium beyond the standard Part B premium collected by Medicare, despite providing more generous benefits than TM does. Cost sharing typically is less than in TM, and additional services are frequently covered. In short, much of the excess MA reimbursement has passed through to beneficiaries through a combination of regulation and competition among MA plans in local markets. Once in place, the differential reimbursement has persisted, since MA's additional benefits are politically difficult to take away.

The more generous MA benefits may be responsible for the overrepresentation of near poor people in these plans, as they may be more willing than the more affluent to give up some of TM's freedom of choice of provider in order to save money. By contrast, the difference in benefits historically has been less relevant to dual eligibles and those with retiree health insurance. If they enrolled in TM, both groups had low or no premiums and low cost sharing, from either Medicaid, in the case of dual eligibles, or a subsidized supplementary policy from their prior employer, in the case of retirees. As a result, a disproportionately high number of those two groups, which comprise roughly half of Medicare beneficiaries, have enrolled in TM.

For the past several years we have been part of a group generating new information about MA, and in this article we try to integrate and synthesize what we have learned and to draw implications for Medicare policy. Our research has shown that changes in policy over the past decade—and perhaps lessons learned by the MA plans—have improved the performance of MA relative to that of TM. Although some favorable selection appears to remain, it has been substantially reduced, and the few comparisons of quality between MA and TM tend to favor MA. Furthermore, there is evidence of spillovers from MA to TM, which may justify a higher reimbursement rate for MA (though not necessarily the current structure of MA reimbursement).

The MA program is not without problems, however. There is evidence of market power in the MA program, either on the plan side or provider side, or both.22,23 Furthermore, as we describe later, Medicare beneficiaries’ choice of health insurance plan is typically more complicated than that for any other group in the United States. Although greater choice is often assumed to be beneficial, the complexity of Medicare's Parts C and D plan choices leads to mistakes by many beneficiaries.24–27

Finally, Medicare's premium policies interfere with the socially efficient division of beneficiaries between MA and TM.28 One symptom of this problem is that although enrollment in the MA program is reaching historical highs, fewer Medicare beneficiaries are in managed care plans than in either commercial insurance or Medicaid, the other major US insurers. Recently, however, Medicare has begun to induce individuals with dual Medicare and Medicaid eligibility, a group for whom the social and private benefits of managed care may be large, to enter Medicare Advantage.

After summarizing and interpreting recent research results, we comment on their relationship to current economic and policy issues in the Medicare program, including new directions for the program as part of the Affordable Care Act.

Framing a Review of MA: The Structure of Choice

We conceptualize MA as a set of sequenced choices by beneficiaries, plans, and Medicare itself or, using economic jargon, as a 3-level principal-agent problem. Beneficiaries are agents who take both public policy and plan contracts as given when choosing among options, including TM. Plans are both principals and agents. Relative to beneficiaries, they are principals that structure contracts to maximize profit (and possibly other goals in the case of nonprofit plans) after accounting for the beneficiaries’ choices. Relative to the government, however, plans are agents that take policy as given when constructing the contracts offered to beneficiaries. The government (Congress and the Centers for Medicare and Medicaid Services [CMS]) is a principal that sets policy, assuming that the plans will maximize profit (or other goals) in determining what contracts to offer to beneficiaries and that beneficiaries will choose between TM and MA and among MA plans according to their decision rules.

We used this 3-level framework to organize our review of recent work, beginning with beneficiaries’ behavior and working up through plan behavior and policy design. Because much of our work was studying how changes in policy changed the behavior of beneficiaries and plans, policy issues appear in this review right from the start.

Beneficiaries’ Behavior Regarding Their Choice of Plan

The Efficiency of Beneficiaries’ Choices

As we noted earlier, more Medicare beneficiaries are choosing MA plans than ever before, 28% in 2013. Nonetheless, compared with employer-based health insurance, in which indemnity insurance or “unmanaged care” has completely failed the market test, this share is still very low, as fewer than 1% of the commercially insured are in “conventional” plans like TM.29 Also as we noted earlier, MA is particularly attractive to lower-income beneficiaries perhaps because of MA's lower out-of-pocket costs.26

We evaluated both the private and the social efficiency of beneficiaries’ choices between TM and MA. Privately, has the beneficiary chosen a plan that maximizes benefits to him or her, less the premiums and out-of-pocket costs? Socially, is the beneficiary in a plan that maximizes benefits (to the beneficiary and perhaps others) less all costs, including those borne by taxpayers? We begin by evaluating the choices from the beneficiary's point of view and then move to the perspective of social welfare.

Several sets of evidence point to beneficiaries’ systematic mistakes in choosing a plan, with our definition of a mistake as a choice not in one's self-interest. Such mistakes are not surprising, given that Medicare presents beneficiaries, virtually all of whom are elderly or disabled, with health insurance choices that are far more complex than those faced by the majority of active workers. If they have a choice of insurance plan at all, active employees typically choose among only 2 or 3 plans that their employer has “preselected,” presumably for value. When enrolling in Medicare, however, the choices are many. Beneficiaries must first decide whether to enroll in TM or MA, and they will be put into TM if they do not make a choice. If they choose MA, they then must choose a plan type (health maintenance organization or HMO, preferred provider organization or PPO, private fee-for-service or PFFS, or medical savings account) and, within the plan type, a specific insurer and plan. If they choose TM, they must decide whether to enroll in Part B (Part B enrollment is mandatory for MA) and whether to purchase a supplementary policy and, if so, which one. In either case, they must decide whether to enroll in Part D and, if they are enrolled in TM, which prescription drug plan to choose. (MA beneficiaries purchase their drug plan through their MA plan.) As an example of excessive choice, beneficiaries in Miami-Dade County in 2008 had to choose among 123 MA plans, 32 of which were PFFS plans.27 In 2013, if they chose to enroll in TM, they had a choice of 73 supplementary plans and 30 Part D plans.

Behavioral economics has established that greater choice does not necessarily lead to better decisions.30 In conventional economic theory, more choices always benefit a consumer because more choices offer the possibility of a better match between what is bought and the consumer's preferences. It follows from conventional theory that adding MA plan options—because of the better chance of matching consumers’ preferences—should move more beneficiaries out of TM. This prediction, however, is inconsistent with the data. More choices of plan in counties have led to higher enrollment in MA, but only up to about 15 plans. Although a choice between 15 and 30 MA plans does not greatly affect the proportion of beneficiaries choosing MA, if more than 30 plans are offered, the proportion choosing MA actually declines.26

A second inconsistency with standard economic theory comes from choices of PFFS plans. Until 2011 when the policy regarding PFFS plans was changed to requiring them to have networks, PFFS plans dominated TM for many beneficiaries. Access to providers was the same as in TM, because providers who accepted TM patients also had to accept PFFS patients and reimbursement at TM rates. In many counties, however, PFFS plans were reimbursed by Medicare at rates higher than those for TM, and thus they offered lower premiums and higher benefits than a TM beneficiary with no supplementary policy could obtain. According to standard theory, all beneficiaries in these counties without supplementary insurance should have enrolled in PFFS. In fact, in 2007, 95% of all beneficiaries would have faced lower expected out-of-pocket costs in a PFFS plan than if they had joined TM and paid for a Medigap policy themselves.26 Beneficiaries with higher cognitive scores, however, were more responsive in their choice of plan to this greater generosity, supporting the interpretation that the complexity of choice prevented some beneficiaries from making good decisions.26

The developing field of behavioral economics has been documenting and drawing the implications of other patterns of choice that do not serve consumers’ best interests. Two such patterns are relevant to our discussion. First, while most beneficiaries choose between MA and TM when they become eligible for Medicare (ie, few are defaulted into TM), very few revise their choice if or when their health and economic situation evolves and the relative costs of TM and MA to them change because of either congressional action or market forces. In other words, they exhibit what the behavioral economics literature calls status quo bias.31 Sinaiko and colleagues documented the stickiness in beneficiaries’ choices in the richly served Medicare health insurance market in Miami-Dade County and interpreted it as indicating this form of mistake.27

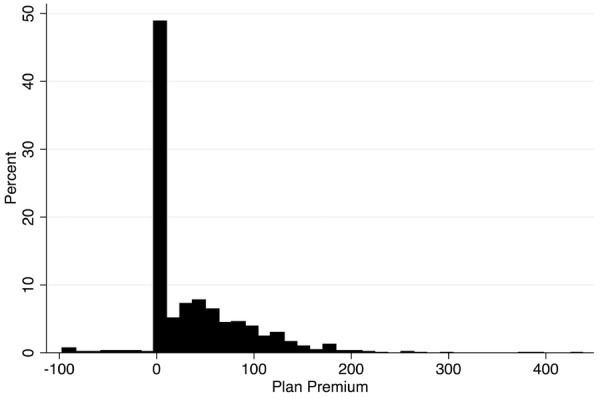

A second behavioral economics phenomenon, salience, may be behind 2 striking facts shown in Figure 1, namely, that almost half of beneficiaries are enrolled in plans that charge a zero premium and that hardly any are enrolled in plans that charge a negative premium. To understand why so many plans might be charging nothing, recall that MA enrollees must enroll in Part B and pay the fixed Part B premium, which in 2014 was $104.90 per month for individual beneficiaries with incomes below $85,000, irrespective of whether they elected TM or MA. (Higher thresholds applied to couples filing jointly.) For most beneficiaries, the Part B premium is deducted directly from their Social Security checks.

Figure 1.

Weighted Distribution of MA

Plan Premiums in 2010 Data derived from the 2010 CMS Medicare Options Compare database, subsetted to local, nonemployer, non-special needs plans.

As Figure 1 shows, many plans do charge a premium, which beneficiaries pay directly to the plan. Plans are, however, allowed to “buy down” the Part B premium, effectively charging a negative premium to join their plan, and as Figure 1 also shows, a few plans do. Beneficiaries who join such plans simply have less deducted from their Social Security checks for the Part B premium. This is likely less visible, or salient, to beneficiaries than is having to write a check for the premium. This difference in salience is consistent with the data shown in Figure 1. According to this interpretation, when choosing a plan, beneficiaries are more responsive to changes in a “positive” premium than to changes in a “negative” premium because the positive premium is more salient. As a result, plans have little incentive to reduce premiums below zero and instead bunch up at zero. In a complementary analysis, Karen Stockley (written communication, January 2014) is leading a group interpreting the bunching as due to the “lack of transparency” in the prices of Part C alternatives. A similar phenomenon explains higher vehicular tolls on toll roads when transponders are available.32

A related, though not mutually exclusive, explanation for the preponderance of zero-premium plans comes from studies of plan choice in Medicare Part D finding that consumers pay too much attention to (ie, overweight) upfront premium costs and too little to the extensiveness of benefits or the degree of cost sharing.24,25 Such overweighting can explain why plans would want to keep premiums lower and cost sharing higher, but it cannot explain why so many plans’ premiums are exactly zero and so few are less than zero, whereas the lack of salience of a negative premium can. Although the proximate effect of beneficiaries’ systematic decision-making biases is to undermine the quality of the match between a beneficiary and a plan, these biases have consequences up the chain of decisions. Some of the mistakes listed earlier contribute to demand inelasticity that plans can exploit in their pricing. For example, in 2006, the first year of Part D, the insurer Humana priced its Part D policies much lower than its competitors and, as a result, obtained a relatively large market share. It subsequently raised its premiums to near the level of its competitors but largely maintained its market share, very likely because of status quo bias.

The design of Medicare payment policy can undo some of the foregoing mistakes, whether viewed from the beneficiary perspective just discussed or a social welfare perspective. From the standpoint of social welfare, we might ask not only how many beneficiaries should be in MA but also which beneficiaries should be in MA and which in TM. TM was designed to mimic the indemnity insurance of the 1960s with no medical management by the insurer and cost sharing to control utilization. By contrast, until the last few years, employers typically offered workers HMO and PPO alternatives with modest cost sharing compared with TM but with medical management, in other words, plans like current MA plans. Although cost sharing has recently risen in employment-based insurance, almost no employers offer an open-network, unmanaged option like TM.29 Using today's employer-based health insurance as a standard, we might say that TM is anachronistic and that all beneficiaries should be in an MA plan.

Though not without merit, such a position disregards the problem that choice among insurance plans, in both Medicare and employer-based health insurance, is characterized by inefficiencies in sorting among plan types caused by inherent limitations in pricing health insurance, some of which are due to asymmetric information and some to regulation.9,33 For Medicare, this means that some beneficiaries might value the unfettered choice of provider and treatments in TM and be willing to pay the extra costs over those of an MA plan alternative. Putting aside any tendency to make systematic mistakes in choices, aligning the beneficiary's utility maximization in the choice of MA or TM with social economic efficiency requires each beneficiary to pay a premium for TM, relative to that for MA, that is equal to the extra costs imposed by staying in TM rather than moving to MA—nowhere near what happens in Medicare currently.34 MA plans charge a single, “community-rated” premium, implying that lower-cost TM beneficiaries will pay too large a premium to join MA and that higher-cost TM beneficiaries will pay too small a premium. This single-premium policy thus contributes to an inefficient match of beneficiaries and plans, keeping too many higher-cost beneficiaries in TM.33

The inefficiency of a single premium for any health plan was emphasized recently in the literature in health economics.28,35,36 Glazer and McGuire are concerned specifically with MA-TM sorting and propose policies to modify Medicare's premium policy to expand the overall demand for MA and move a larger share of high-demand beneficiaries into MA.28,36 We will return later to this issue in the context of Medicare policy.12

A common reason for the difference between private choices and social welfare throughout the economy is the presence of externalities, or spillover benefits or costs. In the case of MA, the spillover benefit from membership in an MA plan is that its lower-cost practice patterns “spill over” and reduce costs for TM beneficiaries. Taking advantage of the widely varying penetration of MA across counties, from under 5% to over 50%, Baicker and colleagues found that hospital stays become less expensive as the MA penetration rates at a hospital and in a county rise.37 A $10 increase in MA reimbursement rates, which leads to an increase in enrollment, reduces a hospital's cost of Medicare admissions by roughly $1. Admission rates, however, do not change; the savings comes from less intensive care conditional on admission.

The Effect of Policy Changes on Beneficiary Choice and Selection

Health economists have taken 2 approaches in constructing models of adverse selection, focusing on either the behavior of consumers or the behavior of plans. In models emphasizing consumer behavior, consumers choose between high- and low-option plans with fixed characteristics.33,38–40 When the price must be the same for all those choosing a given plan, as is typically the case, the more costly consumers are more likely to choose a more generous option, leading to an equilibrium with too high a price for that option and too few people in that plan. Most of the research on selection in Medicare fits this paradigm, with TM being the more generous or “higher” option and the older research showing that sicker, more costly beneficiaries disproportionately chose TM.

A different strain of research emphasizes plan behavior in promoting selection.41 Unlike models of plans with fixed characteristics, this model assumes that plans actively structure their product to attract more profitable (less expensive) consumers. We discuss this form of adverse selection later; next we focus on the relation between consumers’ behavior and selection of plans.

In response to the evidence cited earlier that MA plans were sufficiently popular that Medicare paid more for the beneficiaries in MA than it would have if those same beneficiaries had enrolled in TM, Congress in 1997 mandated that CMS add a measure of health status to the risk adjustment method, and in 2003 it went further by enacting a lock-in so that MA beneficiaries could no longer change each month to TM. Although risk adjustment should affect selection through only the plan's behavior, it is difficult empirically to separate the effects of the new risk adjustment scheme from the lock-in, and thus we describe the data on their combined effect on selection.

Before 1998 the risk adjusters that Medicare used to determine its reimbursement to MA plans consisted of demographic variables such as age, gender, and Medicaid status, but those variables explained only about 1% of the variation in the individual beneficiaries’ annual spending, whereas at least 20% to 25% was explainable.1,42 Put bluntly, even though adjustment that explained only 1% of the variation was better than no risk adjustment, it did not induce plans to select poor risks, in either theory or fact.

The method that Medicare used to move beyond this primitive risk adjustment scheme and comply with the congressional mandate to account for health status was to use diagnostic information from claims or encounter data. Thus, Medicare would pay a plan more for enrolling a beneficiary with a more costly diagnosis, such as breast cancer, than for a beneficiary with a less costly diagnosis, such as pneumonia. The greater amount for more expensive diagnoses was based on the relative cost of treating various diagnoses in TM.

The use of claims or encounter data for this purpose, however, posed a problem because the coding of diagnoses for outpatients’ claims was incomplete, probably because the reimbursement for outpatient services did not depend on the diagnosis.43 By contrast, the coding of diagnoses for inpatients was accurate because this coding formed the basis of diagnosis-related groups (DRGs), which is the basis for Medicare hospital reimbursement.

Given the coding problem with outpatients’ claims, in 2000 CMS added diagnoses coded on inpatient claims as a risk adjuster and ignored diagnoses recorded on outpatient claims. But it gave the method incorporating inpatient diagnoses only 10% weight in calculating reimbursement and continued to base the remaining 90% of reimbursement on the old method of only demographic adjusters, primarily age and gender. This modest weight on inpatient diagnoses addressed an incentive problem that stemmed from using only inpatient diagnoses. Although good medical management by an MA plan could prevent some hospitalizations and reduce cost, prevention meant less reimbursement for the plan and possible damage to its bottom line, since with no hospital admissions there would be no record of an inpatient diagnosis on which to adjust rates. But because 90% of the adjustment was still based solely on demographic adjustment, the plans’ incentives were little changed.

In addition to using diagnoses to adjust reimbursement, CMS began to address the underlying outpatient data problem by enforcing the requirement that plans report diagnoses recorded on outpatient claims or encounter forms. In turn, the plans took steps to ensure the complete coding of outpatient diagnoses when physicians submitted their claims. By 2004, outpatient coding was deemed sufficiently reliable that CMS began a transition to the CMS-HCC (Hierarchical Condition Categories) method of risk adjustment, which adjusts reimbursement to plans using diagnoses recorded on both inpatient and outpatient claims. Each CMS-HCC category has a weight, which is based partly on the cost of treating the diagnosis in TM. If a beneficiary has multiple diagnoses, the weights for each are added together to form a risk score, and reimbursement is approximately proportional to the risk score. (There are a few allowances for interactions, meaning that in a few cases reimbursement for a beneficiary with multiple diagnoses can reflect more than the sum of the weights for each diagnosis.) In 2004 the new CMS-HCC method received 30% weight, in 2005 50%, and in 2006 75%. Since 2007, the new method has been fully in place. Compared with the method used before 2000, incorporating the diagnostic information through the CMS-HCCs has raised the percentage of explained variance in annual individual spending from 1% to 11% to 12%.44

To reduce selection further, the 2003 Medicare Modernization Act changed the policy allowing beneficiaries to move between MA and TM each month. Although originally seen as protecting beneficiaries, their ability to change plans monthly facilitated selection and was notably different from employment-based insurance, in which employees with a choice of plans typically could change their plan only annually. The new, more restrictive rules on changing between MA and TM did not take effect until 2006, at which time Medicare beneficiaries who chose MA were “locked in” to their choice for the last 6 months of the year (ie, they could still change monthly during the first 6 months). In 2007 beneficiaries were locked in for the last 9 months of the year, and in 2011 the lock-in period was further tightened to the last 10.5 months of the year.

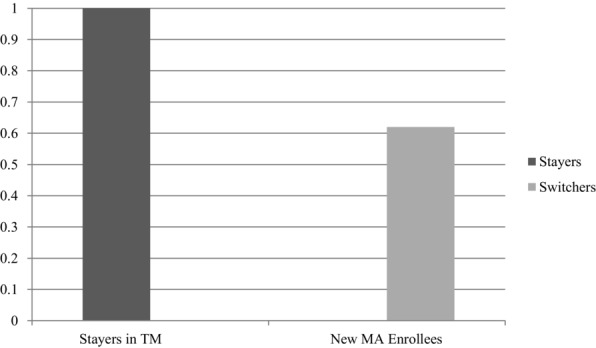

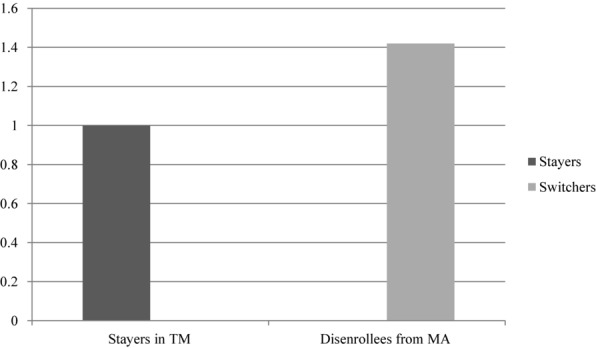

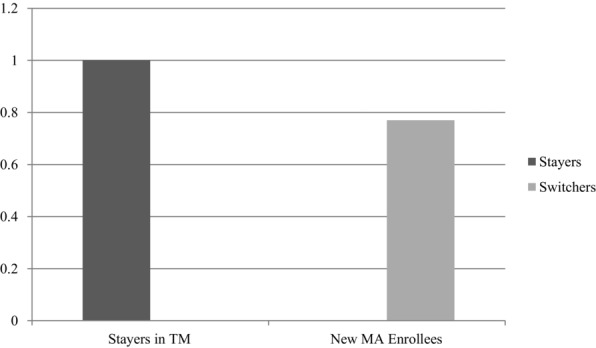

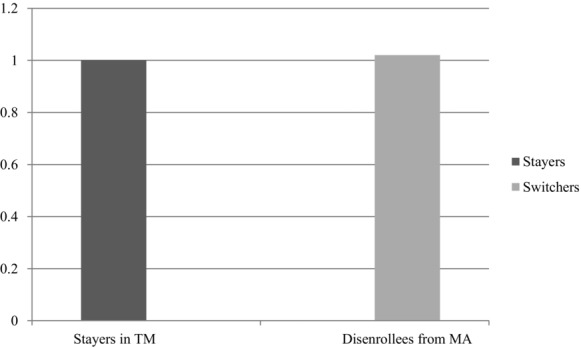

As we mentioned earlier, the timing of implementation makes it difficult to disentangle the independent effects on selection of the changes in risk adjustment from the implementation of the lock-in. Because neither change is likely to be reversed, however, what is important for policy purposes is that the combination of the two did substantially reduce selection.45,46 A traditional measure of selection is a comparison of spending or health status among “switchers” from TM to MA (new enrollees in MA who had been in TM) or from MA to TM (disenrollees from MA) with “stayers” who remained continuously in TM. (Historical comparisons with those stayers who remained in MA were not possible because of the lack of encounter data for services received in MA.) In the 1990s, using this method, the Physician Payment Review Commission and the Medicare Payment Advisory Commission (MedPAC) provided evidence of selection.47,48 They found that those who switched from TM to MA spent much less in TM in the 6 to 12 months before their enrollment in MA and that those who disenrolled from MA into TM spent at least as much in TM in the 6 to 12 months after disenrolling as did those continuously enrolled in TM (Figures 2, 3, 4, 5). In other words, healthy TM beneficiaries seemed to be enrolling in MA and potentially sick MA enrollees were disenrolling. These findings supported the claim that if the beneficiaries in MA had been in TM instead, Medicare would have saved money. Nonetheless, the support was somewhat weak. Because the vast majority of beneficiaries remained in their plans from year to year, these findings on differences among the small percentage who switched shed no light on any possible differences among the stayers in each type of plan.

Figure 2.

Evidence of Selection 1989-1994: Prior Medicare Spending of Those Switching to MA Compared with Those Remaining in TM

Values are based on 1989-1994 data and show spending by new MA enrollees in the 6 months before they joined MA (when they were in TM), compared with TM enrollees matched for age, sex, welfare status, employment status, and county. Stayers were randomly given a pseudodate of enrollment to match the new MA cohort's distribution of enrollment dates.47

Figure 3.

Evidence of Selection 1989-1994: Subsequent Medicare Spending of Those Switching to TM Compared with Those Remaining in TM

Values are based on 1989-1994 data and show spending by MA disenrollees in the 6 months after they left MA (when they were in TM), compared with TM enrollees matched for age, sex, welfare status, employment status, and county. Stayers were randomly given a pseudodate of disenrollment to match the actual disenrollees’ distribution of disenrollment dates.47

Figure 4.

Evidence of Selection 1997: Prior Medicare Spending of Those Switching to MA Compared with Those Remaining in TM

Values are based on 1997 data and show spending by new MA enrollees in the 12 months before they joined MA (when they were in TM), compared with TM enrollees matched for age, sex, welfare status, employment status, and county. Stayers were randomly given a pseudodate of enrollment to match the distribution dates of the new MA cohort's enrollment.48

Figure 5.

Evidence of Little Selection 1997: Subsequent Medicare Spending of Those Switching to TM Compared with Those Remaining in TM

Values are based on 1997 data and show spending by MA disenrollees in the 12 months after they left MA (when they were in TM), compared with TM enrollees matched for age, sex, welfare status, employment status, and county. Stayers were randomly given a pseudodate of disenrollment to match the distribution of the disenrollees’ disenrollment dates.48 The result shown, minimal selection, is much different from that in Figure 3, in part because of differences in methods and perhaps because the data come from a later year. The differences in methods are the following: (1) The data show the spending in 1998 of all disenrollees during 1997 versus the spending by those who did not disenroll. This meant that a person had to survive until January 1998 to be included (death was not counted as disenrollment for this purpose). In particular, if those near death in 1997 left MA and then died before January 1998, they were not included in this sample, but they were included in the 1989-1994 sample shown in Figure 3. MedPAC, however, made an adjustment for this. (2) Those persons in the 1989-1994 sample had to have been enrolled in MA for 3 months. (3) These values use 12 months of postenrollment spending, and Figure 3 uses 6 months. The adjustment for bias from deaths in the MedPAC study was as follows: The “treatment” group was made up of all TM members who enrolled in or disenrolled from MA in year t. To be included, they had to survive until the beginning of year t because the TM comparison group was enrolled in TM in both year t-1 and year t. To correct for possible bias, MedPAC calculated the distribution of enrollment in (and disenrollment from) MA by month for 1997. For example, 80% of the calendar year's enrollment may take place in January, 5% in February, etc. The researchers then randomly assigned the TM comparison group to a pseudomonth of enrollment (or disenrollment) based on these percentages. Finally, they dropped from the comparison group any persons who died before the pseudomonth of enrollment (or disenrollment).48

Stronger evidence of selection was the finding by MedPAC analysts that mortality rates for MA enrollees were 15% lower than those for TM enrollees after adjusting for age, sex, and Medicaid status.48 Since MA could not reduce mortality by 15%, this strongly suggested favorable selection. Indeed, because MA plans did not incur relatively high end-of-life spending as frequently as TM did, the difference in mortality rates alone was estimated to account for about a third of the difference in expenditures that the Congressional Budget Office attributed to favorable selection into MA plans.49

These analyses, however, rely on data from years that predate the better risk adjustment and the institution of a lock-in for longer than a month. Data from more recent years indicate much less selection. For example, by 2008, after the new risk adjustment method and the lock-in had been implemented, the risk scores (ie, the average CMS-HCC weight) of those switching to MA had become much more similar to those remaining in TM (Table 1). But because a plan's reimbursement is approximately proportional to its risk score, this similarity does not show whether MA plans are continuing to profit from favorable selection. To establish whether profitable selection is still occurring, we would need to know whether low-cost persons in a given CMS-HCC category are disproportionately enrolling in MA. If so, enrollment in MA would still be costing Medicare money. Nonetheless, the change in risk scores does imply that beneficiaries’ behavior has changed and that sicker beneficiaries are now more likely to enroll in MA. Although the risk scores of those disenrolling got worse (Table 1), there were about 5 new enrollees for every disenrollee, so a more representative mix of beneficiaries did indeed enroll in MA.

Table 1.

Risk Scores of Switchers to MA vs Stayers in TM and Switchers from MA vs Stayers in TMa

| By MA Type | ||||

|---|---|---|---|---|

| Overall | ||||

| Year | Switch to MA vs Stay TM Difference Switch: Stay (95% CI) | Switch to PFFS vs Stay TM Difference Switch: Stay (95% CI) | Switch to HMO vs Stay TM Difference Switch: Stay (95% CI) | Switch to PPO vs Stay TM Difference Switch: Stay (95% CI) |

| 2004 | −0.113 | −0.152 | −0.109 | −0.103 |

| (−0.120 to −0.107) | (−0.169 to −0.135) | (−0.116 to −0.102) | (−0.171 to −0.035) | |

| 2005 | −0.088 | −0.127 | −0.076 | −0.046 |

| (−0.093 to −0.083) | (−0.136 to −0.118) | (−0.082 to −0.070) | (−0.069 to −0.024) | |

| 2006 | −0.100 | −0.118 | −0.081 | −0.095 |

| (−0.104 to −0.097) | (−0.123 to −0.113) | (−0.086 to −0.075) | (−0.103 to −0.087) | |

| 2007 | −0.050 | −0.042 | −0.096 | −0.018 |

| (−0.054 to −0.047) | (−0.047 to −0.038) | (−0.104 to −0.088) | (−0.029 to −0.007) | |

| 2008 | −0.037 | −0.019 | −0.061 | −0.053 |

| (−0.041 to −0.033) | (−0.025 to −0.014) | (−0.069 to −0.054) | (−0.062 to −0.044) | |

| 2004 | −0.004 | −0.020b | −0.004 | −0.280b |

| (−0.024 to 0.015) | (−0.124 to 0.084) | (−0.023 to 0.016) | (−0.439 to −0.120) | |

| 2005 | 0.032 | 0.026b | 0.033 | −0.090b |

| (−0.002 to 0.066) | (−0.158 to 0.211) | (−0.002 to 0.067) | (−0.542 to 0.361) | |

| 2006 | 0.012 | −0.121 | 0.041 | 0.020 |

| (−0.014 to 0.037) | (−0.171 to −0.07) | (0.012 to 0.071) | (−0.156 to 0.196) | |

| 2007 | 0.069 | 0.041 | 0.098 | 0.064 |

| (0.052 to 0.086) | (0.016 to 0.066) | (0.070 to 0.127) | (0.024 to 0.104) | |

| 2008 | 0.093 | 0.027 | 0.131 | 0.126 |

| (0.074 to 0.111) | (−0.001 to 0.055) | (0.103 to 0.159) | (0.081 to 0.17) | |

Reproduced with permission from Health Affairs.46 The figures not in parentheses are the differences in adjusted risk scores in the given year between TM and the given group of MA beneficiaries. For example, the value −0.113 in the upper left-hand corner means that the adjusted risk score was 0.113 less among all MA enrollees than among all TM enrollees. The mean of the risk score in these years is around 1.1. The risk score is adjusted for age, sex, county MA penetration, and whether the person changed zip code. The figures in parentheses are 95% confidence intervals.

Results for disenrollees from PFFS and PPOs in 2004 and 2005 are from extremely small sample sizes.

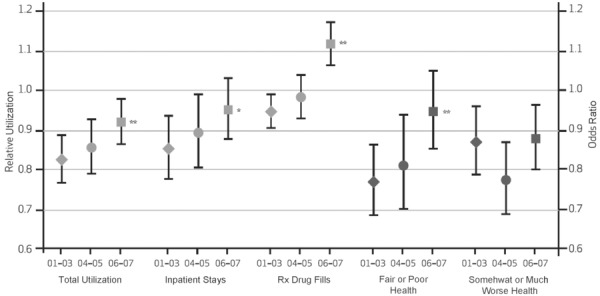

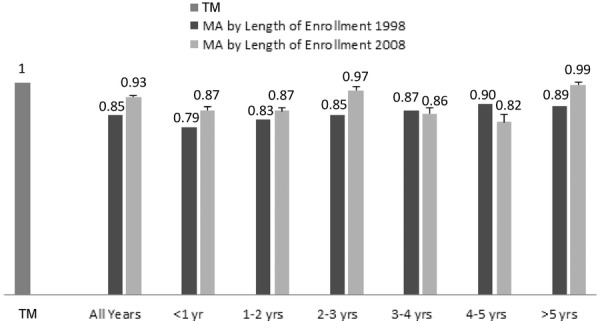

The conclusion that selection was reduced is greatly strengthened by 2 comparisons of all MA beneficiaries with all TM beneficiaries. Such comparisons are especially useful because, as we mentioned, only a small percentage of beneficiaries change plans each year, so the foregoing comparisons of switchers and stayers did not explain how the health status and utilization characteristics of the great majority of beneficiaries who remain in their respective plans year after year may differ from one another. The first is a comparison of how the self-rated health of all MA and all TM beneficiaries changed over time. The proportion of MA beneficiaries rating their health as fair or poor increased markedly in the 2000s such that by 2006–2007, we could not reject the null hypothesis of no difference from TM beneficiaries (Figure 6). The second is a 2008 update of the 1998 mortality differences described earlier. That comparison shows the differences roughly halved for all MA beneficiaries and essentially gone for those enrolled in MA for more than 5 years (Figure 7). Because of the large sample, the estimates are precise enough to indicate that this is a real change. Furthermore, the period before 2008 was a time of increasing MA enrollment. From 1998 to 2008, the proportion of beneficiaries in MA rose from approximately 16% to 21%, and it has continued to increase to 28% at present. If the new enrollees remain in MA, as one might expect given status quo bias, and if the share of MA beneficiaries remains at around 28%, as it has in the past few years, the share of the MA population enrolled for 5 years or more will rise, and overall mortality rates should converge.

Figure 6.

Differences in Utilization and Self-Reported Health Between All MA and All TM Enrollees, 2001-2003, 2004-2005, and 2006-2007

Reproduced with permission from Health Affairs.45 For each measure of utilization and of health, the differences between all participants enrolled in MA (continuously enrolled or switched into MA within calendar years) and all participants enrolled in TM (continuously enrolled or switched into TM during the calendar year) are plotted by period (2001-2003, 2004-2005, and 2006-2007) with 95% confidence intervals. Estimates of relative utilization (RU) and odds ratios (OR) are presented for comparisons of utilization and health indicators, respectively, with TM beneficiaries serving as the reference group. Statistically significant changes in group differences from 2001-2003 to 2006-2007 are noted at p < 0.10(*) and p < 0.05(**) levels.

Figure 7.

MA Mortality/TM Mortality, by Length of Enrollment in MA, 1998, 2008

Reproduced with permission from Health Affairs.46 Rates are adjusted for age, gender, and Medicaid status. For the TM group, anyone who was in MA at any point in 2003-2008 was excluded, and for the MA group, anyone who switched to TM in 2008 was excluded, except for MA enrollees who elected hospice in 2008 and were shown as in TM after that election (this group comprised 2% of MA enrollees who elected hospice). If the latter group is excluded, the 2008 rate for all years would drop to 0.92, the less-than-1-year rate to 0.85, and the more-than-5-year rate to 0.98. The bars above the 2008 rates are the upper limit of a 95% confidence interval. MedPAC did not compute confidence intervals for the 1998 mortality results, so we could not test formally for differences, but Part C enrollment in 1998 was 6 million versus 9.9 million in 2008. TM enrollment was slightly smaller than in 2008. Adjusting for the difference in sample size and the drop in the elderly's mortality rates between 1998 and 2008, confidence intervals in 1998 are about 30% larger than in 2008. Using this value, the mortality differences between 1998 and 2008 for all Part C enrollees, as well as for almost all the other differences shown, are significant at standard levels of significance.

Further bolstering the view that selection decreased is a comparison of risk scores in those counties in which MA expanded more relative to those in which it expanded less or even contracted. According to the favorable selection hypothesis, the persons deemed as best risks at a particular point in time disproportionately enroll in MA. If MA expands in a subsequent period, the new MA enrollees should be disproportionately the best risks formerly enrolled in TM.38,39 As a result of such selection, the expansion of MA should increase the risk scores in both MA and TM, a phenomenon that cancer epidemiologists call the Will Rogers hypothesis (after the Will Rogers remark that when the Okies moved from Oklahoma to California, they raised the average intelligence in both states).50 Contrary to the Will Rogers hypothesis, however, risk scores exhibit almost no relationship to MA penetration rates across counties. In fact, as MA penetration in a county increases, the risk scores of those in both TM and MA in that county are as likely to fall as to rise.46 This implies that the new enrollees are coming approximately at random from the entire risk distribution (as captured by the HCC risk scores), contrary to the favorable selection hypothesis.

One finding, however, supports a view of some remaining selection, that more than half the living persons who disenroll from an MA plan reenroll in MA within a year of disenrolling.46 Why did they disenroll and then reenroll shortly thereafter? A likely possibility is that they wanted to have a procedure done by an out-of-network provider and after the procedure had been completed, they reenrolled. Consistent with this view, those disenrolling have higher risk scores (Table 1). But as mentioned earlier, the proportion of disenrollees in any one year is small, only about 2% to 3%, so their influence on the amount of selection overall is small as well.

With the possible exception of the last finding on reenrollment, none of the tests for selection just described directly bear on the question of whether MA plans continue to be overpaid because of favorable selection. In theory, if MA plans were able to select favorably within an HCC—for example, to attract relatively inexpensive diabetics and inexpensive cancer patients but not attract relatively expensive diabetics and relatively expensive cancer patients—they would be overpaid (relative to what Medicare would have paid for the same beneficiaries in TM). Indeed, Brown and colleagues maintain that this is exactly what happened when the CMS-HCCs were introduced.51 We take up their contention in the next section.

Plan Behavior

Selection

Plans have several instruments to affect the mix of beneficiaries who choose them.52,53 The plans can choose how many and which physicians are in their networks, although they still are subject to Medicare regulations that their networks must be “adequate.” They can choose the formulary placement of various drugs, along with the copayment for those drugs, although like networks, their choices are somewhat constrained by regulation. Finally, the plans can choose how to market themselves.

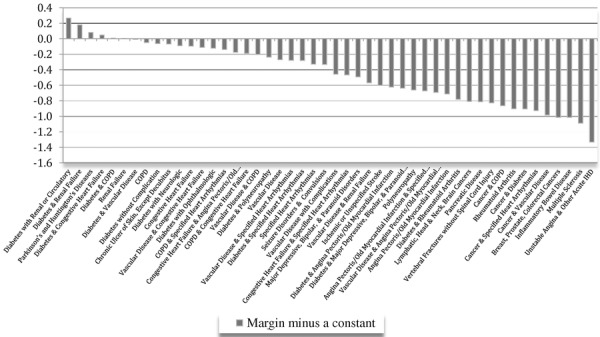

If certain diagnoses are more profitable than others, we might expect plans to have more extensive networks or formularies for the more profitable diagnoses. One way for a diagnostic area to be profitable for a plan is if the plan can manage costs in that area relatively well. For patients with a particular diagnosis or combination of diagnoses, Medicare pays the plans approximately in proportion to what TM spends to treat those diagnoses. But the cost to plans of treating patients with various diagnoses may depart from what TM spends, because of the importance of medical management for some diagnoses and because when negotiating fees with physicians they may have varying degrees of market power. In fact, profitability appears to differ greatly across diagnoses. The data on actual payouts by one plan for 48 relatively common HCCs, or combinations of HCCs, show widely differing margins, meaning that plans pay out relatively less for beneficiaries with certain diagnoses than for others and therefore that such beneficiaries are differentially profitable (Figure 8). Moreover, this plan's margins for these categories of patient do not appear unusual, since they are correlated with the margins of a second plan for these same 48 HCCs (r = 0.39, p < 0.01).

Figure 8.

Margins by HCC or a Combination of HCCs (minus a constant)

Adapted from the Journal of Health Economics.54 The values of the margins are average reimbursement in MA for that diagnosis or combination of diagnoses divided by the average cost in MA for a single plan less a constant to preserve confidentiality. The average reimbursement in MA is approximately proportional to the average cost in TM, so those HCCs or combinations of HCCs to the left in the figure are those for which the ratio of the cost in MA to the cost in TM to treat the condition is larger than those HCCs to the right.

Figure 8 shows that the plan's margins vary across these different diagnoses by 160 percentage points. Such a large difference in margins by HCC offers obvious selection incentives, since the plan earns much more from enrollees with the diagnoses to the left of Figure 8 than from enrollees with the diagnoses to the right. Despite the large difference in margins across the HCCs, however, there is no evidence of selection behavior; the proportion of the plan's MA enrollees in each of the 48 HCCs closely approximates the proportion of TM beneficiaries in those HCCs.54 This plan's distribution of beneficiaries across the 48 HCCs also is close to the entire MA distribution across these 48 HCCs, implying that if other plans have similar margins, there is little selection across HCCs. Not surprisingly, given how closely the plan's distribution of beneficiaries across the HCCs approximates the TM distribution, we cannot reject the null hypothesis of no relationship between the difference in MA and TM shares in an HCC and the margin in that HCC. In fact, the sign of the estimated coefficient is slightly negative, contrary to the selection hypothesis.

This finding of little selection across HCCs casts doubt on Brown and colleagues’ claim of plans’ adapting their selection efforts to select within HCCs, because it surely is less expensive to select across HCCs than within an HCC. This is especially true for the great majority of MA plans that contract with independent physicians and hospitals. As mentioned earlier, an MA plan's principal instruments for attracting favorable risks are its choices regarding its network, formulary, and marketing. Although it is possible to imagine network and formulary choices that would be unattractive to most individuals in certain HCCs, for example, patients with colon cancer, it is harder to imagine network and formulary choices that would appeal to inexpensive colon cancer patients but not appeal to expensive colon cancer patients. Nor are we are aware of marketing efforts directed toward specific disease categories.

But what about Brown and colleagues’ evidence of selection within CMS-HCCs referred to earlier and their claim that the introduction of the HCCs actually increased the amount of selection? We approximately replicated their specification using a much larger sample and obtained a different result.55 Specifically, we looked year-by-year at the 2 years before HCCs were introduced, the 3-year transition period, and the 5 years after full implementation.

Although we, as well as Brown and colleagues, found evidence of selection within an HCC, we found that the amount of such selection for the non-institutionalized, non-duals was not much different in 2002 and 2003, before the HCC program began, than in 2007–2011, after the HCC program was fully in place. Moreover, the amount of selection overall decreased after introducing the HCCs. Among the institutionalized and the duals there were too few switchers (<1%) in the pre-HCC era to obtain reliable results. We interpret these results as consistent with our view of some modest amount of remaining selection, perhaps because those who are sickest within an HCC prefer TM's freedom of choice, perhaps in the form of something so simple as a beneficiary jumping out of MA for a limited period of time to have a procedure done out of the network.

Quality of Care in TM and MA

The plans’ medical management methods could, in principle, improve the quality of their care relative to that of TM. Unfortunately, it is difficult to compare the quality of care in TM and MA because the data necessary to do so are sparse.56,57 A few comparisons can be made, however, from the data reported by beneficiaries in the Consumer Assessment of Healthcare Providers and Systems (CAHPS) surveys, although the beneficiaries’ ability to assess the technical quality of their care clearly is limited. Healthcare Effectiveness Data and Information Set (HEDIS) process measures are available to assess technical quality among MA plans, which must report such measures to CMS, but there is no comparable reporting for TM. Most HEDIS process measures cannot be calculated from the claims data available for TM because the measures require data from the medical chart, for example, the proportion of controlled hypertensives or the proportion of beneficiaries with HbA1c values over 7.

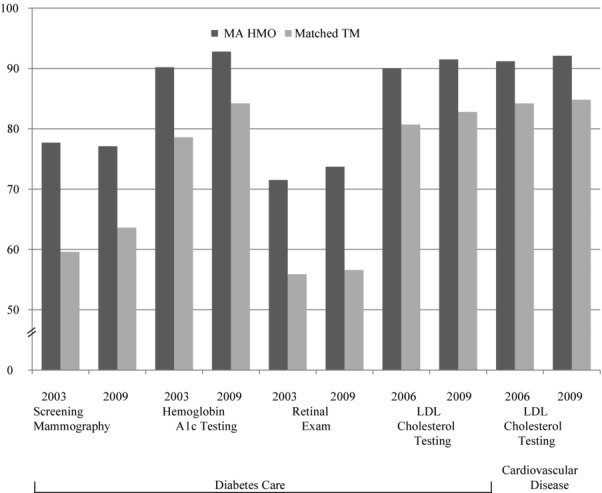

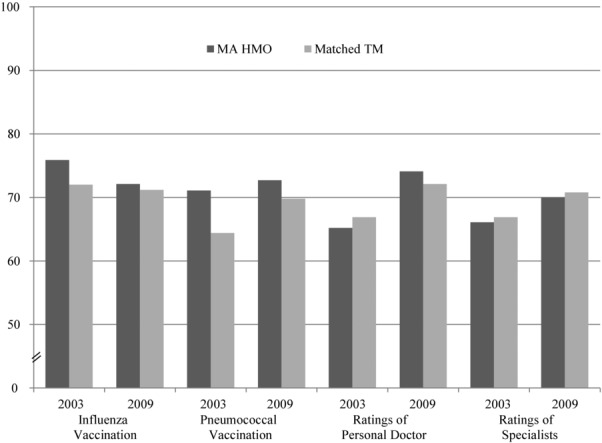

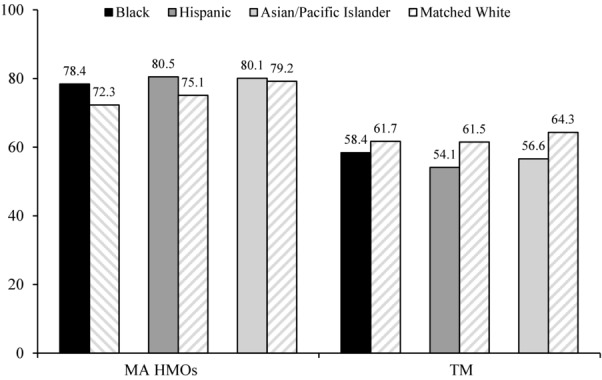

Nonetheless, some comparable HEDIS measures can be calculated from TM claims, and some measures of patient satisfaction can be compared using CAHPS. Those measures that can be compared using claims or CAHPS data are shown in Figures 9 and 10. Most comparisons favor MA. In addition, MA plans may ameliorate disparities. A comparison of differences by racial and ethnic groups in mammography rates shows that MA plans not only reduce disparities but that the traditional differential between whites and minority groups in TM also reverses in MA (Figure 11).

Figure 9.

Quality of Care as Assessed by HEDIS Measures for MA HMOs Matched to TM Beneficiaries in 2003 or 2006 and 2009 (% receiving)

Reproduced with permission from Health Affairs.57 HMO and TM enrollees were matched by age, sex, and race/ethnicity in local areas and weighted by MA HMO plan enrollment to derive national estimates. All differences between MA HMOs and TM were statistically significant (p < 0.001) for each measure in each study year. For LDL cholesterol testing, the measure specifications changed in 2006, so the figures for earlier years are not presented.

Figure 10.

Quality of Care on CAHPS Measures for MA HMOs Matched to TM Beneficiaries in 2003 and 2009 (% receiving or beneficiary ratings on 0-100 scale)

Reproduced with permission from Health Affairs.57 HMO and TM enrollees in counties were matched by age, sex, and race/ethnicity self-reported health status and were weighted by enrollment in MA HMO plans to derive national estimates with 2-tailed p values for each measure by study year. CAHPS measures were not collected for MA HMO enrollees in 2006 or for TM enrollees in 2005 or 2006, and response rates were relatively low for both groups in 2007. For ratings of personal doctor and specialists, proportions represent ratings of 9 or 10 on a 0-10 scale. Two-sided p-values are shown.

Figure 11.

Use of Mammography by Race/Ethnicity Among Women Ages 65-69 in MA HMOs and TM (values are % of users)

Adapted from the Journal of the National Cancer Institute.58

The pattern of margins by HCC (Figure 8) is suggestive as well of better-quality care in MA. MA plans have a financial incentive to manage chronic illnesses so as to minimize total medical and pharmaceutical expense. More specifically, given the low likelihood of disenrollment, they have an incentive to minimize the progression of any disease and to avoid hospitalization. The margin data demonstrated how successful they are because they reflect the cost of treating beneficiaries with the same diagnoses in TM relative to the cost in MA. In other words, high-margin HCCs or combinations of HCCs are those in which the MA cost is low relative to that of TM and vice versa.

The highest margins shown in Figure 8 are for diseases amenable to medical management by primary care physicians. Diabetes, for example, is overrepresented among high-margin HCCs. Fourteen HCCs involve diabetes, and most are toward the left in Figure 8, including 7 of the 11 highest-margin HCCs. Six HCCs involve chronic heart failure, and 5 of those 6 are above the median in profitability. Similarly, 5 of the 6 chronic obstructive pulmonary disease HCCs are above the median in profitability. By contrast, acute ischemic heart disease is the lowest-margin HCC; medical management cannot be effective in acute situations.

At the other end of the spectrum, diseases treated by specialists, especially cancer, are overrepresented among low-margin HCCs, perhaps because MA plans face greater provider market power from medical specialists and thus must pay higher unit prices relative to TM than when negotiating with primary care physicians. All 6 cancer HCCs are among the 12 lowest-margin HCCs; that is, all are in the bottom quartile. In addition to cancer, rheumatoid arthritis and multiple sclerosis are among the low-margin HCCs, also diseases generally managed by specialists. Furthermore, drugs administered by physicians are important to the treatment of cancer, rheumatoid arthritis, and multiple sclerosis, so the relative lack of profitability is consistent with the market power (vis-à-vis MA plans) of physicians who dispense such drugs.

Cost in MA and TM

From the perspective of the Medicare program, costs in MA and TM can be viewed as including both beneficiary cost and Medicare cost, that is, social cost. Earlier literature regarded Medicare managed-care plans as lowering social cost in comparison to TM, just as HMOs’ costs generally were lower than those of non-managed-care plans in employer-based insurance, but these savings were not transferred to Medicare because of selection and the limitations of the risk adjustment methodology in compensating for it.1 There are, however, more recent data regarding social cost. For example, we can use the CAHPS data just described to compare rates of procedure use in MA and TM. Landon and colleagues matched each MA plan's CAHPS data with data from Medicare claims for similar beneficiaries in the same location of the plan for the years 2003 through 2009.56 Rates of ambulatory surgery and emergency department use were 20% to 30% lower in the MA plans. The difference was concentrated in elective procedures regarded as more “discretionary,” such as knee or hip replacements. Repair of a fracture of the femur, a less discretionary procedure, was actually greater in MA.

Minimizing social cost also involves using more durable procedures if equally effective. Landon and colleagues found that coronary problems were more frequently treated with coronary bypass surgery in MA rather than the less durable percutaneous coronary intervention, suggesting not just lower long-run costs on average but a more appropriate use of services, since the patient was potentially spared a repeat procedure.

In an unpublished paper, Landon and colleagues studied resource use in episodes of care for diabetes and cardiovascular disease (written communication, February 2014). Applying a set of standardized price weights to isolate differences in resource use, they found 20% fewer services overall in MA plans relative to those in TM for both disease groups.

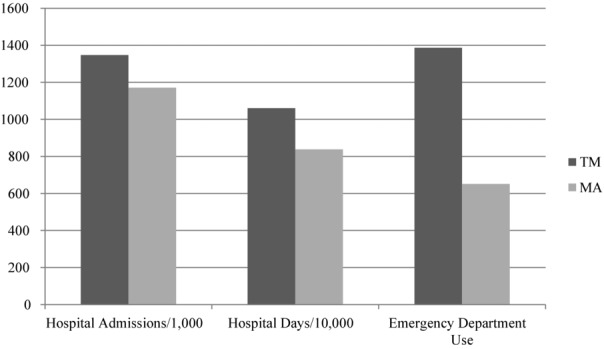

Comparisons of care at the end of life in MA and TM differ and favor MA.59 In 2009, use of the emergency department, for example, was less than half as great in the last 6 months of life for decedents enrolled in MA relative to those enrolled in TM, and hospital admissions were 13% less (Figure 12).

Figure 12.

Hospital Admissions, Hospital Days, and Emergency Department Use Among Decedents in the Last 6 Months of Life, TM and MA, 2009

Adapted from Medical Care.59

How these savings in social cost are divided between Medicare and MA plans depends on the methods by which Medicare determines plan payments. Since 2006, MA plans have submitted bids rather than accept a take-it-or-leave-it price, as they did earlier. Plan bids, however, are calibrated against a benchmark that from the beneficiary's point of view functions much like a voucher. Before 2011 the benchmark for a particular county was set using the same method used to set the earlier take-it-or-leave-it price. If plans bid below this amount—and 95% of them did—beneficiaries received a rebate equal to 75% of the difference between the bid and the benchmark. The rebate could take the form of additional covered services such as dental, lower cost sharing, or lower premiums. (In a true voucher scheme, of course, beneficiaries would receive or pay 100% of the difference in cash.) If it already charged no premium for its MA plan, the plan could lower its price even further by subsidizing the Part B premium, as described earlier.

The Affordable Care Act kept this basic structure of bidding for MA plans but changed both how benchmarks were set and the details of the rebate. Although we are now in a transition between the old and the new systems, by 2017 the benchmark will be solely a function of TM risk-adjusted costs per beneficiary in the county. The highest spending quartile of counties will have a benchmark equal to 95% of (risk-adjusted) per beneficiary TM spending in the county, and the lowest spending quartile will have a benchmark of 115% of TM spending. The 2 intermediate quartiles will receive 100% and 107.5% of TM spending, respectively. And starting in 2012, the ACA made the rebate contingent on a plan's quality rating. The new rebates range from 50% to 70%, depending on the rating rather than the flat 75% under the old system. In addition, the new system pays bonuses to high-quality plans.

We might ask how well this bidding structure yields a result that approximates a model of perfect competition, which would maximize the transfer of social cost savings to the Medicare program. The answer is, imperfectly. Using data from 2006–2010, Song and colleagues found that a $1 increase in the benchmark led to approximately a $0.50 increase in benefits, whereas in a perfectly competitive model it would lead to an increase equal to the amount of the rebate, which in those years would have been close to 75%.22,23 (It would not be exactly 75% because 5% of plans bid above the benchmark and would not have offered rebates even if the benchmark had increased by a small amount.)

Market imperfections, however, could lie on the insurer, the provider side of the market, or both. In many states the insurance market is concentrated, and in the commercial market the insurer has market power.60,61 Because insurers operating in the commercial market are largely the same ones that operate in the MA market, it is likely that they also have market power there. The provider market, however, is becoming increasingly concentrated in many localities as well.62,63 Because the benchmark is public information, a provider with market power that is negotiating its reimbursement rate with a plan should be able to extract some of any increase in the benchmark.

Government Policy Toward Part C Plans

Medicare policy regarding Part C Plans encompasses plan payment methodology, policy for beneficiary premiums, and a large body of regulations applying to other aspects of the plans’ operation, including benefits offered. We focus here on policy for plans’ payment and beneficiary premiums.

Risk Adjustment and the Level of Plan Payment

As described earlier, stricter lock-in periods and better risk adjustment appear to have substantially reduced selection problems in MA. Although further refinement of risk adjustment methods may not be necessary, our work suggested that there are too few disease-disease interactions in the current risk adjustment model because MA plan margins decrease with the number of comorbidities and risk scores.54 In other words, the incremental cost of treating a beneficiary with diseases X and Y is greater than the sum of the independent incremental costs of treating disease X and disease Y. Capturing this pattern in risk adjustment requires adding interaction effects representing the presence of both diseases.

We found several reasons to maintain the level of payment to MA plans at or above the level of TM. First, the quality and appropriateness of care appear to be at least as high in MA as in TM. Second, the social cost of care in MA appears to be lower than in TM. Third, we found evidence for positive “spillovers,” meaning that higher MA enrollment in a county reduces hospital costs in TM in that county. Medicare does not immediately capture the savings, since it pays per admission (unless an admission without a procedure replaces one with a procedure). Rather, the savings would have to be captured later by a smaller update factor. Reducing the percentage of the benchmark paid to MA plans, as was done in the ACA, generates program savings for Medicare, but from the standpoint of the Medicare program's social efficiency, cuts in MA plan payments may be shortsighted.

Premium Regulation—The “Single Premium” Problem and Ways to Deal with It

Glazer and McGuire examined the socially efficient sorting of individuals between TM and MA.28,36 Previously this issue had been formulated as a standard managed competition problem, meaning that reimbursement for TM and MA should be equal, risk adjustment should address selection, and beneficiary choice would lead to an efficient outcome. For example, “The [Medicare Payment Advisory] Commission strongly believes that beneficiaries should be given the choice of delivery systems that private plans can provide and that payment mechanisms should promote financial neutrality between private plans and the traditional program.”13 Although MA beneficiaries are required to purchase Part B at the same price required by TM beneficiaries, MA plans are free to set a premium above that, as we noted, or charge no premium or rebate part or even all of the Part B premium. TM beneficiaries also are free to buy a supplementary policy at a market-determined premium. This is consistent with Enthoven's notion of plans charging beneficiaries for the marginal premium dollar and allowing a choice of plans.64

Glazer and McGuire, however, pointed out that there is heterogeneity in demand among Medicare beneficiaries conditional on their health status and that TM accommodates this heterogeneity (moral hazard).36 MA, in contrast, rations care but may ignore the demand heterogeneity. A more socially efficient premium policy would charge higher-demand consumers a higher premium to elect TM, as described earlier. Although Medicare cannot observe individual “tastes” for medical care, those tastes may be correlated with income. If so, Medicare could charge higher-income beneficiaries more to join TM. Currently, an element of Medicare Part B and Part D premiums is related to income, but the surcharge for higher-income beneficiaries is the same for TM and MA. Glazer and McGuire proposed that the income-related surcharge be dropped for MA, effectively increasing the TM price relative to MA for higher-income Medicare beneficiaries.

Premium policy cannot be used for dual-eligible beneficiaries, who likely benefit disproportionately from the coordinated care that MA plans can provide. Although historically most such beneficiaries were in TM, this is rapidly changing as states convert the dual-eligible population to managed care in a large demonstration project and through the MA Special Needs Plans for duals.65

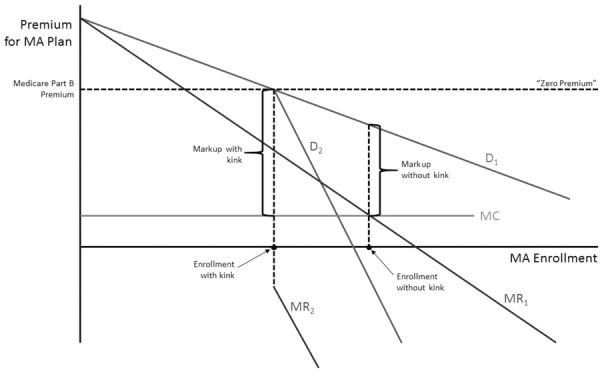

Premium Regulation—Smoothing the Kink in Demand at “Zero Premium”

As we argued in regard to Figure 1, bunching MA premiums at the “zero-premium” level signals a possible change in the slope of the plans’ demand curve. We reasoned that asymmetric “salience” of demand response above and below the zero-premium point caused the bunching of plans charging a zero premium. This idea can be developed further to describe beneficiaries’ demand for membership in an MA plan, thereby implying that the asymmetric salience creates artificial market power for the plans.

Market power flows from demand inelasticity. The less elastic the demand is, the more that a profit-maximizing firm will mark up the price above cost to maximize its profit. The gap between price and (social) cost restricts the quantity demanded, thus leading to social inefficiency. In our context, plans’ market power causes higher prices (premiums) and leads to too few beneficiaries in MA.

Figure 13 shows a “kinked demand curve” (once used in introductory economics to explain the rigidity of prices in an oligopoly). Beneficiaries’ demand for membership is shown as a function of the premium charged by an MA plan. The beneficiary pays the $104.90 Medicare-set Part B premium, plus or minus any premium set by the MA plan. As described, if substantial numbers of beneficiaries disregard the amount deducted from their Social Security checks, regardless of their plan choice, premium reductions by MA plans that already charge a zero or negative premium will have a smaller effect on demand than will a similar reduction in a positive premium, since the reduction in the positive premium reduces the size of the check the beneficiary must write. Under these conditions, there is a “kink” in the demand at the “zero-premium” level.

Figure 13.

The “Kinked Demand Curve” for MA Explains Prevalence of “Zero-Premium Plans,” Inhibits Enrollment, and Reinforces Market Power

This form of demand has adverse consequences for market performance. The plan maximizes profit in which marginal revenue (MR) equals marginal cost (MC). The kinked demand curve creates a discontinuity in the MR schedule at the kink. To the left of the kink, the relevant MR schedule is MR1 associated with D1 demand for a price above the Part B premium. To the right of the kink, the relevant MR schedule is MR2, associated with D2 describing demand for prices below the Part B premium. This is consistent with the bunching, because for a large range of MC schedules, quite a bit above and below the particular MC schedule shown in Figure 13, the profit-maximizing premium is the same: zero.

An additional problem the salience effect causes is that the markup above marginal cost can be high, leading to lower enrollment in MA. If this interpretation has merit, part of the “underenrollment” in MA is due to market power. It implies that MA plans should be “buying down” premiums for Medicare beneficiaries more frequently than they are; that is, they should be giving out cash rebates more frequently. Of course, doing so would mean covering fewer optional services or imposing more cost sharing.

Figure 13 also shows the benefit of smoothing the kink. If the salience effect of high/low price sensitivity could be ironed out, demand would look like D1 throughout the range; that is, D2 would be irrelevant. A profit-maximizing plan would still want to mark up costs in its own interests, but since it would use the MR schedule MR1 for the full range of cost, the markup would be less and MA enrollment would be higher (shown in Figure 13 as “markup without kink”).

An administrative change not altering anything “real” could address this salience-related problem. Beneficiaries could pay for MA plans in the same way they pay for Part B in TM, by having any MA premiums deducted from their Social Security checks. This would be more convenient for the beneficiaries and offer them a choice, for example, of $104.90 per month for TM versus $109.90 for an MA plan that charged monthly a $5 additional premium. In economic terms, this change should increase demand elasticity (decreasing market power for MA plans) and lower prices, leading to more MA enrollment and to more efficient premium-coverage offerings by plans. Moreover, the tendency of beneficiaries to overweight premiums and underweight later cost sharing and higher benefits would help raise MA enrollment.

Leveraging Salience and Status Quo Bias

A simple (but radical and more controversial) change would be to change the “default option” in Medicare. At present, if a beneficiary makes no choice when becoming eligible for Medicare, he or she is, by default, assigned to TM. This default option could be changed to move some or all of the nonchoosers into MA. In Part D, nonchoosers are randomly assigned to lower-cost Part D plans. In the case of one important Medicare population, those eligible for both Medicare and Medicaid, the default policies are already being changed. Massachusetts, soon to be followed by other states, is moving more of the dual eligibles into MA plans by requiring them to choose TM and, if they do not, making an MA plan the default option.

Conclusion

On balance, these more recent findings that we have reviewed point to a more positive view of MA than that of the earlier literature. In our view, the most important charge against MA was that it cost Medicare money without adding value. Selection combined with poor risk adjustment in the 1990s meant that MA enrollees cost Medicare more as a group than they would have cost in TM. Comparisons of the two systems’ quality were lacking, although a natural assumption was that their quality was similar, since most of the same physicians and hospitals delivered the care.

The more recent work indicates that selection is much reduced. To the extent that periodic disenrollment in order to use out-of-network providers is responsible for the residual selection, such behavior could be addressed by mimicking commercial insurance institutions—increasing the lock-in period to a full year and not allowing reenrollment in MA until the next annual open enrollment period. Because comparisons of MA's and TM's quality are still severely limited, we cannot make an overall assessment with confidence, but most of the few comparisons do favor MA. In other words, the integration and coordination of care that MA fosters may well pay off in higher-quality care.

Market power appears to exist in the MA program, on either the plan side or the provider side—and very likely on both sides—because some of any increase in Medicare reimbursement flows to plans or providers rather than to beneficiaries. Furthermore, the choice in Medicare is complex for beneficiaries; some might even say daunting. But it is not necessarily more complex in MA than in TM. Although MA beneficiaries must choose from among many MA plans, TM beneficiaries must choose from among many Medigap plans and many Part D prescription drug plans. Nonetheless, the coexistence of TM and MA dramatically increases the burden of choice for any beneficiary who actively investigates both options. The coexistence of the 2 programs also complicates care for providers, particularly when MA plans shift some of the risk to them, because of the conflicting financial incentives of taking risk relative to fee-for-service.

Because of the ACA's overall reductions in MA reimbursement, which CBO estimated as $136 billion over 10 years, few expect large increases in the future share of beneficiaries in MA. Nonetheless, the share has continued to rise marginally, despite the cuts since 2011.66 And with 28% of the beneficiaries in MA, it is important to understand the value of MA relative to that of TM. CMS has now begun to collect encounter data on MA enrollees, which should permit a richer evaluation of MA than is now possible.

The ACA also introduced a third arm in Medicare, Accountable Care Organizations (ACOs), formed at the discretion of provider groups “that are willing to become accountable for the quality, cost, and overall care of the fee-for-service Medicare beneficiaries assigned to it” (Section 1899[b][2][A] of the ACA). ACOs agree to bear some of the risk in payment, although for the first few years, that risk may be asymmetric (sharing only in gains relative to a target). Beneficiaries do not actively choose ACO membership but instead are assigned to the physician from whom they receive most of their primary care services. If this physician is part of an ACO, then that ACO can share in any cost savings that may arise from treating the beneficiary, with the savings measured against the estimated TM costs for that beneficiary. From the beneficiaries’ point of view, the ACO program looks like TM except that they receive a letter advising them that they can opt out of having CMS share their claims data with the ACO.

The ACO program is like a halfway house between TM and MA. Like MA, ACOs can profit from treating beneficiaries at a lower cost than TM. Unlike MA, however, beneficiaries do not enroll in an ACO and can use any provider participating in TM, with the same financial liability that they would have in TM. In other words, because there are no networks, there are no higher out-of-pocket payments for using an out-of-network physician. Any rationing of care or use of conservative specialists is left to the primary care physician and any medical management used by the ACO. ACO-like organizations, without the specific requirements for Medicare participation, are cropping up in commercial insurance as well.

One might assume that a successful ACO would seek to become an MA plan, since it could then receive the entire savings in care rather than sharing it with Medicare. This, however, is not necessarily the case; ACO reimbursement is based on the beneficiaries’ past expenses attributed to the ACO, updated to reflect increases in TM costs for treating the categories of beneficiaries attributed to the ACO. As described, MA reimbursement varies between 95% and 115% of a county's average TM expense. As a result, especially in counties where MA is paid less than TM, there could be a disincentive to convert a successful ACO to an MA plan. Other features of ACO reimbursement also could persuade an ACO not to convert to an MA plan.

In any event, there currently are 3 types of organizations to compare in Medicare: MA, TM, and ACOs. ACOs are likely to affect the competitive environment for providers and could change the way that beneficiaries are treated in TM. In turn, this could alter the beneficiaries’ choice between MA and TM, and also the incentives facing the MA plans. These issues remain for future work.

Acknowledgments

This article summarizes much of the research conducted using grant no. P01 AG032952, The Role of Private Plans in Medicare, from the National Institute on Aging, whose support is gratefully acknowledged. The authors are grateful to 3 referees for comments on an earlier draft and to John Iglehart for permission to reprint graphical work previously published in Health Affairs. Joseph P. Newhouse wishes to disclose that he is a director of and holds stock in Aetna, which sells both Medicare Advantage and traditional Medicare supplementary plans.

References

- 1.McGuire TG, Newhouse JP, Sinaiko AD. A history of Medicare Part C. Milbank Q. 2011;89(2):289–332. doi: 10.1111/j.1468-0009.2011.00629.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.Gold M, Jacobson G, D'Amico A, Neuman T. Medicare Advantage 2013 spotlight: enrollment market update http://kaiserfamilyfoundation.files.wordpress.com/2013/06/8448.pdf. Published June 2013. Accessed September 7, 2013.

- 3.Centers for Medicare and Medicaid Services. CMS fast facts http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/CMS-Fast-Facts/index.html. Updated January 15, 2014. Accessed February 5, 2014. [DOI] [PubMed]

- 4.Eggers P. Risk differential between Medicare beneficiaries enrolled and not enrolled in an HMO. Health Care Finance Rev. 1980;1(3):91–99. [PMC free article] [PubMed] [Google Scholar]

- 5.Eggers P, Prihoda R. Pre-enrollment reimbursement patterns of Medicare beneficiaries enrolled in “at-risk” HMOs. Health Care Finance Rev. 1982;4(1):55–73. [PMC free article] [PubMed] [Google Scholar]

- 6.Langwell KM, Hadley JP. Evaluation of the Medicare competition demonstrations. Health Care Finance Rev. 1989;11(2):65–80. [PMC free article] [PubMed] [Google Scholar]

- 7.Brown RS, Bergeron JW, Clement DG, Hill JW, Retchin SM. The Medicare Risk Program for HMOs—Final Summary Report on Findings from the Evaluation. Princeton, NJ: Mathematica Policy Research, Inc; 1993. [Google Scholar]

- 8.Brown RS, Clement DG, Hill JW, Retchin SM, Bergeron JW. Do health maintenance organizations work for Medicare. Health Care Finance Rev. 1993;15(1):7–23. [PMC free article] [PubMed] [Google Scholar]