Abstract

Microfinance is a popular intervention for poverty, but the intersection between microfinance and neurologic disorders in low- and middle-income countries (LMIC) has yet to be fully explored. Microfinance institutions (MFIs) provide small loans to impoverished clients who may otherwise not have access to loans, with which they can start their own enterprises.1 To date, MFI clients are usually women, and loans are often given with repayments guaranteed by groups rather than individuals.2 Microfinance programs are offered by both nonprofit and for-profit organizations.2 Although the actual impact of microfinance on poverty can be controversial, microfinance has generated enthusiasm among many philanthropists and private citizens, especially in higher income settings, as a putative “silver bullet for alleviating poverty.”2

Microfinance is a popular intervention for poverty, but the intersection between microfinance and neurologic disorders in low- and middle-income countries (LMIC) has yet to be fully explored. Microfinance institutions (MFIs) provide small loans to impoverished clients who may otherwise not have access to loans, with which they can start their own enterprises.1 To date, MFI clients are usually women, and loans are often given with repayments guaranteed by groups rather than individuals.2 Microfinance programs are offered by both nonprofit and for-profit organizations.2 Although the actual impact of microfinance on poverty can be controversial, microfinance has generated enthusiasm among many philanthropists and private citizens, especially in higher income settings, as a putative “silver bullet for alleviating poverty.”2

MICROFINANCE AND HEALTH

There is evidence that microfinance can be applied successfully to some problems in health care. MFIs require loan repayment reinforced by a social network, so benefits from MFIs are not only financial, but also social. The social network and additional attention provided to MFI beneficiaries have the potential to facilitate new health care initiatives. MFIs can provide financial support while offering patient education, enabling access to health care, and building community capacity for health services and infrastructure.3 A recent review summarizes studies that evaluate the effectiveness of MFIs in improving health care, with various levels of evidence ranging from observational studies to randomized trials.3 Overall, these studies show that (1) microfinance can help with the dissemination of health knowledge to loan recipients, and (2) microloans are feasible to deliver in the health care setting.3

WHY MICROFINANCE MAY BE USEFUL IN NEUROLOGIC DISORDERS

Given that microfinance has been successfully applied to other global health problems, it is worth exploring the application of microfinance to neurologic disorders. In LMIC, the cost of disability secondary to neurologic disorders can be high. Although several examples exist, the disorders that have been best studied include epilepsy, stroke, and traumatic injuries. Epilepsy has substantial socioeconomic implications; people with epilepsy face stigma and lack of access to medications, which may result in the so-called epilepsy treatment gap.4 As another example, stroke is more common in LMIC, and the resulting morbidity and mortality rates are greater than those in higher income countries.5 Even if care is received and the patient returns to baseline functioning, the cost of acute medical care and treatment may be bankrupting. For example, in Togo, the average person spends less than €4 per year on health, but an average hospital stay for acute stroke, lasting 17 days, costs 170 times that amount.6 Finally, there are significant disparities in management and outcomes in spinal cord injuries between LMIC and higher income countries.7 Disparities in outcome may be secondary to lack of access to treatments, medical expertise, or rehabilitation services. Neurologic disorders likely have more devastating effects for patients in LMIC compared to higher income countries because social safety nets and public assistance are often the exception. Although several additional examples exist, it is apparent that neurologic diseases are especially costly in LMIC.

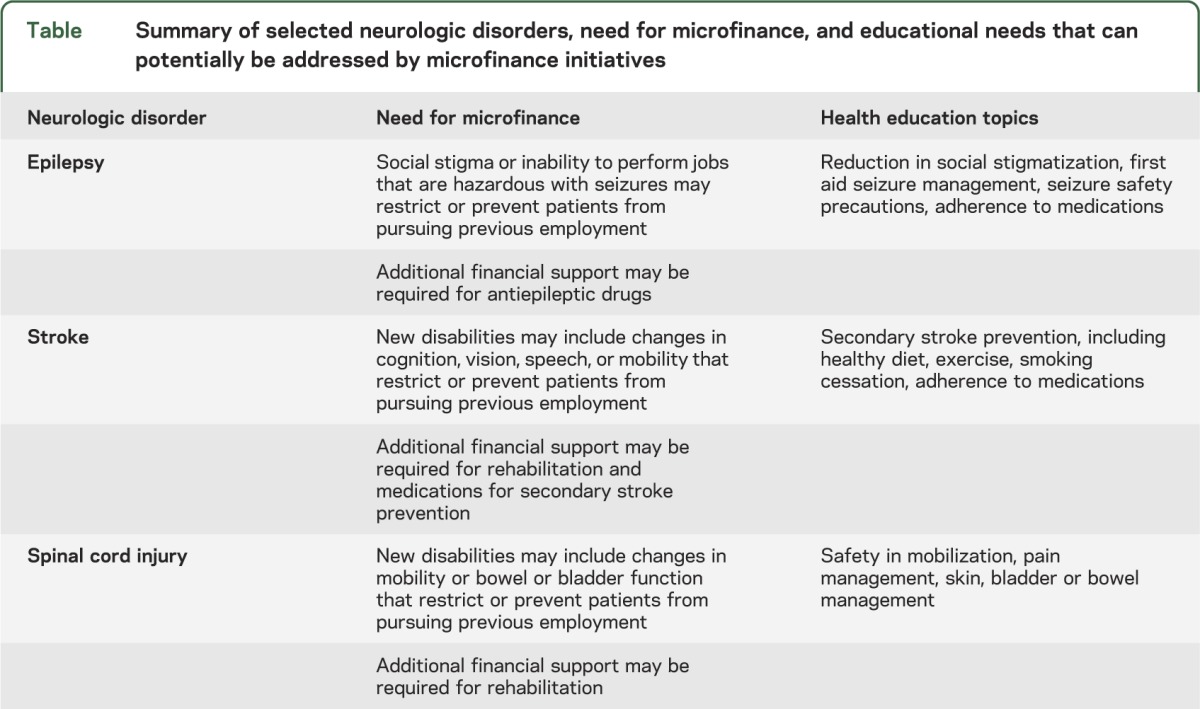

Application of microfinance to neurologic diseases—which often result in long-term disabilities—must take into account the unique challenges associated with long-term disabilities. A study commissioned by Handicap International in 2005 highlighted good practices for funding self-employment of people with disabilities, focusing on the role of microfinance.8 Many people with disabilities did not have access to microfinance, though microfinance could have been helpful; reasons for lack of access to microfinance included stigmatization by MFI staff, self-exclusion, and lack of training for entrepreneurship.8 Overcoming these barriers may require MFIs to be closely linked to established programs for people with disabilities, and provide concurrent vocational and business training.8 As MFIs have the potential to impact health knowledge and behaviors,3 addition of a health education component to microfinance initiatives may be strongly considered to fully take advantage of MFIs. The table summarizes several examples of application of microfinance initiatives to neurologic disorders. While this list is not exclusive, the diseases that are listed seem particularly amenable to MFI support: people with sudden disabilities from stroke and traumatic neurologic injuries can benefit from MFI financial support, while people with epilepsy can overcome stigmatization by accessing the workforce through entrepreneurial means.

Table.

Summary of selected neurologic disorders, need for microfinance, and educational needs that can potentially be addressed by microfinance initiatives

EXISTING DATA ON MICROFINANCE AND NEUROLOGIC DISORDERS

One study currently exists on the application of microfinance to neurologic disorders. A new microfinance initiative in Bangladesh was recently started offering a credit program in tandem with medical rehabilitation and skills retraining.9 This microfinance program is linked to the Center for the Rehabilitation of the Paralysed (CRP) in Savar, Bangladesh, which serves patients with new-onset spinal cord injury, most of whom are young men who had an occupational injury and are permanently paralyzed without the option to return to physically laborious work.9 They often lack formal advanced schooling and, prior to injury, were the main source of income for their families.9 In a survey of 50 individuals at the CRP who were in their final stages of hospital rehabilitation, more than 85% of participants wished to receive interest-free loans as a form of financial aid, including a 2-phased approach with initial funds to offset the costs of rehabilitation and subsequent funds to give them the opportunity to reintegrate economically in their communities.9 Most patients required additional funding support despite receiving financial support at CRP; begging was still required to raise funds in some cases.9 A longer follow-up time, however, will be necessary to assess the ultimate impact of this initiative.

LIMITATIONS OF MICROFINANCE

An open question remains whether provision of microfinance is the optimal way to reduce poverty. Microfinance initiatives seem to have noneconomic benefits such as empowering women, but microenterprises may not be effective for many clients, as few individuals are expected to possess the ability to be successful entrepreneurs.10 Creating employment opportunities within the context of increased labor productivity and public services may be more effective strategies for reducing poverty.10 While resolving this fundamental question about microfinance is beyond the scope of this report, strong support systems—including both vocational training and health education—likely need to be in place for microfinance to succeed in individuals with serious neurologic disorders.

FUTURE DIRECTIONS

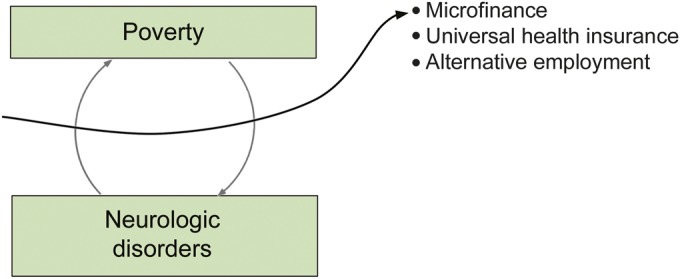

We hypothesize that microfinance has the potential to bring people out of the perpetual cycle of poverty and neurologic disorders (figure): in this cycle, those in poverty are more likely to develop neurologic disorders or neurologic disorders with more serious morbidity (for example, a low-paying, unsafe job that increases risk of traumatic brain or spinal cord injury), and those with neurologic disorders are more likely to become poor (for example, a new long-term disability that reduces employment opportunities). Other interventions that may be helpful in breaking this cycle include the provision of universal health insurance, a major goal promoted by WHO in the coming years, or development of alternative employment opportunities suited to those with disabilities. While we have suggested ways in which microfinance can be applied to various neurologic disorders, it will be important to conduct needs assessments to determine the most amenable neurologic disorders to microfinance, and to identify priorities for financial and educational support in specific neurologic disorders. A key to ensuring the success of microfinance is to select appropriate candidates to receive microfinance loans, so future studies can investigate which recipients may benefit most from microfinance. The latter includes finding ways to reach those with the most need, as well as identifying those with the most potential to maximize microfinance opportunities. Ensuring sustainability of microfinance in neurologic disorders will require optimal collaboration among loan recipients, health care providers, nonprofit organizations, credit programs, donors, and investors.

Figure. Poverty, neurologic disorders, and microfinance.

In this model, we hypothesize that those in poverty are more likely to develop neurologic disorders or neurologic disorders with more serious sequelae, and those with neurologic disorders are more likely to become poor. Microfinance or other measures, such as health insurance or improved employment opportunities, have the potential to bring people out of this cycle.

AUTHOR CONTRIBUTIONS

Janice C. Wong: writing and review of manuscript, literature review. Farrah J. Mateen: writing and review of manuscript, literature review, project design.

STUDY FUNDING

No targeted funding reported.

DISCLOSURE

The authors report no disclosures relevant to the manuscript. Go to Neurology.org for full disclosures.

REFERENCES

- 1.Ofori-Adjei AB. Microfinance: an alternative means of healthcare financing for the poor. Ghana Med J 2007;41:193–194 [PMC free article] [PubMed] [Google Scholar]

- 2.Karnani A. Microfinance misses its mark. In: Stanford Social Innovation Review [serial online] 2007. Available at: www.ssireview.org/articles/entry/microfinance_misses_its_mark. Accessed February 25, 2014 [Google Scholar]

- 3.Leatherman S, Metcalfe M, Geissler K, Dunford C. Integrating microfinance and health strategies: examining the evidence to inform policy and practice. Health Policy Plan 2012;27:85–101 [DOI] [PubMed] [Google Scholar]

- 4.Newton CR, Garcia HH. Epilepsy in poor regions of the world. Lancet 2012;380:1193–1201 [DOI] [PubMed] [Google Scholar]

- 5.Norrving B, Kissela B. The global burden of stroke and need for a continuum of care. Neurology 2013;80:S5–S12 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Guinhouya KM, Tall A, Kombate D, et al. Cost of stroke in Lome (Togo) [in French]. Sante Epub 2010. Aug 4 [DOI] [PubMed] [Google Scholar]

- 7.Burns AS, O'Connell C. The challenge of spinal cord injury care in the developing world. J Spinal Cord Med 2012;35:3–8 [DOI] [PMC free article] [PubMed] [Google Scholar]

- 8.de Klerk T. Funding for self-employment of people with disabilities. Grants, loans, revolving funds or linkage with microfinance programmes. Lepr Rev 2008;79:92–109 [PubMed] [Google Scholar]

- 9.Nahar N, Nuri M, Mahmud I. Financial Aid for the Rehabilitation of Individuals with Spinal Cord Injuries in Bangladesh. Disability, CBR & Inclusive Development [serial online]. 2012;23 Available at: http://dcidj.org/article/view/97. Accessed February 25, 2014 [Google Scholar]

- 10.Karnani AG. Employment, Not Microcredit, is the Solution. Ross School of Business Paper No 1065 [serial online]. 2007. Available at: http://ssrn.com/abstract=962941 or http://dx.doi.org/10.2139/ssrn.962941. Accessed February 25, 2014 [Google Scholar]