Abstract

The collapse of the labor, housing, and stock markets beginning in 2007 created unprecedented challenges for American families. This study examines disparities in wealth holdings leading up to the Great Recession and during the first years of the recovery. All socioeconomic groups experienced declines in wealth following the recession, with higher wealth families experiencing larger absolute declines. In percentage terms, however, the declines were greater for less-advantaged groups as measured by minority status, education, and pre-recession income and wealth, leading to a substantial rise in wealth inequality in just a few years. Despite large changes in wealth, longitudinal analyses demonstrate little change in mobility in the ranking of particular families in the wealth distribution. Between 2007 and 2011, one fourth of American families lost at least 75 percent of their wealth, and more than half of all families lost at least 25 percent of their wealth. Multivariate longitudinal analyses document that these large relative losses were disproportionally concentrated among lower income, less educated, and minority households.

Introduction

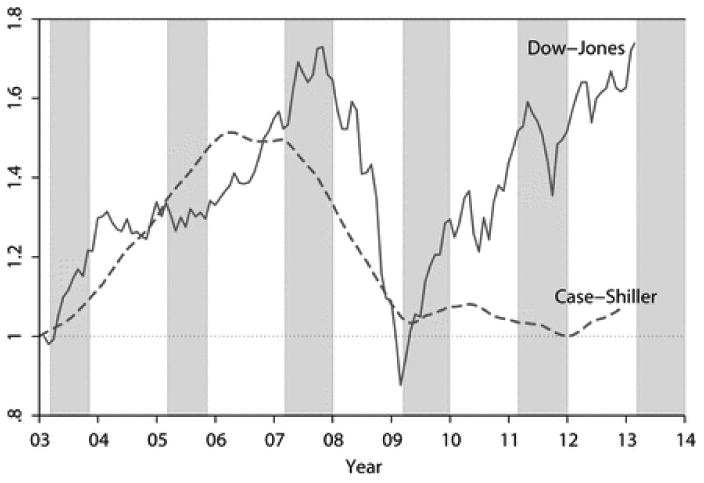

The Great Recession caused an unprecedented decline in wealth holdings among American households. Between 2007 and 2009, average housing prices in the largest metropolitan areas fell by nearly a third as measured by the Case-Shiller Index. Stock prices also collapsed, with the Dow Jones Index losing nearly half of its value between mid-2007 and early 2009 (see Figure A. 1 in Appendix A). These developments were exacerbated by a rapid rise in the unemployment rate from 5 percent in December 2007 to 10 percent in October 2009 and a large reduction in labor market earnings due to increased unemployment, wage cuts, and furloughs.

The enormity of wealth disparities and their growth prior to the Great Recession is well documented (Wolff 1995; 2006; Keister 2000; Klevmarken et al. 2003). As demonstrated below, in 2003 households at the 90th percentile of the net worth distribution held 73 times the net worth of households at the 25th percentile. Similarly, households in the highest income quintile had median wealth that was 45 times the median of households in the lowest income quintile. And whites had median wealth that was over six times that of nonwhites. These disparities dwarf disparities in individual earnings and household incomes (Keister and Moller 2000; Oliver and Shapiro 1997; Scholz and Levine 2004).

This study assesses the extent to which the Great Recession altered the distribution of wealth through 2011. We begin by using repeated cross-sectional data from two widely-used surveys, the Panel Study of Income Dynamics (PSID) and the Survey of Consumer Finances (SCF), to document changes in wealth inequality. Motivated by hypotheses that the Great Recession affected some groups more than others, we further examine whether pre-existing disparities in wealth across socioeconomic groups were exacerbated. We then make use of the longitudinal nature of the PSID data and examine wealth changes for individual households over time. We determine whether the ranking of households based on their wealth after the recession was similar to the ranking prior to the recession, i.e., whether –despite the dramatic declines in wealth due to the Great Recession –the households that were at the top (bottom) of the wealth distribution before the crash remained at the top (bottom) through 2011. Lastly, we estimate the magnitude of wealth losses – and gains – for individual households and identify the households characteristics that were associated with wealth losses to learn what types of household were able to weather the recession more and less effectively.

Background

Long-terms trends in the distribution of wealth

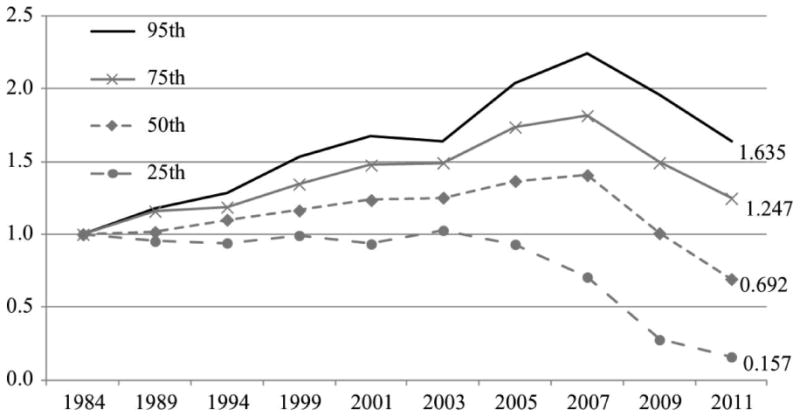

Previous studies have documented trends in the distribution of wealth for the United States from its founding years (Shammas 1993) and have shown that wealth inequality increased throughout the 18th and 19th century, with the most pronounced increases occurring during the industrialization period of the 19th century. The concentration of wealth at the very top, i.e. the share owned by the wealthiest one percent, rose sharply over this period, peaking immediately before the Great Depression of 1929 and falling rapidly in its aftermath (Ohlsson et al. 1997). A gradual decrease in wealth inequality ensued up to the late 1970s (Wolff 1995). Wealth inequality began to increase again in the 1980s: between 1983 and 1989, the share of wealth held by the wealthiest one percent grew from 33.8 percent to 37.4 percent, the net worth of the bottom 40 percent decreased, and the Gini coefficient rose from .799 to .832 (Wolff 2006). The growth of wealth inequality slowed in the 1990s and remained relatively stable during the 2000s leading up to the Great Recession (Wolff 2010 Kennickell 2009). In Figure 1, we index the inflation-adjusted value of net worth at 1.0 in 1984 for households at four points in the distribution. Since this year, the PSID has collected detailed wealth information on a regular basis. Wealth inequality increased between 1984 and 2001, with the net worth at the 95th percentile increasing by about two thirds and that at the 25th percentile declining slightly. The most pronounced increase in inequality occurred between 2001 and 2007, prior to the Great Recession (Gouskova and Stafford 2009). For example, in 2007, net worth at the 95th percentile was more than double that of 1984, whereas net worth at the 25th percentile declined to 70 percent of its 1984 level. We return to a more detailed discussion of recent trends below.

Figure 1. Total net worth relative to 1984, PSID.

The incidence of households with zero or negative net worth has increased since the 1980s (with the exception of a brief and moderate decline in the early 2000s). For example, 15.5 percent had zero or negative net worth in 1983 compared to 18.6 percent in 2007. The amount of debt held by households as a share of their income also rose dramatically in the years leading up to the recession – from 68.4 percent in 1983 to 81.1 percent in 2001 to 118.7 percent in 2007 (Wolff 2010; Main and Sufi 2011). That is, by 2007 households held on average 19 percent more debt than their annual income.

Racial inequalities in wealth holdings are substantial. Oliver and Shapiro (1997) estimate, based on data from the 1988 Survey of Income and Program Participation (SIPP), that the median net worth of African American families was a mere 8 percent that of the median net worth of white families. The racial net worth gap remained around 10 cents on the dollar in the 1990s and 2000s (Wolff 2006; Scholz and Levine 2004).

Early evidence on the effects of the Great Recession on the distribution of wealth

Bricker et al. (2012), using the 2007 and 2010 waves of the cross-sectional SCF, find that the largest relative declines in net worth were for people below the 75th percentile of the wealth distribution. Median wealth declined for all income groups except the top decile. Mean wealth declined more for minorities than whites, while the change in median wealth was similar for the two groups.

Emmons and Noeth (2012), also using the 2007 and 2010 SCF, demonstrate that the percentage losses in wealth were larger for younger families, families headed by young and middle-aged African-Americans and Hispanics, and families headed by people with less education. Analyzing data from a variety of sources through, for the most part, 2009, Wolff et al. (2011) find that almost all groups experienced substantial wealth losses, but the losses were particularly large for young families, minorities, and middle-class households.

Using SCF longitudinal data from 2007 to 2009, Kennickell (2011) finds that the largest relative declines in net worth were for people below the 30th percentile of the wealth distribution and most pronounced for those in the bottom 10 percent who were particularly likely to fall into net debt (Kennickell 2012). Bucks and Moore (2012), using the same panel data, find that two thirds of families had wealth losses, and the median loss among losers was around $60,000. They also found that wealth inequality increased between 2007 and 2009.

Using the 2007 – 2009 longitudinal data from the PSID, Bosworth (2012) finds that the median change in wealth was negative for all three income terciles (based on 2007 income) and education groups, was roughly the same across education groups (although the decline was slightly higher for the high school educated), and was smaller for families in the bottom third of the income distribution in 2007 (-8 .6 percent) than families in the top third (-15.1 percent). Shapiro et al. (2013) show that losses of net worth for African-Americans were greater than for whites between 2007 and 2009.

Based on SIPP data, the Census Bureau reports an increase in median net worth of 30 percent between 2000 and 2005 followed by a sharp decline. By 2011, median net worth was 16 percent below that of 2000 (Gottschalck et al. 2013). Taylor et al. (2011), also using SIPP data, show that between 2004 and 2009, the white-to-black ratio of median net worth increased from 11 to 19 and the white-to-Hispanic ratio from 7 to 15.

Group differences in wealth losses during the Great Recession

One goal of this study is to document changes in wealth disparities across socioeconomic groups. While, for the most part, we do not seek to explain why these changes have occurred, they are likely to have resulted from and changes housing and stock prices, recession-related changes in employment, and savings behaviors. Less-educated, minority, and low-wage workers typically experience greater increases in unemployment and reductions in work hours and earnings during recessions than more advantaged workers (Hoynes, Miller, and Schiller, 2012). As a result, they are less likely to maintain their pre-recession levels of pension contributions and additions to savings and are also more likely to draw down assets to maintain consumption.

This latter effect on wealth holdings may have been exacerbated by the fact that asset prices had declined significantly prior to the rapid increase in unemployment in 2008 and 2009. And the least-advantaged families were less likely to have benefited from the post-2009 recovery in stock prices because they had already withdrawn a substantial share of their market holdings (Bridges and Stafford 2012) and because they had relatively small savings prior to the Great Recession.

Although stock prices rose after 2009, national housing prices remained stagnant through at least the end of 2011. Home equity is the largest component of wealth for many families, and this is particularly true for less-educated, low-income, and minority families (Keister 2000). Families that purchased a home shortly before the collapse of the housing market, who are disproportionately younger families, had lower levels of home equity and therefore were most vulnerable to having an “underwater mortgage,” defined as having negative home equity (Stafford et al. 2012, Owens and Wimer 2013). Also, those living in areas where unemployment was extremely high were more likely to have experienced greater declines in home equity, as there was wide variation in the distribution of housing price declines.

Data

Few nationally representative surveys include detailed assessments of wealth holdings. The Survey of Consumer Finances (SCF) contains the most in-depth information on households' financial assets, real assets, and liabilities. Since 1983, The SCF has typically been administered as a cross-sectional survey on a triennial basis. However, respondents from two survey years have also been re-interviewed in later years. The first SCF panel occurred in the 1980s, the second was a 2009 re-interview of 2007 respondents and thus nicely timed for a longitudinal assessment of wealth losses during the Great Recession. Since 1989, the SCF has oversampled wealthy households through a list sample developed from Internal Revenue Service (IRS) tax records, which captures some of the very large amounts of wealth held by the wealthiest households..

Since 1968, the Panel Study of Income Dynamics (PSID) has collected a broad range of socio-economic and other information on families on an annual basis and since 1997 on a bi-annual basis. The PSID first introduced an extensive wealth module in 1984, which was repeated every five years until 1999 and on a bi-annual basis since then. The last pre-recession wealth measure from the PSID was collected in 2007; survey waves 2009 and 2011 provide information on wealth holdings after the Great Recession. While the PSID wealth module also covers all major wealth components – namely, housing wealth, a range of financial and real assets, retirement wealth, and various types of liabilities – it draws on fewer survey items than does the SCF (for details on the PSID measures, see table A.2 in Appendix A). Nevertheless, total wealth estimates produced from the PSID are comparable to those from the SCF. The primary exception is for the wealthiest 1 to 3 percent of households, which the SCF reaches through its IRS oversample and the PSID does not (Juster et al. 1999; Pfeffer et al., 2013).

The PSID has several advantages for analyzing wealth losses following the Great Recession. First, because of its panel nature, it identifies wealth changes for individual households that cannot be analyzed with cross-sectional data. Unlike the SCF 2007-2009 panel, it can track wealth changes and income changes across a much longer panel.

Second, the PSID includes many socio-economic attributes of households that are measured several years before the recession. Thus, we analyze wealth changes for households classified by their pre-recession permanent income (averaged across the 2003-2007 pre-recession surveys) instead of by single-year incomeii. Permanent income measures have less measurement error than single-year income measures (Solon 1992). Third, the early-release PSID data for 2011 are now available, whereas the SCF data beyond 2010 are not.

Our analyses are weighted to provide nationally representative estimates. The longitudinal analyses are based on a balanced sample of households that responded in each of the 2007, 2009, and 2011 surveys. We restrict the sample to households with the same head in 2007 and 2009 to reduce the impact of changes in the composition of households. The 2011 wealth data are drawn from an early release fileiii. As we show below, we find prolonged and persistent effects of the Great Recession that extend beyond the period covered by the SCF panel.

Net worth in the PSID and SCF are defined as the total sum of housing wealth, financial wealth, real assets, retirement wealth, minus any liabilities (such as mortgages and other debts). All absolute values are reported in constant 2011 dollars.

Results

Repeated cross-sectional analyses

Absolute changes in wealth

Table 1 reports the net worth distribution as estimated using the PSID in the top panel (for longer-term trends see Table B.1 in Appendix B) and the SCF in the bottom panel. For the PSID, we also report net worth excluding home equity and other real estate to demonstrate the importance of changes in the housing market both before and after the recession.

Table 1. Net Worth Distribution, 2003–2011.

| PSID | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

| |||||||||||||

| 2003 | 2005 | 2007 | 2009 | 2011 | Absolute Change | ||||||||

|

| |||||||||||||

| '03-'07 | '07–'11 | '03–'11 | |||||||||||

| Net worth | |||||||||||||

| Mean | 325,627 | 363,709 | 409,024 | 397,032 | 233,575 | 83,397 | −175,449 | −92,052 | |||||

| 5th percentile | −9,413 | −10,136 | −13,019 | −26,737 | −38,800 | −3,606 | −25,781 | −29,387 | |||||

| 25th | 9,780 | 8,869 | 6,726 | 2,630 | 1,500 | −3,054 | −5,226 | −8,280 | |||||

| 50th | 84,964 | 92,721 | 95,471 | 68,365 | 47,000 | 10,507 | −48,471 | −37,964 | |||||

| 75th | 291,821 | 339,781 | 355,305 | 292,007 | 244,000 | 63,484 | −111,305 | −47,821 | |||||

| 95th | 1,151,595 | 1,427,080 | 1,573,105 | 1,371,438 | 1,147,000 | 421,510 | −426,105 | −4,595 | |||||

| Net worth excluding home equity & real estate | |||||||||||||

| Mean | 191,429 | 198,904 | 225,896 | 195,091 | 134,297 | 34,467 | −91,599 | −57,132 | |||||

| 5th percentile | −16,993 | −18,429 | −21,698 | −27,156 | −32,400 | −4,705 | −10,702 | −15,407 | |||||

| 25th | 2,262 | 1,728 | 1,085 | 577 | 25 | −1,177 | −1,060 | −2,237 | |||||

| 50th | 24,450 | 23,036 | 22,240 | 18,873 | 14,000 | −2,210 | −8,240 | −10,450 | |||||

| 75th | 122,250 | 126,698 | 134,528 | 115,335 | 95,000 | 12,278 | −39,528 | −27,250 | |||||

| 95th | 715,163 | 830,448 | 935,604 | 828,315 | 795,500 | 220,441 | −140,104 | 80,338 | |||||

| Observations | 7,822 | 8,002 | 8,289 | 8,690 | 8,187 | ||||||||

| SCF | ||||||||

|---|---|---|---|---|---|---|---|---|

|

| ||||||||

| 2004 | 2007 | 2010 | Absolute Change | |||||

|

| ||||||||

| '04−'07 | '07−'10 | '04−'10 | ||||||

| Net worth | ||||||||

| Mean | 533,133 | 594,324 | 509,763 | 61,191 | −84,561 | −23,370 | ||

| 5th percentile | −3,249 | −4,922 | −15,862 | −1,673 | −10,940 | −12,613 | ||

| 25th | 15,708 | 15,087 | 8,570 | −621 | −6,517 | −7,138 | ||

| 50th | 110,671 | 128,860 | 79,310 | 18,189 | −49,550 | −31,361 | ||

| 75th | 328,830 | 398,361 | 309,309 | 69,531 | −89,052 | −19,521 | ||

| 95th | 1,701,105 | 2,022,300 | 1,919,714 | 321,195 | −102,586 | 218,609 | ||

| Observations | 4,519 | 4,418 | 6,482 | |||||

According to the PSID data, prior to the Great Recession, median wealth increased from $84,964 in 2003 to $92,721 in 2005, and then to $95,471 in 2007. While the absolute increase at the 50th percentile (median) over these four years was about $10,000, increases for wealthier households were substantially greater. Net worth at the 75th percentile increased by over $63,000 to $355,305 in 2007, while net worth at the 95th rose by over $421,000 to $1,573,105 in 2007. At the same time, net worth at the bottom of the distribution declined by $3,000 at the 25th percentile and was negative and falling at the 5th percentile.

In contrast to the 2003-2007 period, net worth declined throughout the distribution between 2007 and 2011. The 95th percentile experienced a decline of more than $426,000 to $1,147,000 while the median fell by about $48,000 to $47,000. The drop at the 5th percentile of nearly $26,000 was especially notable given the fact that net worth at the 5th percentile in 2007 was $13,019. In addition, the declines between 2007 and 2009 and between 2009 and 2011 are remarkably linear. In terms of wealth losses, the Great Recession did not end in mid-2009, the official end date of the recession based on growth in gross domestic product (GDP) as declared by the National Bureau of Economic Research.

At the 95th percentile, the drop in net worth following the Great Recession was nearly identical to the increase experienced in the four years leading up to it, so that net worth was roughly the same in 2011 as in 2003 – about $1.15 million. However, there were larger declines in net worth at other points in the distribution between 2007 and 2011, so all other points shown in Table 1 have lower net worth in 2011 than in 2003. For example, net worth at the median was about $38,000 lower in 2011 than in 2003 ($47,000 vs. $84,964). These trends also apply to mean net worth, which rose by more than $83,000 between 2003 and 2007, and then declined by more than $175,000 between 2007 and 2011, reflecting the broad destruction of private wealth.

The SCF estimates of net worth in any year, shown at the bottom of Table 1, are higher than those in the PSID, most likely due to the fact that the SCF includes the IRS oversample of high wealth households and because the SCF asks many more questions about assets and liabilities than does the PSID (Juster et al. 1999; Pfeffer et al., 2012). Despite the differences in level, however, the patterns of changes in net worth across the distribution are similar in both data sets. At the 95th percentile, the decrease in wealth was very small, about $26,000, between 2007 and 2010, and net worth was higher in 2010 than in 2004 ($1.92 vs. $1.70 million). In contrast, median household wealth declined by $50,000 between 2007 and 2010, and was lower in 2010 than in 2004 ($79,310 vs. $110,671).

In the bottom part of the PSID panel in Table 1, we show the trend in the measure of net worth that excludes home equity and other real estate. These data highlight the significance of the collapse of the housing market on household wealth portfolios. At the median, non-real estate wealth declined by only about $8,000 between 2007 and 2011, compared to a decline in total net worth of over $48,000. However, median net worth excluding real estate was only $14,000 in 2011, compared to $47,000 when real estate is included.

By 2011, the stock market had rebounded from its Great Recession low. More affluent households are more likely to hold stocks and have large portfolios, which presumably allowed them to benefit from the gains in the stock market. As a result, net worth not held in real estate actually increased by more than $80,000 at the 95th percentile between 2003 and 2011 (from $715,163 to $795,500). The same was not the case at the 75th percentile, the median, or at the bottom of the distribution. That is, even excluding real estate, net worth at the median fell at most points of the distribution except the very top between 2003 and 2011. Also, note that net worth excluding real estate already fell before the recession for the bottom half of the distribution. This is different from the trend in net worth including real estate and implies that pre-recession increases in median net worth were entirely driven by increasing home prices. That is, excluding the wealth gains associated with the “housing bubble”, the net worth of the average American family had declined between 2003 and the onset of the recession at the end of 2007.

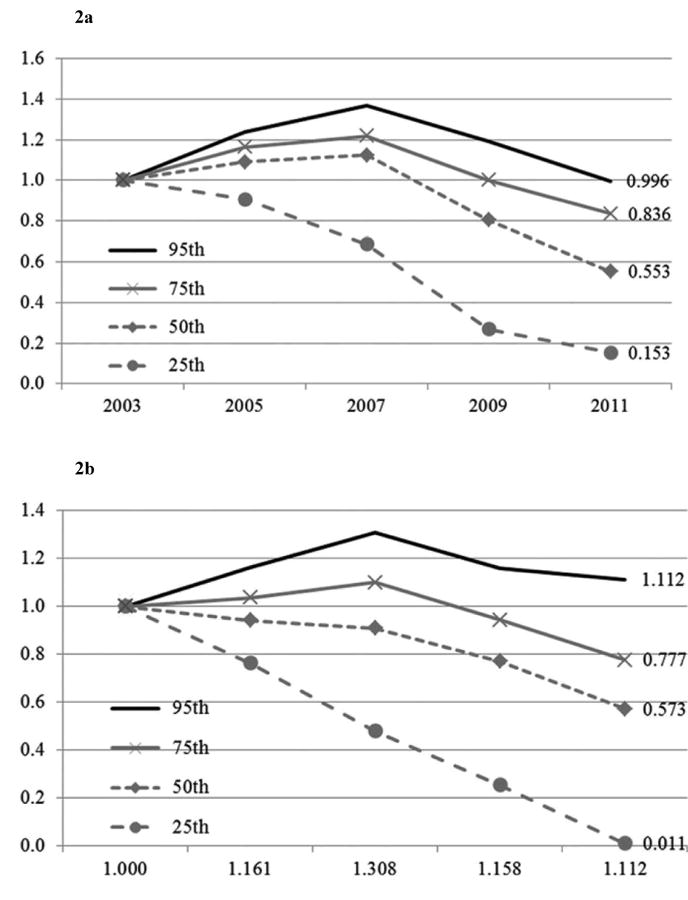

Relative changes in wealth

In Figure 2a for total net worth and Figure 2b for net worth excluding real estate, we report values for PSID households at the 25th, 50th, 75th, and 95th percentile that are all indexed at 1.0 in 2003. Thus, any value on the y-axis above 1.0 represents a percentage increase in wealth over time, and any value below 1.0 represents a percentage decrease.

Figure 2.

a. Total net worth relative to 2003, PSID

b. Net worth excluding real estate relative to 2003, PSID

The figures demonstrate that, in relative terms, declines in net worth were most pronounced at the bottom of the distribution. While households at the 95th percentile of net worth were worth roughly the same in 2011 and 2003 (0.996 in Figure 2a), households at the median in 2011 had only 55 percent of the 2003 median net worth and those at the 25th percentile had only 15.3 percent of those at the 25th percentile in 2003. Moreover, the relative decline in net worth was smaller at higher percentiles than at lower percentiles.

Focusing on non-housing wealth (Figure 2b), the net worth of households at the 95th percentile was 11.2 percent higher in 2011 than in 2003. But below the 75th percentile, there were sharp declines in non-housing net worth. The 75th percentile in 2011 was at just three quarters of its 2003 level. Median household wealth in 2011 was only 57.3 percent of the 2003 level and net worth at the 25th percentile decreased by 99 percent. That is, in 2011, the bottom 25 percent of all households had zero or negative net worth.

Wealth inequality

The Gini coefficient and various percentile ratios from the PSID and SCF data document substantial increases in the dispersion of wealth both before and after the Great Recession (Table 2, for longer-term trends see Table B.2 in Appendix B). Based on PSID data (top row), the Gini coefficient – a measure of inequality across the entire distribution – rose from 0.81 in 2003 to 0.83 in 2007 and to 0.89 in 2009. It remained high at .88 in 2011, a 10 percent total increase between 2003 and 2011. The SCF Gini shows an increase by 5 percent from .809 in 2004 to .846 in 2010.

Table 2. Indicators of Inequality in Net Worth, 2003-2011.

| Indicator of inequality | PSID | SCF | |||||||

|---|---|---|---|---|---|---|---|---|---|

|

|

|

||||||||

| 2003 | 2005 | 2007 | 2009 | 2011 | 2011/2003 | 2004 | 2007 | 2010 | |

| Gini coefficient | 0.814 | 0.815 | 0.832 | 0.890 | 0.879 | 1.1 | 0.809 | 0.816 | 0.846 |

| Percentile ratios | |||||||||

| 50/25 | 8.7 | 10.5 | 14.2 | 26.0 | 31.3 | 3.6 | 7.0 | 8.5 | 9.3 |

| 75/25 | 29.8 | 38.3 | 52.8 | 111.0 | 162.7 | 5.5 | 24.9 | 26.4 | 36.1 |

| 90/25 | 72.8 | 94.4 | 134.1 | 301.0 | 481.3 | 6.6 | 63.0 | 64.4 | 114.4 |

| 95/25 | 117.8 | 160.9 | 233.9 | 521.5 | 764.7 | 6.5 | 108.3 | 134.0 | 224.0 |

| 75/50 | 3.4 | 3.7 | 3.7 | 4.3 | 5.2 | 1.5 | 3.5 | 3.1 | 3.9 |

| 90/50 | 8.4 | 9.0 | 9.4 | 11.6 | 15.4 | 1.8 | 8.9 | 7.5 | 12.4 |

| 95/50 | 13.6 | 15.4 | 16.5 | 20.1 | 24.4 | 1.8 | 15.4 | 15.7 | 24.2 |

| 90/75 | 2.4 | 2.5 | 2.5 | 2.7 | 3.0 | 1.2 | 2.5 | 2.4 | 3.2 |

| 95/75 | 3.9 | 4.2 | 4.4 | 4.7 | 4.7 | 1.2 | 4.3 | 5.1 | 6.2 |

| 95/90 | 1.6 | 1.7 | 1.7 | 1.7 | 1.6 | 1.0 | 1.7 | 2.1 | 2.0 |

Ratios of net worth at various percentiles also demonstrate rising inequality, providing an easily interpreted metric of the magnitude of the change. For example, using the PSID, households at the 50th percentile relative had 8.7 times the net worth of those at the 25th percentile in 2003, but 31.3 times that by 2011. In other words, the 50/25 ratio increased almost fourfold (i.e., 31.3/8.7). The 95/25 ratio was 117.8 in 2003 and increased more than six-fold to 764.7 by 2011.

The SCF percentile ratios show increases in all rows of the table, but the rate of change is somewhat smaller, especially for comparisons at the 25th percentile. For example, the 95/25 ratio roughly doubled from 108.3 to 224.0 between 2004 and 2010, not six-fold as in the PSID data. The 95/50 change is similar in both data sets – an increase from 13.6 to 24.4 in the PSID over eight years, and an increase from 15.4 to 24.2 over six years in the SCF.

Changes in wealth disparities

Disadvantaged groups, whether in terms of socioeconomic status, income, education, marital status or race, have much lower net worth than advantaged groups. The magnitude of these disparities in median net worth is shown in column one of table three for the 2003 PSID data. We display disparities by income quintile, educational attainment, race, age categories, marital status, and whether children are present in the household.

Our focus is on changes in these disparities leading up to (2003-2007) and following (2007-2011) the Great Recession. In almost every instance, the more advantaged group has much higher net worth and experienced a larger absolute decline (or increase, depending on the time period) than the disadvantaged group. For example, households in the bottom income quintile experienced a decline between 2003 and 2011 of $5,824, while the top quintile experienced a decline of $67,447. The pattern of absolute losses is not surprising given the tremendous differences in the level of wealth holdings in 2003: $7,824 for the bottom quintile and $354,647 for the top quintile.

What is perhaps unexpected is the fact that the relative wealth losses over the eight years were far greater for the less-advantaged than for the more-advantaged groups in almost every case. For example, median wealth of the households in the bottom income quintile fell in 2011 to 26 percent of the 2003 level, while median wealth held by the top income quintile fell to just 81 percent of its 2003 level. Similarly, while median wealth fell by 2011 to 69 percent of the 2003 level for non-Hispanic whites and Asians, it fell to 27 percent for nonwhites (African Americans, Hispanics, Native Americans and others). In 2003, the typical non-Hispanic white and Asian household had net worth that was 6.5 times as large as that as the median nonwhite household ($120,594/$18,338); by 2011 this ratio increased to 16.7 ($83,600/$5,000). For groups defined by income, education, and race/ethnicity, those with lower median wealth holdings in 2003 experienced larger relative declines through 2011.

Changes in wealth holdings: longitudinal analysis

Wealth Mobility

Given the tremendous swings in household net worth between 2003 and 2011, the relative position of particular households in the wealth distribution may have changed substantially. To investigate this issue, we use the longitudinal nature of the PSID to estimate wealth mobility between the pre-recession period (i.e., defined as average net worth in the 2005 and 2007 surveys) and the post-recession period (i.e., average of the 2009 and 2011 surveys). As shown in Table 4a, among households who were in the bottom wealth quintile before the Great Recession, 66.2 percent remained in the bottom quintile and an additional 28.3 percent moved up one quintile. Less than 6 percent moved more than one quintile up the distribution. Downward mobility from the top of the distribution was even less likely to occur, as 76.6 percent of households that were in the highest quintile before the recession were still there after the great recession. Also, only 6 percent of the top quintile households moved down more than one quintile.

Table 4A. Quintile-to-Quintile Wealth Mobility during the Great Recession, PSID.

| Net Worth 2005/2007 | Net Worth 2009/2011 | |||||

|---|---|---|---|---|---|---|

|

| ||||||

| 1st | 2nd | 3rd | 4th | 5th | Total | |

| 1st (lowest) quintile | 66.2 | 28.3 | 4.0 | 1.3 | 0.3 | 100 |

| 2nd | 22.7 | 49.0 | 24.0 | 3.8 | 0.6 | 100 |

| 3rd | 10.8 | 17.2 | 51.0 | 18.9 | 2.2 | 100 |

| 4th | 4.0 | 5.3 | 18.8 | 54.8 | 17.2 | 100 |

| 5th (highest) quintile | 1.2 | 2.1 | 2.7 | 17.4 | 76.6 | 100 |

NOTE: Based on balanced panel 2005–2011 for households headed by the same household head in 2005, 2007, and 2009.

Bricker et al. (2011) report similar rates of immobility between 2007 and 2009 using the SCF panel. Among households in the bottom quintile in 2007, 76 percent remained in the bottom quintile in 2009 and 97 percent were in one of the bottom two quintiles. Among families in the top quintile in 2007, 78 percent remained in the top quintile in 2009 and 95 percent were in the top two quintiles.

In sum, despite the significant impact of the Great Recession on the overall dispersion of wealth demonstrated above, the recession did not fundamentally alter the ordering of households along the wealth distribution. Another way to demonstrate this is to compare the PSID recession wealth mobility rates (Table 4a) to mobility rates before the Great Recession (Table 4b). They are strikingly similar across nearly all cells of these two mobility tables. The only type of mobility for which we can observe some change during the recession is the extent of downward mobility from the middle of the distribution: While close to 30 percent of households at the middle quintile showed downward mobility both before and during the recession, the share of households at the middle quintile that was demoted to the lowest quintile doubled (from 5.1 percent before the recession to 10.8 percent after the recession).

Table 4B. Quintile-to-Quintile Wealth Mobility before the Great Recession, PSID.

| Net Worth 2001/2003 | Net Worth 2005/2007 | |||||

|---|---|---|---|---|---|---|

|

| ||||||

| 1st | 2nd | 3rd | 4th | 5th | Total | |

| 1st (lowest) quintile | 71.7 | 20.8 | 6.3 | 0.8 | 0.3 | 100 |

| 2nd | 22.8 | 50.3 | 21.3 | 4.1 | 1.5 | 100 |

| 3rd | 5.1 | 26.1 | 46.4 | 20.0 | 2.4 | 100 |

| 4th | 1.1 | 4.7 | 21.4 | 55.0 | 17.9 | 100 |

| 5th (highest) quintile | 1.2 | 1.2 | 2.8 | 17.9 | 77.0 | 100 |

NOTE: Based on balanced panel 2001-2007 for households headed by the same household head in all years.

Disparities in changes in wealth

The longitudinal data allow us to examine changes in wealth for particular households. In Table 5, we report the share of households experiencing various amounts of absolute losses and gains and selected percentage changes from 2007 to 2011. The top row shows that 12.2 percent of households experienced a loss of $250,000 or more; the second row shows that 33.2 percent of households lost at least $50,000. Although net worth losses were the norm, some households had higher net worth in 2011 than in 2007. In fact, 5.3 percent of households experienced a gain of at least $250,000, and 16.9 percent experienced gains of at least $50,000. A total of 30 percent gained $10,000 or more.

Table 5. Distribution of Change in Net Worth, 2007 to 2011, PSID.

| % | Cumulative % | |

|---|---|---|

| Absolute change (N = 5,839) | ||

| Lost ≥ $250k | 12.2 | 12.2 |

| Lost $50k–$250k | 21.2 | 33.3 |

| Lost $10k–$50k | 14.0 | 47.3 |

| Lost less than $10k | 10.8 | 58.1 |

| No change | 1.8 | 59.8 |

| Gained <$10k | 10.1 | 70.0 |

| Gained $10k–$50k | 13.1 | 83.1 |

| Gained $50k–$250k | 11.6 | 94.7 |

| Gained ≥ $250k | 5.3 | 100.0 |

| Fell into debt (N = 5,839) | ||

| No | 90.9 | 90.9 |

| Yes | 9.1 | 100.0 |

| Percentage change (N = 4,676)a | ||

| Lost 75–100% | 25.1 | 25.1 |

| Lost 50–74% | 11.2 | 36.3 |

| Lost 25–49% | 15.1 | 51.4 |

| Lost <25% | 13.0 | 64.4 |

| Gained <25% | 9.2 | 73.6 |

| Gained 25–99% | 11.7 | 85.3 |

| Gained ≥ 100% | 14.7 | 100.0 |

| Median loss | ||

| Among all with net worth in 2007 = $16,367 | ||

| Among those having lost net worth = $70,348 | ||

Among those holding positive net worth in 2007.

The second panel shows that 9.1 percent of households fell into debt – that is, they had positive net worth in 2007, but negative net worth in 2011.

The third panel in Table 5 shows relative changes in net worth for households that had positive net worth in 2007. A quarter of them lost at least 75 percent of their wealth and 36.3 percent lost at least 50 percent. On the other hand, more than a quarter of families experienced a gain of at least 25 percent. Taking all households who had positive net worth in 2007, the median change by 2011 was a loss of $16,367. And among those who did lose net worth, the median loss was $70,348.

Socioeconomic disparities in wealth changes

We estimate multivariate regressions to assess the marginal effects of various socioeconomic factors on changes in net worth from 2007 to 2011. The independent variables include proxies for permanent net worth quintiles and permanent net income quintiles computed as the average of a household's values for the pre-recession years of 2003, 2005 and 2007, head's educational attainment, race/ethnicity, age, marital status and presence of children in the householdiv. The results are shown in Table 6 for absolute losses for all households and in the first row of Table 7 for relative losses for those households with positive net worth in 2007.

Table 6. Logistic Regressions Predicting Absolute Losses of Net Worth, 2007-2011, PSID.

| Any Loss | Loss of ≥10k | Loss of ≥50k | Loss of ≥250k | Fell in debt | |

|---|---|---|---|---|---|

| Net worth 03-07, Q1 | ref. | ref. | ref. | ref. | |

| Net worth 03-07, Q2 | 1.878°°° (0.213) | 3.434°°° (0.451) | 3.576°°° (0.761) | 1.362+ (0.218) | |

| Net worth 03-07, Q3 | 2.981°°° (0.362) | 7.141°°° (0.979) | 13.357°°° (2.779) | 58.253°°° (60.026) | 1.160 (0.207) |

| Net worth 03-07, Q4 | 3.900°°° (0.525) | 11.242°°° (1.670) | 29.919°°° (6.454) | 395.032°°° (406.133) | 0.661 + (0.158) |

| Net worth 03-07, Q5 | 6.392°°° (0.976) | 18.250°°° (3.065) | 58.569°°° (13.589) | 2004.070°°° (2067.020) | 0.313°°° (0.107) |

| HH income 03-07, Q1 | ref. | ref. | ref. | ref. | ref. |

| HH income 03-07, Q2 | 1.165 (0.145) | 1.050 (0.141) | 1.129 (0.190) | 0.674 (0.230) | 1.061 (0.196) |

| HH income 03-07, Q3 | 1.039 (0.136) | 1.231 (0.176) | 1.268 (0.223) | 0.804 (0.255) | 1.173 (0.240) |

| HH income 03 07, Q4 | 0.952 (0.140) | 1.106 (0.172) | 1.259 (0.237) | 0.967 (0.307) | 1.124 (0.252) |

| HH income 03-07, Q5 | 0.610°° (0.100) | 0.693° (0.119) | 0.905 (0.180) | 0.947 (0.316) | 0.967 (0.267) |

| Head's education: <HS | ref. | ref. | ref. | ref. | ref. |

| Head's education: HS | 0.888 (0.115) | 1.092 (0.144) | 0.980 (0.149) | 0.967 (0.301) | 1.003 (0.198) |

| Head's education: Some college | 0.935 (0.122) | 1.247+ (0.167) | 1.157 (0.179) | 1.066 (0.335) | 1.101 (0.218) |

| Head's education: BA | 0.638°° (0.094) | 0.812 (0.125) | 0.758 (0.134) | 0.786 (0.258) | 0.910 (0.215) |

| Head's education: >BA | 0.716+ (0.135) | 0.990 (0.194) | 0.840 (0.177) | 0.803 (0.282) | 0.805 (0.286) |

| Head's race: White/Asian | 0.703°°° (0.061) | 0.699°°° (0.063) | 0.564°°° (0.060) | 0.260°°° (0.050) | 0.625°°° (0.085) |

| Head's age: <35 | ref. | ref. | ref. | ref. | ref. |

| Head's age: 35-54 | 1.286°° (0.110) | 1.360°°° (0.126) | 1.684°°° (0.192) | 1.864°° (0.426) | 0.745° (0.094) |

| Head's age: 55-64 | 1.213 (0.145) | 1.359° (0.167) | 1.765°°° (0.250) | 1.598+ (0.392) | 0.445°°° (0.093) |

| Head's age: 65- | 1.458°° (0.206) | 1.823°°° (0.266) | 2.278°°° (0.375) | 2.111°° (0.565) | 0.279°°° (0.097) |

| Married | ref. | ref. | ref. | ref. | ref. |

| Unmarried Male Head | 0.925 (0.094) | 0.814+ (0.086) | 0.896 (0.110) | 0.788 (0.159) | 0.675° (0.115) |

| Unmarried Female Head | 0.910 (0.091) | 0.854 (0.090) | 0.794+ (0.096) | 0.571° (0.125) | 0.904 (0.140) |

| Children in HH | 1.209° (0.097) | 1.414°°° (0.120) | 1.429°°° (0.140) | 1.021 (0.163) | 1.001 (0.124) |

| Constant | 0.706° (0.123) | 0.140°°° (0.027) | 0.031°°° (0.008) | 0.001°°° (0.001) | 0.234°°° (0.063) |

|

| |||||

| N | 5,839 | 5,839 | 5,839 | 5,839 | 5,839 |

| Pseudo-R2 | 0.060 | 0.146 | 0.235 | 0.360 | 0.070 |

p<.10,

p<.05,

p<.01,

p<.001; s.e. in parentheses.

Table 7. OLS Regression Predicting Relative Losses of Net Worth, 2007-2011, PSID.

| % Lost | % Lost | |

|---|---|---|

| Net worth 03-07, Q1 | ref. | ref. |

| Net worth 03-07, Q2 | −1.121 (2.128) | −1.083 (2.124) |

| Net worth 03-07, Q3 | 1.500 (2.186) | 1.686 (2.182) |

| Net worth 03-07, Q4 | −0.530 (2.312) | −0.139 (2.310) |

| Net worth 03-07, Q5 | 1.894 −2.547 | 2.120 −2.543 |

| HH income 03-07, Q1 | ref. | ref. |

| HH income 03-07, Q2 | −4.258° (1.979) | −4.302° (1.975) |

| HH income 03-07, Q3 | −3.749+ (2.112) | −3.593+ (2.110) |

| HH income 03-07, Q4 | −3.855+ (2.280) | −3.539 (2.277) |

| HH income 03-07, Q5 | −7.797°° (2.560) | −7.219°° (2.559) |

| Head's education: <HS | ref. | ref. |

| Head's education: HS | −3.010 (2.057) | −3.228 (2.053) |

| Head's education: Some college | −2.039 (2.119) | −2.284 (2.115) |

| Head's education: BA | −10.721°°° (2.340) | −10.920°°° (2.336) |

| Head's education: >BA | −9.358°° (2.920) | −9.692°°° (2.917) |

| Head's race: White/Asian | −13.751°°° (1.442) | −13.349°°° (1.442) |

| Head's age: <35 | ref. | ref. |

| Head's age: 35-54 | −1.065 (1.588) | −1.177 (1.586) |

| Head's age: 55-64 | −4.015° (2.003) | −3.768+ (2.000) |

| Head's age: 65- | −2.414 (2.194) | −1.757 (2.195) |

| Married | ref. | ref. |

| Unmarried Male Head | 3.080+ (1.650) | 3.219+ (1.647) |

| Unmarried Female Head | 2.589+ (1.545) | 3.062° (1.546) |

| Children in HH | 2.922° (1.429) | 2.968° (1.427) |

| Unemployment: None | ref. | |

| Unemployment: 1-26 weeks | 9.421°°° (2.383) | |

| Unemployment: 27 or more weeks | 7.361° (3.160) | |

| Constant | 56.805°°° (3.098) | 55.202°°° (3.114) |

|

| ||

| N | 4,676 | 4,676 |

| R2 | 0.052 | 0.056 |

p<.10,

p<.05,

p<.01,

p<.001; s.e. in parentheses.

It is not surprising that households who had higher net worth prior to the Great Recession experienced greater absolute losses. For example, those in the top net worth quintile were 6.39 times more likely to have experienced any loss and 58.57 times more likely to have lost more than $50,000. These highest net worth households were, however, only one-third as likely to have fallen into debt (last column in Table 6) as the lowest net worth quintile.

Holding pre-recession net worth quintiles constant, there are few significant coefficients for the pre-recession income quintiles. The highest income quintile was about 39 percent less likely to have experienced any loss than the lowest income quintile (holding initial wealth quintile constant) and 31 percent less likely to have lost more than $10,000.

Everything else equal, whites and Asians were much less likely to have lost significant wealth than African Americans, Hispanics, Native Americans and others: 30 percent less likely to have lost any wealth, 37.5 percent less likely to have fallen into debt, and 74 percent less likely to have lost at least $250,000. Households with heads who have a BA degree were 36 percent less likely to have lost any wealth compared to those without a high school degree. In general, the older the household head, the more likely – and higher – the absolute losses. However, the likelihood of falling into debt is highest for households with heads under the age of 25. Married couples were more likely to fall into debt than households with unmarried male heads. Households with children were more likely to lose wealth.

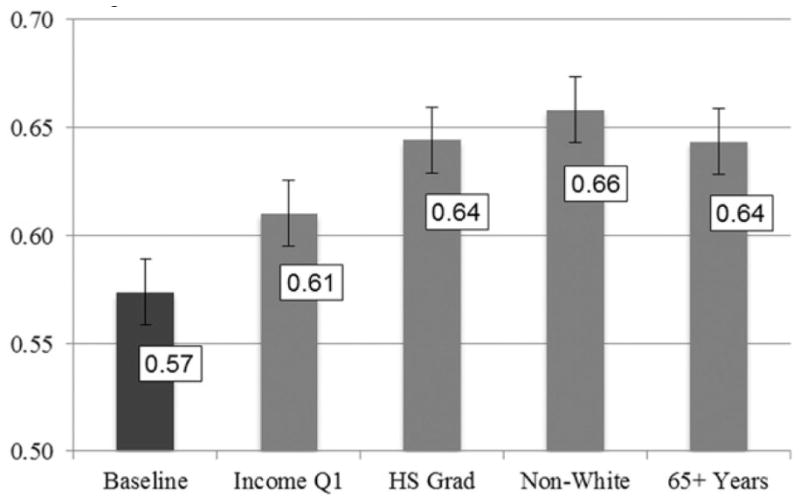

These conditional associations are illustrated graphically by generating, based on the regression coefficients reported in Table 6, predicted probabilities of losing more than $10,000 for several hypothetical households. In Figure 3, we report the predicted probability of losing at least $10,000 for households in the third pre-recession permanent income and third pre-recession permanent wealth quintiles, who have children, and whose head is married, white or Asian, has a college degree, and is between the ages of 35 and 54 years old. For this baseline household, we predict the probability for a loss of at least $10,000 is 57 percent. If instead the household was in the bottom pre-recession income quintile – and the other observed characteristics were the same – this probability would be 61 percent. If the household head was a high school graduate and not a college graduate, the likelihood of loss would be 64 percent. The large differences by race/ethnicity are demonstrated by the fact that the rate would be 66 percent instead of 57 percent if the household head were nonwhite – all else equal.

Figure 3. Predicted probabilities of losing $10,000 or more in net worth, 2007-11, PSID.

Based on regression model shown in Table 6

Note: Baseline predicted probability is for a household in the third pre-recession permanent income and third pre-recession permanent wealth quintiles, with children, and whose household head is married, white or Asian, has a college degree, and is between the ages of 35 and 54 years old, 95 percent CI shown

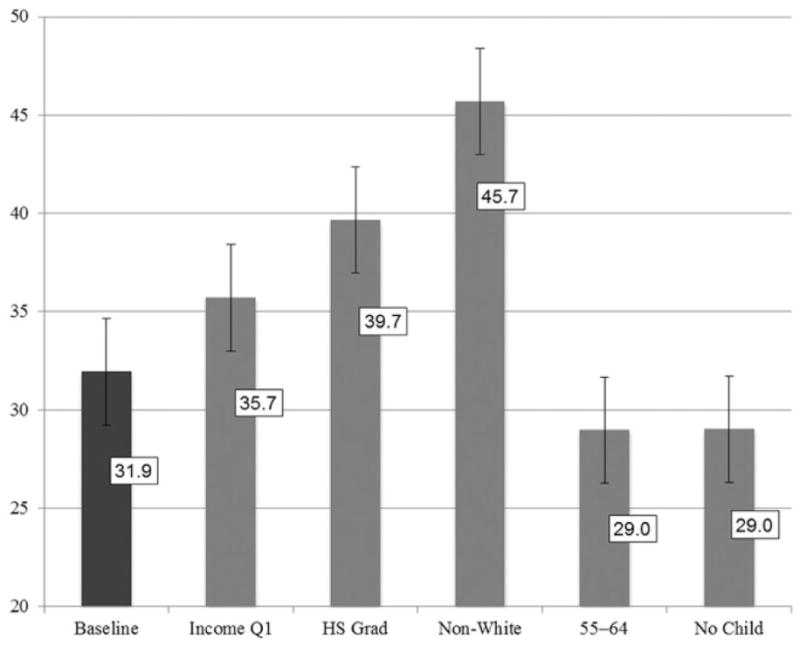

The first row of Table 7 reports the coefficients from a regression model in which the dependent variable is the percentage loss in net worth between 2007 and 2011v. Thus, the sample is restricted to families who had positive net worth in 2007. The mean percentage loss for the sample was 38.2 percent. Households whose mean net income in 2003, 2005 and 2007 placed them in the top quintile lost considerably less than those in the bottom income quintile. Households with highly educated heads (those with the BA or more than a BA) compared to high school dropouts experienced wealth losses that were roughly ten percentage points lower. Households with a white or Asian head lost, all else equal, 13.8 percentage points less than those with a non-white head. Households nearing retirement (55-64) lost four percentage points less than households headed by someone under 35 years old. And households with children lost three percentage points more than those without.

These conditional associations are illustrated with predicted probabilities in Figure 4. Again, the racial differences in wealth losses stand out: The same baseline household described above lost 31.9 percent of its wealth while the same household with a non-white head lost 45.7 percent of its wealth.

Figure 4. Predicted percentage loss of net worth between 2007 and 2011, PSID.

Based on regression model shown in Table 7, first column

Note: Baseline predicted probability is for a household in the third pre-recession permanent income and third pre-recession permanent wealth quintiles, with children, and whose household head is married, white or Asian, has a college degree, and is between the ages of 35 and 54 years old; 95 percent CI shown

Evidence on the impact of unemployment

So far, we have documented the extent, the distribution, and the factors associated with wealth losses after the Great Recession. Because of the extensive effects of the Great Recession on the labor market (Freeman, this issue), we now turn to the potential contribution of unemployment to these wealth losses. If households use their assets to smooth consumption in reaction to income losses, as economic theory suggests, we should observe higher wealth losses for those experiencing unemployment. This is indeed the case, as seen in the second column of Table 7. Households that experienced unemployment in 2008 (by either the household head or partner) lost 7.36 - 9.42 percent more wealth than those who experienced no unemployment, all else equal. However, including differential unemployment experiences in the regression does not significantly change the size of the coefficients on the other variables in the model.

With the PSID data that are currently available, we do not have information on unemployment experiences after 2008. As Freeman shows (this issue), unemployment rates have recovered very slowly since then, with many households experiencing prolonged periods of unemployment. Extended unemployment might in fact explain a larger part of the documented continued decline in net worth through 2011.

Discussion

In terms of household wealth, we could detect very few signs of recovery from the losses associated with the Great Recession. Declines in net worth from 2007 to 2009 were large, and the declines continued through 2011. These wealth losses, however, were not distributed equally. While large absolute amounts of wealth were destroyed at the top of the wealth distribution, households at the bottom of the wealth distribution lost the largest share of their wealth. As a result, wealth inequality increased significantly–the PSID Gini coefficient of household net worth increased by about 10 percent between 2007 and 2011 and the 95/25 ratio increased over six-fold between 2003 and 2011.

Wealth changes following the Great Recession also differed greatly across socio-economic groups and were patterned similar to changes in income and unemployment documented elsewhere (Hout et al. 2011; Smeeding et al. 2011; Freeman this volume). That is, the most disadvantaged groups (non-whites, young adults, the less-educated) experienced the greatest relative wealth losses and were the most likely to have fallen into debt. In addition, we found a particularly strong racial/ethnic bias in losses even when comparing households with otherwise equal socio-economic characteristics.

The American economy has experienced rising income and wealth inequality for several decades and there is little evidence that these trends are likely to reverse in the near term. It is possible that the very slow recovery from the Great Recession will continue to generate increased wealth inequality in the coming years as those hardest hit may still be drawing down assets to cover current consumption.

Table 3. Absolute and Relative Changes in Net Worth by Socioeconomic Status, 2003-2011, PSID.

| Median in 2003 | Change in Median | Relative to Median in 2003 | ||||||

|---|---|---|---|---|---|---|---|---|

|

|

|

|||||||

| '03–'07 | '07–'11 | '03–'11 | 2005 | 2007 | 2009 | 2011 | ||

| Household income quintile | ||||||||

| 1st (bottom) | 7,824 | −4,027 | −1,797 | −5,824 | 0.59 | 0.49 | 0.27 | 0.26 |

| 2nd | 35,942 | −7,734 | −15,707 | −23,442 | 0.95 | 0.78 | 0.60 | 0.35 |

| 3rd | 70,295 | 11,073 | −34,368 | −23,295 | 1.16 | 1.16 | 0.82 | 0.67 |

| 4th | 122,250 | 25,296 | −63,846 | −38,550 | 1.14 | 1.21 | 0.84 | 0.68 |

| 5th | 354,647 | 147,661 | −215,109 | −67,447 | 1.19 | 1.42 | 0.98 | 0.81 |

| Education | ||||||||

| <High school | 22,127 | −6,179 | −11,748 | −17,927 | 0.86 | 0.72 | 0.57 | 0.19 |

| High school | 70,905 | −2,014 | −41,891 | −43,905 | 0.96 | 0.97 | 0.70 | 0.38 |

| Some college | 71,150 | 15,643 | −55,192 | −39,550 | 1.15 | 1.22 | 0.60 | 0.44 |

| BA | 174,818 | 24,804 | −77,122 | −52,318 | 1.17 | 1.14 | 0.86 | 0.70 |

| >BA | 360,638 | 106,412 | −221,549 | −115,138 | 1.23 | 1.30 | 0.81 | 0.68 |

| Race | ||||||||

| Nonwhite | 18,338 | −979 | −12,358 | −13,338 | 1.17 | 0.95 | 0.51 | 0.27 |

| White and Asian | 120,594 | 13,392 | −50,385 | −36,994 | 1.10 | 1.11 | 0.88 | 0.69 |

| Age | ||||||||

| <35 | 10,391 | −2,797 | −2,094 | −4,891 | 0.78 | 0.73 | 0.50 | 0.53 |

| 35–54 | 83,375 | 16,220 | −60,295 | −44,075 | 1.13 | 1.19 | 0.69 | 0.47 |

| 55–64 | 205,991 | 10,989 | −72,380 | −61,391 | 1.12 | 1.05 | 0.81 | 0.70 |

| ≥65 | 221,028 | 36,093 | −64,121 | −28,028 | 1.03 | 1.16 | 1.09 | 0.87 |

| Marital status | ||||||||

| Married | 166,505 | 48,306 | −78,810 | −30,505 | 1.18 | 1.29 | 0.98 | 0.82 |

| Single male | 26,284 | −5,996 | −9,988 | −15,984 | 0.84 | 0.77 | 0.48 | 0.39 |

| Single female | 32,519 | −5,396 | −16,023 | −21,419 | 0.90 | 0.83 | 0.61 | 0.34 |

| Have children in household | ||||||||

| No | 103,301 | 849 | −45,150 | −44,301 | 1.07 | 1.01 | 0.80 | 0.57 |

| Yes | 56,846 | 20,432 | −48,279 | −27,846 | 1.25 | 1.36 | 0.74 | 0.51 |

Appendix A: Information on data sources

Both the Survey of Consumer Finances (SCF) and the Panel Study of Income Dynamics (PSID) collect wealth data through survey questions on the holdings and values of separate asset components. For a description of wealth measurement in the SCF, we refer the reader the Kennickell (2000). For the PSID, Table A.1 documents the survey questions on assets. Figure A.1 shows the PSID field periods (in grey) and their convenient timing compared to the macro-economic shocks of the Great Recession.

Table A. 1. Asset Measures in the PSID.

| Survey Item | Survey Questions |

|---|---|

| Home value | Do you (or anyone else in your family living here) own the (home/apartment), pay rent, or what? Could you toll mo what the present value of your (house/apartment) is—I mean about how much would it bring if you sold it today? |

| Mortgage (since 1994 up to two mortgages) | Do you have a mortgage or loan on this property? About bow much is the remaining principal on this mortgage? |

| Checking and savings | Do you [or anyone in your family living here] have any money in checking or savings accounts, money market funds, certificates of deposit, government savings bonds, or treasury bills, not including assets held in employer-based pensions or IRAs? If you added up all such accounts [for all of your family living here], about how much would they amount to right now? |

| Stocks, mutual funds, investment trusts | Do you [or anyone in your family living here] have any shares of stock in publicly held corporations, mutual funds, or investment trusts, not including stocks in employer-based pensions or IRAs? If you sold all that and paid off anything you owed on it, how much would you have? |

| Other financial assets | Do you [or anyone in your family living here] have any other savings or assets, such as bond funds, cash value in a life insurance policy, a valuable collection for investment purposes, or rights in a trust or estate that you haven't already told us about? If you sold that and paid off any debts on it, how much would you have? |

| Farm or business | Do you [ or anyone in your family living here] own part or all of a farm or business? If you sold all that and paid off any debts on it, how much would you realize on it? |

| Real estate | Do you (or your family living here) have any real estate other than your main home, such as a second home, land, rental real estate, or money owed to you on a land contract? If you sold all that and paid off any debts on it, how much would you realize on it? |

| Vehicles | What is the value of what you [or anyone in your family living here] own on wheels? Including personal vehicles you may have already told me about and any cars, trucks, a motor home, a trailer, or a boat—what are they worth all together, minus anything you still owe on them? |

| Annuities, IRAs | Do you [or anyone in your family living here] have any money in private annuities or Individual Retirement Accounts (IRAs)? How much would they be worth? |

| Credit card debt, student loans, other debt | Aside from the debts that we have already talked about, like any mortgage on your main home or vehicle loans—do you [or anyone in your family living here] currently have any other debts such as credit card charges, student loans, medical or legal bills, or loans from relatives? If you added up all these debts [for all of your family living here], about how much would they amount to right now? |

Figure A.1. Timing of PSID data collection & macro-economic trends.

Case–Shiller Index based on 20 largest metropolitan areas Shaded areas represent PSID field periods

Appendix B: Long-term trends based on the PSID

Long-term trends based on the PSID

Table B1. Net Worth Distributions, PSID 1984–2011.

| PSID | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

|

| ||||||||||

| 1984 | 1989 | 1994 | 1999 | 2001 | 2003 | 2005 | 2007 | 2009 | 2011 | |

| Net worth | ||||||||||

| Mean | 213,702 | 233,547 | 236,132 | 304,021 | 312,200 | 325,627 | 363,709 | 409,024 | 397,032 | 233,575 |

| 5th percentile | −1,299 | −3,628 | −7,437 | −9,397 | −8,827 | −9,413 | −10,136 | −13,019 | −26,737 | −38,800 |

| 10th | 0 | 0 | 0 | 0 | 0 | 0 | −346 | −1,302 | −6,606 | −11,000 |

| 25th | 9,526 | 9,070 | 8,955 | 9,451 | 8,891 | 9,780 | 8,869 | 6,726 | 2,630 | 1,500 |

| 50th | 67,873 | 68,932 | 74,676 | 78,987 | 83,827 | 84,964 | 92,721 | 95,471 | 68,365 | 47,000 |

| 75th | 195,716 | 226,750 | 232,223 | 263,289 | 288,694 | 291,821 | 339,781 | 355,305 | 292,007 | 244,000 |

| 90th | 434,299 | 516,083 | 539,578 | 641,345 | 676,963 | 711,495 | 837,359 | 902,094 | 791,618 | 722,000 |

| 95th | 701,460 | 825,370 | 898,538 | 1,076,109 | 1,174,843 | 1,151,595 | 1,427,080 | 1,573,105 | 1,371,438 | 1,147,000 |

| Net worth excluding home equity & real estate | ||||||||||

| Mean | 121,450 | 117,127 | 129,129 | 196,624 | 190,074 | 191,429 | 198,904 | 225,896 | 195,091 | 134,297 |

| 5th percentile | −3,031 | −6,349 | −10,017 | −12,017 | −13,971 | −16,993 | −18,429 | −21,698 | −27,156 | −32,400 |

| 10th | 0 | −736 | −1,404 | −2,565 | -3,810 | −4,279 | -5,759 | −7,594 | −9,751 | −12,700 |

| 25th | 3,248 | 2,721 | 2,163 | 2,970 | 2,540 | 2,262 | 1,728 | 1,085 | 577 | 25 |

| 50th | 18,403 | 21,768 | 24,133 | 25,654 | 25,440 | 24,450 | 23,036 | 22,240 | 18,873 | 14,000 |

| 75th | 69,930 | 81,630 | 100,934 | 122,868 | 136,536 | 122,250 | 126,698 | 134,528 | 115,335 | 95,000 |

| 90th | 212,495 | 247,611 | 315,702 | 377,313 | 413,037 | 391,200 | 428,470 | 509,578 | 433,031 | 410,000 |

| 95th | 376,710 | 468,012 | 549,595 | 716,956 | 749,359 | 715,163 | 830,448 | 935,604 | 828,315 | 795,500 |

| Observations | 6,918 | 7,114 | 8,658 | 6,997 | 7,406 | 7,822 | 8,002 | 8,289 | 8,690 | 8,187 |

Table B2. Indicators of Inequality in Net Worth, PSID 1984-2011.

| Indicator of Inequality | PSID | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

|

| |||||||||||

| 1984 | 1989 | 1994 | 1999 | 2001 | 2003 | 2005 | 2007 | 2009 | 2011 | 2011/1984 | |

| Gini coefficient | 0.807 | 0.798 | 0.796 | 0.818 | 0.813 | 0.814 | 0.815 | 0.832 | 0.890 | 0.879 | 1.1 |

| Percentile ratios | |||||||||||

| 50/25 | 7.1 | 7.6 | 8.3 | 8.4 | 9.4 | 8.7 | 10.5 | 14.2 | 26.0 | 31.3 | 4.4 |

| 75/25 | 20.5 | 25.0 | 25.9 | 27.9 | 32.5 | 29.8 | 38.3 | 52.8 | 111.0 | 162.7 | 7.9 |

| 90/25 | 45.6 | 56.9 | 60.3 | 67.9 | 76.1 | 72.8 | 94.4 | 134.1 | 301.0 | 481.3 | 10.6 |

| 95/25 | 73.6 | 91.0 | 100.3 | 113.9 | 132.1 | 117.8 | 160.9 | 233.9 | 521.5 | 764.7 | 10.4 |

| 75/50 | 2.9 | 3.3 | 3.1 | 3.3 | 3.4 | 3.4 | 3.7 | 3.7 | 4.3 | 5.2 | 1.8 |

| 90/50 | 6.4 | 7.5 | 7.2 | 8.1 | 8.1 | 8.4 | 9.0 | 9.4 | 11.6 | 15.4 | 2.4 |

| 95/50 | 10.3 | 12.0 | 12.0 | 13.6 | 14.0 | 13.6 | 15.4 | 16.5 | 20.1 | 24.4 | 2.4 |

| 90/75 | 2.2 | 2.3 | 2.3 | 2.4 | 2.3 | 2.4 | 2.5 | 2.5 | 2.7 | 3.0 | 1.3 |

| 95/75 | 3.6 | 3.6 | 3.9 | 4.1 | 4.1 | 3.9 | 4.2 | 4.4 | 4.7 | 4.7 | 1.3 |

| 95/90 | 1.6 | 1.6 | 1.7 | 1.7 | 1.7 | 1.6 | 1.7 | 1.7 | 1.7 | 1.6 | 1.0 |

Footnotes

This research was supported by a grant from the Russell Sage Foundation. Fabian Pfeffer is a Faculty Research Fellow at the Survey Research Center of the Institute for Social Research, University of Michigan. Sheldon Danziger is H.J. Meyer Distinguished University Professor of Public Policy and Director of the National Poverty Center at the Gerald R. Ford School of Public Policy, University of Michigan. Robert Schoeni is Research Professor at the Institute for Social Research and Professor of Economics and Public Policy, University of Michigan. Please direct all correspondence to Fabian T. Pfeffer, fpfeffer@umich.edu, Institute for Social Research, University of Michigan, 4 26 Thompson Street, Ann Arbor, MI 48106.

While wealth is reported as of the interview date, the PSID income measure refers to the year prior to the survey (that is, 2002 that is, 2004, and 2006).

The preliminary 2011 data do not allow us to impose the same restriction to households with an unchanged household head and contain un-imputed missing values. Also, we use the 2009 weights as 2011 weights, which are not yet available. Final data for 2011 will be released in summer 2013.

We have conducted a range of sensitivity tests with different specifications of the pre-recession wealth predictor, such as logged net worth and net debt and the inverse hyperbolic sine transformation. These do not alter the substantive conclusions presented here. These sensitivity checks were motivated by the possibility that a relatively crude measure of baseline wealth, such as the quintile dummy indicators used here, may bias the effects of various indicators of disadvantaged status downwards (e.g. the racial gap). There is some indication that our estimates of the racial effects are conservative based on sensitivity checks that include interactions between baseline wealth and race (results available from the authors).

Regression models that predict net worth gains between 2007 and 2011 generally mirror those presented here and are available from the authors upon request.

References

- Bosworth Barry. Economic Consequences of the Great Recession. Evidence from the Panel Study of Income Dynamics. Center for Retirement Research at Boston College Working Paper (2012-4) 2012 [Google Scholar]

- Bricker Jesse, Bucks Brian, Kennickell Arthur, Mach Traci, Moore Kevin. Surveying the Aftermath of the Storm. Changes in Family Finances from 2007 to 2009. Finance and Economics Discussion Series, Federal Reserve Board, Washington, D C (2011-17) 2011 [Google Scholar]

- Bridges Thomas, Stafford Frank. At the Corner of Main and Wall Street. Family Pension Response to Liquidity Change and Perceived Returns. Michigan Retirement Research Center Working Paper 2012 [Google Scholar]

- Bucks Brian, Moore Kevin. The Great Recessions' Varied Effects on Household Well-Being and Its Consequences for Inequality. Paper presented at the General Conference of The International Association for Research in Income and Wealth 2012 [Google Scholar]

- Emmons WilliamR, Noeth BryanJ. Household Financial Stability. Who Suffered the Most from the Crisis? The Regional Economist. 2012:11–17. [Google Scholar]

- Gouskova Elena, Stafford Frank. Trends in Household Wealth Dynamics , 2005-2007. PSID Technical Paper #09-03 2009 [Google Scholar]

- Gottschalck Alfred, Vornovytskyy Marina, Smith Adam. Household Wealth in the U.S.: 2000 to 2011. Press release by the Census Bureau. 2013 Mar; 2013. [Google Scholar]

- Hout Michael, Levanon Asaf, Cumberworth Erin. Job Loss and Unemployment. In: Grusky DavidB, Western Bruce, Wimer Christopher., editors. The Great Recession. New York: Russell Sage; 2011. pp. 59–126. [Google Scholar]

- Hoynes Hilary, Miller DouglasL, Shaller Jessamyn. Who suffers during recessions? Journal of Economic Perspectives. 2012;26:27–48. [Google Scholar]

- Juster FThomas, Smith JamesP, Stafford Frank. The measurement and structure of household wealth. Labour Economics. 1999;6(2):253–275. [Google Scholar]

- Keister LisaA. Wealth in America Trends in Wealth Inequality. Cambridge: Cambridge University Press; 2000. [Google Scholar]

- Keister LisaA, Moller Stephanie. Wealth Inequality in the United States. Annual Review of Sociology. 2000;26:63–81. [Google Scholar]

- Kennickell ArthurB. Wealth Measurement in the Survey of Consumer Finances?: Methodology and Directions for Future Research. Finance & Economic Discussion Paper, Federal Reserve Board Washington DC 2000 [Google Scholar]

- Kennickell ArthurB. Ponds and Streams. Wealth and Income in the U.S., 1989 to 2007. Finance & Economic Discussion Paper, Federal Reserve Board Washington DC 2009 [Google Scholar]

- Kennickell ArthurB. Tossed and Turned: Wealth Dynamics of U.S. Households 2007 – 2009. Finance & Economic Discussion Paper, Federal Reserve Board Washington DC 2011 [Google Scholar]

- Kennickell ArthurB. The Other, Other Half. Changes in the Finances of the Least Wealthy 50 Percent, 2007-2009. Finance & Economic Discussion Paper, Federal Reserve Board Washington DC 2012 [Google Scholar]

- Klevmarken NAnders, Lupton JosephP, Stafford FrankP. Wealth Dynamics in the 1980s and 1990s. The Journal of Human Resources. 2003;38(2):322–353. [Google Scholar]

- Mian Atif, Sufi Amir. House Prices, Home Equity-Based Borrowing, and the US Household Leverage Crisis. American Economic Review. 2011;101(5):2132–2156. [Google Scholar]

- Ohlsson Henry, Roine Jesper, Waldenström Daniel. Long-Run Changes in the Concentration of Wealth. An Overview of Recent Findings. In: Davies JamesB., editor. Personal Wealth from a Global Perspective. Oxford; Oxford University Press; 2008. pp. 42–63. [Google Scholar]

- Oliver MelvinL, Shapiro ThomasM. Black Wealth, White Wealth A New Perspective on Racial Inequality. New York: Routledge; 1997. [Google Scholar]

- Owens LindsayA, Wimer Christopher. The Dynamics of Mortgage Debt in the Wake of the Great Recession. In: Caputo Richard., editor. Debt Dynamics Original research on Challenges Facing Households and Families in an Age of Rising Inequality. Boulder: Lynne Reiner; 2013. [Google Scholar]

- Produced and distributed by the Institute for Social Research. Survey Research Center, University of Michigan; Ann Arbor, MI: 2003. Panel Study of Income Dynamics, public use dataset. [Google Scholar]

- Pfeffer FabianT, Schoeni RobertF, Andreski Patricia. A comparison of wealth estimates based on the 2007 Panel Study of Income Dynamics and the 2007 Survey of Consumer Finances. PSID Technical Paper 2013 [Google Scholar]

- Scholz KarlJohn, Levine Kara. U.S. Black-White Wealth Inequality. In: Neckerman KathrynM., editor. Social Inequality. New York: Russell Sage; 2004. pp. 895–929. [Google Scholar]

- Shammas Carole. A New Look at Long-Term Trends in Wealth Inequality in the United States. American Historical Review. 2012;98(2):412–431. [Google Scholar]

- Shapiro Thomas, Meschede Tatjana, Osoro Sam. The Roots of the Widening Racial Wealth Gap. Explaining the Black-White Economic Divide. Institute on Assets and Social Policy 2013 [Google Scholar]

- Smeeding TimothyM, Thompson JeffreyP, Levanon Asaf, Burak Esra. Income, Inequality, and Poverty over the Early Stages of the Great Recession. In: Grusky DavidB, Western Bruce, Wimer Christopher., editors. The Great Recession. New York: Russell Sage Foundation; 2011. [Google Scholar]

- Solon Gary. Intergenerational Income Mobility in the United States. American Economic Review. 1992;82(3):393–408. [Google Scholar]

- Stafford Frank, Chen Bing, Schoeni Robert. Mortgage Distress and Financial Liquidity. How U.S. Families are Handling Savings, Mortgages and Other Debts. PSID Technical Paper #12-02 2012 [Google Scholar]

- Wolff EdwardN. Top Heavy. A study of the increasing inequality of wealth in America. New York: Twentieth Century Fund Press; 1995. [Google Scholar]

- Wolff EdwardN. Changes in household wealth in the 1980s and 1990s in the United States. In: Wolff EdwardN., editor. International Perspectives on Household Wealth. Cheltenham: Edward Elgar; 2006. pp. 107–150. [Google Scholar]

- Wolff EdwardN. Recent Trends in Household Wealth in the United States: Rising Debt and the Middle-Class Squeeze. An Update to 2007. Levy Economics Institute Working Paper (589) 2010 [Google Scholar]

- Wolff EdwardN, Owens LindsayA, Burak Esra. How Much Wealth Was Destroyed in the Great Recession? In: Grusky DavidB, Western Bruce, Wimer Christopher., editors. The Great Recession. New York: Russell Sage Foundation; 2011. pp. 127–158. [Google Scholar]