Abstract

Objective

To measure spillover effects of Medicare inpatient hospital prices on the nonelderly (under age 65).

Primary Data Sources

Healthcare Cost and Utilization Project State Inpatient Databases (10 states, 1995–2009) and Medicare Hospital Cost Reports.

Study Design

Outcomes include nonelderly discharges, length of stay and case mix, staffed hospital bed-days, and the share of discharges and days provided to the elderly. We use metropolitan statistical areas as our markets. We use descriptive analyses comparing 1995 and 2009 and panel data fixed-effects regressions. We instrument for Medicare prices using accumulated changes in the Medicare payment formula.

Principal Findings

Medicare price reductions are strongly associated with reductions in nonelderly discharges and hospital capacity. A 10-percent reduction in the Medicare price is estimated to reduce discharges among the nonelderly by about 5 percent. Changes in the Medicare price are not associated with changes in the share of inpatient hospital care provided to the elderly versus nonelderly.

Conclusions

Medicare price reductions appear to broadly constrain hospital operations, with significant reductions in utilization among the nonelderly. The slow Medicare price growth under the Affordable Care Act may result in a spillover slowdown in hospital utilization and spending among the nonelderly.

Keywords: Medicare, hospitals, prices, access/demand/utilization of services, health economics, instrumental variables

Congress has on several occasions cut the prices paid to medical providers to rein in the growth in spending on Medicare, the federal health care program for the elderly and disabled. However, there is little consensus on the effects of such price cuts. Some argue that medical providers respond to price cuts by increasing volume or raising private prices (“cost shifting”), thereby negating Medicare savings and increasing private costs (House Budget Committee 2012, p. 48). Others argue that concerns about cost shifting are overblown, and that payment reforms that reduce spending in Medicare will result in spillover savings in the private sector (Cutler, Davis, and Stremikis 2010).

Medicare is by far the single most important payer in the hospital sector, accounting for about 30 percent of total revenues. It is reasonable to expect, therefore, that changes in Medicare prices will affect hospitals’ operations and overall financial condition. But the effects of Medicare price cuts on the utilization among the nonelderly could go in different directions. Hospitals might increase the volume of services they provide to the nonelderly to recoup lost revenues, or they might scale back overall operations and reduce services provided both to the elderly and nonelderly.

This article uses historical data from 1995 through 2009 to examine the effects of Medicare price cuts on inpatient hospital utilization among the nonelderly. Our study period includes the Balanced Budget Act of 1997 (BBA97), which made substantial cuts to Medicare prices for hospital care. The period following the BBA97 provides a preview, albeit imperfect, of the possible effects of the Medicare price cuts in the Affordable Care Act (ACA) of 2010.

The ACA permanently trims the rate of growth in the prices that Medicare pays to hospitals and most other medical providers. As a result, Medicare prices in 2021 will be about 11 percent lower than they would have been had the ACA not been enacted—this provision accounts for most of the $716 billion in Medicare cuts that garnered so much attention during the presidential campaign.

Previous Literature

Changes in payments for one group of patients can have various types of spillover effects on other patients, which are summarized by Chernew, Baicker, and Martin (2010). The existing literature suggests that it is reasonable to test for Medicare price cuts having a spillover effect on the volume of services among the nonelderly, but it is not clear whether the number of services provided to the nonelderly might increase or decrease. Demand inducement spillovers might increase the volume and intensity of services provided to the nonelderly. But capacity spillovers might reduce non-Medicare volume, and treatment style spillovers might reduce treatment intensity. The net effect of those competing forces is not yet known.

Demand Inducement Spillovers

A demand inducement spillover occurs when one payer reduces the prices it pays and providers respond by increasing the volume of services provided to other payers’ patients. McGuire and Pauly (1991) predict this type of volume spillover in the physician setting, from both an income effect—a negative income shock increases labor supply—and a substitution effect, and Yip (1998) provides empirical support for their model. Morrisey’s (1994) model of hospital behavior predicts that Medicare price cuts will lead hospitals to increase the volume of services provided to private patients, because private patients have now become relatively more profitable. He and Mellor (2012) extend McGuire and Pauly’s theory to the hospital outpatient surgery setting. They find that Medicare price cuts for ambulatory surgery were associated with substantial increases in the number of surgeries provided to patients covered by private fee-for-service insurance and smaller increases in services provided to Medicare beneficiaries, consistent with both an income effect and a substitution effect. Bazzoli et al. (2004/5) is the only study of which we are aware that attempts to test for demand inducement spillovers in the inpatient hospital setting. They examined the period following the Medicare cuts in the BBA97 and compared hospitals facing large Medicare price cuts with those facing small Medicare price cuts. Those facing large cuts appeared to increase Medicare volume and reduce non-Medicare volume. That finding does not fit with any of the theories of hospital behavior and may be a result of limitations in their study design.1

Capacity Spillovers

A capacity spillover occurs when payments for one group of patients become more or less generous, and, as a result, providers adjust their capacity and change the volume of services provided to all patients. Finkelstein (2007) examined the effects of the introduction of Medicare in the late 1960s and 1970s, and found that it clearly encouraged hospitals to increase employment, add beds, and adopt new technologies. And, because of that expanded capacity, Medicare appears to have increased spending on hospital care among both the elderly and nonelderly.

Treatment Pattern Spillovers

Providers appear to adopt a general treatment style that they apply to their patient populations, rather than tailoring treatments based on each patient’s coverage. Treatment style includes the intensity of treatment (e.g., the length of an inpatient stay, the number of procedures performed) and the choice of treatment modality (e.g., surgery versus medical management). This type of spillover has been shown in the inpatient hospital setting by Feder, Hadley, and Zuckerman (1987) and by Dafny (2005), and in the physician setting by Glied and Zivin (2002). By implication, if Medicare price cuts lead hospitals to provide less-intensive services to Medicare patients, we might expect a similar change in treatment patterns among non-Medicare patients.

Methodology and Data Sources

We create a panel dataset with the market year as the unit of observation (129 markets over 15 years, 1995–2009). We use metropolitan statistical areas (MSAs) as our market definition, and, because of data availability, we only include MSAs in 10 selected states. We also group all nonmetropolitan areas in each of our states into a market. For each market year, we measure the actual Medicare price for inpatient hospital care, the accumulated effects of changes in the Medicare payment formula, and the utilization of inpatient hospital services among the nonelderly. We then use descriptive analyses and fixed-effects regressions to assess the relationship between changes in the Medicare payment formula and changes in utilization among the nonelderly. To avoid a negative bias in our regression results, we use two-stage least squares (2SLS) in which we predict the actual Medicare price. (A detailed description of methods, data sources, and results is available in a Technical Appendix.)

The main advantage of our study over previous analyses is that we address a question that has not been taken on squarely before. Beyond that, other strengths of our approach are the use of market-level analysis (discussed below) and the length of the panel data series. The 15-year panel encompasses many significant changes in Medicare inpatient payment policy, and it allows for hospitals to fully adjust to those changes. Finally, we use administrative microdata on the universe of hospital discharges, which avoids sampling error in our outcome measures.

Data Sources

The Healthcare Cost and Utilization Project State Inpatient Databases (HCUP-SID) were used to measure hospital utilization. In states that participate in the HCUP-SID, all acute care hospitals are mandated to report discharge-level microdata for all patient stays. We create our instruments for the Medicare price using changes in the Medicare payment formula, which were identified from a combination of sources, including IPPS proposed and final rules published in the Federal Register, the Provider Specific File, the Impact File, and the Code of Federal Regulations. We created controls for market population and aging using U.S. Census Bureau data. The aging controls equal predicted utilization based on the age distribution in each market. Hospital bed-days only include staffed beds and are measured using the American Hospital Association survey of community hospitals, as reported in the Area Resource File (2009 data were not available). The Medicare Advantage enrollment share is also measured using the Area Resource File.

Why a Market-Level Analysis?

Other researchers have examined the impact of Medicare price changes on hospital volume using a hospital-level analysis (Bazzoli et al. 2004/5; Dafny 2005; He and Mellor 2012). The advantage of a hospital-level analysis is that you can measure fairly precisely the impact of a change in the Medicare payment formula and changes in volume. The limitations of a hospital-level analysis are as follows: (1) it cannot differentiate between shifts in volume among hospitals versus changes in total volume, and (2) it is difficult to identify and measure the effects of facility openings and closures. We chose a market-level analysis because we believed that it was important to measure changes in the total volume of inpatient hospital services provided, including the effects of openings and closures and netting out the effects of any shifts among facilities.

Once we settled on a market-level analysis, we had to choose how to define markets and whether to define markets based on hospital location versus patient residence. We chose MSAs as our market definition. Unlike counties, MSAs represent coherent economic units, albeit large ones. And, unlike hospital service areas or hospital referral regions, we could obtain detailed MSA-year level population data from the Census Bureau, which was important for creating our population and aging controls. We chose to define markets based on hospital location, rather than patient residence, so that Medicare prices and volume could be measured among clearly defined groups of nearby hospitals.

Why Two-Stage Least Squares?

In general, ordinary least squares (OLS) is preferable to 2SLS because it produces coefficient estimates that are more precisely estimated. But we found 2SLS to be preferable because (1) there is good reason to think that an OLS model would produce biased results, and (2) good instruments exist for predicting the Medicare price. OLS would be prone to bias in our case for several reasons. First, Medicare prices are adjusted for case mix using diagnosis-related groups (DRGs), which create a causal link between health status and Medicare prices. If residents of some markets are experiencing relative declines in health status, that could result in an increase in the Medicare price due to treatment of more severe cases, and also an increase in the volume of services. Second, errors in the measurement of volume could produce biased results because of the relationship between price and volume: price equals total revenue divided by volume. Suppose volume is measured with some error—if volume is overstated then price will be understated, and vice versa, creating a spurious negative relationship between price and volume.2 Third, suppose hospitals in some markets shift to providing fewer, but more intensive and higher priced hospital services. Such a shift could be a result, for example, of the closure of a small community hospital that feeds transfers to a tertiary care hospital. Such changes in practice patterns would also create a spurious negative relationship between price and volume. Fourth, errors in the measurement of Medicare revenues will produce mismeasured prices, which will bias OLS results toward zero. In terms of the availability of good instruments, the Medicare payment formula is very well documented, and its relationship with prices is clear and mechanical. Other researchers who have used similar instruments for Medicare prices include Shen (2003), Dafny (2005), and Wu (2010).

Outcomes of Interest

Our key outcomes are the number of hospital discharges and days provided to the nonelderly by hospitals located in each market, and the mean nonelderly length of stay. We also measure the share of discharges for the elderly and the share of days provided to the elderly—these shares capture any possible shifts in hospital output away from the elderly. In the regression analyses, we use the natural logarithms of each outcome as the dependent variable. The “log-log” specification allows the key estimated coefficients to be interpreted as elasticities.

We focus on the nonelderly population in 10 states: Arizona, California, Colorado, Florida, Iowa, Massachusetts, New Jersey, New York, Washington, and Wisconsin. These states were chosen because hospital utilization microdata were available for the period of our study and were reasonably priced, and because they are well populated and geographically diverse. The final analytical sample includes 116 MSAs, representing about one-third of the U.S. population (97 million residents in 2000, 84 million nonelderly). In our regression analyses, we exclude nonmetropolitan markets because of border crossing concerns—in many nonmetropolitan markets, hospitals located in those markets provide a relatively small share of the care received by residents of those markets. Also, a handful of metropolitan markets had no inpatient hospitals for some or all years and, therefore, had missing values and were dropped from the regression analyses.

Medicare price changes could affect nonelderly utilization in two ways: first, spillover effects from hospital-wide responses, or, second, a direct response to changes in Medicare payments for nonelderly patients. We interpret our results mainly as spillover effects, but it is important to note that Medicare does pay for some hospital care for the nonelderly. Less than 3 percent of the nonelderly population is enrolled in Medicare on the basis of disability or end-stage renal disease, but they account for a disproportionate share of inpatient hospital discharges among the nonelderly. Based on hospital discharge statistics from the National Center for Health Statistics, the share of nonelderly hospital discharges with Medicare as the principal expected source of payment has grown from 8 percent in 1995 to 13 percent in 2010.

Medicare Prices

Medicare is a national program, but the price that Medicare pays for inpatient hospital care varies from market to market and from hospital to hospital. Most acute care hospitals are paid by Medicare using the inpatient prospective payment system (IPPS). Under the IPPS, the price that Medicare pays for a given discharge equals a hospital-specific base rate multiplied by a discharge-specific case mix adjustment (or DRG relative weight), plus an outlier payment if the case is unusually costly. Hospital base rates are assigned by the Centers for Medicare and Medicaid Services (CMS) based on national “standardized amounts.” The 2009 standardized amount in a large urban area was $5,552.58 ($3,574.50 for labor-related operating costs, $1,553.91 for non-labor-related operating costs, and $424.17 for capital costs). Base rates are adjusted based on (1) whether the hospital is located in a large urban area, (2) local wages for nurses and other personnel, (3) the share of patients who are low-income (through so-called disproportionate share hospital [DSH] add-ons), (4) the number of medical residents (so-called indirect medical education [IME] payments), (5) whether the hospital is small and located in a rural area (so-called sole community hospitals [SCHs] or “Medicare dependent hospitals” [MDHs]), and many other factors. Even if two hospitals provide exactly the same services, they generally will receive different Medicare prices, and the differences in those prices have changed over time.

Medicare hospital payment policy has been dominated by two major changes since the mid-1990s. First, the Balanced Budget Act of 1997 (BBA97) cut payment rates across the board by setting increases in the national standardized amounts well below inflation for several years. Second, Congress has passed a series of targeted adjustments that have tended to cut Medicare payments to large hospitals and those in urban areas, and boost payments to smaller hospitals and those in rural areas (U.S. Government Accountability Office 2013). The BBA97 and later legislation contain numerous such provisions, including significant reductions in IME and DSH payments, and boosts in the wage index for low-wage urban areas. These targeted payment changes have tended to compress Medicare inpatient prices, that is, reduce them in high-priced markets and increase them in low-priced markets. This compression has not been a clearly stated policy objective, however, but rather has emerged as a result of the political process in Congress.

We measure the actual Medicare price for each MSA using Medicare hospital cost reports. Hospitals differ in their cost reporting periods, so we first standardize time periods by allocating each hospital’s cost report to calendar years. We then sum revenues and discharges and calculate the MSA-year price, where price equals total Medicare inpatient fee-for-service revenues (including amounts paid by the federal government, beneficiaries, and supplemental insurers) divided by Medicare inpatient fee-for-service discharges. We then use the natural logarithm of the actual market-level Medicare price as our endogenous variable.

Conceptually, our Medicare price instruments capture the effect on Medicare inpatient prices of the accumulation of changes in the payment formula from 1995 on. All of our analyses include market dummies and year dummies—the instruments capture the formula-driven divergence from general trends in each market. We consider three types of changes to the payment formula: the hospital-specific rate, SCH/MDH designations and formulas, and the outlier payment formula. Our instruments are created in four steps:

First, for each hospital year and type of payment change, we create a “price pair,” by taking a fixed basket of discharges and simulating two prices: one using the formula for the year in which the discharges actually occurred, and one using the formula for the following year. Several factors are, by design, held constant in the calculation of these price pairs: patient case mix, the hospital wage index, the number of medical residents, the share of the patient population with low incomes, and the hospital’s operating costs per discharge. Differences, if any, between the two prices in a price pair are only due to changes in the payment formula, which could include the standardized base amounts, geographic reclassifications, payment boosts for teaching hospitals and hospitals with large shares of low-income patients, payment boosts for isolated rural hospitals, and the outlier payment formula.

Second, for each hospital year and price pair, we calculate the natural logarithm of the ratio of the price pair (i.e., the price using the next year’s formula divided by the price using the current year’s formula). This yields the logged percentage change in the Medicare price from the current year to the next for that hospital year and type of payment change.

Third, for each hospital year, we calculate the accumulated sum of each of the three logged price–pair ratios. For 1995, these accumulated sums are all set equal to zero for all hospitals. For 1996, the accumulated sums equal (zero plus) the logged price–pair ratios calculated using 1995 claims. For 1997, the accumulated sums equal the 1996 accumulated sums plus the logged price–price ratios calculated using 1996 claims, and so on.

Fourth, we create market-level instruments equal to the discharge-weighted means of the accumulated logged price–pair ratios among hospitals located in each market. In our first-stage analyses, which include market- and year dummies and other controls, the three market-level instruments do a very good job of predicting actual logged Medicare prices, with F-statistics generally over 40.

Descriptive and Regression Analyses

For our descriptive analyses, hospital markets are grouped based on whether the market experienced large or small formula-driven increases in Medicare prices. We then compare these groups of markets in their demographics, location (urban vs rural), and in their hospital utilization in 1995, and the growth in utilization from 1995 to 2009.

We also perform a set of fixed-effects panel data regressions. The main specification is as follows:

where YMSA,t is the logged outcome of interest, ϕMSA is a set of market-fixed effects,  is a set of Census division year-fixed effects,

is a set of Census division year-fixed effects,  is the predicted logged Medicare price from the first-stage regression, UMSA,2000 is the share of the population in the MSA in an urban area in 2000 based on the U.S. Census Bureau’s urban population counts, XMSA,t is a set of market characteristics that vary over time (population, aging, poverty, unemployment, a local hospital operating cost index, and the Medicare Advantage enrollment share), λt is a set of time-varying parameters, κMSA,t is a residual, and η is the coefficient of interest (the estimated elasticity of the outcome with respect to the Medicare price).

is the predicted logged Medicare price from the first-stage regression, UMSA,2000 is the share of the population in the MSA in an urban area in 2000 based on the U.S. Census Bureau’s urban population counts, XMSA,t is a set of market characteristics that vary over time (population, aging, poverty, unemployment, a local hospital operating cost index, and the Medicare Advantage enrollment share), λt is a set of time-varying parameters, κMSA,t is a residual, and η is the coefficient of interest (the estimated elasticity of the outcome with respect to the Medicare price).

All regressions used Stata’s “xtivreg2” command, with population weights and standard errors calculated using the “robust, cluster( )” option.

Results

Among our 10 states, the mean Medicare price per discharge increased from $8,449 in 1995 to $12,741 in 2009, a difference of 50.8 percent (see Table 1). The increase in Medicare prices is smaller than the increase in the hospital input price index over the same period (55.4 percent), which means that Medicare prices, on average, fell slightly in real terms.

Table 1.

Medicare Price Growth Has Varied among Markets

| Markets Grouped Based on Formula-Driven Change in Medicare Price (1995–2009) | ||||

|---|---|---|---|---|

| All Markets | Low | Medium | High | |

| Medicare price (mean) | ||||

| 1995 | $8,449 | $9,304 | $9,018 | $7,242*** |

| 2009 | $12,741 | $13,622 | $13,733 | $11,048*** |

| Difference (%) | 50.8 | 46.4 | 52.3 | 52.6* |

| Difference attributable to formula changes (%) | 22.7 | 16.0 | 22.3*** | 28.1*** |

| Hospital characteristics (1995–2009) | ||||

| Teaching (residents per average daily census) | 0.16 | 0.28 | 0.17** | 0.08*** |

| Ownership (%) | ||||

| Not for profit | 75.5 | 87.3 | 72.1** | 70.7*** |

| For profit | 15.3 | 6.6 | 17.0* | 19.6** |

| Government | 9.2 | 6.1 | 10.8* | 9.7* |

| Population characteristics (2000) | ||||

| Urban (%) | 92.4 | 96.3 | 95.6 | 86.4*** |

| Poverty (%) | 12.4 | 12.4 | 12.3 | 12.5 |

| Number of markets | 116 | 11 | 19 | 86 |

| Population (2,000, millions) | 97.1 | 24.3 | 38.7 | 34.1 |

Note. Stars indicate statistical significance of the differences between low- and medium-growth markets, and between low- and high-growth markets, using a t-test assuming unequal variance. Markets are metropolitan statistical areas (MSAs) in 10 states (AZ, CA, CO, FL, IA, MA, NJ, NY, WA, WI).

*p < .10, **p < .05, ***p < .01.

Source: Author’s calculations using Medicare hospital cost reports and the Healthcare Cost and Utilization Project State Inpatient Databases (HCUP-SID).

Medicare price increases varied among markets. We sorted markets based on the accumulated formula-driven changes in the Medicare price and grouped them into terciles with roughly equal population. In markets in the lowest tercile, Medicare prices increased 46.4 percent, while they increased 52.6 percent in markets in the highest tercile (see Table 1).

Markets that experienced the largest formula-driven Medicare price increases tended to be nonmetropolitan—all nine of the nonmetropolitan markets in our study were in the highest tercile. Markets in the highest price-increase tercile also tended to have large market shares of for-profit hospitals and government hospitals and tended to receive relatively low Medicare prices in 1995. Medicare prices were converging somewhat, with larger price increases in the markets that started the period with relatively low prices. In contrast, markets that experienced the smallest formula-driven price increases tended to have large concentrations of teaching hospitals and tended to be large urban areas.

These differences among the markets are consistent with the specific changes in Medicare’s payment formula that occurred over this period. Hospitals in rural and small urban areas have benefitted a number of changes in payment policy, including the option of converting to “critical access hospital” status, special increases in payments for SCHs and MDHs, and payment boosts targeted at low-wage markets. In contrast, teaching hospitals have faced cuts to their add-on payments, and all hospitals in large urban areas have lost a special 3 percent add-on to their capital payments.

Among the nonelderly, inpatient hospital utilization was lower at the end of our study period, with the inpatient discharge rate falling on average less than 0.1 percent per year, and hospital days per person per year falling on average about 0.3 percent per year (see Table 2). Patients aged 65 and older accounted for a growing share of inpatient hospital discharges, but a shrinking share of hospital days—the discrepancy is a result of large reductions in the lengths of stay for the elderly.

Table 2.

Trends in Nonelderly Hospital Volume and Intensity, and Capacity in Markets with Low, Medium, and High Rates of Growth in Medicare Prices

| Markets Grouped Based on Formula-Driven Change in Medicare Price (1995–2009) | ||||

|---|---|---|---|---|

| All Markets | Low | Medium | High | |

| Volume and intensity of inpatient hospital care provided to the nonelderly | ||||

| Discharges per 1,000, 1995 | 91 | 108 | 83*** | 88*** |

| Annual growth, 1995–2009 (%) | −0.04 | −0.34 | −0.13 | 0.30*** |

| Days per 1,000, 1995 | 410 | 604 | 330*** | 364*** |

| Annual growth, 1995–2009 (%) | −0.32 | −1.42 | 0.18*** | 0.32*** |

| Mean length of stay, 1995 | 4.3 | 5.5 | 3.9*** | 4.0*** |

| Annual growth, 1995–2009 (%) | −0.14 | −1.03 | 0.41*** | 0.03*** |

| Mean case mix, 1995 | 0.84 | 0.85 | 0.83 | 0.85 |

| Annual growth, 1995–2009 (%) | 1.33 | 1.37 | 1.35 | 1.27 |

| Over-65 share of inpatient volume | ||||

| Discharges | ||||

| 1995 (%) | 31.4 | 30.7 | 27.8* | 35.8*** |

| Difference, 1995–2009 (percentage points) | 0.8 | 2.6 | 1.2** | −0.8*** |

| Days | ||||

| 1995 (%) | 41.4 | 44.1 | 35.2*** | 46.5 |

| Difference, 1995–2009 (percentage points) | −4.3 | −4.4 | −2.9 | −5.7 |

| Hospital bed-days available per 1,000, 1995 | 1,129 | 1,385 | 976*** | 1,122*** |

| Annual growth, 1995–2008 (%) | −1.83 | −2.53 | −1.48* | −1.47** |

| Occupancy | ||||

| 1995 (%) | 65.0 | 75.4 | 61.7*** | 61.2*** |

| Difference, 1995–2008 (percentage points) | 5.0 | 2.5 | 9.1*** | 2.3* |

Note. Markets are metropolitan statistical areas (MSAs) in 10 states (AZ, CA, CO, FL, IA, MA, NJ, NY, WA, WI). Hospital bed-days were not available for 2009.

*p < .10, **p < .05, ***p < .01.

Source: Author’s calculations using Medicare hospital cost reports and the Healthcare Cost and Utilization Project State Inpatient Databases (HCUP-SID).

Based on the descriptive analyses, reductions in the Medicare price appear to be related to declines in the number of discharges provided to the nonelderly. In low-price-growth markets, nonelderly discharges fell on average by 0.3 percent per year, whereas in high-price-growth markets discharges increased by 0.3 percent per year. The availability of hospital bed-days fell across all market types but fell fastest in low-price-growth markets. Together these results suggest hospitals facing tight Medicare price constraints reduced their scale of operations and, as a result, the volume of care they provided to the nonelderly. Changes in the share of discharges and days provided to the elderly do not show any clear association with Medicare price changes. This pattern of findings in our descriptive statistics is consistent with Medicare price cuts leading to reductions in hospital capacity and spillover reductions in utilization among the nonelderly.

Consistent with the descriptive analyses, our regression results show that decreases in Medicare prices are associated with decreases in inpatient hospital utilization among the nonelderly (see Table 3). A 10-percent Medicare price cut is associated with around a 5-percent decrease in discharges among the nonelderly and an even larger decrease in hospital bed-days. Changes in the Medicare price are not associated in any statistically robust way with changes in the nonelderly length of stay, nonelderly case mix, or with changes in the share of utilization provided to the elderly. These findings suggest that hospitals have only limited ability or willingness to shift their inpatient services away from the elderly in response to Medicare price cuts.

Table 3.

Two-Stage Least Squares Regressions: Estimated Effects of Changes in the Medicare Price on Hospital Capacity and Hospital Utilization among the under-65 Population

| Model Number | 1 | 2 | 3 | 4 | 5 | 6 |

|---|---|---|---|---|---|---|

| Dependent Variable | Ln(Total Discharges among under-65s) | Ln(Mean Length of Stay among under-65s) | Ln(Mean Case Mix among under-65s) | Ln(Inpatient Hospital Bed-Days Available) | Ln(Over-65 Share of Discharges) | Ln(Over-65 Share of Days) |

| Coefficient estimates (standard errors) | ||||||

| Ln(Medicare price) | 0.475*** (0.146) | −0.036 (0.093) | −0.129 (0.101) | 0.627** (0.253) | −0.005 (0.025) | 0.020 (0.048) |

| Share of population in poverty | 0.002 (0.003) | 0.001 (0.002) | 0.002 (0.002) | 0.009 (0.008) | −0.000 (0.001) | 0.001 (0.001) |

| Share of labor force unemployed | −0.002 (0.003) | 0.001 (0.002) | −0.000 (0.002) | 0.002 (0.006) | −0.001 (0.001) | −0.001 (0.001) |

| Ln(Medicare hospital input cost index) | −0.562*** (0.136) | 0.232*** (0.086) | 0.099 (0.073) | −0.352 (0.238) | −0.013 (0.025) | −0.037 (0.038) |

| Medicare advantage enrollment share | −0.153* (0.081) | 0.031 (0.065) | 0.081 (0.051) | 0.121 (0.153) | 0.006 (0.017) | −0.038* (0.023) |

| R2 | 0.225 | 0.024 | −0.036 | −0.003 | 0.285 | 0.123 |

Note. N = 1,756. The unit of observation is the market year (120 markets), where markets are defined as metropolitan statistical areas (MSAs). The analysis includes MSAs in 10 states (AZ, CA, CO, FL, IA, MA, NJ, NY, WA, WI). All regressions include market-fixed effects, Census division × year-fixed effects, urban population share in 2000 × year dummies (coefficients not shown). Regressions are weighted by the population under age 65, and standard errors are robust, clustered at the market level.

*p < .10, **p < .05, ***p < .01.

Source: Author’s calculations.

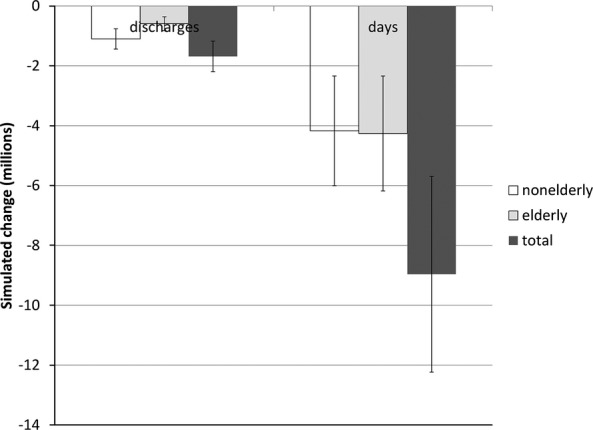

To give a sense of the magnitudes involved, we extrapolated our results to simulate the nationwide utilization effects of a 10-percent decrease in the Medicare price in 2012 (see Figure 1). That price reduction roughly matches the accumulated 10-year effect of the ACA on Medicare hospital prices. The reduction in the Medicare price leads to more than 1 million fewer discharges, and more than 9 million fewer hospital days, with the utilization reductions roughly evenly split between the elderly and nonelderly. (The analyses of utilization changes among the elderly are reported in detail in a companion piece.)

Figure 1.

Simulated Effect of a Ten-Percent Decrease Nationwide in the Medicare Hospital Price Source: Author’s calculations Vertical bars indicate ±one standard error. The population totals used in the simulation are from the year 2012.

We perform a set of sensitivity tests to better understand the robustness of the key results. The alternative specifications include (1) OLS models, (2) models with a simplified set of time trend dummies, (3) models that exclude aging controls, (4) models that include nonmetropolitan markets, and (5) models that include state-specific linear time trends. In general, these alternative specifications produce results quite similar to the results of the main model.

The OLS models are the only specifications that produce results substantially different than the main ones. In the OLS models, the estimated coefficients on the Medicare price are near zero and, except for total days, are not statistically significant. Durbin-Wu-Hausman (DWH) tests strongly reject the null hypothesis that the OLS and 2SLS results are both consistent. The pattern of results is consistent with the OLS results being biased, possibly because of changes in practice patterns or errors in volume measurement.

Conclusions

Some analysts have likened efforts to constrain health care spending to squeezing a balloon—even if costs are constrained successfully in one place, they bulge somewhere else (Schroeder and Cantor 1991). The balloon-squeezing imagery does not fit with our results, however. Our results suggest that the tightening of Medicare payment policy can have spillover effects that help slow utilization and spending growth broadly.

Finkelstein’s (2007) analysis showed that Medicare, when first implemented, spurred broad increases in hospital capacity, with large spending spillovers among the nonelderly. Our results describe a similar spillover but in reverse. Medicare’s impact on the broader health system seems to depend on how Medicare pays providers. In the 1960s and 1970s, Medicare paid hospitals very generously, and so the implementation of Medicare spurred spillover increases in spending and utilization among the nonelderly. Over the period of our study, Medicare kept tight constraints on hospital payments, and those Medicare constraints appear to have contributed to falling inpatient hospital utilization rates among the nonelderly.

Looking ahead, we expect the Medicare provisions in the ACA to slow the growth in hospital spending to a larger degree than has been projected (Congressional Budget Office 2010; Office of the Actuary 2010). Analyses of the effects of the ACA have generally ignored possible effects on utilization rates among the elderly and nonelderly.

Constraining Medicare prices for inpatient hospital care likely has many downstream effects beyond those analyzed in this article. Such effects include shifts to outpatient settings and changes in quality of care and health outcomes. To assess the effects of Medicare price constraints on the efficiency of the health sector, those broader impacts would need to be pinned down, which will require further research.

Acknowledgments

Joint Acknowledgment/Disclosure Statement: The author gratefully acknowledges the National Institute for Health Care Reform (www.nihcr.org) for funding this work, and the assistance of a Technical Advisory Panel (Herbert Wong, Stephanie Cameron, Jack Hadley, Tracy Yee, James Reschovsky, and Jeff Stensland) and two anonymous reviewers. The TAP provided insight and feedback on an earlier draft of this publication. The views expressed in this article are the author’s and should not be interpreted as those of the TAP or the employees of members of the TAP.

Disclosures: None.

Disclaimers: None.

Footnotes

Bazzoli et al. (2004/5) use changes in the actual Medicare price to identify hospitals facing large Medicare price cuts. If Medicare volume is measured with error, that approach will produce a spurious negative relationship between the Medicare price and Medicare volume.

A negative bias from data errors could explain why Bazzoli et al. (2004/5) found that reductions in the Medicare price appeared to increase Medicare volume.

Supporting Information

Additional supporting information may be found in the online version of this article:

Technical Appendix.

References

- Bazzoli GJ, Lindrooth RC, Hasnain-Wynia R. Needleman J. The Balanced Budget Act of 1997 and U.S. Hospital Operations. Inquiry. 2004;41(4):401–17. doi: 10.5034/inquiryjrnl_41.4.401. [DOI] [PubMed] [Google Scholar]

- Chernew M, Baicker K. Martin C. 2010. “Spillovers in Health Care Markets: Implications for Current Law Projections.” Centers for Medicare & Medicaid Services. [accessed on May 5, 2011]. Available at https://www.cms.gov/Reports-TrustFunds/downloads/spillovereffects.pdf.

- Congressional Budget Office. 2010. “Cost Estimate for the Amendment in the Nature of a Substitute for H.R. 4872, Incorporating a Proposed Manager’s Amendment Made Public on March 20, 2010” [accessed on August 23, 2010]. Available at http://www.cbo.gov/ftpdocs/113xx/doc11379/AmendReconProp.pdf.

- Cutler DM, Davis K. Stremikis K. 2010. “The Impact of Health Reform on Health System Spending.” The Commonwealth Fund. [accessed on June 1, 2010]. Available at http://www.americanprogress.org/issues/2010/05/pdf/system_spending.pdf.

- Dafny LS. How Do Hospitals Respond to Price Changes? American Economic Review. 2005;95(5):1525–47. doi: 10.1257/000282805775014236. [DOI] [PubMed] [Google Scholar]

- Feder J, Hadley J. Zuckerman S. How Did Medicare’s Prospective Payment System Affect Hospitals? New England Journal of Medicine. 1987;317(14):867–73. doi: 10.1056/NEJM198710013171405. [DOI] [PubMed] [Google Scholar]

- Finkelstein A. The Aggregate Effects of Health Insurance: Evidence from the Introduction of Medicare. Quarterly Journal of Economics. 2007;122(1):1–37. [Google Scholar]

- Glied S. Zivin JG. How Do Doctors Behave When Some (But Not All) of Their Patients Are in Managed Care? Journal of Health Economics. 2002;21(2):337–53. doi: 10.1016/s0167-6296(01)00131-x. [DOI] [PubMed] [Google Scholar]

- He D. Mellor JM. Hospital Volume Responses to Medicare’s Outpatient Prospective Payment System: Evidence from Florida. Journal of Health Economics. 2012;31:730–43. doi: 10.1016/j.jhealeco.2012.06.001. [DOI] [PubMed] [Google Scholar]

- House Budget Committee. 2012. “The Path to Prosperity: A Blueprint for American Renewal” [accessed on September 6, 2012]. Available at http://budget.house.gov/uploadedfiles/pathtoprosperity2013.pdf.

- McGuire TG. Pauly M. Physician Response to Fee Changes with Multiple Payers. Journal of Health Economics. 1991;10(4):385–410. doi: 10.1016/0167-6296(91)90022-f. [DOI] [PubMed] [Google Scholar]

- Morrisey MA. Cost Shifting in Health Care: Separating Evidence from Rhetoric. Washington, DC: The AEI Press; 1994. [Google Scholar]

- Office of the Actuary. 2010. “Estimated Financial Effects of the “Patient Protection and Affordable Care Act,” as Amended.” Centers for Medicare and Medicaid Services [accessed on April 26, 2010]. Available at https://www.cms.gov/Research-Statistics-Data-and-Systems/Research/ActuarialStudies/Downloads/PPACA_2010-04-22.pdf.

- Schroeder SA. Cantor JC. On Squeezing Balloons—Cost Control Fails Again. New England Journal of Medicine. 1991;325:1099–100. doi: 10.1056/NEJM199110103251510. [DOI] [PubMed] [Google Scholar]

- Shen Y-C. The Effect of Financial Pressure on the Quality of Care in Hospitals. Journal of Health Economics. 2003;22(2):243–69. doi: 10.1016/S0167-6296(02)00124-8. [DOI] [PubMed] [Google Scholar]

- U.S. Government Accountability Office. 2013. “Medicare: Legislative Modifications Have Resulted in Payment Adjustments for Most Hospitals.” GAO-13-334 [accessed on May 26, 2013]. Available at http://www.gao.gov/assets/660/653852.pdf.

- Wu VY. Hospital Cost Shifting Revisited: New Evidence from the Balanced Budget Act of 1997. International Journal of Health Care Finance and Economics. 2010;10(1):61–83. doi: 10.1007/s10754-009-9071-5. [DOI] [PubMed] [Google Scholar]

- Yip WC. Physician Response to Medicare Fee Reductions: Changes in the Volume of Coronary Artery Bypass Graft (CABG) Surgeries in the Medicare and Private Sectors. Journal of Health Economics. 1998;17(6):675–99. doi: 10.1016/s0167-6296(98)00024-1. [DOI] [PubMed] [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Technical Appendix.