Abstract

Context

The Food and Drug Administration (FDA) Safety and Innovation Act has recently relaxed conflict-of-interest rules for FDA advisory committee members, but concerns remain about the influence of members’ financial relationships on the FDA's drug approval process. Using a large newly available data set, this study carefully examined the relationship between the financial interests of FDA Center for Drug Evaluation and Research (CDER) advisory committee members and whether members voted in a way favorable to these interests.

Methods

The study used a data set of voting behavior and reported financial interests of 1,379 FDA advisory committee members who voted in CDER committee meetings that were convened during the 15-year period of 1997–2011. Data on 1,168 questions and 15,739 question-votes from 379 meetings were used in the analyses. Multivariable logit models were used to estimate the relationship between committee members’ financial interests and their voting behavior.

Findings

Individuals with financial interests solely in the sponsoring firm were more likely to vote in favor of the sponsor than members with no financial ties (OR = 1.49, p = 0.03). Members with interests in both the sponsoring firm and its competitors were no more likely to vote in favor of the sponsor than those with no financial ties to any potentially affected firm (OR = 1.16, p = 0.48). Members who served on advisory boards solely for the sponsor were significantly more likely to vote in favor of the sponsor (OR = 4.97, p = 0.005).

Conclusions

There appears to be a pro-sponsor voting bias among advisory committee members who have exclusive financial relationships with the sponsoring firm but not among members who have nonexclusive financial relationships (ie, those with ties to both the sponsor and its competitors). These findings point to important heterogeneities in financial ties and suggest that policymakers will need to be nuanced in their management of financial relationships of FDA advisory committee members.

Keywords: conflict of interest, Food and Drug Administration, drug approval

Policy Points:

FDA Center for Drug Evaluation and Research advisory committee members who have financial ties solely to the firm sponsoring the drug under review are more likely to vote in ways favorable to the sponsor.

Committee members who serve on advisory boards for sponsoring firms show particularly strong pro-sponsor bias.

Contrary to conventional wisdom, committee members who have financial ties to many different firms do not, on average, show proindustry bias in their voting behavior.

Financial relationships between physicians and industry are not all alike. In the view of physicians and patients, different types of relationships vary in their potential to create a conflict of interest: Accepting free textbooks is different from accepting free Super Bowl tickets, which is different from accepting paid travel to conferences.1,2 Dollar amounts are also important: A disposable pen is different from a million-dollar equity stake, although distinctions are made between an equity stake and equivalent reimbursement for research costs.1–3

Beyond these coarse classifications of financial transfers, more subtle distinctions can be made. Rasmussen identifies different kinds of physician-industry collaborative relationships that emerged in the United States between World Wars I and II.4,5 During this period, medical researchers varied in the degree to which they actively collaborated with firms to advance firms’ agendas, and the researchers who were most engaged with industry were driven primarily by deeply resonant matches between their intellectual interests and firms’ commercial goals rather than by purely pecuniary aims. Related to these themes of concordance between researchers and firms, and firms distinguishing among different types of physicians, Tobbell provides historical evidence of industry targeting particular kinds of academic physicians with whom to ally as it sought to counter government-led health care reform initiatives after World War II.6,7 Sismondo's ethnographic work documents ongoing marketing and promotion strategies undertaken by firms to target a small subset of physicians—key opinion leaders—in their efforts to influence a broad swath of physicians.8

These historical and sociological accounts suggest that firms carefully distinguish among different kinds of academic researchers, cultivating physician-industry relationships along dimensions that may not be immediately apparent. These accounts also suggest that legislators and agencies developing public policy would do well to pay closer attention to these various kinds of nuanced physician-industry relationships.

At the Food and Drug Administration (FDA), academic physicians are regularly asked to serve on advisory committees as external experts, aiding the agency in interpreting scientific evidence. The financial ties of some of these external advisers and the potential influence of these ties on FDA advising and downstream decisions have been a concern at least since 1991 when then-FDA commissioner David Kessler authorized an Institute of Medicine (IOM) study of the FDA's use of advisory committees.9 Subsequently, evidence emerged about industry ties of committee members who participated in decisions on products that later experienced safety problems.10,11

As Jasanoff has carefully argued, many actions required of the FDA call for savvy political judgment rather than purely scientific adjudication of therapeutic and safety claims, and the agency has been very effective in using the scientific assessments of its advisory committee experts to justify decisions that are fundamentally political.12 Financial ties of advisory committee members thus complicate an already delicate process.

The stringency of FDA regulation of the financial interests of advisory committee members has waxed and waned. Changes in policy have usually coincided with reauthorizations of the Prescription Drug User Fee Act. This legislation, originally enacted in 1992 and reauthorized every 5 years, gives the FDA the authority to levy user fees on firms submitting product approval applications for FDA review.13 The FDA has periodically issued guidance documents related to these policy changes and uses the term “conflict of interest” to refer to a broad range of industry financial interests held by committee members.14,15 There is some debate in the medical literature as to what is meant precisely by “conflict of interest”16; this article does not take an a priori position on this definition but instead uses the FDA's own definition as a starting benchmark for empirical analysis.

In 2009, the FDA commissioned the Eastern Research Group to conduct a large-scale quantitative study of the relationship between the financial ties of committee members and their voting in drug or device approval recommendations (unpublished report, 2009). This study found no statistically significant relationship between committee members’ financial ties to the firm sponsoring the drug or device under review and the likelihood of their voting in favor of approval. These results were similar to those from an earlier study of drug approvals published by Lurie and colleagues that used a smaller sample of meetings.17

The purpose of this current study was to reevaluate the association between the financial interests of FDA Center for Drug Evaluation and Research (CDER) advisory committee members and their voting behavior by using a much larger and more detailed data set of meetings and by drawing on social science theory to interpret patterns in financial interests and voting.

This larger and more comprehensive data set offered an opportunity for methodological improvement over previous studies, which were limited by their small sample sizes. Although the sample in Lurie and colleagues’ study contained approximately 200 meetings, only 76 meetings could be analyzed for the relationship between voting and financial interest, and only 11 meetings could be analyzed in relation to the drug sponsor. The Eastern Research Group study analyzed, at most, 39 meetings for sponsor relationships. Small sample sizes mean that underlying associations may go undetected. With a 10-fold expansion in the size of the meeting data set, this study significantly improves the degree to which a link between voting and financial interests can be detected.

In addition, the reported associations between financial ties and drug approval voting from previous studies were the result of simple 2-variable relationships, that is, bivariate correlations. In other words, the associations were determined first by looking at the link between voting and financial tie to a sponsor and then, separately, the association between voting and financial tie to a competitor. This kind of analysis, which does not control for both key variables at the same time, is problematic because the (lack of) association between voting and financial tie to the sponsor does not also account for the possibility of someone having ties to both the sponsor and its competitors. In particular, it is entirely plausible that having financial interests in many different firms might cancel out in terms of preferential voting: Economic theory predicts that a single firm may benefit from a financial tie, but if there are multiple competing firms, no single firm has an advantage over the others, so it is possible that none of the firms will preferentially benefit. If this is the case, an incomplete model would lead to the misleading conclusion of no association between voting and financial interests in the sponsoring firm.

This study contributes to research on conflicts of interest by assembling and analyzing a large and detailed data set of the financial ties of senior advisory research scientists; statistically accounting for the effects of multiple financial interests; and applying several different social science models to shed light on different dimensions of the empirical findings. In this way, this analysis contributes to both a statistically sharper and a more nuanced understanding of issues related to the regulation of conflicts of interest in medicine.

Methods

Data

Transcripts of and other supporting documents related to FDA CDER advisory committee meetings that took place between February 1997 and December 2011 were collected from the FDA website.

All transcripts were initially screened, and meetings in which voting took place were identified. From these voting meetings, meetings that were on broad scientific topics and that did not affect a specific product or class of branded products were excluded (eg, voting meetings that affected generic products). The final sample thus consisted of all voting meetings on branded products or on drug classes that included branded products.

For each meeting in the final sample, attendees were identified from transcripts or meeting rosters. Individuals with financial interests in potentially affected firms were identified if these individuals were mentioned in the executive secretary's announcement of financial conflicts of attendees, which was made at the beginning of each committee meeting, or if meeting participants were granted a waiver to attend the meeting despite their financial conflicts, as indicated by the set of waiver documents available online. If waivers to committee members were mentioned in the executive secretary's announcement but the waiver documents were not posted on the FDA website, a Freedom of Information Act (FOIA) request for the waivers was filed and the waivers were obtained through FOIA.

Details related to attendees’ financial interests were obtained from the executive secretary's announcement, the waiver request document pertaining to the individual, or the attendee's acknowledgment of and consent for disclosure document, whichever had the most information.

For each meeting, every question asked of attendees (on which a formal vote was taken) was obtained from the meeting transcripts. Questions coded in the data set included questions on drug approval as well as up-down questions on evidence related to safety and efficacy. The votes of each attendee were recorded using the transcripts of each meeting.

Because this research involved the study and collection of publicly available documents, it was classified as exempt and thus did not require review by the Institutional Review Board.

Analysis

Multivariate logistic regression models were used to estimate the relationship between an individual's voting behavior and his or her financial interest. In all cases, the dependent variable was whether an individual voted in a way favorable to the sponsoring firm.

Two models were estimated using Stata 13. Table 1 reports the formal model specifications. In the first model, the independent variables were (1) whether the individual reported a financial interest solely in the sponsoring firm; (2) whether the individual reported a financial interest solely in firms competing with the sponsor; and (3) whether the individual reported financial interests in both the sponsoring firm and any of its competitors. In the second model, the independent variables included binary variables indicating financial interest in the sponsor only, the competitor only, and both the sponsor and its competitors, for each of the following types of financial relationships: (1) research (investigator or grant/contract recipient), (2) employer grant or contract, (3) ownership interest such as equity or bond holdings as well as income from royalties or licenses, (4) consulting, (5) member of scientific or other advisory board or steering committee, (6) blinded endpoint reviewer or member of data safety monitoring board, and (7) paid speaker.

Table 1.

Model Specifications

| Model 1 Specification |

|

competitors]) competitors]) |

| Model 2 Specification |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Where Pr indicates probability, Λ is the cumulative distribution function of the logistic distribution, and 1 is an indicator function.

These 2 models were estimated using the full sample of questions as well as a smaller sample that excluded those questions/votes in which voting was unanimous; non-unanimous votes may better reflect situations in which the scientific evidence presented is more ambiguous and therefore more subject to interpretation and bias. Since members’ answers to the same question may be correlated, standard errors were clustered on the question.

As robustness checks, the following model variants were also estimated. First, because committees are not equally represented in the overall set of meetings, each observation can be weighted by the inverse share of questions/votes contributed by each committee. Second, because the sample includes multiple questions from the same meeting, models can be estimated with standard errors clustered at the meeting level. Third, because the sample includes multiple votes from the same individual, models can be estimated with person-level fixed effects (although a fixed effect model answers a slightly different question from the one posed in this article). Finally, because of changes in conflict-of-interest policies in 2002 and 2008, models that split the sample before and after policy changes or that include year dummy variables can be estimated. For the most part, the results did not change and, in some cases, were stronger. Estimates from all of these model variants are available on request.

Results

The final sample consisted of 15 years of meetings held for 15 committees. Table 2 gives the distribution of the sample by year and committee; 1,168 questions and 15,739 question-votes from 379 meetings were analyzed. The full data panel included 1,379 unique persons who cast at least 1 vote during the 15 years.

Table 2.

Distribution of Sample by Year and Advisory Committee

| Variable | No. of Meetings (% Sample) | No. of Question-Votes (% Sample) | No. of Questions (% Sample) |

|---|---|---|---|

| Year | |||

| 1997 | 15 (4.0%) | 481 (3.1%) | 53 (4.5%) |

| 1998 | 11 (2.9%) | 250 (1.6%) | 23 (2.0%) |

| 1999 | 14 (3.7%) | 272 (1.7%) | 35 (3.0%) |

| 2000 | 11 (2.9%) | 393 (2.5%) | 42 (3.6%) |

| 2001 | 23 (6.1%) | 996 (6.3%) | 86 (7.4%) |

| 2002 | 22 (5.8%) | 787 (5.0%) | 63 (5.4%) |

| 2003 | 33 (8.7%) | 1,467 (9.3%) | 113 (9.7%) |

| 2004 | 16 (4.2%) | 1,039 (6.6%) | 75 (6.4%) |

| 2005 | 31 (8.2%) | 1,627 (10.3%) | 108 (9.3%) |

| 2006 | 25 (6.6%) | 1,134 (7.2%) | 83 (7.1%) |

| 2007 | 26 (6.9%) | 1,013 (6.4%) | 66 (5.7%) |

| 2008 | 37 (9.8%) | 1,711 (10.9%) | 114 (9.8%) |

| 2009 | 45 (11.9%) | 1,549 (9.8%) | 111 (9.5%) |

| 2010 | 40 (10.6%) | 1,576 (10.0%) | 99 (8.5%) |

| 2011 | 30 (7.9%) | 1,444 (9.2%) | 97 (8.3%) |

| Advisory Committee | |||

| Anti-infective drugs | 30 (7.9%) | 1,455 (9.2%) | 100 (8.6%) |

| Anesthetic and life support drugs | 10 (2.6%) | 246 (1.6%) | 18 (1.5%) |

| Arthritis drugs | 22 (5.8%) | 756 (4.8%) | 47 (4.0%) |

| Antiviral drugs | 20 (5.3%) | 419 (2.7%) | 30 (2.6%) |

| Cardiovascular and renal drugs | 60 (15.8%) | 1,732 (11.0%) | 166 (14.2%) |

| Dermatologic and renal drugs | 24 (6.3%) | 754 (4.8%) | 67 (5.7%) |

| Endocrine and metabolic drugs | 37 (9.8%) | 1,740 (11.1%) | 142 (12.2%) |

| Gastrointestinal drugs | 19 (5.0%) | 1,141 (7.3%) | 86 (7.4%) |

| Nonprescription drugs | 13 (3.4%) | 1,090 (6.9%) | 58 (5.0%) |

| Oncologic drugs | 48 (12.7%) | 1,408 (9.0%) | 106 (9.1%) |

| Pulmonary-allergy drugs | 19 (5.0%) | 1,089 (6.9%) | 72 (6.2%) |

| Peripheral and central nervous system drugs | 23 (6.1%) | 1,386 (8.8%) | 94 (8.1%) |

| Psychopharmacologic drugs | 20 (5.3%) | 914 (5.8%) | 72 (6.2%) |

| Pharmaceutical science and clinical pharmacology drugs | 20 (5.3%) | 560 (3.6%) | 50 (4.3%) |

| Reproductive health drugs | 14 (3.7%) | 1,049 (6.7%) | 60 (5.1%) |

| Total | 379 (100.0%) | 15,739 (100.0%) | 1,168 (100.0%) |

Percentages may not add up exactly to 100% because of rounding.

Table 3 reports summary statistics of the data panel. Since not all committees convened with equal frequency, each committee contributed a different number of meetings; the median number of meetings contributed per committee was 20. On average, there were 14 to 15 voting attendees per meeting and 4 to 5 voting questions per meeting.

Table 3.

Summary Statistics of Data Panel

| Median | Mean | Min | Max | |

|---|---|---|---|---|

| Number of meetings per committee | 20 | 25 | 10 | 60 |

| Number of voting attendees per meeting | 14 | 15 | 3 | 32 |

| Number of voting questions per meeting | 4 | 5 | 1 | 17 |

| % Participants with reported financial interest, by committee | 13.1% | 12.7% | 1.6% | 28.5% |

| % Meetings that have at least 1 participant with financial interest, by committee | 50.0% | 47.0% | 21.4% | 65.0% |

The level of financial conflicts of interest varied a great deal across FDA meetings and could on occasion be substantial. Across all committees, the median level of meeting conflictedness (percentage of individuals with a reported financial conflict of interest) was around 13% (range 2% to 29%). On average, committees reported that half of their meetings were attended by at least 1 person with a financial conflict.

Types of Financial Conflicts

Over the entire data panel, the most frequently reported financial interest was consulting, which accounted for 34% of conflicts (Table 4). The second most frequently reported conflict was an ownership stake (eg, equity or bond) and/or income from royalties and licenses; this accounted for 25% of conflicts. Research-related grant and contract conflicts, linked to either the member (9%) or his or her employer (13%), accounted for 22% of all reported conflicts.

Table 4.

Most Common Types of Financial Interests Reported

| Financial Relationship | Percentage of Conflicts |

|---|---|

| Consulting | 34 |

| Ownership interest (eg, stock), income from royalties or licenses | 25 |

| Paid speaker | 19 |

| Employer grant or contract | 13 |

| Member of advisory board or steering committee | 14 |

| Research (investigator or grant/contract recipient) | 9 |

| Blinded endpoint reviewer or member of data safety monitoring board | 7 |

Relationship Between Financial Conflicts and Voting in Favor of Sponsor

Table 5 shows estimates of the relationship between financial conflicts and the odds of voting in favor of the sponsor. Panel A (top) reports the findings for the full sample. These estimates show that even if a member does not have a financial relationship with an affected firm, the odds are greater than 50–50 that she or he will vote in favor of the sponsor rather than against the sponsor (odds = 1.32, 95% CI [1.20 to 1.46], p < 0.001).

Table 5.

Financial Ties and Voting in Favor of Sponsor

| Financial Tie | Favor Sponsor Versus Not Favor Sponsor Odds (95% CI) p-value | Difference Between Financial Tie and No Financial Tie Odds Ratio (95% CI) p-value |

|---|---|---|

| A. All Votes | ||

| Sponsor only | 1.98*** | 1.49** |

| (1.41,2.77) | (1.04,2.15) | |

| p < 0.001 | p = 0.032 | |

| Competitor only | 1.37** | 1.03 |

| (1.07,1.74) | (0.78,1.36) | |

| p = 0.012 | p = 0.829 | |

| Both sponsor and competitor | 1.54** | 1.16 |

| (1.03,2.29) | (0.77,1.76) | |

| p = 0.034 | p = 0.481 | |

| No financial ties to either sponsor or competitor | 1.32*** | ref |

| (1.20,1.46) | ||

| p < 0.001 | ||

| Number of Question-Votes | 15,739 | |

| Number of voting participants | 1,379 | |

| Number of questions | 1,168 | |

| B. Non-unanimous Votes | ||

| Sponsor only | 1.69*** | 1.56** |

| (1.19,2.40) | (1.06,2.28) | |

| p < 0.001 | p = 0.023 | |

| Competitor only | 1.38** | 1.27 |

| (1.07,1.80) | (0.95,1.71) | |

| p = 0.014 | p = 0.105 | |

| Both sponsor and competitor | 0.85 | 0.79 |

| (0.52,1.42) | (0.47,1.33) | |

| p = 0.543 | p = 0.369 | |

| No financial ties to either sponsor or competitor | 1.09 | ref |

| (0.98,1.20) | ||

| p = 0.102 | ||

| Number of Question-Votes | 9,718 | |

| Number of voting participants | 1,236 | |

| Number of questions | 699 |

***p < 0.01; **p < 0.05; *p < 0.10. Standard errors clustered on question.

If members have a financial relationship solely with the sponsor, they have 1.49 times greater odds of voting for the sponsor (95% CI [1.04,2.15], p = 0.03) than members with no financial ties. If, however, members have relationships with the competitor only or with both the sponsor and its competitors, they are no more likely to vote in favor of the sponsor than members with no financial ties.

When we exclude unanimous votes, thereby focusing on situations in which the safety or efficacy evidence presented is more ambiguous, committee members are generally less likely to vote in favor of the sponsor. In these cases, as Panel B (bottom) shows, the odds of individuals with no financial ties voting in favor of the sponsor become 50–50; that is, they are as likely to vote in favor of the sponsor as against (odds = 1.09, 95% CI [0.98 to 1.20]). Most interesting, those individuals who have ties to both the sponsor and its competitors have much reduced odds of voting in favor of the sponsor relative to against the sponsor (odds = 0.85), although these odds are not statistically different from 1.

Meeting participants who have ties solely to the sponsor are, as before, more likely to vote in favor of the sponsor relative to those with no ties (OR = 1.56, 95% CI [1.06 to 2.28], p = 0.02). This corresponds to an increase in the probability of voting in favor of the sponsor from a baseline of 52.1% (baseline OR = 1.09) to 62.8% (ie, an increase of 10.7 percentage points). Participants who have relationships solely with competitors or with both the sponsor and its competitors did not appear more likely to vote in favor of the sponsor than individuals with no financial ties.

The type of financial relationship also matters. Table 6 reports estimates of the relationship between the type of financial tie and voting in favor of the sponsor. The financial relationship most strongly associated with voting in favor of the sponsor is being a member of an advisory board solely for the sponsor (OR = 4.97, 95% CI [1.62 to 15.29], p < 0.005). Expressed in terms of voting probabilities, this advisory board relationship shifts the baseline probability of voting in favor of the sponsor from 52.1% to 84.4%, an increase of 32.3 percentage points.

Table 6.

Type of Financial Tie and Voting in Favor of Sponsor, Non-unanimous Votes

| Financial Relationship | Favor Sponsor Versus Not Favor Sponsor Odds (95% CI) p-value | Difference Between Financial Tie and No Financial Tie Odds Ratio (95% CI) p-value |

|---|---|---|

| Research (Investigator or Grant/Contract Recipient) | ||

| Sponsor only | 2.34 | 2.14 |

| (0.53,10.30) | (0.48,9.54) | |

| p = 0.261 | p = 0.317 | |

| Competitor only | 0.58 | 0.53 |

| (0.19,1.78) | (0.17,1.63) | |

| p = 0.339 | p = 0.269 | |

| Both sponsor and competitor | .. | .. |

| Employer Grant or Contract | ||

| Sponsor only | 0.97 | 0.89 |

| (0.40,2.37) | (0.37,2.18) | |

| p = 0.955 | p = 0.803 | |

| Competitor only | 1.30 | 1.19 |

| (0.69,2.45) | (0.62,2.29) | |

| p = 0.425 | p = 0.608 | |

| Both sponsor and | 0.35 | 0.32 |

| competitor | (0.02,5.03) | (0.02,4.60) |

| p = 0.441 | p = 0.404 | |

| Ownership Interest (eg, Stock), Income from Royalties or Licenses | ||

| Sponsor only | 2.07* | 1.89* |

| (1.10,3.90) | (0.99,3.64) | |

| p = 0.025 | p = 0.055 | |

| Competitor only | 1.34* | 1.23 |

| (0.95,1.88) | (0.85,1.77) | |

| p = 0.092 | p = 0.276 | |

| Both sponsor and | 1.11 | 1.02 |

| competitor | (0.34,3.63) | (0.31,3.35) |

| p = 0.862 | p = 0.977 | |

| Consulting | ||

| Sponsor only | .. | .. |

| Competitor only | .. | .. |

| Both sponsor and | 0.98 | 0.89 |

| competitor | (0.69,1.38) | (0.62,1.29) |

| p = 0.894 | p = 0.552 | |

| Member of Advisory Board or Steering Committee | ||

| Sponsor only | 5.43*** | 4.97*** |

| (1.78,16.55) | (1.62,15.29) | |

| p = 0.003 | p = 0.005 | |

| Competitor only | 1.55 | 1.42 |

| (0.98,2.47) | (0.88,2.31) | |

| p = 0.062 | p = 0.153 | |

| Both sponsor and competitor | .. | .. |

| Blinded Endpoint Reviewer or Member of Data Safety Monitoring Board | ||

| Sponsor only | 0.31 | 0.28 |

| (0.03,2.95) | (0.03,2.72) | |

| p = 0.305 | p = 0.272 | |

| Competitor only | 0.25** | 0.23** |

| (0.08,0.79) | (0.07,0.73) | |

| p = 0.018 | p = 0.012 | |

| Both sponsor and | 1.83 | 1.68 |

| competitor | (0.17,20.21) | (0.15,18.55) |

| p = 0.621 | p = 0.673 | |

| Paid speaker | ||

| Sponsor only | 1.99* | 1.82* |

| (0.99,4.00) | (0.90,3.70) | |

| p = 0.053 | p = 0.096 | |

| Competitor only | 1.78* | 1.63 |

| (0.94,3.38) | (0.85,3.13) | |

| p = 0.078 | p = 0.143 | |

| Both sponsor and | 0.46 | 0.42* |

| competitor | (0.18,1.18) | (0.17,1.08) |

| p = 0.106 | p = 0.073 | |

| No financial ties to either | 1.09* | ref |

| sponsor or competitor | (0.99,1.21) | |

| p = 0.083 | ||

| Number of Question-Votes | 9,717 | |

| Number of voting participants | 1,236 | |

| Number of questions | 699 | |

Indicates insufficient variability to identify coefficient.

***p < 0.01, **p < 0.05, *p < 0.10. Standard errors clustered on question.

On the one hand, having some kind of ownership interest in or being a paid speaker solely for the sponsoring firm is also associated with voting in favor of the sponsor, but weakly so. On the other hand, being a paid speaker for both the sponsor and its competitors is associated with lower odds of voting in favor of the sponsor.

Discussion

Having a vastly expanded data set of FDA CDER advisory committee member votes and financial interests has allowed us to detect relationships that had previously been missed. In contrast to earlier research, this study finds that individuals with financial interests solely in the sponsoring firm are more likely to vote in favor of the sponsor than are members who have no financial ties; moreover, this pro-sponsor bias appears to be larger when we look at non-unanimous votes—cases in which the scientific evidence may be more ambiguous. At the same time, however, individuals with ties to both the sponsor and its competitors do not appear to vote differently from those with no financial ties.

When we look at specific types of financial relationships, we observe similar patterns. Having an ownership interest in, being a member of an advisory board or a steering committee for, and being a paid speaker for solely the sponsoring firm are associated with greater odds of voting in favor of the sponsor. But receiving honoraria from both the sponsoring firm and its competitors is associated with lower odds of voting in favor of the sponsor.

Economic and sociological theory can help inform the interpretation of these patterns. One hypothesis to explain the null result of having multiple ties is that there is an arms race, with firms competing for a voting advantage. Economic theory predicts that with this kind of firm competition, the end result will be that no single firm has a preferential voting advantage. In this model, all firms would have been better off financially if they had not “invested” in a researcher to try to gain a voting advantage—but given that one firm attempts to gain an advantage by developing a financial relationship with a researcher, it is in the interest of the other firms to also do so. After expenditures have been made, however, no firm has an advantage.

A second hypothesis is, as Rasmussen and Tobbell have discussed, that firms and researchers mutually select each other for different types of collaborative relationships. Researchers with exclusive ties are likely to be those whose professional and intellectual interests reflect, as Rasmussen described it, a “genuine and deep convergence” with the firm's commercial product interests.5 Mutual influence can occur during these sustained relationships. The votes of those with exclusive ties therefore reflect not only the firm's influence but also the researchers’ own scientific beliefs. In contrast, researchers with multiple ties are Rasmussen's “free-lancers.”5 These researchers have industry relationships but are independent minded in the kinds of questions they choose to study and how they conduct their research. In the eyes of individual firms, these researchers are not amenable to influence.

A third hypothesis is that certain types of researchers—those who are particularly successful in their research and respected in the profession—are highly sought after by multiple firms. In Sismondo's model, firms target these successful key opinion leaders with the aim of deploying them to influence other researchers and clinicians. Their high status means that the returns to a firm being able to influence a key opinion leader will be large because of the leader's broad influence among physicians.

The evidence presented here, however, is more consistent with Rasmussen's “free-lancer” model in that those researchers with multiple ties appear less likely to be influenced by any one firm: Advisory committee members who have ties to multiple firms are not more likely to vote in favor of the sponsor than those with no financial ties. Moreover, point estimates suggest that these researchers with multiple ties may vote against the sponsor more frequently than those with no ties at all. Thus, researchers who are key opinion leaders may be influential and persuasive for a variety of reasons—they are charismatic speakers and well connected—but perhaps more important, they are key opinion leaders because they are very good at medical research. This means they are very good at evaluating evidence and identifying potential problems and are thus less likely to be swayed by ambiguous sponsor evidence. These kinds of investigators may be “biased” in terms of helping a particular firm with scientific product development when commissioned to do so, but they are not “biased” in their voting.

The foregoing hypotheses are not, of course, mutually exclusive, and certain aspects of competition, mutual selection, and firm targeting of key opinion leaders for both their influence and their expertise could all be at work. Viewed together, they illustrate the richness and heterogeneity of underlying relationships that have often been pooled together under the rubric of conflict of interest and physician-industry financial ties.

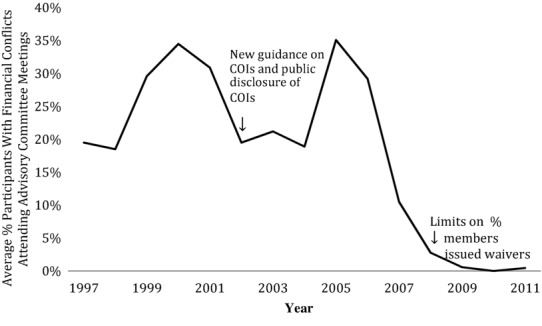

Despite the FDA's reported difficulty in finding advisory committee members with no financial ties,18,19 there has been a shift in the level of financial conflicts in advisory committee meetings. Figure1 shows the historical trend, as reflected in the data set, in the average level of meeting conflictedness. Although there was a dip in 2002 after the FDA issued stringent guidelines on the disclosure of conflicts of interest,20 the level of conflictedness subsequently rebounded to its earlier levels. Since late 2008, however, with the enactment of the Food and Drug Administration Amendments Act, capping the number of conflict-of-interest waivers issued (discussed below),15 there have been consistently low levels of financial conflicts in committee meetings.

Figure 1.

Historical Trends in Financial Conflicts

Eliminating all financial relationships may not be feasible or desirable, and the fact that individuals with multiple financial ties do not favor the sponsor means that policymakers will need to be more sophisticated about the management of financial relationships of advisory committee members. The findings reported here help policymakers focus on the types of financial interests most strongly linked to voting bias. Board work solely for the sponsor appears to be a good reason for recusal. This kind of policy should be undertaken with care, however, because there is likely to be heterogeneity in board memberships and the kind of relationships they reflect.21 Being a member of a data safety monitoring board, for example, appears to reflect skepticism or lack of bias.

What might other policy implications be? Here, it is important to emphasize that these reported estimates need not imply cause and effect. That is, these findings do not necessarily show that firms with exclusive financial relationships are influencing researchers’ or doctors’ preferences or buying their votes—although this is certainly a possibility. An alternative hypothesis is, as discussed earlier, that researchers who have exclusive relationships with particular firms may be true believers in the mechanisms underlying the therapies promoted by these firms, despite the ambiguity of the current evidence.

Although sorting out causality is important, simple associations may be sufficient for some types of policy matters. In the case of whether FDA CDER advisory committee members with certain kinds of financial ties vote differently from members without such ties, the evidence presented here shows that they do. If policymakers believe that the pro-sponsor bias of those with exclusive financial ties (regardless of its source, whether through financial influence or preexisting beliefs) is problematic, then the findings here suggest that excluding individuals with certain kinds of ties from voting or participating may be an expeditious way to limit this bias.

One might argue that the FDA's objective in regulating conflicts of interest may not be to simply reduce bias in voting. This may well be the case. In its guidance documents, the FDA never explicitly states its organizational objective in regulating conflicts of interest and provides several different justifications for issuing waivers to committee members (waivers permit individuals with disqualifying financial interests to participate in meetings). Two of the 3 justifications for waivers suggest an FDA tolerance for bias among its advisory committee members. Citing Section 712(c)(2)(B) of the Federal Food Drug and Cosmetic Act and 18 USC § 208(b), the FDA states that the agency can issue waivers in the following cases: (1) if an individual's financial interest is “not so substantial” that it is likely to affect the individual's committee service; (2) if the need for an individual's expertise outweighs the risk of influence; or (3) if the individual provides “essential” expertise not otherwise obtainable.15 The last 2 reasons appear to concede the possibility of financially driven bias in committee service but balance this bias against the intellectual expertise that a financially conflicted individual would bring to advisory committee deliberations. Thus, the complete elimination of the influence of financial interests in advisory committee activity does not appear to be of paramount importance.

At the same time, the fact that the FDA commissioned the 2009 study to analyze the relationship between financial interests and voting suggests that the agency is at least nominally concerned about voting bias. Thus, a careful reexamination of the association between financial interests and voting, like that documented in this article, is consistent with the agency's priorities even if it is not the single most important factor in the FDA's regulation of financial interests. It is also possible that had the previous studies uncovered biases, the FDA may well have taken more specific actions. Policymaking is a dynamic process, with policies continually being refined and updated as more information becomes available and as stakeholders respond to policies in anticipated and unanticipated ways.

One policy implication of this analysis that some might find troubling is that individuals with many nonexclusive ties do not appear to show a bias in voting. Conventional wisdom has it that the more industry ties a researcher has, the more dependent she or he is on industry and therefore the more influenced by industry he will be. As well, individuals with preexisting industry sympathies may be selected by many firms for collaborations. Thus, one risk of including individuals with many ties is that they harbor a pro-industry bias. More generally, individuals with any ties, whether to the sponsor or a competitor, could have a pro-industry bias relative to those with no ties.

If a pro-industry bias is reflected in systematically voting for approval of pharmacological therapies in the face of ambiguous evidence, then this study does not support—in this specific context—that hypothesis. Individuals with exclusive ties to competitors or with multiple ties to many firms do not appear to vote differently from those with no financial ties at all. It is important, however, to emphasize that these are average effects across many participating individuals and different committees. There may well be specific individuals with strong pro-industry preferences among those researchers with industry ties, and pro-industry preferences may be more manifest in some committees and product markets than others. (One might also argue that, if pro-industry bias is a particularly acute concern for FDA advisory committees, then perhaps there should be more scrutiny of patient representatives who serve on advisory committees; although these representatives may not have direct financial ties to industry, they could have pro-industry bias, preferring to have more, rather than fewer, treatment choices made available.) These kinds of heterogeneity are part of what makes regulating conflicts of interest particularly challenging.

An alternative approach to regulating conflicts of interest is to consider theoretical justifications for conflict-of-interest policies, independent of any detectable empirical consequences of these policies. If conflicts of interest are deemed wrong on first principles, the argument goes, then these conflicts should be banned, regardless of the existence of bias or the size of bias effects.16 While this is a defensible position to take, a full discussion of whether conflict-of-interest policies should be based on consequentialism or on deontological ethics is, unfortunately, beyond the scope of this article. Rather, the focus of this paper is on a much narrower question based on the following premise: Policies are put into place in order to meet an intended objective. Have the enacted policies been effective or ineffective in achieving that objective?

What this study suggests is that, in terms of financial interests and voting, there appears to be a pattern of exclusive ties to the sponsor being associated with a pro-sponsor voting bias, particularly in relation to advisory board ties, but there is no detectable bias among individuals with ties to competitors or ties to both sponsors and competitors. To the extent that the FDA's objective is to minimize bias in voting—and its previous commissioned study indicates that this is one of the FDA's goals—then this study informs the FDA on policy effectiveness. (Note that by using the benchmark that the FDA itself has set, this article implicitly uses a consequentialist approach to conflict-of-interest regulation.)

One limitation of this study is that it reports broad patterns of associations and not causal estimates. However, this limitation, is not, as argued above, a fatal one for some kinds of policy questions related to regulating conflicts of interest. A second limitation of the analysis is that it assumes that having no financial interests is the correct baseline standard; perhaps individuals with no ties are very different from those with financial ties. Although the fixed effects analysis (ie, the analysis that tracks individuals over time as they change their financial relationships) shows similar results, there may be some disagreement over whether having no ties is the appropriate standard. Third, there appears to be a great deal of heterogeneity across different committees in levels of conflictedness, ranging from 2% to 29%. It is possible that the relationship between financial interest and voting could depend on the average levels of conflicts or on other less tangible committee-specific reasons (eg, leadership, organizational, or committee features).

Despite these limitations, there appears to be a clear relationship between some types of financial interests and pro-sponsor voting on FDA CDER advisory committees. At the same time—counter to conventional wisdom—multiple ties to industry need not signal a pro-industry bias or pro–financial interest decision making. For policy, these findings imply that a litmus test of the existence of a financial interest or simple tabulations of an investigator's number of conflicts can be coarse and misleading measures of bias. The analysis from these expanded data underscores the need for the FDA to be more subtle in its management of financial interests as the loosened conflict-of-interest rules of the FDA Safety and Innovation Act are put into place.22

Although more refinements are needed to clarify mechanisms and understand heterogeneity in industry relationships, these findings can provide some initial guidance for policymakers on this important issue.

Acknowledgments

Genevieve Pham-Kanter had full access to all the data in the study and takes responsibility for the data and the accuracy of the data analysis. Laquesha Sanders provided crucial research assistance with data collection and data cleaning; Igor Gorlach provided helpful research assistance with data collection and legal and regulatory research; Magdalina Gugucheva assisted with helpful legal and regulatory research; Kenneth Oshita provided programming assistance; and John Barnes assisted with data collection.

Funding/Support

This research was supported by the Edmond J. Safra Philanthropic Foundation through a grant to the Edmond J. Safra Center for Ethics at Harvard University.

Conflict of Interest Disclosures

Pham-Kanter reports a grant from the National Human Genome Research Institute of the National Institutes of Health to research data sharing.

References

- 1.Wazana A. Physicians and the pharmaceutical industry: is a gift ever just a gift? JAMA. 2000;283:373–380. [Google Scholar]

- 2.Steinman MA, Shlipak MG, McPhee SJ. Of principles and pens: attitudes and practices of medicine housestaff toward pharmaceutical promotions. Am J Med. 2001;110:551–557. doi: 10.1016/s0002-9343(01)00660-x. [DOI] [PubMed] [Google Scholar]

- 3.Weinfurt KP, Hall MA, Dinana MA, et al. Effects of disclosing financial interests on attitudes toward clinical research. J Gen Intern Med. 2008;23:860–866. doi: 10.1007/s11606-008-0590-4. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Rasmussen N. The moral economy of the drug company–medical scientist collaboration in interwar America. Soc Stud Sci. 2004;34:161–195. doi: 10.1177/0306312704042623. [DOI] [PubMed] [Google Scholar]

- 5.Rasmussen N. The drug industry and clinical research in interwar America: three types of physician collaborator. Bull Hist Med. 2005;79:50–80. doi: 10.1353/bhm.2005.0036. [DOI] [PubMed] [Google Scholar]

- 6.Tobbell DA. Allied against reform: pharmaceutical industry-academic physician relations in the United States, 1945-1970. Bull Hist Med. 2008;82:878–912. doi: 10.1353/bhm.0.0126. [DOI] [PubMed] [Google Scholar]

- 7.Tobbell DA. Pills, Power, and Policy: The Struggle for Drug Reform in Cold War America and Its Consequences. Berkeley, CA: University of California Press/Milbank Memorial Fund; 2012. [Google Scholar]

- 8.Sismondo S. Key opinion leaders and the corruption of medical knowledge: what the Sunshine Act will and won't cast light on. J Law Med Ethics. 2013;41:635–643. doi: 10.1111/jlme.12073. [DOI] [PubMed] [Google Scholar]

- 9.Institute of Medicine. Food and Drug Administration Advisory Committees. Washington, DC: National Academies Press; 1992. [PubMed] [Google Scholar]

- 10.Glode ER. Advising under the influence? Conflicts of interest among FDA advisory committee members. Food Drug Law J. 2002;57:293–322. [PubMed] [Google Scholar]

- 11.Steinbrook R. Financial conflicts of interest and the Food and Drug Administration's advisory committees. New Engl J Med. 2005;353:116–119. doi: 10.1056/NEJMp058108. [DOI] [PubMed] [Google Scholar]

- 12.Jasanoff S. The Fifth Branch: Science Advisers as Policymakers. Cambridge, MA: Harvard University Press; 1990. [Google Scholar]

- 13.Public Law. 102–571 http://www.gpo.gov/fdsys/pkg/STATUTE-106/pdf/STATUTE-106-Pg4491.pdf. Accessed March 8, 2014.

- 14.FDA guidance on conflict of interest for advisory committee members, consultants and experts. 2000. FDA website http://www.fda.gov/oc/advisory/conflictofinterest/guidance.html. Accessed March 8, 2014.

- 15.Food and Drug Administration, U.S. Department of Health and Human Services. 2008. Guidance for the public, FDA advisory committee members, and FDA staff on procedures for determining conflict of interest and eligibility for participation in FDA advisory committees http://www.fda.gov/downloads/RegulatoryInformation/Guidances/UCM125646.pdf. Accessed March 8, 2014.

- 16.Lo B, Field MJ, editors. Conflict of Interest in Medical Research, Education, and Practice. Washington, DC: National Academies Press; 2009. Institute of Medicine. [PubMed] [Google Scholar]

- 17.Lurie P, Almeida CM, Stine N, Stine AR, Wolfe SM. Financial conflict of interest disclosure and voting patterns at Food and Drug Administration Drug Advisory committee meetings. JAMA. 2006;295:1921–1928. doi: 10.1001/jama.295.16.1921. [DOI] [PubMed] [Google Scholar]

- 18.Baciu A, Stratton K, Burke SP, editors. The Future of Drug Safety: Promoting and Protecting the Health of the Public. Washington, DC: National Academies Press; 2007. Institute of Medicine. [Google Scholar]

- 19.Eastern Research Group. 2007. Measuring conflict of interest and expertise on FDA advisory committees. October 26.

- 20.Food and Drug Administration, U.S. Department of Health and Human Services. 2002. Draft guidance on disclosure of conflicts of interest for special government employees participating in FDA product specific advisory committees.

- 21.Campbell EG, Gruen RL, Mountford J, Miller LG, Cleary PD, Blumenthal D. A national survey of physician-industry relationships. New Engl J Med. 2007;356:1742–1750. doi: 10.1056/NEJMsa064508. [DOI] [PubMed] [Google Scholar]

- 22.Food and Drug Administration. 2013. Food and Drug Administration Safety and Innovation Act (FDASIA) http://www.fda.gov/RegulatoryInformation/Legislation/FederalFoodDrugandCosmeticActFDCAct/SignificantAmendmentstotheFDCAct/FDASIA/. Accessed March 8, 2014.