Abstract

PURPOSE

We undertook a study to reexamine the relationship between educational debt and primary care practice, accounting for the potentially confounding effect of medical student socioeconomic status.

METHODS

We performed retrospective multivariate analyses of data from 136,232 physicians who graduated from allopathic US medical schools between 1988 and 2000, obtained from the American Association of Medical Colleges Graduate Questionnaire, the American Medical Association Physician Masterfile, and other sources. Need-based loans were used as markers for socioeconomic status of physicians’ families of origin. We examined 2 outcomes: primary care practice and family medicine practice in 2010.

RESULTS

Physicians who graduated from public schools were most likely to practice primary care and family medicine at graduating educational debt levels of $50,000 to $100,000 (2010 dollars; P <.01). This relationship between debt and primary care practice persisted when physicians from different socioeconomic status groups, as approximated by loan type, were examined separately. At higher debt, graduates’ odds of practicing primary care or family medicine declined. In contrast, private school graduates were not less likely to practice primary care or family medicine as debt levels increased.

CONCLUSIONS

High educational debt deters graduates of public medical schools from choosing primary care, but does not appear to influence private school graduates in the same way. Students from relatively lower income families are more strongly influenced by debt. Reducing debt of selected medical students may be effective in promoting a larger primary care physician workforce.

Keywords: undergraduate medical education, health manpower, primary care issues, workforce

INTRODUCTION

Many graduating US medical students are burdened by extremely high educational debt. Educators and policy makers have repeatedly called attention to this growing problem, with particular concern that students with high debt will pursue only relatively lucrative specialties, negatively affecting the primary care workforce.1,2

Studies examining the relationship between debt and primary care choice, however, have produced conflicting results. Several high-quality studies have shown no clear relationship between debt and specialty choice.3–5 Other studies have demonstrated that primary care physicians graduated with more debt than specializing peers, particularly at relatively low levels of debt.6,7 In fact, students with no debt are half as likely to choose primary care as their indebted peers.8

At the other end of the spectrum, students with very high debt also seem less likely to choose primary care, suggesting a deterrent effect as debt increases.9,10 Two small studies have suggested that students’ socioeconomic status may confound the relationship between debt level and primary care specialty choice.8,11 Students from higher-income families, on average, graduate with less educational debt.12

Our purpose was to reexamine the relationship between educational debt and primary care specialty choice using a large retrospective sample of US physicians. This approach allowed us to examine physicians’ specialty choice 9 to 22 years after medical school graduation. We focused particularly on how debt interacted with students’ socioeconomic status, measured through the proxy of need-based educational loans. This study expands on previous research, conducted by the Robert Graham Center, that examined debt as one of many predictors of several workforce outcomes.7

METHODS

Study Sample

We included in the study sample all physicians who graduated from US allopathic medical schools between 1988 and 2000 and were practicing medicine in the United States in 2010. We limited our evaluation to 1988–2000 because student loan information was collected from the American Association of Medical Colleges (AAMC) Graduation Questionnaire only during those years. Osteopathic physicians were excluded because we did not have information about their debt. All physicians were deidentified after the questionnaire data were matched with other data sets and before initiation of this analysis. The study was approved by the Georgetown University Institutional Review Board.

Data Sources

The data set developed for this study incorporates data from multiple sources. Three sources are relevant to this study. The first source, the 2010 American Medical Association (AMA) Physician Masterfile, includes updated comprehensive information about US physicians, including non-AMA members, from hospitals, medical schools, state licensing agencies, professional associations, and surveyed physicians. The Masterfile used by the Robert Graham Center has specific data enhancements, including unique identifiers and up to 6 graduate medical education programs per physician. It reliably assesses accredited physician training experiences and, therefore, specialty. Masterfile data were cross-checked against other sources to maximize accuracy in the final data set.7 The second source, the AAMC Graduation Questionnaire, is administered to all students graduating from accredited US medical schools. Response rates vary between institutions, but the overall response rate for the years studied was approximately 90%.13 The third source, a National Health Service Corps Participant Database, was developed from information provided by the US Health Resources and Services Administration.

We obtained permission from the AAMC and Health Resources and Services Administration for use of their data. Data were extracted and combined to create a unique analysis file. Details of this process have been published previously.7 From the constructed file, 136,232 physicians met inclusion criteria.

Key Variables and Measures

Data sources for specific variables are described in the Supplemental Appendix. We assessed whether graduates in our cohort were in primary care practice and family medicine practice in 2010, that is, 9 to 22 years after their graduation. Primary care practice was defined as provision of direct patient care as general practitioners, family physicians, general pediatricians, general internists, or geriatricians. We used US Department of Agricultural nonmetropolitan Rural-Urban Continuum Code 2003 definitions to identify rural counties.14 Information about rural origins was limited to physicians’ county of birth. Race was not included in the analysis because it was not available from the data sources.

Socioeconomic Status

No direct measures of socioeconomic status were available; therefore, we used student loan information as a proxy measure. Between 1988 and 2000, graduating students were asked to identify the types of loans they received to finance their medical education, selecting relevant loans from a provided list. We systematically searched published literature and Internet sources for information about current and historic student loan eligibility. We also gathered institutional knowledge from financial aid administrators about characteristics of students who might have qualified for these loans.

Three types of loans were identified as likely markers of family income (Supplemental Appendix Table 2). Physicians receiving Loans for Disadvantaged Students and Perkins loans were considered to be from families without many financial resources. Physicians receiving Health Professions Student Loans, but not the aforementioned loans, only were considered middle income. Physicians receiving none of these loans were classified as high income.

We considered but excluded use of other need-based loans as markers. Specifically, Stafford loans and Health Education Loans were excluded because eligibility for these loans does not require consideration of parents’ income.15 As most medical students have little or no personal income or assets, the vast majority qualify for these loans. Primary Care Loans were excluded because they require commitment to a primary care career.16

Analysis

To examine nonlinear relationships between debt and specialty choice, we created 5 variables signifying levels of medical education debt, in $50,000 increments. At each debt level, we calculated the proportion of graduates practicing primary care and the proportion practicing family medicine. We examined 6 groups of graduates: (1) all graduates, (2) public school graduates, (3) private school graduates, (4) recipients of Perkins loans or Loans for Disadvantaged Students, (5) recipients of Health Professions Student Loans, and (6) graduates with loans not based on parents’ income.

Measures previously found to predict primary care practice were then included in a multivariate logistic regression model predicting the outcomes.7 These variables included marital status (at graduation), sex, rural birthplace, age (at graduation), National Health Service Corps scholarship, and medical school characteristics (reported by the schools). We generated separate models for practicing primary care and practicing family medicine, again estimating 6 models for each. We calculated odds ratios for the outcomes of interest. Because the odds of choosing primary care or family medicine were generally greatest for students with debt levels of $50,000 to $100,000, we used this as the reference group. All dollar amounts were adjusted to 2010 dollars using the Consumer Price Index.

Because of secular trends in both students’ career choices and debt levels, we controlled for graduation year in our models. Given that public medical school attendance correlates with both lower educational debt12 and primary care choice,17 multivariate analyses were performed with and without controls for public school attendance. Analyses were conducted using Stata version 11.1 (Stat-Corp LP).

RESULTS

Characteristics of the study sample are shown in Table 1. One in 5 students (20.6%) graduated without educational debt, whereas more than 1 in 10 students (11.1%) had debt greater than $150,000.

Table 1.

Characteristics of Medical School Graduates Overall and Among Those With Loans

| Characteristic | All | Type of Loan Received

|

||

|---|---|---|---|---|

| Perkins/Disadvantaged Student Loans | Health Professions Student Loans | Loans Not Based on Parents’ Income | ||

| Graduates, No. (%) | 136,232 (100) | 42,389 (31.1) | 6,568 (4.8) | 58,309 (42.8) |

| Debt category, % | ||||

| None | 20.6 | 0 | 0 | 0 |

| $1–$50,000 | 17.9 | 10.0 | 12.7 | 32.7 |

| $50,001–$100,000 | 28.6 | 41.0 | 48.9 | 32.8 |

| $100,001–$150,000 | 20.2 | 31.3 | 26.8 | 22.2 |

| $150,001–$200,000 | 7.5 | 11.7 | 8.8 | 8.4 |

| ≥$200,001 | 3.6 | 6.0 | 2.8 | 3.9 |

| Debt amount, $a | ||||

| Mean | 92,689 | 105,407 | 94,135 | 83,281 |

| Median | 85,471 | 97,484 | 87,757 | 73,296 |

| Graduation era, % | ||||

| 1988–1992 | 37.0 | 32.2 | 59.9 | 35.2 |

| 1993–1996 | 33.6 | 34.5 | 35.7 | 32.2 |

| 1997–2000 | 29.4 | 33.3 | 4.4 | 32.7 |

| Demographics | ||||

| Married at graduation, %b | 33.4 | 33.1 | 43.8 | 33.6 |

| Male, % | 60.2 | 58.1 | 61.8 | 60.4 |

| Born in a rural county, % | 0.74 | 0.93 | 1.00 | 0.73 |

| Age at graduation, mean, y | 27.7 | 27.8 | 27.7 | 27.8 |

| Medical school | ||||

| Rural, % | 0.42 | 0.38 | 0.23 | 0.45 |

| Public, % | 62.1 | 67.8 | 65.3 | 59.1 |

| NHSC scholarship, % | 0.42 | 0.37 | 0.35 | 0.53 |

| Community based, % | 5.8 | 8.2 | 3.6 | 5.1 |

NHSC = National Health Service Corps.

Note: Percentages may not sum to 100% because of missing data fields. In particular, debt level was unknown for 3.3% of the study sample.

Mean and median debt levels exclude students with no debt. Debt levels are adjusted to 2010 dollars.

Marital status was unknown for 29.9% of the study sample. Unknown marital status did not predict any study outcomes in multivariate models.

Debt and the Practice of Primary Care or Family Medicine

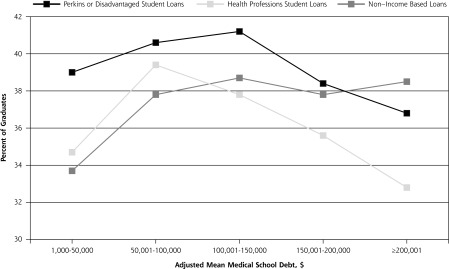

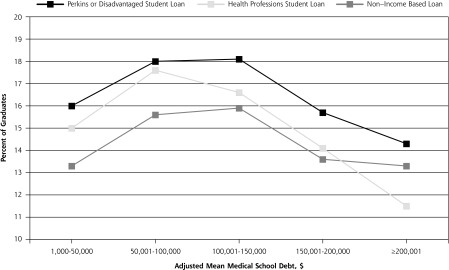

There was a nonlinear relationship between debt level and both primary care practice and family medicine practice (Figures 1 and 2, respectively). In unadjusted analyses, graduates with debt levels between $100,000 and $200,000 were most likely to eventually practice primary care or family medicine, depending on the group examined. The notable exception was private school students, whose likelihood of such practice increased as debt levels increased, without a clear peak (Supplemental Appendix Tables 3 and 4).

Figure 1.

Percent of graduates practicing primary care, by medical school debt level and type of loan received (unadjusted analyses).

Figure 2.

Percent of graduates practicing family medicine, by medical school debt level and type of loan received (unadjusted analyses).

In the first multivariate model, which controls for public school attendance, there was no substantial difference in the odds of practicing in primary care (or family medicine) between graduates with $50,000 to $100,000 debt and those with higher debt (Table 2). By contrast, in the second model, which did not control for public school attendance, there was a significant decrease in the likelihood of practicing in primary care or family medicine as debt levels increased above $100,000. The inverse relationship was also evident when public school graduates were examined separately. Among private school attendees, there was no apparent relationship between debt level and primary care specialty choice at debt levels above $100,000.

Table 2.

Multivariate Odds of Practicing Primary Care or Family Medicine by Type of Loan

| Characteristic | Practicing Primary Care, Odds Ratio | Practicing Family Medicine, Odds Ratio | ||||||

|---|---|---|---|---|---|---|---|---|

|

| ||||||||

| All (Model 1) (N = 136,232) |

All (Model 2) (N = 136,232) |

Public (n = 84,739) |

Private (n = 51,493) |

All (Model 1) (N = 136,232) |

All (Model 2) (N = 136,232) |

Public (n = 84,739) |

Private (n = 51,493) |

|

| Type of loan | ||||||||

| Loan not based on parents’ income (ref) | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| Perkins/Disadvantaged Student Loans | 1.09a | 1.12a | 1.12a | 1.02 | 1.11a | 1.20a | 1.11a | 1.07 |

| Health Professions Student Loans | 1.18a | 1.21a | 1.16a | 1.21a | 1.28a | 1.35a | 1.19a | 1.54a |

| Debt category | ||||||||

| None | 0.78a | 0.76a | 0.79a | 0.83b | 0.69a | 0.65a | 0.67a | 0.91 |

| $1,000–$50,000 | 0.89a | 0.89a | 0.90a | 0.88a | 0.87a | 0.87a | 0.87a | 0.91 |

| $50,001–$100,000 (ref) | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| $100,001–$150,000 | 0.96a | 0.92a | 0.94a | 1.02 | 0.99 | 0.91a | 0.99 | 1.04 |

| $150,001–$200,000 | 0.97 | 0.85a | 0.89a | 1.04 | 1.06 | 0.76a | 0.97 | 1.15a |

| ≥$200,001 | 0.95 | 0.80a | 0.84b | 0.99 | 1.05 | 0.66a | 0.89 | 1.11 |

| Graduation era | ||||||||

| 1988–1992 (ref) | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| 1993–1996 | 1.29a | 1.31a | 1.30a | 1.29a | 1.32a | 1.36a | 1.29a | 1.42a |

| 1997–2000 | 1.76a | 1.83a | 1.93a | 1.58a | 1.99a | 2.21a | 1.83a | 2.44a |

| Demographics | ||||||||

| Married at graduation | 1.25a | 1.27a | 1.26a | 1.22a | 1.51a | 1.58a | 1.51a | 1.52a |

| Male | 0.49a | 0.49a | 0.50a | 0.46a | 0.78a | 0.79a | 0.81a | 0.71a |

| Born in rural county | 1.46a | 1.53a | 1.55a | 0.98 | 1.95a | 2.16a | 2.00a | 1.45 |

| Age at graduation (per year) | 1.02a | 1.02a | 1.02a | 1.02a | 1.04a | 1.04a | 1.04a | 1.05a |

| Medical school | ||||||||

| Rural | 1.40a | 1.20b | – | – | 1.67a | 1.06 | – | – |

| Public | 1.30a | – | – | – | 2.05a | – | – | – |

| NHSC scholarship | 5.83a | 5.35a | 5.50a | 6.15a | 5.44a | 4.26a | 4.53a | 6.25a |

| Community based | 1.28a | 1.36a | 1.31a | 1.08 | 1.37a | 1.59a | 1.43a | 0.99 |

NHSC = National Health Service Corps; ref = reference group.

Notes: Multivariate logistic regression analyses. All variables listed were included. Model 1 controlled for public school attendance; model 2 did not.

P <. 01.

P <. 05.

Debt and Specialization by Type of Loan

Graduates with Perkins or Disadvantaged Student Loans or with Health Professions Student Loans were significantly (P <.01) more likely to practice in primary care or family medicine, compared with peers with loans not based on parents’ income (Table 2). Among these students with loans tied to parents’ income, the data demonstrate an inverse U-shaped relationship between debt level and primary care or family medicine practice, in both univariate and multivariate analyses (Figures 1 and 2, Table 3, and Supplemental Appendix Table 3). With debt of less than $50,000, there was a positive relationship between debt level and primary care practice and family medicine practice. With debt exceeding $100,000, however, students with Perkins or Disadvantaged Student Loans and Health Professions Student Loans were less likely to practice in these fields as debt levels increase. There was also a relationship between high debt and specialization among students without loans based on parents’ income (Table 3, Figure 2, and Supplemental Appendix Table 4). The relationship between high debt and specialization diminished when public school attendance was included in multivariate models, although the relationship persisted. The relationship between high debt and specialization was strongest for students with Health Professions Student Loans and weakest for students with loans not based on parents’ income.

Table 3.

Multivariate Odds of Practicing Primary Care or Family Medicine by Type of Loan

| Characteristic | Practicing Primary Care, Odds Ratio | Practicing Family Medicine, Odds Ratio | ||||

|---|---|---|---|---|---|---|

|

| ||||||

| Perkins/Disadvantaged Student Loan (n = 42,389) |

Health Professions Student Loan (n = 6,568) |

Non–Income-Based Loans (n = 58,309) |

Perkins/Disadvantaged Student Loan (n = 42,389) |

Health Professions Student Loan (n = 6,568) |

Non–Income-Based Loans (n = 58,309) |

|

| Debt category | ||||||

| $1,000–$50,000 | 0.93a | 0.86 | 0.88b | 0.85b | 0.85 | 0.89b |

| $50,001–$100,000 (ref) | 1.00 | 1.00 | 1.00 | 1.0 | 1.00 | 1.00 |

| $100,001–$150,000 | 0.91b | 0.86a | 0.94b | 0.89b | 0.84a | 0.92b |

| $150,001–$200,000 | 0.82b | 0.77b | 0.90b | 0.75b | 0.67b | 0.77b |

| ≥$200,001 | 0.73b | 0.71a | 0.88b | 0.65b | 0.52b | 0.69b |

| Graduation era | ||||||

| 1988–1992 (ref) | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 |

| 1993–1996 | 1.33b | 1.58b | 1.31b | 1.38b | 1.63b | 1.41b |

| 1997–2000 | 1.94b | 1.20 | 1.95b | 2.58b | 1.74 | 2.35b |

| Demographics | ||||||

| Married at graduation | 1.25b | 1.32b | 1.30b | 1.66b | 1.48b | 1.60b |

| Male | 0.50b | 0.51b | 0.49b | 0.77b | 0.90 | 0.80b |

| Born in rural county | 1.37b | 1.86a | 1.60b | 1.84b | 2.23b | 2.32b |

| Age at graduation (per year) | 1.02b | 1.01 | 1.02b | 1.05b | 1.04b | 1.04b |

| Medical school | ||||||

| Rural | 1.01 | 1.05 | 1.25 | 1.07 | 2.17 | 0.85 |

| NHSC scholarship | 3.58b | 6.24b | 6.15b | 2.99b | 3.08b | 4.49b |

| Community based | 1.30b | 1.68b | 1.38b | 1.62b | 1.72b | 1.50b |

NHSC = National Health Service Corps; ref = reference group.

Notes: Multivariate logistic regression analyses showing the odds of physicians who graduated from allopathic US medical schools between 1988 and 2000 practicing primary care or family medicine in 2010. Physicians are grouped into 6 different analyses, based on their types of educational loans. Data from 136,232 physicians were analyzed. All variables listed were included.

P <. 01.

P <.05.

The multivariate models showed 4 key findings. First, public school graduates were most likely to practice both primary care and family medicine at debt levels of $50,000 to $100,000; at higher debt, the odds of such practice declined (Table 2). Second, among private school graduates, family medicine and primary care practice were most likely at any debt greater than $50,000. Third, when graduates from different socioeconomic status groups, as determined by loan type, were examined separately, each group was most likely to practice both primary care and family medicine at debt levels of $50,000 to $100,000 (Table 3). And fourth, graduates with need-based educational loans were more likely to practice primary care or family medicine than students with non–need-based loans (Table 2).

DISCUSSION

Consistent with previous research, we found a nonlinear relationship between debt and specialty choice. We believe that 2 important relationships contribute to this curve (Figure 3). First, graduates with little or no debt may be less likely to choose primary care because they often come from wealthier families (ie, a socioeconomic status effect). The socioeconomic status of a students’ family of origin strongly predicts their educational debt.8,12,18,19 High socioeconomic status also predicts specialization.8,17,19 The reasons for this association remain relatively unexplored but may be related to higher income expectations among students from wealthier families. Second, public school graduates with very high debt may be less likely to choose primary care because they perceive a need for the higher financial return of specialization to finance their debt (ie, a deterrent effect).7

Figure 3.

Theoretical relationships between debt, socioeconomic status, and primary care specialty choice.

We submit that future discussions of the influence of debt on specialty choice should be guided with consideration of both the socioeconomic status effect and the deterrent effect. Although we attempted to isolate the socioeconomic status effect by including students in different socioeconomic cohorts in different multivariate models, our results demonstrated a consistent, positive relationship between increasing debt levels and primary care choice at lower debt levels. This may be because the loan groupings we used are proxies of socioeconomic status, but still contain internal socioeconomic diversity. There may be another explanation, however, for this relationship. Notably, the deterrent effect was not evident among private school students. It is possible that differences in the culture of public and private medical schools create a difference in the way that debt is perceived by graduates.

Previous studies have demonstrated that students from lower-income families are more likely to eventually practice primary care,8,19 and our study supports this association. Students with need-based loans were more likely to choose family medicine practice and primary care practice unless debt was very high. Similarly, public school graduates were 30% more likely to choose primary care and twice as likely to choose family medicine.

Public medical school graduates from lower-income families also appear to be more strongly influenced by debt, suggesting that high debt most strongly affects the career choices of the students who would otherwise be most likely to choose primary care.17 Unfortunately, lower-income students are also more likely to have high debt.12 Limiting these students’ debt, particularly if they show an interest in primary care, may help promote a larger primary care workforce. Of note, students today incur much more debt than those in our analysis, and student debt continues to rise.12

According to the AAMC, 88% of 2012 public school graduates had debt, at a median of $160,000.12 A total of 1,335 allopathic US graduates chose family medicine that year.20 Imagine that the debt of all 2012 public school graduates had been reduced to $100,000 or less. If we assume public school graduates make up 59% of allopathic students12 and are twice as likely to choose family medicine, and the debt-related odds ratios calculated in this study hold true today, we would have graduated approximately 26 to 105 more future family physicians that year. This would be a hefty price to pay for a relatively small difference in the physician workforce. On the other hand, each of those students may have made a substantial lifetime difference in the health of a community.21 If scholarship funds could be targeted effectively, reducing the debt of selected students would be well worth the cost.

At the same time, it must be acknowledged that factors other than absolute debt levels were much more strongly associated with career outcomes. Although educational debt affects medical education in important ways, it is not the primary factor influencing 92% of our students to choose non–family medicine specialties.22

Our study is limited by the absence of a direct measure of socioeconomic status. Although we believe that loan information approximates socioeconomic groups reasonably well for purposes of this study, more direct measures would be better. The AAMC Matriculating Student Questionnaire collects socioeconomic measures, but the AAMC declined to share this data with the research team.

The study is also limited by the historical nature of the analysis. Future researchers might consider using more specific measures of socioeconomic status to evaluate whether the relationships between debt and specialty choice observed here are replicated among contemporary graduates. Today’s graduates have much more debt than those studied, but will also work in health care systems with different challenges and opportunities. As public views of primary care become more favorable, and new care models change the way physicians are paid, debt may influence students differently.

Acknowledgments

Dr Julie Phillips thanks the Robert Graham Center staff and its supporters, the Michigan State University College of Human Medicine Department of Family Medicine, and Elise and Bryant Morris. All authors thank the Josiah Macy Jr. Foundation for their financial support.

Footnotes

Conflicts of interest: authors report none.

Funding support: This research was supported by the Josiah Macy Jr. Foundation.

Previous presentations: These data were presented in part at the North American Primary Care Research Group Annual Meeting, December 2012, New Orleans, Louisiana, and at the Society of Teachers of Family Medicine Annual Spring Conference, April 2012, Seattle, Washington.

Disclaimer: The information and opinions of this article do not necessarily reflect the views or policy of the American Academy of Family Physicians. We are grateful to the AAMC for use of their data, but the findings and conclusions do not reflect their views or policy.

Supplementary materials: Available at http://www.annfammed.org/content/12/6/542/suppl/DC1/.

References

- 1.Adashi EY, Gruppuso PA. Commentary: the unsustainable cost of undergraduate medical education: an overlooked element of US health care reform. Acad Med. 2010;85(5):763–765. [DOI] [PubMed] [Google Scholar]

- 2.Jolly P. Medical school tuition and young physicians’ indebtedness. Health Aff (Millwood). 2005;24(2):527–535. [DOI] [PubMed] [Google Scholar]

- 3.Hauer KE, Durning SJ, Kernan WN, et al. Factors associated with medical students’ career choices regarding internal medicine. JAMA. 2008;300(10):1154–1164. [DOI] [PubMed] [Google Scholar]

- 4.Frank E, Feinglass S. Student loan debt does not predict female physicians’ choice of primary care specialty. J Gen Intern Med. 1999;14(6):347–350. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Kahn MJ, Markert RJ, Lopez FA, Specter S, Randall H, Krane NK. Is medical student choice of a primary care residency influenced by debt? MedGenMed. 2006;8(4):18. [PMC free article] [PubMed] [Google Scholar]

- 6.Colquitt WL, Zeh MC, Killian CD, Cultice JM. Effect of debt on U.S. medical school graduates’ preferences for family medicine, general internal medicine, and general pediatrics. Acad Med. 1996;71(4):399–411. [DOI] [PubMed] [Google Scholar]

- 7.Phillips RL, Dodoo MS, Petterson S, et al. Specialty and Geographic Distribution of the Physician Workforce: What Influences Medical Student and Resident Choices? Washington, DC: The Robert Graham Center for Policy Studies in Family Medicine and Primary Care; 2009. [Google Scholar]

- 8.Phillips JP, Weismantel DP, Gold KJ, Schwenk TL. Medical student debt and primary care specialty intentions. Fam Med. 2010;42(9):616–622. [PubMed] [Google Scholar]

- 9.Rosenblatt RA, Andrilla CH. The impact of US medical students’ debt on their choice of primary care careers: an analysis of data from the 2002 medical school graduation questionnaire. Acad Med. 2005;80(9):815–819. [DOI] [PubMed] [Google Scholar]

- 10.Rosenthal MP, Marquette PA, Diamond JJ. Trends along the debt-income axis: implications for medical students’ selections of family practice careers. Acad Med. 1996;71(6):675–677. [DOI] [PubMed] [Google Scholar]

- 11.Tonkin P. Effect of rising medical student debt on residency specialty selection at the University of Minnesota. Minn Med. 2006;89(6):46–47, 49. [PubMed] [Google Scholar]

- 12.Youngclaus J, Fresne J. Physician Education Debt and the Cost to Attend Medical School. Washington, DC: American Association of Medical Colleges; 2013. [Google Scholar]

- 13.Saha S, Guiton G, Wimmers PF, Wilkerson L. Student body racial and ethnic composition and diversity-related outcomes in US medical schools. JAMA. 2008;300(10):1135–1145. [DOI] [PubMed] [Google Scholar]

- 14.US Department of Agriculture. Rural-Urban Continuum Codes. May 10, 2013. http://www.ers.usda.gov/data-products/rural-urban-continuum-codes.aspx Accessed Apr 24, 2014.

- 15.US Department of Health and Human Services Health Resources and Services Administration. Health Professions Programs: Health Professions Student Loan. http://bhpr.hrsa.gov/dsa/sfag/health_professions/bk1prt1.htm Accessed Jul 11, 2011.

- 16.American Association of Medical Colleges. Health Professions Title VII Student Loan Programs. https://www.aamc.org/advocacy/diversity/74120/laborhhs_labor0028.html Accessed Jul 11, 2011.

- 17.Bennett KL, Phillips JP. Finding, recruiting, and sustaining the future primary care physician workforce: a new theoretical model of specialty choice process. Acad Med. 2010;85(10 Suppl):S81–S88. [DOI] [PubMed] [Google Scholar]

- 18.Zonia SC, Stommel M, Tomaszewski DD. Reasons for student debt during medical education: a Michigan study. J Am Osteopath Assoc. 2002;102(12):669–675. [PubMed] [Google Scholar]

- 19.Cooter R, Erdmann JB, Gonnella JS, Callahan CA, Hojat M, Xu G. Economic diversity in medical education: the relationship between students’ family income and academic performance, career choice, and student debt. Eval Health Prof. 2004;27(3):252–264. [DOI] [PubMed] [Google Scholar]

- 20.Bieck AD, Biggs WS, Crosley PW, Kozakowski SM. Results of the 2012 National Resident Matching Program: family medicine. Fam Med. 2012;44(9):615–619. [PubMed] [Google Scholar]

- 21.Phillips J. Educational debt and career choice: every student matters. Fam Med. 2013;45(7):516. [PubMed] [Google Scholar]

- 22.Biggs WS, Crosley PW, Kozakowski SM. Results of the 2013 National Resident Matching Program: family medicine. Fam Med. 2013;45(9):647–651. [PubMed] [Google Scholar]