Abstract

Background

This paper presents an analysis of the main characteristics of the Gulf Cooperation Council’s (GCC) health financing systems and draws similarities and differences between GCC countries and other high-income and low-income countries, in order to provide recommendations for healthcare policy makers. The paper also illustrates some financial implications of the recent implementation of the Compulsory Employment-based Health Insurance (CEBHI) system in Saudi Arabia.

Methods

Employing a descriptive framework for the country-level analysis of healthcare financing arrangements, we compared expenditure data on healthcare from GCC and other developing and developed countries, mostly using secondary data from the World Health Organization health expenditure database. The analysis was supported by a review of related literature.

Results

There are three significant characteristics affecting healthcare financing in GCC countries: (i) large expatriate populations relative to the national population, which leads GCC countries to use different strategies to control expatriate healthcare expenditure; (ii) substantial government revenue, with correspondingly high government expenditure on healthcare services in GCC countries; and (iii) underdeveloped healthcare systems, with some GCC countries’ healthcare indicators falling below those of upper-middle-income countries.

Conclusion

Reforming the mode of health financing is vital to achieving equitable and efficient healthcare services. Such reform could assist GCC countries in improving their healthcare indicators and bring about a reduction in out-of-pocket payments for healthcare.

Keywords: financing healthcare, health insurance, Saudi health financing, GCC

Background

To date, in spite of their unusual characteristics and demographic challenges, the healthcare financing systems of the Gulf Cooperation Council (GCC) countries have attracted little interest. Unlike other high-income countries, where the people are the main source of healthcare funding (Wang et al., 2010), or in low-income countries, where external assistance resources could be an important source of healthcare financing, GCC countries finance their healthcare services from the revenues of natural resources (oil or gas). Furthermore, GCC countries have unique demographic characteristics that determine how their healthcare systems must be financed. One example is the very high percentage of expatriate residents (Shah, 2009). Clearly, GCC countries have characteristics that differentiate them from both high-income and low-income countries.

In the analysis of healthcare financing, a common approach found in the literature is based on economic development. This literature usually categorizes countries on the basis of their income: developed countries are usually classified as high-income countries, and developing countries are usually classified as low-income countries or in economic transition (Carrin and James, 2004; Gottret and Schieber, 2006; McIntyre, 2007; Mills, 2007). However, some countries can be classified as high-income developing countries. GCC countries such as Bahrain, Oman and the United Arab Emirates (UAE) are considered high-income countries as per the World Bank classification level of income (The World Bank, 2010). In addition, these countries share the urbanization rates of developed countries (The World Bank, 2009). On the other hand, they also share the characteristics of developing countries, such as low literacy rates, poor health profile and challenges in the process and delivery of healthcare (UNDP, 2007; Kaufmann et al., 2009). For example, GCC countries face financial challenges, including health financing (WHO, 2006a, 2006b, 2006c, 2006d, 2006e). However, whilst for some GCC countries a few aspects of healthcare financing have been discussed (Sekhri and Savedoff, 2005; Sekhri et al., 2005), they were not classified as high-income countries.

Our study sought to identify the main characteristics of GCC health financing systems and focuses on both the similarities and differences between GCC countries and other high-income and low-income countries, in order to provide recommendations for health policy makers. Included here are some of the financial and quality of care implications that can be related to the implementation of the Compulsory Employment-based Health Insurance (CEBHI) scheme in Saudi Arabia, which was recently introduced as a strategy for financing healthcare services.

Methods

To facilitate the analysis of healthcare financing in GCC countries, we (i) employed a descriptive framework (as outlined later), (ii) compared and analysed publicly available secondary data on GCC and other developing and developed countries from the World Health Organization (WHO) health expenditure database (WHO, 2010a) and (iii) conducted a literature review of related documents, including unpublished reports about the future of healthcare and financing of health services in the Kingdom of Saudi Arabia.

A framework for the analysis of healthcare financing

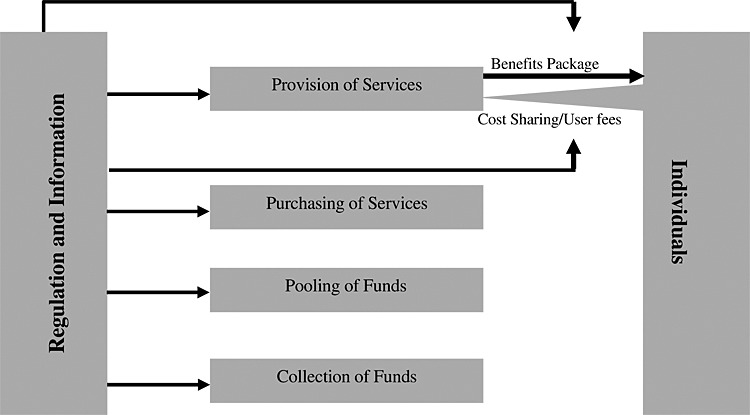

A descriptive framework (Figure 1) developed by Joseph Kutzin (2001), for the country-level analysis of healthcare financing arrangements, which can assist in determining policy options, was adapted to conceptualize different components of GCC health financing resources. This framework comprises revenue-raising mechanisms (i.e. sources of pooled funds and contribution methods), the pooling of healthcare revenues (i.e. the accumulation of prepaid healthcare revenues on behalf of a population), purchasing (i.e. the transfer of pooled resources to service providers on behalf of the population, for which the funds were pooled), the provision of services (i.e. the market structure of services), out-of-pocket (OOP) payments and the benefits package (i.e. not simply a list of services to which the population or beneficiaries of an insurance scheme are entitled, but those services and means of accessing services, for which the purchaser will pay from pooled funds).

Figure 1.

Framework of health system financing functions developed by Joseph Kutzin

Data on healthcare financing

Given the importance of consistency in the methods used to measure national health accounts (The World Bank, WHO, et al., 2003), for the comparison and analysis of national health expenditure for each GCC country, as well as amongst countries from a range of income groups (high income, upper-middle income, lower-middle income, low income), data were selected from a single source to ensure that comparisons were based on the same estimation and data collection methods; hence, the paper uses existing data on health financing from the WHO health expenditure database. Microsoft Office Excel 2003 was used to tabulate each country’s data or income group. The organization of data is by health finance function (WHO, 2010a). Descriptive statistics were used to summarize health expenditure data on GCC countries, as shown in Table 1.

National health expenditures, health workforce density and hospital beds per 10 000 population designed by authors on the basis of the World Health Organization database

| General government expenditure on health as % of THE | Private-sector expenditure on health (PvtHE) as % of THE | GGHE as % of general government expenditure | Per capita government expenditure on health (PPP int. $) | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1995 | 2000 | 2005 | 2008 | 1995 | 2000 | 2004 | 2005 | 2008 | 1995 | 2000 | 2004 | 2005 | 2008 | 1995 | 2000 | 2004 | 2005 | 2008 | |

| GCC countries | |||||||||||||||||||

| Bahrain | 69.6 | 67.5 | 68.9 | 69.7 | 30.4 | 32.5 | 32.8 | 31.1 | 30.3 | 11.3 | 10.2 | 9.4 | 9 | 9.8 | 553 | 541 | 665 | 712 | 865 |

| Kuwait | 82.6 | 77.5 | 75.4 | 76.8 | 17.4 | 22.5 | 22.7 | 24.6 | 23.2 | 6.3 | 6.7 | 6.7 | 6.1 | 6.3 | 866 | 570 | 644 | 551 | 611 |

| Oman | 83.9 | 81.8 | 82 | 73.2 | 16.1 | 18.2 | 18 | 18 | 26.8 | 6.9 | 7.1 | 6.1 | 6.1 | 4.7 | 406 | 506 | 561 | 522 | 434 |

| Qatar | 62.2 | 68.8 | 77.7 | 70.1 | 37.8 | 31.2 | 22.2 | 22.3 | 29.9 | 5 | 5 | 9.7 | 9.7 | 9.7 | 915 | 1000 | 2251 | 2293 | 1990 |

| Saudi Arabia | 67.8 | 81.7 | 81.5 | 78.9 | 32.2 | 18.3 | 18.7 | 18.5 | 21.1 | 4.7 | 9.2 | 8.7 | 8.8 | 8.8 | 247 | 529 | 517 | 536 | 608 |

| United Arab Emirates | 79 | 76.6 | 67.6 | 67.3 | 21 | 23.4 | 31.7 | 32.4 | 32.7 | 8.1 | 7.6 | 8.1 | 8.6 | 8.9 | 727 | 616 | 584 | 543 | 634 |

| World Bank Income Group | |||||||||||||||||||

| Global | 62.2 | 57.8 | 58.9 | 60.4 | 37.8 | 42.2 | 41.1 | 41.1 | 39.6 | 13.8 | 14.5 | 15.5 | 15.4 | 15.2 | 267 | 321 | 407 | 434 | 520 |

| High income | 63.6 | 59.4 | 60.4 | 62.2 | 36.4 | 40.6 | 39.6 | 39.6 | 37.8 | 14.3 | 15.6 | 16.7 | 16.8 | 17.1 | 1318 | 1631 | 2094 | 2225 | 2609 |

| Upper-middle income | 52.8 | 52 | 53.5 | 56.5 | 47.2 | 48 | 46.3 | 46.5 | 43.5 | 10.3 | 8.9 | 9.9 | 9.5 | 9.7 | 192 | 246 | 317 | 346 | 464 |

| Lower-middle income | 42.6 | 37.1 | 39.5 | 44 | 57.4 | 62.9 | 61.7 | 60.5 | 56 | 8.2 | 7.8 | 7.6 | 7.7 | 8 | 27 | 35 | 52 | 58 | 84 |

| Low income | 39.7 | 37.6 | 37.7 | 41.8 | 60.3 | 62.4 | 62.9 | 62.3 | 58.2 | 8 | 7.9 | 7.9 | 7.9 | 8.3 | 12 | 14 | 18 | 20 | 30 |

| Private insurance as % of PvtHE | Out-of-pocket expenditure as % of PvtHE | Per capita total expenditure on health at average exchange rate (US$) | Health workforce density and hospital beds per 10 000 population—GCC countries vs. the World Bank Income Group | ||||||||||||||||

| GCC countries | 1995 | 2000 | 2005 | 2008 | 1995 | 2000 | 2004 | 2005 | 2008 | 1995 | 2000 | 2004 | 2005 | 2008 | Physicians density | Nursing and midwifery personnel | Hospital beds | ||

| Bahrain | 23.4 | 25.4 | 9.1 | 14.9 | 71.3 | 68.7 | 69.3 | 71.6 | 65 | 462 | 483 | 617 | 694 | 1000 | 14.42‡ | 37.30‡ | 18§ | ||

| Kuwait | 6.2 | 6.1 | 8.4 | 8.4 | 93.8 | 93.9 | 91.6 | 91.6 | 91.6 | 615 | 504 | 635 | 658 | 1006 | 17.93§ | 45.50§ | 20§ | ||

| Oman | 23.1 | 21.3 | 22.8 | 24 | 63.2 | 64.4 | 61.8 | 60.3 | 63.5 | 232 | 252 | 290 | 312 | 458 | 19.01‡ | 41.10‡ | 18§ | ||

| Qatar | 0 | 0 | 0 | 0 | 92.7 | 84.5 | 87.2 | 87.7 | 88.7 | 567 | 659 | 1555 | 1939 | 2935 | 27.57* | 73.70* | 22§ | ||

| Saudi Arabia | 13.6 | 18.3 | 19.8 | 36.7 | 47.5 | 41.3 | 38.5 | 34.9 | 28.4 | 177 | 338 | 354 | 507 | 742 | 9.39‡ | 21.00‡ | 21.7‡ | ||

| United Arab Emirates | 19.7 | 20.2 | 22.6 | 22.2 | 71 | 69.4 | 68.1 | 67.3 | 67.6 | 713 | 699 | 794 | 888 | 1551 | 19.30† | 40.90† | 19‡ | ||

| World Bank Income Group | |||||||||||||||||||

| Global | 42.5 | 43.9 | 46.6 | 44.2 | 46.4 | 44.6 | 42.4 | 42.7 | 45.2 | 458 | 484 | 650 | 694 | 866 | 14 | 28 | 29 | ||

| High income | 46.5 | 49.1 | 52.3 | 51.1 | 41.8 | 38.2 | 36.3 | 35.9 | 36.8 | 2455 | 2657 | 3671 | 3887 | 4706 | 28 | 71 | 59 | ||

| Upper-middle income | 24.8 | 24 | 25.6 | 27 | 69.3 | 70.7 | 68.9 | 69.9 | 68.3 | 196 | 221 | 280 | 343 | 572 | 17 | 26 | 36 | ||

| Lower-middle income | 2.8 | 2.6 | 5.2 | 5.5 | 90.4 | 93.2 | 90.5 | 90.7 | 90.7 | 24 | 38 | 51 | 57 | 98 | 8 | 15 | 22 | ||

| Low income | 2.9 | 3.9 | 2.8 | 2.7 | 87.4 | 85.6 | 84.4 | 83.3 | 84.8 | 12 | 14 | 17 | 19 | 31 | 2 | 5 | 13 | ||

World Bank Income Group hospital workforce density based on 2007 data and hospital beds data based on 2005 data.

THE, total expenditure on health; PvtHE, private-sector expenditure on health; GGHE, general government expenditure on health; PPP, purchasing power parity.

Hospital workforce and hospital beds data for GCC countries.

Year 2006 data.

Year 2007 data.

Year 2008 data.

Year 2009 data.

Literature review

By using electronic and hand searches, a review of the limited available literature on GCC healthcare financing methods, including the CEBHI, was conducted. This comprised all articles, reports and official documents that addressed the financing of healthcare in GCC countries from 1992 to 2012. The review drew on a range of different sources, including government documents, books, newspapers, databases (Scopus, Science Direct, ISI Web of Knowledge, JSTOR and PubMed), specialized websites (International Labour Organization, WHO, the World Bank and Google Scholar) and conference papers on Saudi health insurance. The keywords used in the literature search were as follows: GCC healthcare financing; Saudi health financing; Saudi health insurance; health financing in high-income countries; financing of healthcare in low-income countries; the financing of healthcare in GCC countries; the financing of healthcare in Arab countries; the financing of healthcare in the Middle East; and strategic planning in Kuwait, Qatar, the UAE, Oman, Bahrain and Saudi Arabia. Moreover, in combination with the keywords, a range of generic words were included in the searches (e.g. expatriates, social health insurance and minorities).1 Moreover, given that much of the required literature would be in Arabic, a parallel literature search in Arabic was undertaken within Arabic search engines. Finally, keywords relating to the Saudi healthcare system were used, including healthcare systems in Saudi Arabia, healthcare in Saudi Arabia, Saudi health insurance, access to healthcare in Saudi Arabia and healthcare utilization in Saudi Arabia.

This study was granted approval by the King Abdullah International Medical Research Centre through grant number RC09/084, upon recommendation of the Research Committee, following the review of the Institutional Research Board on the ethical aspects of the proposal.

Results

Gulf Cooperation Council countries’ strategies for controlling healthcare financial resources

The GCC countries have substantial expatriate populations. Expressed as a percentage of the population, Kingdom of Bahrain has 40.7%; Kuwait, 68.8%; Oman, 24.4%; Qatar, 78.3%; Saudi Arabia, 25.9%; and the UAE, 71.4% (Shah, 2009). These countries share the objective of minimizing government health expenditure by reducing expatriate healthcare expenses. However, each country uses different strategies. For example, the Ministry of Health (MOH) in the UAE requires all expatriates to pay annual fees for using government healthcare services and additional fees for prescription drugs and diagnostic tests such as X-rays (WHO, 2006j). More recently, the state of Abu Dhabi in the UAE implemented a law obliging all employers to provide health insurance cover for employees and their families under three insurance schemes: one for Nationals (thiqa), one for unskilled labourers and lower-paid employees (basic) and one for higher-skilled expatriates (enhanced). A study found differences in the utilization of medical care amongst these schemes (Koornneef et al., 2012), in that those nationals within the majority high-income group utilized medical services more than those belonging to the expatriate labour worker low-income group. However, the impact of the Abu Dhabi reform is still in its early stages, having been implemented within Abu Dhabi only, as opposed to the entire UAE. By contrast, the Kingdoms of Bahrain and Kuwait use a cost-sharing method to control expatriate utilization of public services. Expatriates pay fees for visiting a district health centre, non-emergency treatment, surgical procedures, normal delivery and other medical services and procedures (WHO, 2006f). Similarly, in Oman, all expatriates in the private sector must be covered by their employer or sponsor (WHO, 2006h).

Saudi Arabia is one of the few GCC countries to have reformed its private healthcare system and reduced expatriate access to government resources. If the CEBHI proves to be an effective scheme for increasing expatriate access to medical care, it could be adapted by other GCC countries, not least, because most of the GCC countries are currently looking into different mechanisms to finance their healthcare services. For example, Qatar’s recently developed strategic plan mentioned that a health insurance scheme will be implemented, following lessons learned from neighbouring countries (Ministry of Health Qatar, 2011). In addition, one of Oman’s national strategic plans was to use health insurance as a tool to reduce healthcare expenditure (Ministry of Health Oman, 2006); however, this did not identify any means of achieving the objective. Although some authors identified financing options for financing healthcare services in Oman, the appropriate financing method to be implemented was not discussed (Al Dhawi et al., 2007). The Kingdom of Bahrain recently examined different options of health insurance as a means of increasing access to medical care to all individuals (Ministry of Health, 2011). The Kuwait national healthcare system is in the process of reforming its healthcare under the new Kuwait Health Assurance Company, which will affect both nationals and expatriates alike (Marius, 2011).

In the next section, Kutzin’s descriptive framework is adapted to conceptualize different components of Saudi Arabia’s health financing resources in connection with GCC countries, as well as low-income, middle-income and high-income countries.

Finance and resource allocation functions

Collection of funds

Oil, a commodity with a fluctuating price, is the main source of revenue for financing healthcare in GCC countries (Sturm et al., 2008). Like other GCC countries, the Saudi government, according to the law, is obliged to provide free healthcare services for its citizens, as per article 31 in the basic role of governance (Government, 1992; Hediger et al., 2007). Many countries including Qatar, a GCC member, use a dedicated part of their ‘sin taxes’ (excise duties imposed on alcohol, tobacco or gambling) to finance some of its healthcare activities (WHO, 2004), although this source of revenue is very limited. However, alcohol and gambling are forbidden in Saudi Arabia, and a tobacco tax has never been used to finance healthcare; even so, scope remains for its introduction given the prevalence of tobacco use.2 Overall, therefore, the bulk of healthcare funding in Saudi Arabia comes from the government’s annual budget; 90% of which is derived from oil revenue (Ministry of Economy and Planning, 2008). Other sources are too limited to be considered adequate for financing healthcare services.

Government expenditure

The GCC governments’ expenditure on health as a percentage of total healthcare expenditure in 2008 is high compared with that of other high-income countries (Table 1). On average, the GCC countries’ general government expenditure on health as a percentage of total health expenditure is 72.5%, whereas the average is 62.2% for high-income countries (WHO, 2010c, 2010d, 2010e, 2010f, 2010g, 2010h). However, the expenditure on health as a percentage, or by per capita, of general expenditure in GCC countries is low, compared with that in other high-income countries. For example, in 2008, per capita government expenditure on health (PPP Int. $) is $857,3 whereas the same figure in high-income countries is $2609. Despite this, GCC countries (except Oman) are between the upper-middle-income and high-income countries in terms of per capita government expenditure on health.

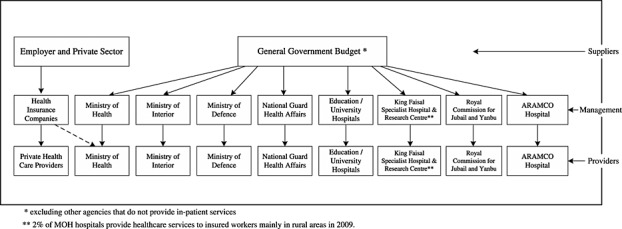

Despite concern regarding the level of general government expenditure on health, it is also the case that GCC countries, as with other Middle Eastern countries, are characterized by fragmentation of the health system. This leads to fragmentation of healthcare financing (Gericke, 2004; Ministry of Health Oman, 2006; General Secretariat of the Executive Council, Department of Planning, and Economy, et al., 2008; Ministry of Health, 2011; Supreme Council of Health, 2011; Al Razzi Holding, 2012). As can be seen in Figure 2, the healthcare funding in Saudi Arabia is split amongst more than eight different government agency budgets, and each agency provides health services for its own targeted population. However, the MOH in Saudi Arabia is the main healthcare provider, accounting for approximately 60% of all health services. Other government offices provide comprehensive health services for their employees and dependents. These providers have maintained a fairly static proportion (approximately 20%) of hospital beds since 1995 (MOH, 1995; MOH, 2003; MOH, 2008), and their budgets are allocated directly from the Ministry of Finance through their respective ministries or agencies. As these groups provide services independently, an individual could potentially have a medical record with all of these groups, whereas other citizens may not have access to any facilities because of the non-availability of services. The benefits offered by these groups are more extensive than those covered by the MOH (Al-Sharqi and Abdullah, 2012). Therefore, in the context of the Saudi healthcare system, the per capita distribution of general government expenditure on health is likely to be inequitable because of the fragmentation of the healthcare budget amongst different government agencies.

Figure 2.

Main healthcare suppliers, management and providers in Saudi Arabia (designed by authors)

Private-sector expenditure

Prior to the implementation of CEBHI, the major source of income for private healthcare services was Saudi individuals, capable of paying OOP expenses and private companies; whereas expatriates who worked in big leading companies received voluntary health insurance through their employers as one of their recruitment benefits. However, there were health insurance companies prevalent in the market without regulations (Mufti, 2000). The implementation of the CEBHI has had a clear and positive impact on payment methods: OOP payments decreased, and private insurance expenditure has increased (Table 1). After the implementation of CEBHI, between 2006 and 2008, there was a huge increase (more than 10%) in private insurance as a percentage of private-sector expenditure on health as a consequence of which, not surprisingly, OOP payments decreased (approximately 4%) (WHO 2006f). The actual proportion of private expenditure from total health expenditure did not change much (from 18% in 2006 to 22% in 2008) (WHO, 2010f). However, in theory at least, because expatriates comprise almost one-third of the population in the private sector, the share of private expenditure would need to be increased to reflect the proportion of the private sector population in Saudi Arabia. In addition, the percentage of Saudi and expatriate workers in private and government companies is 30% of the total population (excluding families) (GOSI, 2008). This segment of the population should receive healthcare services through the private sector (Table 2). Therefore, in accordance with the population makeup, private expenditure on healthcare ought to be more than 30% of the total expenditure on health. However, in 2008, private-sector expenditure on health as a percentage of total health expenditure was only 22%. There are several reasons for this relatively low expenditure:

Low private expenditure is related to the need for more legislation, an unclear vision of the private sector and manpower challenges (Hediger et al., 2007). These reasons apply to all GCC countries. In the Saudi Arabian context, the law for private healthcare services states that at least one of the owners of a health centre must be a physician, thereby discouraging businessmen from investing in healthcare (Cabinet of Ministers, 2002). As a result, the number of healthcare providers during 2006–2008 did not expand as quickly as the number of new health insurance companies (Alkhamis, 2008a, 2008b). For example, according to a report from the MOH, the increase in private health services has not kept abreast of the huge increase in demand on the private sector since 2006 (MOH, 2008).

The growth of private-sector expenditure on healthcare between 2006 and 2008 (54%) was more than the government growth percentage (22%). The large increase (31%) in gross domestic product between 2006 and 2008 meant that although the growth of the private sector (54%) between 2006 and 2008 was more than the government growth percentage (22%), the impact on total health expenditure was small, given the dominance of government expenditure in total expenditure4, when considering the financial implications of CEBHI. However, private-sector expenditure was higher prior to the implementation of CEBHI. For example, private-sector expenditure on health was more than 30% of the total expenditure in 1995 funded from OOP expenses (Table 1). When government expenditure on health was low, private expenditure increased, mainly via OOP payments, and this mode of finance reached 48% in 1998 (WHO, 2010f).

The CEBHI scheme linked the granting or renewal of a residency permit (Iqama) to the confirmation of the provision of a cooperative health insurance policy (Cabinet of Ministers, 1999). There would have been a large number of expatriates whose Iqamas were not due for renewal at the time of implementation in late 2008, meaning employers could have avoided meeting their obligation. There are also reports that some employers pay insurers ‘under the table’ to renew employee residency permits, without the employees actually having health insurance (Alsaedi, 2011). These reports require further investigation to assess the volume of this fraud and the impact this has on private-sector expenditure.

Table 2.

Health service operators, number of hospitals and total beds and primary populations served (2008)

| Health service operators | Number of hospitals/total beds | Primary population served | Percentage of beds in various health sectors |

|---|---|---|---|

| I. Government sector | 58.9 | ||

| a. Ministry of Health | 231/31 720 | All Saudi citizens and expatriate employees in government services | |

| b. Other government sectors | 20.0 | ||

| Ministry of Defense and Aviation | 22/5172 | Employees and their relatives | |

| National Guard | 4/1547 | Employees and their relatives | |

| Ministry of Interior | 1/347 | Employees and their relatives | |

| King Faisal Specialist Hospital and Research Centre | 2/1008 | Referred Saudi citizens | |

| University students and employees | 4/1873 | All Saudi citizens with a focus on university employees and students | |

| Royal Commission for Jubail and Yanbu (RCJY) | 4/459 | RCJY’s employees | |

| ARAMCO Hospital | 2/400 | ARAMCO employees | |

| Red Crescent Society | — | Emergency medical transportation | |

| Total other government sector hospitals/beds | 39/10 806 | ||

| Total government sector hospital/beds | 270/42 526 | ||

| II. Private sector (including company-operated hospitals) | 123/11 362 | Saudi Citizens and expatriates | 21.1 |

| Total hospitals/beds | 393/53 888 | ||

| Rate of beds/10 000 pp | 21.70 |

Source: Authors’ design based on the Ministry of Health data.

In addition, the law governing the supervision of cooperative insurance was only developed in 2003. Prior to this, the health insurance market was under development, and as a consequence, the relationship between healthcare providers and insurers was unregulated. One of the main reasons behind this delay was the resistance from some Islamic scholars who believed that commercial insurance should not be permissible in Islam. Importantly, the constitution of Saudi Arabia is based on the Holy Quran and the Sunnah (Prophet Mohammed’s recorded sayings and actions), and the health insurance scheme must be linked to the constitution of the country. Only cooperative health insurance and not-for-profit health insurance are permissible under Islam. The term ‘cooperative health insurance’ has been used for CEBHI, which has led to legislation being passed, but it has been suggested that CEBHI does not meet the criteria of cooperative health insurance because the money goes back to the insurance company owners (Al-Dussary, 2009). The religious acceptance of insurance was based on the Fatwa of the Council of Senior Scholars, published in 24 March 1977 on cooperative insurance, but this Fatwa does not apply to the current practice of health insurance because it is now private and commercial (Al-Ashak, 2009; Al-Dussary, 2009). The resistance to health insurance prior to approval was apparent during the Council’s voting. The members voted equally (50% accepting and 50% rejecting the scheme) (Majilas Al Shora) (Alrabiah, 2009), with the Council Chairman’s vote being responsible for the passing of the health insurance scheme before eventually being approved by the Royal Cabinet.

Pooling of healthcare revenues

The line item budget is the main budget format used in GCC countries for the government healthcare sector; hence, the pooling of healthcare revenues is fixed and isolated from the demand side. Recently, some of the GCC countries have been moving to change their budget format in order to improve the fit between the demand and supply sides. For example, Qatar, which already has a system of national health accounts, announced in its National Development Strategy 2011–2016 that they want to enhance their monitoring and control of healthcare expenditures. To this end, Qatar will be making the change from lump sum budgets to either activity-based or performance-based budgeting as soon as practicable (Ministry of Health Qatar, 2011).

As already indicated, the pooling of healthcare revenues in the private healthcare sector is fragmented. In Saudi Arabia’s CEBHI context, health insurance companies provide cover based on risk-based pooling similar to voluntary health insurance; that is, insurers charge different premiums for different risk categories and different company sizes. Therefore, the size of the premiums for small employers is critical to the success of the CEBHI scheme, especially because between 2006 and 2007, around 50% of the total number of expatriates were employed by small employers (GOSI, 2008).

Purchasing

Because there is no separation between the purchase and the provision of healthcare in the government sector, providers are paid directly in GCC countries. However, in Saudi Arabia’s private healthcare sector, the CEBHI is part of a market-oriented system, with competition from other providers. The situation is therefore similar to that in the USA, where competition exists between the healthcare providers and health insurance companies. However, in the USA, the competition amongst healthcare providers and health insurance companies has not helped reduce costs, with the presence of many purchasers diluting incentives for providers (Relman, 2007). Specifically, having multiple purchasers has led to different costs for the same health condition or an adjustment of the charges for different purchasers of the same services (Hsiao, 2007; Relman).

Provision of services

Although healthcare expenditure and per capita expenditure in GCC countries are higher than those of upper-middle-income countries, the GCC countries’ healthcare indicators are lower than those of upper-middle-income countries. For example, the density of health personnel in most GCC countries per 10 000 people is still less than that of upper-middle-income countries (WHO, 2010c, 2010d, 2010e, 2010f, 2010g, 2010h). Similarly, the number of beds per 10 000 people in Saudi Arabia and GCC countries is less than that of upper-middle-income countries (Table 1). However, after the implementation of the health insurance plan in Abu Dubai between 2009 and 2010, the total number of healthcare providers grew by 12.4%5 (Dhabi, 2010). In the Saudi Arabian context, a huge disparity exists amongst healthcare providers because of a lack of standardization (Al-Sharqi and Abdullah, 2012). In addition, the majority of healthcare centres and hospitals operate in rented buildings and lack the essential requirements for operating a healthcare facility (Al-Sharqi and Abdullah, 2012). On the other hand, only a few tertiary public healthcare facilities provide state-of-the-art technology with a high-quality of care, but these are difficult to access and hence have fewer patients (Al-Yousuf et al., 2002).

Out-of-pocket payments

With the exception of Saudi Arabia, most GCC countries share the dominance of OOP payments for the financing of healthcare with low-income countries. In Saudi Arabia, since the introduction of the CEBHI scheme, OOP payments have decreased, and private insurance expenditure has increased (WHO, 2010f). In the region more generally, when government expenditure on health is low, private expenditure, specifically OOP payments, tends to be high (WHO, 2009). OOP payments in low-income countries accounts for 56% of the total health expenditure, but only 14% in high-income countries (WHO, 2010f). A recent study showed that 49% of health financing in the Middle East comes from OOP payments (Elgazzar et al., 2010). Although the study did not include GCC countries, the OOP payments in GCC countries are high but for different reasons. Firstly, some GCC countries charge expatriates for the use of government health services. For example in Kuwait, with the highest level of private household OOP payments amongst GCC countries, expatriates have to pay for all types of healthcare visits, including visits to primary healthcare centres (WHO, 2006g). Secondly, GCC countries are high-income countries, and some citizens, if they prefer, have enough money to pay for private facilities, as evidenced by the practice in Qatar (WHO 2006i). In Saudi Arabia, before the implementation of CEBHI, and because of the low quality of public health services, the major source of private-sector expenditure was Saudi individuals capable of paying OOP expenses, and private companies (Mufti, 2000).

Benefits package

Under the unified health policy of Saudi Arabia, the CEBHI scheme has predetermined minimum health benefits. The CEBHI is managed by the Council of Cooperative Health Insurance (CCHI).6 With the scheme, employers must pay the entire premium and cannot choose to cover benefits less than those provided in the unified benefits package. In addition, the CEBHI established that if employers did not subscribe to an insurance plan, or failed to pay insurance premiums for their workers, they would then be required to pay the premiums as well as a fine and could lose the right to employ expatriate workers (Cabinet of Ministers, 1999).

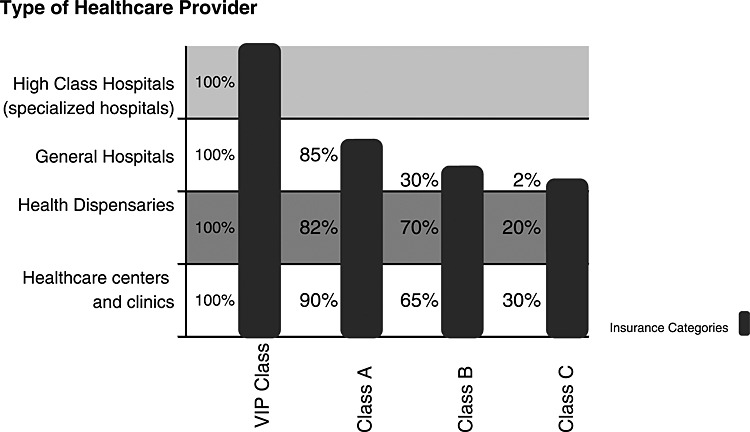

However, there are different classes of health insurance plan (Figure 3). Health insurance providers offer different health insurance packages that range from a basic plan (each insurer uses a different name for such plans, including C Plan or Balsam Direct) up to the highest level or elite plan (VIP, Gold Balsam); each with a corresponding cap on expenditure (Bupa, 2010; Elhout, 2010; Tawuniya, 2010). Each plan has different affiliated medical care providers, hospitals, or clinics, or all (Bupa, 2010; Elhout, 2010; Tawuniya, 2010). These facilities provide a range of services, from primary healthcare services to tertiary healthcare services. All insured expatriate workers can access these providers accordingly, but they may experience a different quality of medical care. The quality and services provided in one class of health insurance plan such as the basic plan are unlikely to be the same as those provided by higher-quality health insurance plans. Figure 3 illustrates the relationship pertaining to the expatriate worker’s access to different types of healthcare providers in accordance with the category of insurance coverage. Those having the highest class of insurance category, such as VIP class, can access all types of healthcare providers (from healthcare centres and clinics to high-class hospitals or specialized hospitals), whereas those having the lowest class of insurance category, such as class C, have very limited access, that is, general hospitals. The basic health insurance plan has limited affiliated hospitals and clinics, and these are known to provide a poorer quality of service than those accessible via the VIP or golden plans. In all plans, expatriates can attend one of their listed hospitals directly without going through a referral system (Bupa, 2010; Elhout, 2010; Tawuniya, 2010). However, if a patient with a basic plan (class C) requires a clinical procedure provided by a healthcare provider not within the affiliated list of hospitals or clinics, permission and referral from their insurer must be obtained (Bupa, 2010; Elhout, 2010; Tawuniya, 2010). In addition, in order to minimize health insurance expenses, some employers have an agreement with insurers to provide reduced services required by the unified medical care benefits package in CEBHI, and some would limit the health insurance plan to one or two specific clinics. However, there is no published empirical evidence regarding the actual implementation of the CEBHI scheme.

Figure 3.

The relationship between different types of healthcare providers and insurance coverage/categories

A further concern regarding the CEBHI benefits package is that the scheme has a fixed predetermined co-payment for outpatients and other services. The co-payment towards the invoice has been determined by the new policy (CCHI, 2009b). However, it is not clear whether the employee’s co-payment is affordable in relation to salary. The average expatriate salary in the private sector was less than $270 per month (Central Department of Statistics and Information, 2008), and it is not clear if this includes housing allowance. An expatriate must pay an average of 10% (specialist physician’s fees) or 30% (consultant physician fees) of their salary to cover the co-payment, excluding the cost of transportation and other expenses. The maximum amount they can pay is $26.67 for specialist visit fees or $40 for a consultant visit. According to WHO, the co-payment is considered to be catastrophic if it is more than 40% of a household’s income (Carrin and James, 2004). Further investigation would be required to determine the extent by which the co-payment is a barrier to accessing medical care.

Financial Implications of the Compulsory Employment-Based Health Insurance Scheme

The literature review and data on health financing from the WHO health expenditure database can help in identifying some financial implications of the CEBHI scheme on both the supply and demand sides of healthcare services. From the supply side, the density of health personnel in Saudi Arabia per 10 000 people is still less than that of upper-middle-income countries and most GCC countries (the density of physicians, dentists and nurses per 10 000 population is 9.39, 2.3 and 21 in Saudi Arabia versus 17, 10 and 26 in upper-middle-countries in 2008 (Table 1). The number of beds per 10 000 people in Saudi Arabia and GCC countries is less than that in upper-middle-income countries (the number of beds per 10 000 people is around 22 in Saudi Arabia versus 36 in upper-middle-income countries in 2009). Although (through CEBHI) Saudi Arabia is one of the few GCC countries to reform its private healthcare system and reduce dependence on government resources, government expenditure on health still dominates total health expenditure, and private expenditure is lower than expected. For example, government expenditure on health not only provides the majority of the healthcare budget but also has the highest percentage of government expenditure on health amongst GCC countries. Additionally, the expenditure on health as a percentage of general government expenditure increased after the implementation of CEBHI from 8.4% in 2007 to 8.8% in 2008 (WHO 2010). On the other hand, the actual proportion of private expenditure from total health expenditure has not changed much. Indeed, all things being equal, private expenditure on healthcare ought to be more than 30% of the total expenditure on health as elaborated earlier. However, low private healthcare expenditure, relative to the population covered by the CEBHI scheme, may be symptomatic of the workload of private providers and the poor quality of private healthcare services; both of which are seen as a potential obstacle in accessing healthcare (Al-Osaimi, 2009). This is borne out by a study in Saudi Arabia, which reported that the low quality of services, accessibility problems and delays in providing services were anticipated challenges that the CEBHI scheme would face after implementation (Al-Omar, 2005). Furthermore, a recent study stressed the importance of regulating the quality of health services in the private sector in Saudi Arabia after the implementation of CEBHI (Al-Sharqi and Abdullah, 2012).

From the demand for medical care perspective, the CEBHI has had a clear positive impact on payment methods: OOP payments have decreased, and private insurance expenditure has increased (WHO, 2009). However, there is a risk that the price of premiums will increase, because currently, there is no control mechanism for ensuring that high-risk expatriate workers will be accepted by insurers. In addition, health insurance companies provide cover on the basis of risk-based pooling similar to voluntary health insurance; that is, insurers charge different premiums for different risk categories and different company sizes. Therefore, the premiums for small employers are critical to the success of the CEBHI scheme, mainly because the growth rate of small companies in Saudi Arabia between 2006 and 2007 having less than five employees is the highest at 26.1%, representing 51.6% of the total number of expatriate workers (GOSI, 2008).

A big challenge on the supply side is that private hospitals are concentrated within the main cities of Saudi Arabia. For example, the cities of Riyadh and Jeddah have 48% of the private hospitals and 55.5% of the total hospital beds (MOH, 2007). In addition, approximately 53% of the nation’s dispensaries and 74% of the private clinics are prevalent in these two regions (MOH, 2007). On the other hand, the insurers were one of the main barriers of access to medical care. The Cooperative Health Insurance Council in 2008 and 2009 reported that the highest percentage of complaints received were in relation to insurance companies (CCHI, 2008; CCHI, 2009a, 2009b). This fact can be attributed to the under-development of the insurance industry. Although the law on Supervision of Cooperative Insurance Companies allows a minimum capital of SR100m for insurance companies and SR200m for companies undertaking insurance and reinsurance activities, most companies have capital below SR100m (Agency, 2008). However, it is not clear whether the fixed co-payment is financially catastrophic for some expatriates, considering that the average expatriate salary is $270 monthly.

Conclusions and Recommendations

The three main characteristics of GCC countries identified in this paper are high-income governments, dominant expatriate populations and under-development of the healthcare system, including healthcare financing. These characteristics impact on the healthcare financing strategies of GCC countries in three ways. Firstly, GCC governments provide the majority share of the health budget, similar to high-income countries. Secondly, GCC countries use different strategies to control expatriate costs, but some of these strategies lead to increased OOP expenses, which is a characteristic of low-income countries. Thirdly, healthcare financing systems in GCC countries are still being developed, as they finance most of their public services (including healthcare services) with revenue from natural resources (i.e. oil or gas). Although GCC countries are examining different options for financing healthcare services, they have not yet identified or implemented any approaches to achieve this objective and are at the stage of searching and learning from one another’s experiences. Additionally, some of their healthcare indicators are identifiable with those from below upper-middle-income countries.

The GCC countries need to reform their healthcare systems including health financing. For example, the distribution of healthcare expenditure may well be inequitable. In the context of the Saudi Arabian healthcare system, spending on healthcare is likely to be inequitable because of the fragmentation of the healthcare budget amongst different government agencies. The benefits offered by the non-MOH agencies are more extensive than those covered by the MOH; therefore, the benefit incidence of the system could potentially be improved either by combining these governmental systems or allocating the budget on the basis of a per capita need formula (Schieber, 2005).

In addition, the current financing structure in GCC countries leads to misalignment between the budget and the demand for services. Anew relationship between the purchasing organization and providers must be established in which there is enhanced monitoring and control of healthcare expenditures. However, to facilitate this, GCC countries, as is the case in Qatar, must develop a system of national health accounts.

Furthermore, equity in access to healthcare has to be an objective in any healthcare service, including GCC countries. Under the law in most GCC countries, including Saudi Arabia, the government is obliged to provide free healthcare services to its citizens, whereas the employers are obliged to provide healthcare services to the expatriate employees. Therefore, the big challenge for GCC countries is how to devise a health insurance scheme that guarantees equitable access to healthcare for all residents whilst financing healthcare differently. Although Saudi Arabia is one of the few GCC countries to reform its private healthcare system and reduce dependence on government resources, government expenditure on health still dominates total health expenditure, and private expenditure is lower than expected. However, the mode of payments has changed mainly by reducing OOP payments. There is also a risk that the price of premiums will increase, and currently, there is no mechanism for ensuring that high-risk expatriate workers will be accepted by insurers. Therefore, it is recommended that a solidarity fund be established to absorb high-risk workers and a policy be developed that will allow small companies to be united as one pool, in order to increase their appeal to insurers and reduce premiums. Finally, the CEBHI scheme might have other implications requiring further study, such as whether the CEBHI increases access to healthcare for expatriates in the private sector, and whether the co-payments paid by expatriates are catastrophic for some.

Acknowledgments

This work was supported by the King Abdullah International Medical Research Centre (KAIMRC), Riyadh, Saudi Arabia (under grant number RC09/084). In addition, we would like to thank Professor John N. Lavis, MD, PhD and Director of McMaster Health Forum, for his assistance in reviewing this paper before submission.

The authors have no competing interests.

A. A. conceived the idea and designed the study, with supervision from A. H. and P. C., as part of his PhD thesis. A. A. drafted the first paper. All authors contributed to revisions of the manuscript and approved the final draft.

Footnotes

Further information on the literature search strategy is available from the authors.

Saudi Arabia is ranked fourth globally for its tobacco consumption(Arabiya, 2012).

This figure is based on the average per capital government expenditure on health (PPP int. $) amongst GCC countries.

The private expenditure on health increased after the implementation of CEBHI by more than 54%, from SR8490bn to SR13 107bn between 2005 and 2008, respectively, but the government expenditure on health increased from SR37 283bn to SR45 537bn during the same period.

Unfortunately, at the time of writing, there were no data available to assess the contribution of this expansion on the quality of care.

The Council of Cooperative Health Insurance is the governmental body responsible for regulating and monitoring the universality of health insurance coverage. The CCHI website is http://www.cchi.gov.sa/Pages/default.aspx

References

- Agency SAM. 2008. The Saudi Insurance Market Survey Report. Riyadh: 24.

- Al Dhawi AA, West DJ, Jr, et al. The challenge of sustaining health care in Oman. Health Care Manag. 2007;26(1):19–30. doi: 10.1097/00126450-200701000-00003. [DOI] [PubMed] [Google Scholar]

- Al Razzi Holding KSCC. 2012. The Economics of Health in Kuwait and GCC States. Retrieved 6-8-2012, 2012, from http://www.alrazzi.com/AxCMSwebLive/EnAlRazziEconomic.cms.

- Al-Ashak A. 2009. Grant Mufti. A. Alkhamis. Riyadh.

- Al-Dussary DM. 2009. Cooperative insurance between Theory and Practice. Cooperative insurance Conference. Riyadh, Islamic International Foundation for Economics & Finance. 1: 18.

- Alkhamis A. 2008a. Saudi Stock Market between the Absent of Hospitals and Increase Number of Insurance Companies. The Reasons? Aleqtisadiah. Riyadh, SRPC. 5501: 1. [DOI] [PubMed]

- Alkhamis A. 2008b. Saudi Stock Market in Absent of Healthcare Providers and Increase Number of Health Insurance Companies. Aleqtisadiah. Riyadh, SRPC. 5494: 1. [DOI] [PubMed]

- Al-Omar DHM. 2005. Infrastructure for Saudi Health Insurance. 1st international Conference in health economics and Endowment. Riyadh, King Faisal Specialist Hospital and Research Centre.

- Al-Osaimi MN. 2009. The Equity in Access to Health Care Services, 2008-2009. Arab Board in Community Medicine. Damascus. Arab Board: 154.

- Alrabiah DA. 2009. How Health Care Provided Before and After Insurance. A. Alkhamis. Riyadh.

- Alsaedi Y. 2011. Fake Health Insurance in order to Legalize Your Residency Permit. AL Madinah Newspaper. Al Madinah, Almadinah 17522.

- Al-Sharqi OZ, Abdullah MT. “Diagnosing” Saudi health reforms: is NHIS the right “prescription”? Int J Health Plann Manage. 2012 doi: 10.1002/hpm.2148. DOI: 10.1002/hpm.2148. [DOI] [PubMed] [Google Scholar]

- Al-Yousuf M, Akerele TM, et al. Organization of the Saudi health system. East Mediterr Health J. 2002;8(4-5):645–653. [PubMed] [Google Scholar]

- Arabiya A. 2012. Saudi Arabia Rank Number 4 in Tobacco Consumption. Retrieved 13 June, 2012, from http://www.alarabiya.net/articles/2012/05/02/211651.html.

- Bupa. 2010. Bupa’s Products. Retrieved May 12th, 2010, from www.bupa.com.sa/arabic/products/BupaCorporates/Schemes/pages/default.aspx.

- Cabinet of Ministers. 1999. Cooperative Health Insurance Law. 71 dated 8-09-1999. T. C. o. Ministers. Riyadh, Saudi e-Government 25.

- Cabinet of Ministers. 2002. Private Health Services. 240 31st of December 2002. T. C. o. Ministers. Makkah AlMokramh, Um AlGorah Newspaper 2.

- Carrin G, James C. 2004. Reaching Universal Coverage via Social Health Insurance: Key Design Features in the Transition Period. Discussion Paper. Geneva, WHO: 50.

- CCHI. 2008. Annual Report. Riyadh, Council Of Cooperative Health Insurance 148.

- CCHI. 2009a. Annual Report. Riyadh, Council Of Cooperative Health Insurance. 1: 156.

- CCHI. 2009b. Rules of Implementation of the Cooperative Health Insurance System 61331/30/1/ض. R. Cabinet. Riyadh, The Council of Cooperative Health Insurance. 2009.

- Central Department of Statistics & Information. 2008. Labour Force Survey. Labour Force Survey. Riyadh. 1: 90.

- Dhabi HAA. 2010. Heath Statistics 2010. from http://www.haad.ae.

- Elgazzar H, Raad F, et al. 2010. WHO PAYS? Out-of-Pocket Health Spending and Equity Implications in the Middle East and North Africa. HNP Discussion Paper. Washington, WHO.

- Elhout A. 2010. MedGulf Health Insurance Programs for Workers. Riyadh.

- General Secretariat of the Executive Council, Department of Planning & Economy. 2008. The Abu Dhabi Economic Vision 2030. Abu Dhabi, The Government of Abu Dhabi: 142.

- Gericke CA. 2004. Comparison of Health Care Financing Arrangements in Egypt and Cuba: Lessons for Health Reform in Egypt Global Medical Forum Middle East Summit. Beirut: 26.

- GOSI. 2008. The Annual Report. Riyadh, GOSI. 30: 171.

- Gottret P, Schieber G. Health Financing Revisited A Practioner’s Guide. Washington DC: The World Bank; 2006. [Google Scholar]

- Government S. 1992. Basic Law of Governance. Royal Order No (A/91) S. Government, Umm al-Qura Gazette No 3397 31.

- Hediger V, Lambert T, et al. Private Solutions for Health Care in the Gulf. McKinsey Quarterly New York: McKinsey & Company; 2007. p. 10. [Google Scholar]

- Hsiao WC. Why is a systemic view of health financing necessary? Health Aff. 2007;26(4):950–961. doi: 10.1377/hlthaff.26.4.950. [DOI] [PubMed] [Google Scholar]

- Kaufmann D, Kraay A, et al. 2009. Governance Matters VIII: Aggregate and Individual Governance Indicators, 1996-2008. SSRN eLibrary.

- Koornneef EJ, Robben PBM, et al. Health system reform in the Emirate of Abu Dhabi, United Arab Emirates. Health Policy. 2012;108(2):115. doi: 10.1016/j.healthpol.2012.08.026. [DOI] [PubMed] [Google Scholar]

- Kutzin J. A descriptive framework for country-level analysis of health care financing arrangements. Health Policy. 2001;56(3):171–204. doi: 10.1016/s0168-8510(00)00149-4. [DOI] [PubMed] [Google Scholar]

- Marius. 2011. Kuwait National Healthcare System Transition Underway. Kuwait: 8.

- McIntyre D. 2007. Learning from Experience: Health Care Financing in Low- and Middle-Income Countries. Geneva, Global Forum for Health Research.

- Mills A. 2007. Strategies to Achieve Universal Coverage: Are There Lessons from Middle Income Countries?: 46.

- Ministry of Economy and Planning. 2008. Achievement of Development Plan, Facts and Figures. Achievement of Development Plan, Facts and Figures. Riyadh, Ministry of Economy and Planning 1: 378.

- Ministry of Health. 2011. Policies & Strategic Direction: Ministry of Health Direction “Bahrain” Manama, Kingdom of Bahrain: 20.

- Ministry of Health Oman. 2006. The National Strategic Plan. Muscat Ministry of Health Sultanate Oman: 351.

- Ministry of Health Qatar. National Health Strategy. Doha: Supreme Council of Health; 2011. p. 306. [Google Scholar]

- MOH. 1995. Annual Statistical Report Riyadh, MOH: 285.

- MOH. 2003. p. 335. Annual Statistical Report Riyadh, MOH. 1.

- MOH. 2007. Health Indicators. M. O. Health. Riyadh, Ministry of Health.

- MOH. 2008. Annual Statistical Report Riyadh, Ministry of Health: 338.

- Mufti MH. 2000. Healthcare Development Strategies in the Kingdom of Saudi Arabia. Kluwer Academic/ Plenum Publishers.

- Relman DA. 2007. A Second Opinion: Rescuing America’s Health Care New York, Public Affairs.

- Schieber GJ. 2005. Health Financing Issues in the Kingdom of Saudi Arabia. 1st International Conference in Health Economics & Endowment. Riyadh, King Faisal Specialist Hospital and Research Centre.

- Sekhri N, Savedoff W. Private health insurance: implications for developing countries. Bull World Health Organ. 2005;83:8. [PMC free article] [PubMed] [Google Scholar]

- Sekhri N, Savedoff W, et al. 2005. p. 35. Regulating Private Health Insurance to Serve the Public Interest: Policy Issues for Developing Countries. World Health Organization Discussion Paper Number 3.

- Shah N. 2009. The Management of Irregular Migration and its Consequence for Development: Gulf Cooperation Council. ILO Asian Regional Programme on Governance of Labour Migration: Working Paper No. 19 Geneva, International Labour Organization: 28.

- Sturm M, Strasky J, et al. 2008. The Gulf Cooperation Council Countries: Economic Structures, Recent Developments, and Role in the Global Economy. Occasional Paper Series. Frankfurt, European Central Bank. 92: 77.

- Supreme Council of Health. 2011. Qatar National Health Accounts—1st Report Years 2009 & 2010: A Baseline Analysis of Health Expenditure and Utilization Doha, Supreme Council of Health: 66.

- Tawuniya. 2010. Prodcuts. Retrieved 24th May, 2010, from www.Tawuniya.com.sa.

- The World Bank. 2009. World Development Indicators 2009. World Development Indicators. T. W. Bank. Washington, DC, World Bank 1.

- The World Bank. 2010. Data, Saudi Arabia. Retrieved 22/09/2010, 2010, from http://data.worldbank.org/country/saudi-arabia.

- The World Bank, WHO. Guide to Producing National Health Accounts with Special Applications for Low-Income and Middle-Income Countries. Geneva: WHO; 2003. p. 309. [Google Scholar]

- UNDP. 2007. UNESCO Institute for Statistics. Human Development Report New York, United Nation.

- Wang H, Switlick K. In: Health Insurance Handbook: How To Make it Work. Connor C, Wang H, et al., editors. Bethesda, MD: Health Systems 20/20 project, Abt Associates In; 2010. p. 96. [Google Scholar]

- WHO. The Establishment and Use of Dedicated Taxes for Health. Geneva: WHO; 2004. p. 80. [Google Scholar]

- WHO. Country Cooperation Strategy for WHO and Bahrain 2005–2010. Geneva: WHO; 2006a. p. 63. [Google Scholar]

- WHO. Country Cooperation Strategy for WHO and Kuwait 2005–2009. Geneva: WHO; 2006b. p. 49. [Google Scholar]

- WHO. Country Cooperation Strategy for WHO and Oman 2005–2009. Geneva: WHO; 2006c. p. 64. [Google Scholar]

- WHO. Country Cooperation Strategy for WHO and Qatar 2005–2009. Geneva: WHO; 2006d. p. 56. [Google Scholar]

- WHO. Country Cooperation Strategy for WHO and the United Arab Emirates 2005–2009. Geneva: WHO; 2006e. p. 51. [Google Scholar]

- WHO. Health System Profile, Bahrain Regional Health System Observatory. Geneva: WHO; 2006f. p. 64. [Google Scholar]

- WHO. Health System Profile, Kuwait Regional Health System Observatory. Geneva: WHO; 2006g. p. 60. [Google Scholar]

- WHO. Health System Profile, Oman. Geneva: Regional Health System Observatory. WHO; 2006h. p. 77. [Google Scholar]

- WHO. Health System Profile, Qatar. Geneva: Regional Health System Observatory. WHO; 2006i. p. 56. [Google Scholar]

- WHO. Health System Profile, United Arab Emirates. Geneva: Regional Health System Observatory. WHO; 2006j. p. 48. [Google Scholar]

- WHO. World Health Statistics 2009. Geneva: Wold Health Statistics. WHO; 2009. p. 149. [Google Scholar]

- WHO. Global Health Expenditure Database. Geneva: WHO; 2010a. 2010. [Google Scholar]

- WHO. Heavy Reliance on Out Of Pocket Expenditure Leads to Financial Barriers for Pool. Geneva: WHO; 2010b. p. 1. [Google Scholar]

- WHO. National Expenditure on Health. Kuwait: World Health Organization, National Health Accounts Series, WHO; 2010c. p. 7. [Google Scholar]

- WHO. National Expenditure on Health. Oman: National Health Accounts Series, WHO; 2010d. p. 7. [Google Scholar]

- WHO. National Expenditure on Health. Qatar: National Health Accounts Series, WHO; 2010e. p. 7. [Google Scholar]

- WHO. National Expenditure on Health. Saudi Arabia: World Health Organization, National Health Accounts Series, WHO; 2010f. p. 7. [Google Scholar]

- WHO. National Expenditure on Health. United Arab Emirates: National Health Accounts Series, WHO; 2010g. p. 7. [Google Scholar]

- WHO. National Expenditure on Health. Bahrain: World Health Organization, National Health Accounts Series, WHO; 2010h. p. 7. [Google Scholar]