Summary

Quantifying the variability in the delivery of ecosystem services across the landscape can be used to set appropriate management targets, evaluate resilience and target conservation efforts. Ecosystem functions and services may exhibit portfolio‐type dynamics, whereby diversity within lower levels promotes stability at more aggregated levels. Portfolio theory provides a framework to characterize the relative performance among ecosystems and the processes that drive differences in performance.

We assessed Pacific salmon Oncorhynchus spp. portfolio performance across their native latitudinal range focusing on the reliability of salmon returns as a metric with which to assess the function of salmon ecosystems and their services to humans.

We used the Sharpe ratio (e.g. the size of the total salmon return to the portfolio relative to its variability (risk)) to evaluate the performance of Chinook and sockeye salmon portfolios across the west coast of North America. We evaluated the effects on portfolio performance from the variance of and covariance among salmon returns within each portfolio, and the association between portfolio performance and watershed attributes.

We found a positive latitudinal trend in the risk‐adjusted performance of Chinook and sockeye salmon portfolios that also correlated negatively with anthropogenic impact on watersheds (e.g. dams and land‐use change). High‐latitude Chinook salmon portfolios were on average 2·5 times more reliable, and their portfolio risk was mainly due to low variance in the individual assets. Sockeye salmon portfolios were also more reliable at higher latitudes, but sources of risk varied among the highest performing portfolios.

Synthesis and applications. Portfolio theory provides a straightforward method for characterizing the resilience of salmon ecosystems and their services. Natural variability in portfolio performance among undeveloped watersheds provides a benchmark for restoration efforts. Locally and regionally, assessing the sources of portfolio risk can guide actions to maintain existing resilience (protect habitat and disturbance regimes that maintain response diversity; employ harvest strategies sensitive to different portfolio components) or improve restoration activities. Improving our understanding of portfolio reliability may allow for management of natural resources that is robust to ongoing environmental change.

Keywords: diversity, ecosystem, geomorphology, management, portfolio effect, Sharpe ratio, stability, watersheds

Short abstract

Portfolio theory provides a straightforward method for characterizing the resilience of salmon ecosystems and their services. Natural variability in portfolio performance among undeveloped watersheds provides a benchmark for restoration efforts. Locally and regionally, assessing the sources of portfolio risk can guide actions to maintain existing resilience (protect habitat and disturbance regimes that maintain response diversity; employ harvest strategies sensitive to different portfolio components) or improve restoration activities. Improving our understanding of portfolio reliability may allow for management of natural resources that is robust to ongoing environmental change.

Introduction

Quantifying the delivery of ecosystem services to humans is of increasing importance for assessing trade‐offs among management alternatives and targeting conservation efforts. Due to the hierarchical organization of ecosystems (Levin 1992), many ecosystem services are likely to be supported through dynamics analogous to those of investment portfolios, where the reliability of these services is greater at coarser scales or higher levels of aggregation than they are in their component parts. Thus, portfolio theory (Markowitz 1952), with a long history in the economics literature, provides a framework and analytical tools for characterizing the relative performance among ecosystems in service delivery (magnitude and reliability) and the processes that drive differences among ecosystems (Koellner & Schmitz 2006).

Portfolio theory links the risk and return of individual assets to the risk and return associated with a portfolio of assets (Figge 2004). Financial analysts use portfolio theory to manage investments in financial assets (e.g. stocks, bonds) or commodities (e.g. wheat, oil) such that they achieve a desired balance between financial gain and risk to the investor. In an ecological context, assets may be genes, populations, species, landscapes or ecosystems. In the classic example of stability–diversity relationships in grasslands (Tilman 1996), assets are plant species that are valued by their biomass and the portfolio return is the community‐level biomass.

Here we focus on portfolio performance which is the return of the portfolio explicitly adjusted for portfolio variance (risk). The portfolio variance is partitioned between variance and covariance among assets. For a given portfolio return, higher portfolio variance is less desirable (‘more risky’). While the risk of an individual asset is the variance of its return, the risk of a portfolio can be quite different from that of its individual assets (Elton et al. 2007). Although increasing variance in the assets will increase the variance of the portfolio, composition and dynamics of assets can mediate the variance of a portfolio in three ways. First, the average across randomly fluctuating assets will reduce the variance of the aggregate assuming they are not perfectly correlated (i.e. stastical averaging, Doak et al. 1998). Secondly, the average across assets will have lower variance if the assets are weakly or negatively correlated (Doak et al. 1998). Finally, the evenness (proportional distribution) of assets in a portfolio modulates the effect of statistical averaging and covariance on portfolio variance (Doak et al. 1998; Figge 2004). If assets are asynchronous, increasing evenness will decrease the variance the portfolio returns, but evenness will have no effect on portfolios with positively synchronous assets. These three mechanisms reduce ‘unsystematic’ risks – those risks that are specific to certain assets but not others (Sharpe 1964). However, portfolio diversification cannot reduce systematic (Sharpe 1964) or aggregate (Lintner 1965) risk where all assets are vulnerable to large‐scale events (e.g. wide‐spread natural disasters, large‐scale shifts in ocean‐climate conditions).

Portfolio theory has been applied in several fisheries contexts including the role of population diversity in fishery reliability (Schindler et al. 2010), developing fisheries management strategies (Edwards, Link & Rountree 2004), and as a risk evaluation tool (Sethi 2010). Other recent applications of portfolio theory include optimizing conservation strategies under climate uncertainty (Ando & Mallory 2012), evaluating spatial management trade‐offs (Halpern et al. 2011) and assessing the spatial and temporal buffering of population dynamics (Thorson et al. 2014).

Pacific salmon Oncorhynchus spp. are important components of the social–ecological systems on the west coast of North America: they support fisheries, act as ecosystem engineers, and provide energy and nutrient subsidies to freshwater and riparian ecosystems (Gende et al. 2002; Schindler et al. 2003). Anadromous Pacific salmon are found across a diverse range of freshwater habitats from central California to the Arctic Circle. Locally adapted populations (Waples, Pess & Beechie 2008) are maintained at fine spatial scales due to strong natal homing (Dittman & Quinn 1996). Their extensive life‐history diversity includes substantial variation in the duration of freshwater and marine life‐history phases and variation in migration timing within and among species (Groot & Margolis 1991). This life‐history diversity is reflected in the weakly correlated dynamics of Pacific salmon (Peterman et al. 1998), even among populations within individual watersheds (Rogers & Schindler 2008), which is important for providing reliable returns that benefit both humans and ecosystems.

The magnitude of variance dampening due to population diversity has been assessed for several salmon ecosystems. In Bristol Bay, variation in the total number of returning sockeye salmon O. nerka would be over two times greater without the existing population and life‐history diversity (Schindler et al. 2010). Variation in fall Chinook salmon O. tshawytscha returns to Central Valley, California (Carlson & Satterthwaite 2011), and spring Chinook productivity in the Snake River, Columbia Basin (Moore et al. 2010), are also lower at the aggregate rather than population level. Compared to sockeye portfolios from pristine habitats, variance dampening at regional levels is reduced and has been declining over time (Carlson & Satterthwaite 2011).

To identify the effects of geomorphic complexity, anthropogenic impacts and between species life‐history diversity on portfolio performance, we compiled data on Chinook and sockeye salmon populations across the west coast of North America and assembled portfolios based upon watersheds. Using a common measure of risk‐adjusted performance (Sharpe ratio, a measure of portfolio return in relation to portfolio risks), we addressed the following questions:

Is there a relationship between salmon portfolio performance, geomorphic complexity and human impact on the landscape?

Do sources of portfolio risk (variance and covariance of salmon population complexes) differ among species and are they related to human impacts on watersheds?

Materials and methods

Salmon Data

We assembled Chinook and sockeye salmon total run and spawner abundance data from watersheds across the west coast of North America at the finest spatial resolution available. Data for Chinook salmon were available from California, the Columbia River Basin, the transboundary region (northern British Columbia and southeast Alaska), Alaska and the Canadian Yukon. Sockeye salmon data were available from Washington, British Columbia and Alaska. Wherever possible, and especially for regions with high harvest pressure, we used total run (catch plus escapement) data. For Chinook salmon in the Pacific Northwest and California, we instead used spawner abundance estimates as these were the most universally collected data and harvest rates tend to be low in these regions. Population sizes were indexed to their year of adult migration to freshwater for spawning because we were interested in the reliability of fishery harvests and annual energy subsidies to ecosystems. These data sets include fish of both hatchery and wild origin. A complete list of data locations, sources and types is provided in Table S6 (Supporting information). We did not include Chinook salmon portfolios from the Oregon and Washington coast, Puget Sound and British Columbia. These populations are harvested in mixed stock fisheries, and we were unable to obtain reliable estimates of total run size to individual watersheds.

Salmon Portfolio Assembly

The performance of a salmon portfolio is expected to vary with the landscape and genetic diversity it incorporates as well as the time period over which performance is measured. We explored three different criteria for defining an asset (as a watershed, genetic unit or management unit) and assembled portfolios for each criterion along a north to south latitudinal gradient. The value of each asset was represented by the total salmon run from one or more salmon populations within the watershed, genetic or management unit. We only discuss watershed‐based results here, while the very similar results for genetic and management units are included in the supporting information. We restricted our analyses to the period 1985–2005 to obtain the greatest number of time series across regions.

For Chinook salmon, we evaluated salmon watershed portfolios at two spatial scales. We first evaluated 13 salmon portfolios (Table S1, Supporting information) where the total watershed area of the portfolio ranged between 2770 and 286 390 km2 (Table 1) and the number of assets within each portfolio ranged from 1 to 23. We then further aggregated these data into six portfolios ranging in area from 69 231 to 670 000 km2 and with one to 47 assets (Table S1, Supporting information). For sockeye salmon, we evaluated five watershed portfolios, ranging in area from 18 477 to 233 000 km2, containing five to 10 assets (Table S2, Supporting information). The watershed area of the portfolio and of individual assets differed in size due to both natural variation and differences in the spatial scale of data collection. For some watershed assets, the total run reflected a single data set, while for other basins, this was the summation of several data sets if multiple populations were present within the watershed. We included only watersheds for which there were continuous data available to estimate variance and covariance with other watersheds in a portfolio.

Table 1.

The total watershed area for each salmon watershed portfolio. Fine‐scale Chinook watershed portfolios are in standard font, and coarse‐scale Chinook watershed portfolios are in italics

| Species | Portfolio | Watershed area (km2) |

|---|---|---|

| Chinook | Canadian Yukon | 286 390 |

| Kuskokwim | 118 000 | |

| Bering | 35 701 | |

| Peninsula/Kodiak | 2770 | |

| Central AK | 66 461 | |

| Southeast AK | 98 718 | |

| Lower Columbia | 44 273 | |

| Middle Columbia | 76 852 | |

| Upper Columbia | 270 171 | |

| Snake | 279 174 | |

| Klamath | 41 377 | |

| Sacramento | 68 596 | |

| San Joaquin | 83 862 | |

| Canadian Yukon | 286 390 | |

| Bering | 153 720 | |

| Gulf of Alaska | 69 231 | |

| Southeast AK | 98 718 | |

| Columbia | 670 000 | |

| California | 193 835 | |

| Sockeye | Bristol Bay | 82 254 |

| Gulf of Alaska | 67 725 | |

| Transboundary | 126 204 | |

| Fraser | 233 000 | |

| Washington | 18 477 |

Salmon Portfolio Performance

We evaluated the performance of salmon portfolios from 1985 to 2005 using a derivation of the Sharpe ratio (Sharpe 1994; Koellner & Schmitz 2006; Moore et al. 2010). This metric standardizes the portfolio return by its risk as determined by both the variance and covariance of the portfolio assets. Higher values of the ratio are desirable because they indicate greater reliability in the portfolio. Riskier portfolios (higher variance) are only preferred using this metric when there is also high mean performance to compensate for lower reliability (Koellner & Schmitz 2006). The Sharpe ratio, or the risk‐adjusted performance (θ, eqn (eqn 1)), of a portfolio is defined as the return on the portfolio (U p) minus a risk‐free index (R f) and then divided by the standard deviation of portfolio variance (σp). We set R f equal to zero as in Moore et al. (2010).

| (eqn 1) |

The return on the portfolio U p (eqn (eqn 2), Elton et al. 2007) is the sum of the mean return μ (mean total run over all years) of each asset j weighted by the relative contribution X of the asset to the portfolio across the entire time period (total asset return across time period/total portfolio return).

| (eqn 2) |

The variance of the portfolio performance (, eqn (eqn 3), Elton et al. 2007) is the sum of the asset variance and covariance within the portfolio. The variance of the assets is the sum across the variance in each asset (variance of total run), , multiplied by it squared proportional contribution to the portfolio . The covariance within the portfolio is calculated as the covariance among each pair of assets (COVjk) weighted by the relative contribution of each asset to the portfolio (X j, X k).

| (eqn 3) |

To explore the different mechanisms determining portfolio performance, we evaluated the relative importance of salmon run variance and salmon run covariance to portfolio risk by calculating the relative proportion of the portfolio variance due to each factor. The salmon abundance data were ln (x + 1)‐transformed to meet assumptions of normality prior to calculating the Sharpe ratios.

Watershed Characteristics

Watershed features were characterized via the Riverscape Analysis Project database (RAP, Whited et al. 2012) that includes a wide array of watershed descriptors derived from remote sensing. We included the following RAP metrics in our analyses (with a single value per portfolio): total watershed area, mean watershed elevation, number of mid‐channel nodes, number of tributary nodes per drainage line, floodplain area, lake area and glacier area. Nodes are points of channel separation or confluence (e.g. number of nodes increase with channel complexity). Watershed area was calculated as the entire drainage area upstream of the ocean confluence (e.g. Fraser River Basin), confluence with a border (e.g. Canadian Yukon) or other major tributaries (e.g. Snake River is upstream of its confluence with the Columbia River) and included inaccessible habitat. In addition, we used two descriptors of anthropogenic impacts: the number of dams present and a human footprint index (HPI). Dam number includes all barriers, from earth dams with little storage capacity to large mainstem dams. The HPI was derived by Sanderson et al. (2002) and incorporated data sets reflecting population density, land transformation, accessibility and electrical power infrastructure. In our analyses, we used the mean HPI value across all grid cells in our watersheds.

We used a principal components analysis (PCA) on ln (x + 1)‐transformed watershed metrics to characterize watersheds by a reduced number of independent variables describing the dominant gradients of variation. We first conducted a PCA on our 13 Chinook salmon portfolio watersheds using all nine watershed variables. We tested for axis significance using the broken stick test (Legendre & Legendre 2012). For the significant axes, we evaluated the variance in the original variables explained by each axis using the structure coefficients. We removed all variables which did not have structure coefficients <|0·7| on the significant axes and then repeated the PCA. We did not conduct PCAs for the coarser scale Chinook or the sockeye salmon portfolios because of the small number of watersheds relative to the number of variables.

Watershed Condition and Salmon Portfolio Performance

We assessed the correlation between salmon portfolio performance and watershed characteristics using Spearman's rank correlations. We calculated the correlation between each composite variable (significant PC axes) and the Sharpe ratio (fine‐scale Chinook portfolios only). In addition, we separately calculated the correlation between each watershed metric and the Sharpe ratio (all Chinook and sockeye salmon portfolios).

All analyses were conducted using R (R Core Team 2012) including the libraries ‘vegan’ (Oksanen et al. 2012), ‘reshape’ (Wickham 2007) and ‘PBSmapping’ (Schnute et al. 2013) as well as ‘biostats’ (K. McGarigal, http://www.umass.edu/landeco/teaching/multivariate/labs/multivariate_labs.html).

Results

Salmon Portfolio Performance

Chinook salmon

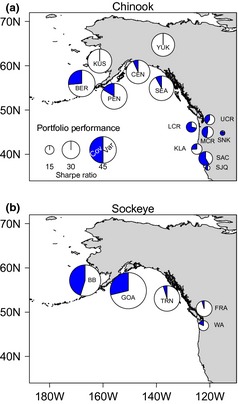

We observed a strong, positive latitudinal gradient in salmon portfolio performance (Fig. 1a, Table S3, Supporting information). The best Chinook salmon portfolios were in Alaskan watersheds, with Sharpe ratios approximately 2·5 times greater than those in the contiguous U.S. In general, asset variance in the Alaskan portfolios contributed more to portfolio risk than the covariance among assets although overall risk was low. This, however, may be in part because some of these watersheds had only one (e.g. Canadian Yukon, Kuskokwim) or few assets (e.g. Bering) that may exhibit a portfolio effect internally (i.e. derived from finer‐scale complexity, Schindler et al. 2010). In general, Columbia River and Californian watershed portfolios performed more poorly and, with the exception of the Klamath‐Trinity watershed, showed a much higher percentage of portfolio risk derived from strong positive covariances among assets. For example, 87% of the portfolio variance in the Snake River portfolio was due to strong positive asset covariance (i.e. the assets tend to boom and bust in unison).

Figure 1.

Risk‐adjusted performance (Sharpe ratio) of Chinook (a) and sockeye (b) salmon portfolios across North America from 1985 to 2005. Bubble size indicates relative size of the Sharpe ratio. Bubble fill indicates the proportional contribution of asset variance (white) and asset covariance (blue) to the total portfolio variance (eqn (eqn 3) in text). Portfolio abbreviations for Chinook are as follows: BER = Bering, CEN = Central Alaska, KLA = Klamath, KUS = Kuskokwim, LCR = Lower Columbia River, MCR = Middle Columbia River, PEN = Alaska Peninsula/Kodiak, SAC = Sacramento, SEA = SE Alaska, SJQ = San Joaquin, SNK = Snake, UCR = Upper Columbia River, YUK = Canadian Yukon. Portfolio abbreviations for sockeye are as follows: BB = Bristol Bay, FRA = Fraser River, GOA = Gulf of Alaska, TRN = Transboundary, WA = Washington state.

Chinook salmon assets aggregated to coarse regional scales produced a similar latitudinal trend in portfolio performance (Fig. S1, Table S3, Supporting information). Alaskan portfolios performed 2–4 times better than the Columbia River and Californian portfolios. Alaskan portfolios varied in the contributions of covariance to portfolio risk (2·6–34·3%, excluding the Canadian Yukon), while the Columbia River and Californian portfolio's risk was dominated by strong positive covariance within the portfolio (73·7% and 90·8%, respectively).

Sockeye salmon

Sockeye salmon portfolio performance also exhibited a distinct latitudinal gradient (Fig. 1b, Table S4, Supporting information) with greater performance at higher latitudes. The performance of the best portfolio, Gulf of Alaska, was 3·6 times greater than the weakest performing portfolio, from Washington state. Covariance contributed substantially more to portfolio risk in the Bristol Bay (45·1%), Gulf of Alaska (28·8%), and Washington (17·7%) portfolios than in the Transboundary (4·7%) and Fraser River (4·6%) portfolios. Overall risk, however, was highest for the Fraser River and Washington portfolios.

Watershed Condition and Salmon Portfolio Performance

Chinook salmon

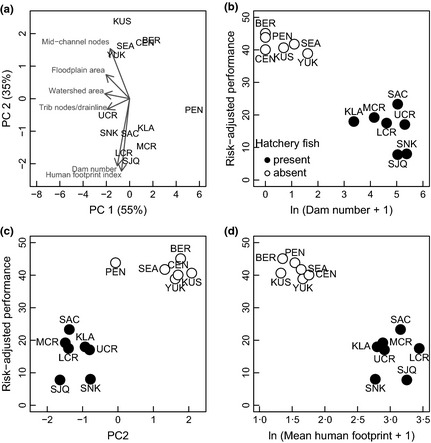

A PCA using six watershed characteristics described 90% of the variation among Chinook salmon watersheds with two significant axes (Fig. 2a). The first PC axis (55% of the total variation) separated the Alaska Peninsula portfolio (small area) from all other watersheds. The second PC axis (35% of total variation) differentiated portfolios based upon watershed complexity (floodplain area and mid‐channel nodes) and anthropogenic impact (dam number and mean human footprint value). Higher latitude portfolios were associated with greater watershed complexity, while lower latitude portfolios were associated with larger anthropogenic impacts (Fig. 2a). Three variables (mean watershed elevation, lake area and glacier area) with low structure correlations in the initial analysis were not used in this final PCA.

Figure 2.

Watershed characteristics of fine‐scale Chinook salmon portfolios and their relationship to portfolio performance. (a) Principal components ordination using the first two axes from a PCA of Chinook salmon portfolio watersheds. Dashed arrows are the loadings of watershed characteristics. Portfolio abbreviations are as in Fig. 1. (b–d) Each point represents a portfolio where filled dots indicate that hatchery fish are present and unfilled dots indicate they are absent. Fine‐scale Chinook salmon portfolio Sharpe ratios are correlated to the number of dams in the portfolio watershed (b), PC 2 (c), and mean human footprint index value (d).

Chinook salmon portfolio performance was negatively associated with the degree of anthropogenic impact within a watershed for the fine‐scale portfolios. Risk‐adjusted performance was negatively correlated with the number of dams in the portfolio (Fig. 2b, Spearman's rank correlation coefficient (r s) = −0·89, P < 0·001) and mean human footprint (Fig. 2d, r s = −0·81, P < 0·005). Additionally, fine‐scale Chinook portfolios were positively correlated with PC 2 (Fig. 2c, r s = 0·73, P < 0·01) where positive PC 2 values are associated with watershed complexity and negative PC 2 values are associated with human impact. Although total glacier area in the watershed was excluded from the PCA analysis, alone it showed a significant correlation with the Sharpe ratio (Fig. S2, Supporting information, r s = 0·79, P < 0·005) with high glacier area associated with high‐performing Alaskan portfolios. Watershed area was not significantly correlated with portfolio performance nor were any other measures of watershed complexity (Table S5, Supporting information).

Sockeye salmon

Sockeye salmon portfolio performance was negatively, but not significantly, correlated with mean HPI (r s = −0·90, P > 0·05) and the number of dams (r s = −0·87, P > 0·05) in watersheds. There were positive, but non‐significant, trends between sockeye salmon portfolio performance and measures of geomorphic complexity including the number of mid‐channel nodes (r s = 0·90, P > 0·05) and total floodplain area (r s = 0·90, P > 0·05). However, we interpret these relationships with caution due to the small number of portfolios considered. See Table S5 (Supporting information) for all performance – watershed variable correlations.

Discussion

Chinook and sockeye salmon portfolios were more reliable (higher Sharpe ratios) at higher latitudes. The inverse correlation of performance with high anthropogenic impact to watersheds (e.g. dams, land use) suggests that intact landscapes produce portfolio dynamics that support the reliable delivery of salmon to ecosystems and people. Chinook and sockeye salmon portfolio also spanned similar ranges of reliability across their habitat range. Previous assessments of Chinook salmon portfolios were from highly degraded ecosystems where life history and genetic diversity have been substantially decreased through habitat loss (McClure et al. 2008) and hatcheries (Naish et al. 2008). Here, however, we saw large differences in reliability of portfolio performance among pristine and degraded watershed portfolios. There was over a fivefold difference in performance between the highest and lowest performance Chinook portfolios, and better performance at high latitudes was driven by both greater magnitude returns and reduced portfolio variance. In high‐latitude Chinook portfolios, portfolio variance was derived primarily from variance in individual assets. For those portfolios for which we had multiple assets, this may indicate that intact habitat produces sufficient response diversity (sensu Elmqvist et al. 2003) among watersheds to reduce covariance. In contrast, poor‐performing Chinook salmon portfolios more often had portfolio variance driven by strong positive covariation among assets, indicating that anthropogenic drivers may synchronize populations (e.g. loss of specific habitats and their populations; habitat homogenization reducing response diversity; reduced genetic diversity due to hatcheries).

There was also substantially greater performance at higher latitudes among the five sockeye salmon portfolios, and high‐latitude portfolios also showed both greater returns and lower variance. The source of risk differed in the two highest performing portfolios, Bristol Bay (equal variance and covariance) and Gulf of Alaska (variance dominated), conveying that neither source of risk is inherently worse for portfolio reliability. Ocean entry locations for assets in Bristol Bay portfolio were much closer geographically than those for the Gulf of Alaska which may explain the relative importance of covariation among assets.

Chinook and sockeye salmon have the greatest life history and genetic diversity of the Pacific salmon species (Waples et al. 2001), yet have differences in their life‐history strategies (stream vs. lake rearing, ocean duration, etc.) which could influence portfolio performance or its sensitivity to changes in environmental conditions. Greater life‐history diversity buffers populations from extreme fluctuations (Greene et al. 2010), and accounting for life‐history diversity increases the magnitude of observed portfolio effects (e.g. age structure, Schindler et al. 2010). However, across their North American range, we calculated a similar range of portfolio performances and no clear differences in the source of portfolio risk.

Chinook salmon portfolios from the Gulf of Alaska were the highest performing portfolio in our analysis. This may both reflect the diversity of intact habitats included in this portfolio and the geographically distant ocean entry locations, which adds further potential for response diversity among assets. The high‐performing Canadian Yukon Chinook portfolio contained one asset, and its stability could be produced by underlying portfolio dynamics from its many subwatersheds (i.e. weak covariation within the population complex, e.g. Rogers & Schindler 2008; Schindler et al. 2010) for which we do not have fine‐scale data. Columbia River Basin Chinook portfolios from the lower, middle and upper Columbia had two times higher risk‐adjusted performance values than the Snake River where increased synchronization and decline in portfolio performance have been previously identified (Moore et al. 2010). Higher performances in other Columbia River portfolios may be due to a greater evenness among population complexes with different life‐history types (fall and spring returns; ocean and stream‐type rearing) and fewer major dams to pass for the lower and middle river populations.

The Bristol Bay sockeye portfolio demonstrated high reliability as shown in previous research (e.g. Schindler et al. 2010) but was in fact lower than the Gulf of Alaska sockeye portfolio. Gulf of Alaska sockeye integrated over three very different watershed regions (Chignik, Kodiak Island, Copper River) each of which contain multiple rearing lakes and associated populations likely causing the substantial reduction in covariance among assets. The Fraser River portfolio performance was half to two‐thirds as high as the Alaskan portfolios, and high portfolio variance was due almost entirely to the high variance in individual assets. Peterman et al. (1998) showed overall weaker patterns of survival rate covariation among Fraser River population complexes compared to among Bristol Bay population complexes. This weaker covariation in combination with the 4‐year cyclic behaviour of major Fraser population complexes may drive the relatively high importance of asset variance for the overall portfolio variance.

We found that the performance of Chinook and sockeye salmon portfolios was negatively correlated with the extent of anthropogenic development of watersheds (i.e. number of dams, mean human footprint). We cannot determine whether this a cause–effect relationship. However, anthropogenic activities have substantially reduced Pacific salmon life history and genetic diversity (McClure et al. 2008; Naish et al. 2008) and led to widespread population extirpations (Gustafson et al. 2007), thus likely compromising portfolio reliability at lower latitudes. Surprisingly, variables describing the geomorphic complexity of watersheds were not strongly correlated with Chinook salmon portfolio performance. One exception was a significant correlation with glacier area, but this was also strongly associated with latitude. One possibility is that across the large latitudinal gradient included in our analyses, regions differ in the watershed features that are important drivers of life‐history diversity and population dynamics leading to no consistent predictors of portfolio performance. Alternatively, it is possible that human development of watersheds and subsequent effects on salmon mask any potential geomorphic effects on portfolio buffering. The scale at which watershed variables are characterized, especially for remotely sensed data, also may not match the scale with which salmon interact in with their environment. Therefore, coarse measures of human impact such as dam number, which reduce geomorphic complexity, may correlate more at our analysis scale. While some watershed variables were associated with sockeye salmon portfolio performance, our inference is limited due to the small number of portfolios.

A central challenge to performing the analyses presented here was in synthesizing comparable data among regions. We used total run data wherever possible, but we used spawning numbers for Columbia Basin and California Chinook populations. Many of these populations are listed under the Endangered Species Act (McClure et al. 2003; Good, Waples & Adams 2005) and are subjected to limited harvest pressure. This is not the case for all populations, however, and in‐river recreational harvest can be substantial. We also did not include any populations with missing data during the focal time period to avoid a portfolio metric with asset variance calculated across varying time‐series lengths and pairwise covariance calculations based on different subsets of the included populations. If these excluded populations had low or negative correlations to the included populations or had large relative abundance with low variance, we might have underestimated portfolio performance. Nonetheless, populations with the most continuous monitoring generally tend to be the most abundant populations, thereby making this a reasonable assumption.

The spatial scale of data collection likely affected the properties characterized by the Sharpe ratio. In general, data were collected at finer spatial scales at more southern latitudes (e.g. Chinook in the Snake River) although there are exceptions (e.g. Chinook in the John Day River). This likely occurred due to a combination of management scale, remoteness (accessibility for data collection) and degree of conservation concern. The number of assets in the portfolio did not lead to a systematic pattern in portfolio performance (Figs S3–4, Supporting information). We saw the highest levels of covariance in portfolios with the most assets (Figs S3–4, Supporting information); however, for Chinook, these portfolios also are impacted by many potential synchronizing mechanisms. In regions where there were fewer assets, they represented a broader spatial extent and likely integrated over a greater number of populations. This could have resulted in reduced variance of the assets because they themselves were governed by finer spatial scale portfolio dynamics.

Our analyses did not differentiate between wild and hatchery origin salmon in the portfolios. In some cases, returns are a mixture of wild and hatchery origin individuals and there are limited data to evaluate the relative contribution of each to the total. In other cases, wild and hatchery fish are estimated separately (e.g. Copper River sockeye). In the Chinook salmon portfolios we considered here, those that included some level of hatchery production in the returns had low performance and high levels of human impact (Fig. 2). The inclusion of hatchery assets could alter portfolio performance through several mechanisms. Artificial propagation may reduce genetic diversity and life‐history diversity within in a single hatchery population (Naish et al. 2008), potentially reducing its response diversity, and therefore increase the variability of year to year returns. Straying of hatchery fish into natural areas may reduce genetic and life‐history variation among populations within a portfolio by both increasing synchrony in their population dynamics and increasing the correlation of returns demographically. In areas with threatened and endangered populations, hatchery populations are often substantially larger than wild populations also reducing portfolio evenness. As hatchery production is likely less affected by variation in the freshwater environment and by the parental population size, however, it could decouple the portfolio performance from the freshwater environment and instead variation in performance would be more dependent on ocean conditions. Depending on the time period considered, hatchery assets may actually improve portfolio performance in degraded watersheds if ocean conditions are productive. Thus, in our measure of portfolio performance, hatchery fish influence both the magnitude of the portfolio return and the risk.

The portfolios we assessed included watersheds that spanned a substantial range in size. Larger watersheds are likely to integrate across more complexity in the landscape (Wiens 1989) and have the potential to produce greater biological diversity than small systems. We reduced differences among portfolio watershed areas as much as possible, but natural variation in watershed size and differences in the scale of data collection determined minimum watershed areas. The relationship between watershed area and portfolio performance was not significant, and both the Canadian Yukon and Alaska Peninsula had high performance indexes despite their dissimilar sizes. Assets were based upon watersheds, and consequently, they integrated over the life history and genetic diversity present within each watershed. Depending on the ecological, conservation or management question, salmon portfolios could be constructed based upon different criteria. We found similar latitudinal trends when we assessed portfolios based upon genetic structure or management regions (Tables S11–14, Figs S5–6, Supporting information).

The ecological and economic value of salmon runs depends on how reliable they are over time. For humans, wide‐ranging consumers and other beneficiaries that sample aggregates of salmon populations, the reliability of salmon yields derives from the portfolio performance of regional populations' complexes (Schindler et al. 2010, 2013). Developing a baseline for salmon portfolio performance is important for evaluating future management alternatives or to assess conservation outcomes. The natural variability in portfolio performance can be quantified in remote watersheds and then used as a benchmark to assess the status of portfolios from degraded watersheds. For all regions, periodic assessments of portfolio reliability could be used to track portfolio resilience and response to ongoing environmental change.

We used a metric of portfolio performance that allowed us to evaluate the relative importance of variance and covariance properties in the portfolio risk to better understand the process that govern the reliable delivery of this ecosystem service. In portfolios where positive covariance is the greatest source of risk, managers may focus on maintaining or restoring disturbance regimes that can promote response diversity and reduce asset synchrony. Similarly, carefully operating hatcheries to limit genetic homogenization may reduce population synchrony. In portfolios where asset variance is the greatest risk, managers may explore whether within asset response diversity may be enhanced through increasing habitat heterogeneity or maintaining the full life‐history diversity of the population (not heavily exploiting only one portion of the run). Furthermore, taking care to not overexploit weaker components of the portfolio at any given time may improve portfolio evenness on average and reduce the effects of asset variance over the long term.

The appropriate spatial and temporal resolution for evaluating portfolio dynamics in social–ecological systems remains unclear for most ecosystems. Here, we used annual data which reflect how both humans and ecosystems interact with and rely upon the seasonal pulse of salmon resources. Therefore, we are addressing the resilience of these portfolios to high‐frequency variability of disturbance regimes and ocean‐climate conditions. However, altering the temporal duration as well as the spatial and temporal resolution of our analyses could address resiliency to low‐frequency climate‐ocean or geomorphic processes. In turn, this would address salmon portfolio resilience on scales acted upon by eco‐evolutionary processes. Analyses of multicentury southwestern Alaska sockeye lakes showed low synchrony among these watershed level assets (Rogers et al. 2013). Pacific salmon portfolios may therefore have the capacity for resilience at multiple temporal scales and in turn promote ecosystem stability across different levels of organization and temporal duration. Developing meaningful measures of ecosystem performance is critical as we seek to maintain and conserve the processes that confer resilience upon ecosystems in face of ongoing environmental change. Last, given that salmon management in particular, and resource management in general, will continue to operate under substantial uncertainty in future responses to changing environmental conditions, maintaining high‐performing resource portfolios may prove to be an effective strategy for reliably delivering ecosystem services to people.

Data accessibility

Data were compiled from numerous sources. All data sources, points of contact, and links to web archives or reports containing the data are included in Table S6 (Supporting information).

Supporting information

Table S1–4. Watershed portfolios and performance metrics.

Table S5. Performance and watershed descriptor correlations.

Table S6. Data sources.

Table S7–14. Management and genetic portfolios and performance metrics.

Figure S1. Chinook salmon coarse‐scale Sharpe ratio map.

Figure S2. Chinook salmon portfolio performance and glacier area.

Figure S3–4. Watershed portfolio performance and asset number.

Figure S5–6. Management and genetic portfolio Sharpe ratio.

Appendix S1. Alternative portfolio methods.

Acknowledgements

Funding for this synthesis was provided by the Gordon and Betty Moore Foundation and the U.S. National Science Foundation Coupled Natural Human Systems Program. We thank Michael Webster for the encouragement to pursue it. We appreciate the assistance of many people who responded to our requests for data including: Brett Barkdull, Bill Bosch, Aaron Bosworth, Steve Cox‐Rogers, Anthony Fritts, Larry Gilbertson, Sue Grant, Steve Heinl, Tracey Hillman, Paul Hoffarth, Damon Holzer, Steve Latham, Maija Meneks, Todd Miller, Louise de Mestral Bezanson, Steve Moffitt, Michelle Moore, Andrew Murdoch, Chuck Parken, Jim Ruzycki, Jason Seals, Toz Soto, Adam St. Savior, Wayne Vandernaald, Joe Zendt. Two anonymous reviewers provided helpful comments.

References

- Ando, A.W. & Mallory, M.L. (2012) Optimal portfolio design to reduce climate‐related conservation uncertainty in the Prairie Pothole Region. Proceedings of the National Academy of Sciences of the United States of America, 109, 6484–6489. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Carlson, S.M. & Satterthwaite, W.H. (2011) Weakened portfolio effect in a collapsed salmon population complex. Canadian Journal of Fisheries and Aquatic Sciences, 68, 1579–1589. [Google Scholar]

- Dittman, A.H. & Quinn, T.P. (1996) Homing in Pacific salmon: mechanisms and ecological basis. Journal of Experimental Biology, 199, 83–91. [DOI] [PubMed] [Google Scholar]

- Doak, D.F. , Bigger, D. , Harding, E.K. , Marvier, M.A. , O'Malley, R.E. & Thomson, D. (1998) The statistical inevitability of stability‐diversity relationships in community ecology. American Naturalist, 151, 264–276. [DOI] [PubMed] [Google Scholar]

- Edwards, S.F. , Link, J.S. & Rountree, B.P. (2004) Portfolio management of wild fish stocks. Ecological Economics, 49, 317–329. [Google Scholar]

- Elmqvist, T. , Folke, C. , Nystrom, M. , Peterson, G. , Bengtsson, J. , Walker, B. & Norberg, J. (2003) Response diversity, ecosystem change, and resilience. Frontiers in Ecology and the Environment, 1, 488–494. [Google Scholar]

- Elton, E.J. , Gruber, M.J. , Brown, S.J. & Goetzmann, W.N. (2007) Modern Portfolio Theory and Investment Analysis, 7th edn John Wiley and Sons, Hoboken, NJ. [Google Scholar]

- Figge, F. (2004) Bio‐folio: applying portfolio theory to biodiversity. Biodiversity and Conservation, 13, 827–849. [Google Scholar]

- Gende, S.M. , Edwards, R.T. , Willson, M.F. & Wipfli, M.S. (2002) Pacific salmon in aquatic and terrestrial ecosystems. BioScience, 52, 917–928. [Google Scholar]

- Good, T.P. , Waples, R.S. & Adams, P. (editors). (2005) Updated status of federally listed ESUs of West Coast salmon and steelhead NOAA Tech. Memo, NMFS‐NWFSC‐66 , pp. 598 U.S. Dept. Commerce, Seattle, WA. [Google Scholar]

- Greene, C.M. , Hall, J.E. , Guilbault, K.R. & Quinn, T.P. (2010) Improved viability of populations with diverse life‐history portfolios. Biology Letters, 6, 382–386. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Groot, C. & Margolis, L. (1991) Pacific Salmon Life Histories. UBC Press, Vancouver, BC: [Google Scholar]

- Gustafson, R.G. , Waples, R.S. , Myers, J.M. , Weitkamp, L.A. , Bryant, G.J. , Johnson, O.W. & Hard, J.J. (2007) Pacific salmon extinctions: quantifying lost and remaining diversity. Conservation Biology, 21, 1009–1020. [DOI] [PubMed] [Google Scholar]

- Halpern, B.S. , White, C. , Lester, S.E. , Costello, C. & Gaines, S.D. (2011) Using portfolio theory to assess tradeoffs between return from natural capital and social equity across space. Biological Conservation, 144, 1499–1507. [Google Scholar]

- Koellner, T. & Schmitz, O.J. (2006) Biodiversity, ecosystem function, and investment risk. BioScience, 56, 977–985. [Google Scholar]

- Legendre, P. & Legendre, L. (2012) Numerical Ecology, 3rd edn Elsevier, Oxford, UK. [Google Scholar]

- Levin, S.A. (1992) The problem of pattern and scale in ecology. Ecology, 73, 1943–1967. [Google Scholar]

- Lintner, J. (1965) The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. The Review of Economics and Statistics, 47, 13–37. [Google Scholar]

- Markowitz, H. (1952) Portfolio selection. The Journal of Finance, 7, 77–91. [Google Scholar]

- McClure, M.M. , Holmes, E.E. , Sanderson, B.L. & Jordan, C.E. (2003) A Large‐Scale, Multispecies Status Assessment: anadromous Salmonids in the Columbia River Basin. Ecological Applications, 13, 964–989. [Google Scholar]

- McClure, M.M. , Carlson, S.M. , Beechie, T.J. , Pess, G.R. , Jorgensen, J.C. , Sogard, S.M. et al (2008) Evolutionary consequences of habitat loss for Pacific anadromous salmonids. Evolutionary Applications, 1, 300–318. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Moore, J.W. , McClure, M. , Rogers, L.A. & Schindler, D.E. (2010) Synchronization and portfolio performance of threatened salmon. Conservation Letters, 3, 340–348. [Google Scholar]

- Naish, K.A. , Taylor, J.E. III , Levin, P.S. , Quinn, T.P. , Winton, J.R. , Huppert, D. & Hilborn, R. (2008) An evaluation of the effects of conservation and fishery enhancement hatcheries on wild populations of salmon. Advances in Marine Biology, 53, 61–194. [DOI] [PubMed] [Google Scholar]

- Oksanen, J. , Blanchet, F.G. , Kindt, R. , Legendre, P. , Minchin, P.R. , O'Hara, R.B. et al (2012) vegan: Community Ecology Package. R package version 2.0‐5. http://CRAN.R-project.org/package=vegan. [Google Scholar]

- Peterman, R.M. , Pyper, B.J. , Lapointe, M.F. , Adkison, M.D. & Walters, C.J. (1998) Patterns of covariation in survival rates of British Columbian and Alaskan sockeye salmon (Oncorhynchus nerka) stocks. Canadian Journal of Fisheries and Aquatic Sciences, 55, 2503–2517. [Google Scholar]

- R Core Development Team . (2012) R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria: ISBN 3‐900051‐07‐0, URL http://www.R-project.org/. [Google Scholar]

- Rogers, L.A. & Schindler, D.E. (2008) Asynchrony in population dynamics of sockeye salmon in southwest Alaska. Oikos, 117, 1578–1586. [Google Scholar]

- Rogers, L.A. , Schindler, D.E. , Lisi, P.J. , Holtgrieve, G.W. , Leavitt, P.R. , Bunting, L. et al (2013) Centennial‐scale fluctuations and regional complexity characterize Pacific salmon population dynamics over the past five centuries. Proceedings of the National Academy of Sciences, 110, 1750–1755. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Sanderson, E.W. , Jaiteh, M. , Levy, M.A. , Redford, K.H. , Wannebo, A.V. & Woolmer, G. (2002) The human footprint and the last of the wild. BioScience, 52, 891–904. [Google Scholar]

- Schindler, D.E. , Scheuerell, M.D. , Moore, J.W. , Gende, S.M. , Francis, T.B. & Palen, W.J. (2003) Pacific salmon and the ecology of coastal ecosystems. Frontiers in Ecology and the Environment, 1, 31–37. [Google Scholar]

- Schindler, D.E. , Hilborn, R. , Chasco, B. , Boatright, C.P. , Quinn, T.P. , Rogers, L.A. & Webster, M.S. (2010) Population diversity and the portfolio effect in an exploited species. Nature, 465, 609–612. [DOI] [PubMed] [Google Scholar]

- Schindler, D.E. , Armstrong, J.B. , Bentley, K.T. , Jankowski, K. , Lisi, P.J. & Payne, L.X. (2013) Riding the crimson tide: mobile terrestrial consumers track phenological variation in spawning of an anadromous fish. Biology Letters, 9, 20130048. doi: 10.1098/rsbl.2013.0048. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Schnute, J.T. , Boers, N. , Haigh, R. , , C. , , G. , Johsnon, A. , Wessel, P. & Antonio, F. (2013) PBSmapping: Mapping Fisheries Data and Spatial Analysis Tools. R package version 2.66.53. http://CRAN.R-project.org/package=PBSmapping. [Google Scholar]

- Sethi, S.A. (2010) Risk management for fisheries. Fish and Fisheries, 11, 341–365. [Google Scholar]

- Sharpe, W.F. (1964) Capital asset prices: a theory of market equilibrium under conditions of risk. The Journal of Finance, 19, 425–442. [Google Scholar]

- Sharpe, W.F. (1994) The Sharpe Ratio. Journal of Portfolio Management, 21, 49–58. [Google Scholar]

- Thorson, J.T. , Scheuerell, M.D. , Buhle, E.R. & Copeland, T. (2014) Spatial variation buffers temporal fluctuations in early juvenile survival for an endangered Pacific salmon. Journal of Animal Ecology, 83, 157–167. [DOI] [PubMed] [Google Scholar]

- Tilman, D. (1996) Biodiversity: population versus ecosystem stability. Ecology, 77, 350–363. [Google Scholar]

- Waples, R.S. , Pess, G.R. & Beechie, T. (2008) Evolutionary history of Pacific salmon in dynamic environments. Evolutionary Applications, 1, 189–206. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Waples, R.S. , Gustafson, R.G. , Weitkamp, L.A. , Myers, J.M. , Johnson, O.W. , Busby, P.J. et al (2001) Characterizing diversity in salmon from the Pacific Northwest. Journal of Fish Biology, 59, 1–41. [Google Scholar]

- Whited, D.C. , Kimball, J.S. , Lucotch, J.A. , Maumenee, N.K. , Wu, H. , Chilcote, S.D. & Stanford, J.A. (2012) A riverscape analysis tool developed to assist wild salmon conservation across the North Pacific Rim. Fisheries, 37, 305–314. [Google Scholar]

- Wickham, H. (2007) Reshaping data with the reshape package. Journal of Statistical Software, 21, 1–20. [Google Scholar]

- Wiens, J.A. (1989) Spatial scaling in ecology. Functional Ecology, 3, 385–397. [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Table S1–4. Watershed portfolios and performance metrics.

Table S5. Performance and watershed descriptor correlations.

Table S6. Data sources.

Table S7–14. Management and genetic portfolios and performance metrics.

Figure S1. Chinook salmon coarse‐scale Sharpe ratio map.

Figure S2. Chinook salmon portfolio performance and glacier area.

Figure S3–4. Watershed portfolio performance and asset number.

Figure S5–6. Management and genetic portfolio Sharpe ratio.

Appendix S1. Alternative portfolio methods.

Data Availability Statement

Data were compiled from numerous sources. All data sources, points of contact, and links to web archives or reports containing the data are included in Table S6 (Supporting information).