Abstract

Background

The modern system of medicine has evolved into a complex, sophisticated and expensive treatment modality in terms of cost of medicines and consumables. In any hospital, approximately 33% of total annual budget is spent on buying materials and supplies including medicines. ABC (Always, Better Control)–VED (Vital, Essential, Desirable) analysis of medical stores of a large teaching, tertiary care hospital of the Armed Forces was carried out to identify the categories of drugs needing focused managerial control.

Methods

Annual consumption and expenditure data of expendable medical stores for one year was extracted from the drug expense book, followed by classification on its annual usage value. Subsequently, the factor of criticality was applied to arrive at a decision matrix for understanding the need for selective managerial control.

Results

The study revealed that out of 1536 items considered for the study, 6.77% (104), 19.27% (296) and 73.95% (1136) items were found to be A, B and C category items respectively. VED analysis revealed that vital items (V) accounted for 13.14% (201), essential items (E) for 56.37% (866) and desirable accounted for 30.49% items (469). ABC–VED matrix analysis of the inventory reveals that only 322 (21%) items out of an inventory of 1536 drugs belonging to category I will require maximum attention.

Conclusion

Scientific inventory management tools need to be applied routinely for efficient management of medical stores, as it contributes to judicious use of limited resources and resultant improvement in patient care.

Keywords: Selective inventory control, ABC analysis, VED analysis, ABC–VED matrix

Introduction

The modern system of medicine has transformed into a more complex, effective, sophisticated and expensive treatment modality in terms of cost of medicines, consumables and equipments. In any tertiary care hospital, approximately 33% of the annual operating budget is spent on buying materials and supplies, medicines being of the prime category.1The medical stores along with the dispensary where distribution of medicines takes place, is one of the most extensively used facility of the hospital and one of the few areas where a large amount of money is consumed by procurement action and maintenance. The medical stores are also related intimately to the overall satisfaction of hospital clientele as non-availability of medicines may lead to poor healthcare delivery and bad reputation for the healthcare organization. There is a need for judicious planning, designing, organizing and maintaining the pharmacy in a manner that results in efficient clinical and administrative services.2

A study conducted by the Department of Personnel and Administrative Reforms in India revealed that not only does the quantity of medicines received fell short of the projected requirement but also the supply was often erratic. Of the various explanations for non-availability of even simple medicines in the third world countries, a large number were found to be related to materials management.3 A study conducted by Pillans et al. in a 1500-bedded state-funded hospital has claimed that better inventory control technique brought about 20% savings in hospital expenditure.4 Multiple published studies have shown that inventory control techniques when made a routine practice in healthcare could bring about substantial improvement in patient care as well as optimal use of resources.5,6

It is a fact that inventory is an idle resource with an economic value and efficient management can definitely bring meaningful savings in hospital expenditure.7 Two factors considered important in medical logistics management are cost and the criticality of the item. Among various selective inventory control techniques, methods that are commonly used are Always, Better Control (ABC) and Vital, Essential and Desirable (VED) analysis. ABC analysis is a method of classifying items or activities according to their annual usage value in monetary terms while VED analysis takes care of the criticality factor of drugs and consumables. ABC analysis had been conceptualized on the universal observation of a small number of items accounting for a large share of the total cost of materials and a comparatively larger number involving an insignificant share. Based on this criterion, items in an inventory are classified into category A (high usage value), B (moderate usage value) and C (low usage value). However health is considered to be priceless and hence medical stores are further classified on the basis of their criticality into Vital (critical for life and patient care), Essential (critical but alternatives acceptable) and Desirable items (low critical value).8–10

The present study was conducted to undertake an ABC–VED analysis of expendable medical stores being held by a large multi-specialty tertiary care hospital of the Armed Forces with a view to improve management and control of inventory of such stores.

Materials and methods

The study was an observational study carried out in the Medical Stores Department of the study hospital for a period of one month.

Annual consumption data of expendable medical stores for the financial year 2011–12 along with expenditure incurred on each item was retrieved from the Drug Expense Register and Medical stores management software (MSMS) being held by the hospital. The data was further transcribed to a MS Excel spreadsheet for quantitative calculations.

Annual usage for each drug (Consumption × Cost) was calculated for the financial year 2011–2012 from the data retrieved. The annual expenditure of individual items thus worked out was arranged in descending order and the cumulative cost of all the items was calculated. The cumulative percentage of expenditure and the cumulative percentage of number of items were then calculated for performing ABC analysis.

To decide upon the criticality of items, the complete inventory of drugs was presented to a group of five clinical experts for categorization of drugs on the basis of criticality, keeping the standard definition of Vital, Essential and Desirable drugs in consideration.

The final list of drugs arranged on the basis of criticality was analyzed for convergence of opinion, the acceptable range of concurrence being a minimum of three experts agreeing for the same classification of each individual item.

Thereupon, a matrix was prepared by combining the results of ABC and VED analysis to evolve an inventory control system that can be used for managerial prioritization. Each window in the matrix was labeled by two alphabets, the first alphabet denoting ABC classification and the second representing VED analysis. From the resultant combination, three categories were classified, category I being constituted by items belonging to AV, AE, AD, BV and CV subcategories. The BE, CE and BD subcategories constituted category II and the remaining items in the CD subcategory constituted category III.

Appropriate interpretations were derived for drugs classified in each window of the ABC–VED matrix for superior but selective control of the inventory being held by the Medical Stores Department.

Results

The drug inventory of the hospital in 2011–2012 consisted of 1536 items.

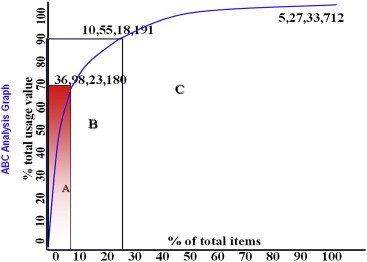

ABC analysis revealed A category items comprising 6.77% (104) expendable items consuming 70.03% of the total stores expenditure and B category items represented by 19.27% items (296) accounting for 19.98% expenditure. An astounding 73.95% (1136) items were found to belong to category C, consuming only 9.98% of the total expenditure (Table 1). The results are also being graphically displayed in Fig. 1 for better appreciation.

Table 1.

ABC analysis of expendable medical stores.

| Analysis parameter | Category |

Total | ||

|---|---|---|---|---|

| A | B | C | ||

| No. of items | 104 | 296 | 1136 | 1536 |

| Cumulative % of items | 6.77 | 19.27 | 73.95 | 99.99 (100%) |

| Percentage of annual consumption | 70.03% | 19.98% | 9.98% | 99.98% |

Fig. 1.

ABC analysis.

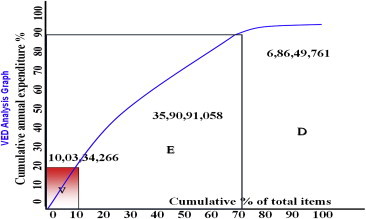

After ABC analysis, VED analysis was subsequently performed for ushering in the parameter of criticality in the analytical process. 13.14% (201) expendable items were found to belong to V group, 56.37% (866) to E group and the balance 30.49% (469) to D group of items (Table 2/Fig. 2).

Table 2.

VED analysis of expendable medical stores.

| S. no | Drug category | No of drugs | % of drugs | Value of drugs (%) |

|---|---|---|---|---|

| 1. | Vital | 201 | 13.14 | 19 |

| 2. | Essential | 866 | 56.37 | 68 |

| 3. | Desirable | 469 | 30.49 | 13 |

| 4. | Total | 1536 | 100 | 100 |

Fig. 2.

VED analysis.

Lastly the results of the ABC and VED analysis were further classified into a combined matrix representing the three essential functional parameters of “Annual consumption, cost and criticality”. 322 (21%) items were found to belong to matrix classification I, whereas 427 (27.83%) items belonged to the CD window (Table 3).

Table 3.

ABC–VED matrix analysis of expendable medical stores.

| Category of drugs | V | E | D | Matrix classification |

|---|---|---|---|---|

| A | AV (62) | AE (72) | AD (66) | I 322 (21%) |

| B | BV (64) | BE (260) | BD (214) | II 786 (51.17%) |

| C | CV (58) | CE (312) | CD (427) | III 427 (27.83%) |

Discussion

In the present healthcare environment of “limited resource and unlimited demand”, no healthcare organization will have abundant resources and hence, optimal utilization of existing resources for contributing towards maximum benefit of hospital clientele will be an essential component of hospital logistics management. Future healthcare managers will have to utilize scientific methods of inventory management and the role of an efficient hospital logistics system cannot be ignored anymore.11,12

In a hospital, inventory will have to be maintained to sustain critical patient care activities but at the same time, a balance needs to be struck to maintain an optimum inventory with minimum investment of working capital. Selective inventory control techniques utilize various criterions towards selected control of hospital inventory, achieving the desired balance between overstocking and stock-out situation for superior operational efficiency of healthcare organizations.

ABC analysis of drugs of the medical stores of the largest tertiary care hospital of the Armed Forces revealed that out of 1536 items in the drug list considered for the study, 6.77% (104) drugs consumed 70.03% and 19.27% (296) drugs consumed 19.98% of total expenditure, the total amounting to only 400 drugs of the total inventory consuming approximately 90% of the operating budget of the hospital towards expendable medical stores, the remaining 73.95% (1136) drugs consuming only 10% of the total expenditure. Similar study carried out by Gupta et al, in 2007 in a 190 bedded hospital showed that 14.4% items consumed 70% of annual drug expenditure comprising the A group while group C constituted 63.7% items which consumed 10% of annual drug expenditure of the hospital.13

The drugs belonging to category A requires strict managerial control, accurate data driven forecasting of demand, close check on budgetary control, minimum safety stock, staggered purchase orders, frequent stock taking and judicious purchasing, stocking, issue and inspection policy. Category B drugs require moderate control by middle level managers whereas category C requires minimum control measures for order and purchase and such functions can be delegated to lower level managers.

ABC analysis alone provides a managerial tool for selectively controlling inventory on annual usage value alone, neglecting the criticality factor which is not acceptable in medical practice. Thus, selective inventory control of medical stores integrates the dual concept of usage and criticality for better and more patient-centric control of drug inventory.

VED analysis revealed that vital items (V) accounted for 13.14% (201) and essential items (E) accounted for 56.37% (866) of the total inventory, while Desirable items accounted for 30.49% (469). Similar study by Gupta et al revealed that 7.3% items constituted Vital, 49.3% were considered essential and 43.4% were considered desirable.13 Another study by Doshi et al conducted at a Government tertiary care hospital in Kerala revealed that 13% of the inventory were vital drugs, 51% essential and 36% were considered desirable.10

Drugs belonging to vital category will require continuous availability and reasonable safety stock with zero tolerance for stock-out options, whereas Essential items can be adjusted to reduced service level with availability of alternative drugs. Desirable group of items require little managerial control over its availability and stocking decisions.

A combination of ABC and VED analysis makes it possible to focus on 322 (21%) items which belongs to category I for strict managerial control, as these items are either expensive or vital, the cumulative annual expenditure for these items being 69.45% of the total annual drug expenditure. Our study findings are similar to a study conducted by Devnani et al., where, 22.09%, 54.63% and 23.28% items were found to belong to category I, II and III items respectively, accounting for 74.21%, 22.23% and 3.56% of annual drug expenditure of the pharmacy.5 Drugs belonging to category I mandates strict control with a low buffer stock with constant vigil on their consumption pattern and stock in hand. The major bulk of drugs belong to category II (51.17%) are of intermediate value in monetary terms as well as their criticality towards patient care and hence, require control and supervision at the middle managerial level. Of particular interest are the drugs belonging to group CE (20.31%) which are vital but of low cost and will require continuous availability on the ward floor. Category III consists of 427 (27.83%) items and only consumes 6.2% of the total annual budget. These items can be ordered in bulk to save on ordering cost and supervision of this group can be delegated to lower level managers.

Our study has demonstrated the utilization and benefits of selective inventory control techniques in medical logistics management. What needs to be appreciated is that the operational efficiency of the medical stores can be substantially improved by focusing on 322 drugs (21%) only out of the total inventory of 1536 items, making stores management function easier, efficient and contributing to optimal utilization of hospital resources. Selective inventory control techniques along with ABC–VED coupling needs to be adopted as a standard protocol by the Medical Stores Department of all service hospitals for scientific management of the inventory being held as well as directing the focus and attention of the Officer – in – charge towards drugs that are both expensive and critical.

The study suffers from the limitation of being a single hospital study and thus the study findings cannot be generalized for all service hospitals. However the concept of selective inventory control is universal for achieving the aim of “Right drug in right quantity at right price and at right place”.

Our study has analyzed the selective inventory control techniques that are available with focus on cost and criticality factor. Major benefits that are expected by adopting selective inventory control techniques are effectiveness and efficiency in management of the medical stores, scientific approach in decision making for purchase, storage and distribution of specific items and selective control function that will ultimately contribute to better patient care. It is time that service hospitals revisit their medical stores management practices and adopt scientific inventory control tools for better and higher efficiency in medical logistics functions.

Conflicts of interest

All authors have none to declare.

References

- 1.Kant S., Pandaw C.S., Nath L.M. A management technique for effective management of medical store in hospitals. Medical store management technique. J Acad Hosp Adm. 1997:41–47. [PubMed] [Google Scholar]

- 2.Kunders G.D., Gopinath S., Katakam A. Hospitals: Planning, Design and Management. Tata McGraw-Hill Publishing Company Limited; New Delhi: 2000. Planning and designing supportive services-Pharmacy; pp. 273–281. [Google Scholar]

- 3.Kidwai M. National Institute of Health and Family Welfare; New Delhi: 1992. Inaugural Address. Logistics and Supply Management for Health and Family Planning Programme: A Report of Inter-country Course; pp. 66–70. [Google Scholar]

- 4.Pillans P.I., Conry I., Gie B.E. Drug cost containment at a large teaching hospital. Pharmacoeconomics. 1992;1:377–382. doi: 10.2165/00019053-199201050-00009. [DOI] [PubMed] [Google Scholar]

- 5.Devnani M., Gupta A., Nigah R. ABC and VED analysis of the pharmacy store of a tertiary care teaching, research and referral healthcare institute of India. J Young Pharm. 2010;2:201–205. doi: 10.4103/0975-1483.63170. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Thawani V.R., Turanker A.V., Sontakke S.D. Economic analysis of drug expenditure at Government Medical College Hospital, Nagpur. Indian J Pharmacol. 2004;36:15–19. [Google Scholar]

- 7.Gopalakrishnan P., Sundaresan M. Prentice Hall; New Delhi: 1985. Materials Management: An Integrated Approach. [Google Scholar]

- 8.Brown R.B. John Wiley and Sons; New York: 1977. Materials Management Systems. [Google Scholar]

- 9.Gandhi P., Basur A. Application of ABC analysis in medical store of ESIC, Delhi. Health Adm. 2000;9 and 10:90–95. [Google Scholar]

- 10.Doshi R.P., Patel N., Jani N., Basu M., Mathew S. iHEA 2007, 6th World Congress: Explorations in Health Economics Paper. 2007. ABC and VED analyses of drug management in a government tertiary care hospital in Kerala. [Google Scholar]

- 11.Gupta S., Kant S. Hospital Stores Management – An Integral Approach. Jaypee Brothers Medical Publishers(P) Ltd; New Delhi: 2000. Inventory control; pp. 60–72. [Google Scholar]

- 12.Das J.K. Inventory control. In: Kaushik M., Agarwal A.K., Arora S.B., editors. Essentials of Logistics and Equipment Managemnt, Manual of Post Graduate Diploma in Hospital and Health Management. Indira Gandhi National Open University, School of Health Sciences; New Delhi: 2001. [Google Scholar]

- 13.Gupta R., Gupta K.K., Jain B.R., Garg R.K. ABC and VED analysis in medical stores inventory control. MJAFI. 2007;63:325–327. doi: 10.1016/S0377-1237(07)80006-2. [DOI] [PMC free article] [PubMed] [Google Scholar]