Abstract

This paper analyzes determinants of ex-manufacturer prices for originator and generic drugs across countries. We focus on drugs to treat HIV/AIDS, TB, and malaria in middle and low-income countries (MLICs), with robustness checks to other therapeutic categories and the full income range of countries. We examine the effects of per capita income, income dispersion, competition from originator and generic substitutes, and whether the drugs are sold to retail pharmacies versus tendered procurement by non-government organizations.

The cross-national income elasticity of prices is 0.27 across the full income range of countries but is 0.0–0.10 between MLICs, implying that drugs are least affordable relative to income in the lowest income countries. Within-country income inequality contributes to relatively high prices in MLICs. Although generics are priced roughly 30% lower than originators on average, the variance is large. Additional generic competitors only weakly affect prices, plausibly because generic quality uncertainty leads to competition on brand rather than price. Tendered procurement that imposes quality standards attracts multinational generic suppliers and significantly reduces prices of originator and generic drugs, compared with their respective prices to retail pharmacies. ©2013 The Authors. Health Economics Published by John Wiley & Sons Ltd.

Keywords: Pharmaceuticals, prices, emerging markets, generics, procurement

1. Introduction

Pharmaceutical pricing in middle and low-income countries (MLICs) is an important and contentious issue. Because most patients lack insurance coverage and pay out-of-pocket for drugs, pricing commensurate with income is critical to affordability. The World Trade Organization's requirement that all countries adopt a 20-year product patent regime as a condition of World Trade Organization membership has prompted concerns that patents undermine generic availability and make drugs unaffordable in MLICs. In theory, patents need not imply high prices if originator firms price discriminate across countries based on per capita income (PCI) (Malueg and Schwartz, 1994; Danzon and Towse, 2003); however, incentives for pricing commensurate with mean income may be undermined by price spillovers across countries (due to parallel trade and external referencing) and by skewness of income distributions (Flynn et al., 2009). In practice, although generic copies are available for most originator drugs, asymmetric information about generic quality potentially undermines price competition. Thus, the affordability of both generic and originator drug prices in MLICs remains an empirical question with little evidence.

This paper outlines a conceptual model of manufacturer pricing of originator and generic drugs across countries, focusing on effects of PCI, competition, and quality uncertainty.1 The empirical analysis uses data from IMS Health on ex-manufacturer prices to retail pharmacies for originator and generic drugs in two large therapeutic categories (cardiovascular and anti-infectives) in 37 countries, including high and low-income countries. We report analyses of the effects of mean PCI and income dispersion (Gini) within a country and the number and types of potential competitor products. To further examine drug markets within MLICs, we use drugs to treat HIV/AIDS, TB, and malaria (a subset of the anti-infective class) to compare IMS ex-manufacturer prices in the retail pharmacy channel, which is characterized by atomistic purchasers and quality uncertainty, with prices charged for the same drugs in the procurement channel, where large institutional purchasers procure from World Health Organization (WHO)-qualified suppliers, using tendering to stimulate price competition. The procurement data are from the WHO's Global Price Reporting Mechanism (GPRM).

For ex-manufacturer prices to retail pharmacies across the full income range of countries, we estimate the price elasticity with respect to PCI at 0.267 for originators and generics combined but 0.100 for MLICs. Income dispersion is associated with relatively high prices in the retail channel in MLICs. Although generics are priced on average 32% below originators in the retail channel, the generic/originator price ratios are widely dispersed and some exceed one. Procurement lowers originator and generic prices by 42% and 34%, compared with their respective retail prices, and this procurement effect cannot be explained by volume. More important appears to be that procurement buyers require WHO prequalification of suppliers, which reduces quality uncertainty, and use tendering to stimulate price competition.

In the remainder of this paper, Section 2 outlines the conceptual framework of originator and generic drug pricing and reviews previous literature; Section 3 describes data and empirical methods; Section 4 reports results of the multivariate regression analysis; Section 5 concludes.

2. Theory and Previous Literature

2.1. Pricing on-patent drugs: mean per capita income and skewness

Consider the strategy of a multinational firm pricing an on-patent, originator drug for the retail pharmacy channel in different countries. Assume initially that price discrimination is feasible across countries, but only one price can be charged in each country, due to price regulation and/or price arbitrage by distributors. Simple price discrimination implies that the profit-maximizing price in each country is inversely related to its demand elasticity (E), which is plausibly inversely related to mean PCI.2 Thus, originator prices are predicted to vary positively with (but not necessarily in proportion to) PCI across countries, and this is plausibly welfare superior to uniform prices across countries.3

In practice, several factors may undermine the expected positive relationship between prices and PCI across countries. First, in most high income countries (HICs), comprehensive health insurance makes consumer demand inelastic, which in turn is counteracted by payer regulation of drug prices. Pricing by manufacturers should still vary positively with PCI across countries, provided that these insurance systems reflect average consumer willingness-to-pay for health, and this is inversely related to demand elasticity.

Second, parallel trade and external referencing by payers undermine manufacturers' ability to price discriminate across countries, creating incentives for firms to charge higher prices in low-income countries than they would under perfect discrimination, accepting smaller market share to avoid low prices spilling over to higher-priced markets. However, in practice, external referencing and parallel trade occur mostly among countries at similar income levels in the same region, especially within the EU. It therefore seems unlikely that fear of price spillovers to HICs is a major cause of high prices in MLICs.

Third, Flynn et al. (2009) show that the highly skewed income distribution in many MLICs would lead a single price monopolist to charge higher prices in poor countries than would be predicted based solely on PCI. No empirical evidence is presented. Although this effect might in theory be mitigated if firms could price discriminate within countries, this requires barriers to price arbitrage, such as separate private versus public payers.4 Price discrimination is unlikely to be sustainable in retail pharmacy markets in MLICs, where most consumers pay cash and retailers are served by common distribution networks. The model of Flynn et al. (2009) therefore predicts that originator drug prices will be positively associated with the Gini measure of skewness, but there is no evidence to date.

Previous empirical evidence on cross-national price differences for on-patent drugs focuses mainly on HICs (e.g., Danzon and Chao, 2000a, 2000b). Danzon and Furukawa (2008) found that prices varied roughly in proportion to income across HICs, but for Brazil, Mexico, and Chile, drug prices were twofold to threefold higher relative to PCI. Empirical evidence on drug prices in MLICs is limited. Maskus (2001) analysis of 20 drugs in 14 countries in 1998 found a correlation between average list price and PCI of roughly 0.5. Scherer and Watel (2001) found that for 15 anti-retroviral drugs in 18 countries for the period 1995–1999, the average price was 85% of the US list price, PCI only weakly contributed to price differences, and the relationship declined over time as companies began offering discounts unrelated to PCI.

2.2. Generics: quality and competition

In most HICs, generic copies of originator drugs can be marketed after expiry of patents and other exclusivities, subject to meeting regulatory requirements of bioequivalence and good manufacturing standards. These regulatory requirements for generic quality enable consumers/payers to treat generics as perfect substitutes for originators, which is a necessary condition for aggressive generic price competition and erosion of originator sales once multiple generics enter an originator market.5 By contrast, drug regulatory agencies in most MLICs admit generic copies that are marketed as functionally equivalent to the originator but are not required by regulation to demonstrate bioequivalence or meet international good manufacturing practice standards. Although most MLICs have adopted TRIPS patent provisions, existing generics were grandfathered and strict requirements for ‘novelty’ have led to patent denials for several new drugs that are patented in the US and EU.6 Thus, generics are available for most molecules in MLICs, but generic quality is heterogeneous and uncertain to consumers.

Given heterogeneous product quality, a drug manufacturer's optimal pricing strategy depends on its type and on the distribution of consumers' perceptions and willingness-to-pay for drug quality. Consumers in MLICs (or their physician/pharmacy agents) may observe three categories of products that differ in expected quality: (i) originator brands have met the strictest safety, efficacy, and purity requirements of the FDA or European Medicines Agency; (ii) generics sold by large, multinational generic producers that have met at least WHO standards of quality; and (iii) domestic generics, which include some firms with established reputations and others of unknown quality.

In such markets with heterogeneous products and consumer preferences, originator firms may rationally adopt a segmentation strategy, raising price to target the most quality-inelastic, price-inelastic consumers, abandoning the more quality-elastic segment to lower-quality generics.7 Multinational generic producers that are WHO-qualified may choose to position themselves as high-quality/high-price generic brands or may choose a lower-price/high-volume strategy. Third, among the heterogeneous domestic generics, some may invest in reputation for brand quality and charge higher prices,8 whereas others charge the lowest prices to attract the most price-sensitive customers. Thus, in generic markets with weak regulatory requirements for quality, most generics are branded generics, and price becomes a signal for quality. A wide dispersion of generic prices is possible in such markets, and the extent of price competition is an empirical question.

2.3. Procurement of drugs for HIV/AIDS, TB, and malaria

Prior to 2000, most HIV/AIDS drugs were originator brands. The standard three-drug cocktail cost up to $10,000 per year or 10 times average PCI in the poorest countries (Kapstein and Busby, 2009). Around 2001, international donors created new non-government organizations (NGOs) such as the Global Fund to Fight AIDS, TB, and Malaria and the Clinton Foundation's HIV/AIDS Initiative (CHAI), with increased resources and new procurement mechanisms. Expanded global demand enabled growth of multinational generic suppliers (mostly Indian) with scale economies. These NGOs purchase mainly from WHO-qualified, generic suppliers, using tendering to stimulate price competition. Originator firms may also have incentives to offer discounts to NGOs, if their demand is more price-elastic than retail channel purchasers and/or their procurement channels reduce price-spillover risks through parallel trade and referencing. Waning et al. (2009) examined prices for 24 generic anti-retroviral drugs (ARVs) procured July 2002–October 2007, as reported to the WHO GPRM. They found that CHAI-eligible contracts have significantly lower prices than non-CHAI-eligible contracts, but volume had no significant effect on price.

Our analysis provides new evidence on cross-national determinants of drug prices in both retail and procurement channels, focusing on effects of both mean PCI and income skewness (Gini), and comparing originator and generic drugs across 37 countries, including HICs and MLICs. Our comparison of prices in the retail channel versus procurement channel focuses on HIV/AIDS, TB, and malaria drugs, comparing pricing by originators, local generics, and large multinational generic suppliers.

3. Data and Methods

3.1. Data

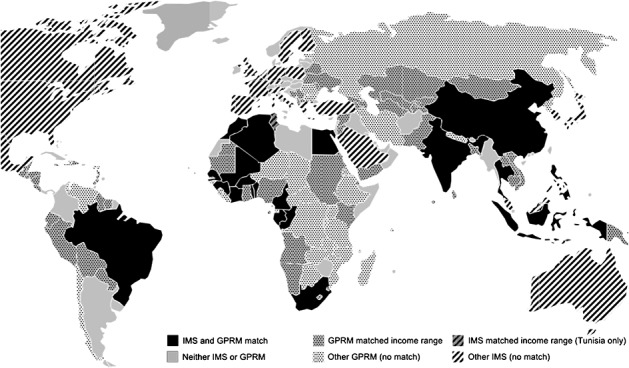

Retail pharmacy channel (IMS): Our IMS MIDAS database reports sales for all drugs in the anti-infectives (J) class and the cardiovascular (C) class for most major industrialized countries and a subset of MLIC countries (Figure 1). IMS reports quarterly ex-manufacturer sales and volume data for each product, in current US dollars, converted from local currencies at quarterly exchange rates.9 We converted the IMS price per standard unit to annual treatment price using the WHO defined daily dose (DDD) for each drug presentation.10 We include year indicators to control for average inflation, exchange rate changes, and other unmeasured year-specific effects.11

Figure 1.

Countries in the matched and matched range samples

3.2. Dataset structure and country groups

Our unit of analysis is average annual ex-manufacturer treatment price for the molecule-country-year, with separate observations for generic and originator products for the retail (IMS) and procurement (GPRM) channels where available, for the period January 2004–June 2008. For the comparison of retail versus procurement prices, our IMS sample is limited to those HIV/AIDS, TB, or malaria drugs that are also procured through GPRM for at least one country. Combination drugs are treated as unique products.13

Ten countries (Algeria, Brazil, China, Egypt, India, Indonesia, Morocco, the Philippines, South Africa, and Thailand) are in both IMS and the GPRM datasets. A group of 10 Sub-Saharan Africa countries are reported aggregated in IMS as ‘French West Africa’.14 We therefore created a comparable, GPRM French West Africa aggregate, defined as the population-weighted average of the country-specific data in GPRM for these individual countries.

We report regression estimates for three country groups: (i) all countries for which we have data; (ii) the eleven matched MLIC countries with both IMS and GPRM data; and (iii) all MLICs in the same PCI range as the matched country sample that report GPRM data. This ‘matched income range’ sample includes more low-income countries and has very similar summary statistics to the eleven ‘matched countries’ (Table I). We base most conclusions on the matched income range sample, which provides more robust evidence on GPRM prices.

Table I.

Summary statistics for HIV/AIDS, TB, and malaria drugs in the retail and procurement channels

| All countries | Matched countries* | Matched income range** | ||||

|---|---|---|---|---|---|---|

| Mean | Std dev | Mean | Std dev | Mean | Std dev | |

| Retail (IMS) sample | ||||||

| Log per capita income | 9.76 | 1.00 | 8.24 | 0.65 | 8.25 | 0.64 |

| Raw per capita income | 24,318 | 14,082 | 4610 | 2812 | 4644 | 2802 |

| Log annual treatment price | 7.01 | 1.81 | 5.45 | 1.57 | 5.43 | 1.58 |

| Raw annual treatment price | 2974 | 3858 | 574 | 827 | 570 | 822 |

| HIV prevalence per 100K | 7.93 | 23.70 | 25.41 | 42.42 | 25.02 | 42.17 |

| Gini coefficient | 34.37 | 13.12 | 40.17 | 18.37 | 40.17 | 18.22 |

| Gini coefficient missing flag | 0.07 | 0.25 | 0.13 | 0.33 | 0.12 | 0.33 |

| Tender gen. manufs. in class-ctry. | 0.75 | 2.17 | 2.52 | 3.68 | 2.48 | 3.66 |

| Retail gen. manufs. In class-ctry. | 7.98 | 17.57 | 20.32 | 29.58 | 20.01 | 29.43 |

| Originator manufs. in class-ctry. | 2.32 | 1.60 | 2.35 | 1.71 | 2.32 | 1.72 |

| Originator present in country | 0.84 | 0.37 | 0.75 | 0.43 | 0.75 | 0.43 |

| Form = *not* oral solid | 0.17 | 0.38 | 0.16 | 0.37 | 0.16 | 0.37 |

| Generic volume (mils) | 3.33 | 15.66 | 6.77 | 23.77 | 6.68 | 23.62 |

| Originator volume (mils) | 1.05 | 4.29 | 1.39 | 6.52 | 1.36 | 6.45 |

| Observations (n)† | 5790 | 1468 | 1493 | |||

| Tendered (GPRM) sample | ||||||

| Log PCI | 7.70 | 0.98 | 8.10 | 0.79 | 8.08 | 0.61 |

| Raw PCI | 3467 | 3451 | 4360 | 2990 | 3867 | 2291 |

| Log annual treatment price | 5.14 | 1.42 | 5.35 | 1.37 | 5.18 | 1.46 |

| Raw annual treatment price | 561 | 2347 | 547 | 1178 | 634 | 2704 |

| HIV prevalence per 100K | 29.23 | 49.26 | 31.47 | 42.14 | 26.21 | 55.88 |

| Gini coefficient | 37.39 | 19.14 | 43.90 | 14.15 | 38.42 | 17.74 |

| Gini coefficient missing flag | 0.17 | 0.38 | 0.05 | 0.22 | 0.13 | 0.34 |

| Tender gen. manufs. in class-ctry. | 1.93 | 1.41 | 1.92 | 1.38 | 1.90 | 1.35 |

| Retail gen. manufs. In class-ctry. | NA | NA | NA | NA | NA | NA |

| Originator manufs. in class-ctry. | 0.76 | 0.89 | 0.79 | 0.90 | 0.73 | 0.89 |

| Originator present in country | 0.45 | 0.50 | 0.46 | 0.50 | 0.44 | 0.50 |

| Form = *not* oral solid | 0.24 | 0.43 | 0.25 | 0.43 | 0.25 | 0.43 |

| Generic volume (mils) | 0.82 | 3.25 | 1.49 | 6.22 | 0.69 | 3.17 |

| Originator volume (mils) | 0.20 | 0.84 | 0.27 | 0.72 | 0.14 | 0.50 |

| Observations (n)† | 5905 | 754 | 3821 | |||

Matched countries = Brazil, China, Algeria, Egypt, India, Indonesia, Morocco, Philippines, Thailand, South Africa, and French West Africa. French West Africa aggregates 10 West African countries (Ivory Coast, Cameroon, Gabon, Senegal, Congo, Benin, Guinea, Togo, Mali, and Burkina Faso).

Matched range countries include all countries with per capita income range of the precisely matched countries by year (roughly $1K–$10K).

Observations at the molecule-country-year-originator/generic-formulation level.

3.3. Methodology

We estimate a quasi difference-in-differences model of log prices with indicator variables to test for differential effects for each license-channel category (retail generics, procurement originators, and procurement generics, designated by the vector Z below) compared with the referent retail originator category:

|

In this pooled equation, a1, a2, and a3 measure the mean price differential of the three channel-license categories—retail generics, procurement originators, and procurement generics—respectively, relative to retail originators; b0 is the income elasticity for IMS originators in the retail channel, and b1 is the vector of differential income effects for generics and the procurement channel; c0 and c1 are the coefficients on the vector of competition variables COMP; d1, d2, and d3, respectively, measure effects of income dispersion, HIV prevalence, and volume; ui and ut are molecule and year fixed effects, and vijt is a random disturbance term. We also estimate separate equations for each of the four license-channel categories (originator brands and generics in the retail and the procurement channels, respectively) to permit all coefficients to differ across categories. The procurement regressions include purchaser indicators, to test for variation in prices paid by different GPRM purchasers, due to scale, bargaining power, or other factors. For the full cardiovascular and anti-infectives classes, we estimate the same specification for the retail channel only.

3.4. Variable definitions and hypotheses

Per capita income, income dispersion, and HIV Prevalence: Per capita income is measured by (log) per capita gross national income in international dollars. Originator drug prices are expected to be positively related to PCI under the joint hypothesis that originators can price discriminate across countries and that price elasticities vary directly with mean PCI. By contrast, if generic markets are price competitive, generics would lack the market power necessary to price discriminate across countries, and generic prices should be invariant with PCI.15

The Gini measure of income equality is expected to be positively related to prices if income inequality leads to higher prices due to demand convexity (Flynn et al., 2009). This effect is expected to occur only for originators, if generics are price competitive, and only in the retail sector.

Some MLIC governments argue that disease burden should justify a lower price, and some originator companies list disease burden as a factor in their corporate responsibility and pricing strategies. If these considerations are significant, HIV prevalence is expected to be inversely related to drug prices.

Number of competitors: We define markets by therapeutic class-country-year, using the IMS classification to define four classes for HIV/AIDS drugs (NRTIs, NNRTIs, PIs, and combinations) and one class each for TB and anti-malarials.16 Originator competitors are the number of originator products in a therapeutic class-country-year. We distinguish two types of generic competitors: tendering generics are generic producers who sold to the procurement channel at least once during our period, in any country, and thus have demonstrated ability to comply with international quality standards and compete on price. Retail generics are firms that never participated in procurement, whose quality and ability to compete on price is more uncertain. Generic competitors are at the therapeutic class-country-year, to allow for inter-molecule (therapeutic) and intra-molecule (generic) competition. In the pooled regressions (Table II), competitor counts include both channels. Under standard competition models, prices are expected to be inversely related to number of competitors. This effect is expected to be weaker in the retail channel than the procurement channel, if uncertain quality undermines price competition in the retail sector. For generic observations, we include an originator present indicator if the molecule originator is present in a country-year. The coefficient is expected to be positive if generics shadow price the originator brand.

Table II.

Effects of income, competition, and procurement, on drug prices: pooled retail and tender channels; HIV/AIDS, TB, and malaria drugs, 2004–2008

| OLS regressions of log annual treatment price, GPRM and IMS data | |||

|---|---|---|---|

| All countries | Matched countries | Per capita income-range countries | |

| Retail channel * generic indicator‡ | −0.425*** | −0.347 | −0.355 |

| [0.123] | [0.233] | [0.222] | |

| −35.1% | −31.2% | −31.6% | |

| Tender channel * originator indicator‡ | −1.227*** | −0.554** | −0.520** |

| [0.195] | [0.242] | [0.252] | |

| −71.2% | −44.2% | −42.4% | |

| Tender channel * generic indicator‡ | −1.688*** | −1.044*** | −1.070*** |

| [0.200] | [0.295] | [0.256] | |

| −81.9% | −66.3% | −66.8% | |

| Log per capita income (lnPCI) | 0.267*** | −0.0501 | 0.100* |

| [0.0494] | [0.0548] | [0.0536] | |

| Gini coefficient | −0.0161*** | 0.0401*** | 0.00292 |

| [0.00549] | [0.0116] | [0.00418] | |

| Gini missing indicator‡ | 0.0912 | −0.163 | −0.0197 |

| [0.101] | [0.157] | [0.0755] | |

| 9.0% | −16.1% | −2.2% | |

| HIV prev. (per 100K) | −0.0006 | −0.0106*** | −0.00137* |

| [0.0008] | [0.00276] | [0.000761] | |

| Log drug volume | −0.0530*** | −0.115*** | −0.106*** |

| [0.0125] | [0.0322] | [0.0178] | |

| Tendering generic firms in class§ | −0.0453** | 0.0168 | 0.00439 |

| [0.0206] | [0.0115] | [0.0115] | |

| Retail generic firms in class§ | −0.00892** | −0.00879*** | −0.00784*** |

| [0.00358] | [0.00224] | [0.00245] | |

| Originator firms in class§ | 0.0180 | 0.0494 | 0.0478** |

| [0.0328] | [0.0448] | [0.0185] | |

| Originator present in molecule‡ | 0.368*** | 0.323*** | 0.312*** |

| [0.0621] | [0.0832] | [0.0618] | |

| 44.2% | 37.6% | 36.4% | |

| Non-oral solid‡ | 0.205** | 0.602*** | 0.182** |

| [0.0852] | [0.147] | [0.0902] | |

| 22.3% | 80.6% | 19.5% | |

| Molecule and year fixed effects | X | X | X |

| Constant | 5.664*** | 5.557*** | 5.966*** |

| [0.611] | [0.893] | [0.588] | |

| Observations | 11,694 | 2222 | 5314 |

| R-squared | 0.794 | 0.697 | 0.675 |

Robust standard errors adjusted for 37 clusters in country in brackets.

Predicted linear effects for indicator variables including variance correction (Kennedy, 1981) reported in italics.

All competition measures are calculated within country-class-year, pooled across channels.

p < 0.1.

p < 0.05.

p < 0.01.

Formulation: An indicator variable is included for non-oral solids such as liquids and creams, which typically have higher production costs and fewer competitors than the tablets and capsules which are the bulk of the observations.

Volume: Volume is measured in annual doses (logged) at the contract level for GPRM and at the molecule-country level for retail originators and generics.

Purchaser indicators: In separate GPRM regressions, we include indicators for the four purchasers with the most contracts: UNICEF, the Global Fund, IDA, and Missionpharma.17 The coefficients should be negative if their aggregate volume gives these purchasers an advantage beyond the contract-specific volume.

3.5. Descriptive statistics

Table I reports descriptive statistics for HIV, TB, and malaria drugs in the retail and procurement channels. The all-country sample includes 37 countries with IMS data, with mean PCI of $24,318 and 112 countries in GPRM with mean PCI of $3467. The matched country sample has 11 countries, with mean PCI of $4610. The matched PCI-range sample includes 73 countries, primarily adding countries with GPRM data, with no material differences in demographic characteristics. Our discussion therefore focuses mainly on the results for the matched PCI-range countries, which have PCI of $1000–$10,000.

For these countries, the retail channel (IMS) has more molecules with both an originator and at least one generic available than the procurement channel (GPRM). The larger mean number of originator and generic competitors per class in the pharmacy channel (2.32 and 20.0) versus the procurement channel (0.73 and 1.90, respectively) largely reflects the much larger number of suppliers of TB and anti-malarial drugs to retail pharmacies. For HIV, the mean count of actual suppliers is larger in the procurement channel, and this may understate potential competitors.18 Whereas most originator firms participate in both the retail and procurement channels, few generic manufacturers serve both channels. Of the 876 generic firms in our data, 766 sell only in retail, 76 sell only in procurement, and 34 sell in both channels. Why many large, tendering generic firms do not sell through the retail channel is an important question for future research. Mean annual doses sold is larger in retail than procurement, again because of the large volume of anti-malarials and TB drugs in the retail sector.

4. Multivariate Regression Estimates

Table II reports pooled brand-channel regressions for log annual treatment price for our three country groups. Robust standard errors are clustered at the country level. Exponentiated coefficients (including a variance correction (Kennedy, 1981)) for indicator variables are in italics. Table III reports separate regressions by channel and brand status for the matched PCI-range countries. These channel-specific equations permit all coefficients to differ by brand and channel status and show effects of individual GPRM purchasers. Our discussion here is based mainly on the pooled regressions, with reference to the channel-specific regressions where relevant.

Table III.

Channel-specific effects of income, competition, and procurement on prices of HIV/AIDS, TB, and malaria drugs, 2004–2008, per capita income-range countries

| OLS regressions of log annual treatment price GPRM and IMS data | |||||

|---|---|---|---|---|---|

| Retail generic | Retail originator | Tender generic | Tender originator | ||

| Log per capita income | −0.378* | −0.0714 | 0.0345 | 0.316*** | |

| [0.200] | [0.283] | [0.0298] | [0.0466] | ||

| Gini coefficient | 0.0860*** | 0.0498*** | −0.000477 | −0.00184 | |

| [0.0172] | [0.0140] | [0.00354] | [0.00568] | ||

| Gini coefficient missing indicator | −0.264 | −0.0396 | 0.0220 | −0.0578 | |

| [0.289] | [0.486] | [0.0534] | [0.122] | ||

| HIV prevalence per 1K | −0.0173*** | −0.0169*** | 0.000574 | −0.00208** | |

| [0.00554] | [0.00200] | [0.000476] | [0.000905] | ||

| Log drug volume | −0.0411* | −0.0701** | −0.0671*** | −0.145*** | |

| [0.0190] | [0.0274] | [0.0130] | [0.0230] | ||

| Competition | Tendering generic firms in class‡ | 0.0997*** | −0.0682*** | 0.0224 | 0.0253 |

| [0.0217] | [0.0142] | [0.0168] | [0.0259] | ||

| Retail generic firms in class‡ | −0.0213*** | −0.00514 | § | § | |

| [0.00206] | [0.00415] | ||||

| Originator firms in class‡ | −0.0769 | 0.144*** | 0.0666*** | 0.00245 | |

| [0.0550] | [0.0392] | [0.0184] | [0.0417] | ||

| Originator present in molecule‡ | 0.328*** | # | 0.0791 | # | |

| [0.0903] | [0.0484] | ||||

| Suppliers | Supplier: UNICEF | −0.0817 | 0.138 | ||

| [0.0530] | [0.0997] | ||||

| Supplier: GlobalFund | 0.228*** | 0.213** | |||

| [0.0617] | [0.0989] | ||||

| Supplier: IDA | 0.203*** | 0.404*** | |||

| [0.0455] | [0.108] | ||||

| Supplier: Missionpharma | 0.194** | −0.0316 | |||

| [0.0870] | [0.115] | ||||

| Non-oral solid | 1.247*** | 1.318*** | 0.0276 | −0.346*** | |

| [0.252] | [0.299] | [0.0542] | [0.0713] | ||

| Molecule and year fixed effects | X | X | X | X | |

| Constant | 5.025** | 5.170* | 4.977*** | 5.063*** | |

| [2.099] | [2.614] | [0.357] | [0.463] | ||

| Observations | 737 | 714 | 3886 | 2088 | |

| R-squared | 0.882 | 0.807 | 0.734 | 0.503 | |

Robust standard errors adjusted for 37 clusters in country in brackets.

All competition measures are calculated within country-class-year, by channel.

There are (by definition) no retail-only firms in the tender channel.

The originator molecule flag is equal to one for every originator observation.

p < 0.1.

p < 0.05.

p < 0.01.

4.1. Brand and channel effects

For the all-countries sample, the price differentials, relative to retail originators, are −35.1% for retail generics, −71.2% for tendered originators, and −81.9% for tendered generics. For the matched PCI-range countries, the differentials relative to retail originators are −31.6 percent for retail generics (but not significant after controlling for volume), −42.4% for tendered originators, and −66.8% for tendered generics. Thus, although retail channel generics in MLICs on average charge 31.6% less than originators, the large variance implies statistical insignificance. By contrast, both originator and generic prices are significantly lower through procurement. These large procurement differentials plausibly reflect procurers' use of competitive tendering and the focus of competition on price, by requiring that suppliers meet WHO qualification to reduce quality risk. Originators may also be more willing to discount to the procurement channel due to reduced risk of price spillovers to high income purchasers in the same or other countries. Excluding volume does not significantly change these mean channel price differentials.

Volume: The average elasticity of price with respect to volume is −0.106 in the pooled estimates. The channel-specific estimates show slightly larger volume elasticities in procurement compared with retail pharmacy: −0.04 and −0.07 for retail generics and originators, respectively, and −0.067 and −0.145 for tendering generics and originators, respectively. Thus, contract volume contributes to lower procurement prices mainly for originators. However, these contract-specific volume elasticities do not capture the scale economies that may have resulted from the expansion of aggregate demand that was associated with procurement.

Income: The income elasticity of prices with respect to average PCI is 0.267 for the full range of countries and only 0.100 in MLICs, or far less than required to maintain prices proportional to PCI. In the channel-specific MLIC regressions, the income elasticity of originator prices is insignificant in the retail channel but 0.32 in the procurement channel, suggesting that originators are more willing to discount to low-income countries in the protected procurement context. The income elasticity of generic prices is insignificant in the procurement channel, as expected if tendering forces generics to price at marginal cost, which varies little across countries. By contrast, in the retail channel, the income elasticity of generics is negative, consistent with the hypothesis that price competition is ineffective in MLIC retail markets.

Income skewness also appears to contribute to higher prices in retail pharmacies in MLICs, but this effect is eliminated by procurement.19 The channel-specific regressions for PCI-range countries show a significant, positive skewness effect for both originator (0.05) and generic prices (0.086) in retail pharmacies but no significant effect in the procurement channel.20

Originator prices are significantly inversely related to HIV prevalence in MLICs, but the effect is small, with larger effects in the pharmacy channel than the GPRM channel.

Overall, this evidence implies that drugs in retail pharmacies are least affordable in the lowest income countries, due to insignificant or perverse PCI-based price differentials for originators and generics and positive skewness effects for both generics and originators. Procurement reduces drug prices on average and eliminates the regressive mean PCI and skewness effects.

Competition: In the all-countries, pooled channels regressions, the marginal effect of an additional tendering generic is to reduce drug prices by 4.5%, compared with only −0.89% for an additional retail generic. The smaller marginal effect for retail generics may partially reflect the much larger mean number of retail generics than tendering generics. Further, our count of tendering competitors may be downward biased, because it omits any who tendered unsuccessfully, unless they chose to sell to retail pharmacies in that country-class-year.

The channel-specific regressions shed further light on the nature of competition. The marginal effect of tendering generics is significantly negative (−0.068) for originator prices but positive for generic prices in the retail sector. By contrast, additional retail generics tend to lower average retail generic prices but have no effect on originator prices. This supports the hypothesis that in the retail channel, tendering generics are more effective competitors for originators and can charge high prices relative to retail generics because tendering generics are perceived to be relatively high quality. In the procurement channel, number of competitors appears to have no effect on prices. This conclusion is tentative due to only observing successful bidders.

Markets with the originator present have 36–44% higher prices on average. The channel-specific regressions confirm that generic prices in the retail channel are 38.3% higher when the molecule originator is present, consistent with shadow pricing by generics. Procurement eliminates this effect.

Retail originator prices are positively associated with the number of originator competitors, contrary to simple price competition models. This may reflect increased promotional spending by originators in crowded classes, which makes product-specific demand more inelastic; the estimates may also be upward biased for net prices if competition leads to increased discounting that is not fully captured by the IMS data. Although these estimates are also potentially upward biased by endogeneity, such bias is mitigated because originators face lengthy regulatory requirements and other delays in launching a new product, which could take at least 2 years. Entry decisions depend on expected prices over the multi-year life of a product, and rapid entry in response to a current price premium would be irrational if other competitors could easily enter and compete down the price.

Overall, this evidence suggests that competition on price is generally weak in retail pharmacies in MLICs. Having multiple originators in a class does not reduce retail prices on average. An additional retail generic has no significant effect on originator prices and a weak (−2.0%) effect on average generic prices. An additional tendering generic reduces originator prices by about 7%, but raises average generic prices, plausibly because tendering generics can charge relatively high prices due to their perceived higher quality. These results are consistent with models in which uncertain quality leads to competition on brand as a proxy for quality, rather than price competition.

Tendering purchaser effects: The channel-specific regressions show that the Global Fund and IDA pay at least 20% higher prices for both generic and originator drugs, and Missionpharma pays a similar premium for generics, compared with smaller purchasers (the omitted category). Given molecule, year, and volume controls, these effects cannot be attributed solely to differences in volume or drugs purchased by different purchasers. These purchaser differentials may reflect their intentional policies to pay prices sufficiently high to continue to attract multiple bidders to this market, which would be strategically rational for large purchasers. It is also possible that our DDD-corrected prices and form indicator do not adequately control for pediatric formulations that may be purchased disproportionately by some payers.21

4.2. Comprehensive anti-infective and cardiovascular class results

As a robustness check on our results for HIV, malaria, and TB drugs, Table IV reports regressions for the entire anti-infectives (J) and cardiovascular (C) classes, for retail originators and generics in the matched PCI-range countries.22 These drug categories are not centrally procured by NGOs, and hence no GPRM data are available. The dependent variable is log price per standard unit rather than log DDD-adjusted annual treatment price as we lacked DDD data for many drugs.

Table IV.

Effects of income, competition, and procurement on drug prices in retail pharmacies: all anti-infective (J) and cardiovascular (C) drugs, per capita income-range countries

| OLS regressions of log price per standard unit, 2004–2008 IMS data | ||||||

|---|---|---|---|---|---|---|

| HIV/AIDS, malaria, and TB drugs | Entire J class (anti-infectives) | Entire C class (cardiovascular) | ||||

| Generics | Originators | Generics | Originators | Generics | Originators | |

| Log per capita income | −0.591* | 0.126 | −0.274 | −0.944*** | −0.269 | −0.940*** |

| [0.272] | [0.341] | [0.303] | [0.160] | [0.287] | [0.125] | |

| Gini coefficient | 0.0738** | 0.0502** | 0.105** | 0.135*** | 0.107*** | 0.139*** |

| [0.0259] | [0.0185] | [0.0340] | [0.0149] | [0.0333] | [0.0119] | |

| Gini missing indicator | −0.54 | 0.145 | −0.825 | −2.052*** | −0.804 | −2.055*** |

| [0.393] | [0.583] | [0.533] | [0.260] | [0.512] | [0.215] | |

| HIV prevalence per 1K | −0.0108 | −0.0199*** | −0.0191** | −0.0242*** | −0.0192** | −0.0244*** |

| [0.00835] | [0.00288] | [0.00762] | [0.00266] | [0.00743] | [0.00207] | |

| Generic firms in class | −0.0123*** | −0.0134*** | −0.00405*** | −0.00227*** | −0.00442*** | −0.00203*** |

| [0.00331] | [0.00284] | [0.000846] | [0.000675] | [0.000966] | [0.000585] | |

| Originator firms in class | 0.00177 | 0.179*** | 0.00715 | −0.0362 | −0.0161 | −0.0566** |

| [0.0944] | [0.0541] | [0.0301] | [0.0290] | [0.0235] | [0.0232] | |

| Originator present in molecule | 0.165 | N/A | −0.11 | N/A | −0.0698 | N/A |

| [0.117] | N/A | [0.126] | N/A | [0.129] | N/A | |

| Generic present in molecule | N/A | −0.0657 | N/A | −0.113 | NA | −0.106 |

| N/A | [0.150] | N/A | [0.0921] | NA | [0.0801] | |

| Non-oral solid flag | 1.685*** | 1.501*** | 0.689*** | 0.621*** | −0.488** | −0.166 |

| [0.294] | [0.227] | [0.169] | [0.100] | [0.161] | [0.148] | |

| OTC flag | 1.057* | 0.887 | 0.505 | 0.631*** | 0.513 | 0.774*** |

| [0.526] | [0.510] | [0.620] | [0.167] | [0.608] | [0.126] | |

| Molecule and year fixed effects | X | X | X | X | X | X |

| Constant | 6.591* | 2.722 | −3.036 | 2.288* | −2.147 | 2.611*** |

| [3.004] | [2.935] | [2.828] | [1.090] | [2.668] | [0.715] | |

| Observations | 766 | 743 | 9207 | 4600 | 7597 | 3942 |

| R-squared | 0.847 | 0.773 | 0.764 | 0.804 | 0.76 | 0.793 |

Robust standard errors adjusted for 37 clusters in country in brackets.

p < 0.1.

p < 0.05.

p < 0.01.

Income elasticities of prices in both classes are significantly negative for originator drugs, whereas Gini coefficients are significantly positive. These estimates are tentative due to significant correlation between log PCI and Gini for these countries. In similar regressions for originators and generics combined for the entire income range of countries, the income elasticity for J and C class pharmacy drugs is around 0.3 and the Gini is insignificant.23

An additional generic competitor reduces generic prices by 0.4% and originator prices by 0.2% in both the J and C classes. Competition from other originators in the class reduces originator prices significantly only for the C class.

Thus, overall, the conclusions from the HIV/TB/malaria drugs are confirmed by these two very large classes. The at best small (0.0–0.3) income elasticity of drug prices implies that prices are least affordable, relative to income, in low-income countries. Income skewness exacerbates these effects. In MLICs, despite multiple competitors, price competition does not appear to be strong in retail channels, plausibly because competitors compete on brand rather than price due to quality uncertainty.

5. Conclusions

This evidence on ex-manufacturer prices for both originator and generic drugs suggests that income-related price discrimination and competition alone are unlikely to achieve affordable prices in low-income countries, within traditional distribution and institutional environments. Drug price elasticities with respect to mean PCI are small across the full income range of countries (0.0–0.3 for originators) but insignificant or negative in MLICs, implying that the poorest countries face the highest prices relative to their PCI. Skewed income distributions in MLICs exacerbate high drug prices relative in PCI. Competition from other originator drugs is largely ineffective in retail channels. Although generic prices are 31% below originator prices on average in MLICs, this differential is not statistically significant due to large variance, and partly reflects the lower and/or less certain quality of generics, not pure price competitiveness.24 A marginal retail generic competitor reduces average generic prices by 0.89%, with no effect on originator prices. By contrast, an additional tendering generic (a generic supplier that has met WHO quality standards and participated in procurement) reduces originator prices by 6.8%.

The evidence from HIV/AIDS, TB, and malaria drugs shows that procurement reduces originator and generic prices by 42.4% and 35%, compared with their respective retail pharmacy prices. Procurement reduces quality uncertainty by imposing minimum quality standards, thereby attracting multinational generic suppliers and focusing competition on price. Originators may also be more willing to grant discounts to procurement because this channel is less prone to price spillovers to other countries.

The findings for retail pharmacy prices of the HIV/AIDS, TB, and malaria drugs are confirmed by similar analysis of ex-manufacturer prices for the entire anti-infective and cardiovascular classes in pharmacies. These broad classes similarly show that prices in MLICs are largely unaffected by mean PCI and competition, and positively related to income skewness, for both generics and originators. This skewness-sensitive pricing of generics is inconsistent with the hypothesis that competition enforces marginal cost pricing by generics.

This evidence suggests that although price discrimination between MLICs countries could in theory be a profit-maximizing (and welfare enhancing) strategy for originators, and generics are widely available, PCI-related pricing is undermined if income distributions are skewed and/or competition focuses on brand, rather than price, due to asymmetric and uncertain quality of generics. Price discrimination within MLICs is unlikely to be feasible when drugs are sold to largely self-pay patients in retail pharmacy channels served by common distribution networks. Encouraging generics has limited benefit in retail channels as long as quality is uncertain. A protected procurement channel, with informed buyers who require minimum quality standards and price competition, can in theory achieve within-country price discrimination and thereby provide drugs at lower prices to targeted poor populations than is possible in the retail sector. Whether public hospitals, targeted insurance programs or other mechanisms might serve as such a protected channel for a broad range of drugs in at least some MLICs is an important question for future research. More generally, finding better mechanisms to enable differential pricing between and within low and middle income countries is an important challenge for firms and policymakers.

Acknowledgments

This research was supported in part by Eli Lilly Inc.'s Project on Fair Prices for Pharmaceuticals. The empirical analysis uses data obtained under license from the IMS Health Incorporated MIDAS™ database. We would like to thank these sponsors for making the research possible. The conclusions and views expressed herein are not necessarily those of Eli Lilly Inc. or IMS Health Inc.

Footnotes

‘Originator’ refers to a research-based, patentable product sold by the originating company, regardless of whether or not the product has a patent in a given market. ‘Generic’ refers to all other drugs, including both branded and unbranded copies.

An inverse relation between uncompensated price elasticity of demand for drugs and mean PCI is plausible if the income elasticity of demand for health is positive, even if the uncompensated price elasticity is invariant with income (Danzon et al., 2012, Hall and Jones, 2007).

Malueg and Schwartz (1994) show that price discrimination is both profit maximizing and welfare superior to uniform pricing, under plausible assumptions about demand dispersion across countries. Szymanski and Valletti (2005) and Valletti and Szymanski (2006) show that price discrimination also leads to more R&D and higher quality products than does uniform pricing. Applying Ramsey pricing principles to the problem of paying for the global joint cost of pharmaceutical R&D also supports the welfare superiority of pricing inversely to PCI, assuming that demand elasticities vary inversely with PCI across countries (Danzon, 1997; Jack and Lanjouw, 2005).

For example, in the US, pharmaceutical firms give voluntary rebates to private health plans for preferred formulary placement and mandatory rebates to some public payers. Brazil regulates prices to the private sector and mandates rebates to the public sector.

Danzon and Furukawa (2011) review literature and provide empirical evidence on generic markets in high and middle income countries.

For example, Section 3(d) of India's Patent Act denies patents for new formulations, combinations, and esters of existing molecules.

Frank and Salkever (1997) develop a segmentation model to show that originators may optimally raise price following generic entry, rather than engage in price competition with generics.

Several MLIC-branded generic firms have been acquired by originator, multinational pharmaceutical companies because of their attractive profit margins.

For most MLICs, IMS reports a single aggregate channel. When IMS reports retail and hospital channels separately, we aggregate to a single channel and calculate an average price weighted by volume.

When WHO DDDs were unavailable, we used recommended daily doses published in the medical literature.

Producer price indexes (PPIs) were available for some but not all countries. We estimated equations for countries with PPIs available, and results were similar to those reported here.

We calculate annual treatment cost by dividing the GPRM contract price and quantity after adjusting quantity by the WHO defined daily dose (DDD) to arrive at the number of annual treatment courses per contract. Our calculated annual treatment cost data closely match an estimate provided in the GPRM data for oral solid formulations. For other formulations, GPRM does not provide annual treatment cost.

Most combinations are ARVs, which include component ARVs of the same or different classes. These combinations were generally produced only by generic manufacturers selling to GPRM and are not in the IMS data. A few molecules have two observations, due to a non-oral solid form in addition to the oral solid form.

Benin, Burkina Faso, Cameroon, Congo, Cote d'Ivoire, Gabon, Guinea, Mali, Senegal, and Togo.

This assumes that the active ingredients of generics are globally traded, and local labor costs are negligible.

We also estimated regressions using a single, aggregated HIV/AIDS class to reflect potential competition between the four sub-classes. This specification had lower significance and explanatory power than the more detailed classification used.

The Clinton Foundation (CHAI) negotiates upper limits on supplier prices for countries that meet eligibility criteria. However, CHAI itself accounts for only 4% of the GPRM contracts. It contracted with IDA for purchase of its pediatric medicines and presumably contracts with other purchasers for adult medicines. Because the CHAI prices are a ceiling price and actual purchasers may negotiate lower prices, we use indicators for actual purchaser rather than CHAI eligibility of the recipient country, in contrast to Waning et al. (2009).

The 20.01 matched income range mean for retail generic competitors reflects high numbers in India and China. As an alternative proxy for potential competitors, we tried measuring competitors at the region-class, rather than country-class level. Regression results were similar but generally less significant than with the country-class measures reported here.

Estimated effects of skewness may be imprecise due to missing Gini data for several low-income countries and high correlation with log PCI for the MLIC countries: 0.51 for MLIC countries in IMS, 0.27 for GPRM countries, and 0.31 for all countries combined. Tests for restricted models do not support excluding the Gini indicators for retail generic and originator regressions.

Diagnostics to identify influential observations (dffits) did flag a small fraction of observations beyond a threshold of  , where p is the number of estimated parameters, and n is the number of observations. Omitting these observations had no significant effect on the coefficients reported in Table III.

, where p is the number of estimated parameters, and n is the number of observations. Omitting these observations had no significant effect on the coefficients reported in Table III.

Pediatric-specific DDDs were applied for clearly pediatric formulations, but some ambiguous cases remained.

Combination products are excluded from the full J-class and C-class analysis because these broad classes include many over-the-counter combination products.

Regressions available from authors.

This evidence from MLICs is consistent with theory and evidence from HICs that branded generics in retail markets tend to compete on brand rather than price (Danzon and Furukawa, 2011).

References

- Danzon P. Price discrimination for pharmaceuticals: welfare effects in the US and EU. International Journal Economics Business. 1997;4(3):301–321. [Google Scholar]

- Danzon PM, Chao L-W. Cross-national price differences for pharmaceuticals: how large and why? Journal of Health Economics. 2000a;19:159–195. doi: 10.1016/s0167-6296(99)00039-9. [DOI] [PubMed] [Google Scholar]

- Danzon P, Chao L-W. Does regulation drive out competition in markets for pharmaceuticals? Journal of Law and Economics. 2000b;43:311–358. [Google Scholar]

- Danzon P, Epstein A. 2009. Effects of Regulation on Drug Launch and Pricing in Interdependent Markets. NBER Working Paper 14041.

- Danzon P, Furukawa M. International prices and availability of pharmaceuticals in 2005. Health Affairs. 2008;27(1):221–233. doi: 10.1377/hlthaff.27.1.221. [DOI] [PubMed] [Google Scholar]

- Danzon P, Furukawa M. 2011. Cross-national Evidence on Generic Pharmaceuticals: Pharmacy vs. Physician-driven Markets. NBERWorking Paper 17226.

- Danzon P, Towse A. Differential pricing for pharmaceuticals: reconciling access, R&D and patents. International Journal Health Care Finance and Econ. 2003;3:183–205. doi: 10.1023/a:1025384819575. [DOI] [PubMed] [Google Scholar]

- Danzon P, et al. 2012. Value-based differential pricing: Efficient prices for drugs in a global context. NBER Working Paper 18593.

- Danzon P, Wang Y, Wang L. The impact of price regulation on the launch delay of new drugs: a study of twenty-five major markets in 1990s. Health Economics. 2012;14(3):269–292. doi: 10.1002/hec.931. [DOI] [PubMed] [Google Scholar]

- Flynn A, et al. An economic justification for open access to essential medicine patents in developing countries. Journal of Law, Medicine, and Ethics. 2009;Summer:184–208. doi: 10.1111/j.1748-720X.2009.00365.x. 2009. [DOI] [PubMed] [Google Scholar]

- Frank RG, Salkever DS. Generic entry and pricing of pharmaceuticals. Journal of Economics and Management Strategy. 1997;6(1):75–90. [Google Scholar]

- Hall RE, Jones CI. The value of life and the rise in health spending. QJE. 2007;122(1):39–72. [Google Scholar]

- Jack W, Lanjouw JO. Financing pharmaceutical innovation: how much should poor countries contribute? The World Bank Economic Review. 2005;19(1):45–67. [Google Scholar]

- Kapstein E, Busby J. 2009. Making markets for merit goods: the political economy of antiretrovirals. Center for Global Development Working Paper 179.

- Kennedy PE. 1981. Estimation with correctly interpreted dummy variables in semilogarithmic equations. AER.

- Malueg D, Schwartz M. Parallel imports, demand dispersion, and international price discrimination. Journal of International Economics. 1994;37:167–195. [Google Scholar]

- Maskus KE. 2001. Parallel Imports in Pharmaceuticals: Implications for Competition and Prices in Developing Countries. Final Report to World Intellectual Property Organization.

- Scherer FM, Watel J. 2001. Post-Trips Options for Access to Patented Medicines in Developing Countries. CMH Working Paper Series, Paper No. WG4: 1. Available at: http://www.whoindia.org/LinkFiles/Commision_on_Macroeconomic_and_Health_04_01.pdf.

- Szymanski S, Valletti T. Parallel trade, price discrimination, investment and price caps. Economic Policy. 2005;20(44):705–749. [Google Scholar]

- Valletti TM, Szymanski S. Parallel trade, international exhaustion and intellectual property rights: a welfare analysis. The Journal of Industrial Economics. 2006;54(4):499–526. [Google Scholar]

- Waning B, et al. Global strategies to reduce the price of anti-retroviral medicines: evidence from transactional databases. Bulletin of the World Health Organization. 2009;87(7) doi: 10.2471/BLT.08.058925. [DOI] [PMC free article] [PubMed] [Google Scholar]