Abstract

Background

Outpatient surgery is increasingly delivered at freestanding ambulatory surgery centers (ASCs), which are thought to deliver quality care at lower costs per episode. The objective of this study was to understand potential facilitators and/or barriers to the introduction of freestanding ASCs in the United States.

Methods

This is an observational study conducted from 2008–2010 using a 20% sample of Medicare claims. Potential determinants of ASC dissemination, including population, system, and legal factors, were compared between markets that always had ASCs, never had ASCs, and those that had new ASCs open during the study. Multivariable logistic regression was used to determine characteristics of markets associated with the opening of a new facility in a previously naïve market.

Results

New ASCs opened in 67 previously naïve markets between 2008 and 2010. ASCs were more likely to open in HSAs that were urban (adjusted OR 4.10; 95% CI 1.51–10.96), had higher per capita income (adjusted OR 3.83; 95% CI 1.43–10.45), and had less competition for outpatient surgery (adjusted OR 2.13; 95% CI 1.02–4.45). Legal considerations and latent need, as measured by case volumes of hospital-based outpatient surgery in 2007, were not associated with the opening of a new ASC.

Conclusions

Freestanding ASCs opened in advantageous socioeconomic environments with the least amount of competition. Because of their associated efficiency advantages, policymakers might consider strategies to promote ASC diffusion in disadvantaged markets to potentially improve access and reduce costs.

Keywords: hospital service area, healthcare market, policy, socioeconomic, regulatory, certificate of need, Herfindahl-Hirschman Index

Introduction

There are nearly 35 million outpatient procedure visits in the United States each year. Traditionally, the majority of these procedures occurred in hospital outpatient departments; however, the number of ambulatory surgery centers (ASCs) has increased dramatically over the last 15 years, such that almost half of all outpatient procedures are now performed in these facilities.1 Advantages of ASC-based care include enhanced patient convenience, improved provider productivity, and lower costs per surgical episode.2–9

Further proliferation of ASCs and continued migration of outpatient surgery to these facilities have the potential to improve the efficiency of the delivery system. In the early days of ASC growth, advances in technology (e.g., improvements in anesthesia, the development of minimally invasive techniques) helped broaden the types of procedures amenable to this delivery setting. More recently, changes in outpatient payment policy in accordance with the Medicare Prescription Drug, Improvement, and Modernization Act (MMA) and the Outpatient Prospective Payment Policy (OPPS)4 have also facilitated their diffusion by expanding the scope of procedures eligible for reimbursement.10 Additional factors, such as physician ownership of such facilities, also may incentivize volume creep of surgical procedures towards these facilities.11 While all of these factors have contributed to ASC proliferation, little is known about the market environments in which these facilities open. For instance, some markets may hinder the opening of a new ASC through stringent certificate of need regulations12,13 or hostile medical-legal climates.14 In contrast, markets with limited competition for outpatient surgical care may be ideal for promoting ASC diffusion due to an apparent lack of external market and regulatory forces.

To better understand market factors associated with ASC opening, we performed a retrospective cohort study using national Medicare data. Understanding the contemporary contextual barriers and/or facilitators will be important for guiding future policies aimed at rationalizing future ASC dissemination.

Methods

Data source

We performed a retrospective cohort study looking at the opening of freestanding Ambulatory Surgery Centers (ASCs) for the years 2008 through 2010 using a 20% sample of national Medicare claims. ASCs were explicitly identified using the Provider of Service (POS) File, which is maintained by the Centers for Medicare and Medicaid Services. We focused on this time period for two reasons. First, it includes most contemporary years of national Medicare data and is, thus, indicative of current practice. Second, and most importantly, Medicare payment policy changed dramatically with the passage of the Medicare Modernization Act of 2003. Effective January 1, 2008, the types of procedures eligible for Medicare payment in ASCs were greatly expanded, increasing the potential role of these facilities in previously untapped markets (i.e., those without any ASCs).4

Identifying healthcare markets in which an ASC entered

Our main outcome for this study was the opening of an ASC in a previously naive healthcare market, which we defined as a Hospital Service Area (HSA) without ASCs as of January 1, 2008. As described by the Dartmouth Atlas,15 each HSA represents a collection of zip codes in which Medicare beneficiaries receive the majority of their primary hospital care. We chose HSAs, as opposed to Hospital Referral Regions, because outpatient surgery is elective, discretionary, and low risk. Thus, patients are likely to undergo such procedures where they commonly receive most of their primary health care rather than where they would be referred for their tertiary care. With this approach, we were able to partition the HSAs in the U.S. into markets where ASCs were never present, those where new facilities opened for the first time during the study period, and those that contained at least one ASC prior to 2008. Extremely small healthcare markets (i.e., those with less than 1,000 inhabitants) were excluded to minimize statistical noise.

Conceptual framework for assessing ASC diffusion

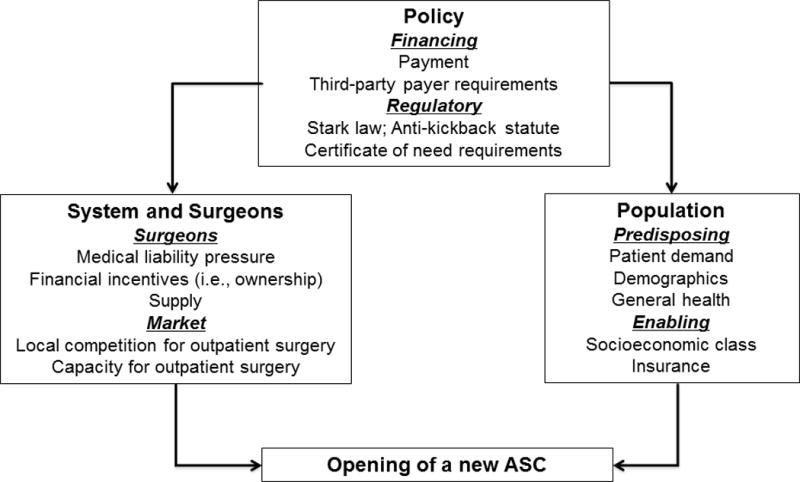

A principal purpose of ASCs is to improve the efficiency of surgical care by increasing quality, reducing costs, or both.2–9 Permitted via safe harbors to the Anti-kickback Statute,16–18 physicians have a financial stake in 90% of all ASCs and own 61% outright.11 Many believe that such organizational relationships, which create lucrative indirect revenue streams,19 are a means by which physicians can recoup lost income due to declining reimbursements.20 Because of this tight link between ASCs and surgeon ownership, our conceptual framework (Figure 1) for ASC diffusion is largely based on models related to utilization.21,22 Implicit in our model is the notion that there is an asymmetry of information between the supplier (i.e., surgeon) and the consumer (i.e., patient population in a healthcare market) such that the latter cannot make a rational choice as to the value of adding a new facility.23 In this context, the surgeon, generally with a monopoly on the information and resources necessary to decide to open a new ASC, controls the decision of adding a new facility.

Figure 1.

Conceptual diagram for ASC diffusion

Informed by our conceptual model, we next enumerated contextual factors from several external sources (i.e., Area Resource File,24 Medical Liability Monitor,25 National directory of Health Planning,26 and the Medical Malpractice Summary Index of States27) that are potentially associated with the opening of a new ASC. These factors are derived from 3 broad categories (i.e., population; system; and legal), and are further detailed in our taxonomy of potential determinants (Table 1). While a variety of factors (e.g., need based legislation, medical liability pressure) may impact a surgeon’s decision to invest in a new facility, we posit that markets with highly concentrated volumes of hospital-based outpatient surgery would be most fertile for ASC expansion into naïve markets. To test this hypothesis, our two key exposure variables consisted of rates of hospital-based outpatient surgery and a measure of concentration of outpatient surgical care, both measured at the HSA level. For the former, we assessed Carrier Standard Analytic File (SAF) claims in 2007 for any Healthcare Common Procedure Codes as the numerator and the eligible Medicare population residing in each HSA as the denominator. This variable served as a proxy for latent need and the potential reservoir of procedures that might be amenable to being delivered at an ASC. For the purpose of analysis, markets were sorted into three equal size groups ranging from less than 4,146 cases per 100,000 beneficiaries in the lowest tercile to more than 5,861 cases per 100,000 beneficiaries in the highest tercile. We assessed the competition or concentration of outpatient surgical care using the Herfindahl-Hirschman Index (HHI).28–30 The HHI, one of the most common measures of market competition, accounts for both the number and relative size of competing forces within an area, in this case ASCs within a HSA. Mathematically, the HHI is calculated by the sum of the squared market shares of all ASCs competing within each market.29 A low HHI (e.g., < 0.25) typically represents a less concentrated, more competitive market, while a high HHI (e.g., > 0.50) suggests a more concentrated market, less competitive market.

Table 1.

Taxonomy of variables potentially associated with contemporary ASC diffusion

| Characteristic | Variables | Data source |

|---|---|---|

| Population | ||

| Social and economic | Female head of household College education or higher Urban population Managed care penetration Per capita income White population |

Area Resource File(24) |

| Beneficiaries | Comorbidity | Carrier SAF |

| System | ||

| Latent need | Hospital-based outpatient procedures per 100,000 beneficiaries | |

| Capacity | Operating rooms per 100,000 population | Area Resource File(24) |

| Competition for outpatient surgery | Market concentration (Herfindahl-Hirschman Index) | Carrier, Outpatient SAFs |

| Legal | ||

| Regulatory | Certificate of need requirement | National Directory of Health Planning(26) |

| Legal | Maximum liability payment | Medical Liability Monitor(25) |

| Damage caps Statute of limitations |

Medical Malpractice Summary Index of States(27) | |

Statistical Analysis

We initially contrasted healthcare markets (ASCs always present, ASCs never present, ASC added for the first time) by the various population, system, and legal factors. Statistical inference was made using the chi square test. To better characterize the implications of latent need and market concentration of outpatient surgery for ASCs opening, we then limited our analysis to HSAs with no ASCs prior to January 1, 2008. With the HSA as our unit of analysis, we fit a logistic model to determine the association of our exposures of interest with the opening of an ASC during 2008 through 2010 in ASC naive markets. In order to ensure that our findings were consistent over time, a sensitivity analysis was performed using years 2002 through 2004. Because these findings were similar in directionality and magnitude, only our models using the most contemporary data are presented. All models were adjusted for the contextual factors described in Table 1.

All analyses were performed using SAS version 9.2 (SAS Institute, Cary, NC). The probability of a Type I error was set at 0.05 and all testing was 2-sided. This study was classified as exempt by the University of Michigan’s Institutional Review Board.

Results

Characteristics of each category of HSAs [i.e. HSAs where ASCs were always present (n=1,224), never present (n=1,702), and added for the first time (n=67)] are compared in Table 2. All population, system, and legal factors differed significantly between the three different HSA categories based on ASC status. Markets where ASCs opened were typified as having advantageous socioeconomic environments, more surgeons, and a higher concentration of outpatient facilities. Further, ASCs opened in generally more regulated (i.e., those governed by certificate of need laws) markets. Additional analyses found that an ample number of surgeons were present in each market type to support ASC presence and diffusion.

Table 2.

Population, system, and regulatory/legal characteristics of hospital service areas where ASCs were always present, never present, and introduced between 2008 and 2010.

| Characteristic | Hospital Service Areas | p-value | ||

|---|---|---|---|---|

| ASCs always present (n=1,224) |

ASCs never present (N=1,702) |

ASCs added (N=67) |

||

| Population | ||||

| Female head-of-household, % | ||||

| Less than 12.8% | 19 | 35 | 31 | <0.001 |

| 12.9% to 16.3% | 37 | 35 | 31 | |

| 16.4% or higher | 44 | 29 | 37 | |

| College education or higher, % | ||||

| 0%–13.8% | 13 | 46 | 22 | <0.001 |

| 13.9%–20.2% | 30 | 32 | 28 | |

| 20.3% + | 56 | 22 | 49 | |

| Urban population, % | ||||

| 0%–38.2% | 7 | 44 | 12 | <0.001 |

| 38.3%–67.3% | 30 | 38 | 43 | |

| 67.4% + | 62 | 18 | 45 | |

| Managed care penetration, % | ||||

| 0%–10.0% | 22 | 34 | 33 | <0.001 |

| 10.1%–20.8% | 33 | 36 | 34 | |

| 20.9% + | 45 | 29 | 33 | |

| Per capita income, % | ||||

| Less than $28,146 | 19 | 43 | 16 | <0.001 |

| $28,147 to $33,928 | 30 | 34 | 33 | |

| $33,929 + | 52 | 22 | 51 | |

| Beneficiaries with Charlson score 2+, % | ||||

| 0%–22.6% | 40 | 29 | 34 | <0.001 |

| 22.7%–26.2% | 32 | 36 | 34 | |

| 26.3% + | 28 | 36 | 31 | |

| Non-white population, % | ||||

| 0%–82.5% | 39 | 32 | 40 | <0.001 |

| 82.6%–92.2% | 27 | 34 | 28 | |

| 92.3% + | 34 | 34 | 31 | |

| System | ||||

| Hospital-based non-ASC outpatient procedures per 100,000 Medicare beneficiaries, % | ||||

| 0–4,146 | 60 | 30 | 42 | <0.001 |

| 4,147–5,860 | 27 | 35 | 27 | |

| 5,861 or more | 14 | 35 | 31 | |

| Operating rooms per 100,000 population, % | ||||

| Less than 6.8 | 33 | 32 | 40 | 0.114 |

| 6.9 to 12.3 | 38 | 35 | 34 | |

| 12.4 or more | 29 | 33 | 25 | |

| Market concentration for outpatient surgery (Herfindahl-Hirschman Index), % | ||||

| 0–0.24 | 29 | 31 | 21 | <0.001 |

| 0.25–0.49 | 42 | 47 | 52 | |

| 0.50 or higher | 29 | 22 | 27 | |

| Legal | ||||

| Certificate of need law, % | 63 | 73 | 76 | <0.001 |

| Maximum liability payment, % | ||||

| Less than $50,980 | 22 | 32 | 27 | <0.001 |

| $50,980 to $104,681 | 41 | 32 | 34 | |

| $104,682 or more | 37 | 35 | 39 | |

| Damage caps for liability, % | ||||

| Less than $500,000 | 34 | 26 | 33 | <0.001 |

| $500,000 to $1,000,000 | 28 | 25 | 39 | |

| $1,000,001 or more | 39 | 49 | 28 | |

| Statute of limitations, % | ||||

| 1 year | 21 | 16 | 15 | 0.011 |

| 2 years | 63 | 67 | 61 | |

| More than 2 years | 16 | 17 | 24 | |

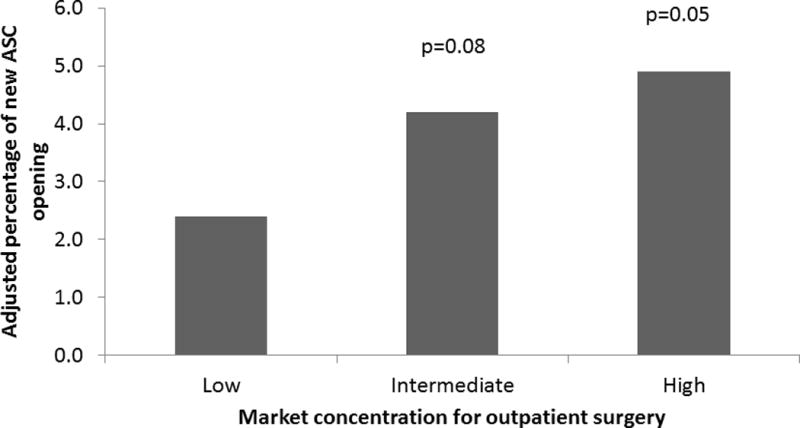

The results of the multivariable logistic model are shown in Table 3. Latent need for a new facility, as assessed by the volume of hospital-based outpatient procedures occurring in an HSA in 2007, was not associated with the opening of a new ASC. In contrast, the market concentration of facilities performing outpatient surgery in 2007, as measured by the HHI, was associated with the opening of a new facility in a previously naïve market. As further illustrated in Figure 2, those HSAs with the highest concentration of outpatient surgery, typifying less competitive markets, were more than twice as likely to open a new ASC than those in highly competitive, less concentrated regions [adjusted odds ratio (OR), 2.13; 95% confidence interval (CI),1.02–4.45). Additionally, markets with higher socioeconomic status were more likely to be associated with the opening of an ASC, as indicated by more urban environments (adjusted OR 4.10, 95% CI 1.51–10.96) and higher per capita income (adjusted OR 3.83, 95% CI 1.43–10.45).

Table 3.

Determinants of an ASC opening in a naïve healthcare market between 2008 and 2010.

| Characteristic | Strata | Beta Estimate (p value) |

Odds Ratio (95% Confidence Interval) |

|---|---|---|---|

| Population | |||

| Female head-of-household, % | Less than 12.8% | 1 | 1 |

| 12.9% to 16.3% | −0.22 (p=0.51) | 0.80 (0.40–1.55) | |

| 16.4% or higher | 0.07 (p=0.85) | 1.07 (0.53–2.23) | |

| College education or higher, % | 0%–13.8% | 1 | 1 |

| 13.9%–20.2% | 0.08 (p=0.84) | 1.08 (0.49–2.37) | |

| 20.3% or higher | 0.20 (p=0.67) | 1.22 (0.48–3.07) | |

| Urban population, % | 0%–38.2% | 1 | 1 |

| 38.3%–67.3% | 1.28 (p=0.0023) | 3.61 (1.58–8.13) | |

| 67.4% or higher | 1.41 (p=0.0062) | 4.10 (1.51–10.96) | |

| Managed care penetration, % | 0%–10.0% | 1 | 1 |

| 10.1%–20.8% | −0.14 (p=0.67) | 0.87 (0.46–1.66) | |

| 20.9% or higher | −0.45 (p=0.23) | 0.64 (0.31–1.32) | |

| Per capita income, % | Less than $28,146 | 1 | 1 |

| $28,147 to $33,928 | 0.83 (0.050) | 2.30 (1.02–5.31) | |

| $33,929 or higher | 1.34 (p=0.0078) | 3.83 (1.43–10.45) | |

| Beneficiaries with Charlson score 2+, % | 0%–22.6% | 1 | 1 |

| 22.7%–26.2% | 0.10 (p=0.77) | 1.11 (0.56–2.16) | |

| 26.3% or higher | 0.77 (p=0.84) | 1.08 (0.52–2.25) | |

| System | |||

| Hospital-based outpatient procedures per 100K beneficiaries, % | 0–4,146 | 1 | 1 |

| 4,147–5,860 | −0.33 (p=0.32) | 0.72 (0.38–1.38) | |

| 5,861 or more | −0.05 (p=0.88) | 0.95 (0.50–1.82) | |

| Operating rooms per 100,000 population, % | Less than 6.8 | 1 | 1 |

| 6.9 to 12.3 | −0.32 (p=0.30) | 0.73 (0.40–1.35) | |

| 12.4 or more | −0.52 (p=0.14) | 0.60 (0.30–1.21) | |

| Market concentration for outpatient surgery (Herfindahl Index), % | 0–0.24 | 1 | 1 |

| 0.25–0.49 | 0.58 (p=0.080) | 1.79 (0.93–3.43) | |

| 0.50 or higher | 0.76 (p=0.048) | 2.13 (1.02–4.45) | |

| Legal | |||

| Certificate of need law, % | No | 1 | 1 |

| Yes | 0.27 (p=0.46) | 1.31 (0.65–2.62) | |

| Maximum liability payment, % | Less than $50,980 | 1 | 1 |

| $50,980 to $104,681 | 0.14 (p=0.71) | 1.15 (0.56–2.36) | |

| $104,682 or more | 0.12 (p=0.74) | 1.13 (0.57–2.31) | |

| Damage caps for liability, % | Less than $500,000 | 1 | 1 |

| $500,000 to $1,000,000 | 0.34 (p=0.35) | 1.40 (0.70–2.89) | |

| $1,000,001 or more | −0.69 (p=0.065) | 0.50 (0.24–1.04) | |

| Statute of limitations, % | 1 year | 1 | 1 |

| 2 years | 0.22 (p=0.62) | 1.24 (0.52–2.85) | |

| More than 2 years | 0.25 (p=0.60) | 1.28 (0.49–3.24) | |

Figure 2.

The association between concentration of outpatient surgical facilities and the opening of an ASC in a new market. P values are reported relative to the low concentration group.

Discussion

Markets where freestanding ASCs opened for the first time had advantageous socioeconomic environments and a higher concentration of outpatient facilities, indicative of lower competition. The medical-legal and regulatory milieu within an HSA, however, was not associated with ASC diffusion. Surprisingly, the latent need for outpatient surgery delivery settings, as measured by the case volumes of hospital-based outpatient surgery, was not linked to decisions to open up a new ASC in naïve markets. Collectively, our findings suggest that freestanding ASCs opened in markets that were economically advantageous, and these decisions were largely independent of the regulatory climate.

Although the literature surrounding ASCs and their value to the delivery system is sparse, much of the focus has centered on the issue of physician-ownership and the associated financial incentives.10,31–33 This study is unique in that it takes a comprehensive approach in looking at the potential mediators of ASC diffusion. Paramount among these conditions is the local market competition for outpatient surgery. From a policy perspective, competition is generally viewed as favorable, as it is associated with lower costs and higher quality. However, this is not always the case in healthcare.34

In order to better understand competition in healthcare, it is helpful to examine the organizational population wherein ASCs are adopted. An organizational population is defined as a group of organizations that have the same form and depend on the same resources.35 Hospitals and ASCs, for example, are members of different organizational populations, as ASCs differentiate themselves from hospitals by focusing on narrow product lines (i.e., a subset of outpatient procedures) and operate more efficiently than a general organization (i.e., a hospital providing a multiproduct service).36,37 For this reason, we chose to evaluate ASC competition according to the concentration of outpatient surgical facilities (which occupy a similar organizational population or niche). Our findings indicate that ASCs tend to enter into HSAs with higher concentrations of outpatient surgical facilities, which is indicative of markets with less competition. Others have looked at ASC competition in the context of inpatient hospital facilities (which occupy a separate organizational population or niche), and have found similar results.38

Independent of our findings related to market competition, our study also noted an important association with socioeconomic class and no relationship with the legal milieu within a HSA. First, we found that the socioeconomics of a region were important determinants of ASC diffusion, with facilities preferentially entering into markets typified by being more urban and with higher per capita incomes. This finding is supported by our previous work using state level data that demonstrated that patients of lower socioeconomic class were significantly less likely to have their outpatient procedures in ASCs compared to hospitals.39 In terms of policy, this finding is important from the perspective of access and inequality insofar as copayments for ASCs are often lower than those associated with hospital-based outpatient surgery. Second, neither the regulatory nor medical-legal characteristics of an HSA were associated with the diffusion of ASCs. In particular, state-level need-based legislation, as determined by the presence of an active certificate of need law, was not associated with ASC dissemination. Previous work by our group and by others has questioned the value of certificate of need laws to curtail the unfettered addition of capacity in a variety of contexts.12,40,41 Collectively, these data suggest that opportunity for a return on investment, as typified by advantageous socioeconomic and noncompetitive climates, trump the regulatory milieu in terms of determining where these facilities open.

This study should be interpreted with two limitations in mind. First and foremost, because we rely on Medicare data, our findings are generalizable to facilities that are Medicare-certified and deliver care to its beneficiaries. However, Medicare is the largest payer of healthcare in the US and a bellwether in terms of health policy. Thus, our findings are generalizable to the largest and most policy relevant group. Second, we do not directly assess the inherent financial incentives associated with opening an ASC. We acknowledge the nature and extent of these incentives likely vary from facility to facility. Nevertheless, almost all ASCs are owned, at least in part, by the physicians who staff them. For this reason, we do not view this as a major weakness.

Conclusions

Freestanding ASCs enter into markets that are economically advantageous and less competitive. Insofar as these facilities deliver the same care at a lower cost, policymakers should consider strategies for promoting their dissemination in economically disadvantaged areas, which may improve access and reduce out-of-pocket expenses for beneficiaries while simultaneously enhancing the efficiency of the outpatient surgery delivery system.

Acknowledgments

This work was supported by funding from the Agency for Healthcare Research and Quality (R01 HS18726) to Dr. Hollenbeck. The views expressed herein do not necessarily represent the views of the Center for Medicare and Medicaid Services or the United States Government.

Funding: AHRQ R01 HS018726, NIH/NIDDK Grant T32 DK07782

Contributor Information

Anne M. Suskind, Email: suskina@med.ucmich.edu.

Yun Zhang, Email: seanyz@med.umich.edu.

Rodney L. Dunn, Email: rldunn@med.umich.edu.

John M. Hollingsworth, Email: kinks@med.umich.edu.

Seth A. Strope, Email: stropes@wudosis.wustl.edu.

References

- 1.Cullen KA, Hall MJ, Golosinskiy A. Ambulatory surgery in the United States, 2006. National health statistics reports. 2009 Jan 28;(11):1–25. [PubMed] [Google Scholar]

- 2.Hollingsworth JM, Saigal CS, Lai JC, Dunn RL, Strope SA, Hollenbeck BK. Surgical quality among Medicare beneficiaries undergoing outpatient urological surgery. The Journal of urology. 2012 Oct;188(4):1274–1278. doi: 10.1016/j.juro.2012.06.031. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 3.Hollingsworth JM, Saigal CS, Lai JC, Dunn RL, Strope SA, Hollenbeck BK. Medicare payments for outpatient urological surgery by location of care. The Journal of urology. 2012 Dec;188(6):2323–2327. doi: 10.1016/j.juro.2012.08.031. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Centers for Medicaire and Medicaid Services. Ambulatory Surgical Center Fee Schedule; payment system fact sheet series. 2013 http://www.cms.gov/Outreach-and-Education/Medicare-Learning-Network-MLN/MLNProducts/downloads/AmbSurgCtrFeepymtfctsht508-09.pdf.

- 5.Merrill DG, Laur JJ. Management by outcomes: efficiency and operational success in the ambulatory surgery center. Anesthesiol Clin. 2010 Jun;28(2):329–351. doi: 10.1016/j.anclin.2010.02.012. [DOI] [PubMed] [Google Scholar]

- 6.Grisel J, Arjmand E. Comparing quality at an ambulatory surgery center and a hospital-based facility: preliminary findings. Otolaryngology–head and neck surgery: official journal of American Academy of Otolaryngology-Head and Neck Surgery. 2009 Dec;141(6):701–709. doi: 10.1016/j.otohns.2009.09.002. [DOI] [PubMed] [Google Scholar]

- 7.Shah RK, Welborn L, Ashktorab S, Stringer E, Zalzal GH. Safety and outcomes of outpatient pediatric otolaryngology procedures at an ambulatory surgery center. The Laryngoscope. 2008 Nov;118(11):1937–1940. doi: 10.1097/MLG.0b013e3181817b9a. [DOI] [PubMed] [Google Scholar]

- 8.Frakes JT. The ambulatory endoscopy center (AEC): what it can do for your gastroenterology practice. Gastrointest Endosc Clin N Am. 2006 Oct;16(4):687–694. doi: 10.1016/j.giec.2006.08.007. [DOI] [PubMed] [Google Scholar]

- 9.Frakes JT. Outpatient endoscopy. The case for the ambulatory surgery center. Gastrointest Endosc Clin N Am. 2002 Apr;12(2):215–227. doi: 10.1016/s1052-5157(01)00004-6. [DOI] [PubMed] [Google Scholar]

- 10.Casalino LP, Devers KJ, Brewster LR. Focused factories? Physician-owned specialty facilities. Health Aff (Millwood) 2003 Nov-Dec;22(6):56–67. doi: 10.1377/hlthaff.22.6.56. [DOI] [PubMed] [Google Scholar]

- 11.Ambulatory Surgery Center Association. Ambulatory surgery centers: A positive trend in health care. http://www.ascassociation.org/ASCA/Resources/ViewDocument/?DocumentKey=7d8441a1-82dd-47b9-b626-8563dc31930c.

- 12.Smith PC, Forgione DA. The development of certificate of need legislation. Journal of health care finance. 2009 Winter;36(2):35–44. [PubMed] [Google Scholar]

- 13.Smith LN. Certificate of need programs: inflationary and anti-competitive for healthcare. Tennessee medicine : journal of the Tennessee Medical Association. 2009 Sep;102(9):47–48. [PubMed] [Google Scholar]

- 14.Rylko-Bauer B, Farmer P. Managed care or managed inequality? A call for critiques of market-based medicine. Medical anthropology quarterly. 2002 Dec;16(4):476–502. doi: 10.1525/maq.2002.16.4.476. [DOI] [PubMed] [Google Scholar]

- 15.Dartmouth. http://www.dartmouthatlas.org/tools/downloads.aspx. 2011. Accessed October 3, 2011, 2011.

- 16.General OoI. Clarification of the initial OIG safe harbor provisions and establishment of additional safe harbor provisions under the Anti-kickback Statue. [PubMed] [Google Scholar]

- 17.Becker S, Biala M. Ambulatory surgery centers–current business and legal issues. Journal of health care finance. 2000 Winter;27(2):1–7. [PubMed] [Google Scholar]

- 18.Choudhry S, Choudhry NK, Brennan TA. Specialty versus community hospitals: what role for the law? Health Aff (Millwood) 2005 Jul-Dec;:W5–361–372. doi: 10.1377/hlthaff.w5.361. Suppl Web Exclusives. [DOI] [PubMed] [Google Scholar]

- 19.Schlossberg S. Supergroups and economies of scale. The Urologic clinics of North America. 2009 Feb;36(1):95–100. vii. doi: 10.1016/j.ucl.2008.08.002. [DOI] [PubMed] [Google Scholar]

- 20.Pham HH, Devers KJ, May JH, Berenson R. Financial pressures spur physician entrepreneurialism. Health Aff (Millwood) 2004 Mar-Apr;23(2):70–81. doi: 10.1377/hlthaff.23.2.70. [DOI] [PubMed] [Google Scholar]

- 21.Aday L. Introduction to heatlh services. New York: Delmar; 1993. [Google Scholar]

- 22.Penchansky R, Thomas JW. The concept of access: definition and relationship to consumer satisfaction. Medical care. 1981 Feb;19(2):127–140. doi: 10.1097/00005650-198102000-00001. [DOI] [PubMed] [Google Scholar]

- 23.Wennberg JE, Barnes BA, Zubkoff M. Professional uncertainty and the problem of supplier-induced demand. Soc Sci Med. 1982;16(7):811–824. doi: 10.1016/0277-9536(82)90234-9. [DOI] [PubMed] [Google Scholar]

- 24.U.S. Department of Health and Human Services F. Area Resource File (ARF); National county-level Health Resource Information Database. 2012 http://arf.hrsa.gov/. Accessed January 4, 2012.

- 25.Medical Liability Monitor. Chicago: 2000–2010. [Google Scholar]

- 26.National Directory of Health Planning, Policy and Regulatory Agencies (2001, 2003, 2007) Falls Church, VA: American Health Planning Association; 2007. [Google Scholar]

- 27.McCullough, Campbell, Lane, LLP. Medical Malpractice Summary Index of States. 2013 http://www.mcandl.com/states.html. Accessed January 3, 2013, 2013.

- 28.Mas-Colell A, Whinston MD, Green JR. Microeconomic Theory. New York: Oxford University Press; 1995. [Google Scholar]

- 29.Baker LC. Measuring competition in health care markets. Health services research. 2001 Apr;36(1 Pt 2):223–251. [PMC free article] [PubMed] [Google Scholar]

- 30.Schneider JE, Li P, Klepser DG, Peterson NA, Brown TT, Scheffler RM. The effect of physician and health plan market concentration on prices in commercial health insurance markets. International journal of health care finance and economics. 2008 Mar;8(1):13–26. doi: 10.1007/s10754-007-9029-4. [DOI] [PubMed] [Google Scholar]

- 31.Iglehart JK. The emergence of physician-owned specialty hospitals. The New England journal of medicine. 2005 Jan 6;352(1):78–84. doi: 10.1056/NEJMhpr043631. [DOI] [PubMed] [Google Scholar]

- 32.Hollingsworth JM, Ye Z, Strope SA, Krein SL, Hollenbeck AT, Hollenbeck BK. Physician-ownership of ambulatory surgery centers linked to higher volume of surgeries. Health Aff (Millwood) 2010 Apr;29(4):683–689. doi: 10.1377/hlthaff.2008.0567. [DOI] [PubMed] [Google Scholar]

- 33.Hollingsworth JM, Krein SL, Ye Z, Kim HM, Hollenbeck BK. Opening of ambulatory surgery centers and procedure use in elderly patients: data from Florida. Arch Surg. 2011 Feb;146(2):187–193. doi: 10.1001/archsurg.2010.335. [DOI] [PubMed] [Google Scholar]

- 34.Morrisey MA. Competition in hospital and health insurance markets: a review and research agenda. Health services research. 2001 Apr;36(1 Pt 2):191–221. [PMC free article] [PubMed] [Google Scholar]

- 35.Lazzeretti L. Density dependence dynamics in the Arezzo jewelry district (1947–2001): Focus on foundings. European Planning Studies. 2006;14(4):431–458. [Google Scholar]

- 36.Al-Amin M, Housman M. Ambulatory surgery center and general hospital competition: entry decisions and strategic choices. Health care management review. 2012 Jul-Sep;37(3):223–234. doi: 10.1097/HMR.0b013e318235ed31. [DOI] [PubMed] [Google Scholar]

- 37.Skinner W. The focused factory. Harvard Business Review. 1974;52(3):113–121. [Google Scholar]

- 38.Bian J, Morrisey MA. HMO penetration, hospital competition, and growth of ambulatory surgery centers. Health care financing review. 2006 Summer;27(4):111–122. [PMC free article] [PubMed] [Google Scholar]

- 39.Strope SA, Sarma A, Ye Z, Wei JT, Hollenbeck BK. Disparities in the use of ambulatory surgical centers: a cross sectional study. BMC health services research. 2009;9:121. doi: 10.1186/1472-6963-9-121. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 40.Jacobs BL, Zhang Y, Skolarus TA, et al. Certificate of need legislation and the dissemination of robotic surgery for prostate cancer. The Journal of urology. 2013 Jan;189(1):80–85. doi: 10.1016/j.juro.2012.08.185. [DOI] [PubMed] [Google Scholar]

- 41.Jacobs BL, Zhang Y, Skolarus TA, et al. Certificate of need regulations and the diffusion of intensity-modulated radiotherapy. Urology. 2012 Nov;80(5):1015–1020. doi: 10.1016/j.urology.2012.07.042. [DOI] [PMC free article] [PubMed] [Google Scholar]