Abstract

Objectives

To assess whether the Affordable Care Act’s (ACA) dependent coverage health insurance mandate had a spillover impact on young adult dental insurance coverage and whether any observed effects varied by household income.

Data

Medical Expenditure Panel Surveys from 2006 through 2011.

Study Design

We employed a difference-in-difference regression approach comparing changes in insurance rates for young adults ages 19–25 years to changes in insurance rates for adults ages 27–30 years. Separate regressions were estimated by categories of household income as a percentage of the Federal Poverty Level (FPL) to understand whether the mandate had heterogeneous spillover effects.

Results

Private dental insurance increased by 6.7 percentage points among young adults compared to a control group of 27–30-year olds. Increases were concentrated at middle-income levels (125–400 percent FPL).

Conclusions

The dependent coverage mandate provision of the Affordable Care Act has not only increased health insurance rates among young adults but also dental insurance coverage rates.

Keywords: Affordable Care Act, dependent coverage mandate, dental insurance

The Patient Protection and Affordable Care Act (ACA) law that passed in 2010 includes many direct changes to the health insurance market and represents the most comprehensive overhaul of the U.S. health care system in recent history. The primary goal of this reform is to increase access to health insurance for U.S. residents, and the law includes many provisions aimed at achieving this goal. For example, insurance companies must issue policies to individuals regardless of health status, and marketplaces have been established for each state to facilitate the purchase of insurance and to allocate tax credits based on household income. One of the first provisions of the ACA to take effect was a change requiring insurers to allow young adults up to age 26 to remain on their parents’ health insurance policies (“dependent coverage mandate”). This change became effective on September 23, 2010, and it only applies to private insurance policies. Recent studies have documented a substantial increase in insurance coverage among persons aged 19–25 years, the population directly impacted by this mandate (Collins et al. 2013). However, little is known about possible spillover effects of this mandate on other employee/dependent benefits. Policy changes that affect the insurance industry and employers to this extent may have unanticipated consequences and potential spillover effects. Thus, it is important for researchers to understand and address possible spillover effects due to the ACA.

Our goal in this paper was to investigate spillover effects in private dental insurance coverage as a result of the ACA policy allowing young adults to remain on parental policies. While the ACA mandate applies only to medical insurance and not to stand-alone dental plans, there are several pathways through which the policy could impact dental coverage. To the extent that dental coverage is included or embedded as part of a medical insurance plan, the mandate would apply directly and would tend to increase dental coverage rates among young adults given the aforementioned gains in young adult health insurance coverage. However, recent survey evidence from the National Association of Dental Plans and Delta Dental Plans Association (Mayer 2013) puts the percentage of dental benefits provided through medical policies at less than 1 percent. The impact of the mandate is indirect and unclear in cases where companies offer only stand-alone dental policies. If employers expect the inclusion of young adults in health insurance plans to increase overall health care costs, they might compensate by lowering wages, by reducing other stand-alone benefits such as dental coverage, or by increasing employee premium contributions for benefits. Such tradeoffs are consistent with the economic theory of compensating differentials, according to which the value of the total compensation package that a worker receives is equal to his/her productivity. Indeed, several prior studies have shown that regulations that mandate increases in the generosity of health insurance coverage provided by employers tend to reduce wages and other fringe benefits (Gruber 1994; Jensen and Morrisey 1999; Miller 2004). Alternatively, if the additional cost of covering young adults is low, employers may allow dependents to be included not only in health insurance plans but also in some or all of the employers’ relevant menu of stand-alone benefits, including dental insurance. Further, employers may choose to apply uniform rules about covering dependents on medical and dental insurance plans to avoid administrative complexity and provide employees consistency. Therefore, the overall impact of the dependent coverage mandate on dental coverage rates is theoretically ambiguous.

To our knowledge, no research to date has evaluated the potential effect of the ACA’s dependent coverage mandate on dental coverage among young adults. This evaluation comes at an important juncture in terms of dental insurance and utilization. Trends in dental insurance coverage since 2000 have varied widely by age group. Children under the age of 19 have seen an increase in dental coverage between 2000 and 2010, primarily due to dental benefits being required as part of the State Children’s Health Insurance Program and Medicaid (Vujicic, Goodell, and Nasseh 2013). By contrast, private dental coverage has declined for adults between 2000 and 2010 with the most significant declines occurring for young adults ages 19–34 (Vujicic, Goodell, and Nasseh 2013). This drop in private dental coverage among nonelderly adults has been shown to be associated with an increase in the rate of public or no insurance (Vujicic and Nasseh 2014). Utilization trends mirror coverage trends from 2000 to 2010. Wall, Vujicic, and Nasseh (2012) show a divergence by age group in terms of percentage of the population that has had a dental visit in the past year. Children (ages 2–20) experienced a 4 percentage point increase in the likelihood of a dental visit between 2000 and 2010, while adults (ages 21–64) experienced a 5 percentage point decline. Having dental insurance drastically alters utilization; 57 percent of individuals with private coverage visit a dentist at least once a year versus 27 percent of those with no coverage (American Dental Association 2012). Several studies have shown that increasing coverage of dental benefits leads to increased utilization of dental services. For example, Choi (2011) finds a significant (16–22 percent) increase in the likelihood of a dental visit within a year of gaining Medicaid coverage. Nasseh and Vujicic (2013) evaluate the 2006 Massachusetts expansion of dental benefits to low-income adults and find an 11 percentage point increase in dental care use among the targeted group of poor nonelderly adults compared to nonpoor adults. Studies have also shown that reducing or eliminating dental benefits among adults leads to significant reductions in access to care and increases in dental-related emergency department use (Pryor and Monopoli 2005; Maiuro 2011; Wallace et al. 2011). Therefore, examining whether the ACA dependent coverage mandate will enhance or counteract the downward trend in young adult dental insurance coverage is an important policy question.

In addition to evaluating the overall impact of the dependent coverage mandate on private dental coverage, we also examine whether this impact varies by household income. The cost of dental care can be a significant barrier to access for low-income adults; low income is associated with less dental service utilization among adults (Vujicic and Nasseh 2014) and, therefore, dental insurance may be particularly important for low-income persons. While the dependent coverage mandate has the potential to affect coverage rates for all income groups, the magnitude of the policy’s impact may vary by income. Indeed, in the case of medical insurance, there is evidence that this mandate has increased overall rates of health insurance among young adults (Cantor et al. 2012; Sommers and Kronick 2012; Antwi, Moriya, and Simon 2013; Sommers et al. 2013), and at the same time, it has had heterogeneous effects by income. Shane and Ayyagari (2014) show that low-income groups benefited the most from this mandate; insurance rates increased by 12 percentage points among young adults with income less than 133 percent of the federal poverty level (FPL), by 9 percentage points for persons between 133 and 400 percent of FPL, and by 6 percentage points for persons with income greater than 400 percent of FPL. Therefore, it is plausible that any potential spillover effects on dental benefits would also differ by income.

Methods

Beginning in September 2010, dependents up to age 26 were allowed to remain on private parental health insurance policies. This was one of the earliest parts of the ACA to take effect and was the only significant policy change to affect private health insurance for young adults during that time. We leverage this quasi-experiment to evaluate whether the dependent coverage policy also influenced private dental coverage among young adults. We examine dental coverage rates among a nationally representative sample of 19–25-year olds in the years prior to the mandate and in the year after the policy took effect. If the dependent coverage policy impacted private dental coverage, we should find a significant difference in the postpolicy period. To factor in changes unrelated to the ACA policy that may have also influenced private dental coverage, we evaluate an additional cohort: a nationally representative sample of 27–30-year-old individuals. The cohort of 27–30-year olds overlaps closely with 19–25-year olds in key socioeconomic indicators and in terms of overall health status. As 27–30-year olds were not affected by the dependent coverage mandate, any changes in dental coverage not driven by the ACA policy would likely affect this group as well as the 19–25-year-old cohort. Therefore, comparing changes in private dental coverage rates between the two groups before and after the ACA policy took effect offers a way to identify the impact of the policy while controlling for other trends.

Data

We use data from the Medical Expenditure Panel Survey (MEPS), a nationally representative survey of families and individuals across the United States. The MEPS collects detailed information on health insurance status, demographics, income, and employment during five interview rounds over a period of 2 years. Information from interview rounds occurring during a single calendar year is aggregated to create a summary measure for the entire year. For MEPS respondents indicating health insurance coverage through a private plan, respondents are asked to list all other benefits that are included as part of their establishment benefit package. Dental insurance is one of the available options for survey respondents (e.g., other options include prescription drug coverage and vision benefits). We therefore identify the individuals indicating they have private dental insurance during each calendar year as part of a comprehensive establishment benefits package. We cannot, however, distinguish whether dental coverage was embedded into the medical insurance plan or was a stand-alone offering. Recent evidence (Mayer 2013), however, suggests that the vast majority of dental benefits through employers are stand-alone plans.

To evaluate annual changes in private dental coverage due to the dependent coverage mandate, we obtain information on pre-ACA coverage from the 2006 through 2009 waves of MEPS and on post-ACA coverage from the 2011 wave of MEPS. Renewable health insurance policies as of September 2010 were eligible for the change in young adult enrollment status, leaving 2011 as the first full year for the young adult policy change to take effect and the first potential year of spillover effects. As our analysis is based on annual changes in coverage and the policy was in effect only for the last few months of 2010, we do not include data from 2010. This avoids any confusion on whether to classify 2010 as a pre-ACA year or a post-ACA year.

Sample Selection

Our sample is restricted to individuals aged 19–30 years. Individuals who were exactly 26 years old at the time of the survey are excluded as we cannot confirm age at the time of the parent’s policy renewal and therefore, cannot determine whether the mandate would apply. We also exclude 286 observations due to missing education status. The dependent coverage mandate only affected private health insurance plans and our measure of dental coverage is also strictly via private establishment plans. Thus, we exclude persons with any public health insurance. Our results are robust, however, to including individuals with public insurance in our policy evaluation regressions. The final analysis sample consists of 19,948 observations that meet the sample selection criteria. Of these, 12,587 belong to the “treatment group” of persons aged 19–25 years and 7,361 belong to “control” group of persons aged 27–30 years.

Statistical Approach

We use a difference-in-difference regression approach that compares the change in private dental insurance rates among persons aged 19–25 years with those for persons aged 27–30. We estimate the following linear regression model:

| 1 |

The dependent variable in equation 1 (DINSit) is a binary indicator which takes the value 1 if individual i has private dental coverage in year t, and 0 otherwise. The variable (YOUNG ADULTit) is a binary indicator that takes the value 1 if individual i belongs to the 19–25 age group and takes the value 0 if individual i belongs to the 27–30 age group. The variable POST ACAt is a binary indicator for observations in 2011, the post-ACA implementation year. The coefficient β2 captures mean differences in dental insurance coverage between 19–25-year olds and 27–30-year olds, while β3 captures secular trends in insurance coverage between 2006 and 2009 (pre-ACA) and 2011 (post-ACA). The main parameter of interest is the coefficient on the interaction term (β1), which represents the change over time in private dental insurance rates for persons aged 19–25 years, compared to those aged 27–30 years. A positive and significant coefficient on β1 indicates that dental insurance coverage for 19–25-year olds increased at a greater rate post-ACA compared to 27–30-year olds. Under the assumption that no other factors were associated with differential trends in private dental insurance for the treatment and control groups, such evidence would suggest that the dependent coverage mandate was effective not only in increasing health insurance coverage rates for young adults but also dental coverage. Given that this was the only policy change affecting young adults during this period, this is a plausible assumption. However, we also perform additional robustness checks to evaluate the sensitivity of our results to alternative assumptions. All statistical analyses include survey weights and clustered standard errors to account for the complex survey design and were performed using STATA version 12 (StataCorp LP 2011).

To identify possible heterogeneity in the impact of the dependent coverage mandate by household income, we estimate equation 1 separately for the following income categories: <125 percent of Federal Poverty Level (FPL), 125–400 percent of FPL, and >400 percent of FPL. We then test for statistically significant differences in the impact of the mandate, captured by the coefficient β1, across these three subpopulations.

Results

Table1 offers a comparison of the key characteristics of the targeted group of young adults versus the older cohort unaffected by the ACA policy change. Not surprisingly, there are significant differences in the two groups by education level and marital status. Women are also slightly more likely to be represented in the older cohort and personal wage income is higher. We include the listed traits as covariates (represented by  ) in our difference-in-difference estimation to account for possible differential trends across the relevant time periods for these characteristics.

) in our difference-in-difference estimation to account for possible differential trends across the relevant time periods for these characteristics.

Table 1.

Descriptive Characteristics of Affected ACA Group and Older Control Cohort† (n = 19,935)

| Variable | Definition | 19–25 | 27–30 |

|---|---|---|---|

| Mean | Mean | ||

| Demographic/socioeconomic | |||

| Age | Age in years | 22.10 | 28.50** |

| Female | 1 if female | 0.45 | 0.48** |

| Black | 1 if black | 0.12 | 0.11 |

| Hispanic | 1 if Hispanic | 0.18 | 0.20 |

| White | 1 if white | 0.63 | 0.62 |

| Other | 1 if other race | 0.08 | 0.08 |

| Married | 1 if married | 0.09 | 0.42** |

| Less than HS education | 1 if 0–11 years of education | 0.18 | 0.12** |

| HS education | 1 if 12 years of education | 0.33 | 0.24** |

| Some college | 1 if 13–15 years of education | 0.36 | 0.25** |

| Bachelors+ | 1 if 16–17 years of education | 0.12 | 0.39** |

| Personal wage income (000s) | Person’s wage income (2011 $) | 14.27 | 31.26** |

| Region | |||

| Northeast | 1 if live in Northeast region | 0.17 | 0.16 |

| Midwest | 1 if live in Midwest region | 0.21 | 0.21 |

| South | 1 if live in South region | 0.38 | 0.37 |

| West | 1 if live in West region | 0.23 | 0.25 |

Significantly different from 19 to 25-year-old category (p < .05).

Calculated using MEPS person weights.

Figure1 plots unadjusted private dental insurance rates for the group of young adults targeted by the ACA dependent coverage policy (19–25 years, darker bars) as well as the slightly older cohort (27–30 years, lighter bars) that was unaffected by the policy. Each bar represents the percentage of individuals in the group that reports having private dental insurance during that year. Panel 1 presents insurance rates for the full sample, panel 2 presents insurance rates for the subsample of persons with income less than 125 percent of FPL, panel 3 presents rates for persons with income between 125 and 400 percent of FPL, and panel 4 presents rates for persons with income greater than 400 percent of FPL. Prior to the implementation of the policy, both groups show declines in private dental coverage from 2006 to 2009. Vujicic and Nasseh (2014) note that several factors, including state Medicaid policies, increases in poverty, or changes in dental reimbursement fees, could have contributed to these declines. The preperiod also coincides with the Great Recession, which may have contributed to declines in dental coverage rates as well. As of 2011, the young adult group affected by the policy change increases coverage rates sharply above the previous trend while the older cohort returns to the prerecession trend. These descriptive findings are very strong evidence of a differential trend between groups beginning after the dependent coverage policy took effect. For persons with household incomes less than 125 percent of FPL, the years from 2006 to 2009 show a marked decline in private dental coverage for both the group affected by the dependent coverage mandate and the older cohort. In 2011, both groups rebound from previous years and return close to 2006 levels. Persons with household incomes greater than 400 percent of FPL experience more gradual declines in coverage between 2007 and 2009 before recovering strongly in 2011. The pattern, once again, is similar for the affected group of young adults and the older cohort. For persons in households with incomes between 125 and 400 percent of FPL, from 2006 to 2009, we find a stable trend for the older cohort and a mild decline in private dental coverage rates for the 19–25-year-old group. Between 2009 and 2011, however, coverage jumps 10 percentage points for the group affected by the dependent coverage mandate with no corresponding increase for the older cohort.

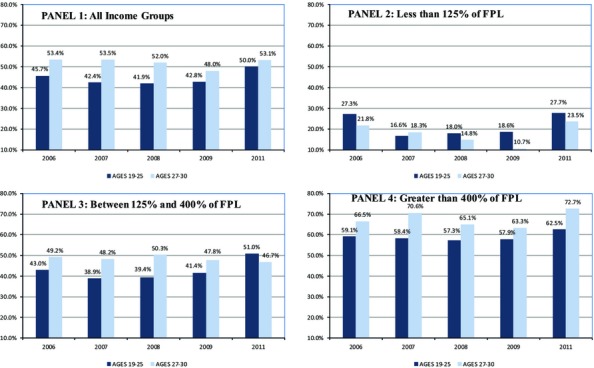

Figure 1.

Mean Private Dental Coverage Rates by Household Income and Age Cohort—2006–2011

Next, we turn to our empirical model to test for the significance of these changes and to assess whether other factors could be contributing to the divergence in private dental coverage rates. Difference-in-difference estimates of the dependent coverage spillover effect are shown in Table2. We include results from the full sample as well as separate results for each of the three income classifications: less than 125 percent of FPL, between 125 and 400 percent of FPL, and greater than 400 percent of FPL. Full sets of regression coefficients are available in Appendix Table S1. Focusing first on estimates from the full sample, the regression confirms the inference from the graphical analysis: evidence suggests the dependent coverage mandate is increasing private dental coverage rates among young adults. For 19–25-year olds, private dental insurance increased by 6.7 percentage points compared to the control group of 27–30-year olds after the mandate took effect.

Table 2.

Difference-in-Difference Regression Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage

| Variable | Percentage Point Change in Private Dental Insurance (Standard Error in Parentheses) | |||

|---|---|---|---|---|

| All Income Groups | <125% of FPL | 125–400% of FPL | >400% of FPL | |

| Treated group × Treated year (19–25-year olds and 2011) | 0.067*** (0.0234) | −0.032 (0.0441) | 0.143*** (0.0300) | −0.007 (0.0458) |

| Treated group (19–25-year olds) | −0.116*** (0.0210) | −0.032 (0.0379) | −0.158*** (0.0279) | −0.111*** (0.0407) |

| Treated year (2011) | 0.001 (0.0179) | 0.081** (0.0389) | −0.053** (0.0245) | 0.044 (0.0296) |

| Observations (N) | 19,948 | 4,358 | 10,400 | 5,190 |

***, ** Significant at p < .05 and .10, respectively.

Turning to the estimates split by household income as a percentage of the Federal Poverty Level, we find an interesting heterogeneity in the results. The largest increases in dental coverage are observed for the middle-income group. Young adults with household incomes between 125 and 400 percent of FPL increased private dental insurance rates by 14 percentage points compared to 27–30-year olds. By contrast, the dependent coverage mandate did not have a significant impact on poorer individuals (<125 percent of FPL) or higher income individuals (>400 percent of FPL). Moreover, tests of the estimates show that the estimate for the 125–400 percent of FPL group was statistically different from the estimates for the other income groups. Both unadjusted changes in coverage rates and our regression estimates point to the low–middle-income group benefitting the most from the spillover effect. We cannot rule out gains for the low-income and high-income groups and visual evidence supports possible gains. However, it is also possible that these groups are merely following the same trends as the slightly older cohort that was unaffected by the mandate.

In results not shown, we evaluated the impact of the dependent coverage mandate on private dental insurance by racial/ethnic group and found that non-Hispanic blacks, Hispanics, and non-Hispanic whites all benefitted from the spillover effect. There were no significant differences in the gains by race/ethnicity.

Robustness Checks

To further test the assumption that no other trends are differentially impacting the affected group of young adults compared to the older cohort, we estimated a difference-in-difference specification with interaction terms for each treated group-year combination. If dental insurance rates were diverging between the young adult group and the older cohort prior to the ACA policy change, we could not clearly attribute our regression estimates to the ACA dependent coverage mandate. In results included in Appendix Table S2, we show that the coefficients for the treated group-year interactions in the years 2008 and 2009 are insignificant and there was a slight negative trend for the 19–25-year-old group in 2007. The coefficient for the year 2011, however, is positive and significant and closely matches the results shown in Table2. Together, this is further evidence that the increase in private dental insurance for young adults only began after the ACA policy change took effect.

As an additional check that private dental insurance gains reflect the dependent coverage policy change, we estimate results separately for married versus unmarried individuals. As marriage provides an additional point of access to private health insurance, it is possible that increases in dental coverage represent marital trends not related to the dependent coverage mandate. Separately estimating results for married versus unmarried individuals allows a check of whether access to private coverage and resulting changes in private dental insurance coverage may be due to differential trends in marriage among young adults rather than the dependent coverage mandate. We use the same estimation procedure and set of covariates from equation 1. Results are contained in Appendix Table S3. For married individuals, we find a positive coefficient (0.048) for the effect of the dependent coverage mandate on private dental coverage, but the effect is not significant (p > .40). For nonmarried persons, we find positive (5.8 percentage point increase in coverage) and significant (p < .05) effects, strongly suggesting that changes in marriage are not responsible for the gains in dental coverage among young adults.

To further test the sensitivity of our preferred specification, we expand the comparison group to include ages 27–34. A significant change in results would indicate that other factors may play a role in the observed changes in private dental insurance. We also include a specification that excludes the demographic, socioeconomic, and geographic control variables included in our preferred specification and listed in Table1. Appendix Table S4 includes results from these additional specifications as well as the results from our preferred specification. We find a slightly stronger effect (+7.9 percentage points) on private dental insurance rates when expanding the comparison group to include individuals up to age 34. When excluding control variables, we find a slightly smaller effect on coverage rates (+5.4 percentage points), confirming the graphical evidence from Figure1 and indicating that confounding among observable characteristics plays a limited role in this case. The differences between these alternate specifications and our preferred estimate are not statistically significant. In total, evidence from these robustness checks strongly supports the conclusions drawn from our preferred estimate.

Discussion

We assessed whether the ACA’s dependent coverage mandate policy had a significant spillover effect on private dental coverage among young adults. We find significant gains in dental insurance, an increase of 6.7 percentage points among young adults in the affected age cohort compared to a group of slightly older adults that were not affected by the policy change. This increase is only slightly smaller than the 9 percentage point increase in medical insurance identified by Shane and Ayyagari (2014) using a similar approach. This suggests that unintended spillover effects of the ACA may be as important as any intended impacts.

Subgroup analysis by income suggests that there are important differences in the impact of the ACA policy. Among the young adults reporting living in poor households (<125 percent of FPL), we do not find significant evidence of gains in dental coverage among young adults. We also find no significant changes for young adults living in relatively high-income households (>400 percent of FPL). Gains in private dental insurance coverage are concentrated among young adults living in households with incomes between 125–400 percent of FPL.

The evidence by household income indicates not only that young adults living in poorer households are much less likely to have private dental coverage, but that this group appears to have suffered bigger declines in coverage during the peak recession years. Less than 30 percent of young adults 19–25 living in poorer households (<125 percent of FPL) had private dental coverage in 2011 compared to more than 50 percent for the low-middle income group and more than 60 percent for the higher income group. However, it is important to note that many low-income persons may have access to dental coverage via Medicaid. In addition, the expansion of Medicaid eligibility up to 138 percent of the FPL under the ACA has the potential to further address any coverage disparities among low-income populations. The majority of the states expanding Medicaid already provide some dental benefits to adults (Yarbrough, Vujicic, and Nasseh 2014). Estimates suggest that the ACA Medicaid expansion combined with increased enrollment due to the “woodwork effect” could potentially reduce the number of low-income adults without dental insurance by up to 35 percent (Yarbrough, Vujicic, and Nasseh 2014). On the other hand, it is also possible that some young adults may switch from public insurance to their parents’ plans (i.e., reverse crowd-out) if the private plans are more generous than the coverage provided by Medicaid.

While much attention has been paid to negative consequences (e.g., canceled policies, labor market effects), unintended or otherwise, due to the Affordable Care Act, our findings suggest that the Affordable Care Act is also having positive spillover effects. The increase in private dental coverage among young adults paired with evidence of very low rates of embedded dental coverage suggests that employer health plans are continuing to offer stand-alone dental benefits to dependents up to age 26. This represents excellent news for the dental health of young adults able to take advantage of the policy change. Given the declines in dental insurance coverage among young adults in the preceding decade, this increase due to the ACA bodes well in terms of improved access to dental care for the group benefitting from parental policies until age 26. As the ACA dependent coverage mandate did not require that stand-alone dental benefits be offered to young adults up to age 26, we speculate that maintaining consistency with health insurance age-out policies was one motivating factor for employers. Employers discontinuing dependent dental benefits at 19 or 23 based on pre-ACA laws would create an odd mismatch in benefits for both companies and employees. We leave corroboration of this notion and other possible explanations for employer and employee choices in this regard for future research.

As additional years of data become available, it will be important to evaluate whether this beneficial spillover effect persists and whether health care reform can address disparities in dental insurance in addition to disparities in medical insurance.

Acknowledgments

Joint Acknowledgment/Disclosure Statement: This research was not supported by funding from any other sources. The authors do not have any conflicts of interest to report.

Disclosures: None.

Disclaimers: None.

Supporting Information

Additional supporting information may be found in the online version of this article:

Appendix SA1: Author Matrix.

Table S1. Difference-in-Difference Regression Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage.

Table S2. Year-Group Interaction Difference-in-Difference Regression Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage.

Table S3. By Marital Status—Difference-in-Difference Regression Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage.

Table S4. Alternate Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage.

References

- American Dental Association. Breaking Down Barriers to Oral Health for All Americans: The Role of Finance. Chicago, IL: American Dental Association; 2012. pp. 975–86. [PubMed] [Google Scholar]

- Antwi YA, Moriya AS. Simon K. Effects of Federal Policy to Insure Young Adults: Evidence from the 2010 Affordable Care Act Dependent Coverage Mandate. American Economic Journal: Economic Policy. 2013;5(4):1–28. [Google Scholar]

- Cantor JC, Monheit AC, DeLia D. Lloyd K. Early Impact of the Affordable Care Act on Health Insurance Coverage of Young Adults. Health Services Research. 2012;47(5):1773–90. doi: 10.1111/j.1475-6773.2012.01458.x. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Choi MK. The Impact of Medicaid Insurance Coverage on Dental Service Use. Journal of Health Economics. 2011;30(5):1020–31. doi: 10.1016/j.jhealeco.2011.08.002. [DOI] [PubMed] [Google Scholar]

- Collins S, Rasmussen P, Garber T. Doty M. Covering Young Adults under the Affordable Care Act: The Importance of Outreach and Medicaid Expansion: Findings from the Commonwealth Fund Health Insurance Tracking Survey of Young Adults. Issue Brief (Commonwealth Fund) 2013;21:1–15. [PubMed] [Google Scholar]

- Gruber J. The Incidence of Mandated Maternity Benefits. The American Economic Review. 1994;84(3):622–41. [PubMed] [Google Scholar]

- Jensen GA. Morrisey MA. Employer-Sponsored Health Insurance and Mandated Benefit Laws. Milbank Quarterly. 1999;77(4):425–59. doi: 10.1111/1468-0009.00147. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Maiuro L. 2011. California Healthcare Foundation “Eliminating Adult Dental Benefits in Medi-Cal: An Analysis of Impact.” [accessed on July 31, 2012]. Available at http://www.chcf.org/~/media/MEDIA%20LIBRARY%20Files/PDF/E/PDF%20EliminatingAdultDentalMediCalcx.pdf.

- Mayer K. 2013. “ Dental Enrollments Jump to Record High ” [accessed on August 14, 2014]. Available at http://www.benefitspro.com/2013/10/18/dental-enrollments-jump-to-record-high.

- Miller R. Estimating the Compensating Differential for Employer-Provided Health Insurance. International Journal of Health Care Finance and Economics. 2004;4(1):27–41. doi: 10.1023/b:ihfe.0000019259.74756.65. [DOI] [PubMed] [Google Scholar]

- Nasseh K. Vujicic M. Health Reform in Massachusetts Increased Adult Dental Care Use, Particularly among the Poor. Health Affairs. 2013;32(9):1639–45. doi: 10.1377/hlthaff.2012.1332. [DOI] [PubMed] [Google Scholar]

- Pryor C. Monopoli M. Eliminating Adult Dental Coverage in Medicaid: An Analysis of the Massachusetts Experience. Washington, DC: Kaiser Commission on Medicaid and the Uninsured; 2005. [Google Scholar]

- Shane DM. Ayyagari P. Will Health Reform Reduce Disparities in Insurance Coverage? Evidence from the Dependent Coverage Mandate. Medical Care. 2014;52(4):528–34. doi: 10.1097/MLR.0000000000000134. [DOI] [PubMed] [Google Scholar]

- Sommers BD. Kronick R. The Affordable Care Act and Insurance Coverage for Young Adults. Journal of the American Medical Association. 2012;307(9):913–4. doi: 10.1001/jama.307.9.913. [DOI] [PubMed] [Google Scholar]

- Sommers BD, Buchmueller T, Decker SL, Carey C. Kronick R. The Affordable Care Act Has Led to Significant Gains in Health Insurance and Access to Care for Young Adults. Health Affairs. 2013;32(1):165–74. doi: 10.1377/hlthaff.2012.0552. [DOI] [PubMed] [Google Scholar]

- StataCorp LP. Stata Statistical Software: Release 12. College Station, TX: StataCorp LP; 2011. [Google Scholar]

- Vujicic M, Goodell S. Nasseh K. Dental Benefits to Expand for Children, Likely Decrease for Adults in Coming Years. Chicago, IL: American Dental Association; 2013. Health Policy Resources Center Research Brief. [Google Scholar]

- Vujicic M. Nasseh K. A Decade in Dental Care Utilization among Adults and Children (2001–2010) Health Services Research. 2014;49(2):460–80. doi: 10.1111/1475-6773.12130. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Wall TP, Vujicic M. Nasseh K. Recent Trends in the Utilization of Dental Care in the United States. Journal of Dental Education. 2012;76(8):1020–7. [PubMed] [Google Scholar]

- Wallace NT, Carlson MJ, Mosen DM, Snyder JJ. Wright BJ. The Individual and Program Impacts of Eliminating Medicaid Dental Benefits in the Oregon Health Plan. American Journal of Public Health. 2011;101(11):2144–50. doi: 10.2105/AJPH.2010.300031. [DOI] [PMC free article] [PubMed] [Google Scholar]

- Yarbrough C, Vujicic M. Nasseh K. More than 8 Million Adults Could Gain Dental Benefits through Medicaid Expansion. Chicago, IL: American Dental Association Health Policy Institute Research Brief; 2014. [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.

Supplementary Materials

Appendix SA1: Author Matrix.

Table S1. Difference-in-Difference Regression Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage.

Table S2. Year-Group Interaction Difference-in-Difference Regression Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage.

Table S3. By Marital Status—Difference-in-Difference Regression Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage.

Table S4. Alternate Estimates of Dependent Coverage Mandate Effect on Private Dental Insurance Coverage.