Abstract

Context

Smokeless tobacco use is well-recognized as occupying a significant portion of overall tobacco consumption in Bangladesh. Yet very little is known about the effectiveness of tax and price policy in controlling the use of smokeless tobacco use in the country.

Aims

The aims of this paper are to examine the price distribution of various smoked and smokeless tobacco products and estimate the effects of changes in the prices of tobacco products on the consumption of smokeless tobacco.

Settings and Design

The data for this paper came from the Wave 3 ITC Bangladesh (ITC BD) Survey conducted between November 2011 and May 2012. It is a cohort survey of a nationally representative sample of adult tobacco users and non-users in Bangladesh selected using a stratified multistage cluster sampling design.

Two measures of smokeless tobacco use are used in the analysis—prevalence of smokeless tobacco use indicating the decision to use smokeless tobacco products, and the frequency of using smokeless tobacco per day indicating intensity of smokeless tobacco use.

Methods and Material

The regression analysis involves estimation of the demand function for the most widely used smokeless tobacco product in Bangladesh, zarda.

Statistical analysis used

The descriptive analysis looks at the characteristics of the price distribution of cigarette, bidi, zarda, and gul using the univariate Epanechnikov kernel density estimation.

Results

It estimates the price elasticity of lower price brands of zarda (the most commonly used smokeless tobacco product in Bangladesh) at -0.64 and of higher-priced brands at -0.39, and the cross-price elasticity of zarda with respect to cigarettes at 0.35.

Conclusions

The tax increase on smokeless tobacco products needs to be greater than the tax increase on smoked tobacco products to bridge the wide price differential between the two types of products that currently encourages downward substitution and discourages quitting behaviour. Finally, a specific excise system replacing the existing ad valorem excise tax can substantially contribute to the revenue collection performance from smokeless tobacco products.

Keywords: Smokeless tobacco, taxation, price elasticity

Introduction

Smokeless tobacco use constitutes a major part of the overall tobacco use in Bangladesh. The Global Adult Tobacco Survey (GATS) in Bangladesh conducted in 2009 found tobacco use prevalent among 43.3% of the adult population (aged 15 and above) [1]. While prevalence of smoked tobacco (cigarettes and bidi) was 23.0%, the prevalence of smokeless tobacco use was higher at 27.2%. Considering the threat that smokeless tobacco use can pose to public health [2], it is of critical importance to identify and promote methods for reducing the use of smokeless tobacco.

According to the World Health Organization, “… a significant increase in tobacco product taxes and prices has been demonstrated to be the single most effective and cost-effective intervention for reducing tobacco use, particularly among the young and the poor” (WHO Technical Manual on Tax Administration Manual, page 18). And yet, although there have been considerable attention paid to the benefits of raising taxes on cigarettes and bidi in Bangladesh, to date, the same attention has not been paid to the possibility that raising taxes on smokeless tobacco products in Bangladesh could also lead to significant reductions in the prevalence of smokeless tobacco.

There are two factors that have contributed to the lack of policy initiatives focusing on using taxation to reduce smokeless tobacco. The first is a general lack of knowledge with respect to the absolute and relative prices of tobacco products—for smokeless tobacco especially, although there exist challenges as well for cigarettes and bidis. Second there is a lack of knowledge about and understanding the implications of the current price structure of tobacco products for overall tobacco consumption. At present, there have been few rigorous studies of price and tax in Bangladesh, and none that has examined in detail the relation between the price distribution of smoked and smokeless tobacco products and the implications on behavior.

This paper seeks to fill this gap in knowledge. Using nationally representative data collected in 2012 by the Wave 3 International Tobacco Control (ITC)Bangladesh Survey, the paper reports the findings on the cross-sectional price distribution of smoked and smokeless tobacco products and draws implications for the tax and price policies for smokeless tobacco products in Bangladesh.

Subjects and Methods

Data source

The data for this paper came from the Wave 3 ITC Bangladesh (ITC BD) Survey conducted between November 2011 and May 2012. A detailed description of the ITC BD Survey can be found in previous publications [3-5]. Briefly, the ITC BD Survey is a cohort survey of a nationally representative sample of tobacco users and non-users conducted in all six administrative divisions of Bangladesh: Barisal, Chittagong, Dhaka, Khulna, Rajshahi, and Sylhet. The target population of the ITC BD Survey consists of users and non-users of tobacco who are 15 years or older. The Wave 1 ITC BD Survey conducted in 2009 consisted of a nationally representative probability sample of 3,111 adult smokers (cigarette and/or bidi) and 2,660 non-smokers selected using a stratified multi-stage cluster sampling design. These respondents were re-contacted in Waves 2 and 3; respondents lost to attrition were replenished with new respondents sampled using the same design as Wave 1. Data were collected using face-to-face interviews.

In Wave 3, the smokeless tobacco and mixed (smoked and smokeless) surveys were introduced with the existing surveys for cigarette and bidi smokers, non-users and quitters of tobacco. In addition, data on retail prices of cigarettes, bidis, and all types of smokeless tobacco products found in the market were collected using a supplementary price protocol. A maximum of five stores were randomly selected from each sampling area where price of each tobacco brand was collected.

In all the waves, written consent was obtained from those respondents. Ethics clearance was obtained from the Office of Research Ethics at the University of Waterloo (Waterloo, Canada) and from the Ethical Review Committee of the Bangladesh Medical Research Council.

Measures

Two measures of smokeless tobacco use are used in the analysis—prevalence of smokeless tobacco use indicating the decision to use smokeless tobacco products, and the frequency of using smokeless tobacco per day indicating intensity of smokeless tobacco use. The status and frequency of smokeless tobacco use are directly reported by the respondents.

The price per gram (gm) of smokeless tobacco (primarily zarda) is derived by dividing the price per pouch or container by the weight of the pouch or container, as reported by the retailers from the stores in a locality or village. The average of this price variable for the village is then attributed to the individuals residing in that village. The prices per stick of cigarette and bidi are similarly derived by dividing the retail price obtained from the stores by the number of sticks in the packs, averaged over the stores for each locality and then attributed to the individuals residing in that locality.

The respondents reported directly on household income, individual level of education, occupation, age, gender, marital status, and whether his/her parents and grandparents use(d) smokeless tobacco. The area of residence and sample types were derived based on the sample design. There are four types of samples—national (representative of the mainstream population), floating (representing the slum area population), border (representing the population close to the land port at the border with India to adjust for influence of cross-border trade), and tribal (representing the indigenous population). These variables were controlled for to determine the relationship between the prices of smoked and smokeless tobacco products and the smokeless tobacco use.

Analyses

The descriptive analysis in this paper looks at the characteristics of the price distribution of cigarette, bidi, zarda, and gul using the univariate Epanechnikov kernel density estimation[6]. Further, we estimate the average price and excise tax per stick of cigarette and bidi and per gm of zarda and gul, and calculate the share of excise tax and total tax (including excise and value-added tax) in the retail price of these products. It is important to look at the share of tax in the retail price for two reasons: first, higher share of tax indicates stronger government control over the prices and the use of the products, thus greater effectiveness of tobacco control through taxation; second, smaller tax share in retail price suggests that there is more room for the government to increase tax and collect more revenue.

The regression analysis involves estimation of the demand function for the most widely used smokeless tobacco product in Bangladesh, zarda, using a two-step method [7]. In the first step, using logit estimation, we estimate the prevalence of zarda use as a function of the prices of zarda, cigarette, and bidi, household income, individual education, occupation, gender, age, marital status, use of smokeless tobacco by parents and grandparents, area of residence, and type of sample (national, floating, border, or tribal). In the second step, using ordinary least squares (OLS) estimation, the intensity of zarda use is estimated as a function of the same variables as in the first step of prevalence estimation.

The coefficients of the price variables from these two equations are used to estimate the own and cross price elasticites of zarda use. The own price elasticity presents the degree of sensitivity of zarda use with respect to variations of its own price. The cross price elasticity, on the other hand, shows how much the consumption of zarda can change in response to changes in the price of smoked tobacco products, such as cigarette and bidi. The price elasticity of prevalence of zarda use is given by the marginal effect of price from the logit regression times the ratio of the average price and the population prevalence of zarda use. The price elasticity of intensity of zarda use is estimated by the coefficient of price from the OLS regression times the ratio of the average price and the average frequency of daily zarda use. The sum of these two price elasticities yields the total price elasticity of zarda use.

Results

Price and tax of tobacco products

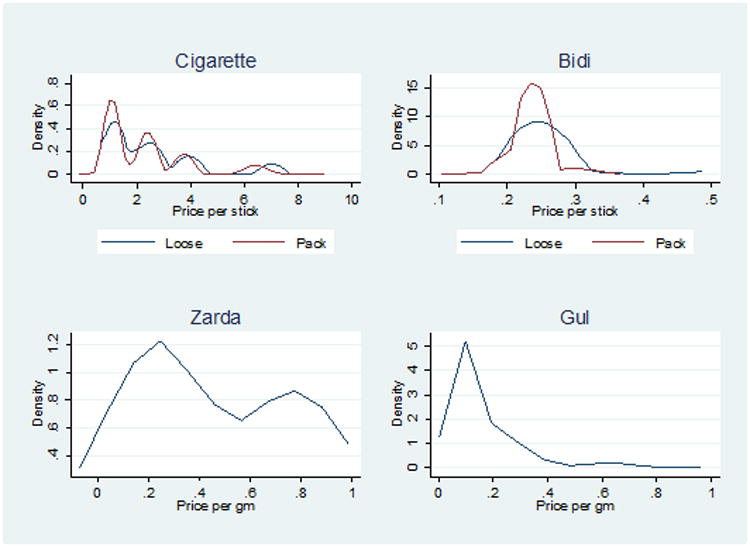

The price distribution of tobacco products in Bangladesh is characterized by wide differential between prices of various tobacco products as well as between prices of brands within specific tobacco products. Figure 1 summarizes the level and variability of price across different tobacco products, such as smoked tobacco products (i.e., cigarette and bidi) and smokeless tobacco products (i.e., zarda and gul). The prices of cigarette and bidi are converted to per stick prices and the prices of zarda and gul are expressed per gm. To the extent that the weight of a stick of cigarette or bidi approaches 1 gm, the prices per stick of the smoked products can be comparable to the price per gm of smokeless tobacco products.

Figure 1. The kernel density of tobacco product prices in Bangladesh, 2011-12.

Source: Authors' calculations based on Wave 3 ITC BD Survey data.

Several observations can be made from Figure 1:

- Cigarette prices demonstrate four distinct and widely dispersed bands ranging from less than 1 Taka to 9 Taka per stick. This price structure closely resembles the specification of four price bands into low, medium, high, and premium categories of cigarettes corresponding to the four-tiered ad valorem supplementary duty (excise) rates applicable to cigarettes. In 2011-12, when the survey was conducted, the supplementary duty rates were as follows:

Category Retail price/pack of 10 sticks (Taka) Supplementary duty rates (% of retail price) Low 11.00 – 11.30 36% Medium 22.50 – 23.00 55% High 32.00 – 36.00 58% Premium 60.00+ 60% The most commonly sold cigarettes brands belong to the low price category, followed by medium, high, and premium brands in that order.

When sold loose or singles, the price per stick of cigarette is on average higher and more variable than the price per stick when sold as a pack.

Bidi prices per stick centre around 0.25 Taka per pack and range from 0.10 to 0.50 Taka. As most of the market is occupied by 25 stick pack non-filtered bidis, a pack of bidi on average cost was 6.25 Taka in 2011-12.

When sold loose or singles, the mean and variance of bidi price are higher compared to pack of 25 sales.

One stick of bidi costs less than one-fourth of one stick of the cheapest cigarette brand.

There are two distinct varieties of zarda available in the market—the cheaper variety that sells for less than 0.60 Taka per gm and the higher-price variety that sells for 0.60 to 1.00 Taka per gm.

The average price of the cheaper variety of zarda is comparable to the bidi price per stick, while the price of higher-price variety zarda is higher than bidi price.

On average, the price of zarda per gm is less than half of the price per stick of the cheapest brand of cigarette.

The price of gul is relatively skewed centring around 0.10 Taka per gm.

The average price of gul is comparable to the lower side of the cheaper price variety of zarda.

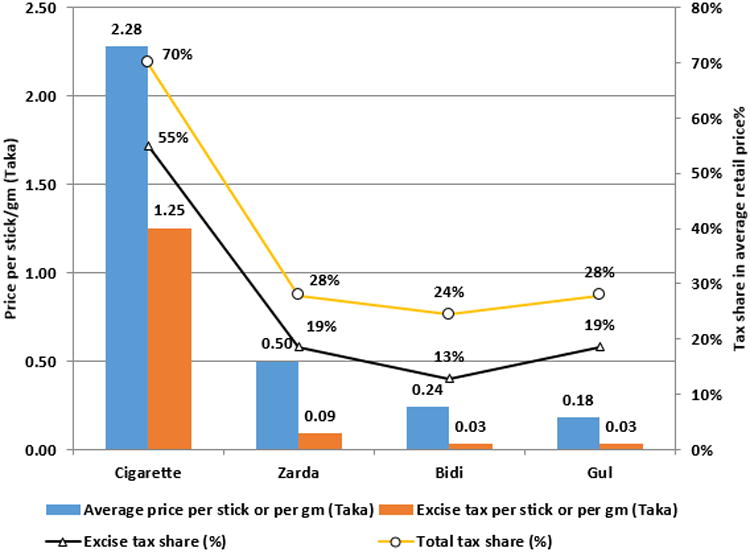

When ordered in one scale for price per stick of smoked tobacco product and price per gm of smokeless tobacco products as in Figure 2 below, it appears that the average gul, bidi, and zarda prices cluster at or below 0.50 Taka while the average cigarette price lies far higher at above 2 Taka. Applying the existing supplementary duties on cigarette at 55% of the retail price (noting that the average price falls in the medium tier), on bidi at 20% of the tariff value of 3.88 Taka per pack of 25 sticks, on zarda and gul at 30% of the ex-factory price, and 15% value-added tax (VAT) on all products, the level and share (in retail price) of excise tax and total tax (excise plus VAT) are calculated. As shown in Figure 2, cigarette tops both with respect to the price and tax levels and the tax shares. While the prices of gul and bidi are close, the tax shares are slightly higher for gul than for bidi.

Figure 2. Retail price and excise tax per stick/gm and excise and total tax share in retail price of tobacco products in Bangladesh, 2011-12.

Source: Authors' calculations based on data from Wave 3 ITC BD Survey data.

Determinants of smokeless tobacco use

The use of smokeless tobacco products can be determined by a number of factors including the price of smokeless tobacco products, the prices of smoked tobacco products (e.g., cigarette and bidi), and individual and household level socio-economic characteristics that reflect the preference of individuals including income, education, occupation, history of smokeless tobacco use in the family, demographics, area of residence, and sample type. To the extent that tobacco taxation policy affects tobacco product prices, it is of interest in the present context to learn what role the prices of tobacco products play in the demand for smokeless tobacco products.

In the estimates of Model 1 in Table 1, the price of zarda appears to influence the prevalence of zarda use negatively as expected. However, the intensity of zarda use is positively affected, which is counterintuitive. Since the price distribution of zarda was found to be bimodal in Figure 1, it can be deduced from the positive and statistically significant coefficient of zarda price that the higher-priced brands are consumed more frequently than the cheaper brands. This may be attributable to the fact that the higher-priced brands are perceived by consumers to be better quality products and are consumed in greater quantity than the cheaper and lower-quality products.

Table 1.

Logit estimates of prevalence of zarda use and OLS estimates of the frequency of daily use of zarda.

| Model 1 | Model 2 | |||||||

|---|---|---|---|---|---|---|---|---|

|

| ||||||||

| Prevalence: Logit estimation | Intensity: OLS estimation | Prevalence: Logit estimation | Intensity: OLS estimation | |||||

|

| ||||||||

| Marginal effect | z-stat | Coef. | t-stat | Marginal effect | z-stat | Coef. | t-stat | |

| Zarda price | -0.0538** | -2.52 | 1.8678*** | 2.93 | ||||

| Zarda price-cheaper brands | -0.5003*** | -12.09 | 1.8426 | 1.36 | ||||

| Interaction for zarda price-higher-price brands | 0.3671*** | 12.37 | 0.0204 | 0.02 | ||||

| Cigarette price | 0.0030*** | 5.54 | 0.0289 | 1.45 | 0.0025*** | 4.73 | 0.0289 | 1.44 |

| Bidi price | 0.0096 | 1.63 | -0.0332 | -0.14 | 0.0055 | 0.96 | -0.0333 | -0.14 |

| Household income | 0.0000 | 0.79 | 0.0000 | 0.74 | 0.0000 | 0.89 | 0.0000 | 0.74 |

| Level of education | ||||||||

| Primary (1–5 years) | -0.0429*** | -4.21 | -0.4338 | -1.09 | -0.0432*** | -4.34 | -0.4336 | -1.09 |

| Secondary (6–8 years) | -0.0613*** | -5.11 | -0.1656 | -0.28 | -0.0565*** | -4.76 | -0.1652 | -0.27 |

| Secondary School Certificate (9–10 years) | -0.1024*** | -9.22 | -0.8861 | -1.01 | -0.0986*** | -9.25 | -0.8862 | -1.01 |

| Higher Secondary Certificate (11–12 years) | -0.1304*** | -11.3 | -2.7031 | -1.29 | -0.1272*** | -12.08 | -2.7035 | -1.29 |

| Bachelor's and above (14 years and above) | -0.1436*** | -14.4 | -3.5404 | -1.50 | -0.1350*** | -13.31 | -3.5412 | -1.5 |

| Occupation | ||||||||

| Tenant farmer | 0.0005 | 0.01 | -0.2840 | -0.22 | 0.0164 | 0.42 | -0.2845 | -0.22 |

| Self-employed in non-farm agriculture | 0.0198 | 0.35 | 1.9558 | 1.00 | 0.0357 | 0.61 | 1.9562 | 1.00 |

| Self-employed in non-agricultural activity | 0.0024 | 0.09 | 0.9040 | 0.99 | 0.0096 | 0.36 | 0.9038 | 0.99 |

| Farm wage labourer | -0.0174 | -0.60 | 0.5976 | 0.49 | -0.0123 | -0.42 | 0.5971 | 0.49 |

| Non-farm agricultural wage labourer | -0.0876** | -3.19 | -1.3764 | -0.67 | -0.0770*** | -2.67 | -1.3733 | -0.67 |

| Non-agricultural wage labourer | -0.0168 | -0.69 | 0.6548 | 0.69 | -0.0024 | -0.09 | 0.6561 | 0.69 |

| Professional | 0.0083 | 0.16 | 1.8835 | 1.03 | 0.0095 | 0.18 | 1.8828 | 1.03 |

| Managerial/administrative/clerking | 0.0135 | 0.27 | 1.0615 | 0.62 | 0.0140 | 0.28 | 1.0607 | 0.61 |

| Student | -0.0562 | -1.14 | 4.3982 | 1.62 | 0.0517*** | 0.37 | 4.3960 | 1.61 |

| Unemployed | -0.0138 | -0.50 | 0.6096 | 0.59 | 0.0293*** | 0.96 | 0.6095 | 0.59 |

| Homemaker | -0.0109 | -0.44 | 0.3596 | 0.40 | 0.0260*** | 0.73 | 0.3604 | 0.40 |

| Others | 0.0363 | 1.42 | 1.2398 | 1.47 | 0.0270*** | 0.08 | 1.2409 | 1.47 |

| Female | 0.1203*** | 6.60 | 0.0566 | 0.11 | 0.1031*** | 5.81 | 0.0566 | 0.11 |

| Age | 0.0041*** | 12.81 | 0.0072 | 0.59 | 0.0039*** | 12.52 | 0.0072 | 0.59 |

| Married | 0.0092 | 0.68 | 0.4260 | 0.88 | 0.0067 | 0.49 | 0.4259 | 0.88 |

| Parents use(d) SLT | 0.0623*** | 5.99 | 0.6955 | 1.54 | 0.0102*** | 0.00 | 0.6949 | 1.54 |

| Grandparents use(d) SLT | 0.0043 | 0.43 | -0.0708 | -0.20 | 0.0099*** | 0.94 | -0.0713 | -0.20 |

| Rural area of residence | 0.0555*** | 4.25 | 1.1366** | 2.33 | 0.0126*** | 0.00 | *1.1371** | 2.32 |

| Floating sample | 0.0782*** | 3.96 | 2.1263*** | 3.99 | 0.0260 | 0.00 | * 2.1279* | 3.95 |

| Border sample | -0.0136 | -0.32 | -2.2180 | -1.24 | 0.0601*** | 0.34 | -2.2172 | -1.23 |

| Tribal sample | -0.0536** | -2.42 | -2.2358** | -2.01 | 0.0253*** | 0.15 | * -2.2355* | -2.01 |

| Constant | -4.8400*** | -10.90 | 1.4673 | 0.69 | -3.6921*** | -8.11 | 1.4728 | 0.68 |

|

| ||||||||

| Observations | 5429 | 725 | 5429 | 725 | ||||

|

| ||||||||

| Pseudo-R squared | 0.1372 | 0.1681 | ||||||

|

| ||||||||

| Adjusted-R squared | 0.0453 | 0.044 | ||||||

|

| ||||||||

| Own price elasticity: Lower-price brands | -0.09 | -0.64 | ||||||

|

|

|

|||||||

| Higher-price brands | -0.39 | |||||||

|

| ||||||||

| Cross price elasticity (cigarette) | 0.35 | |||||||

Note: The t statistics of the coefficients are in parentheses. Omitted categories include male gender, single, illiterate, owner farmers (occupation), urban area of residence and national sample.

p<0.05,

p<0.01,

p<0.001. OLS, ordinary least square

In Model 1, a single price variable for zarda omits the interaction of price with the quality of the product. In order to account for the variation in quality, in Model 2, we create a dummy variable that takes a value of 0 for products priced below 0.60 Taka and 1 for those priced at or above 0.60 Taka. It turns out that the effect of price increase on prevalence of smokeless tobacco use is greater in Model 2 than in Model 1—for increase in zarda price by 1 Taka per gm, the probability of using smokeless tobacco reduces by 0.5003 for cheaper brands and by 0.1332 (- 0.5003 + 0.3671) for higher-priced brands. As expected, the use of higher-priced brands, which are usually consumed by relatively well-off people, is less price-sensitive than the cheaper brands consumed by users from low socio-economic status. However, zarda price in Model 2 does not affect the intensity of smokeless tobacco use.

Cigarette price has a positive effect on zarda use prevalence implying that higher price of cigarettes may lead to greater use of smokeless tobacco. The statistical insignificance of the marginal effect of bidi price indicates that there may not be any substitutability between bidi and smokeless tobacco. Neither the bidi price nor the cigarette price has significant impact on the intensity of smokeless tobacco use.

Among the indicators of socio-economic status, household income is not a significant predictor of smokeless tobacco use, either with respect to prevalence or intensity. However, education plays a significant role in prevalence—the higher the level of education, the lower the rate of prevalence of smokeless tobacco use. Non-farm agricultural wage labourers have lower prevalence, while students, unemployed, and homemakers have higher prevalence of smokeless tobacco use. Neither education nor occupation influences the frequency or intensity of smokeless tobacco use. Smokeless tobacco use is more likely to be observed among women, older persons, people whose parents or grandparents use(d) smokeless tobacco, the population living in the border areas, and the tribal population.

Discussion

Based on the estimates of Model 2, the price elasticity of lower-price brands of zarda is -0.64 and of higher-priced brands is -0.39. It implies that 10% increase in the price of zarda can reduce zarda consumption by 6% for cheaper brands and 4% for more expensive brands. This reduction is fully attributable to the reduction in the prevalence of zarda use. It shows that a tax increase that can induce price increase is expected to significantly reduce the prevalence of smokeless tobacco use among the Bangladeshi population. Note that the price elasticity estimates by lower- and higher-priced brands obtained from Model 2 are much higher than the estimate of -0.09 obtained for all brands together. The downward bias in the price elasticity estimate is likely arising from the omission of the product quality indicator in the regression.

The cross-price elasticity of zarda with respect to cigarette price is estimated to be 0.35 implying that a 10% increase in cigarette price with zarda price unchanged can increase the consumption of zarda by 3.5%. That means if both cigarette and zarda prices are increased by 10%, zarda consumption will be reduced by 2.5% (-6.0% + 3.5%). The positive impact of cigarette price increase will partially offsets the negative impact of zarda price increase.

The positive and significant cross price elasticity with respect to cigarette price thus suggests that higher cigarettes prices can induce some smokers to switch to smokeless tobacco products if the prices of smokeless tobacco products are not increased at the same time. The wide price differential between cigarette and zarda is primarily the reason that drives the substitutability between these two products and the potential downward switching from smoked to smokeless tobacco products. It undermines the public health outcome intended from a given tax increase.

Two important lessons can be drawn from the above findings. First, given the multiplicity of tobacco products and opportunity for switching between smoked and smokeless tobacco products, the tax and prices of all tobacco products should be increased simultaneously. Second, the tax and price increase should be reducing the price differential between smoked and smokeless tobacco products. As such, the tax increase for smokeless tobacco products should be done at a faster rate than smoked tobacco products.

Moreover, the current system of levying supplementary duty and VAT as a percentage of the ex-factory price at the production level makes the tax revenue flow heavily depending on the declaration of the ex-factory price by the producer and subjects it to tax avoidance. Therefore, a specific tax per gm of smokeless tobacco products irrespective of the ex-factory price in place of the supplementary duty as a percentage of the ex-factory price is recommended.

Conclusion

Smokeless tobacco use is well-recognized as occupying a significant portion of overall tobacco consumption in Bangladesh. Yet very little is known about the effectiveness of tax and price policy in controlling the use of smokeless tobacco products in the country. By examining the price distribution of various smoked and smokeless tobacco products and estimating the effects of changes in the prices of tobacco products on the consumption of smokeless tobacco, this paper argues that increasing tax on smokeless tobacco products simultaneously with the tax increase on smoked tobacco products can have significant negative impact on the prevalence of smokeless tobacco use in Bangladesh. Furthermore, the tax increase on smokeless tobacco products needs to be greater than the tax increase on smoked tobacco products to bridge the wide price differential between the two types of products that currently encourages downward substitution and discourages quitting behaviour. Finally, a specific excise system replacing the existing ad valorem excise tax can substantially contribute to the revenue collection performance from smokeless tobacco products.

Key Messages.

Increasing tax on smokeless tobacco products simultaneously with the tax increase on smoked tobacco products can significantly reduce the prevalence of smokeless tobacco use in Bangladesh

Acknowledgments

The authors would like to acknowledge the team members from University of Waterloo and University of Dhaka for their contributions in the ITC Bangladesh Project. The ITC Bangladesh Survey was supported by the International Development Research Centre (IDRC Grant 104831-002), Canadian Institutes for Health Research (Operating Grants 79551 and 115016), the US National Cancer Institute (P01 CA138389), and GTF was supported by a Senior Investigator Award from Ontario Institute for Cancer Research and by a Prevention Scientist Award from the Canadian Cancer Research Institute.

Footnotes

Disclaimer: The authors alone are responsible for the views expressed in this article and they do not necessarily represent the views, decisions or policies of the institutions with which they are affiliated.

References

- 1.World Health Organization (WHO) Bangladesh Global Adult Tobacco Survey: Bangladesh Report 2009. Dhaka, Bangladesh: WHO – Bangladesh; 2009. [Google Scholar]

- 2.International Agency for Research on Cancer (IARC) Smokeless tobacco and some tobacco-specific N-Nirtosamines, vol 89 of IARC Monographs on the Evaluation of Carcinogenic Risks to Humans. Vol. 89 World Health Organization International agency for Research on Cancer; Lyon, France: 2007. [Google Scholar]

- 3.Fong GT, Cummings KM, Borland R, Hastings G, Hyland A, Giovino G, Thompson ME. The conceptual framework of the International Tobacco Control (ITC) Policy Evaluation Project. Tobacco Control. 2006;15:i3–11. doi: 10.1136/tc.2005.015438. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 4.Abdullah AS, Hitchman SC, Driezen P, Nargis N, Quah ACK, Fong GT. Socioeconomic differences in exposure to tobacco smoke pollution (TSP) in Bangladeshi households with children: Findings from the International Tobacco Control (ITC) Bangladesh Survey. International Journal of Environmental Research and Public Health. 2011;8:842–860. doi: 10.3390/ijerph8030842. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 5.Nargis N, Ruthbah UH, Hussain AK, Fong GT, Huq I, Ashiquzzaman SM. The price sensitivity of cigarette consumption in Bangladesh: evidence from the International Tobacco Control (ITC) Bangladesh Wave 1 (2009) and Wave 2 (2010) surveys. Tob Control. 2014 Mar;23(Suppl 1):39–47. doi: 10.1136/tobaccocontrol-2012-050835. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.STATA Base Reference Manual Release 11. StataCorp LP 1985-2009.

- 7.Cragg JG. Some statistical models for limited dependent variables with applications to the demand for durable goods. Econometrica. 1971;39:829–44. [Google Scholar]