Short abstract

This study examines the overall scale and trend of price promotions and discounts in some European countries and the responses of consumers and suppliers to a variety of alcohol regulations, including excise duties.

Abstract

Policies related to alcohol pricing, promotion and discounts provide opportunities to address harms associated with alcohol misuse. However, there are important gaps in information and knowledge about the regulations in place across parts of Europe and their impacts on consumer prices and locations of purchase. Using market data, we explored the overall scale and trend of price promotions and discounts in the off-premise (e.g. supermarket) and on-premise (e.g. restaurants, pubs) across five EU Member States. To better understand the factors that may influence sales in the on- vs. off-premises, we performed regression analysis for four EU Member States with relevant data. This found that increases in broadband penetration and population density were associated with relatively higher levels of off-premise alcohol purchases and that increases in income were associated with relatively higher levels of on-premise purchases of alcohol. There was no statistically significant relationship for female higher education. We further used time-series methods, drawing on data for Ireland, Latvia, Slovenia and Finland, to estimate the impact of changes in excise duty on price (“pass-through”). This showed that a €1 increase in excise duty increased beer prices by €0.50–€2.50 in the off-premise, and increased spirits prices by €0.70–€1.40 in the off-premise. These findings suggest that, depending on the price sensitivity of consumers and other strategies employed by suppliers (e.g. advertising), changes in excise duty may be an effective instrument to reduce harmful alcohol consumption.

The Harmful and Hazardous Use of Alcohol Is a Serious Problem in the EU

The harmful and hazardous use of alcohol results in serious health, social and economic harms, and is the third-leading risk factor for death and disability in the European Union (EU) after tobacco and high blood pressure. Alcohol generates high costs to society; it was estimated that the costs in the EU of alcohol-related harms was around €125 billion in 2003, equivalent to 1.3 percent of GDP. Against this background, there is intense pan-European interest in developing and implementing measures to combat alcohol harms.

Evidence suggests that consumers respond to changes in alcohol prices, and increases in alcohol prices have been linked to reductions in consumption and positive health and social outcomes. We also know that price changes impact on what people drink or where they purchase their alcoholic beverages.

There are many types of pricing policies that governments have at their disposal to address alcohol harms. Taxes are one such policy, but others include restrictions on promotions and discounts, bans on below-cost sales and the introduction of minimum prices on a unit of alcohol.

However, there remain important gaps in our understanding of the various factors that affect how different pricing policy initiatives translate into actual price changes across the EU. At the same time, there is considerable opportunity to learn from the experiences of countries that implement various (non-tax) pricing policies.

This research aims to further our understanding of these issues by addressing the following specific questions:

To what extent have alcohol tax changes been passed through to consumer prices?

What are the trends in the ratio of on-premise to off-premise sales of alcoholic beverages? What factors may be driving these trends?

What are the trends in the use of on- and off-trade alcohol price promotions and discounts?

What is the regulatory landscape in the EU with reference to non-tax alcohol pricing policy, and what lessons can we learn from the diversity of regulatory experiences?

There Is Heterogeneity in Pass-Through in Different Countries, for Different Beverages and in Different Types of Premise

Extensive research has been conducted on the effect of changes in alcohol excise duties on alcohol consumption and harms. The mechanism by which taxation influences consumption is through its pass-through to prices. Pass-through refers to the extent to which taxes are passed through to the price the consumer pays. We estimated pass-through for four Member States that were able to provide relevant data: Finland, Ireland, Latvia and Slovenia. We performed regression analysis for beer and spirits taxes and prices for off-trade alcohol for each country, focusing on tax changes experienced in recent years. As we also obtained on-premise data from Ireland and Finland, we analysed pass-through in the on-trade in those two countries. We provide estimates of the change in real retail prices following a €1 increase in real excise duties. Full pass-through means that consumer prices change by the currency amount of the change in excise duty.

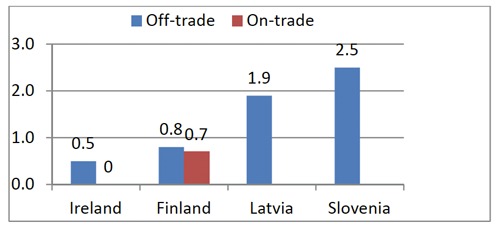

We found there is less than full pass-through in Ireland and Finland for beer excise duties both in the on- and the off-trade, whereas they are more than fully passed through in the off-trade in Latvia and Slovenia (Figure 1).

Figure 1.

Pass-Through for Beer in Ireland, Finland, Latvia and Slovenia

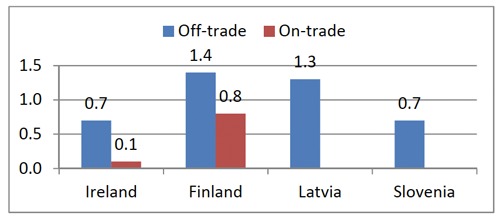

For spirits, the picture is more diverse. We find less than full pass-through in the on-trade in Finland and Ireland, but more than full pass-through in the off-trade in Finland and Latvia. Ireland's and Slovenia's off-trade sectors did not pass on the full amount of excise duty change to prices of spirits (Figure 2).

Figure 2.

Pass-Through for Spirits in Ireland, Finland, Latvia and Slovenia

It is possible that factors such as market structure, consumer preferences, other pricing policies (eg price floors such as Ireland's Grocery Order) and alcohol-related policies (eg changes in drink-driving legislation) affect the extent to which excise duty changes are passed on to consumers. Therefore, it is difficult to predict with precision the effect of changes in excise duty. In view of this, it is useful for policymakers to assess carefully prior responses to excise duty changes in their countries and the other key changes occurring in that environment before implementing new changes.

There Is a Trend Towards More Off-Trade Alcohol Consumption in Many EU Member States

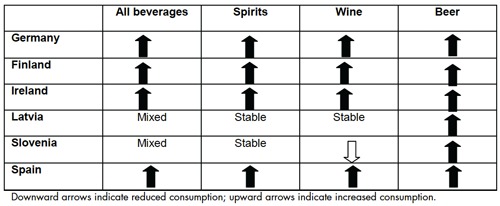

Research suggests that in Belgium, the Netherlands, Portugal, Scotland and other EU countries the share of on-trade alcohol consumption is decreasing relative to the off-trade. We obtained data from six EU countries (Finland, Germany, Ireland, Latvia, Slovenia and Spain) to examine this trend in more detail. In all six countries the ratio of off- to on-trade consumption went up for at least one type of alcoholic beverage during the observed period. The ratio of off- to on-trade consumption indicates the litres of alcohol that are consumed in the off-trade for every one litre of alcohol consumed in the on-trade. In four countries out of six, ratios went up for all beverages, as Table 1 indicates.

Table 1.

Ratio of Off- to On-Trade Consumption of Alcohol, by Beverage, in Six EU Countries, 1997–2010

This is the case even in Ireland and Spain, which had traditionally higher consumption of on-premise alcohol. In those countries in our sample with traditionally higher off-trade alcohol consumption (Finland and Germany) the proportion of alcohol sold through the off-trade has also been increasing relative to on-trade alcohol sales. Latvia and Slovenia, where off-trade consumption has been higher than on-trade consumption since at least the mid-1990s, exhibit stability in the ratio of on- and off-trade sales for selected beverages, an exception in our sample of six countries. The only instance of a decrease in the ratio of off- to on-trade consumption is for wine consumption in Slovenia.

Both Policy and Social and Economic Changes May Influence the Movement of Alcohol Consumption Between the On- and the Off-Trade Sectors

Lower off-trade alcohol prices, driven in part by growing competition in the supermarket sector (and at least in some countries possibly driven by cross-border consumption), may be causing at least part of the shift. Preventive alcohol policies as well as social, cultural, economic and demographic determinants also can play a large role in shift between on- and off-premise consumption of alcohol. In this study we conduct an exploratory analysis of the effect of a number of social, cultural, economic and demographic factors on alcohol consumption by premise. This is the first study we are aware of that attempts to analyse statistically the potential relationship between a variety of determinants. Results suggest that population density, broadband concentration and GDP per capita are statistically significant factors. The relationship is positive for population density and broadband penetration in which increases in those factors are associated with relatively more consumption in the off-trade; whereas the relationship with GDP per capita is negative, so increases in wealth are associated with shifts towards on-trade consumption. The economic downturn experienced in Europe in the last few years may have influenced the trends observed towards increased off-trade consumption.

Alcohol Price Promotions and Discounts Are Prevalent in Many EU Member States

There is some informative research on the impact of off- and on-trade price promotions and discounts, although the evidence base is not well developed. Existing data about the extent of alcohol price promotions and discounts across the EU are limited. A few studies suggest that in France, Ireland, Latvia, the Netherlands, Poland and the UK, price promotions and discounts are common in the off- and on-trade, but this has increasing significance for value in the off-trade.

Many Different Types of Non-Tax Pricing Regulations Are Used Across the EU, but We Know Little About Their Effectiveness in Reducing Alcohol Harms

The regulatory landscape in Europe is diverse, with most countries implementing at least one type of non-tax alcohol pricing regulation. Examples include off-trade retail monopolies (such as in Finland and Sweden), restrictions in off- and/or on-trade discounts and promotions (such as in parts of Germany and Spain), and bans on below-cost sales (such as the one recently abolished in Ireland). In theory, these policies should limit the availability of cheap alcohol; in fact, research shows that retail monopolies have been effective in curbing alcohol harms. However, in practice we know little about whether, and to what extent, the other policies actually achieve their aims. More research is needed in this area (focusing in part on implementation, enforcement and compliance) to assess which ones of these policies are promising and which ones should be improved.

Final Remarks

In spite of extensive evidence that raising alcohol prices reduces alcohol consumption and harms, the real price of alcoholic beverages is decreasing across the EU. This trend has fuelled debate among policymakers, public health practitioners and other stakeholders across the EU about the opportunities, and challenges, of alcohol pricing policies. This study aims to contribute a robust evidence base to inform pricing policy in the region.

As alcohol-related harms continue to present a public health challenge across the EU, this study makes an important contribution to the evidence base on alcohol pricing policy. In addition to the findings from its own analysis, this report also makes a strong case for improved data collection in a number of key areas (such as alcohol prices by beverage and premise type, on- versus off-trade consumption, and the use of price promotions and discounts) that would enhance research and policymaking in the region.

Our Approach

We reviewed influences on alcohol prices and locations of alcohol purchases using a mixed-methods approach. Each research question required a particular approach.

Excise duty pass-through

In order to analyse pass-through, we obtained data on prices and excise duties from Finland, Ireland, Latvia and Slovenia. These were analysed by means of regression analysis to identify the relationship between excise duties and prices.

On- and Off-Premise Sales Trends

We obtained data from six EU countries (Finland, Germany, Ireland, Latvia, Slovenia and Spain) to examine the trend in off- and on-premise sales in more detail. We constructed a ratio of off- to on-premise sales volumes from 1997 to 2010. In order to explore potential factors influencing the off- and on-premise sales trends, we performed regression analysis of selected social and economic determinants of alcohol consumption that have been identified in the literature.

Promotions and Discounts Sales Trends

Existing data and research about the extent of alcohol price promotions and discounts across the EU are limited. Nevertheless, we obtained data on the volume of alcohol sales through discounters (supermarkets selling mostly own-brand products or major brands at discounted prices) as an indication of trends in the retail of discounted alcohol in a small sample of EU countries. We also collected further data and information on alcohol retail practices and pricing regulations across the EU by means of an online survey of experts and policymakers, and interviews with key informants representing 23 national authorities and economic operators across ten Member States.

Alcohol Pricing Regulations

In collaboration with the European Commission Directorate General for Health and Consumers, we identified five regulations seen as of particular interest for more in-depth analysis. Research towards these case studies of non-tax pricing regulations included a review of relevant documents and materials, and key informant interviews.

Limitations

As with any research endeavour, there are limitations to the findings. The main constraints in this research are related to data. Analysis of pass-through required mean prices by beverage for at least one month and monthly price indices. Despite searches and requests for this data from Member States with potentially enough changes in excise duty to identify the pass-through relationship, we obtained data for only four countries. For the overall assessment across countries, improved accuracy and a fuller picture for the range of pass-through could be achieved with data from more countries.

In order to construct the ratio of on- to off-premise sales, data need to be purchased as publicly available information is not available. Resources for this study only allowed for purchase of data on six countries and, again, a more comprehensive picture of the situation across Member States could be made with more data.

Responses to our online survey of EU alcohol experts and government representatives were limited. In order to improve our understanding of the nature and extent of alcohol price promotions and discounts, more systematic (and comparable) efforts to collect information are needed across the Member States. Finally, while there are numerous examples of non-tax price regulations across the EU, research on their effectiveness is scarce. Further research on this is desirable for countries to be able to learn from each other's good practice and use robust evidence as they develop approaches to tackling alcohol harm.