Abstract

Context:

Although Intensive Care Units (ICUs) only account for 10% of the hospital beds, they consume nearly 22% of the hospital resources. Few definitive costing studies have been conducted in Indian settings that would help determine appropriate resource allocation.

Aim:

The aim of this study was to evaluate and compare the cost of intensive care delivery between multispecialty and neurosurgery ICUs at an apex trauma care facility in India.

Materials and Methods:

The study was conducted in a polytrauma and neurosurgery ICU at a 203-bedded Level IV trauma care facility in New Delhi, India, from May 1, 2012 to June 30, 2012. The study was cross-sectional, retrospective, and record-based. Traditional costing was used to arrive at the cost for both direct and indirect cost estimates. The cost centers included in the study were building cost, equipment cost, human resources, materials and supplies, clinical and nonclinical support services, engineering maintenance cost, and biomedical waste management.

Statistical Analysis:

Statistical analysis was performed by Fisher's two tailed t-test.

Results:

Total cost/bed/day for the multispecialty ICU was Rs. 14,976.9/- and for the neurosurgery ICU, it was Rs. 14,306.7/-, workforce constituting nearly half of the expenditure in both ICUs. The cost center wise and overall difference in the cost among the ICUs were statistically significant.

Conclusions:

Quantification of expenditure in running an ICU in a trauma center would assist health-care decision makers in better allocation of resources. Although multispecialty ICUs are more cost-effective, other factors will also play a role in defining the kind of ICU that needs to be designed.

Keywords: Intensive Care Unit, traditional costing method, trauma center

Introduction

Although Intensive Care Units (ICUs) only account for 10% of the hospital beds, they consume nearly 22% of the hospital resources.[1] A diversity of costing methods has resulted in poor external validity and inability to compare findings between such evaluations.[2] There is also a considerable heterogeneity between countries and even within the country in the allocation of resources and distribution of the services.[3] In the USA, guidelines from the Public Health Service Panel on Cost-effectiveness in Health and Medicine have been made applicable to critical care.[4] Not only very few costing studies in ICU settings have been conducted in India to enable the formulation of guidelines, but also intensive care services are also provided free of cost in government hospitals with no budgetary allocation or control. Trauma services are especially vulnerable to cost pressures because their payer mix is often marginal, and the care provided is extremely resource-intensive.[5] Few studies have been conducted in developing countries to assess the cost of ICU. The authors are not aware of any who compare a polytrauma and single specialty ICU within the same setting. The study was undertaken to determine, from a costing perspective, whether a multispecialty ICU is more cost-effective than a unispecialty ICU, all other factors being same.

Thus, an exercise was undertaken to estimate the per bed/day cost delivery of these two disparate ICUs at an apex trauma care facility in India.

Materials and Methods

The study was conducted at a 203-bedded Level IV trauma care facility in New Delhi, India, from May 1, 2012 to June 30, 2012. The study setting was a polytrauma ICU comprising 12 beds and a neurosurgery ICU of twenty beds. The study was cross-sectional, retrospective, and record-based. Data were collected from executive finance committee, accounts section, engineering section, stores department, and computer facility. The traditional (syn-average or gross) costing was used to arrive at the cost for cost estimates. The following cost centers were included in the study.

Capital assets cost

Building cost (ICU, central sterile supply department [CSSD], laundry, and manifold)

Equipment (ICU, laundry, CSSD, and manifold).

Operating cost

Human resources (faculty, residents, nursing staff, technicians, physiotherapists, hospital attendants, sanitary attendants, and security staff)

Materials and supplies

-

Support services

- Clinical: (Laboratory, radiology, physiotherapy, blood bank, manifold, and pneumatic chute system)

- Nonclinical: (Laundry, manifold, CSSD, dietetics, housekeeping, and security)

Engineering maintenance cost

Biomedical waste management (BMW).

Equipment cost, which were not traceable (donated), land cost (donated by the New Delhi Government), administrative cost, computer facility, and medical record department, were not included in the study.

Capital assets annual cost

To arrive at the annual cost of the capital assets, replacement cost was calculated by multiplying procurement cost with cost inflation multiplication factor (cost inflation index for the year 2011–2012/cost inflation index of procurement year). Thereafter, annualized method of depreciation (Recommended by the World Health Organization) was applied to arrive at the annual cost by dividing replacement cost of the asset in the year 2011 by annualization factor. The formula for calculating annualization factor is = (1/r) × (1 − 1/[1 + r]n) where,

-

r is real interest rate,

Formula = ([1 + nominal interest rate]/[1 + annual inflation] −1)

Nominal interest rate is the prevailing National Bank savings rate for the year 2011

n = number of years of life (100 years for building, 10 years for machinery, and 15 years for equipment [fixed]).

On the basis of the above-mentioned methodology, per square meter building annual cost of the trauma center and equipment annual cost were calculated. Thereafter, building cost of ICU and support services was calculated. Building cost was taken from the records of the Expenditure Finance Committee.

Similarly, annual cost of equipment was calculated for the ICUs. Supply order of equipment was taken from the indent books of user department, and cost was retrieved from the stores’ department. Apportioning was not required since all the equipment were dedicated for the ICUs. Annual building cost and equipment cost of support services were apportioned to the ICUs on the basis of workload.

Operating cost

Unstructured interview was held with the ICU staff, and the records of ICU were studied to gain an insight into the functioning of the ICUs and support services. To calculate various floor areas of ICU and support services, records of engineering department were studied. Engineering maintenance cost was calculated by calculating the per square meter engineering maintenance cost for a period of 1 year, the same was apportioned to the ICUs on the basis of workload. Building maintenance cost was taken from the accounts department.

Interviews were also carried out to calculate the time devoted by various categories of hospital staff in ICUs to apportion their salaries. Salary of employees was taken from the accounts section, and mid-point salaries based on the number of hours spent by the health-care worker in the ICU were apportioned. Direct costing was taken for health-care workers who were exclusively dedicated for the ICU.

The tests sent from ICUs to the laboratory for 2 months were averaged out from the records and the cost of the consumables apportioned to per day basis. Similarly, the cost consumables for testing of blood for transfusion were calculated from the cross-tabulation of ICU and blood bank records. Since the center was integrated through a picture archival and retrieval system, the cost of total radiological procedures of the entire study duration was taken and the per day cost was calculated. Cost of consumables was taken for 1 year to account for the fluctuation in consumption to seasonal variation. Actual quantity as per indent book was considered, and cost of the same was taken from rate contracts of the trauma facility.

Average monthly CSSD and ICU load for CSSD were calculated by taking an average of 2 months. The average number of drums, sets, and linen processed in one cycle was calculated from the CSSD records and then, the total number of cycles ran in the CSSD for steam sterilization and ETO for ICU was assessed. Manifold cost was apportioned based on the number of points at each of the ICU. The cost of manifold includes the capital cost, cost of equipment, cost of operations, cost of liquid oxygen, and the cost of the cylinders.

Average monthly laundry and ICU (kilograms) for laundry were calculated by taking an average of 3 months. The per bed cost of dietetics was extracted from a costing study conducted in the same year on dietetics. The BMW cost to the trauma care facility was calculated on per bed basis from the total cost paid by the institution. Per square meter cost of BMW was calculated, and then ICU BMW cost was arrived.

Operating cost for the various support services was taken as quoted in the contract agreement executed between the institution and outsourced agency.

Results

The trauma center is part of a large tertiary care facility and it is spread over an area of 20,600 m2 with 204 beds. The 32 ICU beds are spread over two floors. The second-floor polytrauma ward has 12 beds and the third-floor ward has 20 beds dedicated to neurosurgery cases.

All the cost estimates were calculated for the financial year 2011–2012. Annualization factor for capital assets was calculated to be Rs. 38.5/- and Rs. 8.82/- (12.53) for building, machinery, and equipment (fixed), respectively. Annualized building cost of trauma center was calculated to be INR 1761/- per square meter, and engineering maintenance cost was calculated to be INR 3,784.94/- square meter.

Intensive Care Unit estate and maintenance cost

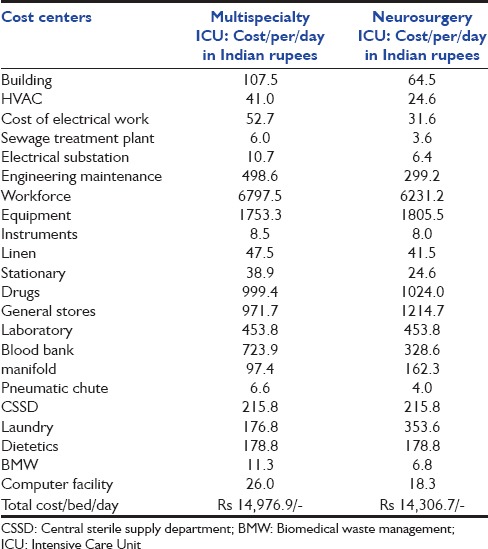

The cost of estates including the building cost (civil, landscaping, sanitary, and tube well), electrical work, heating, ventilation and air conditioning, sewage treatment plant, and the substation apportioned per bed/day was Rs. 218/- for the multispecialty ICU and Rs. 130.7/- for the neurosurgery ICU. The total maintenance cost for the year 2011–2012 was Rs. 102,412,489/-. The per bed/day cost for the multispecialty ICU was Rs. 498.61/- and for the neurosurgery ICU, it was Rs. 299.17/- [Table 1].

Table 1.

Cost comparison of multispecialty and neurosurgery Intensive Care Units of a trauma facility

Workforce cost

The annual workforce costs for the multispecialty and neurosurgery ICUs were Rs. 29,770,860/- and Rs. 44,987,820/-, respectively. The daily cost per bed for multispecialty ICU was Rs. 6797/- and for neurosurgery ICU, it was Rs. 6231/- [Table 1].

Consumables

The daily cost per bed for consumables including equipment, instruments, general store items, linen stationary, and drugs was Rs. 3819.3/- and Rs. 4118.2/- for multispecialty and neurosurgery ICUs, respectively. The equipment alone accounted for 46% and 43% of consumables cost in multispecialty and neurosurgery ICUs, respectively.

Support services cost

The daily cost of clinical support services was Rs. 1281.7/- and Rs. 948.7/- per bed for the multispecialty and neurosurgery ICUs, respectively, the difference was primarily because the blood bank cost was Rs. 723.88/- per bed for the multispecialty ICU and only Rs. 328.56/- for the neurosurgery ICU. Total annualized cost of manifold building and equipment for the years 2011-2012 was calculated to be INR 100,544/- and INR 4,528,671.65/-, respectively. ICU manifold terminal units formed only 5.1% of the total manifold terminal units installed at the trauma facility, and the daily expenses incurred on manifold were Rs. 97.39/- for multispecialty and Rs. 162.31/- for the neurosurgery ICUs.

The total cost due to nonclinical support services was calculated to be Rs. 608.7/- for the multispecialty ICU and Rs. 773/- per bed/day for the neurosurgery ICU. The costs of CSSD and dietetics apportioned to both the ICUs were the same at Rs. 215.8/- and Rs. 178.8/- per bed/day, respectively, whereas the cost of laundry was Rs. 176.8/- for the multispecialty ICU and Rs. 353.6/-/bed/day for the neurosurgery ICU [Table 1].

Monthly cost incurred by the institute on BMW was INR 1,041,666/- and cost apportioned to the center was INR 95,942.92/-. The costs of the BMW management, which were apportioned to the ICUs per month, were Rs. 350.3/- and Rs. 210.8/-, respectively [Table 1].

The per annum cost of multispecialty ICU was Rs 5,366,605/-.

The overall cost was higher in the multispecialty ICU with cost being Rs. 14,977/- per bed/day (Rs. 54,66,605/-per annum) as against the neurosurgery ICU with Rs. 14,307/- per bed/day (Rs. 5,222,055/- per annum).

Discussion

Economic evaluations can provide health-care decision makers with valuable information on the relative efficiency of alternative health-care services. This is even more important since ICUs are resource-intensive and expensive to build and operate. In developing nations, the needs to focus on prudent resource allocation cannot be overemphasized. Majority of the private hospitals ensure fairly accurate cost evaluation measures in ICUs since the patient is directly billed against it. However, in public sector hospitals, little stress is given on cost containment, which can only be assessed after cost evaluation. An institutional study assessed that trauma and acute care surgery patients represent a significant (65%) and increasing institutional cost. Per patient ICU costs were the largest single category, suggesting that cost control efforts should focus heavily on critically ill patients.[6]

This study was conducted at an apex trauma center, primarily with an objective of understanding the various cost centers and cost proportions in an intensive care facility. Secondarily, the study setting also provided an opportunity to compare the cost in running a polytrauma as against a neurosurgery ICU. The intention was to ascertain whether from a purely hospital expenditure perspective, a multispecialty or a single specialty ICU is more effective.

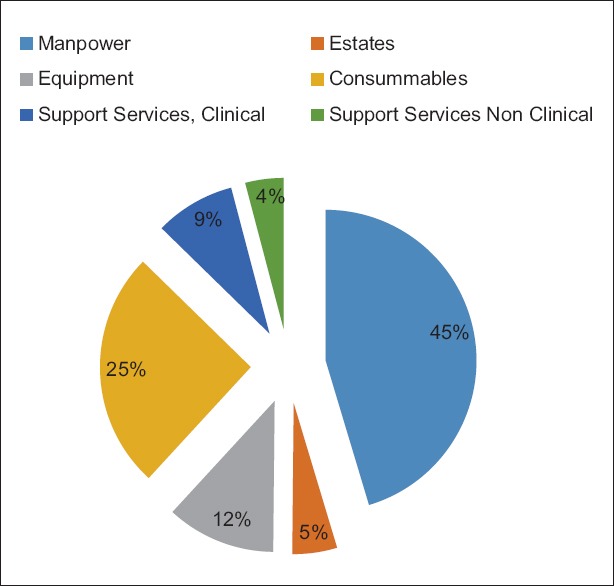

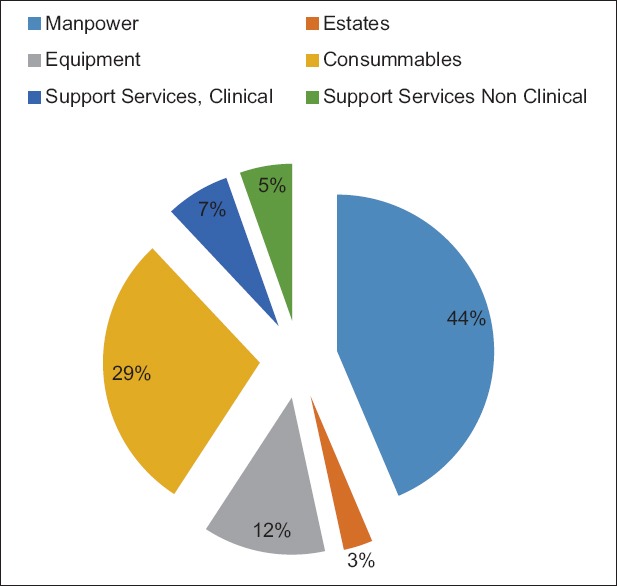

The proportion of expenditure on cost centers between the two ICUs remained the same [Figures 2 and 3], the majority of the expenditure being attributable to workforce (45% and 44%) followed by consumables (25% and 29%), followed by clinical support services, nonclinical support services, and estates, in that order. Therefore, the proportion on expenditure among the various heads remained fairly constant between the two ICUs. A direct cost analysis study of ICU stay in four European countries using a standardized costing methodology revealed a wide variation, between the countries assessed from €1168 to €2025 per day.[7] While this reflects a commonly known fact that far higher expenditure is incurred in the Western world on health care, the same study also suggested that workforce constituted the largest chunk in terms of costs, ranging from 60% to 64% of the expenditure incurred. Costing studies in ICUs in the Indian scenario have been few and far in between.

Figure 2.

Cost proportion among various cost centers in neurosurgery intensive care unit

Figure 3.

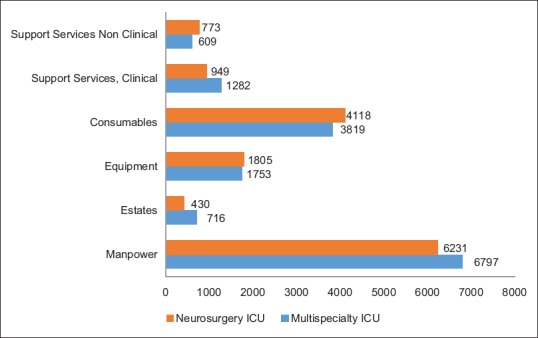

The cost center center wise differences between neurosurgery and multi-specialty intensive care units (ICUs) of trauma center are depicted in the figure. Though the consumable, nonclinical support services cost and equipment cost is higher in the neurosurgery ICU, with the overall cost is lower than multi-specialty ICU primarily because of the manpower and estates costs

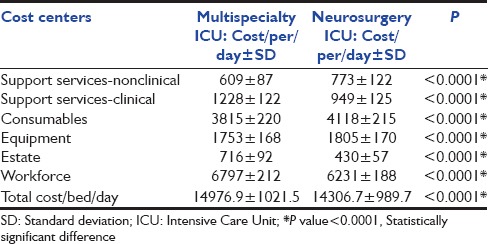

The overall cost was higher in multispecialty ICUs. It can be ascertained perhaps more tellingly from Table 2, the difference between the two ICUs is not only statistically significant with regard to the overall cost, but also when independently analyzed for workforce, equipment, estates, consumables, clinical services, and no clinical services [Table 2]. Data from both foreign and domestic ICUs indicate that 50% to 80% of direct costs are variable personnel costs, primarily for nursing. On an average, ICUs use almost three times as many nursing hours per patient day as do general floors.

Table 2.

Cost centers wise statistical significance between the Intensive Care Units

Viewed from an entirely financial perspective, neurosurgery ICUs outweigh the benefits of a multispecialty trauma ICU [Figure 1]. This may be because the workforce, forming the largest chunk of expenditure, being from the same specialty, can probably be utilized more effectively. Second, although the consumable cost is higher since it is a neurosurgery ICU, it is offset by the fact that the similar structural and engineering cost drives down the capital and maintenance costs. The fact that patients admitted in Neuro surgery ICU have similar clinical profiles with similar needs may have caused the expanses due to the clinical support services to be brought down, as against the multi-specialty ICU. However, outcomes need to be viewed from the clinical prism as well, since multispecialty ICUs would provide the opportunity to treat the patient more holistically and permit interunit transfers and cross consultation and promote pooling of resources.

Figure 1.

Cost proportion among various cost centers in multi-specialty intensive care unit

The primary drawback can be attributed to poor data availability and financial record kept inherent in a government hospital. Although activity-based costing would have been more accurate, it would have been much more tedious and time-consuming. Thus, despite its disadvantages, the research was conducted using the traditional or average costing methodology. Another disadvantage of the study was that the multispecialty ICU was 12-bedded whereas the neurosurgery ICU was 20-bedded, and it is likely that the total operational cost per bed in neurosurgery ICU may have been brought down about by this factor as well.

Conclusions

It is essential for clinicians and administrators to comprehend the enormous resources and the consequent expenses that are involved in commissioning and running an intensive care facility. This study attempts to quantify in financial terms, the expenditure involved in running an ICU in a trauma center to assist doctors and health-care decision makers in the allocation of scarce resource, especially in a country such as India. Although the study does provide evidence that operating a unispecialty ICU such as neurosurgery is more economical than a multispecialty ICU, before sweeping policy decision-making is undertaken, clinical and other factors must be taken into careful consideration. Further, comparative studies in terms of clinical outcomes may aid in choosing between the alternatives.

Financial support and sponsorship

Nil.

Conflicts of interest

There are no conflicts of interest.

References

- 1.Halpern NA, Bettes L, Greenstein R. Federal and nationwide intensive care units and healthcare costs: 1986-1992. Crit Care Med. 1994;22:2001–7. [PubMed] [Google Scholar]

- 2.Joshipura MK, Shah HS, Patel PR, Divatia PA. Trauma care systems in India - An overview. Indian J Crit Care Med. 2004;7:93–7. [Google Scholar]

- 3.Riewpaiboon A, Malaroje S, Kongsawatt S. Effect of costing methods on unit cost of hospital medical services. Trop Med Int Health. 2007;12:554–63. doi: 10.1111/j.1365-3156.2007.01815.x. [DOI] [PubMed] [Google Scholar]

- 4.Weinstein MC, Siegel JE, Gold MR, Kamlet MS, Russell LB. Recommendations of the panel on cost-effectiveness in health and medicine. JAMA. 1996;276:1253–8. [PubMed] [Google Scholar]

- 5.Taheri PA, Wahl WL, Butz DA, Iteld LH, Michaels AJ, Griffes LC, et al. Trauma service cost: The real story. Ann Surg. 1998;227:720–4. doi: 10.1097/00000658-199805000-00012. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 6.Fakhry SM, Martin B, Al Harakeh H, Norcross ED, Ferguson PL. Proportional costs in trauma and acute care surgery patients: Dominant role of intensive care unit costs. J Am Coll Surg. 2013;216:607–14. doi: 10.1016/j.jamcollsurg.2012.12.031. [DOI] [PubMed] [Google Scholar]

- 7.Tan SS, Bakker J, Hoogendoorn ME, Kapila A, Martin J, Pezzi A, et al. Direct cost analysis of intensive care unit stay in four European countries: Applying a standardized costing methodology. Value Health. 2012;15:81–6. doi: 10.1016/j.jval.2011.09.007. [DOI] [PubMed] [Google Scholar]