Abstract

Under the Affordable Care Act, the risk-adjustment program is designed to compensate health plans for enrolling people with poorer health status so that plans compete on cost and quality rather than the avoidance of high-cost individuals. This study examined health plan incentives to limit covered services for mental health and substance use disorders under the risk-adjustment system used in the health insurance Marketplaces. Through a simulation of the program on a population constructed to reflect Marketplace enrollees, we analyzed the cost consequences for plans enrolling people with mental health and substance use disorders. Our assessment points to systematic underpayment to plans for people with these diagnoses. We document how Marketplace risk adjustment does not remove incentives for plans to limit coverage for services associated with mental health and substance use disorders. Adding mental health and substance use diagnoses used in Medicare Part D risk adjustment is one potential policy step toward addressing this problem in the Marketplaces.

Under the Affordable Care Act (ACA), non-grandfathered health insurance plans in the individual and small-group market—including plans offered on the Marketplaces—may rate premiums based only on family size, geography, age, and smoking status (within rating limits). When premiums do not reflect each person’s expected costs, the market becomes vulnerable to adverse selection: the tendency of sicker, higher-cost consumers to choose more generous coverage.1 When plans are not compensated appropriately for enrolling sicker, higher-cost consumers, adverse selection in a market means that plans can profit by distorting benefits to avoid higher-cost individuals, which undermines the value of competition.2 It may also mean that plans enrolling these higher-cost individuals are driven to exit the market, which also undermines the value of competition.3

To mitigate adverse selection, the ACA established a permanent risk-adjustment program, which transfers funds from plans with enrollees who have lower-than-expected health risks to plans with enrollees who have higher-than-expected health risks. This necessary program of the ACA helps ensure that plan premiums reflect differences in scope of benefits and network coverage rather than differences in the health status of enrollees; it also helps mitigate incentives for plans to avoid higher-cost individuals.

Other ACA regulations, such as the requirement for plans to offer “essential health benefits,” which include services for mental health and substance use disorders, also serve to mitigate adverse selection. However, in spite of risk adjustment and other ACA policies, incentives remain for plans to use subtle and difficult-to-regulate “service-level selection” mechanisms to distort their benefit offerings to attract better risks.4–6 Such selection occurs when insurers design their health care services and provider networks to attract more profitable enrollees. For example, plans can work around regulations to create provider networks and drug formularies favoring or disfavoring certain conditions, or they can impose more or less strict care management across different categories of care. Preventing service-level selection on dimensions like covered services can be monitored through a plan’s requirement to provide essential health benefits, but regulating other dimensions of benefits is much more difficult.

Concerns about service-level selection are particularly warranted given two Marketplace features. The first is that narrow-network plans, often labeled “exclusive provider organizations” but also present in other plan designs, have been particularly popular in the Marketplaces and account for a growing portion of plan offerings, with the percentage of exclusive provider organization and health maintenance organization plans increasing 30 percent between 2014 and 2016.7 In narrow networks of providers, it is relatively easy to adjust the availability of certain specialties and services. The second feature is the high variation in prescription drug cost sharing and coverage.8 People with mental health and substance use disorders are particularly vulnerable to these features because they have higher average health care costs, including for prescription drugs, and they tend to use services specific to their subpopulation (such as specialty mental health providers).9,10 In fact, concerns have already been raised about Marketplace plans’ compliance with mental health parity laws and the limited networks of mental health care providers within Marketplaces.11–13

Several researchers have documented how risk-adjustment systems like those used in the Marketplaces affect selection incentives.3,14,15 Indeed, recent research has found that under a risk-adjustment system very similar to the one now used by Marketplaces, significant incentives remain for insurers to discriminate against people with mental health and substance use disorders.16 Another study found evidence that the copayments insurers impose are higher for drugs used by groups of enrollees such as those with mental health and substance use disorders, which are less profitable under the Medicare Part D risk-adjustment system.17 On the other hand, researchers have simulated the extent to which risk adjustment is likely to ameliorate plan-level selection incentives in Marketplace plans and found limited evidence for service-level selection incentives.18,19 However, such studies compared average payments and average costs; they did not study subgroups, examine incentives for plans to construct networks or benefit packages designed to avoid subgroups, or use the risk-adjustment program used by Marketplaces. No studies have looked inside the “black box” of this risk-adjustment formula to see what would explain why a system that includes indications for people with mental health and substance use disorders would systematically undercompensate plans that cover them.

This study examined insurers’ incentives, and the source of those incentives, to engage in service-level selection that puts consumers and providers of mental health and substance use disorders at a disadvantage under the Marketplace risk-adjustment system. To do so, we simulated the Marketplace risk-adjustment system in a population of likely Marketplace enrollees.

Study Data And Methods

Sample

We used data from the 2012–13 Truven Health Analytics MarketScan Commercial Claims and Encounters Database, an updated version of the 2010 MarketScan data used by the Department of Health and Human Services (HHS) to develop the Marketplace risk-adjustment model known as the HHS–Hierarchical Condition Categories (HHS-HCC) model. Following criteria applied by HHS, we kept the 7,072,964 individuals in the MarketScan data that met the inclusion criteria. To create our study sample, we selected a subset of 2,021,800 adults (ages 21–64) using methods from earlier work that used data from the Medical Expenditure Panel Survey to identify people with the characteristics that would make them eligible for the Marketplace (Exhibit 1).20

EXHIBIT 1.

Simulation sample characteristics and spending amounts

| Marketplace estimation sample

|

||

|---|---|---|

| Mean | SD | |

| Age, years | 42.4 | 12.46 |

|

| ||

| Female | 49% | —a |

|

| ||

| Census region | ||

| Northeast | 14% | —a |

| Central | 23 | —a |

| South | 43 | —a |

| West | 20 | —a |

|

| ||

| Spending | ||

| Total | $5,080 | $20,236 |

| Inpatient | 1,378 | 13,657 |

| Outpatient | 2,781 | 10,204 |

| Prescription drugs | 921 | 4,189 |

SOURCE Truven Health Analytics MarketScan Commercial Claims and Encounters Database, 2012–13. NOTES Estimation sample (N = 2, 006, 126) is a subset of adults ages 21–64 in 2012 who were continuously enrolled for 2012–13 with prescription drug and mental health coverage, selected to approximate the likely Marketplace-eligible population as described in Layton et al. Assessing incentives for adverse selection in health plan payment systems (see Note 20 in text). Also shown are the sample standard deviations (SD).

Not applicable.

Risk Adjustment

We calculated risk scores for each individual in the sample using publicly available software for the Marketplace (HHS-HCC) model,21 which is designed by HHS to predict an enrollee’s medical spending in the current year by mapping individual diagnoses (from five-digit International Classification of Diseases, Ninth Revision [ICD-9] diagnosis codes) into one of 100 Hierarchical Condition Categories selected by HHS from the full 264 categories in the diagnostic classification system.22 The HCC indicators become part of a linear regression model predicting cost. The Marketplace model then uses the average risk score for an insurer by state to calculate payment transfers across health plans each year.

The Marketplace model includes nine categories related to mental health and substance use disorders: drug psychosis (81); drug dependence (82); schizophrenia (87); major depressive and bipolar disorders (88); reactive and unspecified psychosis, delusional disorders (89); personality disorders (90); anorexia/bulimia nervosa (94); autistic disorder (102); and pervasive developmental disorders, except autistic disorder (103). Any person who receives at least one diagnosis on a claim from a qualified clinician that maps to one of the Hierarchical Condition Categories will trigger a condition-specific payment to the insurer. A person can have more than one categorical indication.

Individuals with Mental Health and Substance use Disorders

We defined individuals with mental health and substance use disorders as those with any ICD-9 code that maps to any mental health and substance use disorder– related Agency for Healthcare Research and Quality (AHRQ) Clinical Classification Software (CCS) groups.23 Such diagnoses in the ICD-9 map to fifteen different CCS categories.

Payments, in Total and for Mental Health and Substance use Disorders

We defined total payments for an individual as the sum of insurers’ payments and patients’ out-of-pocket payments for inpatient care, outpatient care, and prescription drugs in the MarketScan data. Inpatient mental health spending is defined as the payment associated with any service or encounter with either of the following Major Diagnostic Categories formed by grouping related ICD-9 categories: mental diseases and disorders or alcohol/drug use, and alcohol/drug induced organic mental disorders. We defined outpatient spending as the payment associated with any service or encounter for which the primary diagnosis in a claim is for one of the mental health and substance use disorder ICD-9 codes or for which the claim originated from a mental health and substance use disorder provider. We defined drug spending as the payment associated with any drug included in ten therapeutic classes commonly used for these conditions.

Analysis

To examine the payment consequences for individuals with mental health and substance use disorder diagnoses under the Marketplace model, we first divided all individuals with a relevant diagnosis in the sample into those with at least one diagnosis that falls into one of the nine related categories (“recognized” individuals) and those with no such diagnosis (“unrecognized” individuals). The second group includes people with mental health and substance use disorders who were intentionally excluded from the Marketplace risk-adjustment classification system at the time it was developed, possibly for reasons related to predictive power and potential manipulation; we return to this point below.

Once we distinguished recognized and unrecognized individuals, we analyzed which diagnoses were most prevalent among the un-recognized group by flagging the prevalence and the associated cost of such individuals. We categorized unrecognized individuals with these conditions using the Clinical Classification System, which was developed as a simple way to group diagnoses, rather than Hierarchical Condition Categories, which were developed for use in a payment system. All individuals with mental health and substance use disorders in our sample fall within a CCS category, but not all such individuals fall within a Hierarchical Condition Category.

Next, to evaluate plan selection incentives (how well the risk-adjustment system compensates plans for various subgroups), we calculated predictive ratios for each subgroup. A predictive ratio is constructed by taking the ratio of average plan liabilities (total plan payment to providers minus [compensated] predicted payments based on the Marketplace model) to average total plan payments for each subgroup of individuals with mental health and substance use disorders in the sample.16 Predictive ratios less than 1 indicate that plans are undercompensated for treatment. Finally, using publicly available definitions provided by HHS, we simulated and compared recognized/unrecognized assignment for individuals with mental health and substance use disorders under the three different risk-adjustment programs run by HHS (Marketplace, Medicare Advantage, and Medicare Part D).24

Limitations

Our work has a number of limitations. The sample employed in this study does not reflect actual Marketplace enrollment; instead, it uses a sample identified from MarketScan data, a data source coming mainly from large employer plans. Concern related to the data source is of limited importance for two reasons. First, our sample was constructed to be representative of the Marketplace population. Second, HHS also uses MarketScan data to calibrate its Marketplace risk-adjustment model.25

Additionally, this study did not examine the trade-offs associated with our policy recommendation for an expansion of the Marketplace model to include diagnoses used in the Medicare Part D risk-adjustment model. The Medicare Part D model uses diagnoses already screened and selected by HHS, which should alleviate concern here. However, such trade-offs should be examined in a future study, given the unique concerns embedded in a concurrent risk-adjustment system (HHS-HCC model), which uses diagnoses from the current year to risk-adjust, as opposed to a prospective risk-adjustment system (Medicare Part D model), where the previous year is used.

Study Results

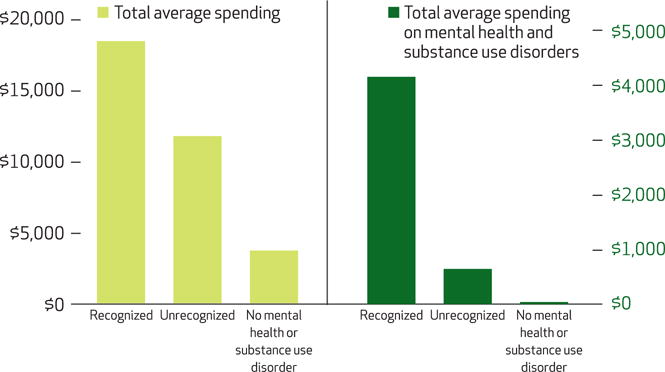

All individuals with mental health and substance use disorder diagnoses have higher spending than those without, but recognized individuals have both higher total and mental health and substance use disorder spending (Exhibit 2).

EXHIBIT 2. Total average spending and total average mental health and substance use spending per person in the sample, 2013.

SOURCE Authors’ analysis of sample data. NOTES Recognized and unrecognized categories (described in the text) are mutually exclusive. People without mental health and substance use disorder diagnoses have mental health spending because some mental health and substance use treatments, particularly prescription drugs, have applications other than treating mental health and substance use disorders.

Individuals with mental health and substance use diagnoses were 14.5 percent of our total sample and had spending that was 2.6 times the sample average in 2013. Among all individuals with those diagnoses, only 20 percent were recognized by the Marketplace risk-adjustment model. Only 30 percent and 58 percent of the total and mental health substance use disorder-specific spending, respectively, was accounted for by the recognized group (see online Appendix Table 1 for more detail).26

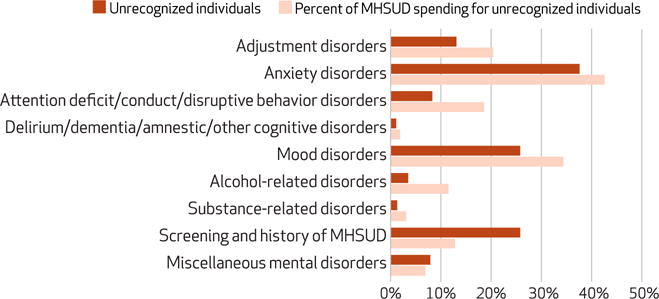

Spending for and representation among the unrecognized group is classified by CCS diagnostic categories and presented in Exhibit 3. While the CCS rows are not mutually exclusive, it is clear that anxiety, mood, and adjustment disorders are the most common clinical categories for unrecognized individuals. The same three categories represent the greatest percentage of total and mental health and substance use disorder spending among the unrecognized group as well. Many individuals with a mood or anxiety disorder are, however, recognized in the risk-adjustment system, which implies that the Marketplace model captures some individuals within a group and misses others (see Appendix Table 2).26

EXHIBIT 3. Clinical Classification Software (CCS) categories for individuals with mental health and substance use diagnoses who are unrecognized by the Marketplace model.

SOURCE Authors’ analysis of sample data. NOTES Percentages of unrecognized individuals (described in the text) and total mental health and substance use disorder (MHSUD) spending are not additive, since individuals can have diagnoses associated with more than one CCS category. For example, a person with a diagnosis code for screening and history of mental health and substance use disorders is also likely represented in another category, such as anxiety disorders. The exhibit does not include CCS categories with less than 1 percent of individuals or less than 1 percent of total spending: developmental disorders, disorders usually diagnosed in infancy/childhood/adolescence, impulse control disorders, personality disorders, schizophrenia and other psychotic disorders, and suicide and intentional self-inflicted injury.

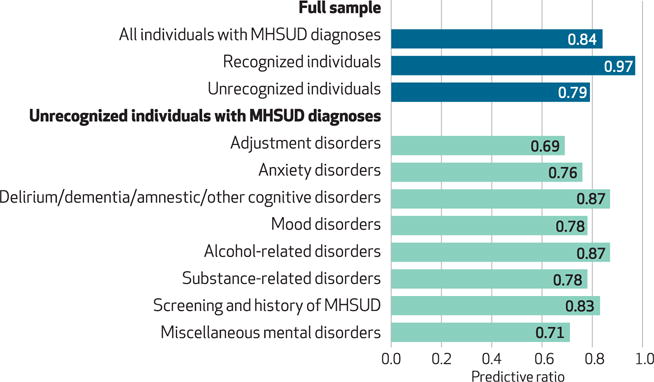

Exhibit 4 presents predictive ratios for the full set of individuals with a mental health and substance use disorder diagnosis and separately for each CCS subgroup among unrecognized individuals. In total, the Marketplace risk-adjustment model undercompensates plans for individuals with mental health and substance use diagnoses by 16 percent (represented by a predictive ratio of 0.84), with 3 percent average undercompensation for the recognized group (0.97) and 21 percent average undercompensation for the unrecognized group (0.79). Stated differently, this means that the existing classification for mental health and substance use disorders does a highly imperfect job of detecting and compensating for costs of care among individuals with mental health and substance use disorders.25 The existing Marketplace risk-adjustment system does a particularly poor job of compensating insurers for unrecognized individuals with adjustment disorders (predictive ratio of 0.69), anxiety disorders (0.76), and mood disorders (0.78) (Exhibit 4).

EXHIBIT 4. Predictive ratios for individuals with mental health and substance use diagnoses who are recognized and unrecognized by the Marketplace model.

SOURCE Authors’ analysis of sample data. NOTES Diagnoses are based on Clinical Classification Software (CCS) categories, as in Exhibit 3. Recognized and unrecognized individuals (described in the text) are mutually exclusive. Predictive ratios measure how well the risk-adjustment system compensates health insurance plans for a subgroup by taking the ratio of average plan liabilities (total plan payments minus [compensated] predicted payments based on the Health and Human Services–Hierarchical Condition Category [HHS-HCC] model to average actual total payments for each subgroup of individuals. The exhibit does not include CCS categories with less than 1 percent of individuals or less than 1 percent of total spending: developmental disorders, disorders usually diagnosed in infancy/childhood/adolescence, impulse control disorders, personality disorders, schizophrenia and other psychotic disorders, and suicide and intentional self-inflicted injury.

Finally, we compared the identification of individuals with mental health and substance use disorders using the Marketplace risk-adjustment model with identification of individuals using alternative risk-adjustment systems currently in use by HHS—that is, a comparison between the HHS-HCC (Marketplace) model, the Medicare Advantage (CMS-HCC) model, the Medicare Part D (CMS-RxHCC) model, and a hybrid model that combines the HCCs used in the CMS-HCC and CMS-RxHCC models, as constructed by the authors. We found that the Marketplace risk-adjustment model was similar to the Medicare Advantage model in that both recognized roughly 20 percent of individuals with mental health and substance use diagnoses. In contrast, the Medicare Part D model recognized 54 percent, and the combined Marketplace and Medicare Part D model recognized 56 percent (see Appendix Exhibit 5).26 In results not presented here, we found that the majority of those captured by the Medicare Part D model but not the Marketplace model had mood or anxiety disorders.

Discussion

The ACA expanded access to insurance and benefit coverage for a substantial number of people with mental health and substance use disorders. Risk adjustment in plans that provide this expanded access is a necessary tool to use in encouraging competition in the market, making sure that plans are appropriately compensated, and mitigating incentives for plans to distort coverage offerings.

In practice, however, it is difficult to create a risk-adjustment system that completely addresses distortionary incentives. These incentives, with respect to people with mental health and substance use diagnoses, are generated in two ways: when they are accounted for by the Marketplace risk-adjustment system (assigned an HCC) but the payments generated by the risk-adjustment system systematically fall short of actual spending, or when the system completely fails to account for them by not assigning them to an HCC to begin with. Our study found that both failures were present for individuals with mental health and substance use diagnoses in the Marketplaces in 2013. It adds to the evidence that incentives remain for plans to distort coverage offerings for individuals with these diagnoses.

We found that the existing Marketplace risk-adjustment model recognized and made an incremental payment for only 20 percent of individuals with a mental health and substance use disorder diagnosis in 2013. While the Marketplace model does successfully recognize and compensate for enrollment of individuals with the most expensive mental health and substance use diagnoses in a health plan, it still underpredicts spending dramatically for individuals with these diagnoses as a whole, on average.

The remaining 80 percent of individuals with mental health and substance use diagnoses were not recognized by the Marketplace risk-adjustment model. Such a finding could be innocuous with respect to plan incentives if these individuals either had spending levels close to the average level of spending in the population or had a separate non–mental health and substance use disorder related HHS-HCC diagnoses (such as diabetes or cancer) that elevated their risk score to match costs in the Marketplace risk-adjustment model. We found that neither of these scenarios was generally true. First, spending for unrecognized individuals was, on average, 2.3 times higher than total spending for all individuals in the sample. Second, the unrecognized group had an average predictive ratio of 0.79, which indicates that this group was undercompensated by 21 percent, even when we accounted for payments triggered by all of the categories in the Marketplace risk-adjustment model (that is, comorbidities compensated by the risk-adjustment system). Taken together, these findings imply that individuals with mental health and substance use diagnoses are unattractive to plans, thereby providing health plans with incentives to limit their selection into the plan.

There are several potential explanations for why the Marketplace risk-adjustment model failed to recognize so many individuals with mental health and substance use diagnoses. First, there are trade-offs that must be weighed when selecting categories for their use in a risk-adjustment system.27 To determine which HCCs to include in the HHS-HCC model, HHS used four main criteria to narrow down the full diagnostic classification to 100 categories used in the final payment system: the categories represent clinically significant, well-defined, and costly medical conditions; they are not especially vulnerable to discretionary diagnostic coding; they do not primarily represent poor quality of medical care; and they identify chronic, predictable, or other conditions that are subject to insurer risk selection, risk segmentation, or provider network selection, rather than random acute events that represent insurance risk. It may be the case that mental health and substance use disorder diagnoses are disproportionally affected by these subjective criteria; however, available reports describing the current system contain no documentation of these concerns.22,27

Second, how prescription drugs are handled under the Marketplace risk-adjustment system may contribute to undercompensation. Our analysis found that while the Medicare Advantage and Marketplace risk-adjustment models recognize essentially the same individuals with mental health and substance use disorders, the Medicare Part D model assigns substantially more individuals to a mental health and substance use disorder HCC. This result is not surprising given that the base model for Marketplace risk adjustment is the Medicare Advantage model, which was designed to predict medical spending, not drug spending. The Marketplace risk-adjustment model is used to predict total costs, including drug spending. Thus, the Marketplace model’s reliance on a model not optimized for predicting drug spending results in its failure to adequately account for conditions such as mood and anxiety disorders that do not typically result in high medical spending but that do result in high prescription drug spending. This result suggests that the Marketplace model may benefit from the incorporation of certain aspects of the Medicare Part D model with respect to the prediction of spending for individuals with mental health and substance use disorder diagnoses. In its most recent final rule governing risk adjustment, HHS indicated openness to such incorporation, confirming plans to explore including prescription drugs into the model.25 The results we present here suggest that including prescription drug claims may not be necessary, as the adoption of the Medicare Part D model, which uses diagnosis codes and does not use prescription drug claims, alone would result in a dramatic increase in the portion of recognized individuals with mental health and substance use disorders.

Conclusion

The ability of risk adjustment to mitigate adverse selection is particularly important for people with mental health and substance use disorders. This study documented how the Marketplace risk-adjustment system generates incentives for plans to engage in service-level selection for services associated with these diagnoses. Our findings add to concerns about health plans’ incentives not to comply with their legal obligation under the Paul Wellstone and Pete Domenici Mental Health Parity and Addiction Equity Act of 2008 to provide mental health benefits on par with medical and surgical benefits. Modification of the risk-adjustment formula should be considered as a way of addressing systematic underpayment for people with mental health and substance use diagnoses. This study suggests one potential step that could be taken to ameliorate this problem: the incorporation of diagnosis codes used in the Medicare Part D (CMSRx-HCC) risk-adjustment model. Future research should be conducted to examine how the incorporation of prescription drugs in risk adjustment can reduce incentives for service-level selection by health plans.

Supplementary Material

Acknowledgments

Ellen Montz was supported by the Agency for Healthcare Research and Quality (Grant No. T32HS000055). Tim Layton acknowledges support from the National Institute of Mental Health (NIMH) (Institutional Training Grant No. T32-019733). Randall Ellis, Sherri Rose, and Thomas McGuire were supported by the NIMH (Grant No. 2R01-MH094290). The content is solely the responsibility of the authors and does not necessarily represent the official views of the Agency for Healthcare Research and Quality.

Contributor Information

Ellen Montz, Email: emontz@fas.harvard.edu, PhD candidate in the Department of Health Care Policy at Harvard University, in Cambridge, Massachusetts.

Tim Layton, Assistant professor of health care policy in the Department of Health Care Policy at Harvard Medical School, in Boston, Massachusetts.

Alisa B. Busch, Assistant professor of psychiatry at McLean Hospital and Harvard Medical School, and an assistant professor of health care policy in the Department of Health Care Policy at Harvard Medical School

Randall P. Ellis, Professor in the Department of Economics at Boston University, in Massachusetts

Sherri Rose, Associate professor of health care policy (biostatistics) in the Department of Health Care Policy at Harvard Medical School.

Thomas G. McGuire, Professor of health economics in the Department of Health Care Policy at Harvard Medical School, and a research associate at the National Bureau of Economic Research, in Cambridge

NOTES

- 1.Cutler DM, Lincoln B, Zeckhauser R. Selection stories: understanding movement across health plans. J Health Econ. 2010;29(6):821–38. doi: 10.1016/j.jhealeco.2010.08.001. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 2.Pauly M. Adverse selection and moral hazard: implications for health insurance markets. In: Sloan FA, Kasper H, editors. Incentives and choice in health care. Cambridge (MA): MIT Press; 2008. pp. 103–30. [Google Scholar]

- 3.Cutler DM, Reber S. Paying for health insurance: the trade-off between competition and adverse selection. Q J Econ. 1998;113(2):433–66. [Google Scholar]

- 4.Ellis RP, McGuire TG. Predictability and predictiveness in health care spending. J Health Econ. 2007;26(1):25–48. doi: 10.1016/j.jhealeco.2006.06.004. [DOI] [PubMed] [Google Scholar]

- 5.Ellis RP, Jiang S, Kuo TC. Does service-level spending show evidence of selection across health plan types? Appl Econ. 2013;45(13):1701–12. [Google Scholar]

- 6.Newhouse JP, McWilliams JM, Price M, Huang J, Fireman B, Hsu J. Do Medicare Advantage plans select enrollees in higher margin clinical categories? J Health Econ. 2013;32(6):1278–88. doi: 10.1016/j.jhealeco.2013.09.003. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 7.Pearson C, Carpenter E. Fewer PPOs offered in Exchanges in 2016 [Internet] Avalere Health; 2015. Nov, [cited 2016 Apr 27]. Available for download from: http://avalere.com/expertise/managed-care/insights/fewer-ppos-offered-on-exchanges-in-2016. [Google Scholar]

- 8.Buttorff C, Andersen MS, Riggs KR, Alexander GC. Comparing employer-sponsored and federal Exchange plans: wide variations in cost sharing for prescription drugs. Health Aff (Millwood) 2015;34(3):467–76. doi: 10.1377/hlthaff.2014.0615. [DOI] [PubMed] [Google Scholar]

- 9.Frank RG, McGuire TG. Economics and mental health. In: Culyer AJ, Newhouse JP, editors. Handbook of health economics. San Diego (CA): Elsevier; 2000. pp. 894–954. [Google Scholar]

- 10.McGuire TG, Sinaiko AD. Regulating a health insurance Marketplace: implications for individuals with mental illness. Psychiatr Serv. 2010;61(11):1074–80. doi: 10.1176/ps.2010.61.11.1074. [DOI] [PubMed] [Google Scholar]

- 11.Berry KN, Huskamp HA, Goldman HH, Barry CL. A tale of two states: do consumers see mental health insurance parity when shopping on state Marketplaces? Psychiatr Serv. 2015;66(6):565–7. doi: 10.1176/appi.ps.201400582. [DOI] [PubMed] [Google Scholar]

- 12.Goodell S. Health Policy Brief: enforcing mental health parity. Health Affairs [serial on the Internet] 2015 Nov 9; [cited 2016 Apr 27]. Available from: http://www.healthaffairs.org/healthpolicybriefs/brief.php?brief_id=147.

- 13.Dorner SC, Jacobs DB, Sommers BD. Adequacy of outpatient specialty care access in Marketplace plans under the Affordable Care Act. JAMA. 2015;314(16):1749–50. doi: 10.1001/jama.2015.9375. [DOI] [PubMed] [Google Scholar]

- 14.Cao Z, McGuire TG. Service level selection by HMO’s in Medicare. J Health Econ. 2003;22(6):915–31. doi: 10.1016/j.jhealeco.2003.06.005. [DOI] [PubMed] [Google Scholar]

- 15.Eggleston K, Bir A. Measuring selection incentives in managed care: evidence from the Massachusetts State Employee Health Insurance Program. J Risk Insur. 2009;76(1):159–75. [Google Scholar]

- 16.McGuire TG, Newhouse JP, Normand SL, Shi J, Zuvekas S. Assessing incentives for service-level selection in private health insurance exchanges. J Health Econ. 2014;(35):47–63. doi: 10.1016/j.jhealeco.2014.01.009. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 17.Carey C. Government payments and insurer benefit design in Medicare Part D. Ann Arbor (MI): University of Michigan; 2014. Working Paper [Google Scholar]

- 18.Weiner JP, Trish E, Abrams C, Lemke K. Adjusting for risk selection in state insurance exchanges will be critically important and feasible, but not easy. Health Aff (Millwood) 2012;31(2):306–15. doi: 10.1377/hlthaff.2011.0420. [DOI] [PubMed] [Google Scholar]

- 19.Barry CL, Weiner JP, Lemke K, Busch SH. Risk-adjustment in health insurance exchanges for individuals with mental illness. Am J Psychiatry. 2012;169(7):704–9. doi: 10.1176/appi.ajp.2012.11071044. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 20.For details about the sample construction, see; Layton TJ, Ellis RP, McGuire TG. Assessing incentives for adverse selection in health plan payment systems. Cambridge (MA): National Bureau of Economic Research; 2015. NBER Working Paper No. 21531 [Google Scholar]

- 21.Centers for Medicare and Medicaid Services. HHS-developed risk-adjustment model [Internet] Baltimore (MD): CMS; SAS software; Center for Consumer Information and Insurance Oversight. [cited 2016 Apr 27] Available for download from: http://www.cms.gov/CCIIO/Resources/Regulations-and-Guidance/Downloads/SASsoftware.zip. [Google Scholar]

- 22.Kautter J, Pope GC, Ingber M, Freeman S, Patterson L, Cohen M, et al. The HHS-HCC risk-adjustment model for individual and small group markets under the Affordable Care Act. Medicare Medicaid Res Rev. 2012;4(3):E1–11. doi: 10.5600/mmrr.004.03.a03. [DOI] [PMC free article] [PubMed] [Google Scholar]

- 23.Agency for Healthcare Research and Quality. Clinical Classification Software (CCS) 2015 [Internet] Rockville (MD): AHRQ; 2016. Mar, [cited 2016 Apr 27]. Available from: https://www.hcup-us.ahrq.gov/toolssoftware/ccs/CCSUsersGuide.pdf. [Google Scholar]

- 24.Department of Health and Human Services. Model software/ICD-9 mappings [Internet] Washington (DC): HHS; [cited 2016 Apr 27]. Available for download from: https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Risk-Adjustors-Items/Risk2006-2011.html. [Google Scholar]

- 25.Department of Health and Human Services. Patient Protection and Affordable Care Act; HHS notice of benefit and payment parameters for 2017. Final rule. Fed Regist. 2016;81(45):12203–352. [PubMed] [Google Scholar]

- 26.To access the Appendix, click on the Appendix link in the box to the right of the article online.

- 27.Department of Health and Human Services. Patient Protection and Affordable Care Act, HHS notice of benefit and payment parameters for 2014 and amendments to the HHS notice of benefit and payment parameters for 2014; final rule. Fed Regist. 2013;78(47):15410–541. [Google Scholar]

Associated Data

This section collects any data citations, data availability statements, or supplementary materials included in this article.